Quick Answer

Use a three-gate launch and approve a corridor only after hard evidence. Start with Gate 1 feasibility, then Gate 2 operability with webhook and retry behavior plus payout reconciliation tests, and then Gate 3 commercial readiness with support SLAs and rollback rules. For tariff-sensitive lanes, account for dated policy moves such as the April 5 and April 9, 2025 U.S. actions before committing spend. If primary and fallback rails cannot be traced end to end, phase the rollout.

How Tariff Pressure Affects Cross-Border Payment Choices#

If you are making expansion calls under tariff pressure, treat this as an operations decision first, not a market-opportunity story. Tariffs and cross-border payments can shift margin assumptions, support load, and launch risk on short timelines, so core planning should happen before onboarding, payouts, and reconciliation go live.

- Policy shifts land on dated schedules

A tariff is a customs duty on goods crossing borders, and tariff changes are implemented on specific dates. The WTO-IMF Tariff Tracker records changes in effective applied duties with implementation dates. In the United States, a 2025 reciprocal tariff action took effect on April 5, 2025 at 12:01 a.m. EDT. That was followed by higher individualized tariffs on April 9, 2025 at 12:01 a.m. EDT, while other countries remained under a 10% tariff baseline.

Practical takeaway: do not approve a new corridor on demand alone if the model is fragile to duty changes. We recommend using an ops-first lens when tariff pressure can change your margin math faster than your team can adjust the launch plan.

- Cross-border payment performance is still uneven by corridor

Cross-border payment performance is still less efficient than domestic performance, and the gap varies by segment and country. BIS notes that cross-border payments remain more costly, slower, less accessible, and less transparent than domestic payments. World Bank reporting also highlights differences in speed, cost, access, and transparency across segments and countries.

One useful signal is the World Bank remittance price indicator at 6.49% globally. It is not a pricing benchmark for every platform, but it is a reminder that cross-border friction is still real. Before launch, validate each corridor with evidence from your own payment flow and reconciliation path, not only provider marketing claims.

- Compliance and tax controls are launch prerequisites

This article is for founders and operators choosing verticals and corridors where payment reliability, compliance workload, and margin durability matter from day one. FATF-linked customer due diligence requires identifying and verifying customer identity using reliable, independent documents, data, or information. For legal entities, beneficial owner identity must also be identified and verified. VAT also belongs in launch planning where your flow touches jurisdictions that treat it as a core consumption tax.

This guide gives you a ranked set of expansion postures, rail-selection criteria, and go or no-go checkpoints tied to constraints like KYC, KYB, AML, VAT, and payout reliability risk. If those constraints do not fit your current margin and operating model, phase the launch instead of forcing a full rollout. Related reading: KYC KYB CIP Explained for Cross-Border Freelancers and Small Teams.

Selection criteria and who this list is for#

Use this list when you are sequencing launches and need corridor-level evidence before you spend on GTM.

- Who this is for

Use it if you are comparing options involving the United States, Canada, China, or Mexico and need to weigh payment risk against growth upside. Keep the analysis at corridor level, not country-level generalizations. WTO Tariff & Trade Data provides official tariff and import data for more than 150 economies (last updated 18 Mar 2026), and the World Bank remittance dataset is built on 367 corridors across 48 sending and 105 receiving countries.

- What this is not for

This is not legal advice or tax filing advice. Use it to decide launch order, provider design, and what to validate before committing budget. If you need tax or withholding guidance, handle that separately. Form W-8BEN is submitted when requested by the withholding agent or payer. Form W-9 provides a correct TIN to payers or brokers. Some U.S. information returns, including Form 1099-NEC, have a January 31 filing deadline.

- How to score each corridor

Use these five practical criteria to compare each corridor consistently:

- Tariff sensitivity: check the tariff source tied to your actual import leg, for U.S. goods exposure, the HTS; for bilateral views, tools such as WITS, including examples like China-on-U.S. tariff pages.

- Settlement reliability: treat cross-border payments as higher-friction until validated; core issues remain cost, speed, transparency, and access.

- Compliance burden (KYC, KYB, AML): include onboarding and controls workload; CIP uses risk-based identity verification, and Canadian beneficial ownership guidance references ownership or control at 25% or more.

- Documentation load (W-8, W-9, 1099): include collection, review, and retrieval requirements only where they apply to your user mix.

- Customer payment experience: score payout ETA clarity, failure handling, and support load when delays occur.

- Minimum evidence before launch

Use one validated payout path, one fallback rail, and auditable reconciliation from collection through payout as a practical operating threshold before go-live. This is a practical operating threshold, not a legal minimum. If your team cannot trace payments cleanly across primary and fallback flows, phase the launch instead of forcing it.

For a step-by-step walkthrough, see PEP Screening for Cross-Border Platforms and Monitoring Obligations.

The five expansion postures under tariff pressure#

Choose posture before country. Your operating model usually drives friction, concentration risk, and tax workload more than headline market size.

| Posture | Best fit | Main tradeoff |

|---|---|---|

| Low-friction launch | Prove demand fast; offer is closer to digital goods or services | Weaker defensibility if onboarding and payment flows are easy to copy |

| Controlled-risk growth | Enter one corridor at a time with one primary rail and one fallback rail | Added overhead across support, finance, and product |

| Compliance-heavy verticals | Regulated or higher-risk services; Merchant of Record first model | Slower onboarding and a longer prelaunch cycle |

| Payout-scale business | High-volume creator, contractor, or marketplace payouts; Virtual Accounts plus batch operations | Exception-handling complexity at scale |

| Tariff-volatility hedging | Continuity matters most; spread exposure across a corridor portfolio | Heavier tax and VAT administration |

- Low-friction launch

Use this when you need to prove demand fast and your offer is closer to digital goods or services. Lower direct customs-duty exposure can make early activation easier, but it does not remove indirect-tax complexity. Cross-border digital sales still create VAT collection challenges, and late-March 2026 reporting described WTO talks on duties for electronic transmissions as deadlocked.

The tradeoff is weaker defensibility if onboarding and payment flows are easy to copy. Before launch, confirm your team can trace payout request, provider reference, ledger entry, and reconciliation output without manual patching. We would rather see you delay the corridor than ask your ops team to debug that chain live.

- Controlled-risk growth

A phased rollout with one primary rail and one fallback rail can be a safer posture when you are entering one corridor at a time. It reduces single-rail dependency in markets that still rely on correspondent banking, where networks have been reported as shrinking and concentrating, with about 20% fewer active relationships and roughly 10% fewer active corridors over seven years.

The tradeoff is added overhead across support, finance, and product. Treat the backup as a live path. If it has not been tested through payout and exception handling, it is not a real fallback.

- Compliance-heavy verticals

For regulated or higher-risk services, a Merchant of Record, or MoR, first model can create a clean accountability boundary. The MoR is the entity legally responsible for processing customer payments and is liable for the financial, legal, and compliance aspects of transactions.

The cost is slower onboarding and a longer prelaunch cycle. FATF also flags inconsistent AML/CFT implementation. That raises costs, slows payments, limits access, and makes customer and beneficial-owner verification harder. Ownership for review, holds, and release decisions must be explicit.

- Payout-scale business

If you run high-volume creator, contractor, or marketplace payouts, Virtual Accounts plus batch operations can improve control and attribution. A virtual account uses a unique identifier, and providers position these setups to improve reporting, reconciliation, and tracking across entities or payee groups.

The tradeoff is exception-handling complexity at scale. Validate that each virtual-account identifier maps correctly and that returned funds can be matched back to the original batch without manual spreadsheet recovery.

- Tariff-volatility hedging

If continuity matters most, spread exposure across a corridor portfolio instead of concentrating in one route. For some platforms, that means comparing options across multiple corridors so a tariff shock in one market does not determine the whole quarter.

The tradeoff is heavier tax and VAT administration. For EU B2C e-commerce, rules changed on 1 July 2021. OSS allows registration in one Member State for eligible supplies. IOSS was created to simplify VAT declaration and payment for certain imported distance sales up to 150€.

For more on international EFT options, see International EFT Payments: How Platforms Can Send Electronic Funds Transfers Across Borders.

Compare payment rails before country launch#

Pick rails before you pick markets. Weak visibility and slow exception recovery can erase country-level upside even when headline fees look attractive.

Use this rule first. If visibility is low and exception paths are unclear, prefer rails with clearer status events and stronger exception handling over lower quoted fees. Cross-border payments still come with gaps in cost, speed, access, and transparency, and progress since the 2020 G20 roadmap has not fully translated into end-user outcomes.

| Rail | Settlement predictability | Transparency | Dispute and exception handling | Ops staffing need | KYC | KYB | AML | Tax-document dependencies | Verification checkpoint |

|---|---|---|---|---|---|---|---|---|---|

| Correspondent banking | Corridor- and intermediary-dependent; do not assume a stable ETA without provider evidence. | End-to-end visibility can be weaker when multiple banks are involved. | Harder when status is sparse or delays come from third-party review; date-of-availability handling matters where remittance rules apply. | Can increase for tracing, returns, and investigations when status data is limited. | Program-dependent for individual onboarding. | Legal-entity onboarding should include beneficial-owner verification. | Cross-border correspondent relationships require elevated risk management and due diligence. | W-9 for U.S. payees where applicable; W-8BEN or W-8BEN-E for foreign payees when requested; 1099 workflows depend on payee type and payment category. | Can you trace request -> provider or bank reference -> ledger posting -> reconciliation export without manual patching? |

| Digital wallets | Digital-payment rails may improve speed, cost, and transparency, but outcomes must be validated by corridor and provider. | Provider-dependent; assess whether status and fee information are visible enough for clear comparisons. | Check date-of-availability handling and how compliance reviews are managed when delays occur. | Program-dependent; validate manual workload for tracing and exceptions. | Program-dependent at platform or wallet level. | Required for legal-entity use cases. | Ongoing screening and monitoring obligations still apply. | Rail choice does not remove W-9, W-8BEN, W-8BEN-E, or 1099 obligations. | Can wallet transaction IDs map cleanly to payout IDs, ledger entries, and reconciliation exports with no manual keying? |

| International EFT | Corridor- and provider-dependent; do not assume uniform settlement timing. | Provider-dependent; prioritize options with clear upfront fee and speed visibility. | Prefer flows where status changes and return reasons are explicit, and account for compliance-triggered delays. | Program-dependent; validate operational load from returns and data-quality issues. | Program-dependent based on onboarding model. | Required for business accounts and entity payouts. | Monitoring and escalation for unusual patterns still apply. | W-9 for U.S. payees where applicable; W-8BEN for foreign individuals; W-8BEN-E for foreign entities; 1099-NEC for nonemployee compensation at $600 or more where applicable. | Can you follow initiation -> provider confirmation -> ledger post -> reconciliation file without manual matching? |

| Virtual Accounts | Depends on underlying payout rails; virtual accounts are control and attribution tools, not speed guarantees. | Can improve attribution when identifiers are carried through the full flow. | Can help isolate returns and mismatches when return and batch references are complete. | Program-dependent; validate reconciliation and exception effort with your mappings. | Program-dependent where individuals are onboarded. | Important for entity segmentation and beneficial-owner evidence. | Monitoring applies across collection and payout flows. | Tax reporting duties remain; for certain categories, 1099-MISC can apply, including $10 for some royalties and $600 for listed categories. | Can each virtual-account identifier map to original request, provider reference, ledger line, and reconciliation export with no manual patching? |

What this comparison should drive#

Do not choose a rail on fee alone when visibility is weak. If you cannot reliably see status, your support and finance teams can become the status layer, and exception cost can outweigh quoted savings. We recommend choosing the rail your team can actually explain and recover when payouts fail.

Treat speed and transparency claims as hypotheses to test by corridor, not guarantees. Validate both primary and fallback rails with live-like tracing before launch.

Keep compliance and tax workflows in the rail decision. KYB with beneficial-owner verification, plus W-8, W-9, and 1099 readiness, is operationally material and should be designed into onboarding and payout flows from day one.

A practical launch check#

Run a live-like test for each rail and ask one question: can your team trace request -> provider reference -> ledger posting -> reconciliation export without manual patching? If not, that rail is not launch-ready for that corridor.

Use a corridor scorecard before you pick markets#

Once rail viability is clear, score corridors before markets. If projected margin cannot absorb tariff exposure plus payment-friction risk, phase the launch instead of forcing a full rollout.

Keep demand and feasibility as separate scores. The Financial Stability Board identifies cross-border frictions as high costs, low speed, limited access, and insufficient transparency, so a strong demand forecast can still fail operationally.

| Market view | What to score | Why it changes launch decisions |

|---|---|---|

| United States (anchor) | Score each destination lane separately, U.S.-Canada, U.S.-Mexico, U.S.-China, instead of one blended North America view. | Corridor conditions vary with local regulation, provider competition, and financial infrastructure. |

| U.S. to Canada | Treat tariff upside as conditional: CUSMA reports preferential, duty-free treatment on over 98% of tariff lines and over 99.9% of bilateral trade, but treatment depends on goods qualifying as USMCA-originating (USMCA entered into force July 1, 2020). | "Canada" is not automatically "duty-free" without origin qualification evidence. |

| U.S. to Mexico | Apply a strict origin-rule check in the tariff score. U.S. order text states non-originating Mexico goods are subject to additional 25% ad valorem duties. | Nearshoring can reduce distance without reducing tariff risk. |

| U.S. to China | Add explicit timing risk, not just headline tariff level. USTR states 178 Section 301 exclusions were extended from Nov 29, 2025 to Nov 10, 2026. | Policy-window changes can shift corridor economics while demand stays flat. |

Across these cards, score supplier concentration explicitly. If your internal supplier mix is still forming, start with a simple internal concentration proxy, for example, top-five supplier share. Then sanity-check it with external concentration measures such as UNCTAD's import product concentration index and the World Bank Herfindahl-Hirschmann import concentration measure. For tariffs, log applied tariffs separately from bound duties so the score reflects current exposure.

For payment feasibility, use corridor evidence, not global averages. The World Bank's 367-corridor coverage and 6.49% global average remittance cost are useful context, but they are not launch proof for a specific lane. Use provider lane-level status and exception data for your go or no-go decision.

Final checkpoint before approval: can your team trace a corridor payout attempt from request to provider reference to final state without spreadsheet patching? If not, separate demand upside from operational readiness and launch in phases.

Build the compliance and tax evidence pack before go live#

If a corridor is still a "maybe," treat it as not launch-ready until the evidence pack is complete, owned, and explicit about what is still unverified.

| Pack item | What to document | Grounded details |

|---|---|---|

| Policy map | KYC, KYB, and AML responsibilities tied to the product flow and escalation path | Name triggers such as individual signup, business onboarding, payout method change, suspicious activity review, and manual override |

| Tax document matrix | Who provides which tax form, when, and why | W-9 for U.S. persons when information returns are required; W-8BEN for foreign individuals; W-8BEN-E for foreign entities; note January 31 for Form 1099-NEC where applicable |

| VAT and e-invoicing notes | VAT and e-invoicing scope by market, with scope limits written down | For EU B2C e-commerce, record whether OSS or IOSS applies, who files, and whether the EUR 10 000 EU-wide threshold is relevant; rules changed on 1 July 2021 |

| Audit trail and unknowns log | Records for each money-movement state transition and a per-market unknowns log | States listed include requested, pending review, held, returned, released, failed, and reconciled; Regulation E says not less than two years; BSA-required records have a five-year baseline |

- Policy map for identity, ownership, and escalation

Build a one-page control map that ties KYC, KYB, and AML responsibilities to the product flow and escalation path. For covered financial institutions, beneficial-ownership procedures must be written to identify and verify beneficial owners of legal-entity customers, and bank CIP procedures must be risk-based and verify customer identity. If your model includes money services business obligations, the AML program also needs customer ID verification plus record creation and retention controls. The key is specificity. Name triggers such as individual signup, business onboarding, payout method change, suspicious activity review, and manual override. We recommend making that map simple enough that your launch owner can use it without translating compliance language mid-rollout.

- Tax document matrix tied to user type and payment flow

Define who provides which tax form, when, and why before opening the first account. Use Form W-9 to collect a correct TIN from U.S. persons when information returns are required. Use W-8BEN to document foreign individual status in U.S. withholding and reporting contexts when requested by the payer or withholding agent. Use W-8BEN-E to document foreign entity status for chapters 3 and 4.

If you issue information returns, note required Form 1099 reporting timelines. That includes January 31 filing for Form 1099-NEC where applicable. Also note the tax year 2023 rule that 10 or more information returns must be filed electronically.

- VAT and e-invoicing notes by market, with scope limits written down

Document VAT and e-invoicing scope by market instead of relying on institutional memory. For EU B2C e-commerce flows, record whether OSS or IOSS applies, who files, and whether the EUR 10 000 EU-wide threshold is relevant to your facts. EU cross-border B2C VAT rules changed on 1 July 2021, and marketplaces or platforms facilitating supplies have record-keeping requirements.

For e-invoicing, keep scope boundaries explicit. The cited EU rule supports mandatory receipt and processing of standard-compliant eInvoices for public contracting authorities or entities, not a blanket private B2B mandate. For deeper VAT context, see Cross-Border VAT for Digital Platforms: OSS IOSS and the EU VAT Gap.

- Audit trail and unknowns log for key money movement states

Make auditability a launch gate by keeping records for each state transition you operate, for example: requested, pending review, held, returned, released, failed, reconciled. Set retention rules in your compliance records. Regulation E requires evidence of compliance to be retained for not less than two years, and BSA-required records have a five-year baseline.

Keep a per-market unknowns log with validated items, assumptions, owner, last-checked date, and decision impact if an assumption fails. This prevents launch approvals based on unlinked assumptions.

Related: E-Invoicing for Platforms: How to Issue and Receive Invoices Electronically Across Borders.

Roll out in three gates instead of one launch#

Treat a cross-border launch as three separate go/no-go decisions, not one, because feasibility, operability, and commercial readiness can fail for different reasons.

| Gate | Pass only when | Notes |

|---|---|---|

| Feasibility | The corridor scorecard meets the minimum bar on cost, speed, access, and transparency; rail coverage is confirmed; compliance ownership is explicitly assigned | Keep tariff source freshness visible; in this research pass the WTO-IMF Tariff Tracker page showed 17 March 2026; name a qualified compliance owner such as a BSA compliance officer or equivalent |

| Operability | Payout status handling, webhook failure and retry behavior, resend actions, and reconciliation outputs work in sandbox and live environments | Trace request to provider event to ledger posting to a payout reconciliation report without manual patching; PayPal may retry non-2xx webhooks up to 25 times over 3 days |

| Commercial readiness | Support scripts, exception SLAs, and rollback criteria are approved before public launch | Define who answers payout-status tickets, when engineering is paged, and what conditions trigger a corridor pause |

- Gate 1. Feasibility

Pass only when the corridor scorecard meets your minimum bar on cost, speed, access, and transparency, rail coverage is confirmed, and compliance ownership is explicitly assigned. Use tariff inputs with evidence discipline, including the WTO-IMF Tariff Tracker's reliability limits, and keep source freshness visible. In this research pass, that page showed 17 March 2026. Make accountability explicit by naming a qualified compliance owner, for example, a BSA compliance officer or equivalent, not a generic placeholder.

- Gate 2. Operability

Pass only when payout status handling, webhook failure and retry behavior, resend actions, and reconciliation outputs work in both sandbox and live environments. A sandbox is an isolated test environment, so treat it as useful but not a guarantee of production behavior. Your hard check is traceability: can you follow each payout from request to provider event to ledger posting to a payout reconciliation report without manual patching? Include retry-cadence differences in testing. For example, Stripe sandbox retries differ from live mode, and PayPal may retry non-2xx webhooks up to 25 times over 3 days.

- Gate 3. Commercial readiness

Pass only when support scripts, exception SLAs, and rollback criteria are approved before public launch. Define who answers payout-status tickets, when engineering is paged, and what conditions trigger a corridor pause. Use documented service level agreements and coordinated recovery procedures rather than ad hoc incident judgment.

For a related walkthrough, see How Graphic Designers Protect Cross-Border Payments and Cash Flow. Before Gate 2 and Gate 3 sign-off, map your webhook statuses, payout retries, and reconciliation exports in the Gruv docs.

Failure modes that erase margin after launch#

Margin erodes after launch when settlement visibility, compliance controls, or tax documentation are only partly operational. Users feel those gaps as payout failures, and your team absorbs the operating cost.

- ETA opacity in Correspondent banking.

The real risk is unclear settlement, not just slow settlement. Cross-border payments are generally slower, more expensive, and more opaque than domestic payments, and multiple intermediary hops can increase fees and delay fund availability. BIS data also shows a network that has been contracting and concentrating, including 2018 declines of about 3.5% in active relationships and 2% in active corridors. If your support view cannot show a provider reference, last status event, and timestamp of the latest update, avoid promising fixed payout dates.

- Partial KYC, KYB, and AML implementation.

Compliance gaps can show up as payout interruptions in live traffic. CIP requires risk-based identity verification, KYB controls include beneficial ownership verification for legal-entity customers, and payment-chain rules allow execution, rejection, or suspension when required originator or beneficiary information is missing. Treat these as state-management flows, not checklist items. Test hold, reject, release, and re-review end to end so support and ledger views match when a payout is stopped. June 2025 FATF Recommendation 16 updates are a practical reminder to keep these flows current.

- Tax-document gaps that change payout amounts.

Missing or incorrect tax documentation can change what gets paid, not just what gets reported later. Tax-document and TIN completeness affect withholding and reporting, Form W-8BEN establishes foreign status for U.S. withholding and reporting, and missing TIN conditions can trigger backup withholding at a flat 24%. Collect required tax documents before first payout and make reconciliation traceable to the tax status used for that payout decision. If you are in covered digital-asset broker scope, Form 1099-DA reporting begins for transactions on or after January 1, 2025.

- Single-provider or single-corridor concentration under tariff pressure.

Concentration risk can turn policy shifts into operating pressure. The correspondent network is documented as more concentrated, with active relationships down about 20% over seven years, and tariff changes can add input-cost pressure at the same time. Avoid depending on one provider path for most volume. Keep a validated fallback route active and trace both primary and backup flows from payout request through provider reference to reconciliation output.

For more on using virtual IBANs to collect globally, see What is a Virtual IBAN and How Do Platforms Use It to Collect Payments Globally?.

Choose your operating model for payment accountability#

Choose the model that makes one entity clearly accountable for tax handling where applicable, compliance decisions, and reconciliation in each corridor. If ownership is ambiguous, the model is not ready for scale.

- Merchant of Record (MoR)

Use MoR when you need the clearest accountability boundary. The MoR is the entity legally authorized to process customer payments, and it carries financial, legal, and compliance responsibility for those transactions, including KYC and AML adherence. Confirm your contract and operating view align. Your team should be able to show, per transaction, which entity is the MoR, who handles tax responsibility where applicable, and who approves holds or releases.

- Direct model with modular rails

Use direct only when your team can operate the controls, not just the routing logic. Payment orchestration can route by conditions such as card country, currency, and amount, and can retry failed payments on a second processor in supported setups. Prove operational readiness before launch. Multi-processor setups are resource-intensive, so you need clear ownership for legal-entity onboarding controls, exception handling, and end-to-end traceability from payment request to provider reference to ledger posting.

- Hybrid by market or product

Use a hybrid model when corridor risk is uneven. Selective MoR by market or product is operationally supported in major provider implementations, which can help teams apply enhanced due diligence expectations in higher-risk jurisdictions while keeping lower-risk corridors on direct rails. Document exactly where responsibility switches. If ownership changes by country, product, or entity, define that in approvals before launch so support, finance, and compliance give the same answer on who owns each transaction.

Track the first 90 days with hard verification checkpoints#

In the first 90 days, the goal is to prove the model is controllable, not just that payouts clear. If you cannot verify outcomes by corridor, rail, and document state on a regular cadence, pause volume growth.

- Weekly corridor metrics

Measure performance by corridor and rail, not as one blended number. Track payout success, return rates, time to resolution, and manual intervention volume by the actual payout path used.

Corridor-level tracking matters because cross-border payments rely on domestic rails at the first and last mile, and conditions vary across systems and regions. A stable global average can hide a single corridor getting slower or more manual.

Use benchmarks for direction, not promises. The FSB framework includes targets such as 75% of cross-border wholesale payments credited within one hour and reconciliation by end of day of crediting, by end-2027. Compare primary vs fallback rail in the same corridor each week. If payout success is flat but manual handling rises, you likely have growing operational drag.

- Weekly auditability trace test

Run a weekly trace test on payout batches and confirm end-to-end lineage: payment request -> provider reference -> ledger posting -> reconciliation export. Include successful, returned, and held payouts.

Can someone outside the launch team retrieve the full chain without engineering intervention or ad hoc spreadsheets? This aligns with transparency expectations on delivery timing and payment-status tracking. It also aligns with recordkeeping expectations that transmittal-order records be retained and retrievable by transmittor identity, with U.S. rules that include a $3,000 threshold in applicable cases. Score trace completeness, not just "reconciled" status.

- Monthly controls review for AML and tax documentation

Hold a monthly controls review that combines customer due diligence, AML exceptions, and tax-document completeness in one operating decision. Ongoing due diligence is continuous, risk-based monitoring and customer-information upkeep, not a one-time onboarding task.

For tax operations, track document quality and status precisely. Form W-9 supports correct TIN reporting. Form W-8BEN is generally valid through the last day of the third succeeding calendar year unless circumstances change. Form 1099-NEC has a January 31 IRS filing deadline. If relevant to your model, Form 1099-DA reporting applies to transactions on or after Jan. 1, 2025. Review exception age and evidence quality, not just document counts.

If two consecutive weekly reviews show unresolved trace gaps or a growing exception backlog, treat that as a pause signal before scaling that corridor.

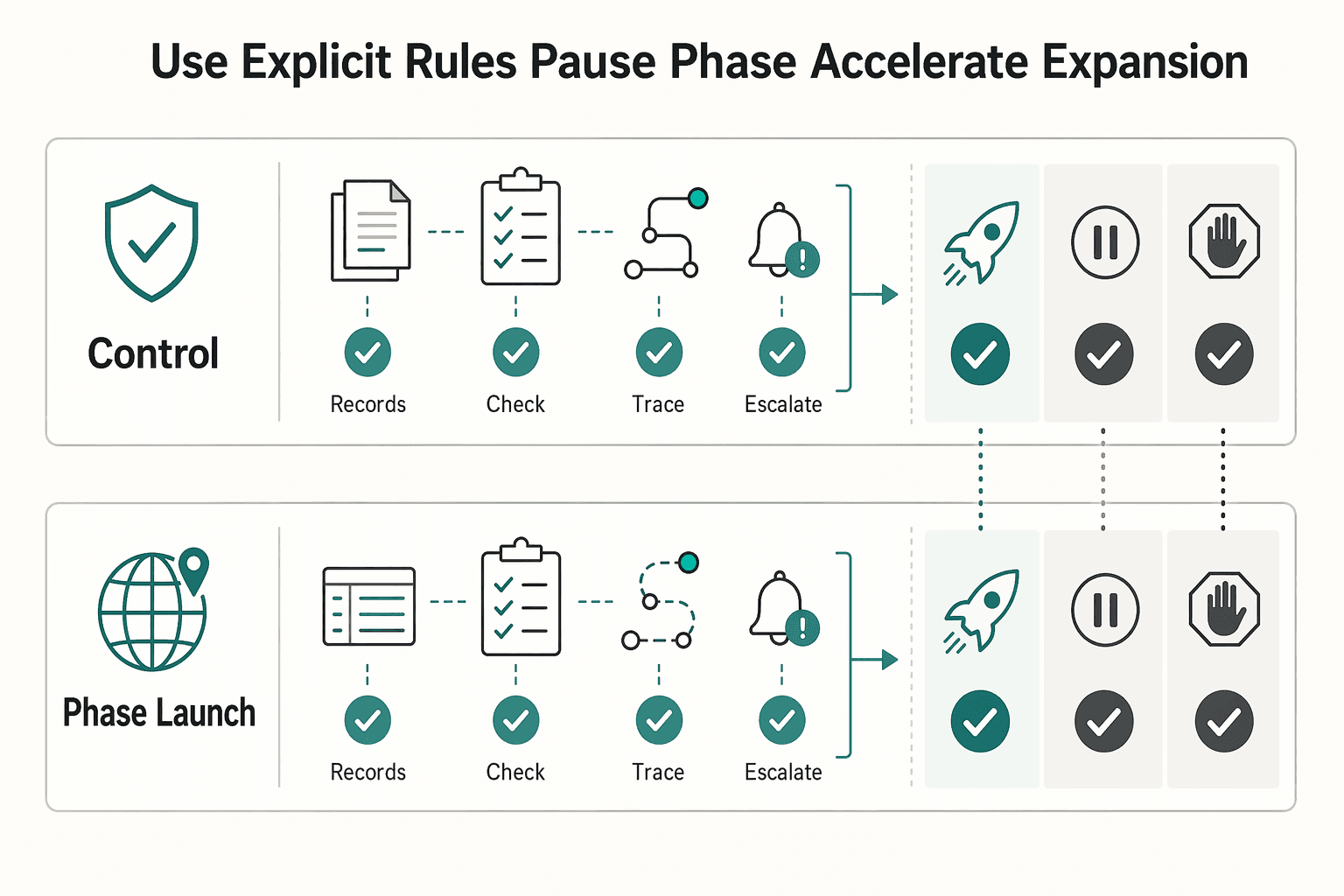

Use explicit rules to pause phase or accelerate expansion#

After an initial operating period, put each corridor in one state: accelerate, phase, or pause. Let control evidence, not demand headlines, decide.

- Accelerate only on repeated control, not one good week

Accelerate only when two consecutive review cycles show stable payout reliability, bounded exceptions, and a support load your team can handle predictably. Treat this as an internal operating rule, not an external standard. If trace completeness or exception age worsens in either cycle, do not accelerate. We would rather see your team hold volume for one more review cycle than scale a corridor it cannot fully explain.

- Phase launch when trade uncertainty rises before your payment data catches up

If tariff uncertainty rises and payment-flow confidence drops, shift to a phased rollout instead of a full launch. Federal Reserve and IMF research both indicate that higher trade-policy uncertainty can reduce investment, activity, and trade, including an IMF-estimated 4.5 percent decline in bilateral trade under higher global uncertainty. Demand narrative is not an operations signal. Strong SMB optimism in PYMNTS does not prove corridor reliability.

- Pause when unknowns are larger than validated controls

Pause a corridor when unknowns grow faster than validated controls. Javelin Strategy & Research can be a useful disruption signal, but it is not enough by itself to make a go or no-go call. Pause when local evidence is thin and you cannot validate reliable payout paths, fallback handling, and audit-ready records.

For a more detailed comparison of payout methods, see When Platforms Should Use Wires vs Local Rails for Cross-Border Payouts.

Conclusion#

The practical answer is to prioritize operability over prediction: choose corridors and rails you can run through disruption, not just in stable conditions. That matters because cross-border payments still face cost, speed, access, and transparency gaps, and improvement targets have a common End-2027 horizon.

- Choose corridors you can verify, not just markets you want

Treat corridor-level evidence as the decision unit. Coverage across 367 country corridors and a 6.49 percent global average remittance cost are useful context, but they do not prove your specific corridor is launch-ready. If you cannot validate a primary path, a fallback path, and clear payment traceability, phase the rollout instead of forcing scale.

- Match expansion posture to your disruption tolerance

Set your tolerance for disruption before you scale. If your operating model cannot absorb delays, exception load, or reduced transparency, narrow scope and tighten controls first. Policy movement is still live, including U.S. tariff action on February 20, 2026, so expansion assumptions should be stress-tested, not treated as fixed.

- Use gate-based rollout with explicit stop conditions

Move corridor by corridor, with clear go or no-go criteria and a minimum evidence pack for operations and control ownership. When unknowns exceed validated controls, pause. Keep AML/CFT execution quality and beneficial-owner verification at the center, because weak implementation can raise cost, slow payments, limit access, and reduce transparency.

If you must choose between faster expansion and better traceability, choose traceability. Coverage can expand later. A weak launch can expose control gaps that are harder to manage at scale. We recommend making that tradeoff explicit before your team commits launch spend.

If you want a corridor-specific readiness check on rails, policy gates, and auditability before committing launch spend, contact Gruv.

Frequently Asked Questions

How do tariffs affect cross-border payments for digital platforms in practical terms?

In practice, tariffs can show up as cash-timing and margin pressure, not just a higher cost line. A tariff is a tax on goods crossing borders, and for U.S. imports, entry summary filing and estimated duty deposit are due within 10 working days after entry. Operational strain can appear when duty cash outflows and seller settlements stop aligning cleanly.

Do tariffs reduce payment volume, increase costs, or both?

Both can happen, and they do not always move at the same time. Tariffs can raise landed costs and weaken competitiveness, while tariff shocks are also associated with persistent pressure on trade activity and broader output. Model demand risk and operating-cost risk separately so you can see when a corridor keeps volume but becomes harder to run.

When should a platform prefer digital wallets over correspondent banking?

Prefer wallet-led routes only when corridor evidence shows strong recipient access and clear payment-status visibility for your payout flow. Correspondent banking can involve multiple intermediaries in one payment chain, which can make tracing and resolution harder. At the same time, digital bank-to-bank flows are not automatically faster in every corridor.

What should founders validate before entering a tariff-exposed corridor?

Validate one primary payout path and one workable fallback before committing launch spend. Then test corridor economics after duty pressure, payment fees, returns, and support handling are included. If your team cannot clearly explain payment status, delay cause, and fallback action, the corridor is not ready for full rollout.

How should teams compare International EFT, Virtual Accounts, and other rails without relying on marketing claims?

Use the same four checks every time: total cost, speed, access, and transparency. That aligns with the core friction set and with the policy emphasis on trackable status and clear service terms. Ask for corridor-level evidence such as cutoffs, return behavior, reconciliation outputs, and failure reasons, because headline fees alone are weak proof.

Which compliance and tax checks are non-negotiable before scaling cross-border payouts?

For U.S.-exposed programs, baseline controls include a written Customer Identification Program, beneficial-owner verification for legal entities, and an effective AML program where MSB obligations apply. Build tax-document workflows for Form W-9, Form W-8BEN, and Form 1099-NEC where applicable, including the $600 nonemployee compensation threshold and the general January 31 filing timeline for 1099-NEC. Also assess whether your account structure can create FBAR filing exposure when aggregate foreign account values exceed $10,000.

How can operators tell the difference between temporary volatility and a corridor they should exit?

Temporary volatility can include slower settlement or more exceptions, but with intact traceability and recoverable workflows. A corridor becomes structurally weak when traceability degrades, exception backlogs keep aging, and fallback options do not reliably clear payments. If holds, returns, and release actions are still not audit-ready, treat it as a corridor viability issue rather than routine noise.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Cross-Border VAT Routing for Digital Platforms Under OSS and IOSS

If you run an EU-facing platform, cross-border VAT is now an operating decision, not a glossary exercise. Since 1 July 2021, your practical job has been to route each flow to the right treatment: Union OSS, non-Union OSS, the import scheme, or a domestic VAT process outside those special schemes.

How Platforms Choose International EFT Payments Across Borders

---

Cross-Border E-Invoicing Controls for Platform Payouts

Step 1: **Treat cross-border e-invoicing as a data operations problem, not a PDF problem.**