Quick Answer

Define the scope as NGN domestic contractor payouts in Nigeria, then run a fixed operating sequence before scale. Collect a minimum evidence pack (legal name, payout destination, KYC status, and hold/review flags), apply eligibility gates, submit, capture callbacks, and close only after reconciliation. Use local rails only for cohorts where pilot records show complete traceability from payout request to final ledger posting. In batch operations, treat "submitted" as in-flight and "reconciled" as the true finish state.

Nigeria contractor payouts on local rails start with the operating model#

If you are evaluating nigeria contractor payouts local rails, start with one practical question: how will money move to a contractor in Nigeria, in NGN, with controls your team can actually run? That matters more than broad policy commentary, because payout outcomes are usually shaped by route choice, compliance handling, and recovery rules.

Step 1 Define local rails narrowly#

Use local rails here to mean local payout pathways for sending contractor funds in NGN. Do not let the term drift into transport content about the Nigerian railway system or PPP project coverage. Search results often mix payment rail discussion with transport-sector material. For a finance, ops, or engineering team trying to ship payouts, that is noise.

Your first checkpoint is simple: write a one-line scope statement and make every owner sign off on it. It should name the country, currency, recipient type, and purpose. For example: "Nigeria contractor payouts in NGN through domestic payout pathways." If your team cannot agree on that sentence, you are not ready to compare routes or promise delivery outcomes.

Step 2 Choose NGN rails only when the operating case is clear#

Local NGN payouts can be a practical starting point when the contractor expects local currency and your team needs a repeatable domestic disbursement path. Use alternatives when coverage is uncertain, when compliance needs are not fully mapped, or when international payment issues such as fees, tax rules, and compliance strategy become the real constraint.

The red flag is assuming "local" automatically means easier. It may be easier for the recipient, but your internal burden can still rise if validation, approval policy, or reconciliation discipline is weak. If you cannot explain why this segment should stay on a domestic route, split the cohort and route only the clearly supported cases first.

Step 3 Commit to a decision-ready output before build starts#

This guide should end in something your team can operate, not just discuss. By the time planning is done, you should have four concrete artifacts:

- a build order for how payouts move from request to completion

- compliance gates that decide what blocks payout and what goes to review

- failure recovery rules for rejected, delayed, or mismatched payouts

- a copy and paste launch checklist your team can use before go live

A good check is whether Finance, Ops, and Engineering can all point to the same decision record and see the same route rules. One common mistake is starting integration work before those rules exist, then discovering later that payout exceptions, tax handling, or compliance review paths were never defined. When that happens, local rails stop being a routing choice and become a cleanup project.

Related: Local Currency Payouts vs USD Payouts: What Contractors Prefer and What Platforms Should Offer.

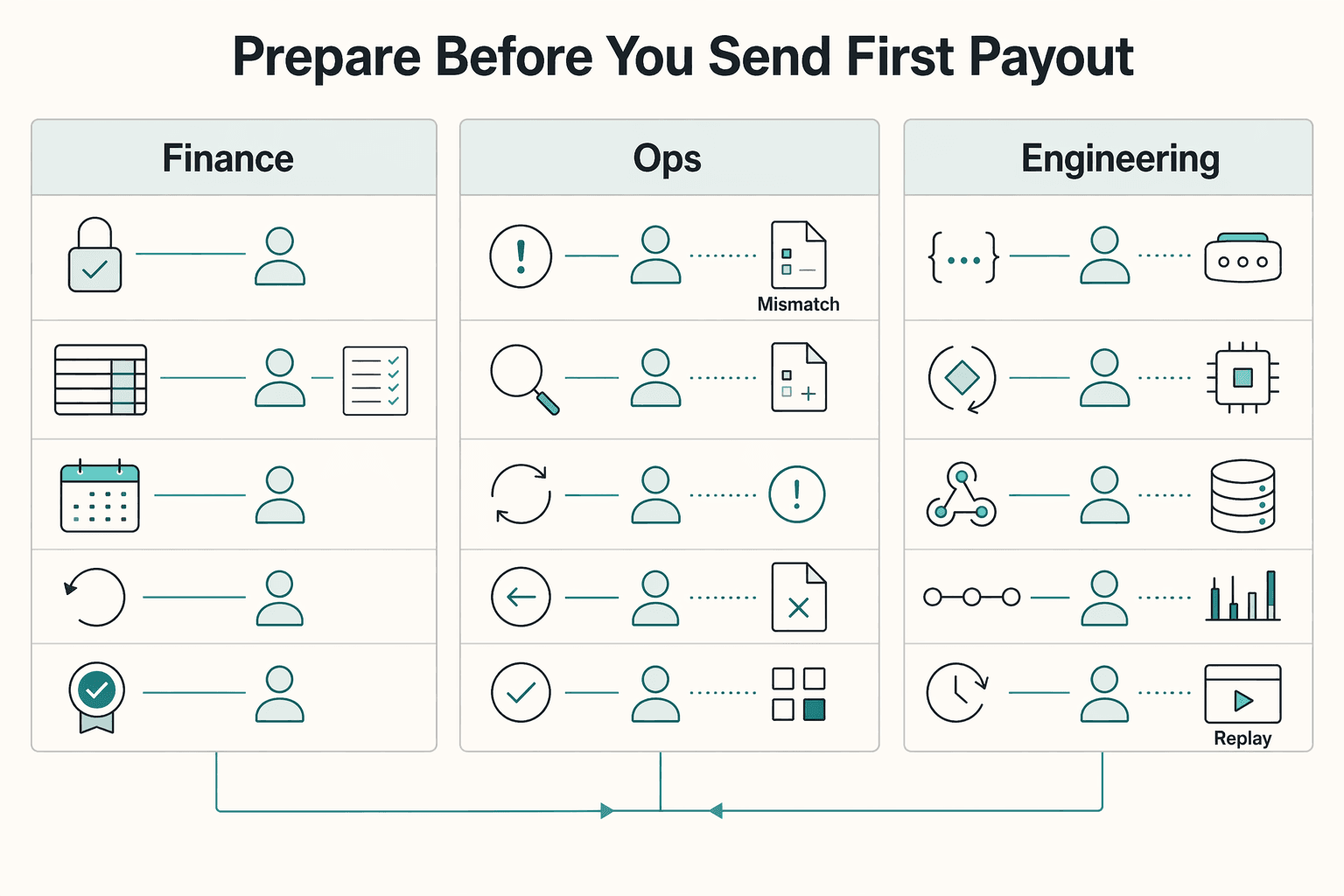

What to prepare before you send the first payout#

Before the first payout, lock scope to NGN, assign clear owners, and standardize the minimum contractor record so your team can run approvals, exceptions, and reconciliation without ambiguity.

| Owner | Primary responsibility | Named systems or outcomes |

|---|---|---|

| Finance | Approval policy | Ledger reconciliation |

| Ops | Exception handling | Rejected or mismatched payouts |

| Engineering | Webhooks and idempotency | Request/callback event trail |

Step 1: Assign owners in writing. Finance owns approval policy and ledger reconciliation. Ops owns exception handling for rejected or mismatched payouts. Engineering owns webhooks, idempotency, and the request/callback event trail. Keep one owner per stage: approval, submission, retry, reversal, and closeout.

Step 2: Gather the minimum evidence pack. Require the same core fields on every contractor before test payouts:

- legal name

- payout destination details

- KYC status

- internal policy flags for holds or manual review

This upfront discipline matters because setup can be due-diligence heavy, and payment setup choices tie directly to fees, tax handling, and compliance strategy.

Step 3: Freeze product scope. Decide whether launch includes Virtual Accounts (to hold funds before payment processing), direct payment methods only, or another managed model your provider supports. Keep version one narrow for this Nigeria cohort.

Step 4: Define launch acceptance criteria before go-live. Set your success-rate target, max unresolved exception count, and daily Finance reconciliation sign-off in advance. If "ready to launch" is not explicit, delay first payout.

What local rails means here and what it does not#

local rails means contractor payouts in NGN (Nigerian Naira) through domestic payout pathways in Nigeria, not transport rail infrastructure.

Use that definition consistently across product, finance, and go-to-market docs to avoid downstream confusion. Search coverage about the Lagos Green Line Metro Rail, the National Assembly, or the 2026 Appropriation Bill is policy context, not payout-architecture guidance.

Step 1 Define the rail by currency and route. State exactly what you support: NGN disbursements to domestic payout destinations. This also distinguishes your flow from cross-border transfers that may use SWIFT messaging, where SWIFT transmits instructions rather than moving funds itself.

Step 2 Treat speed as a measured outcome. Do not publish "fast" or "same day" as a default promise. Validate those outcomes in live operations against your own submission, acceptance, callback, and reconciliation evidence.

Step 3 Qualify coverage claims in customer-facing copy. Use clear qualifiers like "where supported," "when enabled," and "coverage varies by program." This keeps sales and support language aligned with what Ops can actually deliver for each contractor setup path.

If you want a deeper dive, read FedNow vs. RTP: What Real-Time Payment Rails Mean for Gig Platforms and Contractor Payouts.

Choose local rails or alternatives using explicit decision rules#

Use local NGN rails as your default only for contractor segments where local-currency preference and operational controls are both proven in your pilot data. Use an alternative when those controls are incomplete for the SLA you need.

Step 1 Choose a default route from evidence, not copy#

Set a default only after you confirm your records support end-to-end traceability: internal payout ID, beneficiary identifier, provider reference, submission timestamp, callback status, and final ledger posting reference. If those fields are not consistently present, keep that segment off the default path until the gap is fixed.

Step 2 Score each route on control quality#

Compare options on the same decision criteria every time:

| Route option | Recipient experience | Failure visibility via webhooks | Retry safety with idempotency | Reconciliation burden | Exception handling effort |

|---|---|---|---|---|---|

| Local NGN rails | Score from your pilot evidence | Score from your pilot evidence | Score from your pilot evidence | Score from your pilot evidence | Score from your pilot evidence |

| Cross-border bank transfer or wire | Score from your pilot evidence | Score from your pilot evidence | Score from your pilot evidence | Score from your pilot evidence | Score from your pilot evidence |

| Manual review or fallback provider route | Score from your pilot evidence | Score from your pilot evidence | Score from your pilot evidence | Score from your pilot evidence | Score from your pilot evidence |

Use this as a pass/fail tool, not a marketing comparison.

Step 3 Split mixed cohorts instead of forcing one path#

For mixed cohorts, route by segment and make the reason visible in the payout record so Ops can explain each outcome quickly. If a payout does not meet your local-route controls, send it to the documented alternative path instead of forcing it through one rail.

For cross-border edge cases, use wires vs. local rails. For adjacent real-time rail context, use FedNow vs. RTP. We covered related recordkeeping issues in How to Get Local Currency Abroad Without a Recordkeeping Mess. If you want a quick next step on the invoicing side, try the free invoice generator.

Build compliance gates before scaling volume#

Make payout eligibility a hard stop before approval. If you launch first and clean up later, you usually create avoidable rework across bad payouts, missing tax records, and weak audit trails.

| Item | Article handling | Evidence or data |

|---|---|---|

| KYC | Gate before payout approval for every Nigeria payout path | Status, review date, and reviewer or vendor outcome must be visible on the profile |

| KYB | Gate before payout approval for every Nigeria payout path | Status, review date, and reviewer or vendor outcome must be visible on the profile |

| AML | Gate before payout approval for every Nigeria payout path | Status, review date, and reviewer or vendor outcome must be visible on the profile |

| VAT validation | Separate business tax control where required | Use a written policy for what blocks payout and what goes to manual review |

| W-8 | Tie collection to the actual program and reporting setup where enabled | Confirm the required document class is present before first payout approval |

| W-9 | Tie collection to the actual program and reporting setup where enabled | Confirm the required document class is present before first payout approval |

| Form 1099 | Tie collection to the actual program and reporting setup where enabled | Confirm the required document class is present before first payout approval |

| FBAR | Treat as a separate FinCEN reporting obligation, not a contractor onboarding form | Capture maximum account value, currency, and U.S.-dollar conversion rounded up to the next whole dollar |

Step 1 Gate payout eligibility before route assignment#

Put KYC, KYB, and AML checks in front of payout approval for every Nigeria payout path, including local NGN disbursements. A payout should not move from draft to approved unless the profile already shows the required status, review date, and reviewer or vendor outcome.

Use a simple readiness test in pilot traffic: open one payout record and confirm you can see identity status, business status (where relevant), AML outcome, and the timestamp of the latest decision in that same record. If Ops can still push a payout forward with missing fields, the gate is not real.

Step 2 Separate business tax checks from identity checks#

For business accounts, handle VAT validation as its own control where required, with a written policy for what blocks payout and what goes to manual review. The exact rule can vary by program, but Finance, Ops, and Compliance should follow the same one.

Apply that same discipline to tax documents. Tie W-8, W-9, and Form 1099 collection to your actual program and reporting setup where enabled, then confirm the required document class is present before first payout approval.

If FBAR enters scope, treat it as a separate FinCEN reporting obligation for foreign bank and financial accounts, not a contractor onboarding form. Capture data during the year, including maximum account value, currency, and U.S.-dollar conversion rounded up to the next whole dollar (for example, $15,265.25 becomes $15,266).

Step 3 Require audit evidence for every payout state change#

Define required evidence for each payout transition: received, compliance cleared, held for review, approved, submitted, callback received, posted to ledger, reconciled, or reversed. For each change, retain the outcome, reason code, actor, timestamp, related document ID, and provider reference needed for ledger tie-out.

Test this before scale: Compliance and Finance should be able to reconstruct one held payout and one successful payout from the record alone. If FBAR applies, keep filing dates on the compliance calendar as well: April 15, 2026 for all other individuals with an FBAR obligation, and April 15, 2027 for certain U.S. individuals with signature authority but no financial interest under the FIN-2024-NTC7 notice sequence.

Implement the payout lifecycle in a strict order#

Once eligibility is enforced, sequencing becomes the next control. Define one payout lifecycle your team follows every time so outcomes stay safe, timely, and affordable in practice, not just in policy.

Step 1 Create the payout request before execution#

Create a durable payout request first, then let later stages act on that record. Keep the request complete enough for review (payee, amount, currency, destination snapshot, actor, and timestamp) so Ops and Finance can verify what was approved.

Step 2 Apply compliance gates before route and submission#

Run compliance checks as a hard gate before route assignment and transfer submission. If you use credential-based flows (for example, CDD/KYC credential issuance patterns), keep the decision state visible on the payout record before it can move forward.

Step 3 Define event handling rules before go-live#

The source material does not prescribe specific webhook, idempotency, or ledger mechanics. Treat those as implementation choices you must define explicitly, including how you handle retries, duplicates, timeouts, and reversals.

Step 4 Close only after documented verification#

Use clear checkpoints from submission through close, and retain evidence at each state change. If required evidence is missing or inconsistent, keep the payout in exception handling until the record is complete and auditable.

Run payout batches with controls finance teams can trust#

Treat batching as an auditable control unit, not just a bulk transfer file. For Nigeria local-rail contractor payouts, define batch states, evidence requirements, and stop rules before volume scales.

| Batch metric | How to use it | Article note |

|---|---|---|

| Queued count | Track batch health as an operations queue | Do not treat batching as just a finance summary |

| Success count | Track per batch | Headline success rate alone can hide a growing exception queue |

| Retry count | Track per batch | Retries can hide a growing exception queue |

| Unresolved exceptions | Track per batch | Pause new submissions on that route or cohort if exception rate crosses your internal threshold |

| Aging per batch | Track per batch | Settlement times and error rates vary across institutions |

-

Define internal batch states before volume grows. Use statuses such as draft, approved, submitted, partially failed, completed, and reconciled as internal control points. The key is the control boundary at each state: what it means, what evidence is required, and what can no longer change. Before a batch leaves draft, each payout should have a frozen destination snapshot, compliance clearance, and verified beneficiary details, including the required 10-digit NUBAN format where applicable. For any batch ID, Finance should be able to see creator, approver, state-change timestamps, and included payout IDs.

-

Require dual approval for unusual or high-risk batches, and capture override evidence. Do not let one person both prepare and release a batch when value, retry volume, or manual exceptions are outside normal patterns. If a hold is overridden, require a reason code and short note on the batch record, not in chat or email. Keep approver identity, timestamps, reason code, and supporting documentation in the audit trail.

-

Monitor batch health as an operations queue, not just a finance summary. Track queued count, success count, retry count, unresolved exceptions, and aging per batch. This matters in Nigeria because the market is fragmented across more than 20 commercial banks plus dozens of microfinance banks, and settlement times and error rates vary across institutions. If you only track headline success rate, retries can hide a growing exception queue.

-

Publish a daily control report and pause on exception spikes. Tie batch totals to audit-trail records and reconciliation outcomes, with separate views for submitted, completed, partially failed, and reconciled states. Treat submitted as in-flight, not done; close only after reconciliation and exception handling are complete. If exception rate crosses your internal threshold, pause new submissions on that route or cohort and clear the root-cause queue first.

For a step-by-step walkthrough, see How Australian Agencies Can Pay US Contractors With Lower Risk.

Common failure patterns and how to recover fast#

Recover fast by containing risk first and replaying only after the facts are clear. In Nigerian contexts, delays are linked to project performance and financial health, and the effects can spread across clients, contractors, consultants, and the public, not just your Finance queue.

1. Delay chains that keep expanding#

When delays start compounding, pause the affected flow and treat it as an incident, not routine backlog. The immediate goal is to stop further spread while you confirm what is known versus unknown.

2. Incidents with fragmented evidence#

Recovery slows down when facts are split across tools and teams. Keep one incident record with the timeline, current status, owner, and decision notes so everyone works from the same evidence.

3. Premature closure pressure#

Do not close a problem because activity resumed. Close only when the observed issue is resolved, the impact is documented, and ownership for follow-up actions is explicit.

4. Cross-team stalls#

Failures with multi-team impact often linger when accountability is unclear. Assign one owner, set a clear decision path, and document what must happen before normal operations resume.

Related reading: How to Classify a Worker as an Employee vs. an Independent Contractor in the US.

Copy this launch checklist before going live#

Treat go-live as an evidence exercise: each route, control, and finance-close step should be testable and documented before you scale.

- Document route rules by contractor cohort.

Define who goes to local NGN rails, who goes to an alternative route, and the exact switch condition for each case. Keep this written so Ops can identify the correct route from the contractor record without escalation.

- Prove webhook handling and idempotent retries with saved test evidence.

Run and retain test cases for accepted payouts, rejects, delayed callbacks, duplicate callbacks, and manual exception release. Keep request ID, provider reference, callback payload, final ledger state, and operator notes together so outcomes are traceable.

- Enable compliance and tax-document gates before live payouts.

Confirm KYC/KYB/AML states can block or hold payouts per policy. If enabled in your program, assign clear ownership, storage, and release rules for W-8, W-9, Form 1099, and FBAR workflows.

For FBAR mechanics, keep records precise:

- FBAR is the Report of Foreign Bank and Financial Accounts. * Record maximum account values in U.S. dollars, rounded up to the next whole dollar (for example, $15,265.25 -> $15,266). * Value each account separately. * If a calculated maximum value is negative, record 0. * Use the correct due-date scope: April 15, 2026 remains the date for all other obligated individuals; April 15, 2027 applies to certain signature-authority-only individuals.

- Validate reconciliation and audit exports with Finance sign-off.

Run a full-day test batch and confirm counts, totals, and statuses tie from payout submission through daily ledger reconciliation outputs. Finance should verify the audit trail is sufficient to reconstruct approvals, manual changes, and state transitions.

- Launch in phases and expand only after stable batch behavior.

Start with a small cohort, monitor exception aging daily, and pause expansion if repeat failures appear. Do not scale a route while rejects, unmatched ledger entries, or unresolved compliance holds remain unexplained.

Frequently Asked Questions

What does “local rails” mean for contractor payouts in Nigeria?

Here, local rails means domestic NGN settlement paths, not a blanket promise of instant payout. In practice, that usually means commercial bank transfers, NIBSS instant rails, or wallet-based disbursements where supported. Your first verification check is simple but important: the beneficiary account should pass a 10-digit NUBAN format check before you submit anything.

How should we choose between local NGN payouts and cross-border alternatives?

Choose local NGN payout routes when contractors want to receive in naira and you want to reduce delayed credits, failed transfers, and expensive conversion-path friction that can show up in cross-border sending. Route choice is not one-size-fits-all: coverage, institution-level reliability, and your SLA should drive the decision by payout flow. If your source funds are not in NGN, remember the naira is exposed to significant FX volatility, so conversion timing can become an operating issue, not just a treasury issue. For edge cases, this guide pairs well with International Wire Transfer for Platforms: When to Use Wires vs. Local Rails for Cross-Border Payouts.

Which compliance checks should block payout versus trigger manual review?

Set block-versus-review rules in your own policy and provider requirements. A practical pattern is to block when required compliance or account data is missing, and use manual review only for specific gaps that can be resolved with defined evidence. A good rule is this: if nobody can name the exact evidence needed to release the payment, it is not really “under review,” it is just stuck.

What controls are mandatory for reliable payout operations at scale?

Common reliability controls include request idempotency, webhook or callback capture, audit notes for manual changes, and regular ledger reconciliation. It also helps to separate submitted from reconciled, because an upstream success signal is not the same as a finance-close signal. A red flag is any setup where an operator can resend a payout without seeing the original request ID, provider reference, and last accepted status.

How should Finance, Ops, and Engineering split ownership before launch?

No single ownership split is mandated by these sources, but many teams assign Finance to approval policy, ledger treatment, and reconciliation sign-off; Ops to exception handling and beneficiary follow-up; and Engineering to idempotency, callback intake, provider-reference storage, and repair paths for delayed or duplicate events. Before launch, have each team prove one checkpoint in testing: Finance closes a sample batch, Ops clears one held case with documents, and Engineering safely replays a duplicate callback.

How do we run payout batches safely without slowing down month-end close?

Use staged approvals, verify beneficiary files before submission, and pause new batches when exception rates jump instead of pushing volume through. Nigeria is a fragmented banking environment with more than 20 commercial banks plus dozens of microfinance banks, so settlement times and error rates can vary widely across institutions. The practical answer is smaller controllable payout batches, a same-day exception queue, and a hard rule that nothing is “done” until payout counts, totals, and ledger postings all match.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- documents1.worldbank.org/curated/en/099061324063512468/pdf/P176668144...trusted

- elibrary.imf.org/view/journals/087/2021/010/article-A001-en.xmltrusted

- fastpayments.worldbank.org/sites/default/files/2026-02/ID%20Meets%20Ins...trusted

- federalregister.gov/documents/2026/03/25/2026-05791/permitting-r...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- fordlibrarymuseum.gov/the-fords/gerald-r-ford/key-speeches-and-wri...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

FedNow vs RTP for Gig Platform Contractor Payouts

You are not choosing a payments theory memo. You are choosing the institution-backed rail path your bank and provider can actually run for contractor payouts now: FedNow, RTP, or one first and the other after validation.

When Platforms Should Use Wires vs Local Rails for Cross-Border Payouts

Treat rail choice as product logic, not team habit. No rail wins everywhere. SWIFT and local payment rails solve different payout risks, so your job is to route each payout by destination, currency, speed, and cost, not by whichever option sounds more global or more modern.

Local Currency Payouts vs USD Payouts for Contractor Platforms

USD versus local currency is not just a finance setting. For a platform, it changes compliance scope, recipient certainty, reconciliation effort, and how much engineering depth your payout layer needs. In practice, many teams avoid picking one currency forever. A common approach is to set corridor-level rules: use local currency where it is legally and operationally supported, and keep USD as a fallback where legal, coverage, or operational constraints are still real.