Quick Answer

Start by treating straight-through processing stp automated payment matching as an operating model instead of a single feature. Use a six-stage control chain across authorization, processing, matching, exception routing, posting, and reporting, then prove each transaction is traceable from provider reference to ledger outcome. Keep ambiguous or high-impact cases in human review, and align ACH exception timers to settlement windows so routine batch latency is not flagged as a processing failure.

Why Reconciliation Is the Real Test of Straight-Through Processing#

Straight-through processing is strongest when you design it as an end-to-end operating model, not just a matching feature. The practical boundary is simple: STP covers the full transaction path, and automated payment matching is one critical part of that path.

STP means completing transactions with minimal human handling from initiation through completion, including reconciliation-related work. For platform teams, success is not just "payment sent." It is an outcome that is authorized, recorded, matched, posted, and explainable in the ledger. Manual intervention should appear only where policy requires it.

In practice, STP is usually partial, not absolute. Treat it as an STP rate: what share of your flow is reliably automated today. That gives you room for staged rollout, exception routing, and control where data quality or payment-rail behavior is noisy.

Breakdowns often show up in cash application and reconciliation, especially when payment details are inaccurate or incomplete, or when payments are split across channels. That is why stronger automation still needs exception handling. Some items should flow straight through, and some should be flagged for review.

Set the automation boundary early.

- Fully automate deterministic, reversible steps, such as stable matching rules on clean references and status posting when provider and internal records agree

- Keep human review for ambiguous matches, duplicate signals, material reconciliation impact, and timing-sensitive disagreements

Before go-live, test traceability on real transactions from authorization to processor reference, to settlement or bank line, to final ledger result. Also account for ACH timing. Processing runs 23 1/4 hours each business day with four daily settlements. That can create temporary status mismatches that look like failures if your exception logic is too aggressive.

This article gives you a decision-ready path to separate STP from matching, define rules and exception choices, and launch with auditability and cash-application accuracy in focus while reducing manual work where feasible. For a step-by-step walkthrough, see How to Handle Payment Disputes as a Platform Operator.

What STP means for platform payouts in practice#

For platform payouts, STP means the transaction flow runs end to end with minimal human intervention, not just that one step is automated. The standard is a result finance can trust across initiation and validation, posting, payment matching or cash application where relevant, and reconciliation.

A useful test is whether AP and AR can review the same transaction and, with a clear reconciliation design, reach one defensible status and ledger outcome. If the payout looks complete in one system but still needs manual cleanup in receivables or the general ledger, you have partial automation, not true end-to-end processing.

Automated payment matching is a core component, but it is not the whole operating model. It can auto-apply incoming payments to open invoices and clear them. STP still depends on correct posting and reconciliation around the general-ledger boundary, including checks before and after posting.

Use this checkpoint on real transactions.

- Confirm the transaction passed initiation and validation checks

- Confirm the payment match or clearing event

- Confirm the posted ledger result

- Confirm reconciliation around posting is complete

The common risk is a false finish: matched but not posted correctly, posted but not reconciled, or AP and AR resolving the same item with different status logic. Treat that as a design gap, not as full STP. Related: AP Automation vs Manual AP Processing for Marketplace Operators.

STP and automated payment matching are not the same job#

STP and automated payment matching solve different problems. Matching is one control step. STP is end-to-end automation from initiation through completion with minimal manual intervention, and in practice teams often track it as an STP rate rather than an all-or-nothing state.

You can have strong matching and still miss STP if downstream steps break or still require manual handling. That is the practical distinction: a successful match is progress, not proof that the full transaction path is automated.

| Dimension | STP | Automated payment matching |

|---|---|---|

| Scope | End-to-end transaction flow | One stage that links payments, invoices, and supporting records |

| Process span | Multiple downstream steps in the lifecycle | Matching logic and exception handling within the matching stage |

| Input data | Lifecycle events and completion evidence across steps | Invoice references, remittance details, PO data, receipt evidence, and payment details |

| Common failure mode | One stage succeeds but the transaction still fails later in the flow | Unmatched or misapplied items from missing or inaccurate payment details |

| Success metric | Higher STP rate across the lifecycle | Higher correct-match and cash-application outcomes with fewer unresolved exceptions |

