Quick Answer

Start with classification, then RFC and invoice readiness, then ISR sign-off, then SPEI release. Under Mexico's labor-law standard, the working facts matter more than the contractor label, so pause files that already look subordinate or payroll-like. Before the first payout, confirm the contractor's RFC, your CFDI path, the approved ISR position, and a payee record that matches the SPEI instructions. Keep one dated evidence file tying approvals, exceptions, and payment results together.

What to Set Up Before Paying Contractors in Mexico#

For operators, when you are hiring contractors in Mexico, the problem is mainly sequence, not sourcing. Classification comes first, then RFC and invoice readiness, then ISR ownership, then payout execution. When you let that order slip, a file can look clean on paper and still fail under review.

According to Mexico's Federal Labor Law, Article 20 turns on personal subordinate work for salary, and Article 21 presumes the relationship exists between the person who performs the work and the one who receives it. That is why classification belongs before contract signature, invoice setup, or payout batching.

According to SAT's RFC service for people, the RFC is the taxpayer identifier and the person-level workflow starts with registration and status maintenance. If the contractor's tax identity is still incomplete, do not let finance treat the file as payment-ready.

The first practical failure mode is employee-like treatment inside a contractor file. Fixed schedules, day-to-day supervision, or company-controlled tools are not an automatic verdict on their own, but they are strong internal signals that the working facts need another review before the contractor lane keeps moving.

If you cannot defend the classification, do not let tax or payments compensate for it.

To keep control across teams, use explicit checkpoints in order so each handoff is reviewable before the next team acts:

- Classification decision recorded before contract signature

- Documented handoff into tax and payment setup with clear ownership

- Payout release gate before funds move

Keep a traceable approval record from day one. At minimum, record who reviewed classification, which facts supported the decision, and when it was made. Store the agreement, rationale, and payout approvals together so the file can stand on its own later.

Build the file so legal, tax, finance, and ops can each see what was approved before they act. That discipline matters more than speed on the first payment, and it stays useful when you later compare your Mexico controls with a broader Latin America contractor rails view.

Key terms you must align on before onboarding#

Alignment on terms is the first real control. If legal, tax, finance, and ops use different meanings, you can approve files that look clean but still carry real risk.

Start with status terms and classify the worker first. Treat independent contractor as a working classification that must match how the work is actually performed, not just contract wording. The practical check is simple: can you show the person works independently, uses their own tools, and manages their own time? If that evidence is thin, the label is doing too much work.

According to SAT's guidance on Servicios Profesionales (honorarios), people who earn income independently by providing services to companies or individuals belong in a professional-services lane. That does not decide labor classification by itself, but it does tell tax and finance not to blur an independent-services file with payroll language or salary assumptions.

Keep misclassification risk on its own review track. Fixed schedules, manager reporting lines, or company-controlled tools are reasons to reopen the legal review, not reasons to stuff more warnings into the contract and keep going.

Also separate tax and payout work early. A signed agreement does not confirm the RFC, CFDI, ISR, or bank-data work is complete. If those meanings are not stable before volume ramps, resolve them first and only then assign owners to each gate.

Assign clear ownership across legal tax finance and ops#

Assign ownership by gate before payouts start. In Mexico, misclassification risk is high, and worker status is reviewed against multiple criteria, including subordination. Each decision needs a clear owner, not a last-touch handoff.

According to SAT's Régimen de Actividades Empresariales y Servicios Profesionales page, the public workflow is not just "pay": it runs through registration, identification, invoicing, filing, and updates. That is a useful operating model for owner mapping even when your internal workflow uses different names.

| Gate | Primary owner | Core question | Stop trigger |

|---|---|---|---|

| Classification review | Legal | Do the working facts still support an independent service model? | Facts now look directed, subordinate, or payroll-like |

| Documentation review | Legal or finance | Is the rationale, agreement, and version history complete enough to defend later? | Missing, conflicting, or unapproved records |

| RFC and invoice readiness | Tax or finance | Is the payee profile aligned with the RFC record and invoice path? | Unknown tax identity, unresolved invoice path, or mismatched records |

| Payout release | Ops | Did all prior gates clear with no open exception? | Any unresolved hold, mismatch, or unsigned decision |

Name the exception approver before you need one. Set the rule in advance for files where contract wording and working facts conflict. Those cases should route to a named approver with authority to block the contractor lane. If classification and local compliance posture are both unclear, require joint legal and tax sign-off before ops can release payment.

