Quick Answer

Cross-border payment compliance means running two separate control tracks: GDPR and CCPA privacy-transfer requirements for personal data, and KYC/AML payment controls for onboarding, holds, releases, and escalation. In practice, teams should map where data moves, confirm the transfer basis or contract posture, document who owns hold and release decisions, and keep evidence attached to each payout lifecycle step.

What Cross-Border Payment Compliance Covers#

Cross-border payment compliance is two linked jobs, not one checklist: privacy-transfer compliance and payment-control compliance. In the same payout flow, you may need to manage cross-border personal data transfer obligations under GDPR and separate privacy obligations under CCPA. You may also need to run KYC and AML controls that can affect onboarding, payment release, holds, and escalation.

That split matters because the legal triggers are different. Under GDPR, personal data transfers outside the EEA must meet Chapter V conditions. If a destination has an adequacy decision, transfers can proceed without additional safeguards. If not, the path is appropriate safeguards plus enforceable rights and effective legal remedies. Those are privacy-transfer decisions, not payment-screening decisions.

CCPA is a separate lane. California's CCPA regulations govern compliance and provide practical guidance on rights notices, requests, verification, and minors handling. The effective dates cited here for the regulations and amendments are August 14, 2020 and March 15, 2021. Do not treat CCPA language as a GDPR-style transfer mechanism substitute.

On the payments side, AML and KYC stand on their own. FATF frames its Recommendations as an international standard that countries implement through local measures, so one market's control set may not be enough in another. In the U.S. banking context, 31 CFR 1020.220 requires a written, risk-based CIP as part of the AML compliance program. Do not assume that exact rule automatically applies to every non-bank payment platform without checking your actual regulatory setup. Before first live payout, confirm three basics:

- Where personal data leaves the EEA.

- What transfer basis supports that movement.

- Who owns KYC/AML hold and release decisions when payments are blocked.

Keep evidence early, not after an incident. Retain transfer-basis documentation and traceable records for identity checks, payout holds, releases, and escalation decisions.

This article stays at the operator layer: what to implement now, what evidence to keep, and what should trigger legal or compliance review. Because jurisdictions implement privacy and AML rules differently, use this as an operating framework and confirm market-specific requirements with counsel before launch.

For a broader operational view of cross-border rails, costs, compliance, and settlement speed, see Cross-Border Payments Guide for Platform Operators: Rails Costs Compliance and Speed Compared.

Start with a shared compliance vocabulary#

Shared terms are a control, not housekeeping. They determine what gets approved, documented, and escalated.

Under GDPR guidance, a transfer mechanism is the legal route used for transfers of personal data to a third country or an international organization. In practice, that is typically an adequacy decision or appropriate safeguards such as Standard Contractual Clauses (SCCs). It is not the same as saying a vendor is reputable or data is encrypted, and transfer conditions still sit alongside other GDPR obligations.

Keep data localization requirements separate from transfer rules. A transfer can be lawful under GDPR and still fail a local storage mandate. For example, RBI guidance allows payment processing outside India but requires the data to be stored only in India after processing, so your review needs both transfer-path evidence and storage-location evidence.

Apply the same precision under CCPA. A service provider arrangement should map to a written contract with the business, and the business purpose should be specific rather than generic contract-wide language. If you cannot pull the written contract terms and the stated business purpose for a payout-related vendor, treat that arrangement as unverified.

Do not treat CCPA service-provider language as a GDPR transfer mechanism. Keep those terms separate, and your controls are easier to test.

For broader context, see A Guide to GDPR Compliance for SaaS Businesses.

Separate privacy-transfer risk from payment-flow risk#

Treat privacy-transfer legality and payment-flow controls as parallel reviews with shared escalation points. If you collapse them into one approval form, gaps on one side become harder to spot on the other.

| Track | Core decision | What to verify | Typical evidence |

|---|---|---|---|

| Privacy-transfer | Is the cross-border personal-data transfer lawful and correctly contracted? | Whether an adequacy decision applies, or appropriate safeguards such as Standard Contractual Clauses (SCCs) are in place; whether a CCPA service provider or contractor agreement exists when required | Executed SCCs, adequacy assessment record, signed service provider/contractor terms |

| Payment-operations | Should this party be onboarded, monitored, held, or paid? | Customer due diligence status, AML alert handling, monitoring coverage, and payout hold/release criteria under applicable jurisdiction and program rules | KYC file, CDD outcome, alert disposition records, payout decision logs |

| Shared escalation | Does one event change both legal and operational risk? | Whether the same case changes data access, transfer scope, and payout handling | Escalation log linked to the payout case |

On the privacy-transfer track, start with the GDPR route for non-EEA transfers: adequacy decision or appropriate safeguards such as SCCs. For SCC-based transfers, verify the applicable European Commission SCC documentation, including the modernised clauses issued on 4 June 2021. For CCPA-covered disclosures to service providers or contractors, verify the signed agreement for that disclosure. If you cannot name sender, receiver, destination country, and governing transfer document, treat the transfer path as unverified.

