Quick Answer

For platform operators, spend management is the control system for approving, paying, and reconciling contractor spend. In contractor-heavy programs, it should cover onboarding, invoicing, payout visibility, failure handling, tax and verification gates, and bank-to-transaction matching, not just approvals. That is why total cost of ownership matters more than headline per-contractor pricing.

Why Contractor Spend Needs Total Cost and Payout Controls#

For platform operators, contractor spend is not a simple software seat decision. The real cost shows up in money movement, verification gates, failed or delayed payouts, and the finance time required to reconcile what actually happened against what should have happened. That mismatch often starts with the accounting boundary between accrued expenses and accounts payable for contractor liabilities.

That is why a per-contractor list price is a starting point, not a buying model. You can find a visible headline price such as $29 per contractor/month, and it looks easy to compare. But that number does not tell you whether payout fees apply in your setup, how much manual review your team will absorb, or who owns the work when reconciliation breaks. In some payout configurations, additional fees can apply, and when you control manual payout timing and amounts, you are still responsible for matching those payouts to transaction history.

This guide should leave you with a decision-ready way to estimate total cost of ownership and a concrete launch sequence for a spend management platform that supports contractor operations, not just approval screens. If your vendor review currently ends at subscription pricing, stop there and expand the model before you sign. The wrong comparison usually looks cheap in procurement and expensive in month one of operations. If off-contract purchasing is part of the problem, Maverick Spend on Contractor Payments is the adjacent spend-control read.

Much of the hidden cost shows up during implementation. Teams discover that compliance checks differ by country, business type, and enabled capabilities. They also discover that payout coverage is not universal. Connected-account country availability depends on the location of your platform, and cross-border payouts are conditional rather than guaranteed for every program. That means the first verification checkpoint is not a feature list. It is a country and program matrix tied to your actual operating footprint. For the payout side of that matrix, Cross-Border Payments for Platform Operators is the right companion guide.

You should also treat compliance and tax setup as live operating constraints, not fine print. KYC, KYB, AML, and tax handling all need confirmation for the countries and contractor profiles you support. As a concrete example, U.S. reporting posture may require collecting Form W-9 for some payees, while payments to foreign addresses can raise Form 1042-S questions. A vendor saying "we support onboarding" is not enough if you cannot verify what data is collected, when payouts are blocked, and what records your team can export later.

The tradeoff is straightforward. A lighter tool can get you live faster, but it may leave finance and ops carrying manual exception handling and reconciliation work that never appears in the subscription quote. A more operationally complete setup can take longer to launch, but it reduces the risk that contractor support tickets, payout retries, and close-cycle cleanup become your real cost center.

What spend management means for contractor-heavy platforms#

For contractor-heavy platforms, spend management is necessary but not sufficient. A spend management platform gives you real-time control over approvals, policy, and visibility across company spend. A contractor management platform can go further by handling contractor onboarding, localized contracts, invoicing tools, and global contractor payments in the same operating flow.

That boundary matters because procurement-style SaaS spend management is built around source-to-pay control: sourcing, contracts, purchasing, suppliers, invoices, and payments. That is useful for finance discipline, but it is not the same as running contractor payout operations. If your contractors need onboarding, country-aware contracts, and payment execution, do not assume a procurement tool covers those steps just because it has approval chains and budget controls. That procurement boundary is clearer in Indirect Procurement Platforms for Non-Core Spend.

At minimum, your stack needs four table-stakes capabilities:

- invoicing tools so work turns into payable records cleanly

- expense guidelines so policy is set before money moves

- real-time expense tracking so finance and ops can see status before month end

- named ownership across finance, ops, and engineering

The miss in many vendor comparisons is simple: feature lists describe surfaces, not execution. You need rules for what happens when a payout fails, who retries it, how duplicate requests are prevented, and how the final payout is matched back to the invoice or approval record. In practice, that means verifying two things early: whether the provider exposes explicit payout failure events, and whether your integration uses idempotency so a retry does not create a duplicate operation. The matching side is exactly where straight-through processing for automated payment matching becomes useful.

One more checkpoint: webhook delivery is not a perfect stream. Some providers automatically resend undelivered events for up to three days. If engineering does not design for replay handling and finance does not own reconciliation exceptions, your real cost shows up after go-live, not in the demo. That retry reality is easier to test with webhook-driven payment automation for platforms.

The real contractor cost model you should price before vendor selection#

Price the operating reality before you compare vendors. A published per-contractor fee is useful, but if payment, FX, tax, and reconciliation work cost more than the subscription, you should buy for control quality and integration depth, not for the lowest sticker price.

The last section drew the line between approval software and payout operations. This is where that difference hits your budget. A tool that starts at $49 per contractor per month may still be the expensive option if you absorb high transaction fees, currency conversion cost, repeated payout failures, and manual month-end matching work. If you want the finance-view artifact first, start with Payment Reconciliation Dashboards for Subscription Platforms.

Build the five-bucket cost model first#

Use one model for every vendor, and leave unknowns visible instead of smoothing them away. If setup fees, minimums, custom pricing, or overage terms are not disclosed, put them in the model as TBD rather than assuming zero.

| Cost bucket | What to price | What to verify |

|---|---|---|

| Contractor subscription fees | Base per-contractor charge. Example published datapoint: $49 per contractor per month. | Whether pricing changes by contractor count, country, payment method, or plan tier. |

| Payment or transaction fees | Per-payment processing cost. Example published datapoint: 2.9% + 30¢ per successful transaction for domestic cards. | Which fee applies to your actual payout route, not just a generic payments page. |

| Foreign exchange (FX) cost | Currency conversion cost. Example published datapoint: from 0.57%, with fees varying by currency. | Which currencies, corridors, and payout methods your contractor mix actually uses. |

| Implementation effort | Internal engineering, finance, and ops time to integrate, test, and sign off. | What is included in onboarding versus what your team must build or own. |

| Ongoing ops overhead tied to reconciliation | Monthly effort to match payouts to underlying payment batches and clear exceptions. | Export quality, payout-mode behavior, and who resolves mismatches after go-live. |

Two cautions matter here. List pricing is only one line item. And some providers offer custom packages for large volume or unique business models, which means setup terms, minimums, or nonstandard fees may not be visible on first pass. Treat missing commercial terms as procurement risk, not as savings.

Price the operational drag, not just the invoice#

The second part of the model is where many teams undercount. These are recurring labor costs, not edge cases. They show up in support queues, finance close, and tax season.

- Exception handling

Every payout exception creates touch labor. Someone has to identify the issue, contact the contractor, decide whether to retry, and track whether the payment cleared. If the vendor cannot show clear failure states and audit exports, that cost lands in manual follow-up.

- Failed payout retries

Failed payouts are not only a one-time miss. In some payout setups, the external account cannot receive payouts until the platform updates that connected account's external account details. That means your real question in procurement is not "Do retries exist?" but "What failure codes are exposed, and what blocks future payouts?"

- Tax document collection

U.S. tax collection is operating work. Form W-9 is used to provide the correct TIN, and Form W-8 BEN is submitted by foreign beneficial owners when requested by the withholding agent or payer. If you collect these late, year-end reporting gets slower and exception-heavy. That collection layer is easier to harden with W-9 Collection at Scale: A Compliant Onboarding Flow.

- Reporting output

Form 1099-NEC is used to report nonemployee compensation. Form 1042-S is used to report income and amounts withheld for certain foreign-person payments. If your platform cannot produce clean contractor-level data for those outputs, the cost lands on finance and tax ops.

Here is the decision checkpoint: if your non-subscription buckets are larger than the subscription line, stop optimizing for headline price. At that point, the better buy is the one with stronger reconciliation support, clearer payout failure handling, and cleaner exports.

Evidence to collect in procurement#

Do not sign off on a demo alone. Ask for an evidence pack and review it with finance, ops, and engineering together:

- Sample invoices showing how subscription, transaction, FX, and any other fees appear in billing

- Fee schedules with disclosed rates, plus written confirmation of any custom pricing, minimums, or overage rules

- Payout failure codes and status meanings so your team can design retries and support handling

- Audit and reconciliation export examples that let you match bank payouts back to underlying payment batches

That last item is the checkpoint most teams skip. Reconciliation exists to help you match the payouts you receive in your bank account with the batches of payments underneath them, and payout mode can change that work. If the vendor cannot prove this with real exports, assume your ops cost will be higher than the sales price suggests.

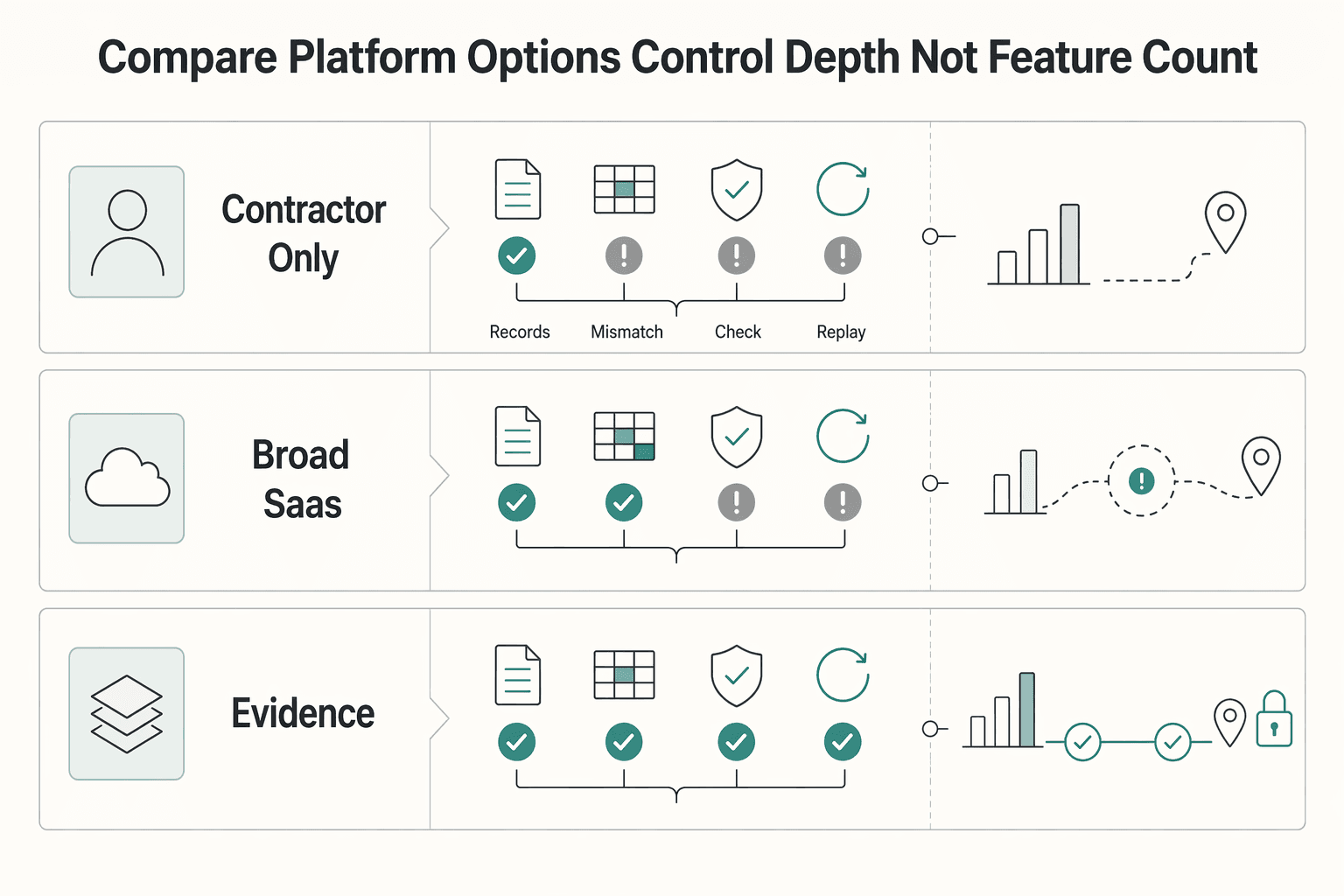

Compare platform options by control depth not by feature count#

Once you have the cost model, the next filter is control depth. For contractor-heavy operations, the better choice is usually the one that can prove reconciliation, failure visibility, and retry safety in your real payout corridors, not the one with the longest feature checklist.

