Quick Answer

Classify the worker based on the real working relationship, not the contract label. For federal tax purposes, the IRS weighs behavioral control, financial control, and the relationship of the parties, while the DOL asks under the FLSA whether the worker is economically dependent on the company or in business for themself. If facts and paperwork conflict, fix the structure before work starts.

Start Here With the Decision That Protects Your Deal#

Start with the real working relationship, because that drives the classification outcome. If the day-to-day setup looks like a common-law employee relationship, calling the worker a contractor in the agreement does not by itself remove the underlying worker misclassification risk.

You also need to check two federal lenses, because the IRS and DOL start from different questions:

| Decision lens | What the agency asks first | Main signal | Why you should care |

|---|---|---|---|

| IRS federal employment tax lens | What business relationship actually exists between the parties? | Evidence of control and independence in the relationship | Employee treatment generally means withholding and depositing income tax, Social Security, and Medicare from wages |

| DOL FLSA lens | Is the worker economically dependent on the employer, or in business for themself? | Economic dependence points toward employee status | FLSA minimum wage and overtime protections attach to employee status; independent contractors generally do not have those protections |

| Contract label alone | What does the paper call the worker? | Not enough by itself | Labels do not override operating facts |

A practical first checkpoint is the IRS common-law framework. The IRS says to determine the relationship before deciding payment and tax treatment. It weighs all evidence of control and independence across three categories: behavioral control, financial control, and the relationship of the parties.

Use that checkpoint before kickoff. If the arrangement is being set up with employee-style oversight in practice, treat it as a classification red flag now, not a drafting cleanup later.

The DOL adds a second lens under the FLSA: is the worker economically dependent on the employer, or in business for themself? So this guide goes beyond contract language alone. It gives you a contract checklist, a behavior checklist, and an evidence checklist.

Scope note: this section uses U.S. federal framing from the IRS and DOL. DOL Fact Sheet 13 cites 29 CFR part 795 as effective March 11, 2024. It also notes current litigation and references Field Assistance Bulletin 2025-1 (May 1, 2025) and an NPRM comment deadline of April 28, 2026, 11:59 ET. Because litigation and rulemaking are active, monitor updates while aligning contract terms, real behavior, and documentation before the deal goes live.

If facts are genuinely disputed, Form SS-8 gives you a concrete IRS determination path for a specific worker. It is a checkpoint option, not a default step for every deal. Related reading: What to Do If You've Been Misclassified as an Independent Contractor.

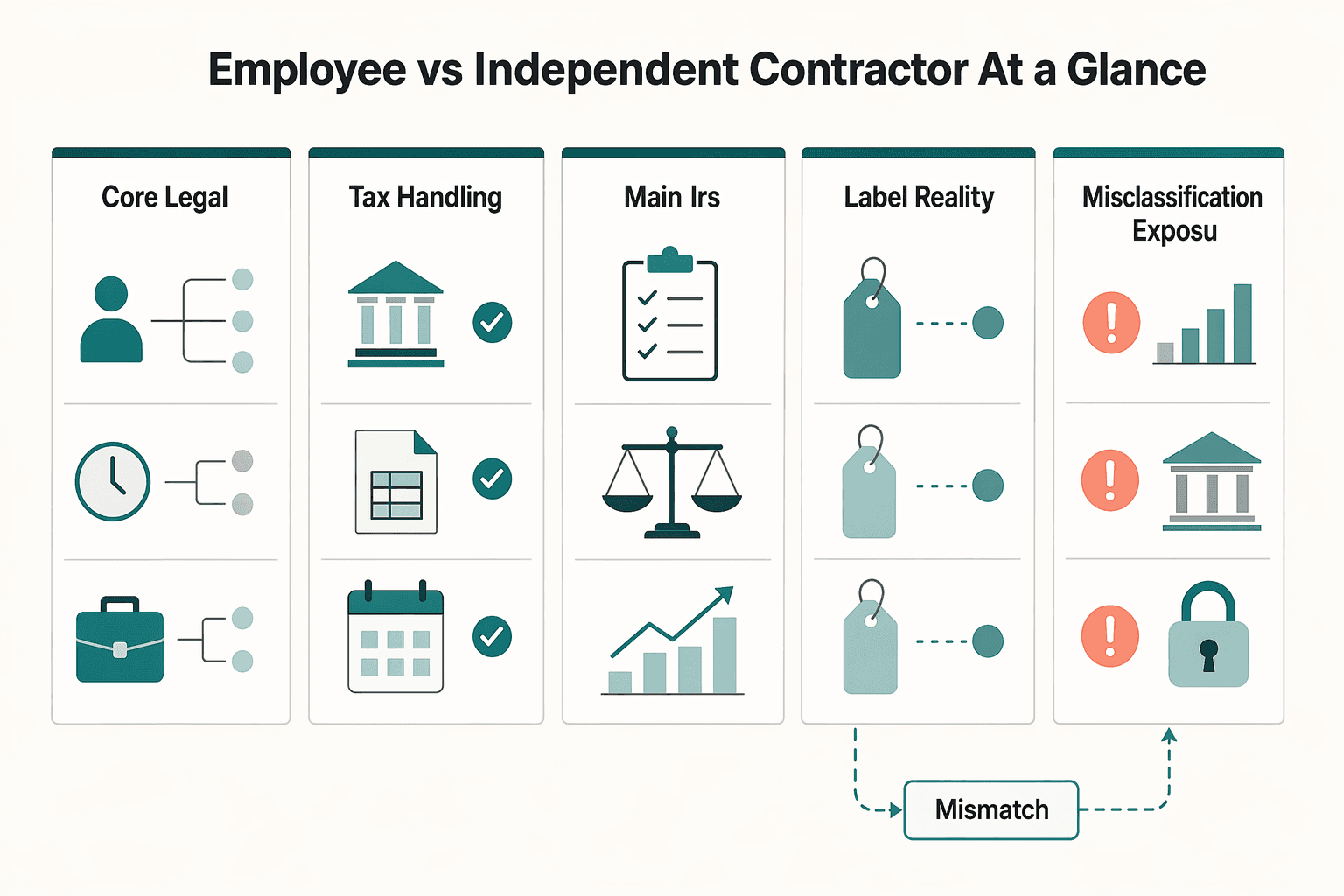

Employee vs Independent Contractor at a Glance#

Use this table as a first-pass screen, not the verdict. If control and tax handling point toward employee treatment, labeling someone a contractor may not reduce misclassification risk.

| Criteria | Employee | Independent contractor |

|---|---|---|

| Core legal signal | The business can control what will be done and how it will be done | The worker is in an independent trade, business, or profession offering services to the public |

| Tax handling signal | Employer generally handles income tax withholding, Social Security tax, Medicare tax, and unemployment tax obligations | Payer generally does not handle those withholdings and tax payments in the same way |

| Main IRS comparison points | Facts across behavioral control, financial control, and relationship of the parties trend toward employment | Facts across those same 3 categories support real business independence |

| Label vs reality | Status depends on the actual working relationship, not just job title or contract wording | A contractor label only helps when the operating facts support it |

| Misclassification exposure | If a worker was misclassified, the business can be held liable for employment taxes | Misclassifying a worker as a contractor can leave employer-paid and employee-withheld taxes unhandled |

Read the control row first#

Start with control in practice. The IRS says an employee is generally someone performing services where the business can control what will be done and how it will be done.

An independent contractor is normally someone in an independent trade, business, or profession offering services to the public. If your contract says "contractor" but the daily work looks like employee-style supervision, treat that as a warning sign.

Use the tax row as a reality check#

Tax handling is an operating signal, not paperwork trivia. In an employee setup, an employer generally must withhold and pay income taxes, Social Security and Medicare taxes, and unemployment taxes. For contractors, the payer generally does not handle taxes on payments in that same way. If a client wants employee-style control but expects contractor-style tax handling, stop and fix the mismatch before work starts.

Run the IRS 3-category screen before signing#

The IRS says to identify the business relationship first, then decide payment and tax treatment. Use all 3 categories together:

| IRS category | What it covers |

|---|---|

| Behavioral control | Whether the company controls, or has the right to control, what the worker does and how the work is done |

| Financial control | Whether the business directs or controls the financial and business aspects of the work |

| Relationship of the parties | Whether facts like contracts, benefits, and relationship terms look more like employment or an independent business relationship |

If the facts are genuinely disputed, Form SS-8 is the IRS path to request a worker-status determination. After that determination, a worker can use Form 8919 to report uncollected Social Security and Medicare taxes where applicable.

Bottom line: focus on control and tax handling, and do not rely on label language when the operating facts point the other way.

For a self-screen, see Are You an Employee or a Contractor? A Self-Assessment Checklist.

IRS Rules That Matter Before You Sign#

If control points toward employee treatment, do not try to force the deal through with contractor tax paperwork. Under IRS rules, classification affects who handles income tax withholding and employment taxes, so this is a structure decision, not admin cleanup.

Before deciding tax treatment, the IRS says to identify the real business relationship first. Under common-law analysis, the IRS weighs behavioral control, financial control, and the relationship of the parties. Labels help only when the day-to-day facts match them.

| Pre-sign question | If the relationship is treated like an employee | If the relationship is treated like an independent contractor | What to do if answers conflict |

|---|---|---|---|

| Who handles tax withholding? | Business generally must withhold and deposit income taxes, Social Security taxes, and Medicare taxes from wages | Business generally does not have to withhold or pay taxes on payments in the same way | Pause and ask why contractor paperwork is being used if employee-style tax handling signals are present |

| Who pays employer-side employment taxes? | Business generally pays the matching employer portion of Social Security and Medicare taxes and unemployment tax | Contractor handles self-employed tax obligations on their side | Escalate if the client wants to avoid employer-side tax obligations while keeping employee-style control |

| How is the relationship documented? | Wage treatment and relationship terms that fit employment | Agreement terms and documentation that fit an independent business relationship | Reconcile the agreement, onboarding, and actual expectations before work starts |

| What is the control expectation? | Business can control what will be done and how it will be done | The business has less control over how the work is done | Treat employee-like control plus contractor forms as a red flag |

The negotiation point that actually saves you#

A practical failure mode is employee-like control with contractor-style paperwork. If a client wants to direct your day-to-day work but avoid the withholding and employment-tax responsibilities that usually come with employee treatment, slow the deal down.

Use a plain line in negotiation: if you need employee-style control, the tax handling and documentation need to match. If the client wants contractor treatment, the operating facts need to support that structure.

Ask these questions before you sign#

Put these questions in writing before any start date, then compare the answers across documents and expected conduct:

- Who is responsible for income tax withholding and employment taxes?

- Will I be paid as wages, or as a service provider under a business agreement?

- What documents define the relationship in practice?

If the agreement says "independent contractor" but the expected working methods look employee-like, treat that as a real classification issue.

Use the IRS self-employed page as your baseline#

If the relationship is truly contractor-to-client, use the IRS Self-Employed Individuals Tax Center as your baseline for self-employed tax obligations. It helps you confirm what shifts to you when the payer is not handling withholding in the employee way.

If facts are disputed or unclear, Form SS-8 is the IRS path for a worker-status determination for federal employment taxes and income tax withholding. Use it when labels and operating facts do not match.

Before you sign, get two answers in clear terms: who controls the work and who handles taxes. If those answers point in different directions, fix the structure before work starts. Related: Understanding Indonesian Taxes for Foreign Workers.

DOL Economic Reality Test in Plain English#

Once the tax lens is clear, run the FLSA lens. For DOL purposes, the question is not what the contract calls you. It is whether you are in business for yourself or economically dependent on the company for work.

Under DOL guidance in 29 CFR part 795, a contractor label alone does not decide status. The agency's position is that actual practice matters more than what is only written or theoretically possible.

What the DOL is actually asking#

In plain English, the DOL looks at how the relationship works in real life. The framing is direct: an independent contractor is in business for themself, while an employee is economically dependent on an employer for work.

In the 2026 proposal materials, two anchors stand out: control over the work and opportunity for profit or loss. If the client controls the work in practice and your upside does not reflect independent business judgment, treat that as a serious classification warning.

DOL employee vs contractor lens#

| Question | Employee signal under FLSA | Independent contractor signal under FLSA |

|---|---|---|

| Core economic position | Economically dependent on the company for work | In business for themself |

| Control in practice | Company meaningfully directs how the work is done | Worker controls how the work is performed |

| Profit or loss | Earnings look more fixed and less tied to business judgment | Worker has a real opportunity for profit or loss based on how they operate |

| Paper terms vs real conduct | Actual practice can outweigh a contractor label | Contract terms help only if day-to-day facts match them |

| FLSA consequence | Minimum wage and overtime protections attach when there is an employment relationship and FLSA coverage | Those employee protections generally do not attach in the same way |

Use this decision rule: if the paper says contractor but the operating facts show dependence, trust the facts first. A practical check before kickoff and again at renewal is to compare your service agreement, onboarding instructions, and live manager behavior. If they do not match, that mismatch is the risk.

Why this matters in rights and obligations#

This is not just a paperwork issue. Under the FLSA, minimum wage and overtime protections apply when there is an employment relationship, and misclassification is treating a worker who is an employee under FLSA as an independent contractor.

The DOL also states that employers are responsible for deciding whether a worker is an employee under the FLSA. So a contractor template does not resolve a relationship that functions like employment.

What is stable and what is moving#

Stable ground: DOL points to guidance at 29 CFR part 795, and the WHD misclassification page references a final rule published on January 10, 2024, effective March 11, 2024.

Moving ground: policy activity continues. Docket WHD-2026-0001 was posted on Feb 27, 2026, with comments due by Apr 28, 2026. It proposes rescinding the current Part 795 analysis in favor of a modified 2021 approach.

Practical move: date-stamp your classification file and keep the contract, work instructions, and a short fact-based note showing why the relationship is independent in practice.

For the full breakdown, read How to Structure a Commission-Based Independent Contractor Agreement.

Reclassification Red Flags Freelancers Miss#

This is where the problem often shows up first: the contract stays the same, but the working relationship shifts. If the client is increasingly controlling how you work, treat that as a serious worker misclassification risk, even if your agreement still says independent contractor.

Under DOL guidance, labels and paperwork are not enough on their own. A signed independent-contractor agreement and a 1099 are weak proof when day-to-day facts look more like an employment relationship.

Behavior signals to review immediately#

| Operating fact | Lower-risk contractor signal | Employee-like risk signal |

|---|---|---|

| Schedule | You control when work is performed and commit to outcomes | A manager sets your schedule or requires fixed internal attendance |

| Supervision | Client evaluates deliverables and results | A manager assigns tasks and controls how the work is done |

| Control of work | You choose how to complete the work within scope | A manager directs day-to-day work methods and execution |

No single fact decides status by itself in every case. But when several of these patterns show up together, especially over time, the relationship may be drifting away from true contractor treatment.

Where false comfort shows up#

A common miss is the contract-reality mismatch: the paper says contractor, but daily operations look subordinate. In practice, that mismatch is the red flag to prioritize.

What to do if control is increasing#

Do not auto-renew and assume the old contract resolves the risk. Pause renewal, document what changed, and renegotiate boundaries around deliverables, deadlines, and acceptance criteria instead of accepting employee-style supervision.