Give one escalation owner stop-payment authority. Designate one escalation owner who can halt payout release when required classification or compliance checks are incomplete. This is an internal control choice, but it prevents late overrides after ops has already queued payment.

Keep a decision log that survives turnover. Keep a traceable log with the date, owner, issue, evidence reviewed, and outcome for each decision. At minimum, retain the classification rationale, signed agreement, relevant compliance approvals, and the hold or release decision. Reviews and disputes should not depend on memory.

Run a classification gate before contract signature#

Classification should be a formal pre-signature control based on documented working facts. If the facts and the draft contract do not match, pause onboarding before anyone signs.

Screen the working setup before labeling the engagement#

Use a short decision table as an internal screening prompt. It helps you spot risk early, but it is not a legal conclusion by itself.

| Working factor | Lower-risk internal signal | Higher-risk internal signal | Action if mixed or higher-risk |

|---|---|---|---|

| Supervision | Review against deliverables and acceptance terms | Ongoing day-to-day instruction | Escalate before signature |

| Schedule control | Person manages hours around deadlines | Fixed hours or attendance expectations | Recheck engagement fit |

| Exclusivity | Free to serve other clients | Continuous availability to one company | Treat as a classification warning |

| Tools and access | Uses own tools and setup | Depends on company-controlled tools or access | Document rationale or stop |

| Commercial setup | Paid for defined services or milestones | Paid mainly for time under close direction | Re-evaluate the lane |

Look for the pattern, not a single row. If the overall setup points to tightly directed work, treat it as a stop-and-review case instead of relying on contract wording alone.

Add a hard stop for employee-like structures#

Set a simple internal rule: if the structure is employee-like in practice, stop the contractor lane and evaluate a different engagement model with legal and tax review. This is a risk-control rule, not a claim about a legal mandate.

Make the gate formal enough to enforce#

The gate only works if people cannot bypass it under deadline pressure. Treat approval like a formal submission process, with a complete written packet, an authorized reviewer, and a dated decision record.

- Require a complete written packet before a defined pre-signature cutoff

- Route questions in writing through the authorized reviewer

- Do not treat late or fax/email/off-channel submissions as approved

- Require a named approver and a dated decision record

At minimum, keep the role scope, who directs the work, schedule or availability assumptions, exclusivity and tool dependencies, the draft agreement version reviewed, and the final rationale. If facts change later, open a new review with a new dated note instead of editing history.

If you need a cleaner starting point for deliverables and acceptance language, use the freelance contract generator before local counsel reviews the draft.

Write contract controls that support the intended relationship#

Once classification is approved, the contract needs to match the operating model. This is a service relationship defined by outputs, not day-to-day direction. If the agreement or the real workflow starts to look like supervised ongoing labor, misclassification risk rises even if the document uses contractor labels.

Write for outputs, not ongoing direction#

Use a signed service agreement with role-specific scope, deliverables, and acceptance terms. Keep control centered on what must be delivered and how completion is accepted, not on attendance, fixed daily hours, or open-ended availability.

Avoid language that implies direct supervision, such as routine daily instruction, company-hour requirements, or manager-style reporting lines. The practical test is whether the person is working independently with control over schedule and tools. Supervision or control can support an employment characterization regardless of label.

If your legal basis is a service model, keep the contract consistent with that basis in plain terms. Define the services, define acceptance, and define change control.

Put invoicing and tax identity into the payment gate#

Payment controls should be explicit. Release payment only after invoice submission and complete tax identity data, including RFC. Do not treat invoice compliance as post-payment cleanup.

According to SAT's factura electrónica service, invoice issuance is a real workflow with XML output, not an after-the-fact memo. If your process depends on CFDI 4.0, make that a hard release gate.

Finance should verify that the payee profile, signed agreement, and invoice record point to the same RFC before the invoice enters payables. When those records do not line up, stop the file and correct the source record before money moves.

Add a reclassification switch, not just a warning#

Contract language helps, but it does not control status on its own because status depends on how work is actually performed. Add a reclassification contingency that triggers when facts shift toward supervision, fixed-hour control, or company-tool dependency.

When that trigger hits, pause new scope under the current contractor lane. Route the case to legal, tax, and finance, then run a documented reassessment before continuing. Keep the decision file complete with the signed agreement, scope and acceptance records, invoice record, RFC check, and any dated status-change decision.

If you want to dry-run the commercial fields before go-live, test them in the free invoice generator and compare them to your Mexico lane requirements.

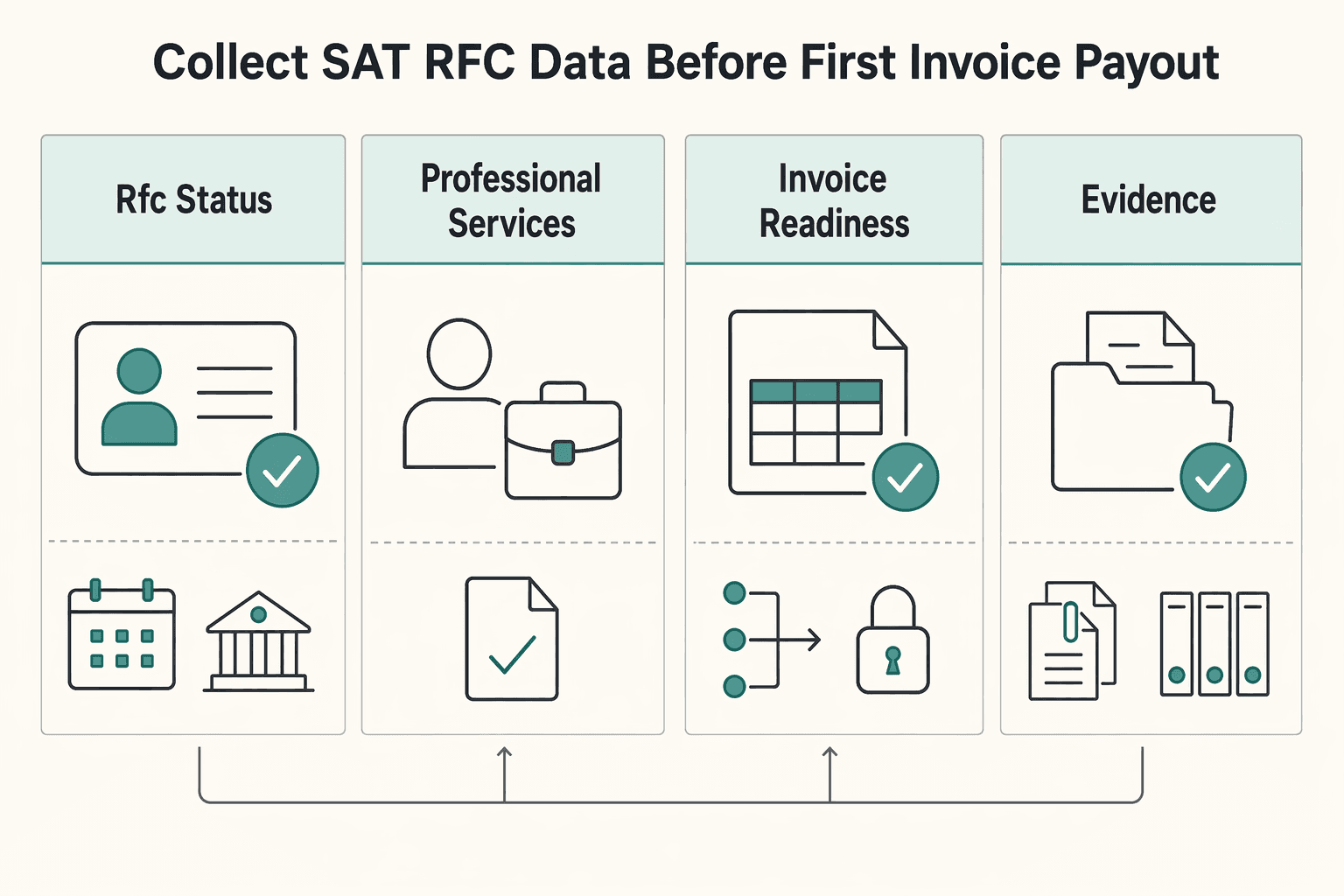

Collect SAT and RFC data before first invoice or payout#

According to SAT's professional-services registration guidance, the RFC identifies the taxpayer and an online start must be concluded at an SAT office within ten days if you use the pre-registration route. That makes RFC completion a pre-payout issue, not an afterthought.

According to SAT's professional-services guidance, a person who earns income independently by providing services to companies or individuals belongs in the services-professionals lane. Use that as a tax-ops signal: match the payee profile, the stated activity, and your invoice path before finance releases the first payment.

Define the minimum record before onboarding opens. Do not rely on a collect-it-later process. Legal, tax, and finance should set one internal standard and apply it consistently. At minimum, the agreement record, payee profile, invoice path, and RFC-related data should be consistent enough to review before money moves.

A simple checkpoint can look like this:

| Control point | Internal pass condition | Evidence to retain |

|---|---|---|

| RFC status | Tax identity is present and reviewed under your policy | Dated record and reviewer |

| Professional-services profile | The stated activity matches the file's service model | Profile snapshot and exception notes |

| Invoice readiness | Contractor can follow your configured CFDI path before payout | Readiness decision and owner sign-off |

| Record consistency | Agreement, payee profile, and invoice identity data align under your checks | Validation result and change log |

If one checkpoint fails, keep the contractor out of the payout batch until it is resolved.

A release-ready first payout file should show:

- One active classification decision

- One active ISR decision

- One payee record that matches the invoice and payout instructions

Build a verification checkpoint that can fail cleanly. Use a binary release rule in your own controls: pass or hold. Keep this framed as internal policy, not as a statement of legal mandate.

If a check fails or the source system returns an exception, reopen the file and record the failure reason. An attempted validation is not the same as a completed validation, and no one should hand-mark the file as verified just to clear a queue.

Keep masked records and a usable audit trail. Mask sensitive values in operational views where full data is not needed. At the same time, keep an audit trail that shows what was checked, when, by whom, and with what result.

A generic "verified" status is weak on its own. A dated decision trail with checkpoint outcomes and exception handling is stronger and easier to defend later.

For a broader payments context after the Mexico controls are stable, compare them against the Latin America contractor rails view.

Decide ISR withholding rules with explicit escalation paths#

Treat ISR handling as a documented tax decision, not an ops assumption. Alongside the RFC and invoice checks, require a tax-owned record that states the live ISR position for that contractor, who approved it, and what changes would trigger re-review.

According to SAT's professional-services regime page, the professional-services lane includes registration, identification, invoicing, filing, and updates. That is enough to keep one rule clear: ops should not infer ISR treatment from a contract label alone.

Build a decision table ops can execute#

The official material used here does not provide a one-size-fits-all ISR table for every contractor scenario. Your operating table should route each case either to an approved internal position or to escalation.

| Scenario in your records | ISR handling status | Required evidence before payout | Escalation owner |

|---|---|---|---|

| Facts match a previously approved pattern and nothing material changed | Use the approved ISR position on file | Tax decision record, RFC status, and invoice-readiness status | Tax owner named in policy |

| Facts are incomplete, conflicting, or newly changed | Hold pending review | Exception note, facts summary, and prior decision if any | Designated tax lead or Mexico tax counsel |

| Previously approved contractor now has contract, payee, or workflow changes | Re-review before release | Change log, updated agreement details, and new tax decision status | Tax owner, with legal review when policy requires |

| The file may belong in a payroll or employment lane instead of a contractor lane | Do not release through the contractor ISR path | Classification reassessment and a new operating decision | Legal plus tax |

A row without a named decision source, required evidence, and an escalation owner is not a control.

Make uncertainty a real stop condition. Use a binary release rule in policy: no approved ISR posture, no payout release. Frame this as your internal control, not as a statement of Mexican legal mandate.

Ops should not infer ISR treatment from contract labels, invoice patterns, or pressure to release and fix later. For program-specific uncertainty, escalate to qualified advisers and record the decision path.

Separate policy from execution. Write ownership in plain language, then enforce it in batch review.

- Tax decision status present

- Effective date present

- Approval owner named

- Tax-registration and invoicing-readiness checks passed

- No open exception tied to the contractor

If any item is missing, fail release cleanly and record the reason.

Watch for status drift and contradictory treatment. Contradictions can show up with existing contractors. Make re-review triggers explicit, such as material contract changes, payee-identity changes, new tax-registration records, or invoicing workflow changes.

Store each decision with an effective-from date and a superseded-by reference so only one active ISR position exists at a time. That prevents duplicate profiles from carrying conflicting treatment.

State unknowns clearly. Do not fill gaps with habit. This material does not provide Mexico ISR rates, filing deadlines, penalty amounts, or a SAT-mandated contractor payout checklist.

For non-routine cases, keep an evidence record with the question, facts used, decision owner or adviser, decision date, and re-check trigger. That is stronger than a generic "ISR verified" status and easier to defend during review.

If the tax team cannot explain the live ISR posture in one sentence, the file is not ready for batch release.

Operate SPEI payouts with release gates and failure handling#

According to Banxico Contigo, sending a SPEI transfer requires the payee's CLABE or debit-card number, and each transfer generates a Comprobante Electronico de Pago (CEP). Treat SPEI as a controlled release step, not as a standalone ops task.

Release gates that matter. Use one pre-release check that ties legal, tax, and payment records together for each payable.

| Release control | What to verify | Hold when |

|---|---|---|

| Beneficiary match | Beneficiary name and CLABE point to the approved payee record | Bank data does not match the active payee profile |

| Tax and invoice state | RFC, invoice path, and approved ISR posture are all present | Any tax or invoicing prerequisite is incomplete |

| Instruction completeness | The payment file contains the fields your provider or bank requires for the corridor | Ops still needs to hand-fill missing fields |

| Reconciliation key | One payable maps to one payout reference and can later be tied to a CEP | A resend would create duplicate or unclear references |

Banxico's public material is consumer-facing rather than a provider implementation manual, so keep your Mexico-specific field list aligned with your bank or payout provider. But the operating rule is still simple: do not create a release file until the beneficiary and tax context are complete.

Use a binary rule: no complete beneficiary and tax-context record, no payout file.

Name the failure modes before you see them live. Define exception categories in advance and assign an owner to each one.

- Rejected payout after submission

- Beneficiary details do not match the approved payee record

- Missing required local beneficiary data (including tax IDs where applicable)

- Missing required reporting, tax, or purpose information for the payout corridor

Treat "almost complete" as a stop condition. If the agreement and amount are approved but required beneficiary or regulatory data is missing from the release record, hold the payout. Log the gap and return it to the right domain owner.

For each failed instruction, keep an exception pack with the original payment reference, returned status or rejection message, contractor record version used, and approved correction before any reattempt.

Retry and reconcile without creating duplicates. Retries need to be idempotent. One approved payable should map to one canonical payout reference.

If an instruction is clearly rejected, correct the source record, document the cause, and reattempt with linkage to the failed attempt. If status is unclear, pause automation and reconcile the internal ledger, provider or bank status, and payable record before any resend.

Shortcuts are usually where duplicate payments are born. If status is unclear, pause automation and reconcile the internal ledger, provider or bank status, and payable record before any resend.

Keep CoDi separate unless you designed for it. CoDi and SPEI sit in separate parts of Banxico's public guidance. Do not switch rails just to hide a control gap in the contractor file.

Switching rails does not solve missing beneficiary, tax, or reporting controls. If a payout fails release gates, fix the control gap first.

Related: How to Pay Contractors in Mexico: SPEI CoDi and SAT Compliance for Foreign Platforms.

Keep an evidence pack that survives audits and disputes#

Keep one versioned, append-only evidence pack per contractor so you can show why a payout was approved at that time. The file should let someone reconstruct the decision path from records, not memory: what was reviewed, who approved it, when, and which version was active when funds moved.

Build the file around decisions, not just attachments. Build the pack so each artifact supports a decision record. If your process includes clause review and source checks, store those items with approval context, dates, and source-version metadata.

A practical rule is simple: every record should show what was reviewed, who approved it, when they approved it, and which version was active at release. For interpretation-sensitive decisions, keep more than the final conclusion. Include the owner, date, and any escalation or specialist handoff logged at the time.

| Record type | Minimum fields to retain | Common failure |

|---|---|---|

| Classification memo | Reviewer, decision date, facts reviewed, and why the service model was accepted | The final answer exists, but the reasoning is missing |

| RFC and activity record | RFC evidence, stated activity, review date, and any exception notes | The payee record changes and no one preserves the earlier version |

| Invoice or CFDI record | Invoice path used, issue date, file reference, and owner who matched it to the payee record | The invoice exists, but cannot be tied back to the reviewed contractor file |

| ISR decision log | Decision owner, effective date, treatment summary, and re-review trigger | Multiple teams keep contradictory tax positions alive at once |

| SPEI release and CEP linkage | Approval ID, payout reference, beneficiary version, CEP or bank status, and reconciliation owner | Payment is visible, but linkage to the approved payable is missing |

Record source-version metadata, not only rule names. If a policy or legal interpretation affects approval, log the source and date you relied on. For example, the LFT text in force as of 2026 and SAT's current CFDI 4.0 service pages should not live only in memory.

Also record the source context. If a source is useful but unofficial, log what you checked and do not treat a page capture as self-explaining legal authority. If meaning is unclear, escalate to counsel or tax specialists and record that escalation.

Preserve change history when the working model shifts. Do not replace old records when facts change. Add a dated delta entry that states what changed, who identified it, and whether payouts were paused pending review.

Mexico-specific controls should not live only in chat threads or payment comments. Keep the RFC validation, CFDI artifacts, ISR approvals, and SPEI status linkage together in the same contractor history.

This history is often what protects the process in audits and disputes. Keeping only the latest records can hide why earlier decisions were reasonable on earlier facts.

Use escalation triggers and confirm local variation safely#

Escalation only works if it actually pauses payouts when facts drift. Treat unclear local variation as a stop point before launch.

For classification and invoicing, escalate when working patterns start to look more directed or supervised than your original contractor rationale. Also escalate when records stop passing your current internal checks. Ops should document the change and hand off for legal or tax review rather than make a legal conclusion during payout execution.

For tax, set explicit stop conditions: unclear tax treatment, changed contractor facts, or records that cannot be validated cleanly. Route these cases to the named tax owner and hold the payout decision until that owner responds. Do not infer Mexico-specific trigger rules from general guidance.

Before you expand a Mexico lane or copy it into another program, confirm what varies locally instead of copying assumptions. In a 2026 workflow, do not reuse pre-2021 outsourcing assumptions or pre-2022 CFDI habits in a 2026 file without rechecking the live rule set.

- Verify whether the planned payout rail is available for that market or program

- Verify whether compliance gating differs by entity, product, or recipient type

- Verify whether tax, security, or data-handling assumptions were copied from another country without review

Temporary workarounds need expiry, not just approval. Record the approver, exact constraint, compensating check, expiration date, and reapproval owner. If you cannot name all five, the exception process is not ready.

Execute a 30-day rollout checklist for a Mexico contractor lane#

Use this 30-day checklist as an internal go or no-go sequence, not as proof that your Mexico lane is compliant.

Week 1. Do not proceed until definitions, ownership, and stop authority are settled in writing. Document how your team will assess contractor status based on jurisdiction-specific legal guidance. Assign named approvers and one person who can stop go-live if facts conflict.

Your checkpoint is simple: each owner can state its gate in one sentence, and all gates are recorded in one decision log.

Week 2. Only after Week 1 is closed should you launch onboarding controls for required contractor and tax records. Keep a hard internal rule that the first payout does not move forward when required records are missing or unverified.

Store evidence for each check: validation result, reviewer, and timestamp.

Week 3. Before live volume, test payout routing and exception handling with sample cases that include both straightforward approvals and stop scenarios. This is usually where unclear ownership shows up fastest.

If the team cannot clearly route an exception to a named owner, the lane is not ready.

Week 4. Run a mock audit on one contractor file from intake through payout, then close gaps before scaling. Your evidence pack should show the classification rationale, contract version, required checks, and payout approval trail.

