Quick Answer

Yes, a platform can manage multi-country accounts payable without a global finance team if control ownership is clear and every payment is explainable end to end. Set who owns approvals, payout release, retries, and close; require traceable status changes and exportable audit records; pilot real corridors under month-end conditions; and verify corridor, entity, tax, and reconciliation support in writing before expanding.

Why multi-country payables get complicated for platforms#

Running international accounts payable platforms multi-country without global finance team is first a control decision, not a tool-shopping exercise. The real choice is where approvals live, who owns payout execution, and how you prove each payment during close or review when something goes wrong.

Accounts payable is still what you owe suppliers for goods or services already received. What changes across borders is the number of teams, systems, and records involved. Finance owns policy and close quality, ops owns execution and exceptions, and engineering may own API integration and money movement behavior. When those lines blur, even a strong vendor stack turns into manual follow-up with no clear accountability.

Before you start#

Use this guide as a decision sequence, not a vendor short list. Cross-border payments are still a multi-year improvement area shaped by legal, regulatory, and supervisory frameworks, so marketing claims can still leave launch blockers at the corridor, entity, or approval level.

Step 1#

Set control ownership before comparing tools. If finance needs tighter policy control, start with approval workflows, payout release rules, and reconciliation evidence. If engineering owns orchestration, retries, and status handling, API depth matters earlier.

That ownership split shapes the rest of this article. You are not only choosing invoice or payout software. You are choosing how requests, approvals, payments, and accounting evidence connect across teams. Lean teams usually struggle when those pieces are split across owners but verified nowhere.

Step 2#

Map the three areas that make or break launch: cross-border payments, approval workflows, and reconciliation. Cross-border execution usually fails on traceability before it fails on coverage. You need to show who approved the payment, the current payout status, and whether the GL matches an independent statement.

In practice, reconciliation means comparing GL balances against independent records and investigating differences. If you cannot do that quickly, adding countries just adds cleanup work. Before launch, test one payment end to end: invoice or request, approval, payout status, posted accounting entry, and an inspection-ready audit trail. If any link depends on inbox searches or spreadsheet comments, the process is not ready to scale. Use payment reconciliation dashboard guidance to standardize that check.

Step 3#

Evaluate vendors against one evidence standard. Tipalti, Routable, Airwallex, Stampli, and Fraxion highlight different strengths, so treat them as different starting points, not interchangeable options.

Tipalti states coverage for cross-border payouts in 200+ countries and territories and 120 local currencies, and positions global scale without adding AP headcount. Airwallex highlights usage by marketplaces and platforms, API money movement capabilities, and 160+ local payment methods across 180+ countries. Routable emphasizes invoice automation, configurable approval workflows, and reconciliation visibility for month-end close. Fraxion positions AP automation inside procure-to-pay. Stampli emphasizes a complete, immutable audit trail.

Do not assume those claims are one-to-one equivalents. Acceptance coverage is not payout coverage, and method counts do not prove fit for your entity setup, approval design, or reconciliation outputs. Build a verification pack with required payout corridors, approval routing, status events, audit-trail exports, and the exact close records finance needs.

That is the sequence this guide follows: centralize ownership and evidence standards, automate what removes manual handling, then verify vendor claims before first live payouts.

What changes when you scale AP across countries with a lean team#

Step 1 Shift the goal from payment success to payment explainability#

As you add countries, payment success is not enough. You need to explain each payment end to end. In Accounts Payable (AP), that means a clear trail from request or invoice through approval, execution, posting, and the final record you can use during review. For issuers, books and records are expected to reflect transactions and asset dispositions in reasonable detail, so a payout without strong Audit records is still a control gap.

A practical check is to pick one completed payment and ask someone outside the day-to-day process to reconstruct it. They should be able to find the original request, approver, payment status history, accounting entry, and an independent statement or provider record confirming settlement. If reconstruction depends on inbox threads or spreadsheet comments, your controls are thinner than they look.

Step 2 Treat multi-currency support as an accounting job, not just a payout feature#

Multi-currency scaling is as much an accounting-control problem as a payout-feature problem. Under IAS 21, a foreign-currency transaction is recorded at the spot rate on the transaction date, and later retranslation can add close work. That makes Multi-currency support a recording and evidence discipline, not just a payments toggle. Also validate FX close behavior against xero multi-currency reconciliation practices.

A common failure mode is approval in one currency, settlement in another, and posting with a different rate than finance expected. The payout can succeed while vendor balances, FX impact, or GL entries stop tying cleanly. Verify early which rate source is used, where it is stored, and whether the rate and settlement currency appear in exportable records.

Step 3 Pause expansion when reconciliation turns into detective work#

Once you scale, Reconciliation is where you prove payment accuracy by comparing records and resolving discrepancies. As you add markets, open items can multiply across currencies, entities, and rails, and cross-border frictions from fragmented messaging standards and data requirements can leave key references inconsistent or missing.

If request-to-payout traceability is slow, treat additional country launches as higher risk until the evidence chain is reliable. Your minimum proof pack should include the invoice or payment request, approval record, currency and rate used, payout reference, status changes, GL posting, and the independent statement line used to reconcile it.

What to prepare before you evaluate any platform#

Do not evaluate vendors until you have documented your current AP process end to end. Without that baseline, polished product claims are easy to overvalue, and implementation gaps usually show up later in reconciliation, compliance, or engineering work.

Step 1 Capture your current evidence pack#

Start with the process you run today. Document invoice intake channels, data extraction, coding, approval routing, invoice matching against PO and receiving records, discrepancy handling before payment, and month-end reconciliation steps.

Use one reconstruction test: hand a recently paid invoice to someone outside the daily workflow and ask them to trace intake, coding, approval, exceptions, payment release, and final reconciliation evidence. If that requires inbox archaeology or individual memory, your baseline is not ready.

Step 2 List your real operating scope#

Define your actual operating scope: entities, payout destinations, settlement currencies, and which markets are live versus planned. Keep knowns and unknowns explicit so vendors are evaluated against real corridors, not a vague global requirement.

Track tax documentation as a separate scope branch, especially for the United States. If U.S. payees are in scope, define who collects Form W-9 and how name and TIN alignment is validated. For foreign persons, track Form W-8BEN as its own onboarding path. For withholding scope, align document flows with a global tax withholding engine.

Step 3 Define non-negotiables before sales calls#

Set three written requirements up front: API integration prerequisites, mass disbursement behavior, and audit-record exports.

For API integration, confirm account setup, authentication flow, and required endpoints, including where country or regulatory scenarios need additional endpoints. For mass disbursements, define failure handling, payout-reference visibility, status-history access, and reconciliation support. For audit records, require invoice-level activity history, including approvals, edits, and communications, plus exportability, including CSV payable-history export if your close process depends on it.

Step 4 Keep one tracker for unresolved vendor questions#

Use one shared tracker across vendors for open questions on country and corridor coverage, entity support, payout destinations, implementation dependencies, support boundaries in the United States and other target markets, export limits, and owners.

Treat published coverage claims as directional until confirmed for your exact use case. Support boundaries can be asymmetric, so require corridor-by-corridor confirmation in writing before procurement. The goal is a short set of verified requirements, explicit unknowns, and clear reject criteria for hidden close, compliance, or engineering risk.

Choose your architecture before choosing a vendor#

Choose the control model first, then shortlist vendors. Your options are AP-automation-led, payout-infrastructure-led, or a hybrid split. That choice determines what you should optimize for in demos.

The processing model drives the integration pattern. Payout-heavy models usually require asynchronous status handling: you submit now and react to later events. AP-led models put more weight on approval routing, exception handling, and audit-trail quality before funds move. This is easier if your payout events follow webhook implementation patterns.

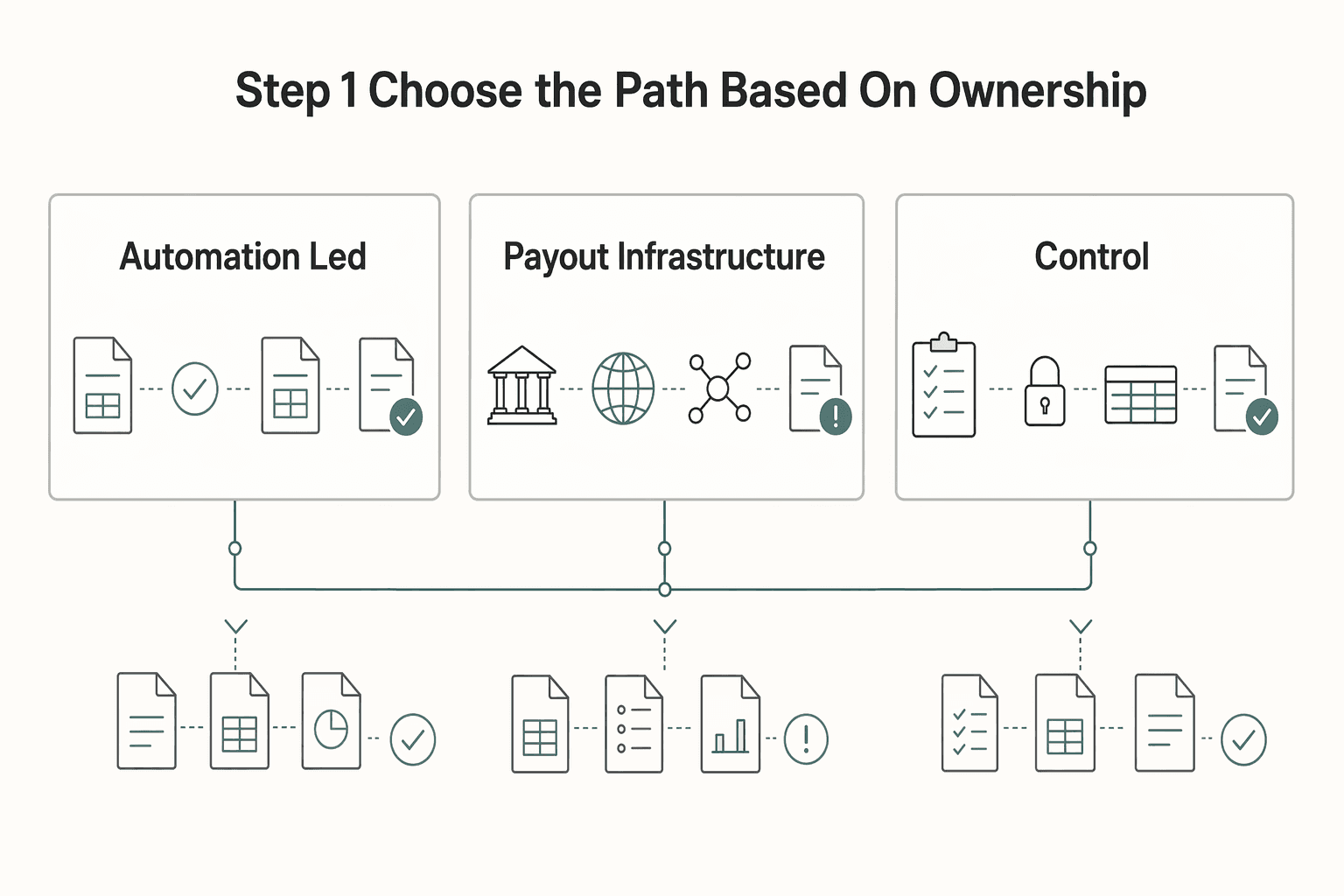

Step 1 Choose the path based on ownership#

AP is more than payout rails. Invoice intake, coding, approvals, payment, and reconciliation are one chain. Pick the path that matches who owns the hardest failures.

| Path | Best fit when | What you gain | What breaks first | Vendor tilt from collected evidence |

|---|---|---|---|---|

| AP automation-led | Finance owns policy, coding variance, approvals, and close quality | Strong approval workflows, policy enforcement, and audit trail before release | Cross-border payout coverage, retry behavior, and rail-level status detail may need another layer | Stampli, Fraxion |

| Payout-infrastructure-led | Engineering owns money movement, retries, status ingestion, and payout orchestration | Strong API integration, event handling, mass payout support, and corridor reach | Finance may need to stitch approvals and audit evidence around payout execution | Tipalti, Routable, Airwallex |

| Hybrid with Platform Payments & Infrastructure plus AP controls | You need engineering-grade payout control and finance-grade approvals | Clear split between approval controls and payout execution | More integration handoffs; reconciliation drift if release IDs do not map cleanly | Usually a combined architecture, not one product |

If the pain is mostly before release, choose AP-led or hybrid. If the pain is mostly after release, such as reruns, status ambiguity, or corridor expansion, choose payout-led or hybrid.

Step 2 Apply one decision rule before demos#

Use one rule: if engineering owns money movement and retries, prioritize API integration. If finance owns process variance, prioritize approval workflows.

Test it with one scenario: a payout times out, the supplier says unpaid, and the invoice is already approved. If engineering owns the outcome, require documented retry behavior, status events, and duplicate-prevention controls. If finance owns it, require approval history, escalation logic, and an audit trail that explains release decisions.

Do not accept feature slides as proof. Ask for API retry docs, webhook or event catalogs, sample status payloads, sample approval-history exports, and payout references used in reconciliation. For reruns, ask exactly how duplicate side effects are prevented. Idempotency is the key concept, but the implementation detail must be explicit.

Step 3 Stress-test every path on the same scenarios#

Use the same three tests for every option so you can compare operator burden directly.

- Failed payout rerun

Simulate a timeout or ambiguous submission status. Verify whether request ID, payout ID, and retry key stay linked, and whether reruns avoid duplicate payment side effects.

- FX timing

Ask when conversion occurs and what triggers the applied rate. Airwallex documents conversion behavior tied to multi-currency wallet balances, so confirm whether FX lands at approval, funding, or payout execution for variance and close control.

- Audit request for cross-border payments and reconciliation evidence

Request one complete trace: approval status and actions, release timestamp, payout status history, and ERP or accounting sync record. Tipalti documents ERP-linked payment status sync, Routable documents 14 webhook events, and Stampli emphasizes approval visibility and audit trail depth. Compare those as evidence, not marketing labels.

Step 4 Score vendors through the same lens#

Tipalti, based on the collected evidence, is payout-infrastructure-led: API-driven payouts across 200+ countries and territories, 120 currencies, 50+ payment methods, plus multi-entity architecture and ERP-linked payment-status sync. Keep open questions explicit: corridor fit for your entities, retry semantics, and country-specific compliance confirmation. For corridor planning, cross-check with a local bank transfer rail map.

Routable also leans API-first, with documented API payables, optional human approval gates, and 14 webhook events. That supports engineering-owned payout flows with finance controls at release points. Open questions remain for non-U.S.-originating entities and deeper AP-control depth.

Airwallex fits payout-plus-FX-heavy designs: API-based global payouts, local clearing in 120+ countries and regions, and documented conversion behavior tied to wallet balances. Unknowns in the collected evidence include approval-routing depth, reconciliation artifact shape, and retry guarantees.

Stampli and Fraxion lean AP-automation-led. Stampli emphasizes multi-level routing, hierarchy-based routing controls, and audit-trail visibility. Fraxion emphasizes policy-driven routing and escalation before financial commitment. For both, treat cross-border corridor and currency capability as unconfirmed unless separately verified.

If you cannot state in one sentence who owns retries and who owns approval exceptions, pause vendor selection until you resolve architecture ownership.

Set the minimum control baseline before first live payouts#

Set your go-live bar around control first and volume second. If a vendor cannot prove approval authority, payout release controls, and traceable status changes end to end, do not send production funds, even if its Mass disbursements demo is strong.

Step 1 Lock approval and release authority#

Separate three decisions before launch: who approves the payable, who releases the payout, and who handles exceptions after release. In shared AP and ops workflows, those owners are often different, so document the handoff from approved to ready for payout to released, with a named owner for each state. Before release, standardize data capture with vendor onboarding automation controls.

Require explicit Approval workflows, not Slack or email signoff. Routable is a practical benchmark: multi-level routing with per-level any or all approval logic, plus visible approval history. In the demo, require one payable to move through approval, release, and an exception path with history visible at each step.

Define escalation before launch: who is paged, who can retry, and what evidence must be attached before the item moves again.

Step 2 Define the audit trail you will accept#

Use a strict standard: an AP audit trail is the documentation needed to verify every event in the accounts payable workflow. For multi-country payouts, your baseline should satisfy internal finance review and external Audit records requests, not just a generic activity log.

Require these fields, or equivalent, in exportable form for each payment event:

- payable or invoice ID

- approver actions and timestamps

- payout release timestamp and actor

- payout or payment order ID

- status transition history

- retry attempts or re-trigger evidence

- webhook delivery or receipt evidence, where applicable

- tax document reference, when relevant

- ERP or accounting sync reference

For regulated flows, retention and retrieval must be explicit. OFAC-covered transactions require full, accurate records and at least 10-year exam availability, and some BSA-required records are retained for 5 years. Do not set one blanket rule across all flows. Map retention by payment type, jurisdiction, and trigger, and confirm the vendor can provide underlying documents if requested before, during, or after a transaction.

Step 3 Place tax compliance checks before funds move#

Put Tax compliance gates before payout release when your entity is the withholding agent. IRS guidance ties withholding to the payment event, so this control cannot be a post-settlement cleanup task. Add pre-release TIN checks using platform TIN matching guidance.

For foreign entities, Form W-8BEN-E documents chapter 3 and chapter 4 status. If a payee claims treaty-rate relief, your payor or withholding-agent process must capture notice of foreign status before release. Policy should name who reviews documents, where they are stored, what blocks release, and how exceptions escalate. If documentation is missing or unclear, treat it as a release blocker. IRS guidance allows conservative withholding treatment, including at least 30% in cases where source or amount facts are unknown at payment time for amounts later determined to be subject to withholding.

Step 4 Block launch if status transitions are not traceable#

Treat this as non-negotiable: you must be able to trace status from approved payable to final payout outcome. Routable documents a payable.status_changed webhook event, Tipalti states payment orders move through progressive statuses, and Airwallex documents webhook delivery, retries, signature verification, and event re-triggering.

Run one failure drill before first live payouts: submit a payment, force an ambiguous or delayed outcome, and verify AP, ops, and engineering all see the same status chain. If the vendor cannot show the emitted event, received event, and matched internal record, block launch. The failure mode is costly and predictable: finance marks paid, the supplier says unpaid, and no one can prove what happened.

Split ownership so lean teams do not become bottlenecks#

Once controls are in place, make ownership explicit. Lean teams become bottlenecks when several functions can block payment decisions but no one is accountable for the cross-functional call.

Step 1 Assign one accountable owner for each decision#

Use a simple RACI for the decisions that create delay: release blockers, retry approval, exception closure, month-end signoff, and vendor escalation. For each decision, assign exactly one accountable owner, and name one DRI for cross-functional International Accounts Payable issues.

That DRI should be the person who drives resolution when product, finance, compliance, and ops disagree. This matters even more in cross-border flows, where regulatory approaches vary by jurisdiction and decisions can bounce between teams without a single owner.

Step 2 Separate policy, execution, and integration reliability#

Use this role split as a starting point, not a universal rule: finance owns policy and close-quality outcomes, ops owns execution SLAs, and engineering owns API integration reliability and retry behavior. Document it as internal control so decision rights, execution responsibility, and monitoring are clear.

Validate ownership with evidence from each function:

- finance: approval and release policy

- ops: SLA targets for review, release, and exception response

- engineering: idempotent retries, backoff for transient failures such as

429, and event history showing retries did not create duplicate payouts

Step 3 Define payment complete the same way across teams#

Use one shared definition of done: payment is complete only when payout status, Audit records, and Reconciliation entries align. Do not treat "sent" or assumed-paid states as complete.

Test this in production-like conditions by forcing a delayed or failed outcome, then confirming internal records, status events, and ledger or external statement evidence still reconcile. Without that check, teams can end up with conflicting statuses and a close process built on an unverified payment.

Implement in a first-90-day sequence with checkpoints#

Use a phased rollout, not a big-bang cutover. If you use a 90-day window, treat it as an operating cadence, not a guaranteed timeline for every platform. Do not add outbound cross-border volume until invoice intake, approvals, and reconciliation are stable enough to explain each payment from request to ledger.

| Phase | Primary focus | Go/no-go checkpoint |

|---|---|---|

| Phase 1 | Stabilize invoice intake, approval routing, and baseline reconciliation reporting; confirm each invoice has a full trail from submitter and approval path to payable record and reconciliation entry | Finance can close a small test population without heroic cleanup, and the team can show written control status, unresolved risks, and accountable owners |

| Phase 2 | Add cross-border payments and limited mass disbursements one rail or one use case at a time; separate validation failures from booking failures and document resubmission steps | Outbound failure and retry controls are proven in writing, with unresolved risks and owners recorded before expanding volume |

| Phase 3 | Expand multi-currency support and broader entity scope only after close quality holds under real operating conditions | Finance signs off on close-process quality, with documented controls, open risks, and accountable owners before adding more currencies, entities, or volume |

Step 1 Stabilize inbound intake before you move money out#

Start with clean Invoice intake, approval routing, and baseline Reconciliation reporting. At this stage, the goal is evidence, not throughput. For a sample set, confirm each invoice has a full trail from submitter and approval path to payable record and reconciliation entry.

Watch for tool sprawl early. When intake, approvals, and reconciliation are split across disconnected workflows, auditability and exception handling become brittle.

Phase 1 checkpoint (go/no-go): finance can close a small test population without heroic cleanup, and the team can show written control status, unresolved risks, and accountable owners.

Step 2 Add outbound payments in a tightly controlled slice#

Introduce Cross-border payments and limited Mass disbursements one rail or one use case at a time. Use payment pre-validation where supported, and separate failure handling for validation failures versus booking failures so recovery actions are explicit. For rail choice, compare to same-day ACH versus wire payout tradeoffs.

In batch flows, correct failed items and resubmit with corrected data. Set release controls before submission, since some provider flows are not cancelable by API after submit.

Run a forced failure test in a safe environment and verify:

- status transitions are clear

- retry ownership is explicit

- resubmission steps are documented

- reconciliation reflects failure state without marking payment complete

Also confirm release blockers up front, including missing tax-status documentation such as Form W-8BEN when requested.

Phase 2 checkpoint (go/no-go): outbound failure and retry controls are proven in writing, with unresolved risks and owners recorded before expanding volume.

Step 3 Expand currencies and entities only after close quality is proven#

Add Multi-currency support and broader entity scope only after close quality holds under real operating conditions. A successful payout is not enough. Finance should confirm approval records, payment status, and reconciliation entries still align as scope expands.

Phase 3 checkpoint (go/no-go): finance signs off on close-process quality, with documented controls, open risks, and accountable owners before adding more currencies, entities, or volume.

Design exception handling before volume#

Do not scale outbound volume until every common payment exception has a clear owner, retry authority, and audit trail. In multi-country AP, the first failure is usually cheaper than the cleanup that follows across ops, finance, and close.

Step 1 Define failure classes your teams can route fast#

Use a short taxonomy with explicit ownership. Start with beneficiary data errors, compliance holds, stale approvals, and posting mismatches between payout status and Reconciliation.

For beneficiary errors, define concrete cases up front: incorrect account number, incorrect recipient institution identifier, or missing beneficiary information. Keep stale approvals defined in writing based on your own trigger, for example approval completed before a material invoice, beneficiary, or amount change, so decisions stay consistent under pressure.

Step 2 Write recovery paths before incidents happen#

Each failure class needs a named action and a named retry owner. Beneficiary-data failures should go back for correction, then be resubmitted only by the owner you assign. Compliance holds should route to compliance or finance review, with separate handling for rejected versus blocked items.

If property is blocked under OFAC rules, initial blocking reports must be filed within 10 business days. Exception records should therefore capture escalation timestamp, reviewer, hold reason, and filing status from day one.

Audit records should include the original payment reference, failure reason, retry or cancellation approver, changed data, and final disposition. For file-based submissions, verify status and reconciliation against the original pain.001 file, not only dashboard events.

For Fedwire ISO 20022 specifically, returns of settled funds use a pacs.004 payment return message. Treat return logic and retry logic as separate controls.

Step 3 Enforce approval-control discipline#

Set one hard rule: no manual workaround that bypasses Approval workflows unless the incident is documented and approved by the designated owner.

Keep incident notes short but complete: why the normal path failed, who authorized the exception, which payment reference was affected, what compensating review was done, and how Reconciliation will reflect the item. This protects management-authorization controls and prevents undocumented control bypasses.

Step 4 Review exceptions weekly and act on cost first#

Use a weekly review cadence to catch drift before month-end. Track counts and aging by failure class, repeat failures by corridor or entity, retries by owner, payout-versus-reconciliation mismatches, and exceptions opened without complete Audit records.

Each week, sample a small set of exceptions and confirm the payment trail, approval trail, and ledger outcome agree. If they do not, pause expansion. Unresolved exceptions can distort close, create duplicate work, and leave gaps in records you may need to keep available for examination for at least 10 years.

Ask vendor questions that force operational clarity#

If a vendor cannot answer AP event handling in writing, treat that as selection risk. You are testing whether finance, ops, and engineering can explain and recover a payment when something fails.

Step 1 Build a scorecard that separates evidence from claims#

Use one scorecard for every vendor with these columns: API integration, Multi-entity support, Multi-currency support, Mass disbursements, and Tax compliance. Add evidence shown and unknowns still open.

This keeps broad coverage claims from hiding corridor-level gaps. Tipalti ties payout scale to multi-entity architecture and cites 200+ countries and territories, 120 currencies, and 50+ payment methods. Airwallex shows different documented scopes: over 200 countries/regions and over 90 currencies in one source, and 200+ countries and regions, 60+ currencies in another. Do not merge those into one number. Mark the scope and confirm which product surface applies to your use case.

Step 2 Ask for exact AP event handling, not general overviews#

Force concrete answers on retries, statuses, and reconciliation artifacts. Ask every vendor:

- What happens after a failed payable or payout: automatic retry, manual retry, or no retry?

- Which status changes are visible to your team, and which require support intervention?

- What artifact exists per AP event: status history, webhook history, export, invoice audit log, or immutable record?

Routable documents that some failed payables are not retried automatically, and unsuccessful payments may end in issue or failed states that can require support to cancel or retry. Airwallex documents webhook retries with exponential backoff over about three days until your endpoint returns 200. Those details define recovery ownership and monitoring design.

Step 3 Require written scope boundaries before procurement moves forward#

Get a written split between generally available features and "where supported" cases by country, currency, or account setup. Airwallex notes that some region and currency capabilities require account-manager confirmation. Routable states capabilities can differ by country and may require additional data, with country-level payment options and regulatory requirements.

Require a corridor matrix in writing: country-by-country payment methods, required beneficiary data, tax-form coverage, and approval behavior. Routable documents multi-level approvals and API tax-form collection for W-9, W-8BEN, and W-8BEN-E.

Step 4 Make unknowns visible vendor by vendor#

| Vendor | Grounded evidence to score | Unknowns to mark openly |

|---|---|---|

| Tipalti | Multi-entity AP positioning; payout API claim for 200+ countries and territories, 120 currencies, 50+ payment methods | Exact corridor coverage, reconciliation artifacts for your AP events, implementation ownership |

| Routable | Payment API, webhook events, country-level capability variation, failed-payment handling, second-level approvals, tax-form collection | Which failed states need support in your flow, exact retry authority, artifact depth for close |

| Airwallex | Broad payout coverage claims, region and currency boundaries, webhook retries over about three days | Which coverage number applies to your path, AP reconciliation evidence, support boundary by region |

| Stampli | Complete invoice audit trails and immutable records | Outbound payout behavior, retry handling, multi-country payment scope if paired with another tool |

| Fraxion | Approval and digital audit-trail positioning on fraxion.biz | SKU-specific AP proof, cross-border payout scope, domain validation because fraxion.com is a different business |

Do not close evaluation with blanks hidden behind "can support" language. If a feature is only available "where supported," record the exact country, currency, payment method, and confirming owner.

Pilot two real corridors before global rollout#

Do not move from vendor selection straight to a broad launch. Pilot two real corridors first, and expand only after the pilot proves close quality, status visibility, and recovery discipline under normal operating pressure. Pick at least one EU pilot lane informed by SEPA disbursement rollout guidance.

Step 1 Pick corridors that expose different kinds of complexity#

Choose two corridors that reflect real business flow and are meaningfully different from each other. Different should mean a different receiving region, currency pair, beneficiary data requirement, or payout method, not just a different country with the same operating conditions.

A constrained live pilot is the right starting posture: start narrow, capture learnings, then add corridors. For each lane, create a one-page corridor sheet with sending entity, sending country, receiving country, currency, payment method, approval path, cut-off assumptions, beneficiary data fields, and expected payout timing.

Step 2 Run the pilot under real approval and timing pressure#

Run the pilot with production-like approvals and real month-end conditions. End-to-end testing matters most when finance is closing, ops is sending batches, and engineering is monitoring status events and retries at the same time.

Do at least two runs per corridor: one smaller batch to validate control points, then one Mass disbursements scenario to test exception handling at volume. Include a run close enough to month-end that finance must reconcile it as part of normal close, not as a side exercise. If you cannot trace a payment from approval to payout result to ledger entry, the pilot is not ready to scale.

Step 3 Inspect batch-level and transaction-level outcomes separately#

Treat batch success and transaction success as separate checks. Payment status reporting should show both overall batch status and individual transaction statuses, because a batch can look complete while some payments fail, stall, or require intervention.

The risk to catch is silent partial failure: ops sees a completed batch, finance assumes funds moved, and Reconciliation breaks later. Require artifacts that prove what happened: batch status export, transaction-level status history, webhook delivery history, approval record, and the close tie-out record.

Step 4 Expand only when the pilot leaves repeatable evidence#

A good pilot is not a payment demo. It leaves repeatable evidence your team can use across new corridors without heroics: finance can close from platform records, ops can isolate exceptions quickly, and engineering can confirm the required end-to-end data stays intact across approval, payout, and reporting.

Use a hard go or no-go gate: expand only after both corridors produce clean evidence packs with the same control checks, exception handling, and close steps. If one corridor still needs spreadsheet rescue or support-led cleanup, fix that before adding countries.

Common mistakes that create expensive rework#

Most expensive AP rework comes from sequencing mistakes, not one dramatic failure. After your pilot, expand only when vendor evidence, control baselines, reconciliation quality, and ownership are explicit and testable.

Mistake 1: Choosing on brand claims instead of operator evidence#

Fix this by scoring vendors on verifiable evidence in Audit records and API integration, not demo polish. Require proof of transaction-level status history, approval records, export fields, and failure or retry behavior. For API reliability, test retry handling and idempotency behavior so the same request is not executed twice during timeouts or network retries.

A practical gate is simple: the vendor can show, in writing or in a live test, how one payment moves from request to approval to payout result to an exportable record.

Mistake 2: Scaling countries before controls are live#

Fix this by enforcing baseline Approval workflows and Tax compliance checkpoints before expansion. Management still owns control effectiveness even when parts of the process are outsourced, so do not treat platform coverage as a control substitute.

In lean teams, duty concentration is a known risk. Separate initiation, approval, and payout release authority where your volume or risk requires it. For U.S. payments to foreign persons, verify you can reliably associate each payment with documentation you can rely on. Without that, default withholding can apply, including the cited 30 percent rule for amounts subject to withholding.

Mistake 3: Letting reconciliation lag behind growth#

Fix this by making Reconciliation a launch gate for every new corridor. Reconciliation is the control that confirms internal records match what you owe and paid, and it is where hidden errors surface.

Require a repeatable close packet per corridor: payout export, batch and transaction statuses, approval evidence, and the close tie-out record. If exceptions cannot be isolated and resolved in the same close cycle, do not scale that corridor.

Mistake 4: Leaving cross-functional ownership informal#

Fix this by assigning one accountable owner for request-to-close AP outcomes across finance, ops, and engineering. Functional teams keep their roles, but one person must own coordination when issues cross boundaries.

Use a one-page ownership map that names who approves policy, who releases payments, who monitors API failures, and who signs off on close quality. Without that single owner, issues sit between teams and rework becomes ongoing overhead.

Conclusion#

The teams that keep multi-country AP lean do it by sequencing the work, not by adding tools or headcount first: assign control ownership, prove traceability, test reconciliation under real pressure, then expand Cross-border payments volume. For country and data constraints, pair your rollout with cross-border payment compliance controls.

If you take one rule from this guide, use this one: do not add the next country until one owner can show authorization, payout status history, and reconciliation evidence for the countries already live.

- Document ownership before you expand scope.

Write down who owns policy, payout execution, and integration reliability. If approval, release, retry, and close review are implied rather than assigned, you are not ready to scale.

- Validate approval and status traceability with evidence, not screenshots.

Use exportable records that show who approved, what changed, and where each payment sits in its status lifecycle. A practical checkpoint is tracing one item from request through approval to final payout status without manual reconstruction.

- Test reconciliation at pilot volume, including a failure case.

Reconciliation is a control, not a reporting afterthought. Include an exception scenario such as a failed payout, stale approval, or posting mismatch, and confirm your team can clear it within the same close cycle.

- Capture vendor limits in writing, especially where support is conditional.

Do not rely on marketing-level coverage claims. Confirm corridor-level support and constraints in writing, including product and region limits such as Tipalti Expenses approval-workflow availability, Airwallex supported-market onboarding, and Routable country and currency delivery support.

- Treat tax documentation as a launch gate, not a later cleanup item.

For U.S.-source payments to foreign persons, payments must be reliably associated with documentation, and Form W-8BEN is submitted when requested by the payer or withholding agent. Without reliable documentation, covered payments can default to 30 percent withholding.

Use this copy-and-paste closeout checklist before the next expansion decision:

- We documented ownership across finance, ops, and engineering.

- We validated Approval workflows, payout status tracking, and Audit records.

- We tested Reconciliation under pilot volume in our live corridors.

- We captured vendor unknowns on coverage, implementation, and Tax compliance in writing.

- We have clear go or no-go gates for the next country expansion.

If you can check every box with records, not assumptions, scale. If you cannot, hold the line and fix the evidence chain first.

Frequently Asked Questions

Can a platform run multi-country AP without building a global finance team?

Sometimes, yes, if the platform and your process remove real manual work instead of just shifting it. Use one operational test: one owner can produce approval evidence, payout status history, and reconciliation records for each live corridor without slowing close.

What minimum controls should be live before scaling international payouts?

Before adding countries, have verifications, reconciliations, authorizations, and approvals live. Separate initiation, approval, and payout release when your risk or volume requires it. If you are making U.S. payments to foreign persons, tie each payment to the required tax documentation, including Form W-8BEN when requested, because many U.S.-source payments otherwise default to 30% withholding.

Should we prioritize coverage, controls, or API integration first?

It depends on who owns the hardest failures. If engineering owns initiation, retries, and batch logic, prioritize API integration first. If finance is absorbing approval variance and reconciliation issues, prioritize controls first, and treat coverage claims as secondary until corridor-level support is proven.

How do we choose between AP automation software and payout infrastructure?

Choose AP automation first when your main bottlenecks are invoice intake, approval routing, ERP sync, and auditability. Choose payout infrastructure first when the constraint is high-volume disbursement control or API-based execution. If neither side covers both control quality and payout execution well enough, use a hybrid model with explicit ownership for retries, release authority, and close evidence.

What should we verify in writing before signing a vendor agreement?

Get written terms for service levels, support boundaries, status updates, exception handling, and exportable evidence for approvals and reconciliation. Confirm what coverage is valid for your contract date and product tier. Also define ownership for W-8 and W-9 intake and any 1099 or 1042 support if U.S. tax workflow is in scope.

How do we pilot international AP without disrupting month-end close?

Run a small pilot through your normal approval and close cycle, not as an isolated side test. Keep the evidence pack tight: payout export, batch and transaction statuses, approval record, and reconciliation tie-out. If exceptions cannot be isolated and cleared within the same close cycle, pause expansion.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumerfinance.gov/rules-policy/regulations/1005/33trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-V/part-5...trusted

- ecfr.gov/current/title-2/subtitle-A/chapter-II/part-2...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-10-design-control-a...trusted

- hhs.gov/sites/default/files/ocio/eplc/EPLC%20Archive...trusted

- irs.gov/forms-pubs/about-form-w-8-bentrusted

- irs.gov/forms-pubs/about-form-w-9trusted

- ojp.gov/tfsc/internal-controls-guide-sheet-508.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: