Quick Answer

Start by classifying the customer: business clients usually follow reverse charge, while private EU buyers can move you into one-stop-shop oss vat reporting for eligible digital sales. For B2B, validate the VAT ID in VIES, match legal name and address, and keep dated proof with your invoice records. For B2C, track the customer’s Member State and monitor the EU-wide threshold before choosing your filing lane. If classification is uncertain, pause and resolve the facts first.

The mention of EU VAT can trigger invoicing anxiety, even for experienced international professionals. That reaction makes sense. The rules look dense, the acronyms pile up, and nobody wants a payment delayed over a tax setup issue.

For most professionals selling high-value services, the way through this is simpler than it first appears. You do not need to become a European tax expert. You need to make one core decision correctly at the start of the engagement: are you dealing with a business customer or a private consumer? Once that is clear, the invoicing path usually gets much simpler.

This guide is built around that decision so you can issue EU invoices with confidence, keep a clean record, and avoid preventable payment friction.

Step 1: The Foundational Question - Is Your Client B2B or B2C?#

Classify the client first, because that decision sets your VAT path for the rest of the engagement. If you get it wrong, you can end up charging VAT when you should not, or missing B2C obligations where OSS may apply.

For B2B, the clearest signal is a VAT ID that you verify against matching business details. Ask for the VAT ID, legal name, and registered address, then validate the number in VIES and confirm it is associated with that name and address. Under Article 18 logic, you are looking for a valid number, matching name and address details, and no contrary information. Use this onboarding checklist every time:

- Verify the VAT ID in VIES.

- Confirm the VAT number is associated with the customer's legal name and address; if details do not match, request confirmation from the relevant tax administration.

- Capture dated evidence of the result, such as a screenshot or PDF.

- Store that evidence with the client record and invoice support files.

- Re-validate after material client changes, such as a new VAT ID, legal name, or address, since VIES checks are point-in-time only.

- Do not treat a VIES confirmation by itself as complete legal proof for a VAT exemption decision.

Handle edge cases with follow-up, not assumptions. If no VAT ID is provided, you may treat the client as non-taxable unless you have contrary information. If VIES shows the number as invalid, do not automatically treat the client as B2C. The number may not yet be activated for intra-EU use, or the registration may still be in progress. Re-check the details, confirm them with the client, and if the problem remains, ask the client to contact its tax administration. If the VAT ID is pending, treat the client as taxable only when you hold other proof and have done reasonable verification. If you need broader tax background around freelance setups, see Taxes in Germany for Freelancers and Expats.

| Client path | Evidence you should hold | Common misclassification risk | Next step |

|---|---|---|---|

| B2B with valid VAT ID | VAT ID, VIES result, matching legal name and address | Accepting a VAT ID tied to a different entity or address | Continue to the B2B VAT treatment path |

| B2B with VAT ID pending | Proof of VAT ID application, business identity details, verification notes | Treating an applicant as fully validated too early | Escalate carefully and document why taxable-person treatment is justified |

| B2C | No VAT ID communicated, or no reliable business proof | Assuming one invalid VIES check automatically means consumer | Continue to B2C analysis and assess whether OSS rules apply |

Step 2: The B2B Protocol - Your 95% Use Case#

For B2B work, most mistakes happen before the invoice goes out, not after. Major economies now have digital tax laws, and more countries continue to adopt similar rules, so consistent checks matter. Confirm the client entity, apply the tax treatment you validated for that engagement, and keep supporting records in one place.

Cross-border B2B service arrangements are not one-size-fits-all. Treat the tax treatment as a verified setup choice based on your facts and jurisdictions, not as an automatic default.

Before you send the invoice#

A quick review helps prevent common invoice issues. Use this pre-send check every time:

- Client identity: legal name, billing or registered address, and the tax identifier you used when classifying the client.

- Entity alignment: contract entity, invoiced entity, and paying entity are consistent, or any differences are documented and confirmed.

- Tax treatment wording: use wording approved for your setup and keep it consistent across invoice templates.

- Field placement: place tax-related notes consistently so finance teams can find them quickly.

- Amount check: the tax section matches the intended treatment and does not carry a leftover default rate.

- Registration checkpoint: confirm whether a registration-threshold decision applies before issuing the invoice.

Correct vs incorrect setup#

| Checkpoint | Correct setup | Incorrect setup | Tax-treatment clarity | Evidence to retain |

|---|---|---|---|---|

| Client entity | Invoice matches verified legal entity and tax ID on file | Invoice is issued to a different or incomplete entity | Clear and consistent with your validated setup | Verification proof plus any entity-confirmation message |

| Tax amount field | Tax lines match intended treatment | Template default adds an unintended tax amount | Clear in the issued invoice | Final issued invoice copy and corrected version if reissued |

| Tax-treatment note | Approved wording is present and consistent | Wording is missing, ad hoc, or inconsistent | Not clear to reviewer or AP team | Template text used plus issued invoice |

| Audit trail | Verification proof and invoice are stored together | Records are scattered or missing | Hard to confirm after the fact | Dated verification record plus final invoice copy |

Your minimum audit file standard#

Keep one small file set for each B2B invoice decision. That gives you practical documentation without turning invoicing into a heavy process:

- The verification proof you relied on.

- The final issued invoice copy.

- A short note only if there was a mismatch or exception and how you resolved it.

- Any record needed to support tax rates, calculation, documentation, and return-filing decisions.

When to escalate instead of guessing#

Escalate before issuing the invoice if client status is unclear or your records conflict. Common triggers include a contract entity that differs from the paying entity, a tax ID that does not match the legal name, or uncertainty about whether a registration-threshold decision applies. Other triggers are requested tax wording you do not recognize or internal records pointing to different treatments. If the facts are clean, send the invoice. If they conflict, pause and resolve the issue with one documented question first.

For a step-by-step walkthrough, see A Guide to VAT Registration for a UK Company Selling to the US. If a tax-identifier check applies in your process, you can use the VAT number validator and store the result with your invoice records.

Step 3: The B2C Edge Case - When the OSS System Applies#

If your customer is a private individual in the EU, you are on the B2C path. This section is only about B2C digital sales to private EU customers, where OSS can become relevant.

Make the threshold trigger explicit in your tracking. In the EU OSS materials used here, the EU-wide threshold is EUR 10 000. Crossing that point can change how you handle VAT for covered supplies, because treatment may shift to the customer's Member State.

The practical sequence#

OSS includes the non-Union, Union, and import schemes, so confirm your establishment and supply facts before choosing one. OSS is optional, and it lets you register in one Member State of identification and use that single portal for declaration and payment.

| Scheme | Return timing | Reporting rule |

|---|---|---|

| Non-Union scheme | Quarterly | If you use it, report all supplies that fall under that scheme through OSS |

| Union scheme | Quarterly | If you use it, report all supplies that fall under that scheme through OSS |

| Import scheme | Monthly | If you use it, report all supplies that fall under that scheme through OSS |

- Determine the customer's EU Member State.

- Apply the VAT treatment for that destination country.

- Submit the OSS VAT return electronically through your Member State of identification portal.

- Remit VAT through that same route.

Two operating rules matter here. Non-Union and Union OSS returns are quarterly, and the import scheme is monthly. If you use an OSS scheme, report all supplies that fall under that scheme through OSS, not just a selected subset.

Monitoring versus filing#

| Checkpoint | Threshold monitoring mode | If you opt to use OSS |

|---|---|---|

| Sales tracking | Track cumulative B2C digital sales to EU private customers against the EUR 10 000 threshold | Track each reportable sale by customer Member State so return data matches VAT treatment |

| Customer classification | Keep B2B and B2C revenue separate | Keep the same separation. OSS applies to supplies within the scheme, not automatically to your entire business |

| Invoicing and checkout behavior | Record customer status and country for each sale | Apply destination-country VAT consistently and keep sale records aligned with the Member State used |

| Filing action | If you have not opted into OSS, continue monitoring and confirm local treatment when facts are unusual | File electronic OSS VAT returns through your chosen portal and remit through that Member State |

| Record pack | Keep a threshold tracker and country-by-country sales summary | Keep the same records plus submitted OSS returns and payment confirmations |

Edge cases that deserve a pause#

Mixed B2B and B2C revenue can create errors. If you serve EU businesses and also sell digital products or services to EU consumers, separate those streams in your books from day one.

| Edge case | What to do | Why it matters |

|---|---|---|

| Mixed B2B and B2C revenue | Separate those streams in your books from day one | Mixed B2B and B2C revenue can create errors |

| A buyer claims business status but your records do not support that classification | Pause and resolve it before invoicing or checkout | Unclear customer status is another risk |

| Platform sales | Do not assume platform sales should be handled like direct sales unless the contract and settlement documentation support that conclusion | A marketplace may be treated as the deemed supplier for VAT purposes |

Unclear customer status is another risk. If a buyer claims business status but your records do not support that classification, pause and resolve it before invoicing or checkout.

Platform sales need extra care. In some situations, a marketplace is treated as the deemed supplier for VAT purposes. Do not assume platform sales should be handled like direct sales unless the contract and settlement documentation support that conclusion.

Pause and get adviser input when customer classification is unclear, the customer's Member State cannot be established cleanly, or platform documentation leaves tax ownership ambiguous. Also remember that OSS returns are additional and do not replace any regular VAT return you still need to file. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Beyond VAT: Bulletproofing Your International Invoice#

Once the VAT treatment is set, invoice quality can determine whether payment flows smoothly or gets stuck. A good invoice matches the client's records, gives accounts payable complete payment instructions, and leaves a clean compliance trail.

Use W-8BEN only when the U.S. withholding trigger is real#

Use Form W-8BEN only when all of this is true: you are an individual, you are the foreign beneficial owner of an amount subject to U.S. withholding, and a U.S. payer or withholding agent asks for it. It is not a default form for every cross-border client.

| Situation | Action or rule | Note |

|---|---|---|

| You are an individual, the foreign beneficial owner of an amount subject to U.S. withholding, and a U.S. payer or withholding agent asks for it | Use Form W-8BEN | It is not a default form for every cross-border client |

| The form remains correct | It generally runs through the last day of the third succeeding calendar year | Unless circumstances change |

| Circumstances change and the form becomes incorrect | Notify the withholding side and submit a new form | Within 30 days |

| You invoice through an entity | Stop and confirm the form type first | Form W-8BEN-E is for entities |

For timing, a valid W-8BEN generally runs through the last day of the third succeeding calendar year unless circumstances change. If circumstances change and the form becomes incorrect, notify the withholding side and submit a new form within 30 days. If you invoice through an entity, stop and confirm the form type first, because Form W-8BEN-E is for entities.

Escalate to a tax professional if the requested U.S. form does not match your payee type. Also escalate if your residence or entity facts have changed, or you cannot identify who the withholding agent is in a U.S.-linked platform flow.

Make payment instructions impossible to misread#

Payment delays are often operational rather than tax-related, especially when the payer cannot reconcile basic invoice terms. Before sending, make sure these four items are explicit:

- Payment currency: show it on totals, not only in notes.

- Due date: use a full date in YYYY-MM-DD format.

- Settlement terms: keep terms clear in both the contract and the invoice. In EU business dealings, terms are generally capped at 60 days unless a different term is expressly agreed and fair.

- Transfer details: include the complete bank-transfer fields needed by the payer, such as beneficiary name, IBAN, and SWIFT/BIC where relevant.

Do not rely on "Net 30" alone. If no payment date is specified, interest entitlement can start 30 days after invoice receipt, which may matter legally but is better avoided operationally.

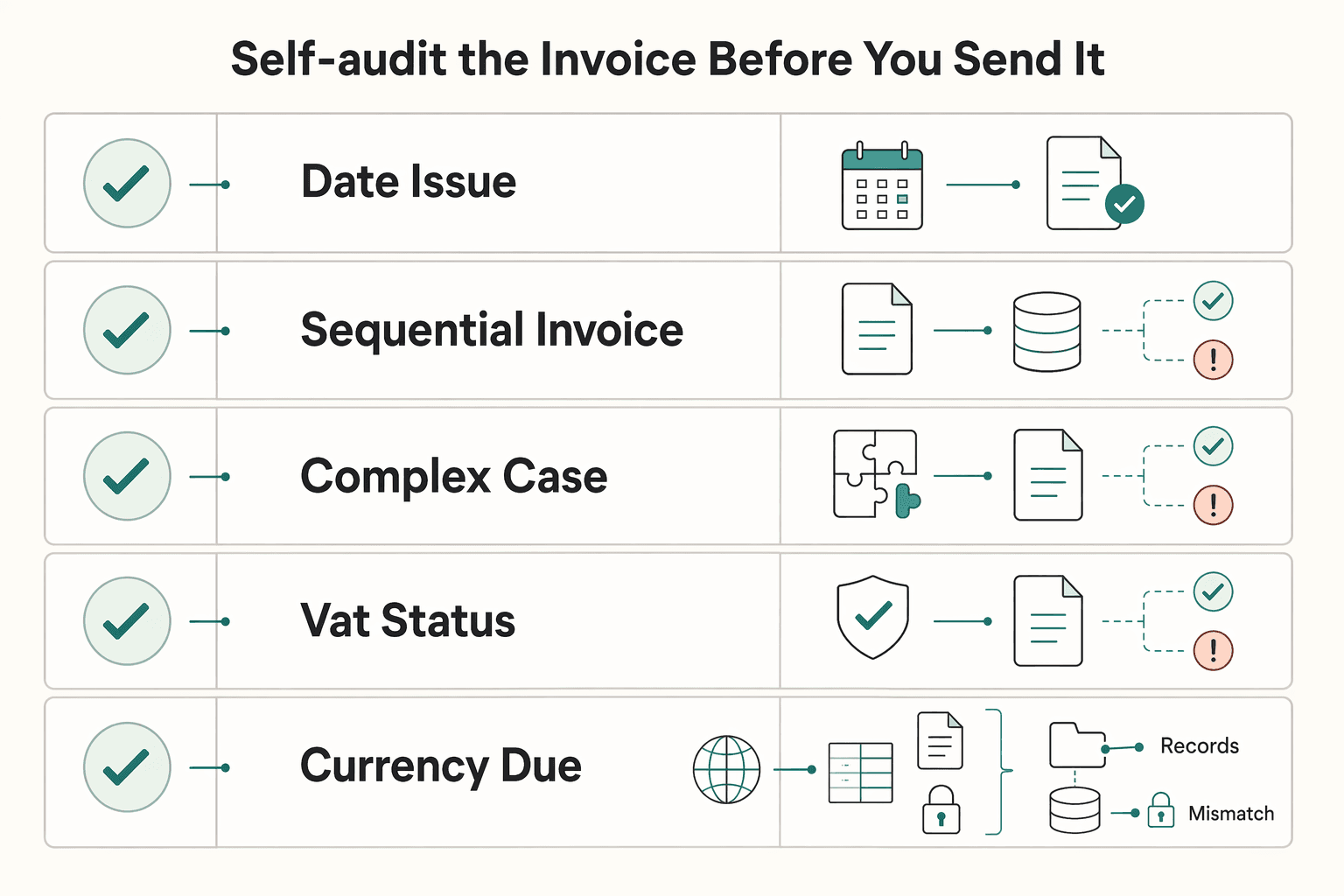

Self-audit the invoice before you send it#

Before you send the invoice, do one final content check. For VAT, Article 226 is your minimum-content anchor, including the date of issue, a sequential unique invoice number, and wording indicating reverse charge or exemption where applicable.

| Required field | Why it matters | Common failure |

|---|---|---|

| Date of issue | Required VAT content and baseline for payment timing | Ambiguous local shorthand date formats |

| Sequential invoice number | Required for traceability and Article 226 compliance | Duplicated or broken numbering sequence |

| Client legal identity details used for billing | Helps AP match invoice to the contracting party | Trading name or outdated legal details |

| VAT status wording (reverse charge/exempt, when applicable) | Makes VAT treatment clear on the invoice itself | Correct treatment internally but missing invoice wording |

| Currency, due date, and transfer details | Reduces preventable payment back-and-forth | Currency mismatch or incomplete bank fields |

After the content check, run this simple process each time so the sent invoice and support file stay together:

- Pre-send review: check tax treatment, numbering, totals, and due date.

- Client-data match: verify legal name and billing or tax details against your contract or onboarding record.

- Retention: store the sent invoice and supporting records. For OSS-reported sales, keep supporting OSS records for up to 10 years.

If you work with digital services to the EU, you might also find this useful: A Guide to VAT MOSS for UK Freelancers Selling Digital Services to the EU.

Conclusion: From Anxiety to Strategic Confidence#

The practical lens is simple: classify the customer first, then follow the VAT path that fits the facts. For services sold to businesses in another EU country, that usually means reverse charge, not OSS. Verify business status, use VIES when an EU VAT number is part of the setup, apply the B2B treatment, and keep the proof with your invoice records.

That split matters because the legal route changes with customer type and place of taxation. For B2B services, Article 44 places taxation where the customer is established, and Article 196 generally makes the customer liable for VAT. For qualifying cross-border B2C sales, OSS can centralize reporting in one Member State. The scheme is optional, but if you use it, you must declare all supplies that fall under that scheme, and OSS returns do not replace domestic VAT returns.

Keep that distinction in mind and use this default sequence every time:

- Classify the customer as business or consumer.

- Verify business status when you rely on B2B treatment, and retain dated evidence.

- Apply the matching VAT treatment, then keep the records that support that choice.

If the facts are unclear, stop before you guess. Confirm customer status and place-of-taxation facts, then escalate when uncertainty remains, including to local tax administration for urgent VIES uncertainty. Keep your process current with periodic rule checks, and get professional advice when your sales mix, jurisdictions, or reporting footprint changes.

Use the VAT reverse-charge checker as a sanity check when you are unsure whether to apply reverse-charge or OSS treatment.

Frequently Asked Questions

Do you need OSS for B2B services to EU clients?

Usually no. B2B transactions under reverse charge are handled via local VAT returns rather than OSS. Confirm customer type first, then apply reverse-charge treatment and local invoice requirements.

What is the practical difference between OSS and reverse charge?

Think of them as separate reporting lanes. OSS lets you declare qualifying EU-wide sales through one return instead of multiple VAT registrations, while reverse charge puts VAT accounting on the business customer for eligible B2B transactions. Use this quick table before filing. | Trigger scenario | Who reports VAT | What you put on the invoice | What you should retain | |---|---|---|---| | Cross-border B2B service to an EU business | Your customer generally accounts for VAT under reverse charge. These transactions are reported in local VAT returns, not OSS | Apply reverse-charge treatment and local invoice requirements | Keep records supporting customer classification and the reporting treatment used | | Cross-border B2C digital sale within the EU that falls into the OSS lane | You report and pay VAT through your OSS return, subject to current eligibility and rule checks | Apply the VAT treatment required for the customer-country outcome under current rules | Keep records supporting classification and amounts reported through OSS | | Local transaction where you have a local VAT reporting obligation | You report it in the relevant local VAT return, not in OSS | Use local invoice treatment that matches that registration | Keep records supporting that local return entry |

Does the EU-wide B2C threshold apply to your B2B work?

No. The EU-wide threshold relates to B2C distance sales, not standard B2B services handled through reverse charge. If you use a checklist or tracker, verify the current threshold before you hardcode it.

Can you report the same cross-border sale in both OSS and a local VAT return?

No. The source material flags this as a common mistake once cross-border sales are being declared through OSS. If you think you duplicated reporting, pause and reconcile your sales list before filing again.

What if you filed late or missed an OSS quarter? Can you fix it retroactively?

Do not assume you can treat it as a simple catch-up filing. The provided FAQ source states that an OSS return cannot be filed retroactively. Gather the invoices, customer-classification support, and draft return data, then get advice before choosing a correction path.

What happens if you invoice an EU business client incorrectly?

Impacts vary by jurisdiction and counterparty. A wrong VAT treatment can require invoice correction and reporting adjustments. The practical move is to correct it quickly, retain an audit trail, and keep a short internal note on why you reissued.

Do you need an EU bank account to invoice EU clients?

Confirm payment-account requirements with your payment provider and local adviser before standardizing your invoicing workflow.

What records should you keep when you use OSS or reverse charge?

Keep records that support your VAT classification and reporting choice, and follow local record-keeping rules. Commission guidance highlights record-keeping requirements for marketplaces/platforms, including cases where they are not deemed suppliers. If a marketplace is involved, document its role because some platforms may be treated as deemed suppliers.

When should you involve a VAT professional?

Escalate when you have mixed B2B and B2C activity, unclear customer status, or multi-country sales that make OSS versus local reporting uncertain. Also escalate when a marketplace sits in the transaction flow and may be treated as a deemed supplier. Ask for a written view on customer classification, reporting lane, and invoice requirements before volume grows.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- europa.eu/youreurope/business/taxation/vat/one-stop-sh...trusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- irs.gov/instructions/iw8bentrusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop/record-keeping-and-audits-oss_entrusted

- vat-one-stop-shop.ec.europa.eu/system/files/2021-07/OSS_guidelines_en.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Taxes in Germany for Freelancers and Expats

Low-stress compliance in Germany comes from decision order, not tax tricks. Use this sequence: confirm core facts, apply conservative temporary assumptions, verify the few points that can break invoices or filings, and keep one evidence file that explains each decision.

VAT MOSS and Non-Union OSS for UK Freelancers Selling to the EU

If you sell digital services from the UK to EU customers, treat UK VAT MOSS as historical and [Non-Union OSS](https://vat-one-stop-shop.ec.europa.eu/one-stop-shop_en) as the current route to assess. You cannot use UK VAT MOSS for sales made from 1 January 2021 onwards. For UK sellers who are not established and have no fixed establishment in the EU, the relevant OSS branch is the **Non-Union scheme**.