Quick Answer

Separate sanctions control from risk investigation. In ofac pep adverse media watchlist screening, a credible unresolved OFAC SDN List match should pause payout release, while PEP and adverse media results should trigger documented CDD or EDD review under policy. The practical model is clear, monitor, escalate with named owners and timestamped rationale. Keep match evidence, reviewer notes, and the linked payment action together so each decision is defensible.

Sanctions Screening as a Payout Control, PEP and Adverse Media as Review Signals#

Use sanctions screening as a payout control, and treat PEP and adverse media as deeper-review signals. If you run a platform that pays contractors, sellers, or creators, you need screening that holds up under AML expectations without turning every weak name match into a frozen payout. That is the real operator problem behind ofac pep adverse media watchlist screening in practice: three controls that sit close together in onboarding and review, but answer different questions and lead to different actions.

Sanctions is the sharp edge. The U.S. Department of the Treasury's Office of Foreign Assets Control, or OFAC, administers and enforces U.S. economic and trade sanctions. Those sanctions can range from blocking the property of specific persons and entities to broader transaction prohibitions. For a payments platform, a credible sanctions hit is not just another risk flag. It can affect whether you are allowed to deal in property or complete the transaction at all.

PEP and adverse media matter for different reasons. They are standard screening categories in onboarding alongside sanctions checks. In practice, those signals usually trigger closer review rather than being treated the same way as a sanctions hit. The practical mistake is treating all three checks as interchangeable and then claiming "we screened them" when the real gap was ownership, escalation, or source review.

This article is built around that operational distinction. It lays out where each check belongs, who should own the decision, how alerts should escalate, and what evidence should survive an internal review or audit. If you deal with cross-border payouts or politically connected counterparties, those distinctions matter. The goal is not maximum friction; it is a process that stops the cases that need stopping and moves legitimate payouts with a recorded rationale.

One checkpoint is worth adopting from day one: test screening effectiveness at implementation and then periodically after go live. Audit work can reach into how your tool filters and matches names, and how potential matches are handled, investigated, and tracked. If you cannot show that chain clearly, you will struggle to explain why a potential match was cleared, escalated, or held.

Read this as an operating outline for compliance, legal, finance, and risk owners, not as jurisdiction-specific legal advice. Legal interpretation still needs specialist counsel. The narrower and more useful goal is to reduce surprises by pairing screening decisions with audit-ready records, named owners, and accountability. That way, your process holds up when someone asks why a payout was released, held, or escalated.

Related: Adverse Media Screening for Contractors: How Platforms Monitor Negative News in Real Time.

At-a-glance comparison operators can use on day one#

Use this table to keep a hard-stop sanctions control separate from deeper-review risk signals.

| Comparison point | OFAC SDN List | PEP | Adverse Media |

|---|---|---|---|

| Purpose | Screen for sanctions-related restrictions. OFAC administers and enforces sanctions, and prohibitions can vary by program, including blocking property/interests in property and other transaction restrictions. | Flag potential political exposure for deeper review under your policy. | Flag potentially relevant negative public information for deeper review under your policy. |

| Trigger point | Set as a release-control checkpoint where a sanctions restriction could affect whether activity can proceed. | Define in your risk policy (for example, onboarding and periodic/event-driven review). | Define in your risk policy (for example, onboarding and periodic/event-driven review). |

| Data inputs | Name and available identifiers against sanctions data. | Name plus the identity/ownership context your policy requires. | Name plus Public Record Information and other Commercially Available Data Sources, where used in your program. |

| Typical disposition | Clear if match is not credible; if credible or unresolved, hold and escalate before release. | Document context and decide whether deeper due diligence is required. | Document context and corroboration, then clear, monitor, or escalate. |

| Escalation owner | Compliance, with legal support where needed. | Compliance or the owner of deeper customer review. | Compliance, investigations, or risk review. |

| What this control does not do | Does not replace KYC, CDD, or EDD. | Does not, by itself, establish a sanctions prohibition or complete due diligence. | Is not proof of misconduct and does not replace identity/ownership review. |

| Hidden cost to plan for | False-positive queue pressure. | Manual-review burden when context is thin. | Investigation latency when sources are incomplete or conflicting. |

The most important row is "what this control does not do." A sanctions result answers a specific sanctions question; it does not complete customer risk assessment on its own.

For day-one setup, keep one clear rule: unresolved sanctions matches do not move forward until compliance review is complete. Then assign explicit ownership and review cadence for PEP and adverse-media outcomes so those alerts are documented, not silently passed.

You might also find this useful: A Guide to Enhanced Due Diligence (EDD) in FinTech.

Where each control fits in your AML decision chain#

Start with identity and customer understanding, then apply watchlist controls by risk type. In practice, KYC and CDD set your baseline at entry, while OFAC, PEP, and Adverse Media screening should continue after onboarding because risk can change over time.

| Decision stage | Main question | Control that matters most | Typical action |

|---|---|---|---|

| Onboarding entry | Is this person or business who they claim to be? | KYC and CDD | Verify identity, ownership, and core profile data before relying on watchlist outcomes |

| Onboarding screening | Is there a legal or risk signal at entry? | OFAC, PEP, Adverse Media screening | Hold and review credible matches before approval or first payout |

| Ongoing monitoring | Has risk changed since approval? | OFAC updates, PEP status changes, new media results | Re-screen on profile, ownership, or payout-detail changes, and on your periodic cycle |

| Pre-payout checkpoint | Can this transaction proceed now? | OFAC sanctions screening | Pause release if a sanctions match is credible or unresolved |

The key boundary is legal exposure. OFAC administers and enforces sanctions, and sanctions programs can range from blocking property and interests in property to broader transaction prohibitions. PEP and adverse media results are risk signals for deeper review; they do not answer the sanctions prohibition question on their own.

Operationally, focus on match quality before clearing anything. Your case file should show the screened name and any secondary identifiers you used, for example, date of birth, country, business registration, or ownership details. Screening on thin or unnormalized data increases both false clears and repeat review work. A practical policy is to treat unresolved sanctions matches as payout blockers and route credible PEP or media matches to documented enhanced review before proceeding.

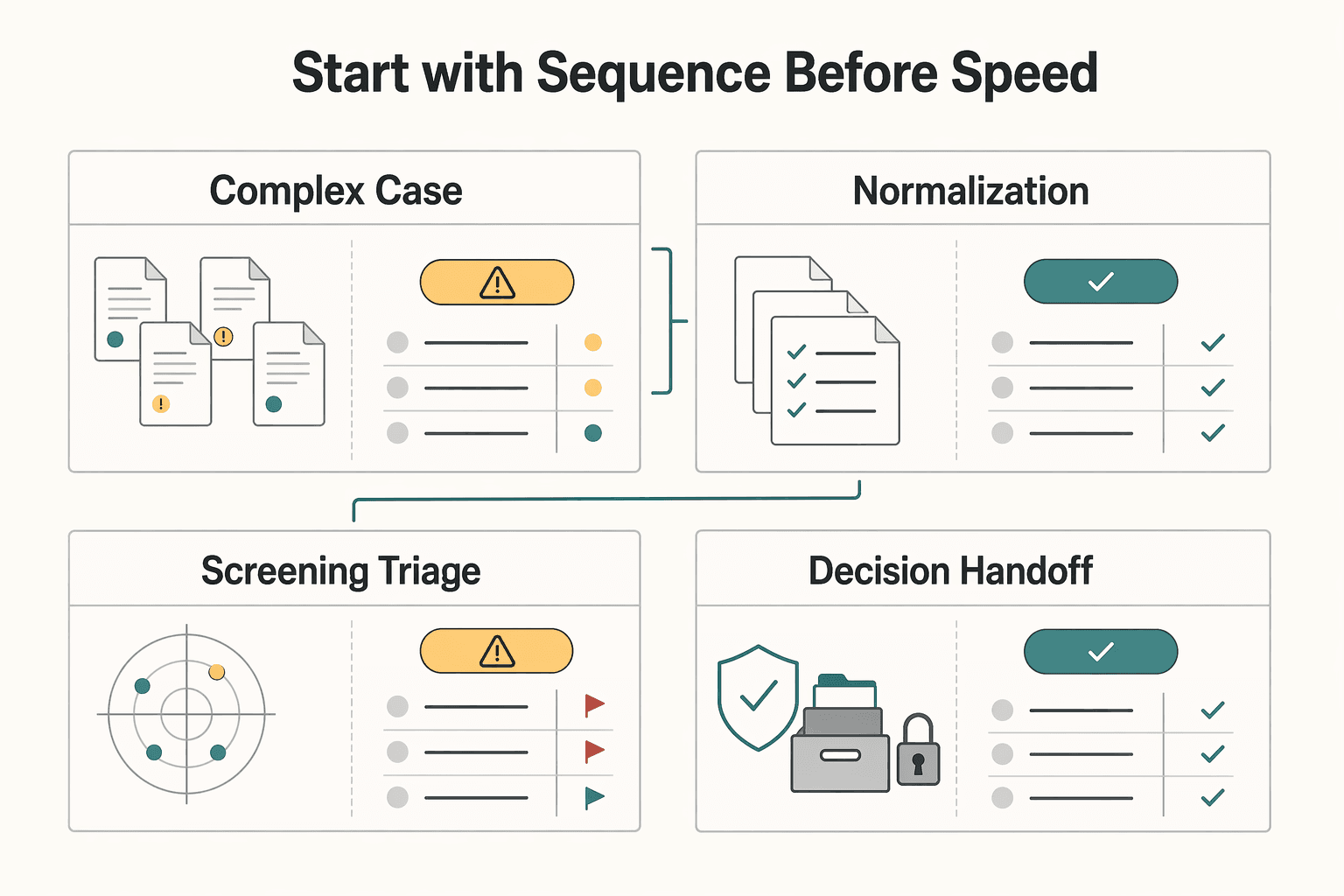

Build the screening sequence and system handoffs#

Sequence is the control: collect and normalize identity data first, then screen, triage, and decide, and make sure the customer and payment record reflects that decision.

Start with sequence before speed#

Screening on thin, unnormalized records creates avoidable noise and weak decisions. A more defensible order is to capture core KYC fields, normalize them, then run sanctions, PEP, and adverse media screening.

| Stage | What must happen | Common break | What to retain |

|---|---|---|---|

| Identity capture | Collect legal name plus available secondary identifiers | Thin records or missing ownership details | Intake values and timestamp |

| Normalization | Standardize names and entity/profile fields before screening | Spelling/transliteration inconsistency, duplicate profiles | Normalized values used for screening |

| Screening and triage | Run sanctions, PEP, and media checks, then route alerts for review | Name-only matches treated as decisive, or alerts cleared too quickly | Match details, reviewer notes, comparison fields |

| Decision handoff | Record the outcome in account and payment workflow | Open alerts disappearing between teams | Final disposition, approver, linked account/payment action |

A practical integrity check is simple: each reviewed alert should show the screened name and the secondary identifiers available at the time. If that comparison record is missing, the clearance is hard to defend.

Silent failures are usually the highest-risk failures#

The failures that create the most exposure may produce no alert at all. Screening can appear healthy while a watchlist stops updating without an error message, so control monitoring has to check feed freshness, not just queue volume.

| Issue | What to watch | Operational note |

|---|---|---|

| Feed freshness | Screening can appear healthy while a watchlist stops updating without an error message | Check feed freshness, not just queue volume |

| Lower sensitivity | Lowering sensitivity can reduce false positives, but it can also miss variants that previously matched | Retest against known positives, near matches, and common name variants |

| Passing UAT once | Passing UAT once at implementation does not prove the control is still working later | Test screening effectiveness periodically after go live |

| List volatility | In 2024 the U.S. Treasury added over 3,100 persons to the SDN List, a 25 percent increase over 2023 | List volatility raises the cost of drift |

Threshold tuning is another quiet failure mode. Screening tools use match sensitivity thresholds to balance detection against alert volume; lowering sensitivity can reduce false positives, but it can also miss variants that previously matched. If thresholds change, retest against known positives, near matches, and common name variants. Passing UAT once at implementation does not prove the control is still working later.

List volatility raises the cost of drift. One cited example reports that in 2024 the U.S. Treasury added over 3,100 persons to the SDN List, a 25 percent increase over 2023. When list activity is moving, stale refreshes and untested threshold changes are more dangerous.

Route by risk type, not queue convenience#

Use escalation paths that match the underlying risk. Potential OFAC SDN List matches should go directly to legal/compliance review. High-confidence adverse media signals tied to corruption risk should move to EDD decisioning, where the team can assess profile context and ownership in more depth.

| Risk type | Review path | Why |

|---|---|---|

| Potential OFAC SDN List matches | Direct legal/compliance review | Use escalation paths that match the underlying risk |

| High-confidence Adverse Media tied to corruption risk | EDD decisioning | Assess profile context and ownership in more depth |

| Third-party intermediaries | Risk-based due diligence | Insufficient scrutiny can create legal, financial, and reputational consequences for the platform |

This is where risk-based due diligence matters, especially when your model relies on third-party intermediaries. Insufficient scrutiny can create legal, financial, and reputational consequences for the platform, not only for the counterparty.

The operating goal is straightforward: prevent alert-state loss across handoffs and keep the case record complete enough that decisions are explainable under pressure.

If you want a deeper dive, read Sanctions Screening for Payment Platforms: How to Run OFAC SDN and Global Watchlist Checks.

Set escalation rules your teams can follow under pressure#

Escalation only works under pressure when each alert type has one owner, one allowed action, and one documentation standard. Keep the model simple enough that teams do not improvise inconsistent decisions.

A practical internal framework is clear, monitor, escalate:

| Disposition lane | When to use it | Primary owner | Case file must show |

|---|---|---|---|

| Clear | Review supports a non-match or low-risk outcome | Compliance | What was screened, what was compared, and why closure was justified |

| Monitor | Risk is credible but not treated as a prohibition | Compliance with enhanced review input | Controls applied, review timing, and ongoing monitoring trigger |

| Escalate | Risk cannot be confidently resolved in routine review | Senior compliance and legal, with payments ops execution | What remains unresolved, decision owner, and final action taken |

Write your rules as direct "if X, do Y" playbooks tied to list scope in your operating footprint, including OFAC, EU, UN, and relevant regional/local lists. This keeps sanctions handling consistent across markets and entities.

Treat escalation as part of one integrated control system, not a standalone sanctions task. In mature programs, sanctions screening is run alongside KYC, PEP, adverse media, and transaction monitoring, which is especially important for cross-border and group-structure operations.

Require a timestamped rationale and reviewer identity for every override. If a second reviewer cannot reconstruct the decision from the case record alone, the control is too weak.

Cut false positives without weakening controls#

Cut noise by tuning matching and review depth by risk type, then require enough evidence before an alert is cleared. Watchlist screening is meant to stop engagement with sanctioned or otherwise high-risk parties, so speed should not replace traceable decisions.

Use sanctions, PEP, and adverse media for different decisions in your process. Sanctions can restrict transactions, while PEP signals elevated risk that usually needs enhanced review rather than an automatic block. Treating every alert type the same increases noise and can blur real priority.

| Tuning choice | What you gain | What you pay for |

|---|---|---|

| Lower match sensitivity across the board | More potential matches reach review | More manual workload and larger queues |

| Higher match sensitivity across the board | Fewer alerts and faster handling | Greater chance that weaker but relevant matches are missed |

| Risk-based tuning plus stronger identifier checks | Better balance between detection and workload | More policy design and ongoing maintenance |

Whatever posture you choose, avoid name-only clearance when additional identifiers are available. Require reviewers to document the matched source, the fields compared, and the rationale for clear, monitor, or escalate.

Then validate drift with periodic sampling of both cleared and escalated cases. If case files no longer show how decisions were reached, your tuning is already too opaque.

For a step-by-step walkthrough, see OFAC Sanctions Screening for Global Businesses.

Monitor continuously and know when to re-screen#

Monitoring only works if you can verify the inputs. If you cannot confirm where your list data came from or whether feeds are current, the rest of the workflow is hard to trust.

| Topic | Supported here | Grounded note |

|---|---|---|

.gov domain | Supported | A .gov domain indicates an official U.S. government organization |

HTTPS | Supported | Sensitive information should be shared only on official, secure websites |

| Specific re-screen trigger events | Not supported here | Only set these details where your policy evidence supports them |

| Risk-tier cadence rules | Not supported here | This section does not include approved support |

| SLA targets | Not supported here | This section does not include approved support |

| Marketplace-versus-B2B frequency guidance | Not supported here | This section does not include approved support |

The clearest supported control here is source verification. When you rely on government list updates, confirm the source is an official .gov website over HTTPS. The DHS guidance states that a .gov domain indicates an official U.S. government organization and that sensitive information should be shared only on official, secure websites.

This section does not include approved support for specific re-screen trigger events, risk-tier cadence rules, SLA targets, or marketplace-versus-B2B frequency guidance, so set those details only where your policy evidence supports them.

Keep an evidence pack ready for audits and internal reviews#

Your screening control is only as strong as its evidence trail. Every alert, review, override, and payout outcome should be traceable from the screening record to the transaction record through one reference ID.

| Evidence set | What it must show | Who will ask for it |

|---|---|---|

| Screening case file | Input data used for the check, source list or dataset, match evidence, reviewer notes, disposition rationale, approver identity, and timestamps | Compliance, internal audit, legal |

| Transaction linkage | Final action (hold, release, or exit) tied to the exact payout or account event affected | Finance, payments ops, compliance |

| Governance file | Policy version in force, exception approvals, case logs, and summary reporting used for AML oversight | Legal, finance, board or committee reviewers |

Run one practical test: pick a sample case and confirm you can follow it end to end with that single ID. You should be able to see the alert, decision, approver, and released or blocked transaction without stitching records across disconnected tools.

For global operators, add a short tax crossover note when identity or account data also supports tax reporting. IRS guidance says Form 8938 is used to report specified foreign financial assets, must be attached to the taxpayer's annual tax return, and may apply alongside FinCEN Form 114 (FBAR). This does not make FATCA or FBAR an AML screening threshold, but weak name, address, or account-country data can still cause downstream reporting errors.

If FATCA reporting is in scope, note whether Form 8938 review was relevant, including the general $50,000 context and the specified domestic entity thresholds: $50,000 on the last day of the tax year or $75,000 at any time during the tax year.

Conclusion#

The practical answer is to treat sanctions, PEP, and adverse media as one coordinated screening set, but not one decision bucket. Sanctions checks answer a legal exposure question. PEP and negative news checks answer risk and investigation questions. If you collapse them into a single "screen everything" rule, you can end up with both outcomes: payment friction for legitimate users and weak escalation when a real sanctions issue appears.

A simple way to keep that distinction alive is to lock in ownership and default actions before you tune anything else.

| Control | What you are actually asking | Default disposition | Typical owner |

|---|---|---|---|

| Sanctions screening | Are you dealing with a sanctioned individual or entity that requires an immediate stop and review? | Hold or block while unresolved | Compliance with legal input |

| PEP screening | Is this customer politically exposed and therefore higher risk, requiring stronger due diligence? | Continue only under CDD or EDD rules if policy allows | Compliance / AML review |

| Adverse Media | Is there credible reporting that changes your fraud, corruption, or reputational risk view? | Review, corroborate, and escalate if material | Compliance / investigations |

That ownership line matters more than most teams expect. Your onboarding policy should be explicit that you screen for sanctioned individuals and entities, PEPs, and adverse media to identify higher-risk customers and make informed decisions. But the evidence standard is different in each lane. A sanctions alert usually needs an immediate hold and fast legal or compliance review. A PEP or media alert needs enough linkage evidence to show you found the right person, what source you relied on, and why you chose CDD, EDD, monitoring, or clearance.

Your evidence pack is what turns policy into something defensible. Keep the screening input, the match details, the reviewer identity, timestamps, the rationale, and the final action tied to the transaction or payout record. One red flag to avoid is treating public records and commercially available data as self-proving. Those sources can contain errors, and some vendor services are not consumer reporting agency outputs under FCRA, so do not repurpose them for eligibility decisions they were not designed to support.

If you need one next step this week, make it operational rather than theoretical. Build the comparison table, write the escalation rules, and standardize the evidence checklist first. Then tune thresholds using real alert outcomes, especially false positives, unresolved alert aging, and cases that required EDD. That sequence gives you a control set you can explain to finance, defend to audit, and improve without guessing.

Frequently Asked Questions

What is the practical difference between OFAC screening, PEP screening, and Adverse Media screening?

OFAC screening is about sanctions compliance risk. OFAC administers and enforces economic and trade sanctions, and many programs require blocking property and interests in property while prohibiting dealing in blocked property. PEP screening and adverse media screening are different risk signals used in a risk-based AML approach, and they are not the same as an OFAC sanctions prohibition.

When should a platform block a payout immediately versus monitor and continue?

Block or hold when you have a credible unresolved sanctions match, because many sanctions programs prohibit dealing in blocked property. PEP or adverse-media alerts are generally handled through risk-based review and ongoing monitoring, with outcomes based on your policy and case assessment. Any unresolved high-risk alert that reaches payout should be treated as a control issue for immediate review.

How often should we re-screen existing users in a risk-based model?

Do not force one calendar rule across everyone. The grounding supports a risk-based approach with ongoing monitoring for sanctions, PEPs, and adverse media, so set cadence and triggers by risk rather than a single fixed interval.

What causes most false positives, and which fixes reduce noise fastest?

The provided grounding does not establish specific false-positive root causes or validated noise-reduction tactics. Treat this as a tuning area: test changes in your own environment and track outcomes rather than assuming one universal fix.

Can adverse media alone justify EDD, or do we need corroborating risk signals?

The grounding supports ongoing adverse-media monitoring in a risk-based AML approach, but it does not set a universal rule that adverse media alone must trigger EDD. In practice, decide based on your policy and case assessment, and keep that decision distinct from sanctions-based legal prohibitions.

What data limitations from Commercially Available Data Sources should be disclosed to leadership?

The provided grounding does not detail Commercially Available Data Source coverage or refresh limits, so avoid hard completeness claims that are not validated internally. Disclose scope and known gaps from your own controls and testing, and clarify that these sources inform risk review rather than replace sanctions obligations.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cs.princeton.edu/courses/archive/spring18/cos226/assignments/...trusted

- dhs.gov/termstrusted

- dhs.gov/sites/default/files/2022-04/DHS%20FY%2021-23...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/businesses/corporations/fatca-information-fo...trusted

- irs.gov/forms-pubs/about-form-8938trusted

- mit.edu/~ecprice/wordlist.100000trusted

- ofac.treasury.gov/faqs/all-faqstrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Sanctions Screening for Payment Platforms Before Payout Release

---

Adverse Media Screening for Contractors on Real-Time Payment Platforms

Adverse media screening belongs in a contractor payout stack only if it helps you make or stop a payment decision fast enough to matter. If alerts pile up without a clear owner, you do not have better control. You have a larger audit problem.

Enhanced Due Diligence in FinTech That Holds Up Under Real Case Volume

For a lean team, practical Enhanced Due Diligence (EDD) is what tends to survive weekly volume. The goal is not bigger files. The goal is repeatable judgment that the next analyst can read and defend without guessing what happened.