Quick Answer

Start with a small planned withdrawal and treat cash as a documented business flow from day one. To get local currency abroad, use a business-linked card when possible, withdraw from an ATM with clear operator and fee disclosure, choose the local-currency prompt, and capture receipt details right away. Then reconcile each debit against your notes and attachments on a weekly cadence so gaps are resolved before reporting.

For a global professional, cash is both a practical necessity and a recordkeeping problem. You need it for ground-level spending like a local fixer, taxi, or coffee. But every untracked withdrawal and every missing receipt creates work later. It can turn into an audit question, an expense you cannot support, or a deduction you cannot defend. That uncertainty pulls attention away from the work itself.

The fix is not chasing the best exchange rate. It is using a disciplined, three-phase protocol that turns each withdrawal into a documented, defensible business expense. Done right, foreign cash stops being something you worry about and becomes something you control. You create a clear chain of custody from your home bank to final reconciliation.

Phase 1: Your Pre-Deployment Capital Strategy#

If you want local currency on arrival with low friction and clean records, do the setup before you fly. Decide what stays on card rails, what truly needs cash, which account will fund it, and how you will document the flow.

1. Build a day-one payment map#

Start with your first 72 hours. The goal is not to arrive with a large cash buffer. It is to plan a small, intentional withdrawal tied to real cash-only use. Use this pre-departure checklist:

| Planning area | Details |

|---|---|

| Card-first spend | prepaid lodging, transport bookings, coworking, app-based rides, other digital bookings |

| Likely cash-only spend | tips, some taxis, tolls, small vendors, market purchases, emergency transit, local on-the-ground advances |

| Verify in-market | card acceptance can vary by city and merchant type, so confirm what is realistically payable by card where you are landing |

| Redundancy | carry more than one payment card so a single decline, fraud flag, or network gap is less likely to block access |

A useful rule is simple. If you can pay digitally before arrival, keep it off your cash ledger. That reduces documentation work during the trip and makes reconciliation easier later.

2. Run the compliance precheck before moving funds#

Before you transfer money into a travel account or multi-currency balance, check that the move will not create reporting work you have not planned for. For U.S. readers, one key issue is aggregate foreign-account value during the year, not just a one-day balance in a single account. Verify the current reporting threshold from official tax, finance, bank, advisor, provider, or source records before you use it.

Keep the precheck light, and do it before spending starts. Once money is moving, your records should already support time, place, and business purpose:

- capture balances in relevant foreign-held accounts on the funding date

- add a short note on transfer purpose

- confirm whether your accountant wants separate tracking for this transfer

3. Choose the disbursement tool, not just "a card"#

The right tool gives you predictable costs, clear records, and dispute terms you understand before you travel. Do not choose on convenience alone.

| Tool | Fees | Limits and access | Dispute handling | Bookkeeping clarity |

|---|---|---|---|---|

| Personal debit card | May include foreign transaction fees and out-of-network ATM fees, depending on issuer | ATM and daily limits vary by bank | Consumer-account protections are tied to personal-purpose account scope; timelines and treatment depend on account type | Lower clarity when business withdrawals mix with personal activity |

| Business debit card | Issuer fees vary; some issuers waive their own ATM fee while third-party surcharges may still apply | Limits vary by bank and account setup | Do not assume consumer protections apply the same way; some zero-liability programs exclude certain commercial cards | Clear separation of business and personal cash activity |

| Multi-currency account card | Designed for cross-border spend and balances; may support many currencies in one account model | ATM access and withdrawal rules vary by provider | Protection terms depend on provider and account or card terms | Can be clear if funded and used only for trip operations |

Two simple rules help you avoid common fee and conversion mistakes:

- using another institution's ATM can trigger both an operator fee and your own bank or credit-union fee

- when prompted at ATM or POS, choose local currency if you want network conversion rates to apply

4. Log the internal transfer with a repeatable format#

Before the first withdrawal, create a simple record for the funding transfer. This is not legally required wording. It is a repeatable control that makes your intent easy to follow later.

Use three fields:

- Purpose tag:

Client workshop / vendor advance / field expenses - Account tag:

Ops travel card xxxxorMulti-currency trip wallet - Expense note: trip location, travel dates, and expected cash uses

For example: Purpose: client workshop. Account: Ops travel card 4421. Note: Funding transfer for Lisbon trip, 12 to 16 May, expected cash uses: taxi arrivals, cash-only meals, venue tips. That one-line structure creates the first link in the chain of custody before any cash leaves an ATM.

You might also find this useful: A Guide to Using a Charles Schwab Debit Card for International ATM Withdrawals.

Phase 2: The In-Country Protocol for Compliant Cash Disbursement#

Once you are on the ground, keep the standard the same every time cash moves. Use a machine or terminal you can identify, treat conversion choices as a records decision, and log enough detail to defend the transaction later.

This is about record quality, not broad claims that one ATM type or one conversion path is always cheaper or safer. For U.S. readers, the same discipline can also support later reporting if aggregate foreign-account value goes over the FBAR filing criterion of $10,000.

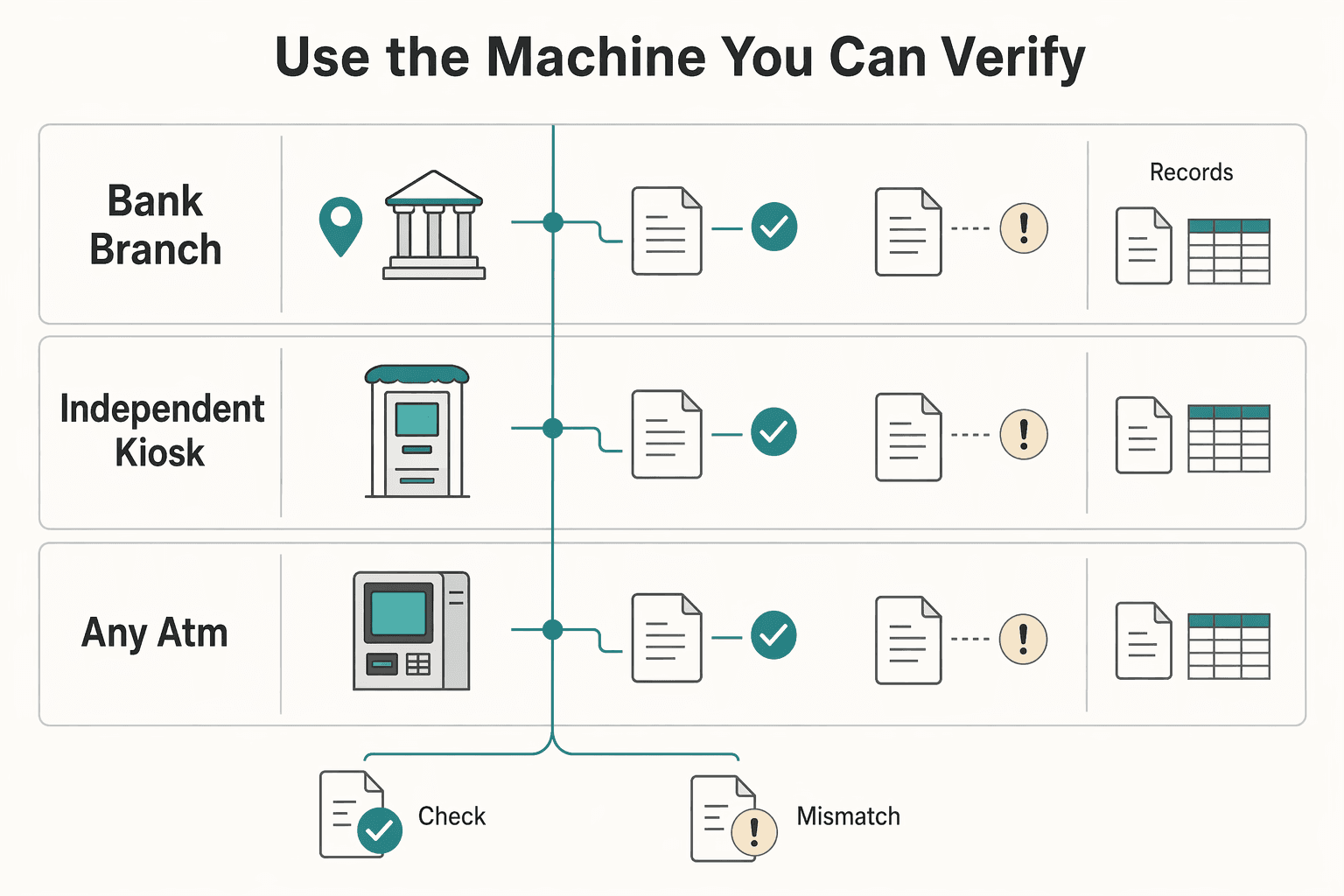

1. Use the machine you can verify, not just the closest one#

Convenience is not the right filter here. Nothing in the evidence provided establishes that bank-branch ATMs are inherently safer or better documented than independent ATMs. Decide based on what you can confirm on the actual screen and device: operator identity, surcharge disclosure before approval, and whether you can get a receipt or transaction reference.

| ATM option | Receipt trail | Fee transparency | Fraud exposure handling | Decision |

|---|---|---|---|---|

| Bank-branch ATM | Verify what the machine actually provides | Verify on-screen disclosure before confirming | Do not assume safer by default; verify operator and transaction details | Use if operator, fees, and receipt or reference are clear |

| Independent or kiosk ATM | Verify what the machine actually provides | Use only when disclosure is explicit before approval | Do not assume higher or lower risk by type alone | Use only if operator, fees, and receipt or reference are all clear |

| Any ATM without clear operator or receipt or reference path | Weak starting record | Weak pre-authorization clarity | Harder to investigate later | Skip |

If a receipt does not print, capture whatever details are available immediately, for example ATM ID, operator name, location, and any visible transaction reference, as an internal recordkeeping step.

2. At the conversion prompt, keep it in local currency for cleaner records#

When the terminal asks whether to process in your home currency or local currency, choosing local currency can make reconciliation cleaner by keeping your records tied to the local amount at the point of withdrawal or payment.

Apply the same approach at checkout terminals that offer on-screen conversion. This does not establish that the choice always lowers total cost, and it does not provide a single required decision flow for every prompt, so treat it as a records-first control unless your issuer terms confirm pricing outcomes.

3. Run a same-day scan-and-tag workflow#

The fastest way to lose control of cash spending is to wait until the end of the trip. Right after each withdrawal or cash handoff, capture the record and tag it before the day ends.

| Log field | What to capture |

|---|---|

| Purpose | what the cash was for |

| Client/project | if tied to an engagement |

| Location | city plus merchant, venue, or branch |

| Payer/payee | who withdrew and who received cash |

The excerpts here do not prescribe a required metadata schema. The fields above work well as an internal log.

For example: Cash withdrawal, Project Delta, Lisbon airport ATM, payer Ops card xxxx, purpose taxi and cash-only meals.

4. Keep a minimum evidence bundle for contractor cash payments#

Cash payments to contractors can require more than proof that you withdrew money. As an internal control, keep one file with the service scope or agreement, the withdrawal record that shows the source of funds, and a payment acknowledgment from the payee.

| Record | Detail |

|---|---|

| Service scope or agreement | keep one file with the service scope or agreement |

| Withdrawal record | shows the source of funds |

| Payment acknowledgment | from the payee |

| Contemporaneous internal note | if documentation is unavailable, record what was paid, to whom, where, who witnessed it, and why the primary document is missing |

This is not a universal legal bundle or a mandated fallback standard when receipts or signatures are missing. If documentation is unavailable, record a contemporaneous internal note with what was paid, to whom, where, who witnessed it, and why the primary document is missing.

Some government disbursing frameworks do not apply here. 4 FAM 360 is for U.S. disbursing officers, and TFM Chapter 3000 applies to certain federal entities using Fiscal Service disbursing functions. Related: The Best Debit Cards for International Travel.

Phase 3: How to Reconcile and Report Foreign Cash with Zero Anxiety#

The closeout process should be short and repeatable: match, attach, label, flag. That is what turns a stack of withdrawals and receipts into books you can trust.

- Match the bank debit

Find the exact debit for each withdrawal or cash-funded spend in your bank feed or statement. Confirm that the date, reference, and amount sequence align with your receipt trail. In this workflow, book the amount you use in your records, and keep the local-currency amount in the memo or attachment for traceability.

- Attach documentary evidence

Before marking the item complete, attach the receipt, paid bill, acknowledgment, or fallback note. Your support should clearly show payee, amount, proof of payment, date, and business purpose. Electronic records are fine if they meet the same standard as paper and stay linked to the booked entry.

- Confirm the purpose tag

Use labels that describe the business event instead of generic placeholders. Better labels make reporting clearer and deductions easier to defend.

| Too generic | Audit-ready label | Why the better label wins |

|---|---|---|

| Cash withdrawal | Cash withdrawal for Project Delta local expenses | Connects source of funds to a specific business use |

| Travel money | Business travel ground transport in Lisbon | Separates deductible travel costs from mixed personal cash |

| Misc. expense | Contractor payment to J. Silva for translation services | Ties cash to a named payee and service |

| Supplies | Project Alpha local materials purchase | Shows what was bought and why it belonged to the business |

- Flag exceptions immediately

Missing or mismatched support rarely gets easier to fix later. Add a same-day fallback note with payee, amount, date, location, proof-of-payment path, business purpose, and why standard documentation is unavailable. This matters because documentary evidence is generally required for lodging. It is also generally required for many other expenditures of $75 or more, with limited exceptions, including certain transportation situations when documentation is not readily available.

For U.S. reporting, keep your base-currency treatment consistent. Amounts reported on a U.S. tax return must be in U.S. dollars, and IRS guidance ties translation to the rate when an item is received, paid, or accrued. In practice, that means keeping both sides of the event in your records: the local-currency context and the U.S.-dollar amount you book.

If a receipt and bank amount do not align, or a payee acknowledgment is missing, leave the item open and attach fallback evidence. Then route it through your documented exception process. A bank debit or canceled check by itself may not establish business purpose.

Finish with an annual reporting check. If your foreign financial accounts exceeded an aggregate $10,000 at any point in the year, add FBAR to your calendar. FBAR is due April 15 with an automatic extension to October 15, and it applies to foreign financial accounts, not physical cash. Keep supporting records at least the general IRS baseline of 3 years, and longer when your facts require it.

If you want a deeper dive, read Separating Business and Personal Finances: An Important Step for LLCs.

Before you lock this workflow, run your own fee scenarios with the payment fee comparison tool. That way, your withdrawal and conversion choices are based on real totals, not assumptions.

From Anxious Tourist to Confident CEO: Your Cash Is Now a Managed Asset#

The advantage here comes from repetition. Run Prepare, Disburse, Reconcile on every trip, not just once. When you treat cash as an operating loop, your records stay cleaner, bookkeeping gets simpler, and closeout feels less stressful.

Use the loop the way you use a pre-departure checklist. Review it before you leave, keep it handy while you travel, and run it again after the trip instead of relying on memory.

| Reactive traveler habit | Managed-asset habit |

|---|---|

| Handles cash with no plan | Plans cash handling before the trip and ties each withdrawal to a clear purpose |

| Waits to track transactions until later | Records each transaction while details are still fresh |

| Tries to remember expenses at closeout | Keeps running notes during the trip, then confirms them at closeout |

| Treats each trip as a new scramble | Repeats the same checklist and review steps each time |

Prepare#

Before departure, review your checklist and decide how you will handle money during the trip. That upfront planning can reduce confusion later.

Disburse#

During the trip, focus on execution and timely record capture at the point of payment so details stay clear.

Reconcile#

After spending, review account activity against your cash use so the trip closes with complete records. Keep this checklist as your default process and run the same loop on the next trip.

For a step-by-step walkthrough, see How to Get Paid in Multiple Currencies Without Losing Your Shirt.

If you want this same control from cash handling through client collections, review Gruv for freelancers to see whether the workflow fits your setup.

Frequently Asked Questions

What is the cleanest way to get local currency for business spending when you arrive?

A practical approach is to use your debit card at an ATM and choose the local-currency option if prompted. If you track business spending internally, save the withdrawal receipt and note what the cash was for. That can make reconciliation easier later.

Should you use your home bank before departure, or wait and use a local bank ATM?

Use a simple rule: get a small landing amount before departure, then compare ATM fees and rates for additional cash after arrival. That gives you a buffer on day one while keeping later withdrawals visible in your account history. | Option | Fees and rate risk | Traceability and reconciliation | | --- | --- | --- | | Home-bank exchange before departure | Banks may beat airport rates by 5 percent or more, and some waive service fees for account holders | Good for planned, pre-trip cash | | Local bank ATM after arrival | Card-network and ATM fees can vary, so check your account terms | Withdrawal records appear in your bank history | | Airport exchange kiosk | “No fee” can still hide a bad rate; travelers can lose 10 percent or more | Weak value for routine withdrawals |

What should you do when a terminal asks whether you want to pay in dollars or local currency?

Choose local currency. Dynamic currency conversion can add about 3 or 4 percent, so the dollar quote is often the more expensive path. Before confirming, decline options like “with conversion” or “charge in USD.” For a deeper walkthrough, see How to Avoid 'Dynamic Currency Conversion' Scams.

Do foreign cash withdrawals count toward your reporting threshold?

Reporting rules vary by jurisdiction and filing type, so verify the current reporting threshold from official tax, finance, bank, advisor, provider, or source records before filing.

What is the safest way to pay an overseas contractor in cash?

Compliance requirements vary, so verify local rules before relying on any single process. For internal controls, keep consistent records of who was paid, when, how much, and the business purpose, and link those notes to the related withdrawal.

What if the ATM gives no receipt or a small cash expense has no usable paper trail?

If standard proof is missing, create an internal note the same day with key details (date, amount, location, payee, business purpose, and what is missing). Same-day notes can be easier to reconcile than unexplained debits reconstructed later.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/part-2trusted

- comptroller.war.gov/Portals/45/documents/fmr/Volume_05.pdftrusted

- consumerfinance.gov/ask-cfpb/how-do-i-avoid-atm-fees-en-981trusted

- ecb.europa.eu/press/blog/html/index.mt.htmltrusted

- ecfr.gov/current/title-26/chapter-I/subchapter-A/part...trusted

- ecfr.gov/current/title-12/chapter-X/part-1005trusted

- fam.state.gov/fam/04fam/04fam0360.htmltrusted

- fdic.gov/consumer-resource-center/2024-04/travel-tips...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How LLC Owners Separate Business and Personal Finances

For an LLC, separating business and personal money is best treated as a weekly habit, not a one-time bank setup. It keeps records cleaner, cuts month-end cleanup, and creates clearer boundaries as the company grows.

The Best Debit Cards for International Travel

If reliable cash access is the priority, do not evaluate this like a perks list. Treat it like continuity planning. Give one card the everyday ATM job, fund a second card for disruptions, and decide that split before you leave.

Using a Charles Schwab Debit Card Abroad for ATM Cash Access

If you're considering the **charles schwab debit card international** setup as your main travel cash tool, start with what Schwab explicitly confirms, then check the details that can still disrupt cash access abroad.