On the payment-operations track, anchor decisions to AML/CFT controls implemented through national frameworks, often aligned with FATF Recommendations. FATF expects CDD, so records should show who was screened, what was reviewed, the risk outcome, and who approved payout release when alerts appeared. FATF also announced R.16 changes on 18 June 2025 to improve cross-border payment transparency, including standardized message data for certain peer-to-peer payments above USD/EUR 1,000 where implemented. Do not apply that threshold as universal across all corridors or programs.

Use shared escalation when either track changes the other. This matters most when:

- a new destination country, processor location, or access pattern changes transfer route or CCPA contract posture

- repeated AML alerts or holds, manual overrides, or unusual payout patterns appear in a corridor or counterparty segment

- an investigation needs broader data access than the original payout purpose

Signed transfer paperwork does not replace onboarding and monitoring controls, and a passed KYC check does not establish transfer-law compliance. Keep both tracks distinct, then bring them together at escalation.

Related: Cross-Border Payment Compliance Annual Update 2026: FATCA CRS DAC7 OECD Pillar Two.

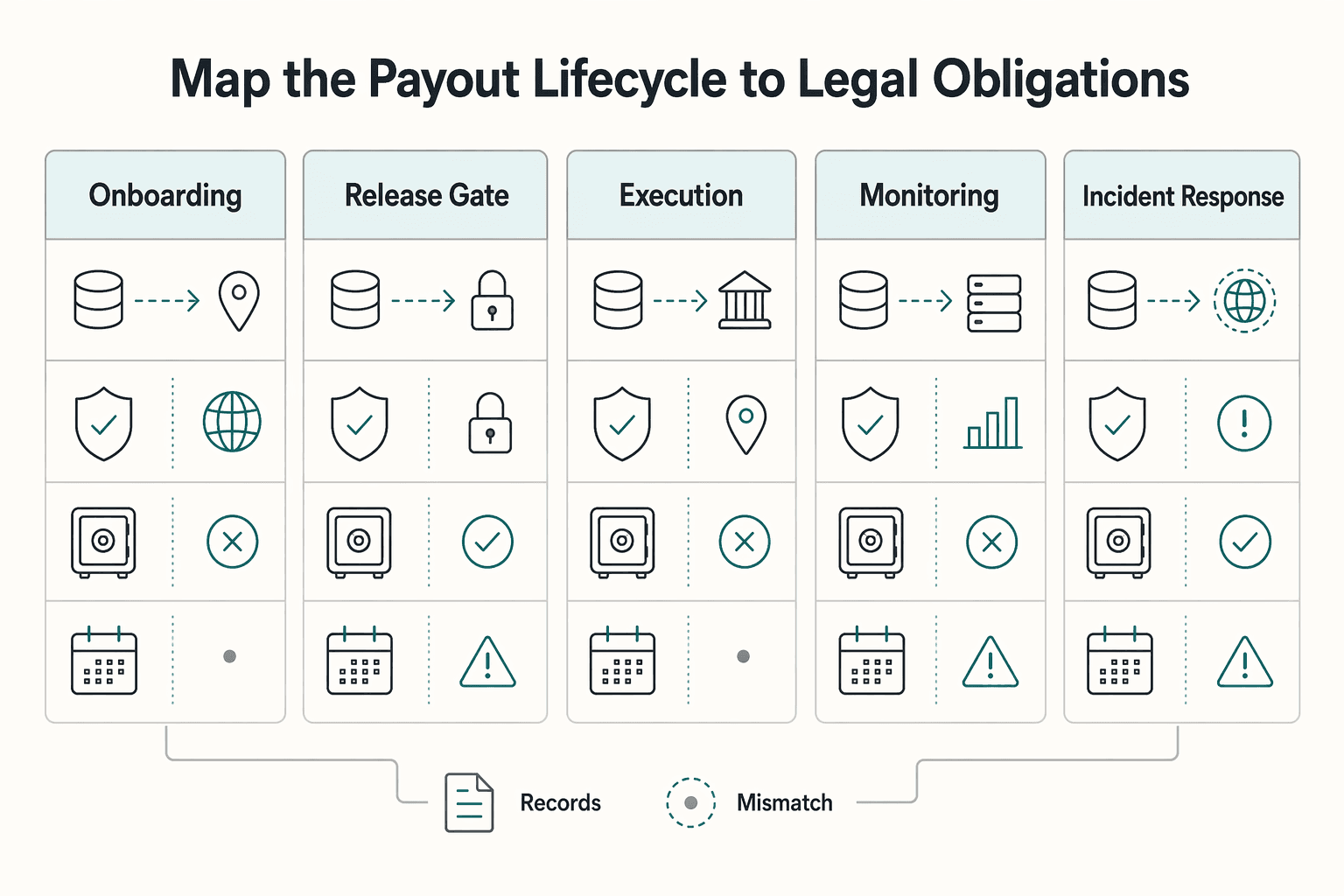

Map the payout lifecycle to legal obligations#

Once the two tracks are separate, map them to the same payout lifecycle. Each step should answer four questions: what data moved, which legal gate applied, whether funds were held, and when ops had to escalate to legal.

| Lifecycle step | GDPR and transfer control | CCPA control | KYC and AML control | Data path and escalation checkpoint |

|---|---|---|---|---|

| Onboarding | Identify whether personal data will leave the EU. If data goes to a third country, apply the Article 44 gate and confirm adequacy or Article 46 safeguards, such as SCCs. | Confirm the recipient is under signed service provider or contractor terms for California-facing data. | Complete CDD/KYC before activation, including screening record, reviewed materials, risk outcome, and approver. | Record sender, receiver, destination country, processor location, and support-access location. If any field is unknown, onboarding is incomplete. If China-linked processing or access is in scope, escalate for PIPL Article 40 localization review before go-live, since localization constraints may apply. |

| Approval | Confirm transfer documents are executed, not draft. Where SCCs are used, verify the modernised clauses issued on 4 June 2021 are the applicable set. | Confirm the contracted party can support consumer-request handling in practice, not only in contract text. | Approve or reject based on CDD outcome and program risk rules. | Require legal review if a new country, processor, or access pattern appears between application and approval. |

