Quick Answer

Platform teams scale AP volume without adding headcount by automating intake, extraction, routing, and posting while shifting staff to exceptions, vendor issues, and close review. The right path depends on the bottleneck: internal invoice workflows inside ERP, payout-event control, reconciliation, or multi-country compliance. Judge vendors by touchless rate plus exception rate, audit-trail quality, webhook reliability, and month-end reconciliation proof.

Finance teams can scale AP volume without scaling headcount if they pick the right platform path#

Use this as a decision list for operators scaling Accounts Payable, not a generic AP automation explainer. In these case-study examples, invoice volume can grow faster than AP headcount when the platform fit is right, but vendor claims still need hard validation.

- OU Health shows what strong platform fit can unlock

Ascend case-study material says OU Health automated 60% of invoices at launch, 3x its prior platform, and later reached a 90% touchless processing rate. Treat that as directional proof that a replacement can materially improve AP execution in a complex environment, not as a neutral market average or a rollout guarantee.

- Virgin Voyages shows the real test is throughput under growth

Case-study material reports a 74% touchless processing rate while invoice volume increased 50% in 6 months. In evaluation, ask for both touchless processing rate and exception rate. One without the other can hide manual cleanup.

- Panera Bread shows "without headcount" can mean role reallocation

Ascend's Panera case-study material reports 40% faster invoice processing and a 60% increase in recognition rates while handling more than 400,000 invoices annually across 2,000 locations. Separately, an AvidXchange Panera customer story says two of the original five employees remained on invoice processing while three moved to more strategic work. In this kind of outcome, the win is shifting people from repetitive validation to exceptions, supplier issues, and control review, not removing humans from AP.

- Selection risk is high because many tools look similar before implementation

Gartner's Market Guide, published 07 August 2023, says the AP invoice automation market continues to evolve, many options look alike, and AI-first entrants may not solve every need from capture to payment. A Workday Marketplace listing for Ascend says best-in-class customers have seen up to 95% touchless processing, but the snippet does not provide independent validation details. Treat ceiling claims as hypotheses. Then verify how touchless is calculated, what stays in exceptions, and how AP cycle time changes after go-live.

APQC publishes cross-industry AP KPI benchmarks, and CFO.com cites top-performing AP cycle time at 2.8 days or faster. You do not need that on day one, but you do need your own baseline before comparing vendors.

Use that lens for the rest of the list. Focus on the criteria that affect scale, the tradeoffs vendors blur, and the implementation controls that can help prevent AP automation and payout failures.

Related: Manufacturing Accounts Payable Automation: How Industrial Platforms Pay Subcontractors and Suppliers.

Who this list is for and how to score each option#

Use this list if your team owns AP outcomes beyond invoice capture, including payout status, reconciliation, and month-end close. If you are only optimizing bookkeeping workflows, this framework is probably broader than you need.

Best fit for teams with shared finance and product ownership#

This is built for founders, finance ops leads, product managers, and engineering owners who are accountable for both money movement and accounting outcomes. AP applications are not just invoice tools. They also touch payments, supplier data, and integrations with ERP and adjacent systems.

When your AP choice affects payout events, webhook handling, vendor reconciliation, and journal posting into ERP, selection risk can show up in close quality, not just queue speed. That is why you need both metrics. Use touchless processing rate for straight-through volume, and exception rate for the manual work still required.

Not for teams solving a narrower back-office problem#

If your scope is limited to OCR, coding suggestions, or controller-only reporting, a simpler AP shortlist is usually enough. This list is for teams where finance, product, and engineering need a shared definition of done across payable, payout, and posted journal states.

Use a simple filter. If webhook delivery behavior and source-to-journal traceability are out of scope for your team, much of this evaluation will be unnecessary.

Gate first, then score#

Before you compare pricing or features, use a pass/fail gate when these controls are required for your use case. Deprioritize options that cannot show traceable posting journals and reliable webhooks.

For journals, verify source-to-GL traceability and inspect fields such as transaction date, audit trail code, journal entry, distribution reference, and source document. Ask the vendor to walk one real invoice from source document to posted journal.

For webhooks, verify retry behavior when acknowledgments fail. A webhook is an HTTPS callback triggered by an event. Reliability depends on documented redelivery behavior and evidence that missed events will not silently break payout status or reconciliation.

Six criteria to score after the gate#

| Criterion | What to verify | Why it matters |

|---|---|---|

| Touchless processing ceiling | How touchless rate is calculated, paired with exception rate | High automation claims are weak if exception volume stays high |

| Exception management depth | Queue visibility, approval bottleneck handling, resolver workflows | Growth pressure often appears in exceptions first |

| Audit trail quality | Source document, journal entry, distribution reference, audit-trail fields | You need source-to-GL traceability for audits and disputes |

| Integration complexity | ERP integration plus API and webhook work across payment and bank systems | Real implementation effort often extends beyond ERP |

| Compliance coverage | Whether KYC/CIP, AML, and beneficial ownership checks are supported where relevant | These controls can be explicit AML requirements for covered financial institutions |

| Reconciliation effort at month-end | How provider statuses, AP records, and journals align during close | Close quality depends on accurate month-end financial reporting |

If options score similarly, use month-end reconciliation evidence as the tie-breaker, not demo smoothness.

What touchless processing actually means in platform AP#

In platform AP, touchless processing means invoices move from intake through coding, approval routing, and ERP posting with minimal manual intervention, not a promise that no human ever touches the process. Some vendors define touchless more strictly as no manual steps from receipt to ERP posting, while other documentation frames it as minimal manual effort. A practical way to evaluate touchless performance is to separate the automation layers instead of trusting one headline percentage.

| Layer | What it does | Main check |

|---|---|---|

| OCR and extraction | Converts printed or handwritten invoice content into usable digital text | Extraction errors can disrupt downstream steps |

| Routing and account coding | Routes invoices to the right coding and approval path | Verify the routing logic matches your operating conditions |

| Exception management | Routes incomplete invoices with missing or invalid information for review and completion | Fix data quality and approval logic before chasing a higher touchless percentage |

| Reconciliation and audit trail | Maintains an audit trail tied to source documents, accounting entries, and journals | Verify traceability supports subledger-to-GL reconciliation and audit readiness |

- OCR and extraction

OCR is the intake layer. It converts printed or handwritten invoice content into usable digital text, for example words, lines, and text blocks. It can speed document-to-data flow, but extraction errors still happen and can disrupt downstream steps.

- Routing and account coding

After extraction, the key question is whether invoices are routed to the right coding and approval path. Routing rules can be predefined in invoice account-coding workflows. The real differentiator is whether that routing logic matches your operating conditions.

- Exception management

Touchless volume only matters if exceptions are under control. Incomplete invoices with missing or invalid information should be routed for review and completion. If exception volume stays high, fix data quality and approval logic before chasing a higher touchless percentage.

- Reconciliation and audit trail

Automation is not credible if you cannot trace outcomes at close. AP records should maintain an audit trail tied to source documents, accounting entries, and journals. That traceability supports subledger-to-GL reconciliation and audit readiness.

A practical checkpoint is to follow one invoice end to end and verify both invoice-to-payment cycle time and error-free disbursement rate. If those improve while traceability holds, the automation is delivering operational value.

For a plain-English overview, see Accounts Payable Automation for Dummies for Platform Operators.

Quick comparison of AP growth platform paths#

Start with the bottleneck that is actually slowing you down. Then require one operational proof before you commit: exception turnaround for Option A, webhook reliability for Option B, reconciliation cycle time for Option C, or audit-trail completeness for Option D. If an option cannot show traceable ledger journals and reliable event handling under retries, eliminate it early.

| Path | Best for | Key pros | Key cons | Implementation burden | Compliance fit (KYC/KYB/AML) | Verification checkpoint |

|---|---|---|---|---|---|---|

| Option A: Workday plus Ascend-style AP automation | Best for: teams already on Workday Financial Management with complex invoice workflows. Watch-out: weak fit if your main pain is downstream payouts or multi-country compliance. | Workday Marketplace positions this path for complex Workday invoice workflows. The listing includes a 60% touchless processing SLA and explicit exception and backlog handling. Vendor cases report scale context, including 400,000 invoices annually across 2,000 locations and 74% touchless with 50% invoice-volume growth in 6 months. | AP-first scope. It does not by itself prove payout-rail control or broad KYC/KYB/AML coverage. OU Health launch performance is inconsistent across sources, with 59% vs 60% at launch. | Medium when Workday governance is already mature. | Strong for AP control traceability. Limited direct evidence here for full KYC/KYB/AML breadth. | Operational proof: exception management turnaround. Sample non-touchless invoices and confirm the manual queue clears within SLA without breaking ERP posting or audit links. |

| Option B: ERP plus payments orchestration layer | Best for: teams keeping ERP as system of record while adding payout logic via APIs and webhooks. Watch-out: poor fit without engineering ownership of retries, duplicates, and event-to-ledger mapping. | Clear ERP and payments separation. Webhook endpoints support real-time event delivery, and idempotency keys support safe retries without duplicate operations. Useful when AP approvals are stable but payout-status visibility is weak. | Retry behavior is unavoidable: Stripe can resend for up to three days. Adyen retries can continue for up to 30 days, and delayed Adyen acknowledgment beyond 10 seconds can cause delivery issues. | High across engineering and finance ops. | Provider-dependent. Verify exact KYB, KYC, and AML scope instead of assuming default coverage. | Operational proof: webhook reliability. Run retry scenarios and confirm idempotent handling helps prevent duplicate ledger entries while preserving reconciliation visibility. |

| Option C: unified AP plus payouts stack with MoR and Virtual Accounts | Best for: teams that want AP events, payout execution, and reconciliation in one operating surface where supported. Watch-out: weak fit if finance, product, and engineering are not aligned on shared ownership. | MoR can carry transaction-compliance duties including KYC/AML and indirect-tax handling. Virtual accounts support traceable routing as sub-ledgers linked to a physical account. | Coverage varies by provider and jurisdiction. Do not assume one stack covers AP automation, MoR liability, virtual accounts, and global compliance everywhere. Virtual accounts do not hold funds directly. | Medium to high. | Potentially strong when MoR scope is active. KYB coverage still requires vendor-specific confirmation. | Operational proof: vendor reconciliation cycle time. Trace one invoice through virtual-account reference, payout status, and ledger posting at close. |

| Option D: compliance-first global payout stack for multi-country AP | Best for: teams where multi-country compliance review is the gating constraint. Watch-out: overbuilt for mostly domestic, low-complexity vendor onboarding. | Aligns to the risk-based approach used in FATF standards. Supports onboarding evidence expectations, including beneficial-owner identification where required. | Heavier document collection and slower rollout. Manual review can spike with poor onboarding data. Obligations vary by operating model. | High across finance, compliance, legal, and ops. | Strongest fit when KYC and AML controls are primary. For U.S. legal-entity onboarding, 31 CFR 1010.230 requires beneficial-owner identification at new account opening. | Operational proof: audit trail completeness. Confirm one cross-border supplier has an exportable evidence chain: onboarding, beneficial-owner record, risk decision, approvals, and payment record. |

Eliminate options quickly based on the real bottleneck. If your issue is Workday invoice coding, approvals, and exception backlog, start with Option A. If ERP is stable but payment-event control is weak, Option B is usually the better fit, but only with strong retry and idempotency operations. If reconciliation drag is larger than invoice intake drag, Option C is attractive when both MoR scope and virtual-account support are real in your markets. If cross-border onboarding and AML controls are already slowing payouts, consider Option D early instead of retrofitting it later.

For a step-by-step walkthrough, see Accounts Receivable Automation for Platforms to Collect from Enterprise Buyers at Scale.

Option A works best when you already run Workday and need faster AP execution#

Pick Option A when the bottleneck is inside Workday Financial Management: invoice intake, coding, approvals, and exception backlog. If the friction starts after AP posting, such as cross-border payouts, KYC/KYB policy gating, or reconciliation across payout rails, this path is a weaker fit.

Best fit#

This is the practical choice for teams already standardized on Workday that want faster AP execution without replacing the finance core. The value is not just automation. It is also a smaller change surface: keep Workday as the system of record and add AP automation within existing infrastructure.

Workday supports integrations through REST APIs and prebuilt connectors, and states those financial connectors are built, maintained, and supported by Workday or certified partners. In practice, that can lower integration risk compared with introducing a separate AP stack.

What the evidence actually supports#

The evidence here is AP-specific, not platform-wide. Results vary by customer, but the pattern is consistent: higher touchless processing, stronger OCR extraction, and less manual handling before posting to Workday.

| Evidence point | Reported result | Why it matters |

|---|---|---|

| Workday Marketplace listing | 60% touchless SLA | Contractual baseline, not only a directional claim |

| Virgin Voyages case | 74% touchless and 50% invoice-volume increase in 6 months | Shows throughput growth alongside a high touchless rate |

| OU Health case/article | 59% touchless at go-live, later 90% vs 40 to 50% in a vendor article, with OCR over 98% | Indicates performance can improve over time and varies by source |

| Panera case | Recognition rates improved from 50% to 85% while processing 400,000 invoices annually across 2,000 locations | Scale evidence for multi-unit AP operations |

Panera is the clearest centralization example. AP was centralized across retail, manufacturing, and overhead, with reduced image retrieval and data-entry effort in preprocessing and downstream approvals research. That is the pattern to look for when business units run inconsistent approval flows and AP spends too much time on manual follow-up.

Where this path stops helping#

The tradeoff is scope. Strong AP automation does not, by itself, prove cross-border payout coverage, KYC or KYB policy gating, or unified reconciliation across payout rails. Treat this as an AP execution decision, not a full payments-infrastructure solution.

Touchless rate alone is not enough. The marketplace listing explicitly includes manual exception processing and backlog management, so exception queues still need operating discipline.

Operator check before you commit#

Ask for one evidence pack, not just one demo. It should include source capture, OCR extraction, auto-coding, exception handling, and final posting into Workday. If a vendor cannot show one invoice end to end, your expected AP gains are probably fragile.

If you have had connector issues before, use OU Health's selection logic and require a Workday Select Partner with instant integration evidence. This path is usually the fastest win when the constraint is internal AP execution, not downstream payment complexity.

Option B fits teams that need ERP control plus a flexible payments orchestration layer#

Choose Option B when you want ERP to remain the approval authority, but you need a separate layer for payout execution and tracking. It works when your team can run API and webhook integrations with strict controls. Without that, you risk duplicate events, status drift, and reconciliation noise.

Best fit#

This path fits teams that trust existing ERP approval workflows and do not want to rebuild them in an AP tool or payout provider. Oracle describes invoice approvals that build approver lists from defined rules. SAP supports one-step or multi-step supplier-invoice approvals with approvers assigned by role, user, or team. That boundary matters: keep AP authority in ERP, then send approved payables out for payout execution and status tracking.

It can support a phased rollout. You can keep existing approval workflows in place, then add a payments orchestration layer for provider routing through APIs.

What you gain#

What you gain here is modular control, not a shortcut. ERP stays the source for supplier invoice records, while the orchestration layer handles payout batching, provider routing, and asynchronous webhook status updates.

That can be practical for higher-volume disbursement flows. PayPal Payouts supports up to 15,000 payments per call. It is also useful when payout rules differ by corridor, partner type, or payout method while ERP approvals stay unchanged.

Where teams get burned#

The risk sits at the integration seams. Webhooks are asynchronous and can be delivered more than once. Stripe notes that duplicate event delivery can happen, and PayPal retries non-2xx webhook deliveries up to 25 times over 3 days. If you do not implement deduplication and retry-safe writes, payout status can become unreliable.

Idempotency is a core control. Stripe idempotency keys can be up to 255 characters and are retained for at least 24 hours before pruning. PayPal rejects a reused sender_batch_id if it was used in the last 30 days. If your payout-creation flow is not mapped to those controls, duplicate or unclear records are more likely.

Another failure mode is contract drift between ERP invoice data and payout payloads. Oracle's payables invoices REST resource includes headers, lines, distributions, installments, flexfields, and attachments, and Oracle also notes that REST updates may not auto-populate related fields. That can create mismatch risk across AP, payout, and journal records.

Concrete use case#

A practical pattern is to keep ERP invoice approvals, then send only approved records into payout batching and status tracking. Require this checkpoint before rollout:

- Show one approved invoice and its ERP approver path in Oracle or SAP.

- Send that approved record into a payout batch.

- Simulate a failed webhook acknowledgment and a duplicate event.

- Prove the audit trail links invoice ID, payout batch ID, provider event ID, and journal reference, and note where manual reconciliation is still required.

If a team can only demo the happy path, treat scale readiness as unproven. Option B is credible when ERP authority stays intact and the orchestration layer handles retries, duplicates, and schema changes safely.

Related reading: Accounts Payable Software Comparison for Platforms That Need Operational Proof.

Option C fits platforms that want AP and payout rails in one operating surface#

Choose Option C when your main bottleneck is downstream: payouts, payout-state disputes, and reconciliation evidence. If approval latency is still the issue, start with Option A or B first.

Best fit#

Option C fits platforms that already control funds movement and need AP automation tightly linked to payout execution. The scope matters here. Unified offerings can cover supplier onboarding, invoice management, payments, and reconciliation in one surface. AP automation can span invoice receipt, matching, approval routing, payment origination, reconciliation, and reporting.

This is most useful when your operating model already runs pay-in and payout as one chain. In Stripe's marketplace pattern, customers pay the marketplace, then the marketplace pays sellers. If finance, product, and engineering already co-own that flow, one AP-plus-payout surface can help reduce handoff ambiguity.

What you gain#

The benefit is tighter linkage between AP events, payout status, and audit evidence. You can run one traceable chain from invoice intake through approval, payout creation, and reconciliation output. That does not guarantee clean books on its own, but it reduces seams.

Virtual account management can help when allocation is the pain point. It uses unique identifiers to allocate transactions to virtual accounts within a physical account, which can simplify allocation mapping across many payees or lines. It only works if your banking and ledger setup consistently uses those identifiers.

Merchant of Record can clarify legal responsibility boundaries in the right configuration. The MoR is the entity with legal responsibility for the transaction, and in Stripe Connect that can be your platform or connected accounts depending on setup. Some managed MoR offerings cover indirect tax compliance in more than 80 countries, but that coverage is product-scoped, not universal.

Where teams get burned#

A common rollout risk is organizational, not purely technical. A unified stack spans onboarding, AP approvals, payout logic, webhooks, and compliance and legal controls. Without clear ownership, approved payables can stall at verification, or payouts can move before finance has audit-ready evidence.

Verification gating is a real operational constraint. In some Stripe setups, the platform must collect and pass required KYC and KYB data. Adyen also requires platform-user verification before payment processing and payouts in that model. Missing onboarding data can block cash movement.

Webhook reliability is the other common failure point. Providers can deliver duplicate webhook events, so retries must be idempotent. Stripe supports idempotency for safe retries, and key retention can be pruned after at least 24 hours, so your internal dedupe controls cannot rely only on provider-side retention.

Concrete use case#

A strong Option C use case is a marketplace platform that wants one traceable path from invoice intake to payout completion. It also needs shared exception handling across finance and operations.

Before rollout, prove the chain on one sampled transaction:

- Show the source payable and approval history.

- Show onboarding and verification status, including required KYC and KYB items when the platform owns collection.

- Create the payout and map payable ID to provider reference, webhook events, and reconciliation records.

- Force duplicate webhook delivery and a retry, then show no duplicate payout or duplicate internal transaction record.

- Produce the reconciliation output used to track payout transactions.

If you cannot produce that evidence pack, the unified model is not production-ready yet.

Pick Option C when payout execution, verification gating, and reconciliation are where you lose time today. If coding, matching, and approval routing are still the blocker, fix those first and expand later.

If you need to build the business case, see Accounts Payable Automation ROI for Platforms That Need Defensible Results.

Option D is strongest for multi-country AP with heavy compliance exposure#

Choose Option D when cross-border compliance is the main constraint, not approval speed. You trade a slower rollout for tighter pre-payment checks and cleaner decision evidence.

Best fit#

Option D fits teams paying suppliers, contractors, or partners across jurisdictions where KYC, KYB, AML, VAT validation, and tax-document handling can be required. The core benefit is control before funds move, with a clear record of why a payee was approved, blocked, or routed for review.

A key control is identity and ownership verification. For covered U.S. financial institutions, 31 CFR 1010.230 requires procedures to identify beneficial owners of legal-entity customers at account opening and include those procedures in the AML program. FATF defines a beneficial owner as the natural person who in the end owns or controls the customer. Even when your platform is not the regulated institution, providers in this model may enforce similar onboarding and payout checks. If beneficial-owner data is inconsistent, treat that as a launch blocker.

What you gain#

The main gain is policy-based routing from the start, based on payee type, country, and documentation state, rather than fixing tax or verification issues after approval.

| Control or document | What you should verify | Why it matters |

|---|---|---|

| Form W-9 | Correct taxpayer identification number for U.S. payees | The IRS uses Form W-9 to provide a correct TIN for information returns |

| Form W-8BEN | Foreign status for an individual in U.S. withholding and reporting contexts | Helps separate foreign individual handling from U.S. payee handling |

| Form 1042-S | Whether nonemployee compensation to nonresident aliens should be reported there, and whether withholding applies | IRS says those payments are reported on Form 1042-S and withholding may be required |

| VIES VAT check | Whether the VAT number validates in the relevant national database, plus the date and result | VIES is a search engine, not a standalone database, and upstream updates are not always immediate |

| FBAR and FEIE touchpoints | Whether these issues are relevant to your case before collecting or tracking anything | FBAR can be triggered when aggregate foreign account value exceeds $10,000. FEIE eligibility includes a foreign tax home, and one path uses 330 full days abroad |

One caution on U.S. reporting: IRS materials are not fully aligned on the 1099-NEC threshold. One FAQ references $600 and notes $2,000 for payments made after December 31, 2025, while another instruction page still states $600 in its context. Do not hardcode a single threshold without checking the current form-year rule. If you file at volume, note the e-file threshold of 10 aggregated information returns.

Where teams get burned#

A common failure is treating a validation check as final proof. VAT validation is a clear example: VIES can return invalid when a number is not registered in the national database, and national-database updates are not always immediate. So the control is not only "VAT passed." It is "VIES result captured, timestamped, and correctly routed when invalid or unavailable."

Another failure is ownership misalignment. Legal may require stricter documentation while operations pushes for speed, and no one defines which payments can proceed, which must pause, and what closes an exception. Without that alignment from day one, controls create queue noise instead of reducing exposure.

Concrete use case#

A strong Option D use case is a platform expanding AP and payouts across countries where tax-form collection and verification are required. Before rollout, test one cross-border payment end to end. Confirm the evidence pack: beneficial-owner or business-verification status where required, the document path used for W-9 or W-8BEN, VAT validation result through VIES where relevant, the reporting decision for 1099 or 1042-S, and the approval log explaining why the payment proceeded.

If you can produce that file cleanly, the added controls are working. If not, you are adding complexity without reducing exposure.

How to choose between build, buy, and hybrid at each growth stage#

Treat stage as a guide, not a rule. Start with reuse where possible, then buy when reliability controls are still maturing, use hybrid when there is a persistent boundary gap, and build only where your logic is truly proprietary.

| Stage | Default path | Use when |

|---|---|---|

| Early stage | Buy | Webhook duplicate handling and idempotent retries are not yet consistently covered |

| Mid-stage | Hybrid | The AP layer handles invoice processing and supplier data well, but payout or compliance-gated routing does not fit cleanly in the same product |

| Late stage | Selective build | Routing or risk logic is truly proprietary, while common controls stay in reused or off-the-shelf components |

- Early stage: buying can be lower risk if reliability basics are not yet proven.

If you do not yet have consistent engineering coverage for webhook duplicate handling and idempotent retries, buying is usually lower risk. The practical goal at this stage is stable AP flow and a usable audit trail, not custom payment infrastructure.

Keep the verification test simple: replay an event, force a timeout, and confirm retries do not create duplicate side effects. If duplicate deliveries or status drift create reconciliation noise, your build posture is likely premature.

- Mid-stage: use hybrid when the gap is specific and recurring.

Hybrid is often justified when your AP layer handles invoice processing and supplier data well, but payout or compliance-gated routing needs rules that do not fit cleanly in the same product. AP applications are centered on invoice processing, payment facilitation, and supplier master-data management. Your platform may still need separate logic around routing and exceptions.

The decision point is boundary quality, not vendor count. Keep commodity workflow in the bought layer, and add custom logic only where the rule is truly platform-specific. Validate with messy cases and confirm exceptions resolve with a traceable audit trail, not spreadsheet bridges.

- Late stage: build selectively, keep commodity controls in proven infrastructure.

At higher scale, selective build can make sense for proprietary routing or risk logic. But reuse-before-buy-build still applies: default to reused or off-the-shelf components for common controls unless there is a clear reason not to.

For beneficial ownership controls, do not assume scope is static. Check current applicability of 31 CFR 1010.230 and any later changes, including reported FinCEN exceptive relief dated February 13, 2026, before deciding what to build internally.

- Use a fixed sequence before comparing license price.

Do not start with feature debates. First agree on measurable verification criteria and failure outcomes. Then run the decision sequence: define failure cost, map required controls, test exception handling with real edge cases, and only then compare total cost of ownership. This order prevents attractive demos from masking operating burden. Lifecycle cost includes indirect effort, not only license spend.

Use this decision checkpoint as a working scorecard by mapping webhook reliability, ledger journals, and exception handling requirements against the Gruv docs.

First 90 days of implementation without operational surprises#

Use this 90-day sequence as an operating plan, and gate progress by proof, not enthusiasm. If reconciliation is not clean, automation will only move defects faster.

- Days 1 to 30: baseline the process you actually have.

Start with defensible metrics: AP cycle time, first-time error-free disbursements, and cost per invoice, plus internal counts like exception backlog and reconciliation defects. AP cycle time is measured as calendar days from invoice receipt to payment transmission, and APQC reports this benchmark from a sample of 2,227 organizations. Track first-time error-free disbursements alongside cycle time so faster processing does not hide payment-quality regressions.

Build an evidence pack from live transactions: source invoice, approval record, payment status, and resulting ledger journals. This is where audit-trail gaps can surface early.

- Days 31 to 60: configure in a non-production lane and test failure paths early.

Set OCR, coding rules, approval routing, and webhook handling in sandbox before any production cutover. Treat duplicate webhook deliveries as normal, log processed event IDs, and reject repeats. Validate idempotent ledger posting by replaying the same event and confirming retries do not create duplicate journal side effects.

Also test posting-profile change risk explicitly. Reconciliation can fail if posting profiles change after transactions already exist, so reconcile before and after any change.

- Days 61 to 90: cut over by vendor cohort, not all at once.

Use phased cohorts so failures are isolated and reversible, for example 25%, then 50%, then 100%. Start with lower-variance invoice patterns and lower compliance complexity, then expand.

Enforce verification and AML policy gates where required. If you use a provider for verification, remember that provider verification may enable charges or payouts but does not automatically satisfy independent legal KYC obligations. For regulated businesses such as MSBs, AML program requirements apply. Route low-confidence OCR outputs to human review instead of auto-posting them.

- Verification checkpoint: no phase advance without sampled reconciliation.

Before each phase change, reconcile sampled transactions across source documents, internal ledger journals, and payout or provider statuses. Use a payout reconciliation report when available to align checks to settlement batches. If sampled records do not agree, stop the rollout. Webhook retries can continue for up to 3 days, so drift may appear after initial processing.

What breaks first when AP volume grows and how to prevent it#

At scale, common AP failure points are extraction quality, status consistency, and compliance gating. If someone claims you can scale "without headcount," ask how they handle exceptions, reconcile drift, and maintain a defensible audit trail under retries.

| Failure point | Grounded detail | Preventive control |

|---|---|---|

| OCR confidence drops | OCR reliability can fall on messy layouts; for financial decisions, a 90% or higher threshold is a reasonable benchmark | Enforce minimum confidence thresholds and route low-confidence outputs to human review |

| Status drift between AP and the payout provider | Webhook handlers can run multiple times, event snapshots can be stale, and retries can continue for up to three days | Use duplicate-safe handling, fetch latest provider state before downstream posting, and store processed event IDs |

| Compliance and tax controls get added too late | Incomplete verification can block payouts, and Form 1099-NEC must be furnished to recipients by January 31 | Design verification and tax-document workflows before launch |

- OCR confidence drops before teams react

As invoice formats diversify, OCR reliability can fall on messy layouts, especially merged or inconsistent tables. The practical control is to enforce minimum confidence thresholds and route low-confidence outputs to human review, not just chase a higher touchless rate. For financial decisions, a 90% or higher threshold is a reasonable benchmark.

- Status drift emerges between AP and the payout provider

Webhook handlers can run multiple times, including concurrently, and event snapshots can be stale when processed. Use duplicate-safe handling, fetch latest provider state before downstream posting, and define a clear internal source of truth when statuses conflict. Store processed event IDs and reconcile AP records against provider payout status, because retries can continue for up to three days and drift can appear after initial processing.

- Compliance and tax controls get added too late

If verification checks are incomplete, payment processing or payouts can be blocked, and tiered verification can temporarily pause payouts when additional checks are required. Design verification and tax-document workflows before launch, not after exceptions pile up. For U.S. flows where applicable, if no TIN is provided, backup withholding may need to start immediately, and Form 1099-NEC must be furnished to recipients by January 31.

AP automation can expand team capacity, but "without headcount" only holds up when verification discipline does too. Touchless rate is useful. Clean reconciliation and auditability are the real proof.

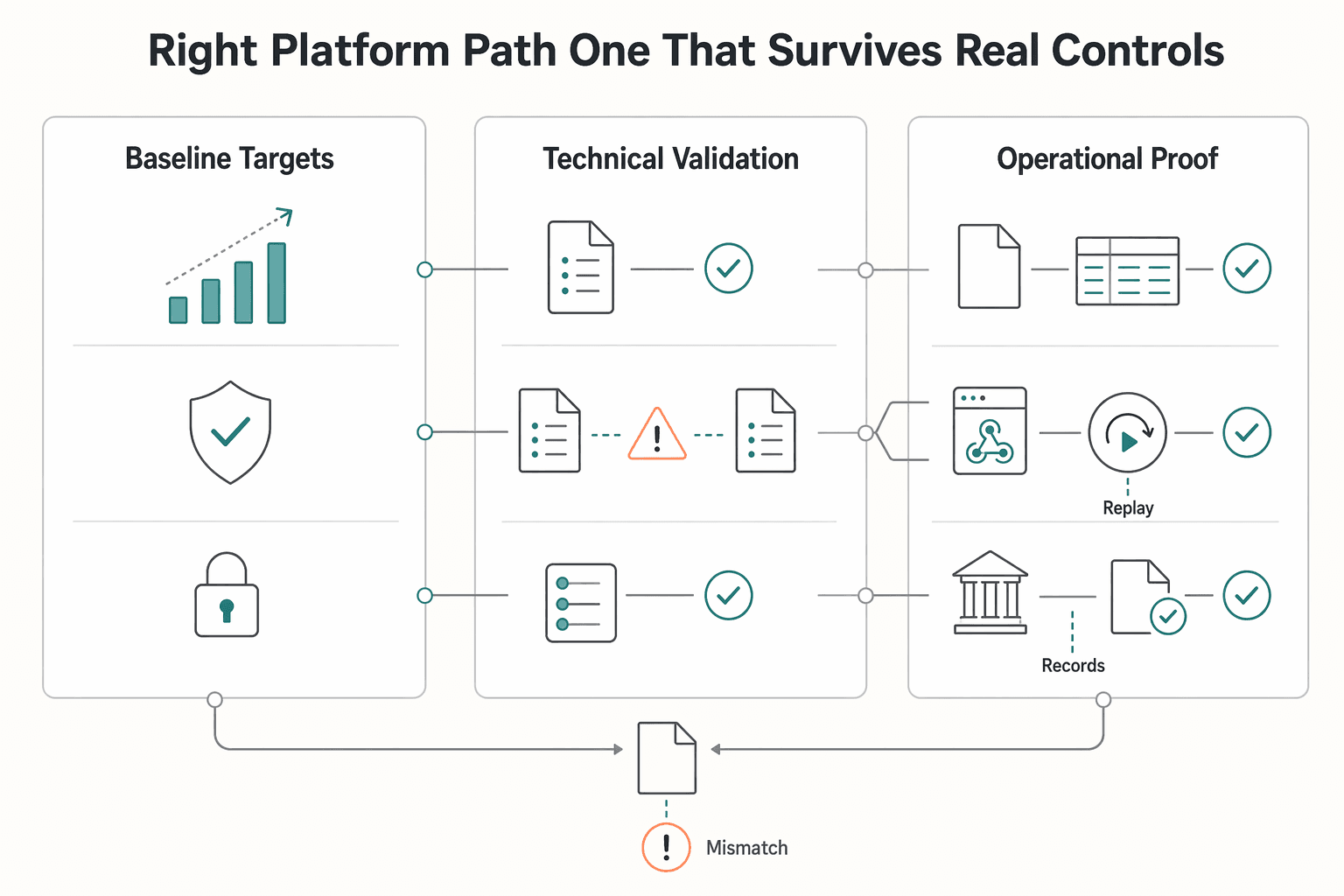

The right platform path is the one that survives real controls and real volume#

Choose the path that fits your growth stage, control requirements, and engineering capacity after go-live, not the platform with the biggest touchless claim.

- Match the path to your operating reality

If your ERP and approvals are stable, an automated invoice processing approach focused on capture, extraction, and approvals may be enough. If payout logic, webhook reliability, and ledger posting are equally critical, a more modular approach may fit better. For multi-country payouts or heavier policy gates, prioritize compliance depth and reconciliation clarity over demo quality. The practical test is simple: can this option produce traceable journals, reliable event handling, and a clear audit trail from source document to payment status without manual patchwork?

- Design exception handling, audit trail quality, and reconciliation up front

AP automation covers the end-to-end payment lifecycle. Automated invoice processing is only the capture, extraction, and approval subset. If your design stops at OCR and routing, manual work can shift downstream into exceptions, status drift, and close cleanup.

Set three non-negotiable checkpoints early:

- Exception handling: define ownership, queue-aging targets, and stop rules for low-confidence OCR, vendor master changes, tax-document gaps, and status conflicts. - Audit trail completeness: sampled transactions should always tie source invoice, extracted fields, approval record, provider or webhook status, and posted journal entry. - Reconciliation discipline: reconciliation means comparing systems of record and resolving differences. If AP records, provider events, and the ledger do not agree, resolve the gap before it compounds.

Also plan for duplicate and delayed events. Webhook delivery is not exactly once, duplicates can happen, and undelivered events may be resent for up to three days. Without idempotent posting, retries can create duplicate side effects.

- Prove readiness in a time-boxed pilot with explicit pass/fail gates

Before full rollout, run a time-boxed pilot and treat it like a canary: limited scope, measured outcomes, and clear continue-or-rollback criteria.

| Pilot checkpoint | What to verify | Fail signal |

|---|---|---|

| Baseline and targets | Track invoices per AP FTE, cycle time, exception backlog, and error-free disbursement quality | No agreed baseline, or success defined only as "more automation" |

| Technical validation | In sandbox or test mode, verify duplicate-safe webhooks, idempotent retries, and journal posting integrity | Duplicate postings, missing events, or no clear status source of truth |

| Operational proof | Sample transactions to confirm source document, approval, payout status, and ledger alignment | Reconciliation breaks, unclear ownership, or unresolved exceptions growing |

If you are SOX-scoped or approaching it, control evidence matters even more: 404(a) requires management to assess ICFR effectiveness, and 404(b) adds auditor attestation. The right choice is the one you can explain, test, and keep reliable under real volume. For the cross-border version of this decision, see International Accounts Payable for Platforms.

If outsourcing is part of the plan, see Accounts Payable Outsourcing for Platforms When and How to Hand Off Your Payables to a Third Party.

If your pilot exposes payout status drift or reconciliation overhead, evaluate a compliance-gated rollout path with Gruv Payouts.

Frequently Asked Questions

How do you scale Accounts Payable without adding headcount in practice?

Scale AP by automating routine steps and moving people to exceptions, vendor issues, and close-quality checks. Start with intake, extraction, routing, and status updates, then confirm each step leaves a clear audit trail. The goal is role reallocation, not removing humans from AP.

What should we automate first in AP if we can only fund one phase this quarter?

Automate the biggest manual bottleneck first. If invoice handling is the constraint, start with intake, OCR extraction, and routing. If payout-status drift is the bigger problem, prioritize webhook handling and reconciliation, then sample invoices to confirm the source document, extracted fields, approval record, and posted journal align.

What does touchless processing include and what still needs human review?

Touchless processing means invoices move from intake through extraction, coding, approval routing, and ERP posting with minimal manual intervention. Human review should still handle low-confidence OCR, policy exceptions, vendor master changes, tax-document gaps, and status conflicts with the ledger. OCR confidence scores run from 0 to 100, and at intake at least 150 DPI is a practical baseline for stronger extraction.

Which KPIs actually prove AP automation is working beyond vendor claims?

Use a balanced KPI set, not just touchless rate. Track cost per invoice, first-time error-free disbursement quality, and cycle time, then add exception backlog and reconciliation defects. That shows whether AP is getting faster and staying accurate.

How should a platform handle AP growth across multi-country payouts and compliance gates?

Use a risk-based control model so higher-risk flows get more scrutiny. Align W-9 collection to U.S. TIN requirements and use W-8BEN when requested by the withholding agent or payer in U.S. withholding or reporting contexts. Assess beneficial-owner identification where relevant, and if foreign financial accounts are involved, review FBAR exposure once aggregate value exceeds $10,000.

When should we choose build, buy, or hybrid for AP automation and payout infrastructure?

Buy first when your team cannot reliably handle retries, duplicate-safe event processing, and ledger posting. Choose hybrid when ERP and approval flows are solid but payout rails or compliance needs do not fit cleanly in one product. Build selectively only where routing or risk logic is truly proprietary, while keeping commodity workflows on proven infrastructure.

What are the most common implementation failures in OCR, webhooks, and vendor reconciliation?

The most common failures happen at the seams between systems. OCR breaks when teams skip confidence thresholds and intake quality checks, webhooks break when teams assume single delivery even though duplicates and retries can occur for up to three days, and reconciliation breaks when AP records, provider status, and ledger journals do not agree. Idempotency is the retry-safety control that helps prevent duplicate side effects.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- advocacy.sba.gov/2026/02/18/fincen-issues-exceptive-relief-to...trusted

- department.va.gov/financial-policy-documents/financial-documen...trusted

- digital.gov/guides/web-analytics-playbook/know-what-your...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- finance.cornell.edu/controller/internalcontrols/unitlevelactivit...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: