Quick Answer

Start by scoring each target market on evidence readiness. In this cross-border compliance annual update 2026, the clearest operational anchors are U.S. Form 8938 and separate FBAR handling, plus EU OSS mechanics such as scheme selection and filing cadence. Launch only where you can show named owners, documented threshold or exclusion checks, and traceability from request through reconciliation. If BOI, DAC7, CRS, or Pillar Two obligations are still assumption-based in your file, limit scope to a pilot or pause.

Separate stable obligations from moving signals#

Treat 2026 as a split compliance environment, not a single global trend. Requirements can differ across markets, so launch readiness has to be judged market by market. The practical question is simple: where are your controls already strong enough for first payout, and where are they not?

Start by separating stable obligations from moving signals. On the stable side, U.S. foreign-asset reporting remains in force. The IRS Form 8938 page, last reviewed 31-Mar-2026, shows no recent developments, and the Form 8938 instructions state that section 6038D reporting obligations are not affected. For specified domestic entities, Form 8938 may apply when specified foreign financial assets exceed $50,000 on the last day of the tax year or $75,000 at any time during the year. It is filed with the annual return by that return's due date, including extensions.

Do not treat Form 8938 and FBAR as substitutes. The Form 8938 instructions explicitly state that filing Form 8938 does not remove the requirement to file FinCEN Form 114, or FBAR. Before first payout, confirm who owns that determination and where the supporting record is kept.

Execution friction is the other part of the 2026 picture. Many cross-border payments still depend on correspondent banks and multiple intermediaries, which can make flows slower and more expensive. ECB reporting notes that only 40% of international B2B transactions settle within one working day. Nearly one-third of cross-border payments cost more than 3% of the amount sent. Global correspondent banking provision is down 20% versus the mid-2000s.

This cross-border compliance annual update 2026 is for founders and operators making launch decisions, not just tracking headlines. Use it to decide where to launch, where to wait, and what must be true before money moves. If you cannot verify entity classification, reporting ownership, and exception traceability from initiation through reconciliation, you do not have launch readiness yet.

Scope is intentionally narrow: FATCA, CRS, DAC7, OECD Pillar Two, CTA/BOI status, and cross-border payments implementation signals. Where public detail is incomplete, that uncertainty is called out directly. This is not country-by-country legal advice.

For recurring obligation tracking, use Build a Global Contractor Payment Compliance Calendar for Monthly, Quarterly, and Annual Obligations.

The 2026 compliance shift founders cannot ignore#

The main shift is not one new global rule. For practical planning, separate what is operationally clear from what is still directional or unverified. If you operate across jurisdictions, set a highest-common-denominator baseline first, then localize down only where that is legally justified.

| OSS point | Supported detail |

|---|---|

| Deemed supplier status | Confirm that status before go-live because it changes who is treated as making the supply. |

| Member State of identification | It is defined by the scheme and establishment facts. |

| Union and non-Union schemes | Returns are quarterly. |

| Import scheme | Returns are monthly. |

| OSS VAT returns | They are additional and do not replace domestic VAT returns. |

| Record set | Keep OSS registration evidence, return calendar, and audit record location together. |

| Exclusion risk | A Member State can exclude a taxable person or intermediary from an OSS scheme. |

| VAT Cross-border Rulings request | File it under the national VAT-ruling conditions of the country where you submit it. |

Before you change launch plans, separate verified signals from commentary. You may hear that U.S. CTA/BOI direction is narrowing while Europe is coordinating through AMLA or an EU Single Rulebook, but these materials do not establish those U.S., AMLA, or Single Rulebook points directly.

What is verified here is EU-side coordination in VAT administration. Under OSS, a taxable person can register in one Member State for covered cross-border supplies, and the Member State of identification is defined by the scheme and establishment facts. OSS can simplify filing, but OSS VAT returns are additional and do not replace domestic VAT returns. If your platform may be treated as a deemed supplier, confirm that status before go-live because it changes who is treated as making the supply. In practice, keep ownership and records explicit:

- Confirm which OSS scheme applies and your Member State of identification.

- Run to the filing cadence: quarterly for Union and non-Union schemes, monthly for the import scheme.

- Keep OSS registration evidence, return calendar, and audit record location together.

- Account for exclusion risk: a Member State can exclude a taxable person or intermediary from an OSS scheme.

- If you need a VAT Cross-border Rulings request, file it under the national VAT-ruling conditions of the country where you submit it.

That gives you a practical baseline for the rest of this guide: act on the mechanics you can name and document, and treat everything else as a validation item until it is proven. For the freelancer-risk structure behind that baseline, read Cross-Border Freelancer Risk Mitigation Through Structure and Compliance.

Core terms and why each one changes payment-market choices#

Do not treat these terms as interchangeable when planning rollout. In these sources, only FATCA-linked Form 8938 mechanics and the separate FBAR requirement on FinCEN Form 114 are operationally defined. For CRS, DAC7, OECD Pillar Two, BOI, and foreign reporting company, use this as a prompt to validate locally before you lock product rules or market sequencing.

| Term | Plain-language meaning supported here | Why this matters for platform rollout |

|---|---|---|

| FATCA | A U.S. regime name shown in IRS Form 8938 materials, Foreign Account Tax Compliance Act. | It can require specified persons to report specified foreign financial assets above applicable thresholds, which affects year-end data readiness. |

| Common Reporting Standard (CRS) | Confirm with the relevant authority. | Treat as a prompt for market-specific tax or reporting review, not as a rule set you can implement directly. |

| DAC7 | Confirm with the relevant authority. | If it appears in diligence, pause and confirm country-specific obligations before finalizing onboarding fields or reporting ownership. |

| OECD Pillar Two | Confirm with the relevant authority. | Do not assume rules, rates, or timelines when making entity or expansion decisions. |

| BOI | Confirm with the relevant authority. | Do not assume filing scope or ownership responsibilities without U.S. legal confirmation first. |

| foreign reporting company | Confirm with the relevant authority. | Treat as an entity-classification and responsibility question that needs documented legal validation. |

The U.S. term that actually changes day-to-day operations#

For day-to-day operations, Form 8938 is the verified anchor. IRS materials state that Form 8938 is used to report specified foreign financial assets, including foreign financial institution accounts, when the filer is a specified person and thresholds are met. The cited thresholds include an aggregate-value trigger of $50,000 for certain filers, and for certain specified domestic entities, $50,000 at year end or $75,000 at any time during the year.

That has direct implications for onboarding and reconciliation. Form 8938 captures taxpayer identification number, filer type, asset and account inventory, and whether foreign assets were acquired or sold during the tax year. Your records need to support counts, maximum values, and lifecycle changes, not just static account existence.

What this changes operationally#

Treat reporting cadence as a hard control point. Form 8938 is attached to the annual return and due with that return, including extensions. Keep FBAR separate in your controls, because filing Form 8938 does not replace FinCEN Form 114.

For entity planning, confirm before rollout whether your structure could be treated as a specified domestic entity if it holds specified foreign financial assets. For partner due diligence, verify where accounts are maintained, since some accounts tied to U.S. institutions or branches are excluded from Form 8938 reporting.

Where the uncertainty boundary is#

Keep the boundary clear in this update. The source set supports Form 8938 and FBAR mechanics, but it does not provide jurisdiction-level implementation detail for CRS, DAC7, OECD Pillar Two, BOI, or foreign reporting company. If those terms are driving go-live choices, get market-by-market legal validation before implementation.

For a concrete VAT-validation task, use How to verify a European VAT number using the 'VIES' system.

Expansion market comparison for 2026 compliance friction#

Once the terms are clear, compare markets by the mechanics you can actually operate before first payout. CTA/BOI, AMLA and the EU Single Rulebook, and FSB or G20 signals are escalation flags here, not implementation specs.

| Regime signal | Key named rules or mechanisms | Likely operator burden | Evidence required before launch | Escalation owner |

|---|---|---|---|---|

| U.S. entity-transparency signal | CTA, BOI | Verify filing scope and applicable exemptions with a qualified adviser. | Entity chart, registration facts, ownership memo, written U.S. legal view on BOI status and filing responsibility | U.S. legal with compliance |

| EU coordination signal | AMLA, EU Single Rulebook | Directional only. Useful for posture, not enough for operating rules. | Country-specific legal note, control-mapping memo, named owner for local interpretation | EU legal with compliance |

| EU cross-border VAT execution | OSS, CBR, Member State of identification, deemed supplier | Concrete if prepared up front. Work concentrates in scheme choice, records, and filing cadence. | VAT registration proof, scheme-selection memo, deemed-supplier analysis, record-keeping design, CBR plan when treatment is unclear | Tax with payments ops |

| Cross-border payments implementation pressure | FSB, G20 Roadmap for Enhancing Cross-border Payments | Not covered as a direct operator rule here. | Provider documentation for traceability, reconciliation outputs, exception handling, payout-timing assumptions | Payments ops with partner management |

Do not confuse lower near-term complexity with lower risk. If your launch case depends mostly on directional U.S. or global signals without a clear filing owner, required records, and timing, you are deferring compliance work, not reducing it.

By contrast, EU VAT execution gives you usable mechanics now. OSS allows registration in one Member State for covered VAT declaration and payment, with reported simplification benefits of up to 95% red-tape reduction. That benefit depends on getting scope, scheme choice, and records right on day one.

If you use OSS, two controls matter most: return cadence and scope completeness. Returns are quarterly in the non-Union and Union schemes, and monthly in the import scheme. If you use a scheme, all supplies under that scheme must be declared through OSS. Confirm your Member State of identification early, because in certain Union-scheme cases it binds the current calendar year plus the next two.

Use CBR when VAT treatment is genuinely unclear. It supports advance rulings on complex cross-border VAT transactions. Requests must be filed in a participating country where you are VAT-registered and must follow that country's national VAT-ruling conditions.

Decision checkpoint#

- Advance launch when operating mechanics are concrete and owners are in place. In this material, that is usually an EU VAT case with documented registration, scheme choice, records, cadence, and deemed-supplier treatment.

- Limit launch scope when the commercial case is strong but the regime signal is still directional. Require written legal interpretation before broader rollout.

- Hold launch when the market case depends on unsupported assumptions about CTA/BOI, AMLA or the EU Single Rulebook, FSB or G20, CRS, DAC7, or OECD Pillar Two, and you cannot name the filing owner, required records, and escalation path.

For the country-by-country payout checklist, read Cross-Border Compliance Checklist for Platform Payouts: Licenses Registrations and Reporting by Country.

U.S. reporting scope changed and entity classification now decides risk#

For U.S. entity-transparency questions, the safe reading here is restraint. Treat BOI scope as undetermined in this material and make decisions from verified entity facts, not policy interpretation. The sources provide operational detail for FBAR, FinCEN Form 114. They do not provide BOI rule text, a BOI exemption map, or a supported definition of a foreign reporting company under an Interim Final Rule analysis.

What to do at onboarding#

At onboarding, capture entity facts early: legal name, formation jurisdiction, U.S. registration status, ownership chain, and control. If those facts are incomplete or inconsistent, trigger legal review and require a written BOI status memo with a named owner, filing conclusion, and document location.

Use this internal operating rule: if ownership and registration facts are not cleanly established, escalate for legal review before deciding on payout activation, and document BOI status. That is a control choice, not a legal claim from this material.

Keep FBAR work separate from BOI work#

Do not treat FBAR readiness as BOI readiness. In this material, FBAR is operationally specified, and the practical U.S. reporting mechanics are FBAR-specific:

| Control point | Supported detail |

|---|---|

| BOI relationship | Do not treat FBAR readiness as BOI readiness. |

| Filing threshold | File FBAR, FinCEN Form 114, when one account maximum, or aggregated account maximums, exceed $10,000 during the calendar year. |

| Below-threshold case | If the threshold is not reached, FBAR is not required on that test. |

| Fewer than 25 accounts | If aggregate maximum value cannot be determined, item 15a allows "amount unknown". |

| Exchange rate | If no Treasury Financial Management Service exchange rate is available, use another verifiable rate and keep the source. |

| Due date | Due April 15 with automatic extension to October 15. |

| Correction | If a prior FBAR is wrong, submit a new FBAR and mark it as an amendment. |

| BSA e-filing XML | Missing required XML elements can cause rejection. |

Those are FBAR controls. BOI scope and accountability still require a separate legal determination.

EU and OECD signals that affect cross-border payout rollout#

If you cannot maintain one evidence standard across EU markets, delay a multi-country launch and start with a one-jurisdiction pilot. Here, the most concrete rollout constraints come from EU VAT operations, especially OSS and CBR. AMLA, the EU Single Rulebook, DAC7, CRS, and OECD Pillar Two are planning signals, not detailed rulebooks you can implement from this evidence alone.

Coordination matters more than local improvisation#

Treat AMLA and the EU Single Rulebook as coordination signals, not operational specs. The practical implication is straightforward: do not improvise market by market on onboarding evidence, tax classification notes, or exception handling for the same payout model.

The harmonization pressure you can actually see is in OSS design: one Member State of identification, a centralized declaration and payment flow, and defined record-keeping and audit expectations. That structure raises the cost of fragmented controls across markets.

The concrete EU levers you can actually design around#

The first design choice is your OSS Member State of identification. Where multiple fixed-establishment options exist, that choice is binding for the calendar year plus the next two years and cannot be changed freely unless the current fixed establishment is dissolved.

| Lever | What it changes operationally | Risk if mis-scoped |

|---|---|---|

| OSS Member State of identification | Registration owner, filing location, scheme administration | Locked into a weak setup for the current year plus two following years |

| OSS scheme type | Return cadence and reporting design | Non-Union and Union are quarterly; import is monthly |

| OSS scope rule | Data mapping and reconciliation coverage | Supplies under that scheme must be declared via its OSS return |

| VAT Cross-border Rulings, CBR | VAT treatment path for complex cross-border transactions | Delay or inconsistent treatment if you rely on assumptions instead of an advance ruling |

Before launch, run one live-like flow from onboarding to return-ready records. Confirm the classification path, scheme choice, cadence, and ownership for records, audits, and scheme exit handling.

Where DAC7, CRS, and Pillar Two may affect sequencing#

Treat DAC7, CRS, and OECD Pillar Two as potential sequencing constraints for market entry and legal-entity planning, but do not treat this material as a source for their thresholds, deadlines, or implementation mechanics. If legal, tax, and payments operations cannot produce one shared evidence pack across markets in scope, do not scale regionally yet.

Start with one country, validate the classification and reporting path, then expand. For complex multi-party VAT questions, use CBR where available and file in a participating country where the taxable person is VAT-registered, under that country's national VAT ruling conditions. Country program detail varies, so legal validation is required before final launch commitments.

For a step-by-step walkthrough, see Digital Rupee Cross-Border Payments for Freelancers in 2026.

Cross-border payments execution signals from FSB and industry#

Execution pressure matters even when the rule text does not come from your direct regulator. Treat the Financial Stability Board, or FSB, as a signal that expectations can tighten across banks, partners, and payment providers.

| Check | Supported detail |

|---|---|

| Provider-level evidence | Tie payout timing and traceability promises to provider-level evidence, not marketing language. |

| Status visibility | Before launch, require proof of status visibility. |

| Exception ownership | Before launch, require proof of exception ownership. |

| Timing claims | Before launch, require documented limits on timing claims. |

| Traceability test | Run a live-like flow to confirm that the payout can be traced from request through provider records into your reconciliation output. |

| Customer-facing promises | If that chain is unclear, avoid precise timing or end-to-end tracking promises. |

On 12 March 2026, the FSB announced a new implementation phase under the G20 Roadmap for Enhancing Cross-border Payments after the FSB Cross-border Payments Summit. The roadmap focus is practical outcomes. With 2027 approaching, the message is delivery pressure: public authorities are being encouraged to produce action plans, and industry is expected to deliver tangible end-user benefits.

That is why Swift and the Institute of International Finance, or IIF, matter as operator signals, not just background commentary. The IIF position on February 6, 2026 emphasized operationalizing existing standards rather than creating new policy and flagged inconsistency risk across frameworks. In practice, if your teams rely on mixed provider and partner assumptions, you can end up with mismatched product claims, support scripts, and audit evidence.

For planning, tie payout timing and traceability promises to provider-level evidence, not marketing language. Before launch, require proof of status visibility, exception ownership, and documented limits on timing claims. Then run a live-like flow to confirm that the payout can be traced from request through provider records into your reconciliation output. If that chain is unclear, avoid precise timing or end-to-end tracking promises. For privacy and localization constraints, read Cross-Border Payment Compliance: GDPR CCPA and Data Localization Requirements.

Minimum evidence pack to approve a new market launch#

Do not scale a new market unless each launch artifact has a named owner and a review trail. The minimum pack is not every possible document. It is the set you need to prove Form 8938 and FBAR decision ownership, filing checkpoints, and exception handling before first live volume.

Provider transparency only helps if your own file shows what was approved, which assumptions were accepted, and who acts when those assumptions fail.

What the launch file should contain#

Use one approval file per market, even when one product launches across multiple countries. Keep it short, assignable, and reviewable. Red line: no broad launch if ownership is unclear between legal, tax, compliance, and payments operations.

| Control item | Primary owner | Minimum artifact | Why it belongs in the file |

|---|---|---|---|

| Filer-scope note | Legal and Tax | Short memo naming filer type assumptions (for example, specified person checks) and account-holder structure | Form 8938 scope depends on who files and what assets are in scope |

| Form 8938 threshold checkpoint | Tax | Threshold test note for the applicable filer category; for certain specified domestic entities, include the $50,000 year-end and $75,000 any-time tests | Form 8938 filing is threshold-based, not automatic |

| Form 8938 exclusion checkpoint | Tax or Compliance | Note on applicable exclusions, including whether any account is maintained by a U.S. payer | Prevents unnecessary or incorrect Form 8938 reporting |

| Form 8938 / FBAR decision note | Tax or Finance | Brief note on whether account structure creates a Form 8938 or FinCEN Form 114 review point, plus escalation path | Prevents treating one form as a substitute for the other |

| Annual return attachment checkpoint | Tax | Filing checklist that Form 8938, when required, is attached to the annual return by the return due date, including extensions | Converts policy into a concrete filing control |

| Update review log | Tax or Compliance | Dated reminder to re-check Form 8938 form/instructions before filing cycles | The form and instructions can be updated over time |

Tax document controls that matter before activation#

For U.S. tax controls in this section, treat Form 8938 and FinCEN Form 114, or FBAR, as separate checks. Filing Form 8938 does not remove a separate FBAR obligation where FBAR is otherwise required.

Use platform data collection to support that decision point, not to over-collect. Capture enough structured data to flag when U.S. tax review is needed, including whether account setup falls into exclusions relevant to Form 8938 review, such as accounts maintained by a U.S. payer.

Be precise about Form 8938 scope. It applies to specified foreign financial assets when the applicable reporting threshold is exceeded and the filer is a specified person. For certain specified domestic entities, the referenced threshold is more than $50,000 on the last day of the tax year or more than $75,000 at any time during the year. If no income tax return is required for the year, Form 8938 is not required. If required, it must be attached to the annual return and filed by that return's due date, including extensions.

Two operating cautions follow. Do not assume Form 8938 applies to every U.S.-connected case, and do not treat a Form 8938 review as a full closeout when FBAR may still apply. Keep the Form 8938 versus FBAR comparison in your control mapping.

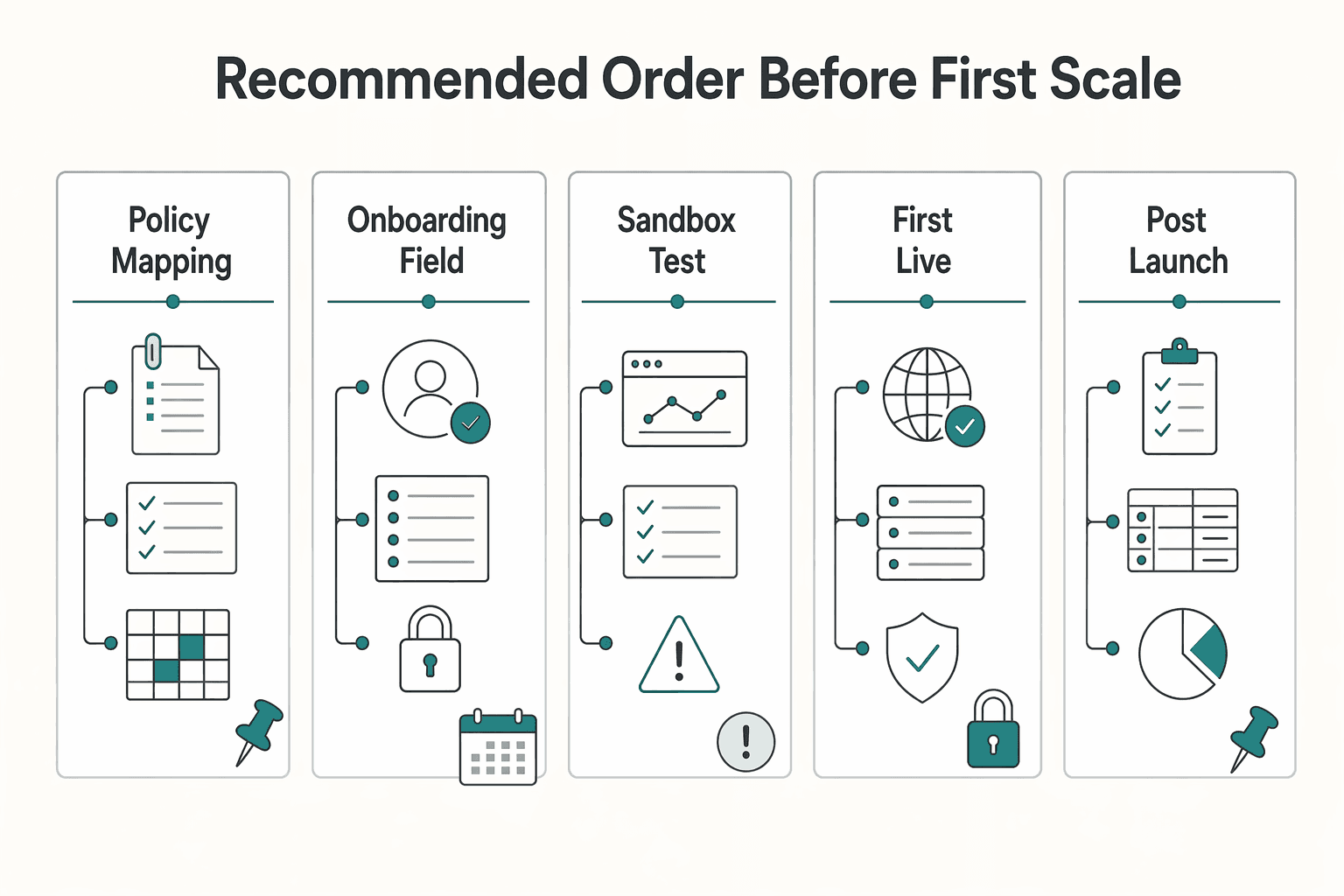

Recommended order before first scale#

Use this sequence as operating discipline, not as a legal mandate. It keeps policy, data capture, testing, and audit review in order:

- Policy mapping

Draft the filer-scope note, threshold and exclusion checkpoints, and Form 8938/FBAR decision note first, with open questions visible.

- Onboarding field validation

Confirm forms and internal records capture the facts those checkpoints require.

- Sandbox test

Run a full flow from payout request to provider response to ledger posting to reconciliation export.

- First live payout with enhanced monitoring

Start with constrained volume and named reviewers, then verify exception routing for holds, rejects, and returns.

- Post-launch audit review

Compare live evidence to the launch file after initial activity, and re-check Form 8938 materials as they are continuous-use documents that can be updated.

The key checkpoint is traceability: one record path from request, to provider event, to ledger posting, to reconciliation export, plus a defined exception path when that chain breaks. Launch when the evidence pack can withstand a bad first week, not just a clean demo.

Use this evidence pack as a hard launch gate, then map each owner to an auditable execution flow in Gruv Docs.

Rollout sequencing rules for founders choosing where to expand first#

Expand first where your current controls already produce complete reporting evidence and clear entity transparency. If a market adds unresolved tax, reporting, or entity questions during launch week, sequence it later even if demand is stronger.

Start with control fit, not market size#

Start with markets where your existing onboarding data, reporting ownership, and audit trail already support your cross-border reporting decisions. Move later to markets that add interpretation, more owners, or more fragmented evidence requirements, especially when CRS, DAC7, or Pillar Two scope is still uncertain.

For U.S.-linked flows, test whether your current data can support Form 8938 review without new collection. Form 8938 applies to specified foreign financial assets when thresholds are exceeded. Some account types are excluded, including certain accounts maintained by a U.S. payer. For certain specified domestic entities, the cited threshold is more than $50,000 at year end or more than $75,000 at any time. If your onboarding cannot separate those facts, you are moving too fast.

Keep filing mechanics in scope. If Form 8938 is required, it must be attached to the annual return and filed by that return's due date, including extensions. Keep the FBAR check separate as well, since filing Form 8938 does not remove a FinCEN Form 114 obligation where FBAR is otherwise required.

Use explicit if-then gates before GTM spend#

Set internal gates that force ownership before scale:

- If DAC7 scope is still unclear, keep the market in pilot mode until you confirm applicability, name the reporting owner, and define the required source-data path.

- If Pillar Two implications for your planned entity structure are still unclear, pause broader GTM spend until finance has reviewed the assumptions.

- If a Europe cluster is under review, treat it as a separate decision from a single-country pilot, because Commission proposal text identifies Member State rule fragmentation as an operating obstacle.

Choose launch shape deliberately#

| Launch shape | When it fits | Main advantage | Main tradeoff |

|---|---|---|---|

| Single-market pilot | Controls are proven in one jurisdiction, but assumptions still need live validation | Narrowest operational exposure and easiest exception handling | Slower coverage |

| Regional cluster launch | Evidence standards and ownership are truly reusable across countries | Better rollout efficiency | Higher exposure to rule fragmentation and reporting drift |

| Parallel global launch | Entity, reporting, finance, and payments controls are already consistent across jurisdictions | Fastest coverage | Highest compliance debt if one assumption fails |

Stop conditions#

Pause expansion when any of these are unresolved at approval time:

- no named reporting owner

- no complete audit trail from request to provider event to ledger posting to reconciliation output

- legal-entity classification is missing, conflicted, or still assumption-based

If a stop condition is open, reduce scope: run a pilot, limit volume, or wait until ownership and evidence are complete.

For trade-policy pressure on payment choices, read Tariff Pressure and Cross-Border Payment Choices for Platforms.

Frequent operator mistakes that turn into expensive compliance rework#

Most expensive compliance rework starts as setup rework. If ownership, control design, and escalation paths are unclear at launch, teams usually end up rebuilding onboarding and partner responses after go-live. That is why stop conditions matter. Many failed expansions are not market failures. They are control failures.

Ownership design comes too late#

A repeat mistake is treating operating structure as cleanup work after launch. When core ownership decisions are delayed, teams often have to rework workflows and documentation after go-live.

Use a pre-launch checkpoint: require named owners for critical operations and customer data. If those owners cannot clearly confirm accountability, keep the market in pilot scope.

Dispute exposure is part of payments expansion#

Dispute risk belongs in payments rollout, not a separate workstream. As you expand, service and financial failures can escalate quickly if controls do not scale with them. Before first live payout, verify three internal controls:

- Named owners for critical operations and customer data

- Integration reliability across the workflow

- Risk controls and operating-model readiness

Reconciliation after launch is already too late#

If reconciliation and exception handling are weak at launch, scale magnifies the problem. That is how mistakes turn into chargebacks and service misses, and why cleanup becomes expensive.

Run one hard pre-scale test: confirm ownership, integration reliability, value tracking, risk controls, and operating-model readiness before expansion. Pilot programs help because they keep the blast radius small while you validate those controls.

More data does not mean better compliance#

Collecting more inputs does not replace control readiness. Before expanding use cases or users, confirm ownership, integration reliability, value tracking, risk controls, and operating-model readiness.

If those checkpoints are unclear, keep the rollout in pilot scope while controls are validated.

No escalation path when jurisdictions conflict#

Another repeat mistake is neglecting jurisdiction-specific compliance. When jurisdiction-specific questions stay unresolved and no one owns the decision, teams expand on assumptions.

Define escalation before launch: name the decider and record the rationale while issues remain open. Without that chain, expensive rework usually appears later.

For control design, use 8 Resilient Compliance Controls for Payment Platforms in 2026.

Conclusion#

The right 2026 move is to enter the market where your controls, evidence ownership, and rollout capacity already match the compliance burden, not the market that only looks largest on paper.

Use this cross-border compliance annual update 2026 as a decision filter, not a trend recap. A market is attractive when you can already support the required documentation, reporting checks, and exception handling. If core assumptions about payout speed, reporting, or entity status are still unverified, treat that as a readiness gap.

Policy headlines are not execution readiness. Cross-border payments still remain slower and more expensive overall than domestic rails. Unresolved frictions can drive fragmentation, so do not promise faster settlement or better traceability before your own records and support paths can consistently prove those outcomes.

If your expansion also touches EU-linked trade exposure, threshold detail should drive sequencing. CBAM is financially binding for imports from January 1, 2026. Importers below 50 tons per year of CBAM-relevant goods are excluded from core obligations, and delaying preparation can still create operational and financial disruption for importers above that threshold. Also plan to the timeline: no certificate purchases in 2026, certificates available from February 2027, and the annual declaration and certificate surrender deadline is 30 September.

Next step: run one target market through your checklist and force a go, pilot, or pause decision based on evidence. Document what obligations may apply, what evidence you can produce now, and what still requires country-program confirmation with counsel before product and GTM commitments.

If you want a market-by-market go/no-go review before rollout, talk to Gruv.

Frequently Asked Questions

What changed in U.S. cross-border reporting in 2026 for payment operators?

From the IRS materials used here, no new Form 8938 development was announced. The page says "None at this time" and shows a 31-Mar-2026 review date. The filing mechanics remain the same: attach Form 8938 to the annual return and file by that return's due date, including extensions. The operational checkpoint is still scope and threshold status, including whether the filer is a specified person and whether applicable Form 8938 thresholds are met.

How should a multinational platform handle regulatory divergence between U.S. and EU signals?

This material supports U.S. Form 8938 and FBAR points only. EU requirements are outside this pack and should be confirmed independently before launch.

What does the FSB implementation phase change for day-to-day payments operations?

No supported FSB implementation detail is included in this material. That means no specific operational change can be asserted here from FSB summaries alone. Treat it as an open validation item before making customer-facing promises.

How do FATCA, CRS, DAC7, and OECD Pillar Two affect market-entry sequencing decisions?

This section can only support the U.S. Form 8938 and FBAR part of that question, not detailed CRS, DAC7, or Pillar Two implementation rules. If a U.S. entity may be in scope, confirm whether Form 8938 applies and whether thresholds are met. Also keep the separation clear: filing Form 8938 does not remove a separate FinCEN Form 114 obligation.

Which risks matter most beyond AML headlines when expanding payout coverage?

A core risk is treating Form 8938 and FBAR as substitutes when they are separate obligations that may both apply. Another is weak filing-readiness on required checkpoints, since Form 8938 captures tax-period context and account-status questions such as whether foreign deposit or custodial accounts were closed during the tax year.

What is still unknown from current public summaries and should be validated before launch?

The current materials do not support specific 2026 claims for CTA or BOI scope changes, EU AMLA or Single Rulebook impacts, FSB operational effects, or detailed CRS, DAC7, and OECD Pillar Two implementation. Even within Form 8938, some higher-threshold variants are referenced but not quantified here. Validate filer category, threshold, and obligation directly before go-live.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- federalreserve.gov/econres/notes/feds-notes/payment-stablecoins...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

- fincen.gov/system/files/shared/FBAR%20Line%20Item%20Fil...trusted

- irs.gov/businesses/corporations/compliance-assurance...trusted

- irs.gov/pub/irs-pdf/i8938.pdftrusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- ustr.gov/sites/default/files/files/Issue_Areas/IP/202...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: