Quick Answer

Use a hard release gate: place any beneficiary bank-detail change on hold, verify through an out-of-band callback to a trusted contact, and require second approval before funds move. For an accounts payable fraud prevention business email compromise platform, detection alone is not enough if AP can still release on email instructions. Keep an evidence file for each decision with request source, verifier identity, timestamps, approval chain, and final outcome, and escalate suspected loss through your financial institution and IC3.gov.

Why Business Email Compromise Becomes an AP Problem#

Treat Business Email Compromise and Email Account Compromise as payment-release risks first. Email is often the delivery path. Loss happens when accounts payable accepts a fraudulent invoice, a bogus payment update request, or another convincing impersonation message and releases funds.

- Why this moved into AP ownership

Business Email Compromise is, in the FBI's words, "one of the most financially damaging online crimes," and it often looks like ordinary finance traffic rather than obvious phishing. A common pattern is a vendor message with updated payment details, which is exactly the kind of request AP teams process every day. That is why inbox filtering matters, but it is not enough on its own. If your team can still change bank details or approve a transfer from email alone, the real control gap is in payment verification and release.

- Why platform operators should care now

This is not a narrow U.S.-only issue. IC3 reported 305,033 domestic and international BEC incidents from October 2013 to December 2023, with exposed losses of $55,499,915,582, and the scam has been reported in all 50 states and 186 countries. For platforms handling contractor, seller, or creator payouts across markets, that matters because the targets are often the people performing legitimate transfer-of-funds requests. If you manage cross-border disbursements, you are not just defending email accounts. You are defending the last approval step before money leaves.

- What you should expect from this article

This piece is built for practical decision-making by compliance, legal, finance, and risk owners, not broad awareness training. You should come away knowing which controls belong in the email layer, which belong in vendor master and bank-change approval, and which belong at payout release. Use a simple checkpoint: when a payment update request arrives, can you verify it against vendor master data, confirm it through an independent callback or other out-of-band check, and show who approved it, when, and on what evidence?

That is where teams fail in practice. They may spot suspicious messages after the fact, but still be unable to reconstruct the source request, verifier identity, timestamp, approval chain, or the reason a payment was released anyway.

Use that standard throughout this piece. Choose controls that stop funds moving on bad instructions and leave an audit trail strong enough for internal review, legal scrutiny, and regulator questions.

Related: Accounts Payable Automation ROI: How Platforms Calculate the Business Case for Payables Technology.

How to choose an AP BEC platform without overbuying#

Choose for pre-release payment control and audit traceability first, then feature depth. This guidance fits teams running high-volume wire transfers or payout batches across multiple markets. If you are a single-entity AP team with low payment-change volume, tighter procedures, callback discipline, and stronger approval controls may deliver more than a large platform.

- Buy for the loss path, not for general email anxiety

If your top risk is executive impersonation, fake invoice pressure, or payment-update fraud, prioritize controls that can block release before funds move. Detection that only flags suspicious messages after they arrive is still useful, but secondary if it cannot place a hold, force second review, or prevent release.

Your practical checkpoint: when bank details change, require out-of-band voice confirmation with a trusted contact, and use a number from your known contact list, not from the request.

- Test vendor master controls before fancy detection

Vendor master control is often where preventable losses are stopped. Your shortlist should show how requested payment instructions are checked against an authoritative vendor contact master, and what happens before funds move when data does not match.

A common failure mode is a convincing thread that uses untrusted contact details or stale vendor records. If the platform cannot show who is authorized to approve payment-instruction changes, AP is left improvising at the highest-risk step.

- Require ERP fit that preserves approvals and evidence

ERP fit matters when it keeps approvals, holds, and exceptions inside normal AP operations under real volume. If teams must rekey between inbox, vendor master, and payment release, both execution and evidence quality degrade.

Ask to see the exact exception path: request received, mismatch detected, payment put on hold, approver assigned, and release blocked until verification is complete. If critical steps are off-platform or spreadsheet-based, treat that as operational debt.

- Prefer traceability over feature breadth

If a control cannot produce audit-ready evidence for legal or compliance review, treat it as secondary. For each escalated event, you should be able to show the source request, known contact used for verification, verifier identity, timestamp, approval chain, and why payment was released or denied.

Dual approval is a baseline for higher-risk transactions, and some guidance allows up to 9 approval levels for sensitive payments. More layers are not automatically better. Choose the fewest steps that still provide a defensible record and support regular adherence testing.

For a separate email setup walkthrough, see How to Create a Business Email Address for Your Freelance Business.

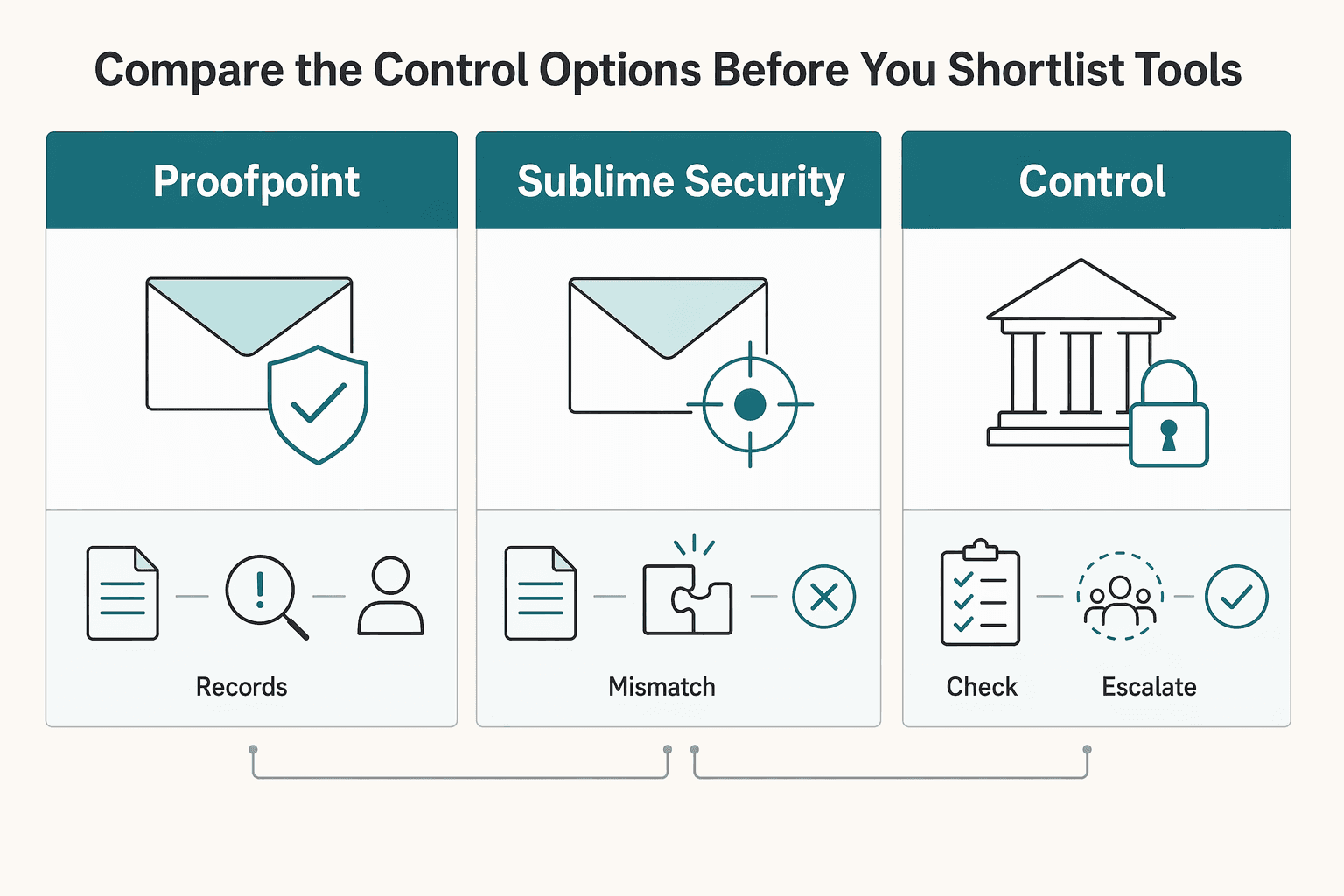

Compare the control options before you shortlist tools#

Do not compare these tools as if they control the same moment of risk. If your loss path is a fake invoice or payment-update request, start by asking whether the control can prevent release before funds move, or mainly improve inbox detection.

FBI examples show why this matters: requests can look legitimate and still send money to criminals. So treat email-layer detection and AP-layer payment controls as different control points in the same incident path.

| Option | Best for | Key pros | Key cons | Stops fake invoice and payment update request before funds move | Verification burden on accounts payable | Concrete use case |

|---|---|---|---|---|---|---|

| Proofpoint | Teams seeing supplier impersonation and compromised supplier account attempts | Proofpoint states it can detect and block BEC variants and identify impersonated supplier domains/compromised supplier accounts | Strong message-layer protection does not by itself show payment holds or payee-validation controls | Partly. It can block/quarantine suspicious email before AP action, but that is not the same as blocking release | Moderate. Fewer risky emails reach AP, but suspicious payment changes still need independent verification | A supplier bank-change request arrives from an impersonated domain and is flagged before AP processes the update |

| Sublime Security | Security teams prioritizing autonomous stopping of targeted attacks | Sublime states it autonomously stops targeted attacks, which can reduce security-team busywork | Like other email-layer tools, it may leave a gap between detection and payment control if approvals are outside the tool | Partly. Strong early attack stopping, but not proof that payment release is blocked | Moderate. Security triage can drop, while AP still performs verification for payment-instruction changes | A targeted urgent payment request to finance is stopped before it enters a normal approval flow |

| ESET-style email controls | Teams improving baseline BEC recognition and email-side protection | Supports identifying BEC behavior where a message mimics a known source | Limited fit for pre-release payment control and payment-investigation evidence | Limited. Helps identify risky email, but does not itself validate payee changes or hold disbursements | High. AP still needs out-of-band checks (for example, calling the company to confirm legitimacy) | A fake invoice is identified as suspicious, but AP must still verify outside email before any payment action |

| AP-native controls | Teams where payment-update and bank-detail change fraud are core exposure | Can correlate contact details, account numbers, emails, and payments to detect fraud patterns; some vendors state they keep a complete audit trail | Added holds/approvals can slow legitimate urgent payments | Yes, when configured to block release pending verification | Focused. Routine items can be streamlined, but exceptions still require human verification | A bank-change request triggers a hold, AP verifies through a trusted vendor contact path, and release stays blocked until approval |

When two candidates can show both pre-release prevention and usable investigation logs for wire-fraud scenarios, keep the shortlist tight. Test those finalists harder instead of adding more vendors.

In demos, require a step-by-step payment-update scenario: where the hold occurs, who verifies, how release stays blocked until verification, and what audit record remains after approve/deny. If that chain is missing, you are likely buying detection support, not a full payment control.

The common failure mode is false comfort: suspicious email is flagged, but AP still executes the highest-risk verification work manually under time pressure. Vendor claims like blocked payees or estimated savings can inform evaluation, but your decision should rest on whether you can consistently prevent and document payment-change decisions.

Related: Finance Automation and Accounts Payable Growth: How Platforms Scale AP Without Scaling Headcount.

Option 1 sender and conversation risk controls#

Use this option when fraud attempts blend into normal-looking email exchanges, especially executive impersonation and vendor payment-update requests. Sender and conversation risk controls help detect BEC patterns that can bypass traditional filters by analyzing thread context, sender behavior, subject shifts, and message content, not just links or signatures.

Where this option earns its place#

This option is strongest in the gray zone where an email looks legitimate but the request changes the risk. Common examples include a familiar vendor sending updated payment details or an urgent transfer request that appears to come from leadership. It is also relevant when attackers gain access to legitimate billing or invoice threads and insert fraudulent instructions mid-conversation.

A practical use case is a known vendor thread that has been about invoice timing, then suddenly asks for new bank details or a different remittance path. A useful control flags that context shift, not only the sender domain.

What it will not do on its own#

This is not a complete control by itself. A risk alert in email does not, on its own, confirm that a payment change is blocked before release. You still need independent verification in the AP process before funds move.

The main failure mode is strong inbox detection with weak payment verification. If a flagged request can still be approved without an out-of-band check, exposure remains.

What to verify in a demo#

Ask for one live thread-based fraud scenario, not a generic phishing example. Confirm that:

- The alert explains why the message is risky (for example, thread change, sender behavior, or unusual request pattern).

- The case can be routed to manual verification outside email, such as calling a trusted contact directly.

- The review record captures the source message, timing, reviewer action, and final disposition (denied, escalated, or cleared).

If your biggest pattern is executive pressure messages and thread interception, keep this on your shortlist. If payment-change approval is the bigger risk, pair this immediately with stronger AP payment controls instead of treating conversation analysis as the full answer.

Option 2 bank detail change controls in accounts payable#

If bank-detail updates are your main wire-fraud exposure, make this your primary release control: when a request changes beneficiary bank data, hold payment until you complete out-of-band verification and a second approval.

This option matters because BEC targets legitimate fund-transfer workflows, not just obviously suspicious emails. FBI IC3 describes BEC as unauthorized fund transfers through compromised or impersonated accounts, with 305,033 incidents and $55,499,915,582 in exposed loss reported across October 2013 to December 2023. If your AP process accepts bank-detail changes by email, this is a direct risk point.

Where this option is strongest#

This control works at the decision point that matters: whether vendor bank details change and whether funds are released. Use an explicit rule for payment-instruction changes:

Ifa request changes beneficiary bank data, payment type, or payment location,thenmove it to hold.- Verify through a secondary channel or out-of-band confirmation.

- Require a second approver before release.

Out-of-band means using trusted contact details you already have, not details provided in the request. That is the mechanism that interrupts fake invoice and bank-switch fraud inside otherwise normal vendor relationships.

What to verify before you trust the control#

A credible demo should show the full path, not just an approval UI:

- Email request arrives and triggers hold status.

- Verifier calls a trusted number already on file (or uses another independent channel).

- A second approver is required before vendor master or payment release.

Watch for two failure modes:

- The verifier uses phone or contact details from the suspicious request.

- Dual approval exists, but tiering is weak, so urgent and routine requests clog one queue and staff bypass controls.

Tier by risk so higher-risk bank-detail changes get mandatory friction while routine invoices do not.

The evidence pack to require every time#

For every approved bank-detail change, keep an evidence pack that supports who-changed-what review:

| Evidence item | Required detail |

|---|---|

| Original request source | Message copy or ticket reference |

| Verification identity | Trusted contact source used |

| Verifier name | Timestamp and result |

| Second approver identity | Timestamp |

| Vendor bank details | Before/after vendor bank details |

| Final decision | Held, denied, escalated, or released |

This audit trace supports investigation and compliance review, and it helps incident response teams review all requests involving payment-type or payment-location changes when compromise is suspected.

The tradeoff is cycle time. If beneficiary changes are your primary loss path, that friction is usually lower cost than releasing funds based only on inbox-level checks.

Option 3 payout release gates and payment rail controls#

Use this option when your main risk is a bad payout release, not just a suspicious email. The control is straightforward: tie payout execution to verification status so risky disbursements can be paused before funds move.

KYC, KYB, AML, and sanctions checks do not solve BEC by themselves. Their value is that they create an enforceable payout eligibility gate. In supported platform models, payouts are enabled only after required verification succeeds, and later data changes can retrigger checks and temporarily disallow payouts.

Where this option earns its keep#

This is strongest for high-volume payout programs where one release decision can affect many disbursements. If beneficiary details change near release time, pause the affected payout batch or account and route it to compliance review instead of treating it as routine.

Coverage will not be uniform across markets or programs. Verification requirements can vary by country, capabilities, and business type. Stripe has published connected-account verification updates across 33 countries in Europe (support notice updated March 2026), and Adyen also states requirements vary by operating country or region.

What to verify before you trust the control#

Ask the vendor to show one end-to-end path with:

- an account that cannot receive payouts until KYC or KYB checks are complete

- a post-onboarding data change that retriggers verification and blocks payout release until checks clear

- an exception workflow that records what changed, who reviewed it, and whether the payout was released, denied, or escalated

The key test is whether the payment rail enforces verification state at release time. A common failure mode is policy drift: one region enforces the gate while another relies on looser manual handling.

For U.S. covered institutions, beneficial ownership should be handled as part of AML procedures, not optional background data. 31 CFR 1010.230 ties written procedures for identifying and verifying beneficial owners to the AML compliance program. If you support business payees, confirm where beneficial-owner status appears in release decisions and what happens when it is missing or stale.

The tradeoff is operational friction. Risk-based sanctions design is meant to reflect product, customer, transaction, and geographic exposure, not one flat rule. Keep the gate targeted to risky release events, document verification state and change history, and prevent quiet regional bypasses.

Option 4 investigation and escalation checkpoints legal will accept#

For suspected Email Account Compromise, use a defined escalation path in the first 30 minutes: pause risky payment activity, notify the right owners, and preserve records for investigation. This is an evidence-and-containment workflow, not routine inbox triage.

| Escalation trigger | Action | Key record |

|---|---|---|

| Executive impersonation to a wire-capable employee | Do not verify by replying to the same email thread; confirm through known contact data | Log who verified, when, and through which channel |

| Urgent wire pressure or last-minute payment change | Move the case out of normal AP handling into the named incident path | If a transfer may already be fraudulent, contact your financial institution immediately and prepare IC3 reporting at ic3.gov |

| Mismatch between vendor master data and payment instructions | Freeze release and preserve the full case record | Keep the original message, received payment instructions, vendor master snapshot, callback notes, approver names, timestamps, and centralized out-of-band logs |

The risk level justifies that structure. IC3 has described BEC as the "$55 Billion Scam," and its 2024 PSA reports a 9% increase in identified global exposed losses between December 2022 and December 2023.

- Executive impersonation to a wire-capable employee

Escalate immediately when a message appears to come from a CEO or CFO and targets someone who can release wires. Do not verify by replying to the same email thread. Confirm through known contact data, and log who verified, when, and through which channel.

- Urgent wire pressure or last-minute payment change

Treat confidential, urgent, or immediate wire requests as escalation events, especially when payment instructions change unexpectedly. Move the case out of normal AP handling into the named incident path. If a transfer may already be fraudulent, contact your financial institution immediately and prepare IC3 reporting at ic3.gov.

- Mismatch between vendor master data and payment instructions

If incoming bank details do not match vendor master data, freeze release and preserve the full case record. Keep the original message, received payment instructions, vendor master snapshot, callback notes, approver names, timestamps, and centralized out-of-band logs. This gives legal and compliance teams what they need to review and act quickly.

Option 5 cross-border tax and compliance signals that affect fraud decisions#

Use cross-border tax and compliance records as risk context, not as payment clearance. They improve anomaly decisions in multi-market programs, but they should never override a bank-detail hold or out-of-band verification when payment instructions change.

- W-9, W-8BEN, and TIN matching

Form W-9 provides a payee name and TIN for information returns, and Form W-8BEN is provided to the payer or withholding agent by a foreign person. That distinction helps with risk triage. A shift from a stable W-9 profile to a new foreign bank account may be legitimate, but it should still trigger enhanced verification. IRS TIN Matching can validate name/TIN combinations before filing, but a matched tax identity does not prove control of a newly provided bank account.

- 1099 records versus international withholding records

Form 1099-MISC covers specific payment-reporting categories, while cross-border payments can also require Form 1042-S and Form 1042 reporting. A complete file and clean history should raise confidence in scoring, not auto-approve a routing change. If payment instructions change, keep the same verification standard.

- FBAR and FEIE as context signals

FBAR (FinCEN Form 114) is tied to foreign account ownership or authority, including when aggregate foreign account value exceeds $10,000 during the year. Form 2555 is used to compute FEIE, and the IRS lists a maximum exclusion of $132,900 per qualifying person for tax year 2026. These records can explain why foreign-account activity appears in a profile. They still do not prove the requested destination account is controlled by the true beneficiary.

Keep these records in the evidence pack with the original request, vendor master snapshot, callback notes, and approval trail. The common failure mode is treating a complete compliance file as legitimacy proof and letting a well-documented BEC request pass.

Conclusion#

The practical answer is not one more inbox filter. It is a layered set of checkpoints in AP that catches risk where money can still be stopped: the thread, the bank change request, the payout release, and the escalation record.

-

Start with conversation risk, then assume it is not enough. Business Email Compromise remains one of the most financially damaging online crimes, and IC3 reported 305,033 incidents with $55,499,915,582 in exposed loss from October 2013 through December 2023. Attackers can also gain access to legitimate billing and invoice threads, which is why conversation-level detection matters in the first place. Still, if you stop at email analysis, you can miss the real decision point. Use it to surface suspicious context early, then force a payment check before release.

-

Make bank detail changes pass a hard checkpoint every time. A payment update request is not just vendor maintenance when it changes account information. A core control is a two-step confirmation outside the original email channel, followed by dual controls for approval of higher-risk transactions. In practice, that means a callback using contact details your team sourced independently, not the phone number inside the request. Keep an evidence pack with the request source, verifier identity, timestamp, approval chain, and vendor master snapshot. If the change lands near release time, hold it rather than trying to "clear it quickly."

-

Treat escalation as part of prevention, not just cleanup. When fraud is suspected after initiation, move immediately with the originating financial institution and request a recall or reversal, then file IC3 reporting and contact your local FBI field office as appropriate. Speed matters, but documentation does too. A scattered trail of screenshots and chat messages slows legal and compliance review right when you need a defensible record. Your escalation file should show what changed, who verified it, what failed, and when the team acted.

-

Shortlist by risk fit, then test against real cases before rollout. Validate shortlisted controls against concrete scenarios before you buy broadly, especially trusted-thread abuse, payment-instruction changes, and approval-bypass attempts. J.P. Morgan's summary of 2026 Nacha changes points to evaluating fraud detection and monitoring requirements, and for affected organizations the phased dates begin March 20, 2026 and June 19, 2026. Use that as a forcing function to test where your controls fail: trusted thread abuse, late beneficiary changes, weak dual approval, or poor case records.

Done well, this can reduce wire fraud exposure while keeping routine payouts operational. The winning setup is the one your team can verify, document, and enforce at the exact moment money would otherwise leave.

Frequently Asked Questions

What is Business Email Compromise in accounts payable operations?

In accounts payable, Business Email Compromise is a transfer-of-funds scam where someone impersonates a trusted sender or uses a real business email account to push a payment, invoice, or bank detail change. The practical AP version is usually a fake invoice or a supplier bank switch request. The FBI also refers to some of these cases as Email Account Compromise when the attacker is sending from a compromised real mailbox.

Why do Business Email Compromise attacks evade traditional email security controls?

Many of these attacks do not look like classic phishing because the attacker may be inside a legitimate billing or invoice thread. That means the message can inherit a real conversation history, trusted sender context, and believable urgency. If your control stops at inbox filtering, you can still approve a bad payment because the loss happens at the release decision, not just when the message arrives.

Which controls should be mandatory before approving a payment update request?

At minimum, require out-of-band verification through a secondary channel and do not rely on email alone for account changes. The FBI's practical check is simple: look up the company's phone number on your own instead of using the contact details inside the request.

What events should trigger immediate escalation to compliance or legal?

Escalate quickly when a payment request shows social-engineering pressure or suspicious account-information changes. A suspected payment loss should trigger immediate contact with the originating financial institution to request a recall or reversal, plus formal IC3 reporting. Whether compliance or legal must be engaged immediately depends on your jurisdiction and internal policy.

How should teams balance fraud prevention against payout speed targets?

Do not let speed targets override payment-change verification, especially for beneficiary bank changes close to release time. A good rule is selective friction: stable repeat payments move normally, but any change to account information gets a hold until independent callback verification is complete. That tradeoff is justified by the scale of the problem alone. CISA cites FBI-reported BEC losses of over $2.7 billion in 2024.

Is user awareness training enough without vendor master data and payout release controls?

No. Training matters, but CISA presents awareness as one part of a broader set of essential steps, not as a standalone answer. If you want real AP BEC coverage, pair user awareness with independent verification of payment updates and broader technical and operational controls that can stop a bad transfer before funds move.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cisa.gov/news-events/alerts/2015/06/24/business-email...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fbi.gov/how-we-can-help-you/scams-and-safety/common-...trusted

- irs.gov/tax-professionals/taxpayer-identification-nu...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Internal Controls for AP Platforms to Prevent Fraudulent Disbursements

Start here: your AP control design should reduce fraudulent disbursements and payment errors without turning every payout into a bureaucratic exercise. In practice, that means clear escalation points at the moments where money can move incorrectly, not extra approvals added just to look controlled.

Accounts Payable Automation ROI for Platforms That Need Defensible Results

---

How Platform Teams Scale AP Volume Without Adding Headcount

Use this as a decision list for operators scaling Accounts Payable, not a generic AP automation explainer. In these case-study examples, invoice volume can grow faster than AP headcount when the platform fit is right, but vendor claims still need hard validation.