Use a short checkpoint file before you respond:

- current agreement and scope

- current work instructions

- recent examples of schedule demands, task assignment, or controlled work

- invoices or milestones showing whether you are paid for outcomes or managed like staff

Build a quarterly reality check#

A quarterly review is not a legal requirement, but it is a practical control. Each quarter, confirm who sets the schedule and who decides how the work gets done. If the answer is getting weaker, reset the operating model or stop treating the role as independent contractor.

If you want a deeper dive, read How to Legally Avoid Double Taxation: A Freelancer's Guide to Tax Treaties.

Contract Clauses That Keep You Independent#

After you check behavior, check the paper. Clause review is not a federal safe harbor, but it can reveal risk signals early. A contract label alone does not control status. DOL looks at the economic realities of the full relationship, and the IRS says you must first identify the real business relationship before deciding treatment.

At the federal level, classification also changes obligations and protections: employees and independent contractors are treated differently for tax withholding and FLSA coverage.

Read each clause with one question: does this look like two businesses allocating risk, or employee-style control with contractor-style exposure? Use that as a risk screen, not a standalone legal test.

Protective language versus employee-like language#

| Clause | Protective clause language (risk lens, not a federal safe harbor) | Employee-like or one-sided risk signals |

|---|---|---|

| Termination | Clear notice, payment for completed work through end date, and handoff tied to deliverables or milestones | At-will termination on vague dissatisfaction, unclear payment duties, and open-ended post-termination cooperation |

| Limitation of Liability | Balanced cap structure, or narrow carve-outs for specific high-risk issues (for example confidentiality or IP breach) | Client limits its own exposure but carves your side out so broadly that your cap is mostly unusable |

| Indemnification | Narrow, defined triggers tied to your own breach, negligence, or agreed IP commitments within scope | One-way indemnity for anything "arising out of," "related to," or "in connection with" the services, including risks you cannot realistically control |

| Governing Law | Law with a real connection to the parties or deal, chosen for predictable commercial enforcement | Distant law selected mainly for client advantage and higher enforcement burden for you |

| Jurisdiction | Specific venue reasonably connected to the work or parties, or a neutral forum both sides can access | Client-home venue only, with most travel and enforcement burden on you |

| Dispute Resolution | Clear process, timeline, and forum with mutual obligations | Vague escalation, mandatory internal complaint routes, or client-controlled delay points before you can bring a real claim |

The clause that deserves the hardest pushback#

If indemnification is broad and one-way while control rights are employer-like, renegotiate before signing. That combination can increase your contract risk and can be a mismatch signal, but no single clause by itself determines federal worker status.

The failure mode most freelancers miss#

Vague termination rights plus broad limitation-of-liability carve-outs can create a lopsided result: the client exits quickly, payment gets disputed, and claims against you still sit outside the cap. That is a contract-risk problem on its own, and it can also be part of a broader mismatch signal when day-to-day control looks employee-like.

How to audit before signature#

Do one pass that compares contract language to actual operations. Federal classification looks at the full relationship:

| Review area | What to compare |

|---|---|

| Agreement and SOW | who controls method, schedule, and task assignment |

| Payment terms | are you paid for outcomes or managed like staff |

| Approval flow | deliverable acceptance versus layered internal supervision |

| Onboarding instructions | any manager-style reporting lines or fixed attendance demands |

If the paper says "independent contractor" but operations say "follow our direction and absorb our risk," treat it as a structural issue and renegotiate before signature.

This pairs well with our guide on How to Handle Termination of an International Contractor.

Turn your clause audit into a cleaner first draft with Gruv's Freelance Contract Generator, then finalize language for your jurisdiction.

Operating Like a Business After the Contract Is Signed#

Good contract language is not enough. Your conduct after signing should support the same story. If you want treatment as an independent contractor, run the engagement like one business providing services to another. In practice, that can include clearly defined work, acceptance of agreed outputs, invoicing for services, and vendor-style progress updates rather than supervised staff reporting.

Use one simple check throughout the project: do your records show a business relationship, or day-to-day direction that looks like employee management? The IRS says payment treatment starts with the underlying business relationship. The U.S. Department of Labor (DOL) says status under the FLSA turns on economic realities, not labels.

Vendor conduct versus employee-like conduct#

| Operating point | Business-to-business signal | Employee-like signal | Why it matters |

|---|---|---|---|

| Work definition | Scope tied to deliverables, milestones, or a statement of work | Open-ended task stream assigned as needs arise | Open-ended assignment can look less like a separate business relationship |

| Progress communication | Periodic updates on outcomes, blockers, and delivery dates | Ongoing supervisory check-ins or routine step-by-step approvals | Ongoing supervision can support an economic-dependence narrative |

| Payment trail | Invoice tied to agreed services or accepted milestones | Payment flow that does not track defined services | The IRS looks first at the real business relationship before payment treatment |

| Change handling | Written scope, timeline, or fee updates when work expands | Informal reassignment into internal priorities without a commercial reset | Undocumented control shifts can make independent-contractor treatment harder to support |

Use this as an operating check, not a safe harbor. The goal is consistency between contract terms and actual practice.

Keep boundaries visible in writing#

Boundary drift can happen gradually. A client may start with outcome-based work, then shift toward closer control over how work is done. When that happens, restate boundaries in writing and treat it as a scope discussion.

A simple checkpoint: if a new request changes control over method, timing, or sequence, consider documenting it as a change to the engagement. Confirm current deliverables, describe the new request, and propose updated scope, timeline, or fees.

Documentation hygiene that helps#

Consistent records matter more than perfect records. Keep a clear trail from scope to acceptance to payment, such as the agreement, SOW, acceptance notes, invoices, and written scope changes.

If your working pattern starts to mirror internal employee management, your facts become harder to support as independent contractor treatment. If supervision increases, consider a written reset that confirms deliverables and deadlines, identifies the new control request, and proposes revised terms.

For a step-by-step walkthrough, see The Department of Labor's New Independent Contractor Rule (2026).

Cross-Border Reality for US Client Work#

Before moving on to evidence and defense, keep one boundary clear: worker classification is one question, and cross-border personal reporting is another. The employee-versus-contractor analysis for U.S. client work does not, by itself, determine whether Form 8938 or FBAR filing duties apply.

The terms can sound related, but they are not interchangeable. Form 8938 sits in the IRS and FATCA reporting lane, and FinCEN Form 114 (FBAR) is a separate filing.

| Track | Main question | Examples you may see | What it does not settle |

|---|---|---|---|

| Worker classification | Are you operating as an employee or an independent contractor? | Contract terms, operating facts, classification analysis | Form 8938/FBAR filing obligations |

| Foreign asset reporting | Do you have reportable specified foreign financial assets or foreign accounts? | Form 8938, FATCA, FinCEN Form 114 | Whether your U.S. worker classification is correct |

| Personal tax filing | What returns or schedules may apply to your own tax situation? | Annual return and related schedules | Whether a client can treat you as a contractor |

Practical checkpoint: if Form 8938 is in play, treat it as its own filing test. IRS framing is a two-part gate: specified person status plus a reportable interest in specified foreign financial assets. If it applies, Form 8938 is attached to your annual return by that return's due date, including extensions. Thresholds are not one-size-fits-all, and IRS notes higher thresholds for joint filers or taxpayers residing abroad, so do not assume the baseline $50,000 figure is your rule.

A common failure mode is treating Form 8938 and FBAR as substitutes. Form 8938 instructions explicitly state that filing Form 8938 does not remove the requirement to file FinCEN Form 114 when FBAR is required.

Use this article for classification only. It does not provide state-specific tests, state penalty schedules, or non-U.S. country reporting rules.

We covered this in detail in Independent Contractor Status for Cross-Border Freelancer Contracts.

Build an Evidence Pack Before Problems Start#

If you may need to defend the relationship later, build the file now. Worker status is scrutinized across industries, and misclassification exposure can be substantial.

Your evidence pack should do two jobs: show what you agreed and show how the work actually operated over time. Labels alone do not decide status.

| Evidence item | What it helps show | Weak substitute or red flag |

|---|---|---|

| Signed agreement and documented scope changes | What control, deliverables, and responsibilities were agreed, and what changed later | A contract with no record of changes even though the work evolved |

| Invoices and payment confirmations | Business-style billing and payment history, including gross-pay handling without withholding | Only a 1099 or only bank deposits with no invoice trail |

| Communications reflecting vendor status | Outcome and deliverable updates rather than day-to-day employee-style supervision | Messages that read like direct supervision or ongoing internal management |

| Checkpoint log on control and dependency facts | When facts changed, who requested it, and whether the relationship moved toward employee treatment | No dated log, or relying on memory after a dispute starts |

Keep the checkpoint log simple: date, what changed, who asked for it, and why it does or does not affect classification. This is the bridge between contract language and real conduct.

The common failure mode is clean paperwork and messy operations. A contractor label, 1099, and gross pay without withholding can still fail if the day-to-day facts look like employment. Use a practical check for your own process: if you cannot explain the full relationship clearly and without contradictions, your file is not ready.

If California is in scope, add a separate state-law checkpoint. California's ABC test is not national, and contractor treatment there requires meeting all three conditions. A label or 1099 alone is not enough.

Keep a live misclassification-defense folder for each client and update it whenever control changes. The strongest file tells one consistent story from contract terms to invoices to day-to-day conduct.

Client Pushback Scripts and Decision Rules#

This is where you protect classification in real time. Use pushback early to keep the day-to-day facts aligned with contractor treatment, not employee-style supervision.

| Client move | Why it is a red flag | What to say |

|---|---|---|

| Daily check-ins, fixed internal hours, manager approval for routine work | DOL economic reality analysis includes degree of control, and employee-style supervision can weigh against contractor treatment | "I can commit to outcomes and timelines, but not employee-style supervision. Let's set deliverables, deadlines, and review points instead." |

| "We'll just handle this as contractor paperwork" while expecting staff-like behavior | Classification is assessed case by case based on the real relationship, not labels alone | "Let's align the paperwork with the real relationship." |

| Broad one-way Indemnification plus tight control rights | Indemnity alone does not decide status, but this combination can shift risk to you while control looks employee-like | "If you need this level of control, we should either narrow indemnification or reprice the engagement for the added risk." |

Use this escalation ladder when terms drift. Clarify the issue in writing with one concrete example. Then propose alternative language tied to deliverables and acceptance criteria, and pause onboarding if it remains unresolved.

Decision rule: before accepting new supervision terms, review all six DOL economic reality factors, not just control. Named factors include control, opportunity for profit or loss, permanence of the relationship, and investments, and no single factor is automatically decisive.

If the client insists on employee-like control and refuses to narrow one-sided Indemnification, walk away or reprice for the added exposure. If you rely on rule text, verify it against an official Federal Register edition rather than an XML rendering alone.

Make the Classification Decision Defensible Before You Start#

The through line is simple: decide classification before kickoff, because relationship facts matter more than labels alone. If the real working setup points to employee-style control, calling someone an independent contractor in the contract will not fix it.

Use the same sequence every time so your decision is consistent and defensible:

| Step | What to check | Supports contractor treatment | Red flag to fix before start |

|---|---|---|---|

| At-a-glance screen | Overall relationship under common-law factors | Facts show limited right to direct how work is done and limited control over the business side of the job | Employee-style direction or control paired with contractor paperwork |

| Clause audit | What the contract actually says about control and relationship | Written terms align with independent service and match expected practice | Contractor label, but clauses grant supervision-style control rights |

| Operating-boundary setup | How work will run day to day | Day-to-day model stays consistent with contractor-style independence | Day-to-day practice shifts toward staff-like control over how work is done |

| Evidence-pack maintenance | What you can prove later about control and relationship | Records consistently show how the relationship operated over time | No reliable record of how the relationship actually operated |

Anchor your review in the IRS common-law framework: behavioral control, financial control, and relationship of the parties. Ask directly who controls how the work is done, who controls the business side of the job, and what the full relationship record shows over time. A written contract matters, but it is only one fact in a broader analysis.

Then protect the classification in operations, not just in drafting. Contracts and day-to-day practice can diverge, so keep boundaries clear and document material changes in control. If control-heavy clauses remain unresolved, pause before kickoff rather than treating them as minor wording issues.

If federal tax status is still genuinely disputed after that review, file IRS Form SS-8 for a formal determination. Also, if you consult the DOL rule entry published on 01/10/2024 (89 FR 1638), do not rely on the Federal Register XML page alone for legal research. Verify against an official edition.

If you want contractor payments and records to stay operationally clear as you scale, talk to Gruv.

Frequently Asked Questions

What is the core difference between an employee and an independent contractor in the U.S.?

The core difference depends on the legal lens you are using. Under the FLSA, the DOL looks at economic realities, including whether the worker is economically dependent on the employer or in business for themself. For federal employment tax, the IRS applies common law rules and weighs behavioral control, financial control, and the relationship of the parties.

Does calling someone an independent contractor in the contract make it legally true?

No. Contract labels alone do not control status. If the day-to-day facts show employee-style direction and control, that can conflict with contractor treatment.

Who is generally responsible for payroll tax withholding in an employee relationship?

In an employee relationship, the business generally must withhold and deposit income tax, Social Security tax, and Medicare tax from wages. The business generally also pays the matching employer share of Social Security and Medicare taxes and pays unemployment tax.

Do independent contractors receive federal minimum wage and overtime protections under the FLSA?

Generally no. Minimum wage and overtime protections attach when there is an employment relationship and FLSA coverage. Misclassification can cause workers to miss protections they were entitled to as employees.

Is there one single U.S. classification test that controls every situation?

No. The IRS uses common law rules for federal employment tax, while the DOL says FLSA employment is broader than common law control standards used in other federal contexts. Use the right legal lens for the specific issue instead of relying on one shortcut test.

What can I rely on now if federal rules are being litigated or updated?

Rely on current IRS guidance for tax classification and current DOL guidance for FLSA analysis, including materials tied to 29 CFR Part 795. The DOL says its 2024 rule, effective March 11, 2024, is being litigated but remains in effect for private litigation. Because policy activity is ongoing, confirm current agency pages before final decisions.

What key details are still unknown without full state-law analysis?

Federal guidance does not resolve every state-law consequence. You still need state-specific analysis for wage and hour, unemployment, workers' compensation, and related classification outcomes. If tax treatment is disputed, Form SS-8 is a concrete federal checkpoint for a worker-status determination for employment taxes and income tax withholding.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- dol.gov/agencies/whd/fact-sheets/13-flsa-employment-...trusted

- dol.gov/agencies/whd/flsa/misclassificationtrusted

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- federalregister.gov/documents/2024/01/10/2024-00067/employee-or-...trusted

- irs.gov/businesses/small-businesses-self-employed/in...trusted

- irs.gov/taxtopics/tc762trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC11321953trusted

- regulations.gov/document/WHD-2026-0001-0001trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Freelancers Can Legally Avoid Double Taxation With Tax Treaties

Classify the tax problem before you touch a return. If your income is mostly personal service fees across borders, this guide fits. If your issue is C corporation profits and shareholder dividends, you are solving a different problem.

Indonesia Tax for Foreigners With a Defensible Filing Path

---

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.