Mexico can be attractive for nearshoring and collaboration, but scale should stay gated by legally compliant hiring and complete records.

You might also find this useful: Platform operator guide for Mexico contractor payouts.

Before scaling volume, map each week's gate to your payout implementation, bank cutoffs, and exception workflow in the Gruv docs.

Conclusion#

The core risk-control issue in hiring contractors in Mexico is sequence: classify first, decide tax and invoicing posture second, execute payment third. If you reverse that order, unresolved legal and tax questions show up after money has already moved.

The first gate is factual classification, not the contract label. Under Mexico's Federal Labor Law, the question is whether the relationship is personal, subordinated work for payment. If work is scheduled or directly supervised, treat it as a non-routine case even if the agreement uses contractor wording.

Your strongest early control is a written classification rationale tied to real working facts. Labels alone are weak support, and an employment relationship can be presumed from facts even without a written employment agreement.

After classification, move to tax and invoicing with the same discipline. RFC, CFDI, and ISR ownership still need named decisions even when the contractor model looks right. If tax treatment or invoice support is unclear, stop the file before payout.

Keep the operating model simple and strict with three release gates:

- Legal confirms current facts do not show subordination under Mexico's Federal Labor Law.

- Tax or compliance confirms the RFC, invoice path, and approved ISR posture are complete under your policy and local advice.

- Finance or payments releases payout only after the first two approvals are recorded and no escalation is open.

Watch for drift. Scope can start independent and later become scheduled or supervised. Reopen classification as soon as facts change, and do not use foreign regulations, blog titles, or table-of-contents text as substitutes for Mexico-specific legal authority. Clear ownership, hard stop points, and audit-ready records prevent most costly surprises.

If you want a market-specific readiness review for hiring contractors in Mexico, tax, and payout controls, talk with Gruv.

Frequently Asked Questions

Are independent contractors legal in Mexico?

Mexico allows independent professional services, but the contractor label is not decisive on its own. The core legal check is whether the real relationship looks like subordinated personal work for salary, so teams should review the facts before treating the file as a contractor engagement.

What triggers reclassification from contractor to employee under Mexican rules?

There is no single official trigger list in the sources used here. Re-review the file when the work starts looking subordinate in practice, when schedule or supervision tightens, or when the contractor record no longer matches the way the work is being managed.

What are the immediate consequences of employee misclassification in Mexico?

The immediate operational consequence is that the file should leave the routine contractor lane. Mexico's labor-law text presumes a work relationship between the person who provides personal work and the one who receives it, so unresolved cases should be paused and reassessed before more money moves.

What is the minimum onboarding documentation before first contractor payout?

The official sources here do not provide a single statutory minimum packet, so treat your file as an internal control standard. In practice, keep the classification memo, service agreement, RFC record, invoice path, approved ISR posture, and payee data complete before first payout.

When should we pause payouts and escalate to local legal or tax counsel?

Pause when the facts shift toward subordination, when RFC or invoice data conflict, or when the tax owner has not approved the ISR treatment on the file. The safest control is a hard stop before release, not a post-payment cleanup.

Which controls should finance and ops check before releasing a SPEI batch?

Check that the payee record matches the beneficiary details, the CLABE or other payment identifier is complete, the RFC and invoice controls passed, the ISR posture is approved, and the payment reference can be reconciled afterward. If any of those checks are incomplete, hold the SPEI release.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- diputados.gob.mx/LeyesBiblio/pdf/LFT.pdftrusted

- sat.gob.mx/portal/public/tramites/inscripcion-y-aviso-a...trusted

- sat.gob.mx/portal/public/tramites/inscripcion-al-rfc-pftrusted

- wwwmat.sat.gob.mx/consulta/36193/inscribete-en-el-rfc-como-per...trusted

- wwwmat.sat.gob.mx/consulta/36192/conoce-el-regimen-de-servicio...trusted

- banxico.org.mx/footer-es/preguntas-frecuentes-dudas-ba.htmlexternal

- banxico.org.mx/sistemas-de-pago/d/%7B89B6CCF0-6070-7389-3DD...external

- contigo.banxico.org.mx/accesos-rapidos.htmlexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: