Quick Answer

Start by selecting the operating model for your global accounts payable strategy multi-country platform, then sequence controls and execution in phases. The article recommends deciding between a single multi-entity setup and a modular AP+FX+payout design before tool optimization. From there, standardize approval gates, map currency paths, and run a 90-day implementation with named owners across finance, product, and engineering. Success is verified through traceable status from invoice receipt to settlement and accounting export.

What a global accounts payable strategy needs to cover#

Multi-country AP can break for a simple reason: payment volume grows faster than control design. Once invoices and supplier payouts move across multiple countries, you are no longer solving a basic back-office task. You are deciding how approvals, compliance checks, FX handling, and settlement visibility will work across entities with different tax filings, bank accounts, vendor relationships, and sometimes separate ERP instances.

That is why a multi-country AP strategy should start with architecture, not invoice intake screens or a shortlist of automation features. On paper, international accounts payable is still just unpaid foreign supplier invoices. In practice, the operating burden changes fast once those invoices trigger cross-border payments. Without automation and global payments support, the process gets more costly, riskier, and harder to see. The first red flag often appears when finance cannot explain where an invoice sits, who approved it, which entity owns it, and what currency will actually settle.

The governance problem sharpens as you add entities. AP localization is not just language support or local invoice formats. In practice, it becomes a financial governance issue, especially when a business is operating in 20+ countries at once. Headquarters still needs consolidated AP visibility, ideally normalized into a reporting currency, without waiting for month-end close to understand exposure. If you cannot pull that view today, scaling risk may already be showing up in reporting lag, exception handling, and manual reconciliation.

The first real choice is where you want complexity to live: inside one multi-entity AP platform, or across a modular stack with separate AP, FX, and payout layers. Neither pattern is automatically better. A tighter platform can reduce coordination overhead when your team does not want to own deep payments engineering across compliance, FX, and settlement. A modular stack can give you more control when payment logic is part of the product, but it also creates more integration points to monitor, test, and reconcile.

Use a simple checkpoint before you go deeper. If finance, product, and engineering cannot agree on one status trail from invoice receipt to approval to payout to ledger export, pause expansion and fix that first. That shared view matters more than almost any feature comparison. This guide is built to help you make that call, then sequence the next phases so controls, tooling, and payout operations mature together instead of drifting apart.

Related: Finance Automation and Accounts Payable Growth: How Platforms Scale AP Without Scaling Headcount.

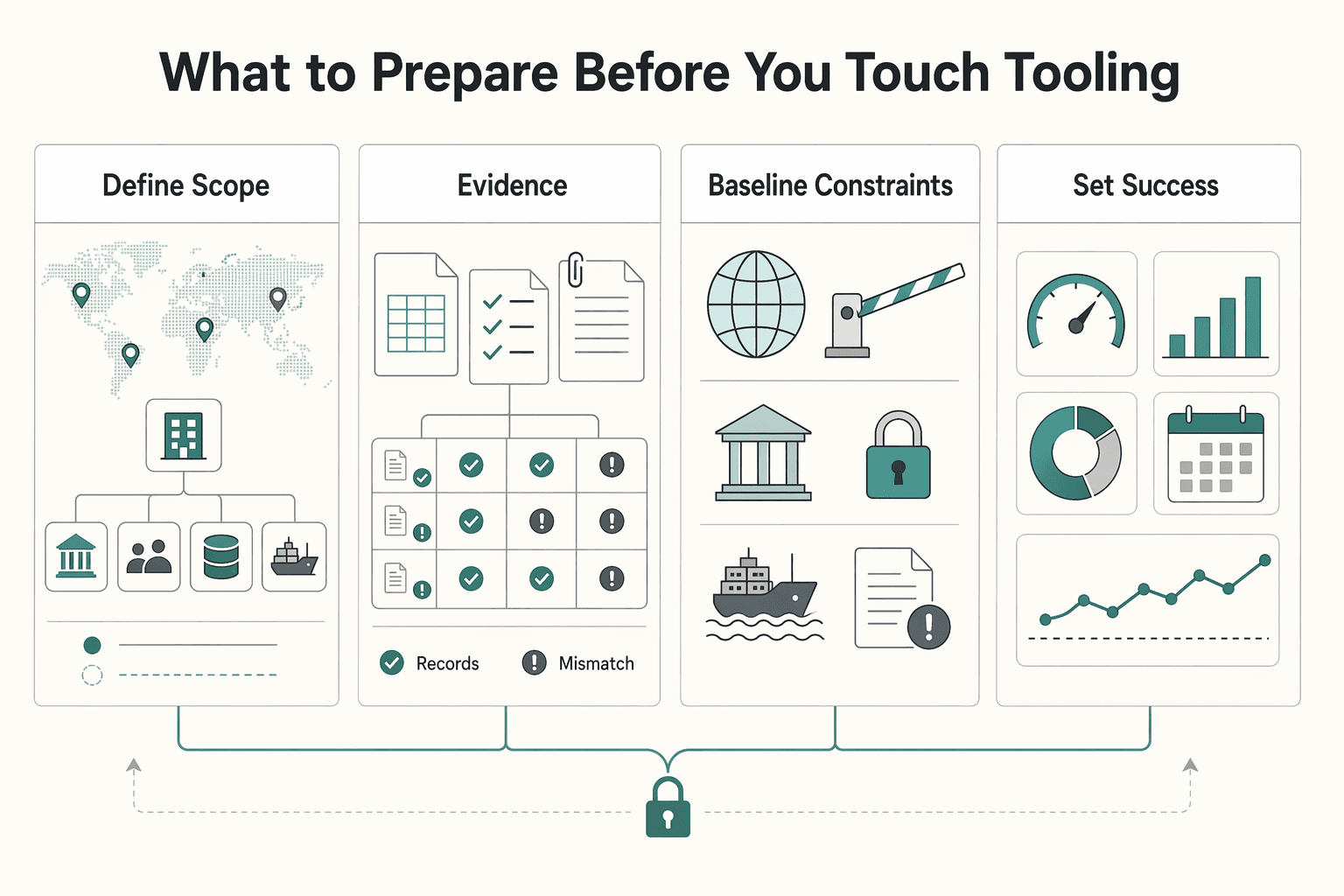

What to prepare before you touch tooling#

Before you evaluate tools, lock four things in writing: scope, evidence, market constraints, and KPI baselines. Otherwise, automation preserves data silos and invoice exceptions instead of fixing them.

| Step | Focus | What to capture |

|---|---|---|

| Define scope in writing | Build an entity map | Name each legal entity, bank-account owner, vendor owner, ERP instance, and active payout corridor; mark where international invoicing is required versus optional; map each invoice source to one owning entity and one approval path |

| Assemble the evidence pack | Collect current approval paths, ERP integration points, and open exceptions in supplier payouts | Include a sample of delayed or failed invoice flows and identify where controls rely on PO checks versus three-way matching |

| Baseline constraints by market | Document applicable tax, currency, and e-invoicing requirements by market | Record the owner and current workaround for each open gap |

| Set success criteria before demos | Define baseline KPIs for cycle time, exception rate, and cash-flow visibility | Name the system of record for each metric; if exception aging is not measurable today, treat that as a first-phase requirement |

Step 1. Define scope in writing. Build an entity map that names each legal entity, bank-account owner, vendor owner, ERP instance, and active payout corridor. Mark where international invoicing is required versus optional. Every invoice source should map to one owning entity and one approval path.

Step 2. Assemble the evidence pack. Collect current approval paths, ERP integration points, and open exceptions in supplier payouts. Include a sample of delayed or failed invoice flows and identify where controls rely on PO checks versus three-way matching, since goods receipt is a distinct verification point. This shows where disconnected process risk is already showing up.

Step 3. Baseline constraints by market. Document applicable tax, currency, and e-invoicing requirements by market, plus the owner and current workaround for each open gap. Multi-entity AP often spans different tax, banking, vendor, and ERP setups, so centralized visibility only works when local compliance gaps are explicit.

Step 4. Set success criteria before demos. Define baseline KPIs for cycle time, exception rate, and cash-flow visibility, and name the system of record for each metric, for example ERP timestamps, approval logs, or payout-status data. If you cannot measure exception aging today, make that a first-phase requirement.

For a step-by-step walkthrough, see Accounts Payable vs Accounts Receivable for Freelancers.

Choose your architecture before you optimize processes#

Choose the architecture that fits your operating risk first, because your process improvements will inherit its constraints. If you do not have deep payments engineering and you operate across broad jurisdictional compliance exposure, bias toward a tighter multi-entity AP platform. If your product depends on custom payment logic and component-level control, use a modular stack and plan for more integration ownership.

You have two viable patterns: a single multi-entity AP platform, or a stack with separate AP, FX, and payout layers. Consolidation usually means fewer systems to coordinate, which can reduce data mismatches and status gaps. Modular design gives you more control to add, replace, or upgrade components without rewiring the whole stack, but only if interfaces and ownership are clean from the start.

| Criteria | Single multi-entity AP platform | Modular AP + FX + payout stack | What to verify |

|---|---|---|---|

| ERP fit | Strong when ERP is the system of record and you want fewer side tools | Strong when your team can own stable interfaces across tools | Reconcile invoice, approval, and payout status back to ERP without manual patching |

| AP automation depth | Often tighter in one platform | Depends on vendor mix and integration quality | Test PO, two-way, and three-way match on real exception cases |

| Failure visibility | Simpler when fewer systems hold state | Strong only with a shared status model across layers | Trace each case end-to-end from intake to settlement |

| Approval flexibility | Good for standard finance controls | Better for custom product/entity logic | Confirm entity-specific approval rules and overrides work cleanly |

| Ownership of cross-border payments risk | More risk handled inside one platform boundary | More risk handled by your team across providers | Assign owners for retries, blocked beneficiaries, and settlement mismatches |

Do not choose on launch speed alone. Some API-first providers claim faster implementation, including claims like up to 66% setup-time reduction, but those are vendor claims, not guaranteed outcomes. Use your own evidence pack and exception history as the decision test.

Before committing, run one proof test with three real cases: a clean invoice, an approval exception, and a failed or delayed payout. Choose the option where ownership, current state, and audit evidence are clear at each handoff.

Finally, price the cost of change, not just the cost to launch. Replacing fragmented rails later is often harder than slower initial standardization, while modular flexibility pays off only when contracts, data models, and status handling are truly decoupled from day one. If useful, see Internal Controls for Accounts Payable on Platforms: How to Prevent Fraud and Ensure Accurate Disbursements and try the free invoice generator.

Design a control model that survives audits and scale#

Once your architecture is set, lock the control spine before adding countries: keep one global approval model, and allow only documented local overlays for compliance standards, tax laws, and e-invoicing mandates.

Step 1. Standardize one approval spine, then layer local rules on top. Build one approval matrix across entities by amount, spend type, and role. Treat local variation as an overlay, not a separate workflow. If a country needs tax review before posting or extra e-invoicing checks, add it as a named branch in the same logic.

Use a drift check: test the same invoice amount and supplier type across three entities. The route should match unless a written local rule changes it, and that rule should be traceable in your policy register.

Step 2. Put hard gates in front of supplier payouts and keep immutable evidence. Do not treat approval and payout as loosely related events. Before release, require policy gates: approved invoice state, correct approver level, beneficiary verification status, and any required compliance review.

Your audit evidence should let you reconstruct the decision: invoice record, approval timestamps, approver identity, rule outcome, payout release event, and the supplier bank-detail version used at release. If payout can still be run manually outside that path, the control model is weaker than it looks.

Step 3. Add tax-reporting steps early when your structure makes them relevant. If your setup includes foreign financial assets or offshore account relationships that may affect U.S. reporting, assign finance or tax ownership at account opening and at any material change.

IRS guidance states certain U.S. taxpayers with foreign financial assets generally report using Form 8938, and Form 8938 is attached to the annual tax return. Do not hardcode one threshold for every filer: IRS notes a general $50,000 threshold for certain U.S. taxpayers, while Form 8938 instructions also reference $75,000 at any time during the tax year for specified domestic entities, and thresholds may be higher in some cases. Compare Form 8938 and FBAR (FinCEN Form 114) requirements because some cases require one or both. Also, Rev. Proc. 2020-17 does not remove section 6038D reporting obligations. Penalties can start at $10,000 and rise up to $50,000 for continued failure after IRS notification.

Step 4. Define exception classes and assign one owner to each. At minimum, define invoice mismatch, blocked beneficiary, stale approval, and unresolved compliance review. Each class needs a named owner, response clock, exit rule, and required evidence before release or closure. If exceptions can bounce between AP, payments, and compliance without a decision owner, they will age silently and resurface as payout failures or quarter-end escalations.

Build the currency and settlement model to prevent margin leakage#

Currency design is a margin control. Make collection, conversion, and settlement choices explicit, or you will absorb avoidable FX cost and reconciliation noise.

Step 1. Map every collection-to-payout path. For each country or supplier corridor, document one path from customer payment to supplier disbursement: collection currency, whether you use multi-currency acquiring, conversion timing, settlement currency, and payout currency. Multi-currency payment processing gives you flexibility to accept, process, and settle in multiple currencies, but only if each path has a defined rule.

Run a hard check on a small set of high-volume corridors: can your team answer, without provider back-and-forth, where you collect, where you settle, and where conversion occurs? If the answer is "processor default," the path is not designed yet.

Step 2. Choose like-for-like settlement where it removes unnecessary conversion. If you collect in a currency you also need downstream, keep funds in that currency where possible. Like-for-like settlement reduces forced conversion between intake and disbursement and can lower avoidable FX friction.

The tradeoff is operational. Some setups let customers pay in local currency while you receive a preferred base currency, often with pre-agreed rates or added fees. That can work when liabilities are mostly in the base currency, but it is inefficient if you convert at settlement and then convert again before payout.

Step 3. Define quote controls before you automate conversion. Set FX controls first: reject stale quotes, define approved conversion windows, and require each FX event to reconcile to ledger output. Your evidence pack should include source amount and currency, quote timestamp or reference, applied rate, converted amount, settlement currency, and resulting ledger entry.

This matters because settlement can land one to three business days later depending on provider and geography. Without event-to-ledger reconciliation, AP, treasury, and finance will end up working from different numbers and closing manually.

Step 4. Decide treasury policy first for mismatched currency exposure. If liabilities are mainly in EUR and revenues settle in GBP, set treasury policy before building automation. Decide whether conversion happens on receipt, on a schedule, or under another approved rule, then automate triggers and gate manual overrides behind approval.

Your verification check is simple: can an approved EUR payout move without ad hoc spreadsheet rate-shopping? If not, the model still depends on manual judgment and leaves margin exposed.

Execute a 90-day build sequence with named owners#

If you run this in 90 days, treat the timeline as an internal execution framework with explicit ownership, not as a universal benchmark. The goal is to avoid moving architecture, controls, and product behavior at the same time without clear decision rights.

Step 1#

Days 1-30: lock architecture and ownership before automation. Document the end-to-end flow by entity and country, then assign one owner to each decision area before implementation starts.

- Finance owns control requirements and evidence fields.

- Product owns user states and operational behavior.

- Engineering owns interface contracts, idempotent processing, and alerting.

Step 2#

Days 31-60: implement approvals, AP automation, and payout status visibility. Make status traceable across approvals, payout execution, and accounting output so operations can follow one flow end to end.

For fixed recurring obligations, automate where the payment amount and timing are stable. Standing orders are pre-authorized instructions for recurring fixed or calculated payments, often on intervals such as weekly, monthly, or quarterly. They can reduce manual processing work, improve cash flow predictability, and help avoid late fees, but they are a poor fit when approvals, amounts, or beneficiary details change frequently.

Step 3#

Days 61-90: harden production with reconciliation and exception drills. Before rollout is considered complete, validate that the same transaction set can be traced through request, approval, payout event, settlement result, and accounting export, including non-happy-path scenarios.

Keep ownership visible in incident handling: finance approves controls, product approves state behavior, and engineering owns reliability signals and recovery paths.

For the full breakdown, read The Best International Bank Accounts for Global Citizens.

Track the KPIs that prove the strategy is working#

Use one shared KPI scorecard across finance, product, engineering, and operations to confirm whether the strategy is working. If each team reports performance differently, you lose the visibility KPIs are meant to create. For a multi-country AP operation, keep the core set: invoice-to-approval time, payout success rate, exception aging, and close-cycle predictability.

Step 1#

Define one scorecard and tie each KPI to an operating outcome.

| KPI | What it should reveal | Why it matters |

|---|---|---|

| Invoice-to-approval time | Where approvals are slowing | Spend control and workflow speed |

| Payout success rate | Whether supplier payouts complete without avoidable failures | Reliable supplier payouts |

| Exception aging | What unresolved work is building up | Manual intervention and rework risk |

| Close-cycle predictability | Whether accounting output stays stable | Cash flow management quality |

For each KPI, name the owner, source record, and expected action. If payout success drops and no one can separate blocked beneficiaries, stale approvals, and bad beneficiary data, the metric is too broad to manage.

Step 2#

Use the scorecard to reduce error-prone work, not just report volume. Monitoring AP KPIs helps surface errors, and payment-process automation can improve cash-flow visibility and on-time payment records. In day-to-day operations, that should show up as fewer inbox chases, fewer manual retries, and less rework across approvals, payout events, and ERP posting.

Watch for mixed signals. If disbursement volume looks healthy while exception aging rises, pause expansion and fix the break in approvals, data capture, or payout handling.

Step 3#

Run recurring control and architecture checks so the KPI trend is practical. In control reviews, test transaction samples against your compliance standards and confirm the evidence pack still includes request, approval, payout event, settlement result, and accounting export. In architecture reviews, compare growth plans against the current entity map, payout corridors, ERP steps, and local invoicing requirements.

Focus on operating drift, not just trend lines. If new countries or entities require workarounds outside the shared status model, the design is fragmenting.

Fix common failure modes before they become chronic#

AP issues usually get expensive when control design drifts, not just when volume grows. Fix this early by keeping local requirements aligned to workflow controls, enforcing one shared status model from invoice through payout, and keeping reconciliation evidence consistent from request to export.

Step 1#

Review local requirements regularly and map each change to a control point. In multi-entity operations, drift starts quietly: one entity changes invoice fields, another changes beneficiary-data capture, and a third routes payments outside the documented path.

Focus reviews on the local factors most likely to fragment execution: tax laws, currency regulations, and e-invoicing mandates. Then map each change to where it affects work: invoice intake, approval rules, payout eligibility, or ERP export. Standardized workflow documentation only works if it is updated when the process changes.

Step 2#

Enforce one status model across AP automation, FX, and payout events. Fragmented visibility is a common AP failure mode: finance may see "approved," while payments sees "blocked," and treasury sees "pending."

Use one end-to-end status chain such as request, approval, payout event, settlement result, and accounting export. The labels can vary, but consistency cannot. You should be able to trace a transaction without pulling updates from multiple teams; otherwise delays, vendor friction, and missed timing benefits follow, even when rails can settle obligations in seconds rather than days.

Step 3#

Standardize the evidence pack so reconciliation stays manageable as you scale. Regular reconciliation and review are core AP best practices, especially across entities. Keep a consistent minimum pack for each transaction path: request, approval, settlement result, and accounting export. If FX is involved, include the conversion record.

Backlogs usually grow when entities store different proof or exceptions are handled in inboxes and spreadsheets. During close, sample exceptions and confirm each has an owner, a reason code, and enough evidence to resolve without rebuilding the case manually. If exceptions are growing and controls are not keeping up, treat that as a scale warning and stabilize operations before expanding further.

For a practical guide to managing multi-country payables with a lean team, read International Accounts Payable for Platforms: How to Manage Multi-Country Payables Without a Global Finance Team.

Conclusion#

The goal is not faster automation for its own sake. It is sequencing the hard decisions in the right order: choose architecture first, lock controls second, then build and expand at a pace your team can verify.

That matters because cross-border payments still carry recurring risks the 2024 FSB progress report highlights: high cost, slow speed, insufficient access, and weak transparency. A multi-country AP platform is more likely to hold up when you reduce those risks through explicit ownership, visible status, and audit trails, not when you simply add more payout coverage.

- Confirm the architecture and owner set.

Decide whether one multi-entity AP platform or a modular stack will own invoice intake, approvals, FX decisions, payout execution, and accounting export. Your verification point is simple: one invoice should be traceable from approval to settlement result to accounting output without asking multiple teams to reconstruct the path. If you cannot do that before launch, the visibility gap is already signaling where scale is likely to break.

- Finalize country requirements and map them to named control gates.

Write down where international invoicing is required and which entities face local tax, currency, or invoicing requirements, then define exactly where each rule enters the process. The check here is whether every local requirement attaches to a field, approval gate, beneficiary check, or export record. If a rule lives only in someone's memory or in a local spreadsheet, you increase the risk of compliance drift and exception-driven work later.

- Implement AP, FX, and payout handling with shared status visibility.

Build one status model across approval, conversion, settlement, and reconciliation so finance and operations see the same truth. When you connect tools, choose the integration method deliberately: API if you need real-time processing, bank feeds if your setup is simpler and timing tolerance is wider. Automation can improve accuracy, speed processing, and simplify currency conversion handling, but it does not replace monitoring or audit trails.

- Instrument KPIs and recovery paths before volume rises.

Track invoice-to-approval time, payout success rate, exception aging, and close-cycle predictability from the start, not after the first messy month-end. Also define recovery owners for blocked beneficiary, stale approval, invoice mismatch, and unresolved compliance review. A strong checkpoint is whether the evidence pack exists for each transaction path: request, approval, settlement result, and accounting export.

- Review quarterly before you add more countries.

Expansion should follow proof, not optimism. If exception volume is growing faster than payment volume, pause rollout and repair the control design first. That is a practical test for whether your global AP strategy, jurisdictional compliance handling, and currency operations are aligned well enough to make scaling cross-border payments predictable instead of reactive.

Related reading: The Best Multi-Currency Accounts for Digital Nomads and Freelancers.

Frequently Asked Questions

What is a global AP strategy for a multi-country platform in practical terms?

It means one operating model for invoice intake, approval, payout, and reconciliation across entities, with local overlays where compliance requirements require them. It is not just translation or country-specific UI. Once you are dealing with 20+ countries, AP localization becomes a governance question: centralized visibility plus local compliance handling.

Should we choose one multi-entity platform or a multi-vendor payment stack?

If your bigger risk is fragmented visibility, manual handoffs, and uneven compliance handling, a single multi-entity AP platform is often the simpler choice. A multi-vendor stack can work if you have clear product reasons to separate AP and payouts and can reliably manage the integration points. A quick test is whether you can trace one invoice from approval to settlement result to accounting export without asking multiple teams.

What should we complete in the first 90 days to avoid rework?

Finish architecture and country scope early, not after launch pressure hits. In the first phase, lock the tool pattern, confirm ERP interfaces, and document international invoicing needs. Next, implement approval routing and core AP automation steps such as invoice digitization, matching, and payment processing. Then harden reconciliation/reporting, exception handling, and payout status tracking so teams are not rebuilding controls later.

How do we reduce FX leakage without slowing supplier payouts?

Decide conversion timing before you automate payouts, and use a consistent treasury rule instead of ad hoc conversion at payment time. Also check destination-country payment method coverage first, because not all methods are available everywhere and global ACH is not universal.

Which KPIs best show whether global AP operations are healthy?

Track one shared set across finance, operations, and payments: invoice-to-approval time, payout success rate, exception aging, and close-cycle predictability. These can show whether AP automation is reducing manual intervention across invoice digitization, matching, approval routing, payment processing, and reconciliation/reporting. If exception volume grows faster than payment volume, treat that as a stop signal for expansion.

What usually breaks first when scaling AP across new countries?

A common failure point is local rule drift. One entity changes required invoice details, another applies different beneficiary checks, and a third pays outside the documented path, so controls stop matching reality. Manual processes make this worse because they raise the risk of errors, fraud, and inefficiency at exactly the point volume is rising.

How do we keep local compliance needs from fragmenting global operations?

Keep the global core fixed and localize only at named control points. Non-negotiable controls should remain consistent, while local changes attach only to the field, gate, or export record affected by a country requirement. If a local requirement cannot be mapped to a specific control point, it will likely become exception-driven work later.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- appropriations.senate.gov/download/fy26-homeland-jestrusted

- cms.gov/regulations-and-guidance/guidance/manuals/do...trusted

- docs.house.gov/meetings/RU/RU00/20260303/118842/BILLS-1192i...trusted

- ecb.europa.eu/press/annual-reports-financial-statements/an...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- irs.gov/businesses/corporations/fatca-information-fo...trusted

- irs.gov/forms-pubs/about-form-8938trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC10072045trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

International Accounts Payable for Platforms: How to Manage Multi-Country Payables Without a Global Finance Team

Running **international accounts payable platforms multi-country without global finance team** is first a control decision, not a tool-shopping exercise. The real choice is where approvals live, who owns payout execution, and how you prove each payment during close or review when something goes wrong.

How Platform Teams Scale AP Volume Without Adding Headcount

Use this as a decision list for operators scaling Accounts Payable, not a generic AP automation explainer. In these case-study examples, invoice volume can grow faster than AP headcount when the platform fit is right, but vendor claims still need hard validation.

Internal Controls for AP Platforms to Prevent Fraudulent Disbursements

Start here: your AP control design should reduce fraudulent disbursements and payment errors without turning every payout into a bureaucratic exercise. In practice, that means clear escalation points at the moments where money can move incorrectly, not extra approvals added just to look controlled.