What matching actually covers#

Matching also has subtypes, and they behave differently in operations.

| Matching type | Data checked | Key note |

|---|---|---|

| Invoice matching | Invoice and supporting evidence | Associates an invoice with supporting evidence |

| 2-way matching | Purchase order and invoice details within tolerance rules | May be the highest-fidelity control you can automate when only PO and invoice data are reliably available |

| 3-way matching | PO, invoice, and receipt evidence | Adds an extra control check because it requires receipt data |

If your process depends on fulfillment proof, 3-way matching adds an extra control check because it requires receipt data. If only PO and invoice data are reliably available, 2-way matching may be the highest-fidelity control you can automate at that stage.

Which problem to solve first#

Start with the exception source, not a generic automation goal. If unresolved remittances, missing references, or inaccurate payment details create most of the manual work, matching controls and remittance quality are often the first lever. If the bigger problem is cross-step handoffs across the full transaction lifecycle, broader STP design may be the better starting point.

Use a simple verification check on "automated" items. Confirm the evidence fits the chosen method. That may be PO plus invoice for 2-way, PO plus invoice plus receipt for 3-way, or usable remittance and reference data for receivables. A technically successful match can still fail later if a required record is missing, late, or inaccurate.

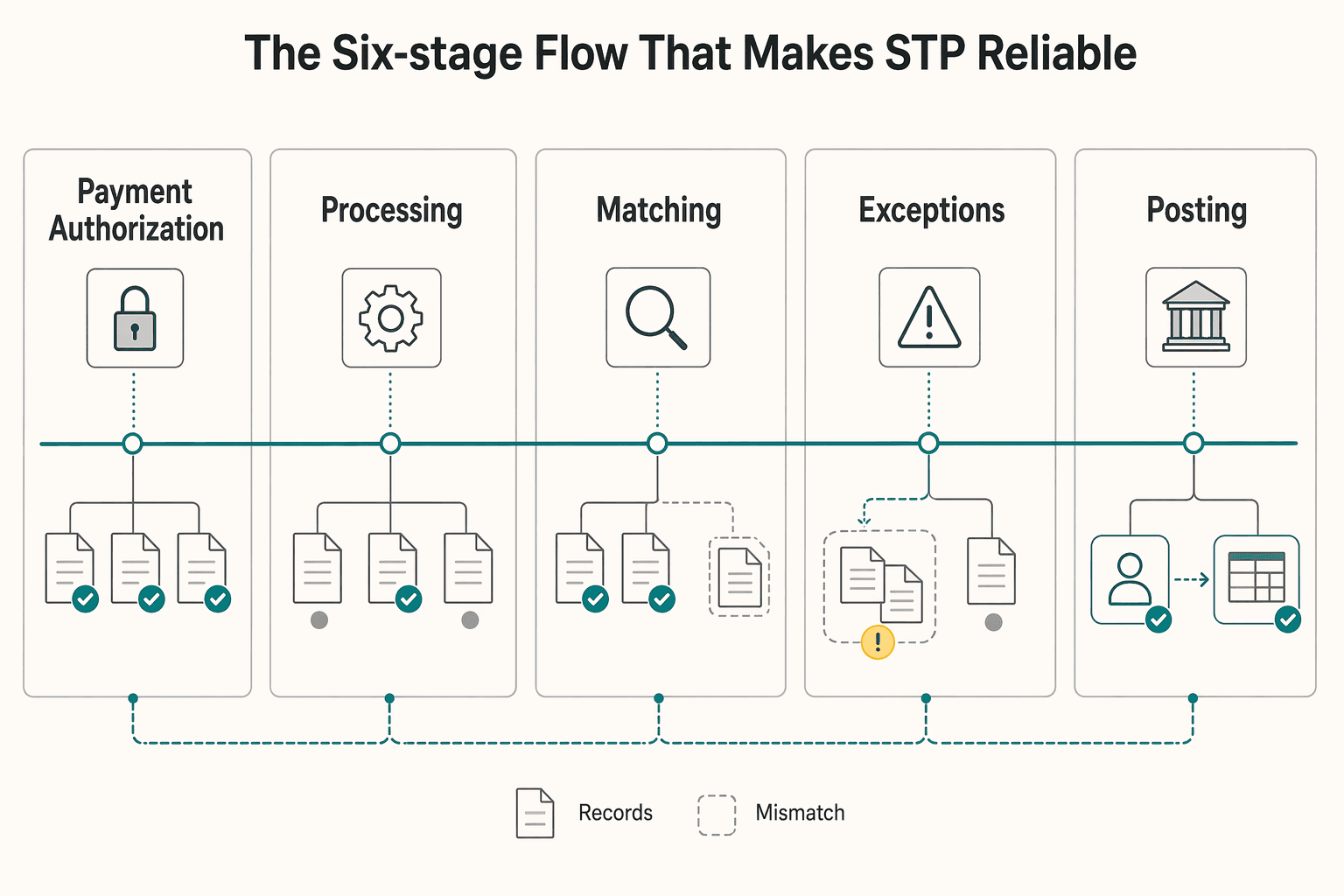

The six-stage flow that makes STP reliable#

Reliable STP comes from stage-by-stage control, not just a successful match. Use this six-stage operating model as one practical template to keep traceability from authorization through reconciliation, while remembering that STP sequences can vary by implementation.

| Stage | What must happen | Practical handoff (example; org-specific) | Verification checkpoint |

|---|---|---|---|

| Payment authorization | Confirm the payment is allowed under your policy, amount, counterparty, and method rules. | Product defines approval rules and statuses; engineering enforces them in the payment path; finance ops validates control and accounting fit. | Store a unique transaction ID, approval outcome, timestamp, and actor or rule source for every authorized payment. |

| Processing | Move the payment through network processing, for example authorization, clearing, and settlement. | Engineering owns provider integrations and state transitions; product owns user-visible statuses; finance ops defines when status is financially practical. | Map provider reference IDs to your internal transaction ID, and make duplicate webhook delivery idempotent so state is not applied twice. |

| Matching | Link payment and remittance data to the correct invoice or obligation. This is where cash application begins in AR. | Finance ops owns match rules and tolerances; engineering provides remittance fields and matching outputs; product defines what users can view or correct. | Keep match evidence: amount, payer or payee identifier, invoice reference, remittance detail, and rule or confidence used. |

| Exception workflows | Route unmatched, partial, or conflicting items to investigation instead of forcing automation through. | Finance ops owns investigation and resolution; engineering routes full case context; product shows exception status clearly. | Record reason code, owner, opened timestamp, and linked transaction evidence for every exception. |

| Posting | Commit only verified matches to the customer account or ledger after required exception handling. | Finance ops sets posting and review requirements; engineering writes journal and ledger events; product exposes final status. | Before posting, confirm payment, account, and ledger destination align; if review-before-post is enabled, retain that approval with the journal record. |

| Reporting | Reconcile applied and posted outcomes against bank records and operational status data. | Finance ops owns reconciliation evidence; engineering provides exports and bank mappings; product consumes the same source of truth for status. | Reconcile bank, receivables, and payables regularly, and resolve any bank-versus-ledger status mismatch. |

Cash application sits between matching and posting: matching decides where money should go, exception handling interrupts when evidence is weak or incomplete, and posting makes that decision real in AR or the ledger. Preserving a human-review gate before final posting can help you avoid unwinding a wrong posted item later.

Timing controls matter just as much as matching logic. If your exception clock starts before the rail has had time to settle, you create avoidable manual work. For ACH, settlement timing can include current-day windows such as 1:00 p.m. ET and 5:00 p.m. ET, plus future-business-day timing such as 8:30 a.m. ET. Exception triggers should align to expected settlement behavior.

Treat a payment as straight through only when you can prove one auditable chain of IDs, timestamps, and evidence across all six stages. If a handoff cannot be reconstructed, that path is still an exception path, not reliable STP. Related reading: How Payment Platforms Really Price FX Markup and Exchange Rate Spread.

The minimum data contract required before you automate matching#

Before you enable automated matching, define a data contract that lets you trace every posted outcome back to clear evidence. If you cannot name the source system, owner, validation rule, and fallback for each required field, do not auto-post.

Start with fields that survive handoffs#

The minimum contract is not a universal banking standard. It is the smallest field set your team needs to prove why cash was matched, posted, or held.

In practice, these five groups are a useful baseline before go-live.

- Payer and payee identifiers

- Invoice reference or other remittance information

- Amount

- Transaction and settlement timestamps

- Status events delivered through webhooks or equivalent provider updates

Remittance detail is a practical dependency, not a nice-to-have. Invoice numbers, applied discounts, and similar references make reconciliation faster. When remittance is incomplete, research effort rises and cash application slows. You do not need perfect remittance on every payment, but you do need a clear fallback when it is missing. Do not guess and post.

A useful readiness check is simple: sample recent payments and confirm you can reconstruct one chain from invoice record to provider transaction to posted ledger entry from stored fields alone. If that chain breaks, fix the contract before you scale volume.

Duplicate protection is part of the contract#

Duplicate prevention belongs in the contract because retries can change financial outcomes. Keep request deduplication and event deduplication as separate controls.

First, use idempotency keys on retryable create and update requests. Stripe supports idempotency keys on POST requests and describes them as unique retry keys that let the server recognize repeated attempts for the same operation. Use a UUID or a stable business key only when it is truly unique for that operation.

Second, store provider reference IDs and processed webhook event IDs. Webhook endpoints can receive the same event more than once, and failed deliveries can be retried. Posting logic should check whether an event ID was already processed before applying state again. When provider events include both request ID and idempotency key, store both alongside your internal transaction ID so ops can distinguish a retry from a distinct action.

A common failure pattern is payment creation being idempotent while duplicate webhook deliveries still trigger duplicate posting. You need both controls.

ACH timing can look like a matching failure when it is not#

For ACH, timing can create false exceptions if your rules fire too early. ACH is batch-based, and settlement timing should determine when matching and exception clocks start.

| Timing point | Detail | Operational note |

|---|---|---|

| Processing day | ACH processes payments 23-1/4 hours each banking day | Settlement timing should determine when matching and exception clocks start |

| Daily settlements | ACH settles payments four times each banking day | Set exception timing to the rail's expected settlement behavior |

| Standard settlement calendar | Standard settlement does not occur on weekends or federal holidays | Do not use authorization or file submission time alone |

| Later Same Day ACH window | 4:45 p.m. ET deadline with settlement at 6:00 p.m. ET | Include available settlement timestamp in the contract |

Nacha states ACH processes payments 23-1/4 hours each banking day and settles payments four times each banking day. Standard settlement does not occur on weekends or federal holidays. For later Same Day ACH, the Federal Reserve describes a 4:45 p.m. ET deadline with settlement at 6:00 p.m. ET. Same Day ACH also has a stated cap of up to $1 million.

Set exception timing to the rail's expected settlement behavior, not just authorization or file submission time. If you label ACH transactions unmatched before the relevant window has passed, you can create avoidable manual work. Include ACH processing date, available settlement timestamp, and provider status events in the contract so teams can separate true matching failures from normal rail timing.

Readiness table#

| Required field | Source system | Owner | Validation rule | Fallback behavior when missing |

|---|---|---|---|---|

| Payer and payee identifier | Invoice or customer/vendor master, plus payment provider record | Finance ops for naming rules; engineering for mapping | Must map to one internal account or counterparty record with no ambiguity | Route to review queue and block auto-posting until identity is confirmed |

| Invoice reference or remittance detail | Invoice or ERP record, customer submission, provider remittance fields | Finance ops | Must match an open invoice or approved obligation, or pass a documented alternate match rule | Hold for research or remittance enrichment; do not force a guessed match |

| Amount | Invoice record and provider transaction | Finance ops | Amount must equal expected amount or fall within your documented tolerance | Create an exception for partial, over, or conflicting payment rather than auto-applying |

| Provider reference ID and internal transaction ID | Payment provider and internal payments service | Engineering | Both IDs must be stored and linked one to one for every posted transaction | Stop posting and raise an integration defect if link is missing |

| Webhook event ID, request ID, and idempotency key | Provider event payload | Engineering | Event ID must be unique in processed-events storage; idempotency key must map to the original operation when available | Accept the event for review only after dedupe check; never post twice from repeated delivery |

| Transaction and settlement timestamps | Provider events, ACH file/header metadata, bank or provider status feed | Engineering with finance ops sign-off | Timestamps must be recorded in a consistent timezone and retained with status changes | Delay exception creation until the expected ACH settlement window has passed |

Do not treat match rate alone as readiness. Readiness means you can prevent duplicate posting, explain every posted item, and avoid false ACH exceptions caused by settlement timing.

Choosing rule-based matching, AI, or a hybrid model#

For reliable posting, many teams start with deterministic rules as a baseline, then add ML where ambiguity remains. In practice, hybrid models are common: rules handle clear matches, and uncertain cases stay with finance for review.

Once your data contract is stable, decide which outcomes are safe to auto-apply and which should stay in suggestion mode.

Rules first when inputs are predictable#

Rule-based automation, whether BPA or RPA, works best when inputs, outputs, and triggers are clearly defined. In matching systems, rule conditions can enforce exact or tolerance-based matches, so finance can explain why a transaction was applied.

This approach is especially defensible when your source data has enough reference attributes to avoid ambiguity. Deterministic engines can also model different match shapes directly, including one-to-one, one-to-many, many-to-one, many-to-many, and zero-amount logic. For many-to-many types, Oracle requires a Match Exactly condition.

Where AI helps and where it should stop#

AI and ML can help when references are incomplete or inconsistent and your team has manual history to learn from. SAP's framing is practical: rules match most items, unmatched items stay manual, and ML complements standard rules by learning from past manual actions.

Use ML as a suggestion and prioritization layer, not a blanket auto-posting layer. Confidence scoring supports that design: confidence values can run from 0 to 1, with high-confidence outcomes eligible for automation and low-confidence outcomes routed to human review. Thresholds are implementation-specific, so set them based on your own risk, materiality, and reversibility.

Hybrid selection table#

| Model choice | Best use case | Main risk | Review requirement |

|---|---|---|---|

| Rules only | Stable formats and reference-rich data | More unmatched items when references are missing or ambiguous | Manual review of unmatched items and rule exceptions |

| ML suggestions only | Inconsistent references where teams want suggestion support | Over-trusting suggestions without enough controls | Reviewer must confirm or discard each suggestion |

| Hybrid (rules + ML) | Rules baseline exists and ambiguity is concentrated in exceptions | Control gaps when rule and model outcomes conflict | Rules auto-apply only in defined cases; low-confidence items go to review |

Set escalation policy before go-live#

Define the low-confidence path before launch. Your policy should assign reviewer ownership, define when manual review is mandatory, and require confirm-or-discard decisions for suggested matches.

A practical control is to retain enough evidence to reconstruct each decision, including the confidence score, candidate matches, reviewer action, and final posted outcome. If a decision cannot be explained from stored evidence, tighten controls before you expand automation.

This pairs well with our guide on Choosing Escrow, MoR, or Direct Payment by Operational Ownership.

Design exception routing before you scale throughput#

Define exception routing before volume rises. A conservative policy is to let automation clear only cases you can unwind cleanly, and send decisions that could materially change cash application or reconciliation to human review.

Start with a practical taxonomy#

You do not need a perfect master list, but you do need a stable working list early. Start with a small set that matches your real exception patterns, such as remittance mismatches, incorrect recipient items, misrouted payments, timing issues, and return events.

Use labels that separate remittance issues from rail or settlement issues so each queue has a clear next action, evidence trail, and owner. Keep categories tight enough that a reviewer can act without reconstructing the full payment history every time.

Assign owners and timing by exception type#

Route each exception type to one primary resolver and one fallback, based on who can make the correct posting or routing decision fastest. The org chart matters less than decision clarity and handoff speed.

Set explicit response targets for timing-sensitive exceptions. FedACH publishes same-day electronic return windows, including 10:30 a.m. ET transmission with 1:00 p.m. ET current-day settlement, and Nacha bulletin language includes role-based accountability with request-for-return status updates within 10 banking days. If ACH is part of your flow, pair this with ACH Payment Processing for Platforms: How to Move Money via the US Banking Network.

Auto-resolve only what stays reversible#

In practice, exception handling is where payment processing diverges from normal STP flow. SAP Exception Control is built for those situations, and configured threshold breaches can push payment orders into exception handling when incorrect recipient items exceed permitted limits.

A conservative operating rule is to automate corrections that are reversible without changing final ledger intent, and route material ledger-impact decisions to human review before posting. SAP also distinguishes timing and state. Invalid recipient items can be removed from outgoing payment orders, but already posted clearing items cannot simply be excluded and can be marked 76 (Redirected).

Preserve evidence for audit and re-review#

Your exception process should preserve enough evidence to explain every decision after retries, reversals, and month-end close. Keep the original payment event, remittance text, candidate invoice matches, provider reference ID, timestamps, ownership history, reviewer action, and final posting or reversal result.

Also keep retry-safety records on your side. Stripe idempotency keys can be up to 255 characters and may be removed after they are at least 24 hours old, so provider-side request history alone is not a durable audit trail.

Integration checkpoints for engineering and finance ops#

Once exception ownership is set, treat the integration boundary as a shared control point. Engineering and finance ops should be able to point to the same payment state, ledger outcome, and evidence trail.

Make webhook handling replay-safe#

Webhook updates are asynchronous, so your source of truth cannot be only a product screen or front-end callback. Define the webhook contract early: accepted event types, required fields, duplicate detection rules, and late-event behavior.

Build around two controls. Deduplicate inbound events, because duplicate deliveries can happen and, on Stripe, undelivered events can be retried for up to three days. Use idempotency on outbound writes where supported so retries return the prior result instead of creating a second side effect.

On Stripe, idempotency keys can be up to 255 characters and may be pruned after they are at least 24 hours old, so keep your own durable processing and posting record. Also verify signatures against the exact raw payload, because request-body mutation can fail verification and block otherwise valid updates.

Normalize instant and batch rails into one reconciliation model#

If you support both real-time rails and batch rails, map them into one internal reconciliation model. ACH is batch-oriented, while FedNow runs near real-time with 24x7x365 processing, so timing differs even when ledger intent does not.

Your internal record should consistently track processing state, settlement timing, payout or batch linkage, and exception outcome across rails. Avoid collapsing different states into one label if finance still needs payout, batch-close, or bank-movement linkage for reconciliation.

Test failure cases before launch#

Before launch, test the failure modes that break reconciliation in production.

| Failure case | What to confirm | Evidence sample |

|---|---|---|

| Duplicate event delivery | One state change, one posting decision, and one audit entry | Provider event ID, receive timestamp, internal payment ID, final product status, export row, and exception-routing result |

| Out-of-order delivery | Later events arriving first do not regress state or create conflicting records | Provider event ID, receive timestamp, internal payment ID, final product status, export row, and exception-routing result |

| Missing payload data | Records missing key matching fields are held for review, not auto-posted | Provider event ID, receive timestamp, internal payment ID, final product status, export row, and exception-routing result |

For sign-off, capture one evidence sample per case with provider event ID, receive timestamp, internal payment ID, final product status, export row, and exception-routing result.

Reconcile exports to what users see#

Treat finance exports as reconciliation artifacts, not a mirror of UI status text. Use provider reporting that preserves transaction-to-payout linkage, and include order-management linkage where finance workflows require it.

Go live only when each item can be traced end to end from provider report to internal order or invoice to product-visible status. That is the control that prevents split-brain operations between support, finance, and accounting teams.

Use this section as a pre-launch review: map webhook retries, idempotency handling, and status surfaces against the implementation patterns in the Gruv docs.

Controls that keep automation fast without weakening risk posture#

Fast automation is defensible when every auto-authorization or auto-posting decision ties back to a policy gate you can reconstruct later. If a decision cannot be explained for audit, AP, AR, or support, route it to exception handling instead of straight-through flow.

For STP, keep the decision and its evidence on the same transaction trail. An operator should be able to trace one item from provider event ID to internal payment ID to finance export row. Then they should be able to see whether it was auto-approved, held, or sent to review. Use a simple checkpoint: test one auto-approved payment and one routed exception, and confirm both can be independently reconstructed without chat threads or side spreadsheets.

Do not apply one global control set across all markets. Verification requirements vary by country, legal-entity type, and the financial products or capabilities you offer. For example, a sole proprietorship in Belgium may need a registration number while one in the United Kingdom may not. If you use PSP onboarding, treat it as an input, not proof that your own legal KYC or verification obligations are satisfied. Where PSD2 and Strong Customer Authentication apply, outsourcing parts of the flow does not outsource accountability.

Rail behavior also changes control design. Same Day ACH uses scheduled windows; published windows include 10:30 a.m. ET, Noon ET, and 1:00 p.m. ET. RTP is different: recipients receive funds within seconds, and settlement is final and irrevocable. Controls tuned for ACH delays should not be reused unchanged for RTP.

Keep logs thin but usable. Data minimisation means storing only what is necessary, and logging practice warns against collecting too much or too little. Keep the identifiers and timestamps needed for cash application and reconciliation, but avoid spreading raw personal data across routine logs, tickets, and exception queues. Store evidence once, then reference it everywhere else.

KPI scoreboard and launch checklist for the first 90 days#

In the first 90 days, judge the launch by operational trend quality, not raw volume. STP progress is most visible when manual effort and matching friction decline as volume scales.

| Measure | What it tells you | First checkpoint |

|---|---|---|

| Manual-touch rate | A practical proxy for STP rate, not your intended one | Sample auto-posted items and verify no hidden spreadsheet or support intervention was needed |

| Exception routing volume and age | Whether rules are too strict, too loose, or under-modeled | Split true unmatched items from timing-related holds, especially by rail |

| Match accuracy and duplicate-post rate | Whether automated matching is reliable | Map provider event IDs and idempotency keys to one internal payment ID so retries do not create second postings |

| Cash application lag and reconciliation close time | Whether AR and AP can close cleanly | Confirm finance exports, ledger outcomes, and product statuses agree on the same transaction set |

Do not rely on aggregate movement alone. A falling manual-touch rate can hide rising duplicate posts or slower reconciliation. Webhook-based systems can deliver the same event more than once, and some providers do not guarantee delivery order, so duplicate-post rate should be tracked separately. Exception aging should also reflect retry behavior during outages: Stripe can resend undelivered events for up to three days, and event-list backfill is limited to the last 30 days.

Use a named-owner launch checklist, even if sign-off is informal.

- Finance ops: confirm AP and AR can reconstruct one auto-posted payment and one exception from provider event to ledger export without side notes

- Engineering: test duplicate events, out-of-order events, endpoint failure, and replay handling before cutover

- Product: verify status surfaces clearly reflect asynchronous outcomes, including bank confirmations and dispute-related changes, so operations is not working from stale states

Use external benchmarks as context, not as a direct target. APQC benchmarks are segmented by industry and revenue band, so comparisons should be normalized. Ardent Partners Accounts Payable Metrics that Matter is useful directional input, but the February 2025 edition reflects a sample of 212 AP professionals. If comparables do not fit your operating model, set an internal baseline in week 1 and manage to week-over-week improvement.

Conclusion#

STP is strongest when matching, exception ownership, and retry-safe integration are designed as one operating model. If those controls are weak, automation can shift work into cash application and reconciliation instead of removing it.

Start with a clear data contract before you expand automation. Use consistent internal and provider references, complete payment data, and usable webhook event payloads. Better data quality is the first prerequisite for stronger STP. When data is missing or inaccurate, route items to explicit exception handling instead of forcing auto-posting.

Treat idempotency and event replay as core controls. Idempotency keys make request retries safe, but webhook events can still be retried for up to three days. Consumers should deduplicate already processed events and return success so retries stop. Since idempotency keys can be pruned after 24 hours, keep your own processed-event history and duplicate-post controls before anything hits the ledger.

Scale only after verification passes. Trace sample auto-posted items from raw event to match decision to ledger output without relying on spreadsheet repair in the middle. Confirm cash application lands on the correct invoice where relevant. Roll out in phases and judge progress by reconciliation outcomes like duplicate-post rate, exception aging, cash application lag, and close effort, not raw transaction volume. For ACH flows, account for rail timing. The network processes payments 23 1/4 hours each business day and settles four times a day, so some lags can reflect timing effects rather than true breaks.

When you move from design to rollout, align your exception ownership model with compliance-gated disbursement flows and batch tracking in Gruv Payouts, where enabled.

Frequently Asked Questions

What is straight-through processing in payments, in plain terms?

Straight-through processing means a transaction moves through its lifecycle with minimal manual intervention. It is not all or nothing, so teams usually manage to an STP rate rather than assuming every case can be automated. Some exceptions still need human review.

How is STP different from automated payment matching?

STP is the end-to-end operating outcome, while automated payment matching is one control inside that flow. Matching links receipts to the correct open transaction and then either applies them automatically or routes them for review. If matching quality is weak, STP performance can plateau even when payment execution is automated.

What data is required for reliable automated payment matching?

Use stable internal IDs and consistent provider references so each transaction can be traced to one internal payment record. A practical baseline is attaching your own IDs to payment objects and keeping one payment object per order or customer session so attempt history stays clear. Use idempotency keys on retries to prevent duplicate effects.

What should be auto-approved versus routed to human review?

Auto-approve matches that are exact or clearly within your defined tolerances. Route ambiguous or high-impact cases to human review, including mismatch scenarios that cannot pass matching checks. In AP workflows, failed tolerance checks should place the invoice on hold, and payment should wait until that hold is explicitly released.

Which KPIs prove STP is actually improving operations?

Track STP rate, manual-touch rate, exception volume and aging, match accuracy, duplicate-post rate, cash application lag, and reconciliation close time. For receivables-heavy teams, DSO can add context on how quickly credit sales convert to cash, but it should not replace transaction-level accuracy checks. A reliable test is tracing sample auto-posted items from provider event to ledger output.

Can STP work across ACH payment processing and other payout rails?

Yes, but only if your matching logic reflects rail-specific timing instead of assuming instant settlement everywhere. ACH is batch-based with scheduled settlement, and Same Day ACH settles three times daily with payments up to $1 million. Multi-rail designs should use one reconciliation framework with rail-aware status handling, including regional payment-method differences where relevant.

When should a team add AI or machine learning to matching logic?

Add ML after deterministic rules handle clear cases and the remaining workload is repetitive, messy, or exception-heavy. A hybrid model works best when rules handle obvious matches and ML ranks or recommends harder cases. Keep humans responsible for complicated exceptions that require manual clearing.

What is the easiest way to avoid false confidence after launch?

Do not treat higher volume as proof that automation is healthy. Webhook retries can continue for up to three days, and event-list retrieval may only cover the last 30 days, so replay-safe processing and duplicate controls are critical. If an auto-posted item cannot be reconstructed from event to match decision to ledger outcome, it is not truly straight through.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- csrc.nist.gov/glossary/term/artificial_intelligencetrusted

- eba.europa.eu/publications-and-media/press-releases/eba-cl...trusted

- ecb.europa.eu/services/glossary/html/act7s.en.htmltrusted

- federalreserve.gov/paymentsystems/fednow_about.htmtrusted

- federalreserve.gov/paymentsystems/fedach_about.htmtrusted

- legislation.gov.uk/eur/2016/679/article/5trusted

- achdevguide.nacha.org/how-ach-worksexternal

- achdevguide.nacha.org/ach-file-overviewexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platform Teams Use 2-Way and 3-Way Invoice Matching to Stop Overpayment

Platform teams do not need another glossary entry on invoice matching. They need controls that stop real overpayment paths before money goes out the door. At its core, invoice matching compares an invoice with supporting records before payment. The practical question is what you add when a clean match still does not mean the invoice should be paid as submitted.

A Canadian Freelancer's Guide to Setting Up a US Stripe Account

Start with your Canadian Stripe account if your goal is to protect margin without adding U.S.-entity complexity. It is often the simpler path, and with the right payout setup you can receive USD without forcing immediate conversion.

ACH Payment Processing Platforms for U.S. Collections and Payouts

Start with the outcome, not the feature label. You may need a setup that collects money in and sends money out over the U.S. banking network, not just a generic bank-transfer option. In practice, that often means ACH debits for collections and ACH credits for payouts, with controls your product, engineering, and finance teams can run in production.