Quick Answer

Build AP internal controls around the payment lifecycle: risk-tiered vendor onboarding, hard invoice validation before queue entry, segregated approvals, and pre-release payment authorization checks. Then add detective monitoring and a rule-based escalation matrix for monitor, hold, block, or legal/compliance review. For platforms handling cross-border payouts, require legal and compliance sign-off by corridor and keep a complete audit trail so each decision is reconstructable.

Internal controls for AP on platforms start with one promise#

Step 1 Define the promise#

Start here: your AP control design should reduce fraudulent disbursements and payment errors without turning every payout into a bureaucratic exercise. In practice, that means clear escalation points at the moments where money can move incorrectly, not extra approvals added just to look controlled.

Accounts Payable (AP) internal controls are the policies and procedures used to prevent fraud, reduce human error, and improve payment accuracy. That matters here, but keep the promise realistic. Good controls provide reasonable assurance against unauthorized asset misuse and support prompt detection and correction. They do not eliminate risk, and they should not pretend to.

Use an early checkpoint: can your team say, in a single sentence, what happens when a payout looks wrong? If the answer is vague, routed through inboxes, or depends on who is online, you do not have a control point yet. You have discretion, and that is where both fraud and avoidable errors can hide.

Step 2 Set the scope for platform payouts#

This article focuses on AP for contractor, seller, and creator cross-border payouts. That includes the full payout path, from payee setup and payment approval through release and reconciliation, where a platform is sending funds across markets and needs clean handling of both fraud risk and operational mistakes.

The cross-border piece matters more than many teams expect. These payment operations sit inside several national and regional legal, data, and regulatory regimes, so a control design that works in one market or program should not be copied blindly into another. If you support multiple payout corridors, get legal and compliance sign-off before treating any jurisdiction-specific rule as standard.

Before you redesign anything, verify three basics for each payout lane: the market or corridor, the program or entity making the payment, and the legal or compliance owner who must review local requirements. One failure mode is building one global rule set that looks efficient on paper but is wrong for a specific corridor. That can create either release delays or compliance exposure.

Step 3 Use the right outputs from the start#

The rest of this article is operational: a lifecycle control model, a reporting checklist, and decision rules for when to block, hold, release, or escalate. That is the working set you need if you want controls that Finance, Risk, and Payments Ops can actually use under pressure.

The tradeoff is straightforward. Cross-border payout programs are usually under pressure to improve speed, transparency, access, and cost, but speed without decision rules can let bad payments get released. The goal is not maximum friction. It is explicit handling: low-risk payments move cleanly, suspicious ones pause in a defined place, and the highest-risk cases escalate with evidence attached.

Keep that promise in view and the rest of the design gets easier to judge. Every control should answer one question clearly: does it prevent a bad payment, catch one quickly, or tell the operator exactly when to stop and ask for help?

You might also find this useful: Accounts Payable vs Accounts Receivable for Freelancers.

What to prepare before you redesign AP controls#

Before redesigning anything, lock four basics: named owners with delegated authority, separation of duties at key payout steps, current evidence artifacts, and clear success criteria with monitoring and response rules.

| Step | Focus | Key requirement |

|---|---|---|

| Assign owners and authority | Control points where a payout can be created, approved, or released | Assign one accountable owner with clear authority to approve, stop, or escalate |

| Gather current evidence | Current disbursement artifacts | Collect policy documents, exception queues, payout logs, and audit trail exports |

| Split payment paths by risk | Standard invoices, urgent payouts, and high-risk geographies | Define stricter checks where exposure is higher |

| Define success and response rules | Outcome criteria, monitoring, and prompt action | Set outcome criteria upfront and define how you will monitor compliance and what prompt action looks like |

Step 1 Assign owners and authority#

For each control point where a payout can be created, approved, or released (vendor onboarding, approval workflows, payment authorization), assign one accountable owner with clear authority to approve, stop, or escalate. Shared input across Finance, Risk, and Payments Ops is useful, but ownership should not be ambiguous. If one person can update payee details, approve, and release funds, treat that as a separation-of-duties gap to fix before redesign.

Step 2 Gather the evidence you already have#

Collect the current disbursement artifacts: policy documents, exception queues, payout logs, and audit trail exports. Use them to reconstruct the transaction flow from setup through release, including changes, overrides, and approvals. If decisions are happening in chat or email instead of the recorded trail, document that gap explicitly.

Step 3 Split payment paths by risk before writing rules#

Do not apply one control pattern to every lane. Separate standard invoices, urgent payouts, and high-risk geographies first, then define stricter checks where exposure is higher. This keeps lower-risk payouts moving while preserving tighter review where risk is concentrated.

Step 4 Define success and response rules before changes#

Set outcome criteria upfront: fewer unauthorized payments, fewer manual reversals, and faster close with cleaner evidence packs. Also define how you will monitor compliance and what prompt action looks like when noncompliance appears. If you cannot compare before and after using your existing control evidence, delay the redesign until measurement is clear.

Related: What Is Know Your Artist (KYA)? How Music Platforms Stop Streaming Fraud Before It Starts

Map fraud and error risks to the AP lifecycle#

Map risks to exact transaction checkpoints across the AP lifecycle, or the map will not prevent bad payouts. If you cannot name the stage that should stop a failure, the risk map is still too generic.

Step 1 Draw the lifecycle from onboarding through reconciliation#

Map the full payment path: vendor onboarding, invoice intake and validation, approval, payment authorization and release, and reconciliation. Internal control risk assessment should be done at both entity and transaction levels; use the entity view to prioritize higher-risk payout lanes, and the transaction view to pinpoint where a billing scheme or process error can pass through.

Tag each stage for both fraud and simple error. In practice, mark where false or altered invoices can enter, where valid invoices can be altered or paid twice, where unsupported spend can be approved, and where reconciliation would first reveal an incorrect disbursement. If a stage has no tagged risk, the map is likely too loose.

Test the map by tracing one recent disbursement from vendor creation to payment release and identifying which control should stop each bad variant.

Step 2 Attach concrete fraud scenarios, trigger signals, and checkpoints#

Use specific scenario rows, not broad categories. Start with shell company schemes, pay-and-return schemes, and personal purchase schemes. Then define trigger signals and recurring checks tied to those schemes; data-analytics tests are useful for this and are associated with lower fraud losses when used early.

| Scenario | Likely stage | Trigger signals | Control checkpoint that should catch it | Owner | Evidence | Response |

|---|---|---|---|---|---|---|

| Shell company scheme | Vendor onboarding, first invoice | New vendor added shortly before invoice submission; vendor detail changes before first payout; invoice pattern shifts that do not fit the lane | Independent vendor verification before activation, then invoice validation before payment enters queue | Vendor onboarding owner | Vendor master change log, first invoice, approval trail, audit trail export | Hold activation or payment, perform independent review, escalate if mismatch remains |

| Pay-and-return scheme | Invoice validation, disbursement, reconciliation | Altered invoice version, repeat invoice, duplicate amount, duplicate payment, return request after payout | Duplicate and alteration checks before approval, then reconciliation review if a return or credit appears | Invoice validation owner | Invoice versions, duplicate check result, payout log, reconciliation record | Stop second payment, offset or recover funds, review linked invoices for pattern repetition |

| Personal purchase scheme | Approval, post-payment review | Invoice does not match business purpose, support is incomplete, purchase pattern shifts from normal behavior | Support and policy check before approval, then reconciliation review for unsupported spend | Approval owner | Invoice support, approver record, payout log, coding history | Reject or reverse unsupported spend, escalate repeated misuse |

Place the strongest checkpoint at the first stage where the scheme becomes visible. Do not let reconciliation be the first real control for a shell company pattern.

Step 3 Add accountable handling so the map becomes operational#

For each row, define owner, evidence, and response. Owner is one accountable role (not a team label). Evidence is the exact artifact that proves the review happened (for example, vendor change log, invoice image, approval record, or audit trail export). Response is a defined action such as hold, reject, recover, or escalate.

Most failures happen when trigger signals exist but handling is unclear. Alerts without accountable ownership and evidence quickly become noise, and allowing one person to both edit vendor details and release payment can collapse separation of duties.

Before moving to preventive control design, run this map against a small set of historical exceptions: one duplicate-payment case, one vendor-change case, and one unsupported-spend case. If the map does not show who should have caught each case, what evidence should exist, and what response should follow, revise it now.

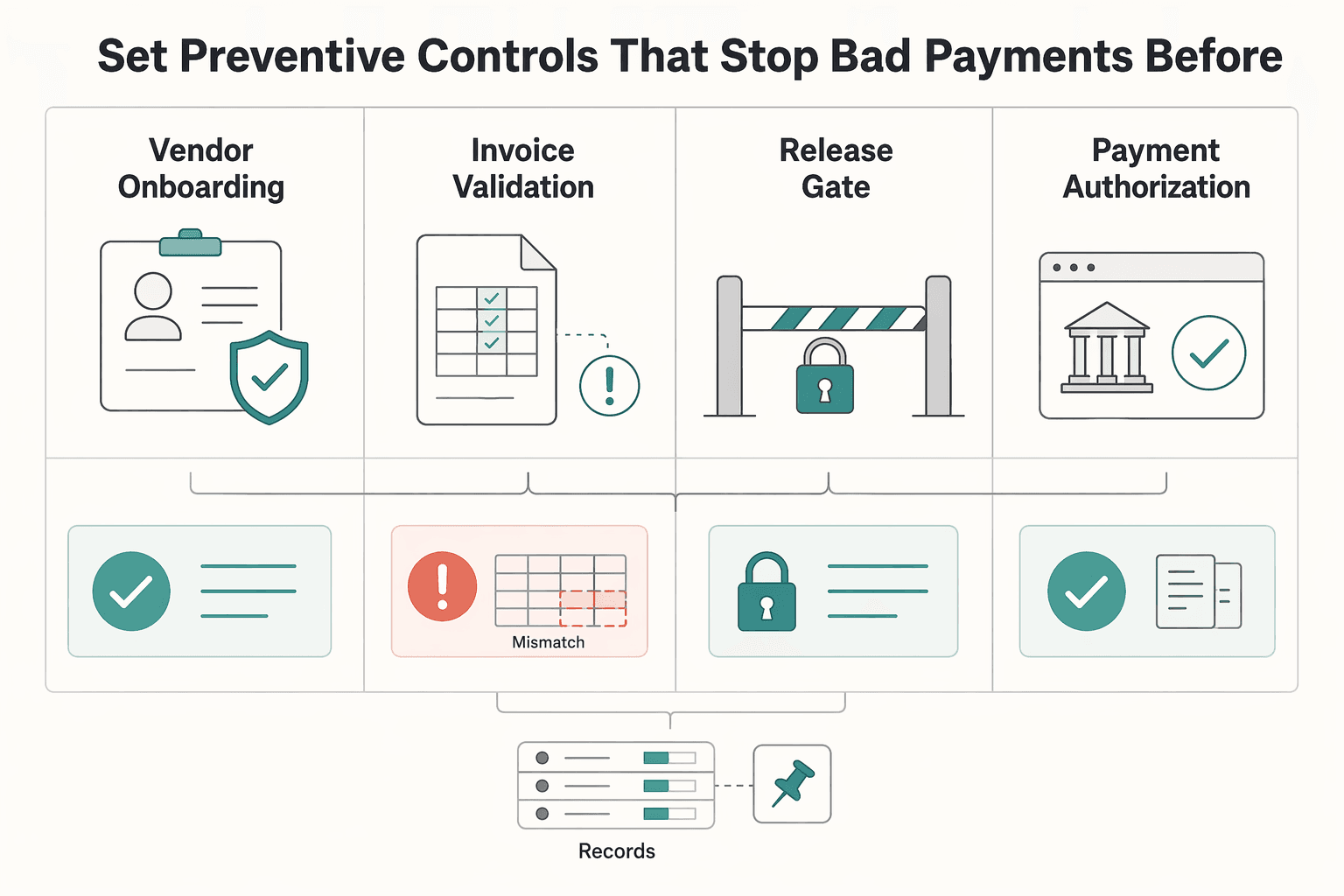

Set preventive controls that stop bad payments before release#

Put your strongest controls before funds are released, not after reconciliation. Treat vendor onboarding, invoice validation, approval, and payment authorization as separate gates with explicit hold-or-pass rules.

| Control point | Before release | If not met |

|---|---|---|

| Vendor onboarding | Scale due diligence to risk, complexity, and exposure; require independent verification for significant changes through a separate communication channel | Keep the payee out of payable status |

| Invoice validation | Require complete invoice content plus receiving evidence or other authorizing documentation before an invoice can move toward payment | Reject or return noncompliant invoices quickly |

| Approval workflow | Increase approval depth with payment risk and keep segregation of duties | The same person cannot edit vendor details, approve the invoice, and release payment |

| Payment authorization | Compare the approved instruction to the actual payment data and keep corridor checks explicit for cross-border flows | Hold requests that breach corridor policy, contain beneficiary/bank-detail mismatches, or lack required support |

Step 1. Tighten vendor onboarding based on payout risk. Scale due diligence to risk, complexity, and exposure instead of treating every payee the same. Apply stronger checks before higher-impact payout lanes go live, and add extra friction for high-impact profile changes, especially remittance detail updates. For significant changes, require independent verification through a separate communication channel before activation or payment release. If the vendor change log is not backed by out-of-band verification, keep the payee out of payable status.

Step 2. Enforce invoice validation before queue entry. Defective invoices should fail fast. A practical benchmark is to require complete invoice content plus receiving evidence (or other authorizing documentation) before an invoice can move toward payment. Reject or return noncompliant invoices quickly instead of leaving them in indefinite suspense. Keep duplicate checks, policy checks, and required support as hard pre-queue requirements.

Step 3. Build tiered approval workflows with segregation of duties. Approval depth should increase with payment risk, while low-risk repeat flows stay efficient. This keeps controls credible without slowing routine disbursements. Separate responsibilities so the same person cannot edit vendor details, approve the invoice, and release payment.

Step 4. Apply payment authorization gates right before release. Before release, compare the approved instruction to the actual payment data and block mismatches. Hold requests that breach corridor policy, contain beneficiary/bank-detail mismatches, or lack required support. For cross-border flows, keep corridor checks explicit because sanctions obligations can apply to both domestic and international payments, even if implementation varies by platform model.

Keep the release evidence pack complete: approved invoice, receiving or authorizing documentation, vendor verification record, approval trail, and release log. Missing artifacts should trigger a hold, not discretion.

For a step-by-step walkthrough, see Subscription Billing Platforms for Plans, Add-Ons, Coupons, and Dunning.

Add detective controls that catch what prevention misses#

Pre-release gates are necessary, but they are not enough. Assume some bad payments will clear, then use detective controls to find them quickly, trace the cause, and prevent repeat failures.

Step 1. Review post-release patterns, not just single exceptions. Focus on recurring anomalies that can indicate fraudulent disbursements or asset misappropriation. Use ongoing monitoring methods such as comparisons, reconciliations, trend analysis, and data analytics to identify improper payments or potential fraud.

Close each anomaly review with a clear disposition: what happened, who reviewed it, and whether it is isolated or part of a pattern. Do not close alerts one by one without checking for repeated links across vendors, approvers, or payout lanes.

Step 2. Tag every exception by where the control broke. Do not keep one undifferentiated queue. Classify exceptions by control point, such as onboarding, invoice validation, approval, authorization, and override, so you can see where controls fail repeatedly.

More than half of occupational fraud cases involve missing controls or control overrides. If flagged payments repeatedly trace to overrides, tighten who can bypass controls and how each bypass is evidenced, and assign corrective-action ownership for each root cause.

Step 3. Automate first-pass detection, then require human adjudication. Use automated monitoring to continuously evaluate controls and transactions and surface velocity or behavior anomalies. Treat unusual payments as triggers for inquiry, not immediate proof of misconduct.

Require reviewer judgment for complex cases by checking support, vendor history, approval rationale, and release context. This keeps alerts useful and reduces avoidable false-positive noise.

Step 4. Preserve an end-to-end audit trail that can reconstruct each payment. Keep audit records long enough to support after-the-fact investigation, and make reconstruction fast. For each flagged payment, retain linked evidence from vendor creation or change through invoice intake, approval, release, return/reversal, and final case notes.

At minimum, keep the change log, approval trail, payment instruction, release log, exception notes, and override rationale tied by transaction or case ID. If records cannot be connected across systems, detective controls break when investigation speed matters most.

Define escalation points with explicit decision rules#

Escalation should be rule-based, not improvised: map each case to monitor, hold, block, or legal/compliance escalation based on unauthorized-payment risk, control-failure severity, and documented evidence.

Step 1. Build the matrix before the next incident#

Use one matrix so every case lands in a defined path:

| Action | Use it when | Minimum evidence | Immediate owner |

|---|---|---|---|

| Monitor | Weak signal, no confirmed control break, no current payment risk | Alert details, transaction ID, reviewer note, next review date | AP or Payments Ops |

| Hold | Reasonable grounds to suspect fraud or dishonesty, investigation still open | Objective factual basis, linked transactions, contact attempts, case owner | Payments Ops with Risk |

| Block | Beneficiary mismatch after approval, unauthorized instruction, or release-gate failure before funds move | Approval record, beneficiary record, mismatch proof, release-stop log | Payments Ops or Treasury control owner |

| Legal/compliance escalation | Suspected BEC, repeated override pattern, significant control deficiency, or possible external reporting duty | Incident summary, affected transactions, control logs, remediation owner, decision record | Legal or Compliance |

If teams keep creating one-off exceptions, tighten the matrix or sharpen the trigger definitions.

Step 2. Make non-negotiable triggers explicit#

Treat these as automatic escalation triggers:

- Suspected Business Email Compromise (BEC).

- Beneficiary mismatch after approval.

- Repeated override patterns.

BEC merits immediate escalation because these requests can appear to come from known sources and look legitimate, while still being financially damaging fraud. If fraudulent transfer is suspected, escalate through banking channels immediately rather than waiting for the next batch review. For deeper BEC detail, see Accounts Payable Fraud Prevention: How Platforms Detect and Stop Business Email Compromise.

For override patterns, escalate the pattern, not just the individual payment. Repeated bypasses indicate a control deficiency that should be remediated on a timely basis.

Step 3. Restrict override authority and log every override#

Define exactly which roles can override holds or blocks, and require explicit delegated authority. If delegated authority is unclear, do not allow the override.

Require a consistent evidence set each time:

- Why the control fired.

- Why release is still requested.

- What records were reviewed.

- Who approved the override.

- What compensating check follows release.

Log the rationale with transaction/case ID, timestamp, approver identity, underlying evidence, and follow-up owner in the audit trail.

Step 4. Keep a regulator-ready incident packet#

For serious suspicious-payout events, maintain a standard packet so you do not reconstruct evidence from inboxes later.

Include at minimum:

- Event timeline from request to release, hold, return, or reversal.

- Affected transactions and counterparties.

- Approval trail and control logs.

- Override history (if any).

- Actions taken to contact the payer or relevant third parties.

- Remediation actions with named owners.

- Legal/compliance review notes.

- Owner sign-off that the record is complete.

In the UK, after the Payment Services (Amendment) Regulations 2024 came into force on 30 October 2024, some outbound APP payments can be delayed for up to 4 business days when there are reasonable grounds to suspect fraud or dishonesty, and no longer than necessary for investigation. Whether or not that specific rule applies to your lane, the control logic is useful: objective factual foundation, bounded delay, documented investigation, and clear ownership.

Implement in phases so controls improve without freezing operations#

Implement in phases to reduce rollout risk: pilot preventive controls in one payout lane first, add detective monitoring after that lane is stable, then expand with idempotent execution and phase checkpoints.

| Phase | Action | Checkpoint |

|---|---|---|

| Pilot one lane | Use one lane in your disbursement flow to validate that controls can prevent unintended payments | Confirm each hold or block is explainable from the audit trail |

| Add detective monitoring | Track and document incidents after the preventive layer is stable | Review exception aging, false-positive rate, release delays, and reconciliation defects |

| Make retries idempotent | Keep one stable idempotency key per payout instruction | Require repeated requests with that key to return the same result |

| Expand lane by lane | Scale to additional cross-border payout paths only after reviewing checkpoint evidence from the prior phase | Pause expansion and tune that lane if noise and delays rise without better case quality or reconciliation outcomes |

Step 1. Pilot one lane with preventive controls first. Start with a small subset rather than changing every payout path at once. Use one lane in your disbursement flow to validate that controls can prevent unintended payments before broader release, and confirm each hold or block is explainable from the audit trail.

Step 2. Add detective monitoring after the preventive layer is stable. A balanced design uses both preventive and detective controls, but staging them helps avoid alert noise early in rollout. Once the first lane is stable, track and document incidents and review:

- exception aging

- false-positive rate

- release delays

- reconciliation defects

Step 3. Make retries idempotent before expansion. Use idempotent retry logic in the disbursement function so retries do not create duplicate movements. Keep one stable idempotency key per payout instruction, and require repeated requests with that key to return the same result.

Step 4. Expand lane by lane after each phase check. Scale to additional cross-border payout paths only after reviewing checkpoint evidence from the prior phase. If noise and delays rise without better case quality or reconciliation outcomes, pause expansion and tune that lane before proceeding.

Common mistakes that create fraud gaps and how to recover#

Most AP fraud gaps come from routine control breakdowns: weak invoice checks, one-size vendor onboarding, unclear escalation, and incomplete records. Fixing these four areas closes many of the highest-risk openings first.

Mistake: relying on approvals without strong invoice validation. Recovery: Put pre-approval checks in front of reviewers for duplicate invoice number, amount, vendor match, and required supporting documents. Approval by itself will not catch bad or repeated data, and billing schemes are a common fraudulent disbursement pattern, cited at 22% of asset misappropriation schemes. Under speed pressure, duplicate-payment risk also rises, so held invoices should show a clear, recorded reason without extra reconstruction.

Mistake: treating all vendors the same at onboarding. Recovery: Tier onboarding to risk and payment exposure instead of applying one standard flow to every payee. Use stronger checks where risk is higher, and review the master vendor file for abnormal or suspicious activity. This risk-based approach keeps controls commensurate with exposure while reducing unnecessary friction for lower-risk vendors.

Mistake: leaving escalation points vague. Recovery: Define explicit escalation triggers and assign ownership for hold, investigation, and release decisions. If suspicious incidents are not elevated as needed, the rule is too loose and should be tightened. Escalation should be an operational control, not an informal expectation.

Mistake: weak evidence retention after control breaches. Recovery: Standardize audit-trail exports and incident documentation for every breach. Keep the records needed to reconstruct what happened, including invoice/supporting records, vendor-change history, approvals, payout status, reconciliation notes, and the final hold-or-release rationale. If the case cannot be rebuilt from records, the control is harder to defend and improve.

The practical takeaway and copy-paste checklist#

Build controls by payment lifecycle stage, not by generic policy bucket. This keeps controls tight at the handoffs where risk concentrates (onboarding, approvals, authorization) while preserving speed in routine lanes.

Use risk-proportionate tradeoffs: tighten where loss or regulatory risk is higher, and keep low-risk repeatable payouts efficient.

- Assign named owners for each stage.

Set one accountable owner for vendor onboarding, one for approval workflows, and one for payment authorization. Keep segregation of duties explicit, because weak or overridden controls are a major fraud-loss driver. Checkpoint: for high-risk payouts, approver, releaser, and overrider are not the same person.

- Map top billing schemes to lifecycle controls.

List the billing schemes and error patterns you actually see, then attach one preventive and one detective control at the relevant stage. Checkpoint: each risk line includes an owner, required evidence, and a defined response.

- Publish hard escalation rules for unauthorized payments and BEC indicators.

Do not leave these calls to in-the-moment judgment. BEC is one of the most financially damaging online crimes, and compromised email can be used for unauthorized fund transfers. Rule: if remit details change after approval, or a request shows suspicious email pressure, hold the payout and require documented re-verification before release. For deeper playbooks, see Accounts Payable Fraud Prevention: How Platforms Detect and Stop Business Email Compromise.

- Standardize the audit trail evidence pack.

Use the same packet for incidents and periodic reviews: payment timeline, affected transactions, control logs, override rationale, supporting documents, remediation actions, and owner sign-off. Checkpoint: a reviewer can determine why a payment was released, held, or blocked without side-channel context.

- Roll out by lane before expanding to all cross-border payouts.

Pilot one lane, review exception aging, false-positive rate, release delays, and reconciliation defects, then decide on expansion. Cross-border rollout should include explicit legal, regulatory, and supervisory readiness gates, with controls proportionate to lane risk. Red flag: one global rule set applied to every corridor without periodic reassessment.

If you want a deeper dive, read Finance Automation and Accounts Payable Growth: How Platforms Scale AP Without Scaling Headcount.

Frequently Asked Questions

What AP internal controls most effectively prevent fraudulent disbursements on platforms?

Start with a risk-based control stack: tiered vendor onboarding, invoice validation before approval, stronger approvals for higher-risk payouts, and a pre-release authorization check for beneficiary and remit details. A critical failure point is control override, so overrides should be rare, named, and logged. ACFE's 2024 data reports that more than half of occupational frauds occur because controls are missing or overridden.

Which controls improve disbursement accuracy fastest without slowing all payouts?

A practical first set is duplicate invoice checks, required-document checks, and pre-release matching of vendor, invoice, amount, and beneficiary details. These controls can catch common errors before money moves without requiring human review on every routine payment.

How should automated controls and manual review be split in high-risk payment flows?

Automate deterministic checks: duplicate invoice number, amount mismatch, missing support, and beneficiary-detail mismatch. Keep human review for context-heavy cases such as suspected BEC, repeated overrides, or a vendor bank-detail change pushed through email pressure. A good checkpoint is a case record that shows both the machine hold reason and the human release-or-escalate rationale.

What are early warning signs of billing fraud in day-to-day AP operations?

Watch for vendor banking-detail or remit-detail changes, repeated urgency, and approval overrides that cluster around one payee or operator. A familiar vendor suddenly sending an invoice with updated address or payment details is a known BEC signal, and BEC remains one of the most financially damaging online crimes. Track tips as their own signal stream too: ACFE found 43% of occupational frauds were detected by a tip.

When should a payment be monitored versus held, blocked, or escalated to legal/compliance?

There is no single global threshold, so tie the action to risk concentration and to whether funds can still be stopped. Monitor when the signal is weak and core data still matches. Hold when support is incomplete or a change request appears after approval. Block when pre-release authorization fails, such as a beneficiary mismatch. Escalate to legal or compliance for suspected BEC, repeated override patterns, or market-specific issues where local rules may affect whether you can release, reverse, or report.

How do you adapt AP controls across markets where compliance requirements differ?

Keep the core control logic consistent, then adapt evidence requirements, review owners, and release rules by jurisdiction and payout corridor. FATF is explicit that countries should adapt implementation to their own legal, administrative, and operational frameworks, and BIS flags legal, regulatory, supervisory, and cross-border data standards as practical design constraints. If you operate across markets, maintain a country or corridor matrix that names required documents, restricted scenarios, and the approver with legal or compliance sign-off.

What minimum reporting should leadership review weekly and monthly to catch control drift?

There is no legally fixed global cadence, but a practical baseline is weekly and monthly reporting. Weekly, review held, blocked, and released counts; exception aging; override volume; vendor detail change requests; tip volume; and false-positive rate by control point. Monthly, add trend analysis by source of failure such as onboarding, validation, or authorization, plus manual reversals, reconciliation defects, and evidence-pack completeness for escalated cases. Include override and tip reporting on purpose: ACFE's 2024 study covered 1,921 real cases across 138 countries and territories, and it identifies both control override and tip-driven detection as major signals.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- csrc.nist.gov/glossary/term/Security_Audit_Trailtrusted

- fbi.gov/how-we-can-help-you/scams-and-safety/common-...trusted

- gao.gov/assets/gao-25-107721.pdftrusted

- guides.gaoinnovations.gov/greenbook/2025/principle-3-establish-structu...trusted

- guides.gaoinnovations.gov/greenbook/2025/appendix-ii-examples-of-preve...trusted

- irs.gov/taxtopics/tc305trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Stop Business Email Compromise in Accounts Payable

Treat Business Email Compromise and Email Account Compromise as payment-release risks first. Email is often the delivery path. Loss happens when accounts payable accepts a fraudulent invoice, a bogus payment update request, or another convincing impersonation message and releases funds.

How Platform Teams Scale AP Volume Without Adding Headcount

Use this as a decision list for operators scaling Accounts Payable, not a generic AP automation explainer. In these case-study examples, invoice volume can grow faster than AP headcount when the platform fit is right, but vendor claims still need hard validation.

What Is Know Your Artist (KYA)? How Music Platforms Stop Streaming Fraud Before It Starts

So this piece stays practical. You will see where basic identity checks end, where KYA adds real value, and where enhanced review is worth the extra operational load. You will also see a failure mode many teams miss: collecting signals without a clear action path. A flag that does not route to a defined approve, hold, or reject decision is not much of a control.