Quick Answer

A digital nomad financial review is a yearly evidence-based check of compliance, cash flow, and resilience so you can stay ahead of tax, banking, insurance, and contract problems. The review should track residency days, separate account monitoring from filing, test invoice and payment processes, verify reserves and insurance, and confirm retirement and contract decisions with current rules and records.

Pillar 1: Fortify Your Compliance Shield - Are You Protected From Catastrophic Risk?#

Treat compliance as an annual evidence process. If residency, reporting, or invoice rules may apply in more than one jurisdiction, flag that early and escalate before you file returns or send year-end invoices.

Track residency the way tax authorities test it#

Start with where you were physically present, then test those facts against each country's rules. There is no universal 183-day rule, and passing one country's test does not automatically prevent dual residence elsewhere.

| Residency test type | What triggers review | What records to keep | Common failure mode |

|---|---|---|---|

| Calendar-based | You are near a year-based threshold (for example, 183 days in a tax year) | Passport stamps, flight receipts, accommodation records, dated travel log | Assuming arrival/departure days do not count when a jurisdiction counts any part of a day |

| Rolling-period | Presence is split across year-end or prior years (for example, U.S. substantial presence or Ireland's 183/280 structure) | Month-by-month day counts, entry/exit dates, prior-year logs | Checking one calendar year only and missing multi-year tests |

| Ties-based | Day count is lower, but personal or work ties are strong (for example, UK sufficient ties) | Lease records, family location evidence, workday logs, contracts, local registrations, bank/utility records | Looking only at day count and ignoring ties |

Use two checkpoints in your review. First, reconcile your day log to travel and booking evidence. Second, if domestic tests conflict, treat treaty tie-breakers as a sequential test. Confirm against the exact treaty text before you decide your filing position.

Split U.S. account monitoring from U.S. filing#

If you are a U.S. person, separate year-round monitoring from filing. Monitoring means tracking the highest aggregate value across all foreign financial accounts. FBAR is triggered if the combined value exceeds $10,000 at any point in the year.

| Item | What it covers | Key threshold or timing |

|---|---|---|

| Monitoring | Tracking the highest aggregate value across all foreign financial accounts | Year-round |

| FBAR (FinCEN Form 114) | Separate filing requirement | Triggered if the combined value exceeds $10,000 at any point in the year; due April 15 with an automatic extension to October 15 |

| Form 8938 | Different requirement attached to your tax return; it does not replace FBAR | Specified unmarried individuals living abroad: $200,000/$300,000; specified married joint filers living abroad: $400,000/$600,000 |

Filing is separate. FBAR (FinCEN Form 114) is due April 15 with an automatic extension to October 15. Form 8938 attaches to your tax return, and it does not replace FBAR. For specified unmarried individuals living abroad, thresholds include $200,000/$300,000; for specified married joint filers living abroad, thresholds include $400,000/$600,000. Keep a checklist note to verify current filing thresholds and penalty ranges each year instead of copying old assumptions.

Review PE risk before your client flags it#

Permanent establishment risk is not limited to a fixed office. It can also arise when someone has authority to conclude contracts in the enterprise's name. If your role or working setup moved in that direction, escalate quickly.

For your annual evidence pack, keep your signed contract, SOW, approval trail, role description in client materials, and any office or coworking arrangement linked to the engagement. If the facts changed mid-year, record when they changed.

Use invoice QA to protect cash flow#

Invoice compliance is also a payment-control step. Missing or incorrect tax data can delay payment, and U.S. backup withholding can reduce reportable contractor payments by 24% when TIN or certification requirements fail. Before you send any material invoice, run this check:

| Check | What to confirm | Evidence |

|---|---|---|

| EU VAT numbers | Validate in VIES where relevant; VIES does not validate UK (GB) VAT numbers | VIES result |

| Reverse-charge treatment | Check whether it applies and confirm the required wording for the specific jurisdiction and current rules | Tax-status notes |

| Required invoice fields | Confirm a unique sequential invoice number, invoice date, supplier/customer identifying details, and required tax IDs | Final invoice PDF |

Store the VIES result, final invoice PDF, and tax-status notes in the same client folder so you can clear payment holds quickly. For related cross-border planning context, see A Guide to the Malaysian Digital Nomad Visa (DE Rantau).

Pillar 2: Optimize Your Cash Flow Command Center - Is Your Money Working For You, or Against You?#

Once compliance is under control, cash flow is usually the next pressure point. Treat it as a review-and-adjust process: assign every payment quickly, give each account one job, and reconcile every deduction from invoice amount to settled amount.

Review your allocation logic, not just your balance#

If you use a Profit First-style approach, run it as a checklist, not a slogan. Keep a simple account map: income clearing, tax reserve, owner pay, operating expense, and profit or buffer. Different labels are fine. What matters is that each account has one purpose and transfers happen on a consistent cadence. Use this review sequence:

- Write your allocation rule beside each account, with the current allocation range pending advisor/source verification.

- Check recent payments and confirm each split followed your rule within your transfer window.

- Flag pressure points: tax reserve repeatedly tapped, owner pay constantly short, or blurred business/personal spending.

- Rebalance after reviewing a full period of inflows and outflows, not one unusual month.

The control check is simple: payment records, transfer logs, and account exports should match, with written reasons for exceptions.

Keep a layered banking stack#

If your home base, business, and banking are spread across countries, one account may not cover every need. A layered setup can add fallback routes, but every extra layer adds upkeep. Treat consolidation as a tradeoff to test, not an automatic upgrade.

| Account type | Primary use case | Main risk | Operational tradeoff | Avoid when |

|---|---|---|---|---|

| Home-base bank | Can serve as a continuity anchor for core reserves | Cross-border access can be slower or more manual | Continuity vs day-to-day flexibility | Reliable remote access or maintenance is not practical |

| Multi-currency account | Can centralize receiving payments and holding working balances | Concentration risk if it becomes your only rail | Flexibility vs single-point dependency | It is also your only reserve store and payout path |

| Local account | Can support recurring local spend where you operate | Admin burden and local banking friction | Local convenience vs account upkeep | Local use is occasional or short-term |

On a regular cadence (for example, quarterly), run a live resilience check. Receive funds, send funds, and confirm access still works across your critical accounts.

Reconcile fee erosion from invoice to settlement#

Do not guess at fee drag. Reconcile it from gross invoice to spendable net, line by line:

- Record invoice amount and invoice currency.

- Record processor or gateway deductions.

- Record FX conversion details, with current FX and fee benchmarks pending source verification.

- Record transfer costs, including intermediary or receiving-bank deductions.

- Record holds, reserves, reversals, or chargeback impacts.

- Record final settled amount available to use.

Keep one evidence bundle per sample payment: invoice, remittance details, payout report, FX record, and receiving account entry. If gross-to-net cannot be explained line by line, the process is not yet under control.

Track three monthly dashboard lines: effective take-home rate, average settlement time, and avoidable fee categories. Then align invoice terms with payout timing so your promised payment window matches when funds are actually released. You might also find this useful: Pre-Departure Checklist: 25 Essential Legal and Financial Tasks Before Leaving the US to Become a Digital Nomad. Before you lock your payment stack, run a quick side-by-side cost check so your cash-flow plan is based on real fee tradeoffs: Compare payment fees.

Pillar 3: Build Your Resilience Fortress - How Bulletproof is Your Business-of-One?#

After you map cash flow, pressure-test resilience. If income pauses, you get sick, or a dispute delays payment, can you keep operating without breaking your plan? In your annual review, verify four things with evidence: continuity capital, insurance fit, retirement/investing risk, and contract protections.

Continuity capital#

Start by separating business-critical costs from personal baseline costs. If those categories are muddy, your reserve target will be too. A commonly cited planning benchmark is 3-6 months of essential expenses, but treat that as guidance, not a universal rule.

| Reserve bucket | What to include | What to verify now | Target note |

|---|---|---|---|

| Business-critical expenses | Core software, key contractors, payroll (if any), recurring compliance costs, minimum tax set-asides, essential subscriptions | Last 3 months of expenses, where funds are held, transfer/access speed, whether funds are mixed with operating cash | Current reserve target range pending advisor/source verification |

| Personal baseline expenses | Housing, food, insurance, transport, debt minimums, dependent support, essential phone/internet | Last 3 months of spending, true baseline vs aspirational budget, access if you change countries | Current reserve target range pending advisor/source verification |

| Combined continuity reserve | Total needed if income drops and life continues | Single-point-of-failure risk, cash access, whether reserves are exposed to market swings | Current reserve target range pending advisor/source verification |

Keep this reserve simple and accessible. If part of it is in U.S. banks, review FDIC structure: $250,000 per depositor, per FDIC-insured bank, per ownership category.

Insurance audit#

Insurance fit drifts as your travel pattern, work setup, and equipment change. Run a coverage check against how and where you actually work now. For U.S. travelers, medical costs abroad are your responsibility, and Medicare/Medicaid generally do not pay for care outside the U.S.

Confirm what each policy covers instead of assuming one policy handles everything. The CDC distinguishes travel disruption, travel health, and medical evacuation insurance as different coverages.

Checklist for this review:

- Compare your current countries, trip duration, and work activities to policy territory, exclusions, and claims process.

- Verify coverage still fits long stays, remote work setup, and equipment risk.

- Store declarations page, policy wording, country coverage list, and claims instructions in one folder.

- Escalate to a licensed broker/adviser if countries, work type, or equipment profile changed.

Retirement and investing#

For cross-border taxpayers, account and fund domicile can materially affect tax treatment. For U.S. taxpayers, a foreign corporation can be a PFIC under IRC Section 1297 if it meets the 75% passive income test or the 50% passive assets test. Certain direct or indirect shareholders may also need to file Form 8621. If a non-U.S. institution recommends pooled funds, pause and verify PFIC treatment before you invest.

| Account option | Who it generally fits | What to verify | Current published figure |

|---|---|---|---|

| One-participant 401(k) | Business owner with no employees, or owner plus spouse | Eligibility, employee vs employer contribution mechanics, provider support for your tax profile | 2026 employee elective deferral limit: $24,500 |

| Traditional or Roth IRA | Earners using a personal retirement account | Income eligibility, deduction/Roth phaseout issues, custodian access while abroad | 2026 IRA contribution limit: $7,500 |

| SIMPLE IRA | Small businesses using a SIMPLE structure | Employer obligations, employee notice rules, catch-up eligibility, fit with current setup | 2026 catch-up: $4,000 standard, $5,250 for eligible ages 60-63; full contribution limits pending provider/source verification |

If you see PFIC exposure, Form 8621 history, or unclear contribution eligibility, escalate to a qualified tax adviser.

Contract clause audit#

Weak contract language usually shows up later as payment friction, scope fights, or messy exits. Treat contract review as cash flow protection and downside control. Audit your MSA, SOW template, and last three signed deals in this order:

| Clause area | What to review |

|---|---|

| Scope control | Deliverables, revision limits, acceptance triggers, and client dependencies are specific enough to invoice cleanly |

| Payment protection | Invoice timing, due dates, deposits/milestones, and late-payment terms are explicit in writing |

| Termination terms | Notice, offboarding, and payment treatment at termination are clear |

| Dispute handling | If you use arbitration, compare your clause to AAA or ICC standard drafting language; do not assume enforceability in every jurisdiction |

| Governing law/jurisdiction | Confirm the contract clearly states which law applies in a dispute |

If you use a kill fee or fixed cancellation remedy, have counsel confirm it is drafted as a valid liquidated-damages approach under your chosen law. Keep an evidence pack with signed agreements, current templates, redlines, and a short note on which clauses need legal review before your next deal. Related: Should Your Freelance Business Accept Credit Cards?.

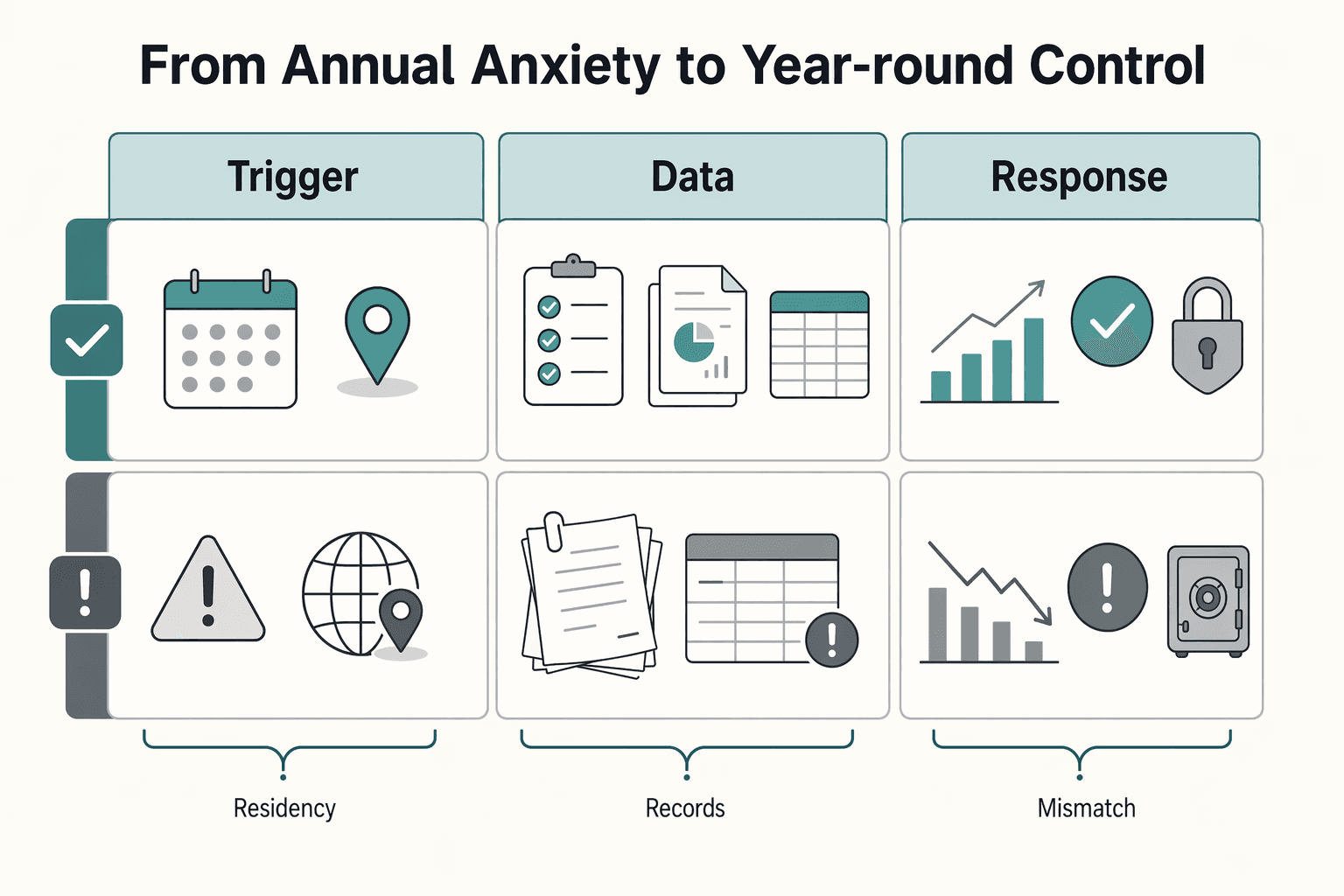

From Annual Anxiety to Year-Round Control#

Your review works best as a year-round practice, not a once-a-year scramble. When you stay on top of it, the payoff is practical: fewer surprises, faster decisions, cleaner records, and clearer next actions. An early approach means acting before issues compound. A reactive one starts after a problem forces a response.

| Process area | Reactive | Early |

|---|---|---|

| Trigger | A deadline, notice, charge error, or cash squeeze forces action | Routine checkpoints surface issues early |

| Data | Statements, contracts, travel records, and receipts are scattered | One recordkeeping setup and evidence folder summarize transactions |

| Response | Last-minute fixes and rushed decisions | Planned adjustments to taxes, cash reserves, contracts, and coverage |

That only works if your records are easy to pull when you need them. Keep your setup simple, but make sure it clearly shows income, expenses, and transaction summaries. Electronic records are fine too, as long as you can quickly pull what you need, including transaction summaries and your balance sheet. Use a three-part cadence:

- Check regularly

Review account and credit card statements as a habit to spot mistakes or unauthorized charges early. Reconcile major account changes and whether your tax reserve still matches actual collections.

- Review at period close

Close your books and update your balance sheet, then compare profit, cash, and reserves against what actually happened. If U.S. estimated tax applies to you, track the IRS four payment periods and due dates (calendar-year schedule): Jan. 1-March 31, April 15; April 1-May 31, June 15; June 1-Aug. 31, Sept. 15; Sept. 1-Dec. 31, Jan. 15 (following year). Underpaying by those due dates can trigger penalties, even if you expect a refund later.

- Decide in your annual strategy pass

Every January, run a withholding checkup if withholding applies to your setup. Then make your higher-leverage decisions across the three pillars: compliance, cash flow allocation, and resilience gaps (insurance, reserves, retirement, and contract terms).

Start your next cycle with the checklist artifacts you already built: evidence folder, account register, tax residency log, visa-stay log, contracts, returns, statements, and insurance documents. Roll them into your current-year dashboard, then schedule your next regular check and period-close review now.

If you want a deeper dive, read Japan Digital Nomad Visa: A Guide to the New 2025 Program.

If you want to turn this checklist into a repeatable operating workflow, use a freelancer-focused setup for invoicing, collection, payout controls, and audit-ready records where supported. Explore Gruv for freelancers.

Frequently Asked Questions

How do I track tax residency days as a U.S. digital nomad?

Track separate logs for tax residency, visa stays, and account reporting so your records stay easier to review. Start with where you were physically present, then reconcile your calendar against passport stamps, booking records, and local registration documents. Flag every country where your status or living pattern changed.

What should a financial review checklist for a high-income digital nomad include?

Build the checklist around the items most likely to disrupt cash flow: location tracking, filing-status changes, account-reporting checks, tax set-asides, insurance fit, retirement eligibility, and contract terms. Keep one evidence folder with returns, account statements, insurance documents, signed client contracts, and any relevant state forms. If Kentucky applies, confirm whether Form 740-NP fits and keep the Social Security number shown on the return plus the exact whole-dollar refund amount for status checks.

How should I budget for a fluctuating six-figure income as a freelancer?

Use percentage-based allocations instead of fixed monthly promises. In your annual review, use your last 12 months of deposits to reset tax, owner-pay, operating, and reserve percentages based on actual collections.

What are the biggest financial mistakes high-earning digital nomads make?

The biggest mistake is treating separate obligations as one blur and relying on memory or informal advice. One bad assumption can create avoidable errors or delays. Verify instructions on authentic government tax sites by confirming a .gov domain and HTTPS, then document what changed by jurisdiction before you reuse last year's process.

Do I need to file an FBAR if I only use Wise or Revolut?

Possibly. If you are a U.S. person, FBAR is a separate filing requirement triggered when the combined value across all foreign financial accounts exceeds $10,000 at any point in the year. Keep a master account register and track the highest aggregate value year-round instead of assuming no filing is required.

What's the difference between a SEP-IRA and a Solo 401(k) for a freelancer?

The practical difference is usually contribution mechanics versus admin load, but the exact answer depends on current plan rules and provider terms. In your annual review, confirm eligibility, provider support, current contribution rules, and setup or ongoing requirements for each option. The better fit depends on current rules and your operating preferences.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cdc.gov/yellow-book/hcp/health-care-abroad/travel-in...trusted

- consumer.ftc.gov/articles/using-credit-cards-and-disputing-ch...trusted

- consumerfinance.gov/an-essential-guide-to-building-an-emergency-...trusted

- fdic.gov/resources/deposit-insurance/understanding-de...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/businesses/comparison-of-form-8938-and-fbar-...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC10088568trusted

- revenue.ky.gov/Forms/740-NP(P)%20(2023).pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Japan Digital Nomad Visa 2026: Six-Month Planning Runbook

Treat this as your operating model: identify the right mission first, commit to one route, and keep dated records before you make irreversible plans. That is what keeps the rest of your timeline, paperwork, and decisions coherent.

Should Your Freelance Business Accept Credit Cards?

Offer card payments, but stay in control of how money reaches you. The goal is not a smoother checkout screen. It is predictable cash you can use to run the business.

Connect Wise to Xero Without Reconciliation Surprises

**Short answer:** To connect Wise to Xero without reconciliation surprises, first confirm you mean **Wise** rather than **ConnectWise**, connect the correct **Wise Business** profile to the correct **Xero** organisation, document where each active currency should appear in Xero, and test one real transaction before you turn on more features.