A broad feature grid can hide the actual split between approvals and money movement. Contractor tools, SaaS spend management products, and integrated payout stacks solve different problems, and the gap shows up most clearly in finance close, payout exception handling, and engineering support load.

| Path | What it is good at | Finance outcome | Ops outcome | Engineering outcome | Main tradeoff and what to verify |

|---|---|---|---|---|---|

| Contractor-only tooling | Centralized contractor management with contracts, invoicing, and multi-currency payments. One marketed example highlights payments in 120+ currencies. | Better contractor records than generic expense tools, but you still need to test how far the audit trail runs into payout settlement and month-end matching. | Faster start for onboarding and routine payouts if the vendor owns more of the flow. Exception speed depends on whether payout statuses and failure reasons are exposed clearly. | Lower lift if you adopt the vendor's flow as designed. Still verify webhooks, duplicate-event handling, and export quality before go-live. | Fastest path for many teams, but controls can be thinner once you get into retries, FX, and bank matching. Confirm country and currency coverage for your contractor mix before assuming support. |

| Broad SaaS spend management tooling | Business spend management across sourcing, contracts, invoices, and related company spend controls. | Usually strong on policy, approvals, and purchase-side history. Often weaker when you need contractor payout settlement detail rather than approval records alone. | Good for pre-spend controls and visibility. Less helpful if contractor payments run through a separate provider and exceptions live outside the tool. | Often faster to deploy for approvals and card programs. Integration work grows when contractor payouts require another stack. | Good control surface for purchasing, not a guarantee of payout depth. Verify whether contractor payments are native or stitched in, and do not treat corporate cards as proof of cross-border payout control. |

| Integrated money-movement stack using Virtual Accounts, payout batches, and Merchant of Record (MoR) where supported | Cash visibility from virtual account structures, API-led disbursement, and tighter ownership of payment operations. Payout APIs can support large batch sends, with one example allowing 15,000 payments per call. | Deepest potential reconciliation if you can tie each payout to the batch of transactions it settles. Best option when finance needs traceability from transaction batch to bank movement. | Strongest payout visibility when webhook events and failure codes are available. Better for fast triage and controlled retries. | Highest integration effort, but best control over idempotency, retries, and webhook consumers that must tolerate duplicate deliveries. | Longer build, fewer downstream surprises if done well. Verify market and program coverage, settlement currencies by country, MoR availability, and whether some payout configurations add extra fees. |

The team lens matters more than the category label. Finance should care most about whether the audit trail reaches settlement and whether a payout can be reconciled back to the underlying transaction batch. Ops should care about observable failure states, exposed failure codes, and whether exceptions can be cleared without opening tickets for every miss. Engineering should care about two unglamorous details that decide reliability: can requests be retried safely with idempotency protection, and can webhook consumers handle duplicate deliveries without creating duplicate payout actions?

Here is the hard rule: if your business depends on cross-border payouts, choose the option that proves reconciliation depth and idempotency handling, not just expense approvals or card controls. A strong corporate cards product does not answer whether finance can reconcile each payout with the transactions it settles, or whether your retry logic will avoid paying the same contractor twice.

The tradeoff is simple. Contractor-only and broad spend tools usually get you live faster, but the controls can stop at approval history or top-level payout status. An integrated stack takes longer to wire up, especially if you are using Virtual Accounts and batch disbursements, but you get better traceability and fewer unpleasant surprises in failed payouts, duplicate events, and month-end close. Where multi-entity balances matter, Multi-Currency Wallet Platform Sub-Wallets for Contractors is a useful architecture reference.

Before you decide, ask each vendor for the same evidence pack: a sample payout reconciliation export, webhook payload examples, failure-code documentation, and a market or program coverage matrix. That last check is non-negotiable. Country support, settlement currencies, and MoR treatment vary by market and program, so you should confirm availability before you assume a feature exists in your operating footprint.

Decide your architecture by stage, volume, and risk profile#

Use a risk-based approach here, not a maturity fantasy. If your contractor program is still low volume, mostly domestic, and can tolerate some manual handling, a simpler contractor management platform or a narrower spend management platform can be enough at first. If you are adding countries, currencies, or payout frequency quickly, you should move to stronger compliance gates and payout orchestration earlier, before exceptions pile up.

The control-depth choice from the last section only works if it matches the shape of your program. Early-stage teams can often start with basic invoicing tools, clear expense guidelines, and a visible approval path, then add deeper payout controls once failure handling becomes a weekly issue instead of a rare one. High-growth teams should not wait for a magic payment count. Cross-border payments bring known friction around cost, speed, transparency, and access, so the design pressure arrives before the dashboard looks busy.

Here is the clearest rule: if your contractor mix includes cross-border work and variable foreign exchange (FX) exposure, prioritize FX controls, global contractor payments, and policy gating over cosmetic reporting. A polished reporting layer will not help when finance cannot explain rate movement, ops cannot see why a payout failed, or engineering cannot retry safely without risking duplicates. In that case, verify two things before go-live: whether payout release can be blocked when required tax or onboarding data is missing, and whether failed payout states come with usable reason codes rather than a generic error.

Risk is easier to judge if you score your program on three dimensions. First, payout criticality: if missed or late payouts would disrupt supply, treat reliability and retry safety as first-order requirements. Second, tax complexity: mixed U.S. and foreign contractor populations mean you need a clean record path for Form W-9, Form W-8 BEN, and potentially Form 1042-S related reporting. Third, tolerance for manual exception handling: if your team can absorb occasional manual fixes, you can defer some automation; if not, thin controls will turn into month-end reconciliation pain fast.

| Control area | Do now | Defer until later |

|---|---|---|

| Policy and approval | Set expense guidelines, payout approval rules, and release gates for missing contractor data | Granular reporting views by team or region |

| Payout operations | Define payout states, failure handling, and who clears exceptions within an SLA | Advanced routing or corridor-specific optimization |

| Tax and records | Collect and retain the core contractor tax data your reporting posture depends on, including W-9 or W-8 BEN where applicable | Edge-case reporting automation if volume is still small |

| Integration quality | Require idempotent request handling and test duplicate webhook delivery before launch | Nice-to-have dashboards that do not change control quality |

Ownership should stay explicit. Finance owns policy, reporting, and the evidence pack needed for close. Ops owns exception SLAs, queue review, and escalation when payouts stall. Engineering owns the integration surface, including retries, webhook handling, and the audit trail between request, payout status, and settlement. If one area has shared ownership, name a final decision-maker anyway. That is usually where hidden contractor cost starts.

Roll out in seven checkpoints across finance, ops, and engineering#

Rollout should be staged, not feature-complete on day one. If you do the sequence out of order, you usually learn about weak controls during first-month reconciliation, when fixes are slower, riskier, and more expensive.

-

Lock policy before code. Finance should publish expense guidelines, approval rules, and the exact release gates for missing contractor data. This is where you decide what can be paid automatically, what must be held, and who can clear exceptions. If a payout is allowed to bypass missing tax or verification data here, engineering will later encode the wrong behavior perfectly.

-

Design retries and event handling next. Engineering needs explicit idempotency for payout-creation requests so timeouts and retries do not create duplicate side effects. Pair that with webhook handling that expects delayed and repeated deliveries, because live-mode event delivery can be retried for up to three days with exponential backoff. A good checkpoint is to test duplicate webhook delivery and confirm your state machine stays correct.

-

Define the operating artifacts before the pilot. Require four documents, not just a demo:

- a payout state map from request to settlement or failure - a failure-code matrix with owner and next action for each code - an audit trail export sample that links request, approval, payout status, and settlement reference - a monthly reconciliation pack format showing how finance will match the general ledger against bank and related subledgers, then work exceptions

-

Put compliance gates in the live payout path. Verification checks such as KYC, KYB, and AML need to happen before payout release, not after a failed transfer. In some connected-account models, payout capabilities can be disabled until the required information is provided, so you want that state visible to ops before a payment date is missed.

-

Collect tax profiles early enough to matter. W-8 and W-9 collection should be complete before year-end reporting pressure starts. For U.S. nonemployee reporting, Form 1099-NEC is due on or before January 31, so waiting until January to chase documentation is asking for manual cleanup.

-

Run a pilot with written success criteria. Agree in advance on payout success rate, exception aging, ledger-to-bank match rate, and turnaround time for holds and retries. Do not make these hallway metrics. Put owners on each one, and review them from actual pilot data, not vendor screenshots.

-

Only then expand by cohort. Reconciliation sign-off should happen before broader rollout. The real test is whether finance can clear the month with the evidence pack provided, ops can work exception queues without guesswork, and engineering can retry safely without duplicate payouts.

One red flag deserves special attention: if your audit trail sample cannot show a clean chain from approval to settlement, stop there. A platform that pays contractors but cannot explain why a payout failed, retried, or settled will create hidden spend long before anyone blames the tool.

Build compliance and tax controls into day-one operations#

Treat compliance and tax as release criteria, not cleanup work after launch. If your team cannot pull auditable payout and tax records quickly for a sample contractor, pause expansion and harden those flows first, because scale only multiplies missing evidence.

Country coverage and program rules do vary, sometimes materially. The safest way to confirm scope is not to ask a vendor whether they "support global payouts," but to verify your exact footprint: country, payee type, regulated entity, and payout product. For U.S.-linked programs, identity controls often map to Customer Identification Program requirements, which call for risk-based identity verification, and business onboarding may also require beneficial ownership verification for legal entities. Do not promise internal stakeholders that KYC, KYB, and AML checks behave the same in every market or account model.

In practice, your payout gate should block release until the payee record is complete enough for your program's compliance posture. That usually means the contractor or supplier profile, verification status, and tax form status all resolve before money moves. A strong checkpoint is simple: pick five live or pilot payees and confirm you can show who was verified, what information was missing, who approved an exception, and whether the payout was held or released. A common failure mode is letting ops override a missing document for "just this one urgent payment," then discovering later that reporting and reconciliation no longer line up cleanly. If you need one upstream flow for that record, Supplier Onboarding Automation for W-9, Bank, and KYC in One Flow is directly relevant.

For U.S. tax handling, separate domestic and foreign-person paths early. IRS guidance for U.S. independent contractors treats Form W-9 as the first step, and the W-9 should be kept in your files for four years. If required taxpayer identification details are not furnished, backup withholding can apply at 24%, so missing tax data is not just an admin problem. For U.S. nonemployee compensation, reporting ties to Form 1099-NEC.

Foreign-person payments need their own branch. Collect the appropriate W-8 before payment logic is finalized, and do not assume no withholding means no reporting. IRS guidance is explicit that amounts can still be reportable on IRS Form 1042-S even when withholding is not required, including cases where a treaty or code exception results in zero withholding. If your team handles foreign contractor payouts, this is worth a deeper read in IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments. A deeper walk-through lives in IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

Keep an evidence pack ready on demand:

- payee verification status with KYC, KYB, or AML hold history

- stored W-9 or W-8 linked to the payee and payout record

- 1099 or 1042-S reporting logic for that payee class

- approval and settlement records tied to the same payment

Finally, governance does not stop at tax forms. If your U.S. reporting posture includes foreign financial accounts, track potential FBAR exposure separately. FBAR is filed on FinCEN Form 114, not with the federal income tax return, and the trigger uses an aggregate foreign-account value test over $10,000 at any time during the calendar year. The annual due date is April 15, with an automatic extension to October 15. That is why compliance quality is an operating capability: AML rules themselves require internal controls for ongoing compliance, not a one-time setup you check off during implementation.

Red flags that signal hidden contractor spend before it hurts margin#

Once compliance gates are in place, hidden cost usually shows up in exceptions, retries, and cleanup work, not in the headline subscription price. If your team is carrying unresolved payout exceptions week to week, or approving repeated manual overrides to push urgent payments through, treat that as an early warning that your contractor cost model is missing real operating expense.

The first red flags are operational: delayed reconciliation, missing audit trail links between the original request and the final settlement, and payout records that cannot show who approved what. Treasury controls depend on detailed documentation, clear audit trails, and proper approvals for transactions. A practical check is to pull a sample of recent contractor payouts and confirm each one has a linked request ID, approval record, payout status history, and settlement reference. If any step lives only in email or chat, finance will end up reconstructing the story by hand.

Integration issues are where margin damage often compounds. Weak idempotency means a retry can accidentally create the same operation twice instead of safely retrying it once. Brittle webhooks create a second failure mode because failed deliveries are retried, and already processed events need to be ignored explicitly. You also want a clean payout state map with statuses such as processing, posted, failed, returned, or canceled. If those transitions are unclear, a returned payout can look settled long enough to trigger duplicate reissues. Returned payouts are often caused by incorrect destination information, and they are typically returned within 2 to 3 business days, so stale payee data is a real cost signal. Before rollout, validate that path with Payment Sandbox Testing for Cards, Webhooks, and Failure Modes.