| Execution | Limit transfers to data needed to create and settle the payout. If execution sends data outside the EU, log the exact transfer path. | Keep disclosures within the signed service provider or contractor relationship. | Run execution-stage screening and release controls under your AML program. | Add a pre-release checkpoint: if processing shifts to a new region or a manual override follows an alert, hold payout, log reason, and escalate as required. |

| Monitoring | Recheck whether ongoing access, storage, or support changed the transfer route. | Maintain processes to receive and process California consumer requests tied to payout-flow data. | Perform ongoing due diligence and transaction scrutiny; escalate suspicious patterns for reporting analysis. | Repeated holds by corridor, counterparty type, or processor trigger joint transfer-scope and AML-control review. |

| Incident response | Start breach triage immediately; supervisory notification may be due within 72 hours of awareness, with a separate high-risk data-subject notification branch. | Route incidents so California request-handling duties remain operational during containment. | Preserve alert, account, and transaction history needed for suspicious-activity analysis and internal investigation. | Escalate from ops to legal immediately if the incident expands data access, introduces a new transfer route, or requires emergency cross-region sharing. For China-linked incidents, include localization and outbound-transfer analysis where applicable. |

Treat data movement as a release condition#

Do not rely on assumed geography at any payout stage. Treat transfer-path mapping as a release control: exporter, importer, destination country, processor, and support-access locations should be explicit in the case file. If you cannot name that path, transfer analysis is incomplete.

Use three hard checkpoints#

In practice, three checkpoints do most of the work here.

- When data leaves a region

Log the exact change event: new processor, storage region, support-access location, or destination country. For EU data, confirm adequacy or SCC coverage before go-live. For California data, confirm the service provider or contractor contract still matches actual disclosures.

- When a payout is held

A hold can change data access and review footprint, not just payout timing. Capture hold reason, reviewer, review region, and release or rejection decision.

- When ops must escalate to legal

Escalate for new-country exposure, new personal-data sharing patterns, breach events, or China-linked processing that raises PIPL Article 40 localization concerns. Also escalate when repeated overrides or suspicious-activity reviews require broader access than the original payout purpose.

Keep evidence attached to the lifecycle step#

Cross-border controls are harder to operate when transfer records, contracts, and AML evidence live in separate systems. Keep evidence at the decision step. Store transfer mechanism and contract records at onboarding and approval, the CDD file at onboarding, hold and release logs at execution, alert dispositions at monitoring, and the breach timeline at incident response. If one held payout case cannot answer where data started, where it moved, what covered that move, and who approved the outcome, the map is not operational.

Choose the transfer path before you scale volume#

Do not wait for volume to force the decision. For EEA personal data, confirm early whether an adequacy decision applies or whether you need SCCs or another GDPR safeguard for a third-country transfer.

| Transfer path | Use it when | Verify before expansion |

|---|---|---|

| Adequacy decision | Personal data moves from the EEA to a destination covered by an EU adequacy decision | Confirm the destination and recipient match the adequacy path, and record exporter, importer, country, and processing/support-access locations in the case file. |

| SCCs | No adequacy decision applies and you are using contractual safeguards for an EEA-to-third-country transfer | Use the modernised SCCs issued on 4 June 2021, make sure the correct parties signed, and complete annexes so data categories, purposes, and parties are not blank. |

| Hold and escalate | You cannot confirm adequacy, safeguards, or the actual transfer path | Pause rollout, keep that corridor or vendor out of production, and escalate to counsel before routing more personal data through that route. |

GDPR Chapter V (Articles 44 to 50) governs international transfers, so an approval packet that says only "EU data may be processed abroad" may still be a placeholder rather than a transfer decision.

Match the legal path to the contract set#

Your transfer basis and contract posture need to match the real data flow. If you rely on SCCs, the signed SCC package should sit inside the same commercial relationship that handles the in-scope personal data flow. If you rely on adequacy, your data-processing terms should still reflect real roles, purposes, and disclosure patterns.

For CCPA exposure, service provider and contractor terms are operational controls too, with separate obligations and contract limits on reuse or disclosure outside the direct business relationship. Those terms do not replace GDPR transfer documentation. In many flows, you may need both.

A practical check is to open one live vendor file and confirm that signed processing terms, any SCCs, and CCPA service-provider or contractor terms all point to the same legal entity, the same service, and the same data path.

Pause expansion when paperwork lags volume#

If transfer volume is rising but annexes are incomplete, pause expansion and finish the documentation first. There is no fixed legal volume trigger for that pause, but scale increases exposure when the legal path is still ambiguous. Escalate to counsel when any of these are true:

- The destination country or transfer mechanism is unclear.

- The vendor file has CCPA service-provider language but no valid GDPR transfer basis for the same flow.

- The operating model changes data access, review, or retention beyond current contract terms.

- The jurisdiction raises local restrictions or localization questions that adequacy or SCCs alone do not resolve.

Adequacy decisions and SCCs are transfer tools, not blanket approval for every market or operating model. If country setup, processor structure, or review model is unusual, get legal review before adding more volume to that route.

Design for data localization without breaking payouts#

A valid transfer mechanism is not enough on its own. You can satisfy GDPR transfer requirements and still run into local storage or access limits in some jurisdictions. Before adding volume, test your actual payout architecture against data localization requirements.

Start with a concrete map: where payout data is stored, where it is processed, and who can access it from outside the market. That map matters because localization measures can still impede transborder data flows even when your Chapter V transfer path is documented.

Map the real data footprint#

Do not rely on high-level vendor claims like "hosted globally" or "processed regionally." For one live payout flow, record the actual path for onboarding data, payout instructions, fraud review notes, support tickets, logs, and backups.

| Element | What to document | Verification check |

|---|---|---|

| Storage | Primary region, backup region, and any market-specific storage location for payout records and logs | Compare contract terms, product settings, and admin-console region configuration |

| Processing | Where sanctions review, fraud screening, reconciliation, and support handling occur in practice | Confirm whether batch jobs, analytics, or support tools move personal data outside the intended region |

| Access | Which teams, subprocessors, and support staff can view or retrieve records from another country | Test one real access path, including emergency support access |

Watch for side channels. Even if production records are in-region, logs, alerts, or manual review queues may still replicate abroad and create similar compliance risk.

Minimize what leaves the market#

Use data minimization as a default control. GDPR requires data to be limited to what is necessary, and CCPA regulations apply a reasonably necessary and proportionate standard to collection, use, retention, and sharing.

For payout events and logs, keep only the fields needed for settlement, reconciliation, fraud review, or legal retention. Prefer tokenized identifiers, masked account data, and short reason codes, with full-record retrieval reserved for narrower investigation paths.

A practical check is to sample recent event payloads and log entries and challenge each personal-data field. If the only justification is "might be useful later," remove it or gate it behind tighter access.

When localization blocks the preferred vendor flow#

Treat GDPR transfer documentation and CCPA service-provider or contractor terms as related but different controls. CCPA does not directly govern international transfer mechanisms, and those contracts do not resolve jurisdictions that require local storage or local handling.

China is a clear escalation case: PIPL Article 40 includes a domestic storage obligation for certain handlers of personal information collected and produced within China. If China is in scope, escalate early and confirm whether the vendor, hosting model, and support-access pattern can meet local requirements.

If localization blocks the preferred stack, practical options often include:

- Split processing by region for affected markets.

- Roll out market by market where architecture and contracts are already supportable.

When localization constraints are unresolved, a narrower staged model may be easier to implement and govern than forcing one global stack.

Set the minimum control set before entering a new market#

Set a hard launch gate before first payout. If you cannot show a valid transfer mechanism, documented service-provider/contractor arrangements, and live KYC/AML decision points with evidence, you are not ready to launch.

This gate should stay narrow. Teams usually get into trouble when they treat market entry as a contract-filing exercise or overbuild controls that do not reduce first-month risk. The practical test is whether one real payout flow is lawful, reviewed, and controllable.

The launch gate should fit on one page#

Keep the launch gate short and evidence-based. If one item is missing, hold launch.

| Control area | What must be true before go live | What to verify |

|---|---|---|

| Transfer mechanism | For any EU personal data export, Chapter V conditions are identified and matched to the actual flow | Confirm whether the path relies on adequacy decisions under GDPR Article 45 or appropriate safeguards under Article 46, such as Standard Contractual Clauses (SCCs) |

| Service provider arrangements | Vendor contracts for California-linked personal information include required CCPA restrictions and specific business purpose language | Read operative clauses and confirm retention, use, and disclosure are limited to allowed purposes |

| KYC/AML policy gates | Policy defines when payouts are held or released based on onboarding and screening outcomes | Test one onboarding case and one payout release case to verify hold/pass logic in production |

| Operational traceability | Alerts, exceptions, and approvals are attributable to named owners and can be reconstructed later | Pull one completed case and verify timestamps, reviewer identity, reason for decision, and final disposition |

The transfer basis is the key lever. GDPR requires Chapter V conditions before transfer, so you should be able to point to the selected path for each EU export: adequacy where available, or Article 46 safeguards where it is not.

Contracts and privacy terms are necessary, but not enough#

Signed paperwork alone does not close the risk. CCPA service provider arrangements must be specific about business purposes and must restrict retaining, using, or disclosing personal information outside allowed scope. Those terms are necessary, but they do not replace GDPR transfer documentation.

Use one concrete verification step for a vendor in onboarding, fraud review, support, or payout processing. Confirm that the contract entity matches the operating entity, the relevant data types are covered, and the contract posture aligns with your transfer path.

Require evidence that operational gates are real#

Do not accept "we monitor alerts" without proof. Before first live payout, verify that alerts are handled, exceptions have owners, and approval history is traceable. You should be able to retrieve a case showing what triggered review, who reviewed it, whether payout was held or released, and why.

In an MSB context, the baseline is an effective written AML program with policies, procedures, and internal controls. That does not require one approval-chain design, but it does require that KYC/AML gates exist beyond tribal knowledge or ticket comments.

A practical decision rule is to test one pilot cohort before broader release. This is not a universal legal requirement. If you cannot produce audit-ready artifacts for that cohort, do not open contractor or seller payouts at scale. If suspicious activity reporting applies to your entity type, copies of filed SARs and supporting documentation in this cited MSB context carry a five-year retention obligation.

Be explicit about what is not in scope yet#

List controls you are intentionally deferring so their absence is not mistaken for oversight. Common examples include:

- market-wide automation for low-volume manual-review categories

- expansion to additional seller types with different risk profiles

- extra analytics fields or support-tool integrations that increase data movement without changing launch risk

- country-specific enhancements that depend on later legal review or higher volume

Launch when you can show, for one live cohort, a lawful transfer path, contract terms that match data use, and working KYC/AML gates with named owners and traceable decisions. If any artifact is missing, stop before first payout.

Before launch, align your control checklist to an implementation surface your ops and engineering teams can verify in one place: Review Gruv docs.

Assign owners and escalation triggers across teams#

Ownership needs to follow the risk type, and escalation triggers need to be defined before the first exception. That is what gives each payout case a clear, traceable decision trail across legal, compliance, and operations.

A workable split is this: legal and privacy interpret GDPR and CCPA duties, compliance and risk run day-to-day AML controls and monitoring, and finance and payments ops close reconciliation and incident outcomes. This is an operating model, not a universal legal requirement, but it matches what each function should be able to evidence.

| Team | Owner scope | What they should be able to produce |

|---|---|---|

| Legal and privacy | Transfer-rule interpretation, consumer-rights handling, regulator-facing position | Transfer basis for each flow (Article 45 adequacy or Article 46 safeguards such as SCCs), and rationale for exceptions |

| Compliance and risk | Day-to-day AML coordination, monitoring, and escalation | Screening outcomes, alert dispositions, hold/release decisions, and named ownership for ongoing monitoring |

| Finance and payments ops | Reconciliation, payout status control, incident closure | Ledger impact, release/reversal status, closure notes, and proof the operational outcome matches the approved decision |

Keep controller accountability explicit on privacy decisions. Under GDPR accountability, the controller must be able to demonstrate compliance, so transfer choices should not live only in informal channels. For CCPA request handling, make sure intake ownership and timeline handling are clear, including acknowledgement within 10 business days and substantive response within 45 calendar days.

Define the triggers before the first real exception#

Write escalation triggers before launch and make them visible to ops. Typical triggers include:

- transfer documentation is missing, inconsistent, or no longer matches the live entity or vendor flow

- repeated AML monitoring alerts or payout holds on the same corridor, seller type, or rule set without operational resolution

- a data access, deletion, or correction request cannot be fulfilled from current records

- regulator-facing, law-enforcement, or formal complaint requests arrive

- a suspected personal-data breach affects payout records or support tooling

When a transfer path is approved, verify that the contracting entity, operating entity, and actual data recipient match in practice.

Keep one escalation log per payout case#

Use one case-linked escalation log even if execution spans Jira, ticketing, and monitoring systems. This is an operational control choice, but it is usually the cleanest way to preserve traceability when multiple teams touch one event.

At minimum, capture case ID, payout ID, jurisdiction, owner, trigger reason, transfer basis, hold or release status, timestamps, and final disposition. For privacy incidents, record the breach-log entry and whether authority-notification timing is in scope. For AML incidents, record whether the event became reportable and who owns next actions.

Centralized first, then local where complexity warrants it#

For small launches, centralized approvals can improve consistency and help early control fixes. As jurisdiction-specific differences become material, market-level approvals can become more defensible, with central oversight to keep standards aligned.

Use the structure that matches your risk complexity. Centralization can improve efficiency and cross-jurisdiction coverage, but it can also bottleneck local nuance if one queue owns everything.

For a step-by-step walkthrough, see Cross-Border Freelancer Risk Mitigation Through Structure and Compliance.

Build an audit evidence pack that survives review#

Build one standard evidence pack per payout program, corridor, or escalated case so a reviewer can quickly verify the transfer basis, the payout decision path, and the final money movement.

If a reviewer has to infer which entity signed what, or whether a held payout was released or reversed, the pack can fail review even when the underlying decision was reasonable.

Start with the transfer basis and contract posture#

Start by documenting the live transfer basis. For GDPR transfers, keep the applicable adequacy decision when one exists, or executed Standard Contractual Clauses (SCCs) when data moves to a third country without adequacy.

Then include the executed CCPA service provider or contractor agreement where relevant. Treat this as a separate requirement. A CCPA contract does not replace GDPR transfer documentation.

| Evidence lane | What to include | What to verify |

|---|---|---|

| Privacy transfer basis | Adequacy decision reference or executed SCCs, contracting entity and recipient details | Entity names match the live processor, country path matches the actual flow, contract version is final |

| Payment operations | KYC/CIP identity-verification outcome, beneficial-owner checks where relevant, AML alert disposition, payout hold/release history | Case IDs and payout IDs align across systems, and recorded decisions match the documented payout outcome |

| U.S. tax reporting | FBAR, FinCEN references, FATCA-related records, Form 8938 support where applicable | Tax artifacts are labeled separately and not treated as privacy-transfer evidence |

Add the artifacts that explain the payout decision#

Include evidence showing how the payment decision was reached, not just the final status. Keep identity-verification evidence for KYC/CIP, and beneficial-owner identification and verification records where those rules apply.

For AML, keep the alert history and final disposition, including what triggered review, who reviewed it, whether payout was held, released, or reversed, and what evidence supported that outcome. If a case reached suspicious activity reporting, keep that branch complete. Include the SAR timing window (30 calendar days after initial detection, plus up to 30 additional days if no suspect is identified), supporting documentation, and retention handling (five years for SAR copies/supporting documentation).

Keep U.S. tax reporting separate from privacy evidence#

For U.S.-linked programs, keep FBAR, FinCEN, FATCA, and Form 8938 materials in a separate tax-reporting lane from SCCs and service-provider agreements.

FBAR (FinCEN Form 114) is filed with FinCEN, not with the IRS, and Form 8938 does not replace FBAR obligations. FBAR also carries its own threshold and timeline framework, including the $10,000 aggregate foreign-account trigger, April 15 due date, and automatic extension to October 15. FATCA is a separate reporting regime tied to foreign assets held by U.S. account holders, so applicability should be assessed on the facts of each program.

Check the pack before each quarterly review#

Before each quarterly compliance review, run a short evidence QA check. This is an operating control, not a stated legal requirement. Check three items every cycle:

- Completeness: transfer basis is present, service-provider arrangement is executed where relevant, payout decision log is attached, and the case links to KYC/CIP and AML records.

- Retention: records are stored under the correct policy, and SAR-related documentation follows the applicable retention rule.

- Retrieval speed: a reviewer can retrieve the full file within a reasonable time.

Pressure-test retrieval with one approved payout, one held payout, and one escalated case. If legal basis, disposition, and money-movement proof are hard to retrieve, fix indexing before scale increases.

Related reading: How Graphic Designers Protect Cross-Border Payments and Cash Flow.

Avoid the failure patterns that create regulatory surprises#

Regulatory surprises can come from mixing separate obligations or launching before controls are stable. These are the failure modes worth guarding against early.

Do not swap CCPA contract language for GDPR transfer coverage#

CCPA service-provider or contractor terms do not replace GDPR transfer requirements. For EU personal data sent to a third country, your transfer basis must still hold under GDPR Chapter V (Articles 44-50), including an adequacy decision where available or appropriate safeguards such as SCCs.

Before launch, verify that signed entity names, recipient, and country path in your adequacy or SCC record match the processor actually handling payout data. If those records point to the wrong entity or route, you can still have a transfer-compliance gap even when the commercial contract is complete.

Do not launch payouts on untuned monitoring#

KYC and AML controls are ongoing, not a one-time onboarding step. The baseline expectation is customer due diligence, ongoing monitoring, and investigation or reporting of unusual or suspicious transactions. In U.S. banking supervision, SAR filing is a formal required control.

Run a pilot cohort before full rollout and check whether alert handling and reviewer dispositions align with actual money movement, including holds, releases, and reversals. Repeated manual overrides without clear documented disposition can signal that monitoring is not yet stable.

Treat data localization requirements as an architecture input#

Data-localization requirements can create compliance risk even when transfer-law documentation is in place. OECD reporting shows these measures are widespread and increasing in restrictiveness (100 measures across 40 countries by early 2023).

Map where payout data is stored, processed, and accessed, including vendor support access. If localization requirements conflict with your current setup, scope a regional processing design or delay entry until controls are workable. Late discovery can increase compliance burden and fragment operations.

Clear ownership helps reduce surprises: legal for GDPR, CCPA, and localization interpretation, compliance for KYC/AML execution, and operations and finance for reconciliation and closure. If a high-risk exception has no named owner or escalation deadline, treat it as unresolved risk.

Roll out in phases and verify before each expansion step#

A phased rollout can help keep controls stable while you scale. Lock the transfer path first, expand only when control evidence is repeatable, and revalidate each cohort before go-live.

Phase 1 starts with one corridor and one documented transfer decision#

Use one payout corridor as a proof point and document the GDPR transfer basis before volume grows. For that route, confirm whether the transfer relies on an adequacy decision or on appropriate safeguards such as SCCs, since those are distinct paths.

Before expansion, verify the actual country path, the receiving entity, and that contracts match that route. If adequacy is not available, document the safeguard path before expansion rather than deferring it.

Phase 2 is an internal gate, not a victory lap#

Treat Phase 2 as an internal governance gate, not a legal entitlement to launch. This gate is not a statutory requirement under GDPR, CCPA, or FATF, but it helps confirm the pilot can be repeated without control drift.

Review more than document presence. GDPR calls for regularly testing, assessing, and evaluating technical and organizational security measures, so use this phase to check control effectiveness and close or formally track unresolved escalations against your pre-agreed criteria.

Phase 3 expands in cohorts and revalidates assumptions each time#

Expand in small cohorts and revalidate privacy and monitoring assumptions each time. FATF's risk-based approach and ongoing implementation assessment support recurring checks as corridor risk and transaction patterns change.

For California exposure, keep governance checkpoints current with regulatory updates. CPPA lists completed regulation packages, including a package in September 2025, and states specified regulations became effective on January 1, 2026.

Keep a standing change log or your controls will age out#

Maintain a standing change log for regulatory updates, contract amendments, vendor-routing changes, and transfer-mechanism revisions. The log should show what changed, who reviewed it, and whether reapproval was required.

Use one trigger consistently: if a new market changes the data route, legal basis, or AML risk profile, treat it as a revalidation event rather than a copy-paste launch.

Conclusion#

The most defensible approach is operational: run transfer-law controls and payment controls as separate tracks, then connect them through clear senior ownership, escalation, and retrievable evidence.

That separation reflects different duties. GDPR Chapter V requires transfer conditions to be met for third-country transfers. AML/CFT controls follow a separate FATF risk-based approach focused on identifying and prioritizing financial-crime risk. CCPA adds contract discipline for service-provider processing on behalf of a business under a written contract. When teams merge these into one generic checklist, gaps get easier to miss.

Before scaling, run a concrete check on one corridor, one receiving-entity type, and one live or pilot payout path. Confirm you can show the transfer map, the documented transfer basis, the CCPA contract posture when California data is in scope, and payment-side records showing key control decisions and escalations. If any artifact is missing, incomplete, or ownerless, treat that as a control gap.

Accountability requires more than policy text: you must be able to demonstrate compliance. For CCPA-linked operations, consumer-request records and response handling must be retained for at least 24 months, so your review should confirm those records are retrievable.

Use this as the immediate next step:

- Map actual transfers first using the EDPB "know your transfers" sequence.

- Verify transfer mechanism and contract terms against the real payout path.

- Test one end-to-end evidence file, including decision history and alert disposition.

- Log missing artifacts, unclear ownership, and route-change triggers before increasing volume.

This structure can reduce surprises without overbuilding controls your team cannot maintain. If you need to validate market-by-market payout controls and escalation coverage before expansion, talk with Gruv.

Frequently Asked Questions

What does cross-border payment compliance mean under GDPR and CCPA in practical terms?

In practice, one payout flow must pass two separate tests. GDPR covers whether personal data can lawfully move to a third country under Chapter V, usually through adequacy or safeguards such as SCCs. CCPA separately governs service-provider or contractor handling, so contract terms and business purposes must match the real payout path.

Do SCCs and CCPA service-provider terms both apply to the same payout flow?

Yes. They often apply together because they solve different problems. SCCs support the EU transfer path, while CCPA service-provider or contractor terms restrict how California personal information may be retained, used, or disclosed.

What is the minimum control set before launching payouts in a new market?

At minimum, have a valid transfer mechanism, executed service-provider or contractor terms that match the actual route, and live KYC/AML decision points with evidence. Before first payout, you should be able to show alert handling, exception ownership, and approval history for a real case. If any artifact is missing, hold launch.

How should legal, compliance, finance, and payments ops split responsibilities?

A workable split is legal and privacy on GDPR and CCPA interpretation, compliance and risk on AML coordination and monitoring, and finance and payments ops on reconciliation and case closure. Keep handoffs traceable so each escalation and decision has a named owner.

What events should trigger immediate escalation to legal counsel?

Escalate immediately when transfer documentation is missing or no longer matches the live route, when a new country or data-sharing pattern appears, when vendor use may exceed agreed purposes, or when a suspected personal-data breach affects payout records or support tooling. Also escalate repeated holds, overrides, or suspicious-activity reviews that require broader data access than the original payout purpose. China-linked processing that raises localization concerns is another trigger.

What evidence should we retain for an audit-ready cross-border payout program?

Retain the transfer basis for each corridor or flow, such as adequacy rationale or executed SCCs, plus executed service-provider or contractor agreements where relevant. Keep KYC/CIP or CDD records, AML alert history, hold and release logs, escalation records, and change-log approvals. The file should let a reviewer quickly see where data moved, what covered that move, who approved the payout decision, and the final outcome.

How do data localization requirements change architecture and vendor choices?

Data localization is separate from transfer-law analysis and can still block an otherwise documented transfer path. It changes architecture and vendor choices by forcing you to map where payout data is stored, processed, and accessed, including support and backups. If localization conflicts with the preferred stack, use regional processing or delay entry until the setup is workable.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cppa.ca.gov/regulations/pdf/ccpa_statute.pdftrusted

- cppa.ca.gov/faq.htmltrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalregister.gov/documents/2016/05/11/2016-10567/customer-due...trusted

- irs.gov/businesses/comparison-of-form-8938-and-fbar-...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- oag.ca.gov/privacy/ccpa/regstrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: