Quick Answer

Start by classifying each transaction, then route it to Union OSS, non-Union OSS, IOSS, or domestic VAT reporting. Since 1 July 2021, the EU framework expects scheme-by-scheme routing, not one global setting. Check establishment, import presence, and taxable-person or deemed-supplier role before filing. Keep cadence split in your controls: Union and non-Union returns are quarterly, while import returns are monthly. If a flow cannot be clearly classified, stop automation and escalate through legal review or a VAT Cross-Border Ruling request.

How VAT routing works under OSS and IOSS#

If you run an EU-facing platform, cross-border VAT is now an operating decision, not a glossary exercise. Since 1 July 2021, your practical job has been to route each flow to the right treatment: Union OSS, non-Union OSS, the import scheme, or a domestic VAT process outside those special schemes.

The expanded One Stop Shop framework covers three special schemes: non-Union, Union, and import. A taxable person using one of them registers in one Member State of identification and files OSS VAT returns electronically for in-scope supplies and VAT due. But OSS does not replace everything. Those returns sit alongside domestic VAT returns where local obligations still apply.

This guide uses a ranked format because most teams need routing decisions first, not theory. For each common setup, the section gives:

- the platform model and who it suits

- the likely VAT route

- the operational upside

- the main limitation or failure mode

- the escalation trigger

Use one baseline rule throughout: choose by transaction flow, not by brand or team structure. A single platform may need to handle EU B2C services, distance sales of goods, imports, and domestic reporting in parallel. The EUR 10 000 EU-wide threshold can also affect whether certain TBE services and intra-EU distance sales of goods may remain taxed in the Member State of establishment.

Your first control checkpoint is data traceability. You should be able to show why a transaction was routed to a specific treatment, including when a marketplace or platform could be treated as a deemed supplier in certain goods scenarios.

Record-keeping requirements apply to platforms facilitating supplies of goods and services. If your team cannot reproduce why a sale was routed to a specific scheme without rebuilding it in spreadsheets, the control is not mature.

The scope here is intentionally narrow: what teams can operationalize now under EU VAT e-commerce rules, plus clear points where interpretation still needs escalation. Where treatment is clear, this guide is direct. Where ambiguity is real, especially in complex cross-border structures, the right move is escalation, including VAT Cross-Border Rulings for advance treatment in participating EU countries.

If you want a deeper dive, read A guide to the 'One-Stop-Shop' (OSS) for VAT in the EU.

How to choose the right route for your platform#

Start with transaction facts, then choose the scheme. The cleanest sequence is to classify the flow, confirm establishment status, test whether imports are in scope, and confirm whether you are the taxable person. Then test whether the platform could be treated as a deemed supplier.

| Step | What to confirm | Notable detail |

|---|---|---|

| Start with the supply type | Separate B2C services, TBE services, and distance sales of goods | The expanded OSS framework includes non-Union, Union, and import schemes |

| Check establishment | If the taxable person is established in the EU, test the Union scheme first; if there is no EU establishment, non-Union OSS may be available | Some choices can bind the business for the calendar year plus the next two calendar years |

| Handle imports separately | If an import leg exists, evaluate the import scheme separately | Union and non-Union returns are quarterly, while import-scheme returns are monthly |

| Confirm liability role | Confirm whether the platform is acting as the taxable person or could be treated as a deemed supplier | If role or treatment remains unclear in a complex cross-border case, escalate before filing |

- Start with the supply type

Separate B2C services, TBE services, and distance sales of goods before selecting a scheme. The expanded OSS framework includes three special schemes (non-Union, Union, and import), so it is not a single route for every cross-border flow.

- Check establishment before selecting Union or non-Union OSS

If the taxable person is established in the EU, test the Union scheme first. If there is no EU establishment, non-Union OSS may be available for eligible supplies, and the taxable person can choose any Member State of identification. Registration is in one Member State of identification, and some choices can bind the business for the calendar year plus the next two calendar years.

- Handle imports as a separate routing decision

If an import leg exists, evaluate the import scheme separately instead of assuming the Union or non-Union route covers it. Build filing cadence into your controls: Union and non-Union returns are quarterly, while import-scheme returns are monthly.

- Confirm liability role before filing or automation

Confirm whether the platform is acting as the taxable person or could be treated as a deemed supplier in certain goods scenarios. Use this as a routing control across compliance, legal, and finance. If role or treatment remains unclear in a complex cross-border case, escalate before filing, including through VAT Cross-Border Rulings.

Related: A Guide to VAT MOSS for UK Freelancers Selling Digital Services to the EU.

Best when you sell cross-border B2C from an EU base#

If your platform is EU-established and sells cross-border B2C into multiple Member States of Consumption, Union OSS can be a practical starting route.

- Best for: EU-based platforms or marketplaces with recurring cross-border B2C activity across several EU markets.

- Main benefit: one identification state and one electronic OSS VAT return for supplies covered by the scheme.

- Main constraint: the OSS VAT return is additional and does not replace your domestic VAT return.

Since 1 July 2021, EU B2C e-commerce VAT rules have allowed online sellers, including platforms and marketplaces, to register in one EU Member State. They can declare and pay VAT there on relevant cross-border supplies. Under the Union scheme, the identification state is normally where the taxable person is established.

If your facts allow a choice among eligible states, treat that as a long-term control decision. It can bind for the current calendar year plus the next two calendar years.

The gain is consolidation. You file once through that state, and the data and payment are transmitted to the relevant Member States of Consumption. That supports a centralized compliance model across several EU consumer markets.

The main failure mode is weak routing discipline. OSS is optional to join, but once you use a scheme, all supplies that fall under it must be declared through its OSS return. At quarter end, keep two controls in place. Reconcile OSS-covered turnover against the domestic VAT population, and verify that no in-scope cross-border B2C supplies were left in the wrong filing track. Also keep import flows on a separate calendar, because Union and non-Union returns are quarterly while import-scheme returns are monthly.

Use this route when establishment, supply classification, and destination VAT treatment are clear. If those facts are genuinely uncertain in a complex cross-border case, pause automation and escalate early, including through VAT Cross-Border Rulings.

Best when you are non-EU and provide B2C services into the EU#

If you are non-EU, have no EU business or fixed establishment, and your EU-facing model is B2C services, non-Union OSS can be the right starting route. It concentrates filing in one Member State of identification instead of separate registrations across multiple Member States for supplies within the scheme.

The benefit here is administrative concentration, not broader relief. OSS schemes are optional, but once you use one, you must declare all supplies that fall under that scheme through that scheme's OSS return.

Why this route fits#

For non-Union OSS, eligibility turns on facts, not product wording. You need no EU establishment and supplies that fall within the non-Union scheme. If eligible, you can choose any identification state, and that state issues a dedicated VAT ID in EUxxxyyyyyz format. That ID is limited to supplies declared under the non-Union scheme. Treat that limitation as a control point in billing and tax logic.

Where teams get caught#

The common mistake is trying to stretch non-Union OSS beyond its scope. It is not a catch-all for every EU-facing flow run by a non-EU platform. If goods or import legs appear, assess the Union or import scheme separately.

For services-only fact patterns, non-Union OSS is often the first route to test.

If classification is genuinely unclear, escalate early. For complex cross-border VAT treatment, consider requesting a VAT Cross-Border Ruling for advance guidance.

What to verify before go-live#

Before launch, confirm and document the following:

- no EU business or fixed establishment

- service classification for each in-scope flow

- chosen identification state

- Member State of Consumption mapping used in returns

- issued

EUxxxyyyyyzidentifier and its restricted use

Also align your filing calendar: non-Union and Union OSS returns are quarterly, while import-scheme returns are monthly. Keep the core constraint visible as well: OSS returns are additional and do not replace domestic VAT returns where those still apply.

For a step-by-step walkthrough, see Global VAT Compliance Map for Digital Services Platform Operators.

Best when you import low-value goods for EU consumers#

Use Import One Stop Shop, or IOSS, when you facilitate imported distance sales of goods into the EU and each consignment does not exceed 150€. If your flow includes an import leg, reassess whether a services-only route still covers your VAT obligations.

Why this route fits#

The import scheme is built to simplify VAT declaration and payment for eligible imported distance sales. It sits within the enlarged OSS framework that has applied since 1 July 2021.

The operational benefit is concentrated filing: one Member State of identification and electronic OSS VAT returns for supplies in scope. For setup, treat that state as a constraint tied to business-establishment facts, not a broad free-choice field.

Where teams mis-scope it#

IOSS covers the import slice only. It is not a universal lane for all EU-facing VAT obligations, and OSS VAT returns are additional rather than replacements for regular VAT returns.

The main risk is scope control. The 150€ consignment ceiling is part of the scheme boundary, so mixed baskets or fulfillment designs that move transactions outside that boundary need a defined exception path before go-live.

What to verify before go-live#

Before go-live, confirm these points in writing:

- each in-scope transaction is an imported distance sale of goods

- each consignment is at or below 150€

- your Member State of identification matches the business-establishment facts

- your tax logic clearly separates import-scheme supplies from supplies reported through other OSS schemes or regular VAT returns, where applicable

- your reporting process supports monthly import-scheme returns

The real tradeoff#

The import scheme is optional, but once you use it, you must report all supplies that fall under that scheme through its OSS return. So the real question is not just eligibility. It is whether you can keep the scope boundary clean period after period.

If your model mixes import and non-import flows and classification remains unclear, escalate early and consider advance guidance through a VAT Cross-Border Ruling in a participating Member State.

Best when deemed-supplier risk is your biggest unknown#

Treat deemed-supplier exposure as a legal classification question first, then build automation. If your product, checkout, or fulfillment design puts platform control at the center, move that flow to legal review before you lock tax logic.

Start from what is conditional#

Deemed-supplier treatment is not automatic across all platform flows. The OSS guidance describes platforms facilitating goods supplies as deemed supplier only in certain circumstances, so each flow needs its own classification decision.

That decision drives downstream reporting design: who is treated as the taxable person, who is responsible for invoicing, and which return population the transaction enters. Decide role first, then scheme and reporting.

Map roles before returns#

Build a role map for each material flow before changing OSS logic, invoice templates, or reports. Track unresolved points by flow and country where relevant instead of forcing one global conclusion.

| Checkpoint | What to pin down | Why it matters |

|---|---|---|

| Taxable Person | Which entity is treated as making the supply for VAT purposes | Sets liability and scheme population |

| Intermediary role | Whether the platform facilitates only or is treated as supplier | Avoids over- or understating platform VAT responsibility |

| Customer-facing invoice responsibility | Which party is shown as invoicing the customer | Supports record-keeping and audit defensibility |

One risk is applying one global rule across different scenarios. Prevent that by classifying each flow first, then applying scheme logic to that classification.

Keep records even when you are not deemed supplier#

Record-keeping obligations still apply to platforms, including cases where the platform is not deemed supplier. Keep evidence by flow and by filing period so treatment decisions can be reproduced during audit. Minimum evidence pack:

- role map, including seller, platform, and customer-facing invoice party

- classification note showing why the flow was included in or excluded from a scheme

- version history for tax-logic changes affecting treatment

- unresolved interpretation log by flow and country, with approvals for overrides

Watch reporting consequences#

If a taxable person uses an OSS scheme, all supplies in that scheme must be declared through that scheme's OSS return. OSS returns are additional and do not replace domestic VAT returns.

That can make misclassification costly in practice. It can distort who reports the supply and where reconciliation breaks between OSS and domestic filings. Before submission, reconcile deemed-supplier and non-deemed-supplier populations against the same transaction universe.

Escalate uncertainty through CBR#

When internal analysis cannot resolve a complex cross-border fact pattern, escalate through VAT Cross-Border Rulings for advance treatment certainty. File in a participating EU country where you are VAT-registered, and frame the request around the specific blocked scenario.

If your team is still looking for one universal deemed-supplier rule, treat that as a warning sign. Use a narrower control loop instead: classify each flow, log open points by country, and escalate only the unresolved cases before they affect returns and invoices.

We covered this in detail in How Platform Operators Make EU VAT OSS Filing Defensible.

Best when you run mixed flows and need one decision table#

For mixed flows, build one decision table before you automate anything. It should separate scheme selection, filing cadence, exclusions, and escalation points, so each transaction type has a clear route.

Scheme decision table#

Use this table as an operating map. It is not a substitute for legal analysis.

| Scheme | Eligibility signal | Covered transaction type | Filing cadence | Key exclusions | Known unknowns |

|---|---|---|---|---|---|

| Union OSS | Use when the flow fits Union-scheme scope and can be reported through one identification state | Covered distance sales and cross-border services in Union-scheme scope | Quarterly | OSS VAT return is additional and does not replace the domestic VAT return | Public summaries do not fully resolve all fact patterns, especially where platform role or deemed-supplier treatment is unclear |

| Non-Union OSS | Taxable person has neither business nor fixed establishment in the EU and can choose any identification state | Supplies that fall under Non-Union-scheme scope | Quarterly | Do not treat it as coverage for import-goods obligations | Services-only cases still need establishment and scope checks; public summaries do not settle every scenario |

| Import Scheme (IOSS) | Test separately when there are distance sales of low value imported goods not exceeding 150€ | Distance sales of imported goods up to 150€ | Monthly | Covers the import slice; OSS returns are additional and do not replace domestic VAT return obligations | Mixed checkout, supplier-role, and deemed-supplier questions often need legal review before setup |

If your answer depends on whether the platform is only facilitating or is treated as a deemed supplier, mark that flow as counsel-required before filing logic is finalized.

The Member State of identification is a control decision, not an admin detail. It is the single EU country where you register for the scheme, and in specified Union-scheme choices the selection can bind for the current calendar year plus two following years.

Operational ownership table#

Once the route is set, assign owners before returns start moving, and keep the control checks explicit.

| Control area | Primary owner | Core control check | Escalation trigger |

|---|---|---|---|

| OSS VAT return preparation | Central tax or finance ops | Population includes all supplies that fall under that OSS scheme | In-scope transactions missing or misclassified |

| Domestic VAT return reconciliation | Local VAT owner or domestic registration owner | Domestic and OSS filings reconcile to the same transaction universe | Reconciliation breaks between domestic and OSS tracks |

| Exception handling | Named exception owner | Overrides and interpretation gaps are logged with version history | Repeated manual fixes without durable rationale |

| Escalation sign-off | Head of Tax, legal, or finance leadership | One clear approval path for interpretive issues | Deemed-supplier uncertainty or other complex cross-border VAT treatment questions; escalate to CBR when needed |

Direct routing rules#

- If the flow is services only and there is no business or fixed establishment in the EU, evaluate Non-Union OSS first, then confirm scope before filing.

- If an import leg exists, test IOSS separately and check whether distance sales of imported goods stay within the 150€ condition.

- If a flow is in an OSS scheme, do not split that scheme population across local filings and the OSS VAT return.

- If role classification is unresolved, especially on deemed-supplier treatment, pause automation and escalate before the next submission cycle.

Keep filing calendars separate. Union and Non-Union run quarterly, while import runs monthly, so do not run mixed flows on one assumed filing calendar. For a broader comparison, see GST Digital Marketplace Platform Comparison for Australia, Canada, and India. Before you lock the decision table into operations, map each rule to implementation controls and audit trails in Gruv Docs.

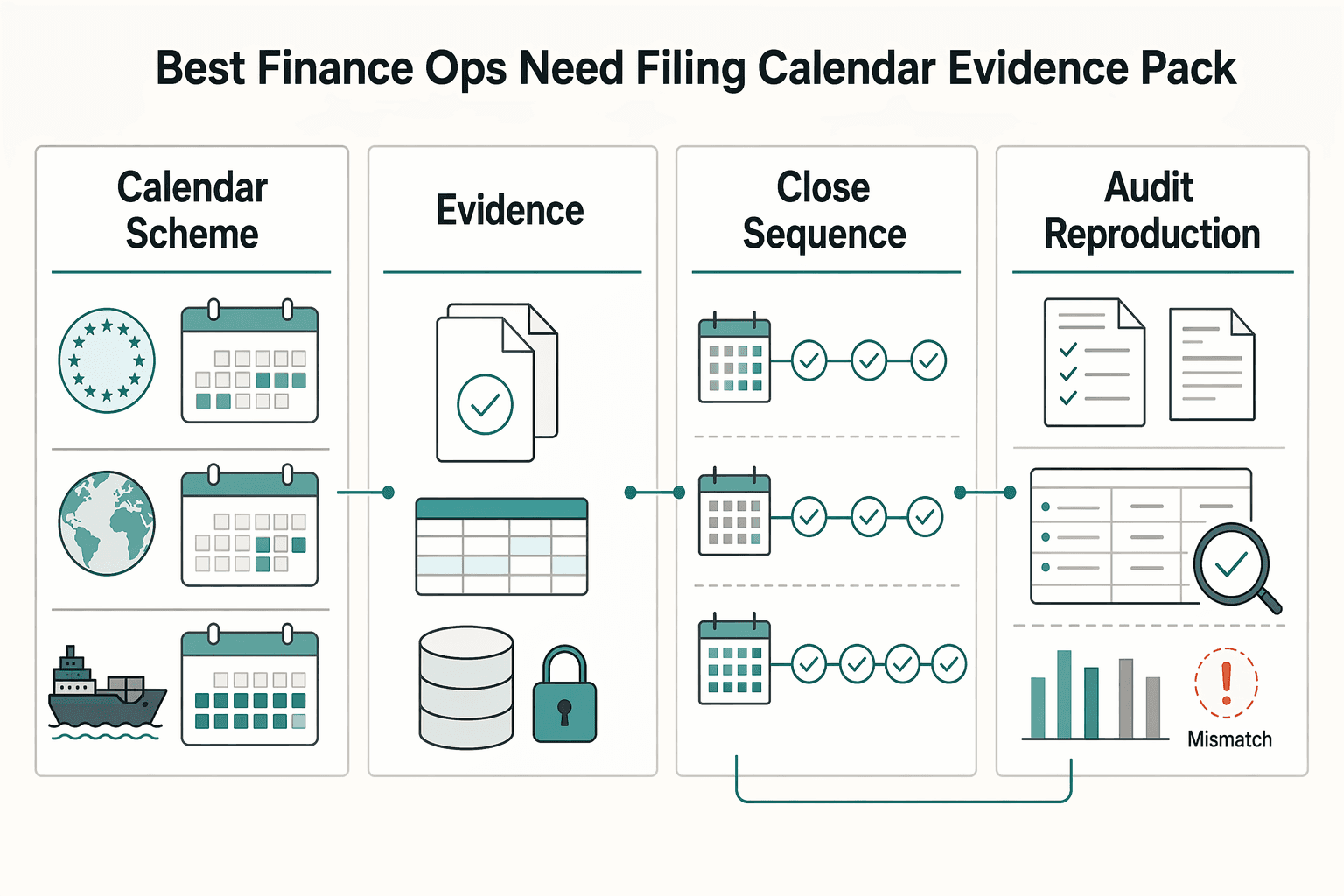

Best when finance ops need a filing calendar and evidence pack#

If finance ops owns filing, build the calendar around the scheme and keep an evidence pack that can be reproduced from system records. That is a practical way to reduce late-cycle rework and weak audit trails when OSS and import flows run together.

| Control area | What to keep or do | Grounded point |

|---|---|---|

| Calendar by scheme | Set deadlines from scheme cadence first | Union and non-Union OSS are quarterly, and import is monthly |

| Minimum evidence pack | Keep transaction classification, VAT logic version, identification state, Member State of Consumption, and return-ready exports for the OSS VAT Return | Treat this as an operating minimum, not a legal template |

| Close sequence | Classify flows first, lock ownership second, generate return datasets third, and reconcile to the VAT return last | This helps avoid reconciling before the scheme population is final |

| Audit-reproduction checkpoint | Regenerate records needed for Record Keeping and Audits in OSS from logs and source exports | If reproduction fails, fix the control before expanding automation |

- Calendar by scheme, not by team habit

Set deadlines from scheme cadence first: Union and non-Union OSS are quarterly, and import is monthly. If your transaction population spans multiple schemes, run separate close tracks even when one team owns all filings. Do not force monthly and quarterly populations into one cycle and patch the gaps near submission.

- Keep a minimum evidence pack for each period

Use a practical control set, for example: transaction classification, VAT logic version, identification state, Member State of Consumption, and return-ready exports for the OSS VAT Return. Treat this as an operating minimum, not a legal template.

The Member State of identification is the single EU country where you register for the OSS scheme. In specified Union-scheme cases, that choice can bind for the calendar year plus the next two years. Member State of Consumption needs to stay intact because returns and VAT due are routed from the registration state to the relevant consumption states.

- Run the close sequence in control order

A practical sequence is: classify flows first, lock ownership second, generate return datasets third, and reconcile to the VAT return last. This helps avoid reconciling before the scheme population is final.

If you choose an OSS scheme, all supplies under that scheme must be declared through that scheme's OSS return. The OSS return is additional and does not replace the VAT return, so reconciliation should test for both omissions and double counting across the two tracks.

- Use an audit-reproduction checkpoint before pressure hits

Pass criteria: records needed for Record Keeping and Audits in OSS can be regenerated from logs and source exports, without rebuilding the filing story manually in spreadsheets. This checkpoint matters even when a platform is not treated as deemed supplier, because record-keeping duties can still apply.

If reproduction fails, fix the control before expanding automation. If the blocker is a genuinely complex cross-border VAT fact pattern, escalate for legal review or consider an advance VAT Cross-Border Ruling in participating EU countries.

Best when audit readiness is weak but filing is already live#

If filing is already live but your team cannot defend scheme decisions, treat audit evidence as part of filing control now, not as a cleanup task later. Build a controlled evidence register for each OSS VAT return period, along with a log for manual overrides and unresolved judgments. Since OSS VAT returns are additional and do not replace domestic VAT returns, keep evidence aligned to both obligations where relevant.

- Decision trail for Deemed Supplier judgments

Keep a dated record for each case where the platform might be treated as a Deemed Supplier: transaction facts, conclusion, and approver. Online marketplaces and platforms can be treated, in certain circumstances, as having received and supplied goods themselves. Also keep records when the platform is not treated as deemed supplier, because record-keeping duties can still apply.

- Transaction-to-scheme mapping by filing period

For each quarterly Union or non-Union period and each monthly import period, retain the mapping from transaction type to scheme choice, not just filed totals. Tie each population to the relevant return, the Member State of identification, and the Member State details used in the filing. The standard is reproducibility from source exports, not spreadsheet reconstruction under audit pressure.

- Deregistration and exclusion watchlist

Track potential Deregistration and exclusion changes in a visible log. A taxable person or intermediary can leave a scheme voluntarily, or be excluded by a Member State, so this cannot live only in inboxes or adviser memory. When facts change, recheck your filing basis before the next period.

Verification checkpoint: for any period, can you produce records, invoices, and bad-debt-related support without a manual rebuild? If not, fix the register before the next cycle. If the facts raise genuinely complex cross-border VAT questions, escalate early and consider a VAT Cross-Border Ruling request under the national conditions of a participating EU country.

Best when legal uncertainty should stop automation#

Use automation only for rules that stay consistent across flows and countries. If the legal answer is uncertain, route the case to approval before filing.

| Trigger | Why it matters | Required response |

|---|---|---|

| Mixed-flow role conflict | OSS has three schemes, and return cadence also differs: quarterly for Union and non-Union, monthly for import | Role and scheme judgments should be reviewed before filing |

| Member State of Consumption splits the answer | The same facts can produce different filing logic by Member State of Consumption | Keep these cases behind reviewer gates and store the supporting analysis in the period file |

| Deregistration needs a replacement filing plan first | A taxable person or intermediary can leave voluntarily or be excluded, and OSS returns are additional rather than a replacement for domestic VAT returns | Document which supplies leave the scheme, who owns the replacement path, and how Member State of identification records are handled |

| Bad debt assumptions belong in review, not code | OSS materials include rules on records, invoices, and bad debt relief, but they do not provide one EU-wide bad-debt rule for every case | Get jurisdiction-specific confirmation |

- Mixed-flow role conflict

If your model combines services, imported goods, and platform-facilitated goods, one tax rule may not be enough. OSS has three schemes: non-Union, Union, and import. Return cadence also differs: quarterly for Union and non-Union, monthly for import. When Taxable Person or Intermediary responsibility, or deemed-supplier treatment for platform-facilitated goods, is unclear, role and scheme judgments should be reviewed before filing. Verification checkpoint: test one sample order per flow and confirm why one scheme was used and why the other two were excluded.

- Member State of Consumption splits the answer

If the same facts can produce different filing logic by Member State of Consumption, stop full auto-routing for those markets. OSS is optional, but once you use a scheme, all supplies in that scheme must be declared through that OSS return. Keep these cases behind reviewer gates and store the supporting analysis in the period file.

- Deregistration needs a replacement filing plan first

Treat Deregistration as a control event, not an admin toggle. A taxable person or intermediary can leave voluntarily or be excluded, and OSS returns are additional rather than a replacement for domestic VAT returns. Before any move, document which supplies leave the scheme, who owns the replacement path, and how Member State of identification records are handled.

- Bad debt assumptions belong in review, not code

Do not hard-code one bad-debt treatment across markets. OSS materials include rules on records, invoices, and bad debt relief, but they do not provide one EU-wide bad-debt rule for every case. When treatment is uncertain, get jurisdiction-specific confirmation. For complex cross-border VAT questions, consider a VAT Cross-Border Ruling request filed under national conditions in a participating EU country.

Conclusion#

The defensible approach is a sequence, not an acronym. Before the next filing cycle, map each in-scope flow to the relevant OSS special scheme: Union OSS, Non-Union OSS, or the Import Scheme.

-

Classify each flow first. Start at transaction level, then map to the relevant OSS special scheme. For each in-scope transaction, keep a clear link to the Member State of identification used for that scheme. If you choose that state under the Union scheme from multiple fixed establishments, that decision can bind you for the current calendar year plus the next two.

-

Choose the scheme by flow, then apply it consistently. The schemes are optional, but once you use one, all supplies that fall under that scheme must be declared through that scheme's OSS VAT return. Do not force mixed goods, services, and import legs into one shortcut rule. Test each leg on its own facts, especially where deemed-supplier treatment is uncertain.

-

Treat filing cadence as a control design issue. Union and non-Union returns are quarterly, and import-scheme returns are monthly. OSS returns are electronic and additional, not a replacement for the regular VAT return, so your close process should show what was included in OSS and what remained in regular VAT reporting.

-

Keep reproducible records and escalate gray zones early. Platforms have record-keeping obligations for facilitated goods and services, including scenarios where deemed-supplier status may not apply. Your period file should let a reviewer reproduce classification, scheme choice, identification state, and filed return data. For genuinely complex cross-border cases, consider requesting a VAT Cross-Border Ruling in a participating EU country where you are VAT-registered.

If your team needs help deciding where to automate versus where to keep approval gates for VAT-sensitive flows, talk to Gruv.

Frequently Asked Questions

What is the practical difference between One Stop Shop (OSS) and Import One Stop Shop (IOSS) for platforms?

In the provided OSS materials, the practical difference is scheme scope and filing cadence. The OSS framework covers three special schemes: non-Union, Union, and import. Non-Union and Union returns are filed quarterly, while import returns are filed monthly. In practice, separate import-scheme activity from non-import B2C activity before you do anything else.

When does a platform need Import Scheme handling instead of Union OSS or Non-Union OSS?

Use import-scheme handling for transactions that fall under the import scheme, rather than forcing one quarterly rule across all transaction types. If your model mixes import-scheme activity with services or other B2C cross-border activity, test and route the import leg separately. As a control check, a non-Union VAT ID in EUxxxyyyyyz format is limited to non-Union-scheme declarations.

Do OSS VAT Return submissions replace a Domestic VAT Return?

No. OSS VAT returns are additional and do not replace the domestic VAT return. Your process should reconcile OSS-reported activity with domestic VAT activity instead of treating OSS as a full substitute.

How often are returns filed under Union OSS, Non-Union OSS, and Import Scheme?

Union and non-Union scheme returns are filed quarterly, and import-scheme returns are filed monthly. Treat that as a control-design issue, because a quarterly-only close cycle will miss or delay import-scheme obligations.

How should teams apply the EU-wide threshold logic to Telecommunications, Broadcasting and Electronic (TBE) Services and distance sales?

Apply the EU-wide EUR 10 000 threshold that replaced older intra-EU distance-sales thresholds from 1 July 2021. Below that threshold, qualifying TBE services and intra-EU distance sales may remain taxed in the Member State where you are established. If you use an OSS scheme, declare all supplies that fall under that scheme through that scheme’s OSS return.

When can Online Marketplaces/Platforms be treated as a Deemed Supplier?

The supported answer is narrow: marketplaces and platforms facilitating supplies of goods can be treated as deemed suppliers in certain circumstances. Do not encode a blanket rule when platform-role facts are mixed or unclear. For genuinely complex cross-border cases, consider a VAT Cross-border Ruling in a participating EU country before scaling automation.

What records are essential to pass Record Keeping and Audits in OSS reviews?

At minimum, maintain records that support transaction treatment, invoices, and bad-debt handling, since those are explicitly in scope for OSS rules. Record-keeping duties also apply to platforms facilitating goods and services, including cases where the platform is not a deemed supplier. Your period file should let a reviewer reproduce the classification, scheme choice, identification state, and filed dataset without rebuilding evidence from scratch.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- legislation.gov.uk/eudr/2006/112/article/28trusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- oecd.org/en/publications/international-vat-gst-guidel...trusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: