Quick Answer

Start by assigning one owner and one due date to every case, then run payment disputes platform operator workflows through a fight-concede-escalate table based on reason code and evidence quality. Keep hard clocks visible: many response windows run 7 to 21 days, and missed deadlines can auto-lose the dispute. Use reusable representment files, and treat a case as finished only when provider status and ledger impact both match.

How to handle payment disputes as a platform operator using ownership, clocks, and ledger checks#

Payment disputes create operational and financial risk early, not just later as a finance line item. For a platform operator, the exposure is not only the disputed amount. It is also the labor to work the case and the drag from slower resolution when cases move across multiple parties and platforms.

A payment dispute is a formal claim from a cardholder or issuing bank about a payment. A chargeback is a dispute where a cardholder questions a payment with their issuer. Representment is the process of contesting a chargeback to recover funds. These distinctions matter because unclear terminology can blur ownership across Product, Support, Finance, and Payments Ops.

The cost goes well beyond fees. Disputes consume operational resources, and resolution often spans multiple platforms. In practice, the flow usually includes issuer, acquirer, and merchant handoffs, which can increase processing time and make deadline management harder.

Start by verifying liability in your own setup. In Stripe Connect marketplace configurations, the platform is in the end liable for chargebacks and related costs for both destination charges and separate charges and transfers. If your team still treats disputes as a merchant-only issue, fix that before you design queues, rules, or automation.

A costly failure mode is delay paired with weak evidence. Missing evidence deadlines can lead to an automatic chargeback loss. Contested disputes can also take two to three months, so aging backlog is an operational risk, not a cosmetic metric.

Verify the basics first#

Before you optimize anything, confirm three things in your environment:

| Check | What to confirm |

|---|---|

| Liability location | Whether your platform, your merchant, or both absorb chargeback losses and related costs |

| Deadline source | Where evidence deadlines appear, who sees them, and whether those deadlines are tracked in your own tools or only in a provider console |

| Case trail | That each dispute ties back to the original transaction and the records needed for representment when appropriate |

- Liability location

Check your PSP or marketplace agreement and confirm whether your platform, your merchant, or both absorb chargeback losses and related costs.

- Deadline source

Identify where evidence deadlines appear, who sees them, and whether those deadlines are tracked in your own tools or only in a provider console.

- Case trail

Make sure each dispute ties back to the original transaction and the records needed for representment when appropriate.

If these basics are unreliable, extra tooling usually helps you process confusion faster, not resolve it better.

Scale matters too. Stripe cites a projected 24% global increase in chargebacks from 2025 to 2028, totaling 324 million transactions each year. It also notes that when dispute rates exceed card-network thresholds, additional network fines can range from $50 to $150 per dispute.

This guide is for platform operators who need practical choices, not theory. The next sections move through the decisions in order: define ownership, set evidence standards, choose where automation helps, and keep human judgment where conceding, contesting, or escalating changes the outcome.

Related: What Is Dunning? A Platform Operator's Guide to Recovering Failed Recurring Payments.

Define the dispute terms and who owns each decision#

Lock down language and ownership first. Use one dispute vocabulary and one accountable owner for each decision so cases are routed and handled consistently.

- Standardize the terms in writing

Use scheme-grounded definitions for external dispute events, then label internal finance terms as internal. A payment dispute or chargeback starts when a cardholder questions a payment and the issuer initiates a formal dispute. Representment is contesting that chargeback to recover funds. Treat write-off and recovery as internal accounting labels, not universal scheme definitions. Verify this by aligning the terms across support macros, finance close notes, and dispute-tool field labels.

- Assign one accountable owner per decision

Split ownership across merchant support, issuer-facing ops, and acquirer-facing ops, since issuer and acquirer workflows both participate in formal filings and document exchange. In RACI, keep exactly one accountable owner for each task. A practical split is merchant support for seller notification and evidence intake, issuer-facing ops for dispute intake triage, acquirer-facing ops for filing and document submission, and one named approver for the final accept-or-defend decision. Each case record should show the current owner for intake, evidence approval, and final decision.

- Name one escalation owner for scheme-rule exceptions

Dispute flow differs by card scheme and payment method, and rules change over time. Visa guidance includes dated effective conditions, for example 13 April 2024 versus 12 April 2024, and Mastercard publishes dated editions, for example Merchant Edition 27 January 2026. Assign one escalation owner to interpret rule changes and update routing when rule conditions or evidence requirements change. Without that owner, exceptions drift between teams and cases get handled inconsistently.

Need the full breakdown? Read How Platform Operators Should Plan PCI DSS Level and Cost.

Gather prerequisites before you touch the first queue#

Before you process live disputes, make sure every case has complete inputs, your evidence structure is reusable, access is tested, and internal SLA targets are set against known external clocks.

Build a minimum case file for every dispute#

Start every case with one baseline packet before deciding to concede or file representment:

- transaction timeline in chronological order

- customer communications

- fulfillment proof, delivery or access

- refund history

- provider transaction and dispute financial references from your merchant stack

Keep the timeline first in your internal view: authorization, capture, fulfillment or access, customer contact, refund attempt, dispute notice. If analysts have to reconstruct this across multiple tools, cases are harder to review consistently as volume rises.

Do not use one evidence standard for every reason code. Evidence needs vary by dispute reason, and fulfillment proof is central for service and subscription disputes. Include partial-refund history too, because the unrefunded portion can still be disputed. Review recent chargebacks and confirm each can be understood from the case file alone.

Standardize the evidence folder before the first submission#

Use one consistent top-level folder spine across dispute types, then add reason-specific checklists inside it.

Suggested top-level sections:

- receipts and order records

- customer communications

- policies and terms

- system logs

- fulfillment artifacts

- provider references

This gives you reuse and auditability without pretending every reason code needs the same documents. Keep the layout standard, but keep the requirements reason-specific.

Do not file early with an incomplete pack. Some flows allow one submission only, with no edits or supplemental evidence after filing.

Confirm access, permissions, and event visibility#

Test permissions before analysts touch the queue. Access to accepting disputes and submitting evidence is often role-gated.

Minimum access to validate:

- dispute console

- transaction and dispute financial records

- document upload paths

- webhook and event logs for async updates

Webhooks matter operationally because status changes arrive asynchronously, and delivery can retry for up to three days. Verify logs show whether events were received, retried, or missed. Run one access test per role and one end-to-end event test, then store audit notes.

Set internal SLA targets before volume forces bad habits#

Set internal SLA targets now, because external timelines differ by scheme and reason context. A single vague "respond quickly" target is not enough.

| Window | Context |

|---|---|

| 30 days from receiving the NoC | Example defense window |

| 120 days | Issuer window from delivery in cited guidance |

| 540 days | General outer bound in cited guidance |

Ground your internal timing model against known external windows, including:

30 days from receiving the NoCas an example defense window120 daysas an issuer window from delivery in cited guidance540 daysas a general outer bound in cited guidance

Define separate internal targets for intake, evidence collection, approval, and submission, and triage by deadline risk plus evidence readiness so cases do not age out in backlog.

Map the lifecycle from first alert to final ledger impact#

Turn your dispute process into explicit states with clear ownership, clocks, and ledger checkpoints. If cases sit in a vague "open" bucket, deadlines can slip and reconciliation work can pile up for Finance.

Define internal states and clocks#

Define your internal states even when providers use different labels. One practical internal operating model is intake, triage, evidence collection, review, submission, ruling, and post-resolution write-off or recovery. Treat this as your operating sequence, not a universal provider sequence.

For each state, store four fields in the case record:

- owner, one team or role

- entry trigger

- exit condition

- SLA clock rule

Clock rules need to reflect real provider deadlines. On Stripe, response deadlines are usually 7 to 21 days by network, and missing the deadline means you automatically lose the dispute.

Attach provider status signals to each state so analysts can act without guessing:

- Stripe: Dashboard, email, webhooks, and API notifications

- Finix: response states like

NEEDS_RESPONSEto indicate required action - Primer:

DISPUTE.STATUSwebhook on every status or type change

Sample five recent cases and confirm each has a clear alert source, current state, single owner, and active clock.

Set clock rules and blocker codes#

Set clock start and stop rules and blocker codes so cases cannot age silently. There is no universal cross-provider start point, so start your internal clock when your team can act, usually when the notice lands in a usable case record.

Use internal blocker reasons, for example:

- missing transaction reference

- missing customer communication history

- missing fulfillment proof

- unclear liability owner

- webhook received but no internal case created

Avoid catch-all blockers like "needs review." If a clock is paused, require both a blocker code and a next check date.

Separate early-stage inquiries from full chargebacks when they share a queue. For example, PayPal inquiry cases can remain in inquiry for a 20-day period before escalation to PayPal.

Separate operational close from financial close#

Close disputes in two stages: operational close at ruling, then financial close after ledger reconciliation. Provider case status alone is not enough.

On Stripe, disputed funds are typically withdrawn immediately and returned only if the case is resolved in your favor, and Stripe also debits the dispute amount plus a dispute fee at creation. That creates financial impact before the ruling.

Map each provider outcome to ledger events:

- Stripe: match dispute reference to initial debit, dispute fee, and any recovery

- Finix: confirm the funds pull appears as a

MERCHANT_DEBITtransfer where applicable

This matters because issuer decisions can take 60-75 days after evidence submission, and full dispute lifecycles can run 2 to 3 months. Reconcile yesterday's dispute creations and resolutions against ledger entries, and route unmatched items into post-resolution review.

Use a handoff matrix for cross-team exceptions#

Use an internal handoff matrix so Support, Finance, and Engineering route missing-data issues differently from fraud-risk decisions.

| Trigger | Primary owner | Secondary owner | Next action |

|---|---|---|---|

| Missing delivery or access proof | Support | Engineering | Support requests fulfillment artifacts; Engineering joins only if logs are missing or inaccessible |

| Provider alert received but no internal case or broken webhook trail | Engineering | Finance | Engineering restores event capture and backfills case creation; Finance holds manual posting until references are complete |

| Disputed funds or fee posted but no matching case | Finance | Support | Finance reconciles ledger impact; Support adds customer context and evidence links |

| High-confidence fraud pattern with weak customer legitimacy | Finance or Risk owner | Support | Concede or escalate under fraud policy instead of forcing weak representment |

If you use Stripe Connect, include one explicit ownership rule in the matrix: charge type plus negative-balance responsibility determines who responds to the dispute. Test one dispute per supported charge type and confirm the responder of record and debit responsibility match the matrix.

Set decision rules for fight, concede, or escalate#

Once each case has a state and a clock, make the response rule-based, not analyst-by-analyst. Fight only when the reason code, evidence quality, and time remaining support representment.

Build a default decision table by reason code#

Build a reason-code decision table and make it the queue default. Defend-versus-accept should follow the dispute reason code and evidence readiness, not whoever picked up the case.

| Case pattern | Default action | Why | Verification point |

|---|---|---|---|

| Reason code is defensible and compelling, relevant evidence is already available | Fight | Defend only when sufficient compelling evidence exists | Case record shows reason code, evidence checklist, and submission owner before review |

| Transaction value is low relative to handling effort | Concede fast | Some disputes are not worth the evidence effort | Record includes value, estimated handling effort, and concede reason |

| Evidence does not meet defense requirements, or key proof is still missing late in the clock | Concede unless manually approved | Late evidence can become un-submittable, and weak files consume effort without improving odds | Missing document is named explicitly, not hidden under "needs review" |

| Case needs nonstandard data collection, raises privacy or compliance concerns, or falls outside policy | Escalate | Evidence collection must stay within privacy and legal limits, and the issuer decides the final outcome | Escalation owner and decision deadline are attached to the case |

Keep the table short enough to apply in under a minute.

Use midpoint logic to concede weak cases earlier#

Use midpoint logic so weak cases do not consume the full window. Scheme-level timeframes set the outer boundary, and merchant deadlines are often 20 to 45 days after notification, so your internal trigger should fire well before deadline pressure.

One operating rule to test: if evidence is still incomplete by your internal SLA midpoint, concede early unless expected recovery clearly exceeds handling cost. Treat this as an operating control, not a universal law.

Be explicit about what "incomplete" means. Require analysts to name the missing document and the last realistic retrieval date.

Score fightable cases to focus effort#

Use a confidence score to prioritize effort across fightable cases. The issuer decides the final ruling, so the score should guide resource allocation, not suggest control over the outcome.

Use one consistent score model tied to:

- reason-code fit

- payment method

- evidence availability and relevance

- cost relative to likely recovery

If you use Stripe signals, use them as inputs, not guarantees. Stripe Radar tiers, for example 5 dots 60% down to 1 dot 5%, can help with prioritization. Smart Disputes still does not guarantee favorable outcomes.

Create a narrow exception lane#

Separate policy exceptions from standard handling. Create a narrow, visible override path for relationship, precedent, or brand-risk cases so exceptions do not break queue discipline.

Use one exception label, one approver role, and one required note explaining why the case sits outside normal policy. Route legal or compliance review through this same exception lane when evidence-collection scope is sensitive.

Watch for false-economy behavior#

Track false-economy behavior weekly. Fighting weak cases can consume resources with little expected recovery, especially when evidence does not meet defense requirements.

Watch for low-value, weak-evidence cases that stayed open late and were still fought. If that band grows, tighten concede criteria or move the midpoint trigger earlier. The goal is a cleaner case mix: stronger representment files, faster concessions where odds are poor, and fewer late escalations as deadlines tighten.

For broader benchmarks, see State of Platform Payments: Benchmark Report for B2B Marketplace Operators.

Build evidence standards that survive issuer scrutiny#

Treat evidence quality as a gate, not a cleanup task. A defensible case is a reason-code and scheme-specific packet that is readable on first review and does not introduce PCI or privacy risk.

Create separate templates by reason and scheme#

Use separate evidence templates by dispute reason and scheme, not one generic packet. Reason codes determine what proof matters, and representment is the acquirer response to a first chargeback, so templates should match both the dispute category and the submission path.

Split each template into mandatory and optional fields. Keep mandatory fields focused on the transaction timeline, customer communications, and reason-code-specific proof such as active acceptance of terms at checkout. Use optional fields to add context without blocking submission when required files are complete.

Before you mark a case ready, require the template to show the reason code, scheme, required document list, and source of each file. If you support Visa CE3 for eligible friendly-fraud cases, keep CE3 as its own branch. Validate against your acquirer rules before hard-coding checks. Published guidance shows at least two prior undisputed transactions on the same payment method, with an upper bound shown as either 364 or 365 days depending on source.

Check proof quality before submission#

Run proof-quality checks before final submission. Issuer review is easier when evidence is chronological and readable without interpretation.

Verify these four items every time:

- timeline consistency across transaction and support records

- customer consent trail, such as checkout proof showing active acceptance of terms

- artifact quality, with readable text and clear images

- refund and resolution attempts, supported by processor logs and merchant account statements, not narrative alone

This is a common failure point. Mismatched dates, unreadable screenshots, or missing consent records can weaken the file, and some consumer dispute flows require documented prior resolution attempts with the business.

Store evidence with traceability and data controls#

Store evidence to protect data and preserve traceability. Use PCI DSS as the baseline control: minimize stored card data, mask or truncate printed card data, and do not retain card verification codes after authorization.

Handle redaction as a high-impact action. Redaction is not reversible and can affect related logs or events, so track it explicitly. Keep an internal evidence manifest with file ID, uploader, upload time, document type, case ID, and redaction status. Keep webhook or event-code history with it so dispute state changes remain auditable.

Turn failed submissions into structured feedback#

Convert failed submissions into structured feedback. Define standard reject reasons in internal QA before anything is sent to the acquirer.

Use fixed labels such as unreadable artifact, missing consent proof, incomplete refund evidence, wrong reason-code template, timeline gap, and redaction issue. In some integrations, you can delete uploaded defense documents and resubmit before final defense. After submission, updates may no longer be possible. Some flows are effectively one-shot, and one published Mastercard guideline context includes a 40-day defense deadline and a 19-page cap.

Use one verification check: every rejected packet must produce one structured reason, one owner, and one template or training action. If the same reject reason repeats weekly, fix the template or the upstream data capture.

Related: How Platform Operators Control Employee Expenses with Automation.

Choose tooling with a buy-build decision table#

Choose tooling based on operational fit, not demos. Use PSP-native tools when most dispute volume sits with one PSP. Use specialist SaaS when you need faster rollout with prebuilt workflows. Build internally when control over logic and data handling is worth the engineering ownership.

Compare the three realistic tooling paths#

Map the three realistic paths before vendor calls, then compare them on the same criteria.

| Path | Integration depth | Evidence automation coverage | Rule flexibility | Analyst override and reporting | Commercial watch-outs |

|---|---|---|---|---|---|

| PSP-native tools | Deep in that PSP environment | Can automate key dispute tasks for eligible cases | Bounded by provider controls | Varies by provider workflow and fields | May include per-transaction fees and, for platform setups, connected-account fees |

| Specialist SaaS | Can be lighter initial integration, depending on connectors and enrichment inputs | Prebuilt workflows can reduce manual assembly work | Varies by product and plan | Override controls and reporting depth vary widely | Subscription or usage pricing, plus portability and lock-in risk |

| Internal tooling | Defined by what your team builds and maintains | Depends on your own data capture, mapping, and submission flows | Highest direct control | Highest control if properly staffed | Highest build and maintenance burden |

Stripe is a clear PSP-native example. Smart Disputes automates evidence collection, compilation, and submission for eligible card disputes, and can auto-submit before timeout if no one takes action. Stripe also states outcomes are not guaranteed because the issuer makes the final decision. For marketplace flows, Stripe states the platform is in the end liable for chargebacks and related costs for destination charges and separate charges and transfers.

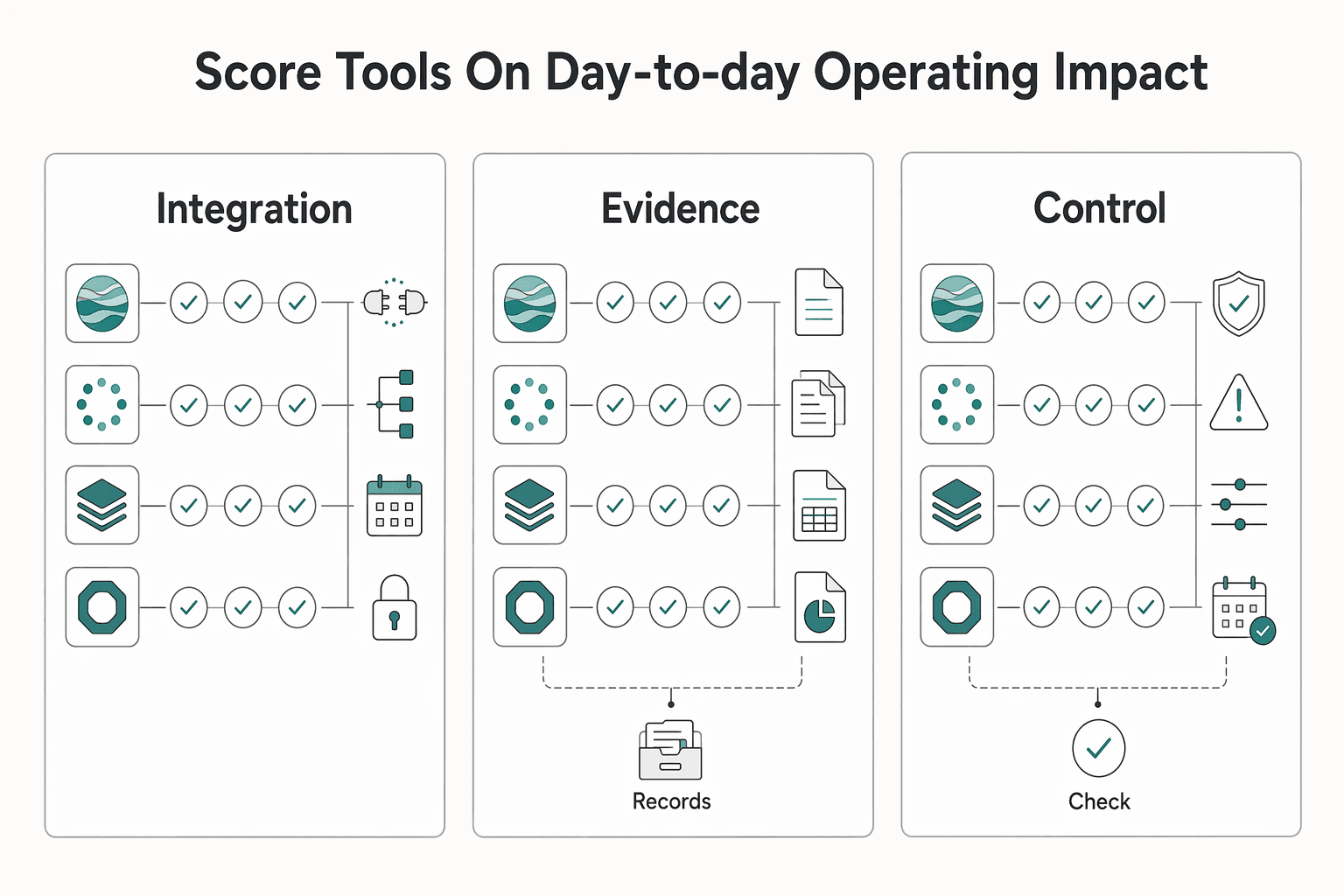

Score tools on day-to-day operating impact#

Score each option against day-to-day operating impact with five checks:

- How deep is the integration? Galileo Dispute API 3.0 is a lifecycle API path that creates and submits disputes into Galileo's dispute platform. If you run an in-house flow around Galileo, confirm exactly what still requires Galileo integration.

- How much evidence work is truly automated? Ask vendors to run sample closed cases and show what is auto-collected versus analyst-assembled.

- Can you change rules without vendor dependency? Stripe Radar for Fraud Teams supports custom rule writing for business-specific controls.

- Can analysts override automation cleanly? Chargeflow documents per-dispute signal overrides.

- Is reporting usable for queue and deadline control? Missing evidence deadlines can lead to automatic chargeback loss, so deadline and status visibility is a hard requirement.

Use Galileo, ACI Worldwide, Chargeflow, and Quavo as reference points, then validate claims in your own flow. ACI's Rabobank case study cites automation of eligibility checks and questionnaire submissions through VROL and Mastercom. Quavo's build-versus-buy framing is useful for tradeoff structure, not final proof.

Pressure-test commercials before commitment#

Get commercials in writing before you commit. Confirm:

- implementation effort, including API work, data mapping, and QA on evidence output

- expected analyst workload after go-live

- data export rights for case history, evidence files, and rule configuration

- cost and staffing impact if dispute volume doubles

Stripe Radar pricing includes a fee per evaluated transaction, and Radar for Platforms also includes a connected-account fee. SaaS can offer faster deployment and lower upfront costs, while build gives fuller control over features, maintenance, and data security. Choose based on the operating model your team can sustain.

For a step-by-step walkthrough, see What Is Vendor Management? A Platform Operator's Guide to Supplier Lifecycle Control.

Wire events and retries so automation does not create accounting errors#

Treat dispute events as accounting inputs, not just queue updates. Duplicate deliveries and delayed callbacks are normal, so build idempotency and reconciliation into the core flow.

Enforce idempotency before any posting or case change#

Webhook endpoints can receive the same event more than once. Log and check the provider event ID before you create a case, update case status, or post a loss or recovery entry. If the same update arrives again, return success without repeating the underlying action.

Use one control test for every provider event ID: one processing record, one case transition, and at most one ledger impact. One failure mode is double-posting ledger entries when a callback is retried after a timeout or transient 5xx response.

Accept fast, persist first, reconcile later#

Acknowledge quickly, persist the payload, then reconcile asynchronously. Accept the webhook with a 2xx status, store the message, and process it after receipt. Provider timing may not match your internal SLA clocks, and related objects can arrive asynchronously.

For Stripe dispute flows, events such as charge.dispute.created can arrive before your internal case has full context. Persist first, retrieve missing objects by API, then reconcile internal case state against ledger outcomes before closure. Your verification rule is simple: every resolved dispute has a matching internal status and matching accounting result, with no orphaned case and no orphaned journal entry.

Monitor stale states and retry storms#

Alert on stale states and retry storms, not only hard failures. Stripe can resend undelivered events for up to 3 days. Adyen retries three times immediately, then can continue from a retry queue for up to 30 days. PayPal Braintree resends every hour for up to 24 hours in production (up to 3 hours in sandbox), and a webhook that takes longer than 30 seconds is treated as a timeout.

| Provider | Retry pattern | Timing note |

|---|---|---|

| Stripe | Can resend undelivered events | For up to 3 days |

| Adyen | Retries three times immediately, then can continue from a retry queue | For up to 30 days |

| PayPal Braintree | Resends every hour | Up to 24 hours in production, up to 3 hours in sandbox; a webhook that takes longer than 30 seconds is treated as a timeout |

Monitor two signals:

- cases stuck waiting for provider updates beyond your expected window

- spikes in redeliveries for the same event type or endpoint

If retries bunch during an outage, slow your own retry pressure instead of increasing it and making recovery harder.

Related: What Is AP Automation? A Platform Operator's Guide to Eliminating Manual Payables.

Run a weekly governance rhythm with KPIs that drive action#

Weekly dispute governance should be decision-first, not reporting-first. Run one weekly review with a short KPI pack, and require each metric to trigger a clear action. Anything that does not drive staffing, rules, product, or evidence changes belongs in a monthly appendix.

Lock KPI definitions before reviewing trends#

Lock KPI definitions first so weekly trends stay trustworthy. Track new disputes, open backlog including SLA-breached cases, outcomes to dispute submissions, average closing time, and dispute write-offs, then add one exposure metric for leadership: dispute rate or dispute activity, labeled correctly.

Keep the distinction clean: dispute rate is disputes on successful payments by charge date, while dispute activity is by dispute date. Include a deadline lens in backlog reporting, because response windows are usually 7 to 21 days after notification and missing evidence deadlines can lead to automatic chargeback loss. Each week, reconcile new-case counts to provider intake and reconcile write-offs and dispute outcomes to the ledger.

Segment the metrics before diagnosing performance#

Segment before you diagnose performance. Review metrics at least by payment method and country. Where possible, add card brand and reason code.

This avoids false conclusions, because dispute exposure is not the same across payment methods. Reason codes vary by brand and can vary by region or network, so segmentation helps you isolate whether the issue is queue execution or a specific policy, onboarding, UX, or evidence gap.

Tie each KPI to a named decision#

Map every KPI to one named decision so the meeting ends with execution, not commentary.

| KPI | Decision it should trigger |

|---|---|

| Open backlog (including SLA-breached cases) | Temporary staffing change, queue reprioritization, or faster concede rules for weak cases nearing deadline |

| Outcomes to dispute submissions | Evidence template revision or tighter fight criteria by reason code |

| Average closing time | Tooling or handoff fix when cases stall |

| Dispute write-offs and related costs | Product, fraud, or merchant policy review when losses stay high |

| Dispute rate or dispute activity | Risk review as activity approaches levels treated as excessive, for example 0.75% in Stripe guidance |

Do not read weekly outcome swings in isolation. Outcome visibility can lag 60 to 75 days, and disputes can still arrive up to 120 days after the original payment.

Split dashboards for leaders and operators#

Use separate dashboards for leaders and operators. Keep the exec view narrow: new-dispute trend, dispute rate or activity, dispute write-offs and related costs, SLA-breached open cases, and the highest-activity segments.

Use the operator view for queue control: aging buckets, open urgent cases, average closing time, evidence-submission performance, and slices by payment method, region, card brand, and reason code. End each review with an owner and due date per decision, then confirm at the next review whether each KPI movement ties to a completed action, a deliberate hold, or a documented data issue.

Execute the first 90 days without overbuilding#

Treat the first 90 days as a stabilization sequence, not a tooling sprint. Automating messy intake before ownership, deadline tracking, and evidence quality are reliable is how control breaks down.

Days 0 to 30. Stabilize intake first#

In days 0-30, stabilize intake first because outcome feedback lags and deadlines do not. Disputes can take 30-90 days to resolve, while response windows can be much shorter, often 7-21 days depending on network and flow.

For each new case, require one owner, one due date, one current state, and one baseline evidence pack for your top dispute categories. A practical baseline often includes transaction timeline, customer communications, fulfillment proof, refund history, and provider reference so the first representment submission is usable.

By day 30, spot-check recent cases and confirm you can answer quickly:

- Who owns it?

- When is evidence due?

- What is still missing?

- Does internal case status match provider status?

If those answers are inconsistent, do not expand automation yet. Early submission quality matters because some flows allow only one submission and may not allow supplemental edits.

Days 31 to 60. Add fight and concede rules, then automate only clear data pulls#

In days 31-60, implement explicit fight and concede rules, then automate only the data pulls that remove obvious manual drag. After a chargeback, the branch is clear: accept it or defend it.

Do not defend everything. Booked chargebacks can carry fees, and weak cases consume analyst time without improving recovery. Start with reason categories where evidence quality is repeatable, keep exceptions narrow and named, and prevent one-off overrides from breaking queue discipline.

If volume is growing, move from console-only handling toward API- and webhook-driven intake. High-volume handling is better suited to API-based processing, and webhook events are a documented way to track status changes. Each intake event should create or update exactly one internal case, with provider reference or event code stored for auditability.

By day 60. Reconcile operations and finance together#

Before you add advanced routing, put reconciliation in place by day 60. Disputes affect both operations and finance: chargebacks can debit the payment amount plus a processing fee, and successful defenses can return funds.

By day 60, reconcile on a schedule:

- provider outcome

- internal case state

- ledger posting

If provider outcomes and ledger effects do not match, fix that gap before adding routing complexity.

Days 61 to 90. Optimize routing with measured outcomes#

In days 61-90, optimize routing and tool decisions using measured outcomes, not vendor claims. Prioritize by deadline risk, evidence completeness, and observed win/loss history by category.

If a segment keeps losing despite timely handling, tighten concede rules there and reallocate analyst time to cases where evidence changes outcomes. Make vendor or build decisions only when your baseline is stable across backlog aging, evidence-submission completeness, reconciliation accuracy, and analyst touch time per case.

Add a monthly stop-go gate alongside weekly governance. Visa evaluates dispute and fraud performance monthly, and entities above thresholds can be required to implement mitigation measures. Internally, if backlog aging worsens in any monthly check, pause new automation scope and fix data quality first. Monitoring programs do not depend on whether some disputes are eventually won, and your build sequence should not either.

Related reading: How to Build a Global Accounts Payable Strategy for a Multi-Country Platform.

Before expanding automation scope, map your dispute lifecycle to idempotent events and ledger reconciliation patterns in the Gruv docs.

Avoid the mistakes that make dispute programs fail#

Once your baseline is stable, many dispute programs break down in four places: weak prioritization, premature staffing cuts, thin KPIs, and unclear ownership. Fix those before adding more automation.

Do not prioritize all chargebacks the same way#

Do not treat all chargebacks as equal priority. Route by deadline risk and evidence readiness, because dispute categories require different evidence and response handling, and response windows are usually 7 to 21 days depending on the card network.

Use a fast queue check: in a sample of open cases, confirm each has one due date, one dispute category, and one evidence status. Missing the response deadline is a hard failure because you automatically lose the dispute and cannot recover the funds.

Do not cut analyst capacity too early#

Do not assume SaaS adoption immediately reduces analyst capacity. Tooling can help collect and submit evidence, but your team still decides whether to accept or challenge each case, and the issuer bank still decides the outcome.

Keep overlap staffing until manual exception work is consistently low. If analysts are still cleaning evidence, reassigning ownership, or resolving duplicate cases after go-live, you have shifted work, not removed it.

Do not run the program on win rate alone#

Do not run the program on win rate alone. Won and lost disputes both count toward dispute-rate exposure, and disputes can arrive up to 120 days after payment.

Track dispute activity separately from dispute rate, and do not apply one scheme's threshold to every network just because one provider flags 0.75% as excessive activity.

Do not leave ownership ambiguous#

Do not leave ownership ambiguous between merchant support and finance ops. Assign one accountable owner for each lifecycle stage, especially for the accept-or-challenge decision.

Document ownership for intake, evidence approval, submission, and reconciliation, and confirm liability setup on connected accounts so it is clear whether the platform or the connected account responds. If current ownership is unclear, that case is already at risk.

Conclusion#

Your edge is disciplined operations, not a single tool. Clear ownership, explicit fight-or-concede rules, reliable evidence, and deadline control matter more. For each case in NEEDS_RESPONSE, your team should know immediately who decides, what evidence is required, and how the ledger changes if you lose, concede, or recover.

- Define dispute terms and owners across your core teams.

Use one shared dispute glossary and assign a named owner for each decision point. Validate this with recent cases: each one should show an intake owner, a fight-or-concede owner, and an escalation contact. If disputes sit in unrelated queues, decisions slow down and outcomes can degrade.

- Publish lifecycle states with response clocks, blockers, and escalation paths.

Document the path from intake to triage, evidence collection, submission, ruling, and reconciliation, and map actions to states like NEEDS_RESPONSE and ACCEPTED. Keep deadline handling explicit: dispute response windows are often 7 to 21 days, and missed deadlines can auto-lose the case. If you run PayPal-style inquiry flows, track the separate 20-day inquiry window so cases do not age out.

- Implement fight, concede, and escalate rules with evidence quality gates.

Write the rule down so analysts are not relying on instinct alone. Defended cases should include the evidence pack submitted; conceded cases should record why they were accepted. The operational goal is simple: strong files get worked on time, weak files do not consume deadline capacity.

- Choose tooling with a buy-build table, not vendor promises.

Evaluate tools on operational fit: deadline visibility, evidence collection support, analyst override controls, and outcome data for reconciliation. Automation can help execution, but your team still has to evaluate each dispute and choose the response. If a tool cannot show the full flow from alert to evidence submission to ledger outcome, treat it as unproven.

- Reconcile every dispute outcome to ledger impact and a regular KPI review.

A case is not done when a provider marks it closed. Confirm dispute debits and recoveries match settlement and internal loss reporting. Review a KPI set on a regular cadence, for example weekly: new disputes, backlog aging, response timeliness, evidence completeness, handling time, and net loss after recovery.

- If useful, reassess at day 30, 60, and 90 before scaling automation scope.

Use these checkpoints as operating reviews, not a universal standard. At day 30, verify ownership and state discipline; at day 60, test whether fight and concede rules reduce avoidable work; at day 90, decide whether more automation is justified. If aging or reconciliation worsens, pause expansion and fix data quality first.

If you want a platform-specific review of dispute operations, payout controls, and audit readiness, talk with Gruv.

Frequently Asked Questions

What should a platform operator do first when payment disputes spike?

Start with triage, not new tooling. Check every open case for dispute category, response deadline, and evidence status, then review the response guidance for that category before building a defense. Validate that staff alerts are firing for new disputes, because missing a deadline can automatically forfeit the case.

Should we fight every chargeback or concede some quickly?

No. Defend disputes where you have sufficient compelling evidence, and concede when required defense documents are missing or do not meet defense requirements. Prioritize strong cases so they do not age into deadline failures while analysts work weak files.

When is third-party dispute automation worth it for a growing platform?

Automation is usually most useful when evidence collection, alerting, and submission handling are slowing response execution. If ownership is unclear or data quality is weak, tooling is less likely to help on its own. For Stripe users, Smart Disputes is built in with no extra integration, and Stripe Apps provides third-party dispute-management options.

Who should own dispute decisions: support, risk, finance, or payments ops?

Team names matter less than clear accountability. Assign one owner for the concede-or-fight decision and one owner for post-resolution reconciliation, with support, risk, and finance feeding required inputs. Keep final ownership explicit in marketplace setups, because the platform can be ultimately liable for chargebacks and related costs.

Which weekly metrics actually predict dispute loss risk?

Track deadline aging, evidence completeness by reason category, dispute activity, handling time, and reconciliation accuracy between provider outcomes and your ledger. Win rate alone is not enough because all disputes count toward dispute-rate math whether won or lost. Also keep exposure tracking scheme-specific: dispute activity benchmarks and VAMP monitoring are not the same metric, and thresholds can change over time.

How do we decide between Stripe-native dispute tooling, an external SaaS, and internal tooling?

Separate payment-risk prevention from dispute-response operations before choosing a path. For lower implementation effort inside Stripe, start with Stripe-native dispute tooling like Smart Disputes; for broader vendor coverage, evaluate third-party apps; for custom routing and evidence workflows, use the Disputes API plus webhooks. Choose internal tooling only if your team can reliably handle webhook events and ledger reconciliation.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- consumerfinance.gov/ask-cfpb/how-can-i-get-a-refund-on-a-product...trusted

- docs.stripe.com/disputes/respondingtrusted

- docs.stripe.com/connect/marketplace/tasks/refunds-disputestrusted

- it.cornell.edu/it-service-management/raci-and-rasci-definit...trusted

- stripe.com/guides/introduction-to-payment-disputestrusted

- stripe.com/resources/more/representment-explainedtrusted

- checkout.com/docs/payments/process-disputes/dispute-reaso...external

- developer.visa.com/capabilities/visa-resolve-onlineexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments

If you own compliance, legal, finance, or risk for a platform paying foreign contractors, sellers, or creators, you may need to make **Form 1042-S** operational. That means clear decisions, reliable checks, and escalation points your team can apply and defend.

What Is Dunning? A Platform Operator's Guide to Recovering Failed Recurring Payments

Dunning management is an accounts-receivable process for recovering overdue balances. In recurring billing, it also covers failed-transaction notices and overdue-payment reminders. For platform teams, that means dunning is not an ad hoc email task. It is an operating process with clear triggers, owners, and end states.

State of Platform Payments Benchmark Report for B2B Marketplace Expansion

This article translates broad payments narratives into expansion decisions: where a B2B marketplace operator should launch first, what to delay, and what to validate before committing product and GTM budget in 2026.