Use this cost of failure checklist when judging the damage:

- finance rework time to investigate return reasons and reconcile the ledger

- contractor support load from payment status confusion and reissue requests

- FX leakage when cross-border payouts must be retried or re-sent later

- delayed close cycles when open exceptions keep reconciliation unfinished

If manual exception handling is rising, do not just add headcount. Fix the evidence chain, event deduplication, and payout-status handling first.

Conclusion#

The buying decision should come down to operating control and verified total cost of ownership, not the neatness of a subscription line item. TCO is the full lifecycle view, including direct and indirect costs, so a contractor tool that looks cheap on paper can still be expensive once payout exceptions, failed retries, and reconciliation work start landing on finance, ops, and engineering.

That is why the next move is not another vendor demo. Build your cost table and your checkpoint list side by side. Put subscription fees, payment charges, and internal handling effort in the same model, then pair that with the controls you need before money moves: onboarding, identity verification, payout release, payout matching, and exception recovery. If your indirect costs look likely to rival or exceed the visible software fee, treat control quality as the main buying variable.

Do not roll this out to your full contractor base first. Pressure test one pilot cohort before go-live, and make the pilot broad enough to expose the real edges: account creation, identity verification, payout initiation, payout settlement, and reporting back to your team. A useful checkpoint is simple: can the vendor show that a payout hitting your bank account can be matched back to the underlying transaction batch, not just to a dashboard status? If they cannot demonstrate that clearly, reconciliation risk is still yours.

The other proof point is failure behavior. You should ask the vendor to show what happens when a webhook is delivered more than once, because that can happen, and what happens when a payout request is retried. The answer you want is not "we handle it somehow." You want a concrete demonstration of duplicate event tolerance and idempotent retry safety so the same action is not performed twice by accident.

A practical buyer stance is to stay skeptical until the product proves itself in your actual contractor flow. Ask vendors to walk through your real scenarios, including a held verification case, a failed payout, a retry, and the final reconciliation output. If they only show approval screens and happy-path payout screens, you still do not know enough.

So the decision rule is straightforward: pick the platform that can prove lifecycle cost, payout-to-transaction matching, and exception safety in a pilot. Headline price can help narrow a list, but it should not decide who runs your contractor operations.

Frequently Asked Questions

Is per-contractor pricing enough to estimate contractor spend management costs?

No. A published starting price such as $49 per contractor per month is only the visible subscription line, not your full cost model. You should add payout charges like 0.25% plus 25 cents per payout and, for cross-border flows, pricing that can start at 0.25% of payout volume, then pressure test the manual work around exceptions and reconciliation.

What costs are usually missing from list pricing for contractor management tools?

The common gaps are payment execution fees, cross-border payout charges, and the internal work needed to clean up failed or duplicated payment events. Tax-document collection also creates real operating cost if the product leaves your team to handle W-9, W-8 BEN, or 1042-S work outside the platform.

Do spend management tools include localized contracts, invoicing tools, and global contractor payments by default?

Not by default. Some contractor-focused products do bundle localized contracts, invoicing tools, and global contractor payments, while procurement-centered suites may stay closer to source-to-contract, procure-to-pay, and supplier management. The practical check is to confirm those features in the exact plan and countries you are buying.

How should platform operators choose between a contractor management platform and broader SaaS spend management tooling?

Choose based on the operating job, not the label. If your main need is procurement control and supplier spend visibility, broader SaaS spend management can fit. If you need contractor onboarding, contract handling, invoicing, and payout execution, a contractor management platform is usually the closer match.

What are the minimum controls needed before scaling cross-border contractor payouts?

Start with country-specific KYC checks, tax-document collection for W-9 and W-8 BEN, 1042-S reporting where applicable, and idempotent payment retry handling. Also assume duplicate webhook delivery will happen and design event processing to ignore already handled events.

What should finance, ops, and engineering each own during implementation?

Assign one named owner for each control before launch. Finance usually owns tax-document policy, reporting, and fee review; ops usually owns contractor communications and payout exception handling; engineering usually owns API retries, idempotent request design, and duplicate webhook protection.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- bis.org/cpmi/cross_border.htmtrusted

- bis.org/cpmi/publ/brief5.htmtrusted

- docs.stripe.com/api/idempotent_requeststrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/forms-pubs/about-form-1042-strusted

- fatf-gafi.org/en/publications/Fatfrecommendations/Risk-bas...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: