Quick Answer

Map vat on digital services for platform operators by liability first, then process. In practice, test who controls charging, customer terms, and service access, and escalate high-control models for legal review. For EU exposure, design around OSS as optional, apply scheme cadence (quarterly for Union/non-Union, monthly for import), and remember OSS filings do not replace domestic VAT returns. Close each month only after reconciliations and a locked evidence file.

How to Use This VAT Compliance Map#

For platform operators, VAT on digital services is first a liability and evidence issue, not just a rate issue. If you facilitate cross-border transactions between buyers and sellers, the key question is whether a tax authority may treat your platform as liable for VAT or GST on the transactions it facilitates.

This guide is for compliance, legal, finance, and risk owners who have to defend that position in practice. The goal is practical control: decide when platform liability is likely, what to check each month, and when to escalate to specialist counsel.

Start by keeping the scope tight. This guide focuses on digital services and electronically supplied services, where VAT or GST has applied in many countries for years. OECD guidance also describes policy options that can make platforms liable for VAT or GST and increase data-sharing cooperation with tax authorities.

Keep that scope separate from low-value goods, which are outside this section.

Your core monthly checkpoint is simple. VAT or GST filings should reconcile with platform and payment data. In practice, that means:

- Confirm return figures align with platform transaction records.

- Confirm payment-flow records are consistent with the filed position.

- Escalate quickly when product or payment changes create mismatches.

That discipline matters because authorities are described as cross-checking returns against commercial and platform data, and inconsistencies raise audit exposure. It also keeps 2026 in context: around 1 January 2026, the pressure described here is largely stronger transparency and enforcement, not an entirely new set of digital VAT concepts.

Start with the terms that drive liability#

Liability decisions usually go wrong at the labeling stage, so define the core terms before deciding who files, registers, or remits.

VAT and GST are consumption taxes. For cross-border digital services, your first tax question is place of supply: which country should tax the transaction. Start with classification, not rates. Check whether the supply is a digital service, where the consumer is located, and whether the customer is a consumer or a business. If the supply is not a digital service, general place-of-supply rules for services can apply instead.

A deemed-supplier rule, or deeming provision, is a key platform-liability trigger. Under this approach, a platform operator can be treated as liable for VAT or GST on sales made through the platform, even when the underlying trader performs the service. UK guidance is a concrete example. For digital services supplied to consumers through a third-party platform or marketplace, the platform is responsible for accounting for VAT. Treat that as a trigger to test for, not a universal outcome in every jurisdiction.

Non-resident digital service provider status also changes exposure quickly. Tax obligations can attach even if your business is based outside the taxing country. For example, if supplies are liable to UK VAT, a business based outside the UK may still need to register for UK VAT. In practice, keep "no local entity" separate from "no tax obligation."

Draw the boundary early between digital services and other types of supplies so your team does not apply the wrong controls. They are often grouped internally because both involve cross-border activity, but the tax treatment can differ. Also, do not assume an order confirmation naming the seller or developer resolves liability. Keep product classification notes, customer-status logic, and payment-flow evidence aligned from day one.

Need the full breakdown? Read Singapore GST OVR Compliance Decisions for Platform Operators.

Decide when your platform is likely the VAT supplier#

For EU exposure, treat platform control of customer charging and customer-facing terms as an internal escalation signal, then validate that position with local advice.

Treat this as an operating rule, not a legal test. In the excerpts available here, deemed-supplier treatment is confirmed in certain goods-marketplace circumstances, and the excerpts do not provide a complete yes/no checklist for all platform models. If your team is relying on labels alone, stop and document how the transaction actually works.

Use control questions before labels#

Assess the live flow, not contract shorthand. Focus on:

- Who authorizes or captures the customer charge

- Who controls access to the service or delivery point

- Who sets customer-facing terms such as pricing, refunds, cancellations, and usage

If the platform controls most of these, move to platform-liability legal review. If the seller or creator controls them end to end, intermediary treatment may be easier to defend, but evidence and record-keeping duties can still apply.

Scenario contrast that changes posture#

| Platform model | Charge and terms control | Practical posture |

|---|---|---|

| Creator subscription platform | Platform collects payment and sets standard customer terms | Escalate early; potential higher exposure |

| Pure listing service | Seller sets price and terms and contracts directly with buyer | Potentially lower exposure if the operating model matches the contracts |

| Mixed marketplace | Platform handles payment while seller controls core delivery terms | Ambiguous; treat as an escalation case |

Build an evidence file before you need it#

Do not wait for an audit to assemble the basics. Keep a compact file that shows who controlled the transaction at the time of sale, including:

- Checkout and payment authorization flow

- Customer terms and seller terms in force for the period

- Invoice or receipt logic showing whose name appears

- Payout and reversal flow, including who receives funds first and who can reverse

Keep version history as well. It helps show which terms applied during the audited period.

Record-keeping can still apply even where a platform is not treated as a deemed supplier, so "not supplier" is not the same as "no evidence duty."

When your facts are still unclear#

If the facts are complex, escalate instead of forcing certainty. The EU VAT Cross-border Rulings mechanism allows advance rulings on complex cross-border VAT treatment. Requests are filed in a participating EU country where the applicant is VAT-registered, and one company can file on behalf of others in a multi-company request.

Decide and document supplier posture first. Then decide whether OSS is useful. OSS is optional, and OSS returns do not replace domestic VAT returns.

Related: A Guide to VAT MOSS for UK Freelancers Selling Digital Services to the EU.

Build a country triage map before you design process#

Build the map around evidence quality first, then geography. The avoidable failure is designing one process for eight markets when only one is well supported in your current records.

If a market has potential VAT or GST exposure and supplier liability is still unclear, route it to the high-risk lane immediately and tighten evidence retention from day one.

Start with confidence, not geography#

Your map should show both your current tax posture and your confidence in that posture. Without both, country lists can look complete while hiding where legal support is thin or assumed.

In this source pack, only the European Union has enough official detail to support immediate process design. The non-EU markets below are not established here, so keep them in a validation lane until local advice confirms scope, triggers, and platform treatment.

| Jurisdiction | Regime status | Likely trigger type for triage | Confidence level | Suggested lane |

|---|---|---|---|---|

| European Union | Known active cross-border B2C VAT framework with OSS and platform record-keeping obligations from official EU sources | Cross-border digital or e-services exposure, platform-role review, OSS eligibility and filing design | Known from source | Immediate implementation |

| Saudi Arabia | Confirm with the relevant authority | Local confirmation needed | Needs local validation | Counsel-required before scaling |

| United Arab Emirates | Confirm with the relevant authority | Local confirmation needed | Needs local validation | Counsel-required before scaling |

| Oman | Confirm with the relevant authority | Local confirmation needed | Needs local validation | Counsel-required before scaling |

| Paraguay | Confirm with the relevant authority | Local confirmation needed | Needs local validation | Counsel-required before scaling |

| Peru | Confirm with the relevant authority | Local confirmation needed | Needs local validation | Counsel-required before scaling |

| Philippines | Confirm with the relevant authority | Local confirmation needed | Needs local validation | Counsel-required before scaling |

| Brazil | Confirm with the relevant authority | Local confirmation needed | Needs local validation | Counsel-required before scaling |

Keep this table blunt. Commercial priority does not change evidence quality.

What the EU row lets you build now#

The EU row supports concrete controls now. Official EU sources confirm OSS schemes, single-member-state registration for OSS, and scheme-specific filing cadence: quarterly for non-Union and Union schemes, and monthly for import. They also confirm that OSS returns do not replace domestic VAT returns.

That is enough to define ownership checkpoints. If you plan to use OSS, confirm scheme fit before assigning filing operations. For example, if the business has no EU establishment, the non-Union scheme may be relevant and a taxable person can choose any Member State of identification.

EU sources also confirm record-keeping duties for marketplaces and platforms, including where they are not deemed suppliers. So "not supplier" is not a basis to reduce retention scope.

Separate known facts from open questions#

Use two explicit fields on every row:

- Known from source: what official guidance or signed local advice supports now

- Needs local validation: unresolved scope, registration trigger, liability split, invoicing, and filing-path points

This prevents two common errors: cloning the EU OSS model into every market, and downgrading risk because current volume is low while liability is still unclear.

For the EU, one open question may still matter. The facts may be complex enough to seek a VAT Cross-border Ruling. CBR is available for complex cross-border transactions involving at least two participating EU countries, and participation is not universal across all Member States.

Use a simple routing rule#

Keep routing to three lanes:

| Lane | Use when |

|---|---|

| Immediate implementation | Regime and core obligations are supported well enough to build now |

| Monitor-only | No active implementation decision and no source-backed trigger requiring immediate build |

| Counsel-required before scaling | Regime scope or platform liability remains unverified |

Use one decision rule across markets. If a market has potential VAT or GST exposure and the liability split is unclear, route it to the high-risk lane and preserve more evidence than seems necessary. That can include checkout logic, terms history, invoice examples, payout and reversal flows, and scheme-selection notes.

For a step-by-step walkthrough, see EU Digital Services Act for Marketplace Operators.

What changed in 2026 and what did not#

2026 is not a confirmed reset of VAT rules for digital services. What is clearly supported is an existing EU framework with structured reporting, data exchange, and record-keeping controls.

The core framework predates 2026#

In the European Union, key mechanics were already in place before 2026. MOSS started on 1 January 2015, and it was extended to OSS from 1 July 2021. That means the core tax architecture shown in this material is not new in 2026.

What matters operationally is the control burden inside that architecture. EU OSS materials confirm electronic VAT returns, declaration of supplies and VAT due, and transmission by the Member State of identification to Member States of consumption through a secure network. They also confirm that OSS returns are additional and do not replace domestic VAT returns.

What the European Union clearly supports today#

The EU source set is enough to design a concrete process now. It supports the following baseline:

- Register in one Member State of identification for OSS.

- Treat OSS as optional, with three schemes: non-Union, Union, and import.

- Run filing cadence by scheme: quarterly for non-Union and Union, monthly for import.

- Keep record-keeping and audit readiness in scope from the start.

For operators, two checks are critical each cycle. Confirm scheme fit based on real footprint and supplies. Confirm whether domestic VAT returns still apply outside OSS.

What this section cannot confirm for 2026#

This pack does not establish ViDA-specific obligations, timelines, or new registration duties. Use ViDA as a signal to verify local requirements, not as a template assumption.

Keep the boundary clear. In the EU, build around confirmed OSS and, for complex cross-border cases, consider VAT Cross-border Rulings under national ruling conditions. Outside the EU, do not infer 2026 enforcement positions from EU logic alone. Keep Saudi Arabia, the UAE, Oman, Paraguay, Peru, the Philippines, and Brazil in local-verification status until counsel confirms scope, liability split, and reporting mechanics.

If you want a deeper dive, read Brazil Digital Services Tax: CIDE and ISS Obligations for Platform Operators.

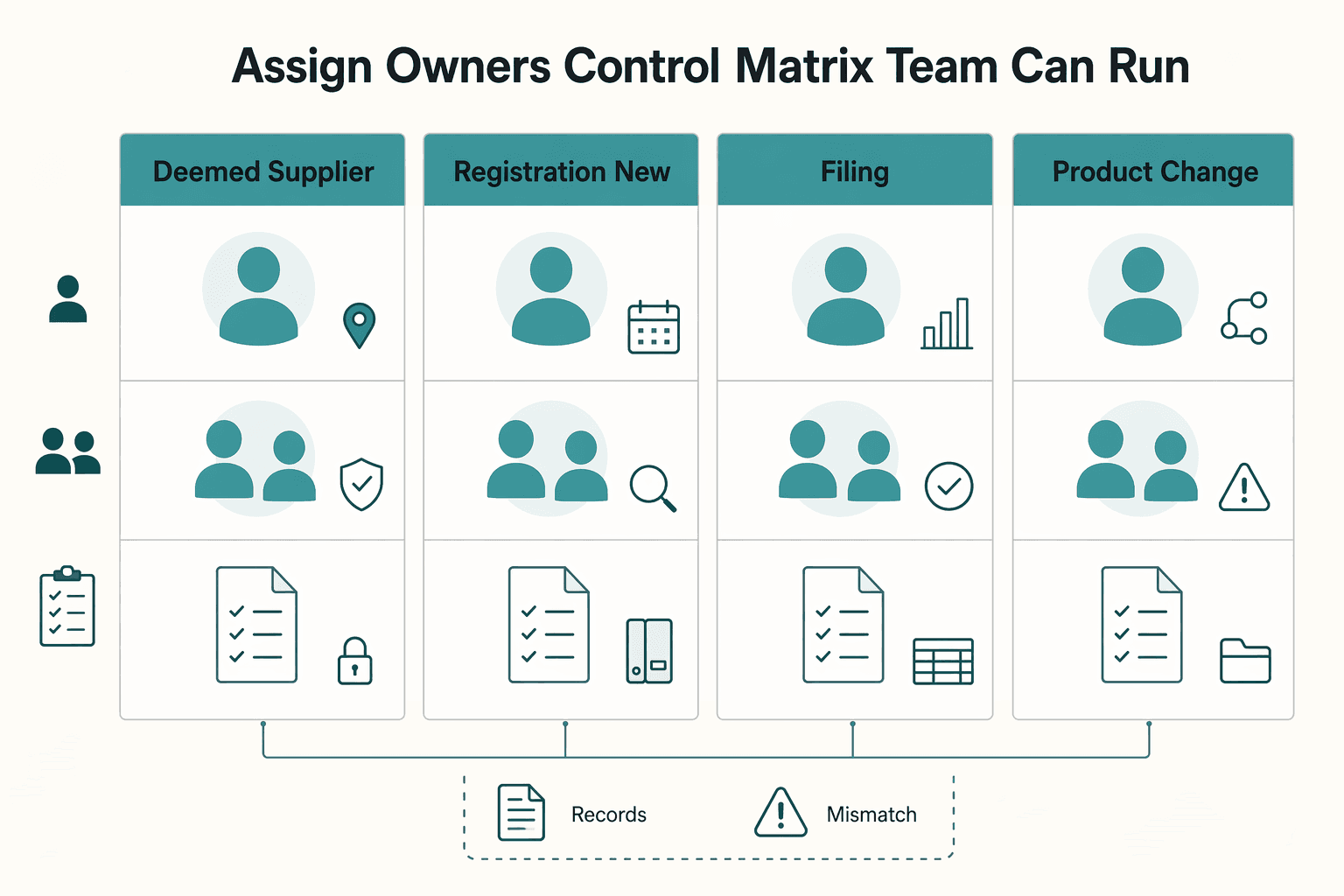

Assign owners with a control matrix your team can run#

Treat this as an execution problem. For each control, assign one primary owner, one backup reviewer, and a written procedure for each decision. Shared ownership without explicit criteria and retained evidence can make platform VAT controls brittle.

Use the matrix below as an operating model, then adapt ownership to your structure. The point is not to make every team a tax specialist. It is to define who decides, what evidence is retained, and which record proves the control ran.

| Control area | Example primary owner | Core decision | Evidence artifacts | System of record |

|---|---|---|---|---|

| Deemed-supplier rule assessment | Legal with Tax review | Whether current facts support your chosen treatment, or whether the position is still unclear | Contract clauses, current terms, payout flow diagram, platform role memo, approval ticket | Policy-gate log, legal approval record |

| Registration check for new market or model change | Tax | Whether the current model needs local registration review | Scope memo, assumptions, launch ticket, counsel request if unclear | Policy-gate log, market launch checklist |

| Filing input preparation | Finance Ops with Tax sign-off | What transaction population, tax amounts, and adjustments feed the filing support pack | Reconciliation export, ledger journals, exception register, filing workbook | Ledger, reconciliation export, filing folder |

| Product change review | Product with Tax or Legal escalation | Whether checkout, invoicing, or payout changes affect tax treatment or evidence quality | Change request, invoice logic spec, updated payout flow, approval record | Product ticket log, policy-gate log |

What the evidence pack should prove#

Your evidence pack should prove two things: the control exists, and the control was followed. Keep legal and operational evidence together for each audit period, including tickets, logs, emails, or signed forms that show who approved what and when.

If you use Gruv, map controls to existing records where supported, such as ledger journals, reconciliation exports, and policy-gate logs. These are practical anchors for internal review and counsel follow-up.

Verification and failure modes#

Run one recurring checkpoint: sample the last 5 relevant approval tickets and confirm the required approval evidence is attached. If any sample is missing required approval evidence, treat it as a control failure and remediate.

Plan for unintended change as a core failure mode. When product or process changes are introduced, review downstream tax and evidence impacts before the next filing cycle. If execution is outsourced, keep internal monitoring and oversight in place.

What to escalate and how fast#

Escalate to tax counsel when the legal position is unclear, when operating facts and documented treatment diverge, or when a filing could be wrong because the product reality changed. Escalate when analysis relies mainly on non-binding reference material without a clear legal anchor.

Lower-risk gaps can go to an internal approval committee, such as missing evidence, late support packs, or reconciliation breaks. Set turnaround targets by risk tier and document those targets in the control procedure.

Run a monthly evidence pack and reconciliation cycle#

Run one monthly control cycle that produces both filing outputs and the evidence behind them. If your team can prepare a VAT or GST filing without the support pack, the control is likely not strong enough.

Use one fixed order every month#

Keep the sequence stable with one internal order each month: pull the full transaction universe, classify supplies, apply jurisdiction logic, reconcile tax outputs to source records, then lock the evidence pack used for submission. This helps prevent teams from adjusting totals first and explaining the population later.

For platform operators, start with completeness. Confirm the extract covers all channels that affect taxable events or the tax base, including refunds, reversals, credits, and manual adjustments. Then confirm classification logic still matches current product and payment flows, especially where platform liability may depend on how the platform facilitates the sale.

Define the minimum evidence pack#

Keep a defensible monthly pack tied to the filing period. A practical minimum pack can include:

- Transaction extracts used for filing support, including period dates, source system, pull timestamp, and filters

- Platform-role rationale, whether in a memo or approved ticket, for the treatment used in scope

- Contract snapshot for the period, including effective terms, seller agreement, and relevant checkout terms, not only the latest version

- Exception register for excluded, overridden, or unresolved items, with owner, reason, and status

This record set helps connect calculation to legal position and supports data-sharing or follow-up requests.

Set checkpoints before filing#

Do not rely on a vague reasonableness review. Use explicit pre-filing gates:

| Gate | What to define | Approval or escalation |

|---|---|---|

| Mismatch tolerance | Internal variance threshold between transaction support and draft filing totals | Mandatory escalation above that threshold |

| Exception aging | What can remain unresolved and how long | Who can approve filing with open items |

| Sign-off | Named approval that reconciliation is complete, exceptions are resolved or approved, and the evidence pack is locked | Named approval |

There is no universal global tolerance or aging threshold provided in the cited guidance, so these controls should be set internally by market and filing type.

The failure mode to watch is straightforward: product changes the payment flow, but tax classification logic does not change with it. When checkout, collection, settlement, or refund handling changes, rerun classification review before the next filing cycle.

Before each filing cycle, run a quick consistency check on counterparty tax IDs and records with the VAT Number Validator.

Design contracts and payment flows to reduce avoidable VAT risk#

If your legal position and customer journey conflict, the customer journey can become the bigger VAT risk. For platform operators, the practical goal is consistent signals across contract terms, invoices, payment authorization, price display, and cancellation handling.

Pick a contract pattern, then make the customer journey match it#

Choose one operating pattern and keep every customer-facing artifact aligned with it. As a practical business framing, a platform-as-principal model presents the platform more directly in the sale, while a platform-as-intermediary model keeps the underlying seller or service provider more visible and the platform in a facilitation role.

That choice feeds into VAT role analysis, and mixed facts make that analysis harder to defend. Specific legal outcomes can vary by jurisdiction and facts. The contract label alone is not enough, and payment processing details are only one part of the picture. What matters is consistency. When your documents and product behavior point in different directions, your position gets weaker.

If you want to preserve an intermediary position, avoid customer-facing language that makes the platform look like the seller. When billing language, commercial presentation, and post-sale handling shift toward a platform-first experience, escalate before launch instead of trying to justify the mismatch later.

The details that strengthen or weaken your file#

Small implementation details can decide whether an online-services setup is compliant or exposed. Price display, VAT calculation, and cancellation-right handling are core controls, not cosmetic choices.

A stronger evidence pattern is simple and consistent:

- The checkout names the same party shown in the T&Cs and invoice.

- Payment authorization wording matches that party and stays clear about who supplies the service.

- Refund, cancellation, and support wording follow the same role allocation as the contract.

A common failure mode is misalignment: intermediary language in legal terms, but platform-first wording in checkout, invoicing, and cancellation flows. That can increase VAT ambiguity.

In the European Union, digital services are treated differently from physical goods, so this alignment check matters even more. If your filing position depends on role analysis, retain the exact contract snapshot and live customer-flow evidence for the filing period, not just the current version.

Verify what an auditor would actually see#

Run one live-transaction review whenever checkout, invoicing, or refund logic changes. Confirm the named supplier, VAT display, payment authorization wording, invoice issuer, and cancellation path still match your intended position.

Keep a minimum document pack: effective customer T&Cs, seller terms, invoice template, checkout screenshots, payment confirmation wording, and a short role-rationale memo. Keep version and go-live dates. Invoicing and record-keeping are explicit compliance checkpoints for online service providers, so undated screenshots and generic templates are weak evidence.

Accept the tradeoff early#

Reducing operational friction can increase VAT ambiguity. A unified checkout and platform-first support and billing language can improve customer experience while blurring role allocation.

Clearer contractual allocation may require tighter legal drafting, product constraints, and stricter document control. Make that tradeoff explicitly. If you choose a simpler customer journey, plan for more legal review and stronger evidence retention. If you prioritize lower role ambiguity, accept the added operational overhead.

Spot red flags that should trigger counsel immediately#

Some issues should not wait for a routine monthly review. Escalate immediately when the uncertainty is about legal character, filing scope, or evidence, not just a VAT rate.

| Red flag | Immediate step | Detail |

|---|---|---|

| A new EU launch where supplier role is unclear and undocumented | Involve counsel before launch | Consider whether a VAT Cross-border Ruling is appropriate for genuinely complex cross-border setups |

| A mismatch between platform or payment data and filed VAT totals | Treat this as a hard stop, especially if you use OSS | Confirm that all supplies within the chosen OSS scheme were declared through OSS, and confirm that no one treated OSS returns as replacing domestic VAT returns |

| Conflicts between contract language and product behavior | Escalate | Send counsel the primary evidence set from the filing period: signed terms, checkout and invoice snapshots, payment and settlement extracts, filed returns, and the reconciliation bridge |

| Any assumption that DAC7 reporting is enough for VAT evidence | Keep a separate VAT evidence pack | EU marketplace rules include record-keeping requirements even where the platform is not the deemed supplier |

In practice, the fastest test is whether you can produce a dated supplier-role memo that matches the live product, contracts, invoicing, and payment flow. If you cannot, involve counsel before launch. The same urgency applies when OSS figures do not tie to platform or payment data, or when terms allocate the supply one way but checkout, invoicing, or payment flows show another reality.

Do not treat DAC7 reporting as a substitute for VAT-specific record keeping. EU marketplace rules include record-keeping requirements even where the platform is not the deemed supplier, so keep a separate VAT evidence pack.

Related reading: UK Online Safety Act Compliance for Marketplace and Platform Operators.

Implement in 90 days without overbuilding#

Use the first 90 days to prove control, evidence, and escalation discipline before you scale automation. Treat this as an operating plan template, not a legal test for market-specific VAT outcomes. Market-by-market VAT status, registration triggers, and threshold rules should remain explicitly unknown here until jurisdiction-specific advice is confirmed.

| Period | Focus | Done when |

|---|---|---|

| Days 1-30 | Define terms, decision ownership, and escalation rules | Each item has a named owner, approval path, and effective date |

| Days 31-60 | Run a control matrix and evidence-pack process in Finance Ops | A reviewer can trace source records to dated filing support for a monthly sample |

| Days 61-90 | Complete one dry cycle and one live cycle, then measure exceptions | Open risks are explained, assigned, and tracked to resolution |

Days 1-30#

Standardize language first so Legal, Product, and Finance Ops are making decisions on the same definitions. Keep the first taxonomy short and practical: what the flow is, who approves, what evidence is required, and when escalation is mandatory.

Date-stamp every decision artifact. Effective dates and approvers are the minimum checkpoint if you need to show what position was in force at a given time.

Days 31-60#

Make controls runnable, not theoretical. Your control matrix should map each monthly step to one owner, one source record set, and one expected output.

Build a consistent evidence-pack template and use it every cycle. The goal is reconstructability: another reviewer should be able to follow the trail without collecting context from multiple teams.

Days 61-90#

Run one dry cycle on a closed month, then one live cycle with the same owners and approval path. Use milestone-style measurement with clearly defined metrics, then track exceptions and unresolved risks.

Keep scope tight while you learn. In regulated environments, fragmentation, heavy rules, and limited scalability can hurt investment growth, so start with the highest-volume and highest-liability scenarios before a broader rollout.

Conclusion#

For platform operators, the priority is not a bigger rate table. It is a repeatable liability decision path, a market triage map, and a monthly evidence cycle your team can run and defend.

The core question is whether your platform may be treated as the VAT or GST supplier for the transaction. In practice, that means checking who set prices, dispatched service providers, issued payment requests as tax invoices, and collected payments, then testing those facts against the legal position you plan to file on. If those facts point to platform control, treat deemed-supplier risk as live until local advice confirms otherwise.

Your strongest defense is period-specific evidence tied to transaction reality. Keep the transaction universe, classification logic for the period, contract or terms snapshots with effective dates, payout-flow documentation, invoice behavior, and reconciliations from filings back to source transactions and payment totals. If a filed figure cannot be traced back, it is not well defended.

This discipline matters more as tax authorities gain more data and better matching capability. In the EU, the trend is toward more digital reporting, updated platform VAT rules, and single-registration mechanics. More automatic information exchange raises the cost of weak reconciliation.

Keep country-specific unknowns on an explicit escalation list. Where platform control is significant, exposure can be broader than commission-only assumptions in some jurisdictions.

Run three operating rules:

- Document your liability decision path before launch, and update it when checkout, invoicing, or payout behavior changes.

- Maintain a market triage map that separates confirmed treatment from items needing local validation.

- Close each month with a locked evidence pack only after reconciliation to transaction, ledger, and payment data is complete.

If you can show, for each filing period, who controlled what, why treatment followed, and where local unknowns were escalated, you reduce reassessment risk and operational chaos.

This pairs well with our guide on Canadian GST/HST Registration for Platform Operators in the Digital Economy.

If you want to pressure-test your liability model and rollout plan by market, talk with Gruv to confirm operational fit and coverage.

Frequently Asked Questions

When is a platform operator treated as the VAT supplier for digital services?

A platform operator can be treated as the VAT supplier when a deemed-supplier rule makes the platform responsible for charging and collecting VAT, unless the underlying provider already does so. That proposal is described for passenger transport and short-term accommodation platforms, so do not assume the same outcome across every market or platform type.

Do 2026 changes under VAT in the Digital Age create new registrations for every non-resident digital service provider?

No. ViDA should not be treated as a blanket trigger for new registrations for every non-resident digital service provider. Use it as a signal to verify registration and reporting obligations by market.

How is digital-services VAT different from low-value goods rules under the VAT e-commerce package?

The excerpts confirm a shared OSS/IOSS framework for VAT declaration and payment in one Member State and note that, as of July 2021, it covers B2C services and distance sales of goods. They do not provide a full side-by-side legal test for low-value goods versus digital services, so do not assume identical liability or evidence rules.

What minimum monthly controls reduce VAT surprise exposure for cross-border platforms?

Run a repeatable monthly control set that covers reporting information, declaration-process readiness, and verification procedures. Keep period records organized so filing positions can be checked and defended. The excerpts do not set fixed mismatch tolerances, exception-aging thresholds, or mandatory sign-off SLAs.

What evidence should we retain to defend deemed-supplier or intermediary treatment in an audit?

Keep a dated evidence pack for each filing period that supports who charged and collected VAT and how amounts were reported. Retain the records needed for reporting information, declaration process, and verification procedures. DAC7-style reporting discipline can help structure records, but it does not replace VAT-specific evidence.

When should a VAT issue be escalated to specialist tax counsel instead of handled internally?

Escalate when supplier-role treatment is unclear for the relevant market or platform model, when registration posture changes rely on template assumptions instead of market-specific analysis, or when a team assumes DAC7 reporting automatically satisfies VAT evidence requirements. Escalate early where registration and documentation burden is high, since errors can be costly to unwind.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- documents1.worldbank.org/curated/en/099140301092229225/pdf/P172259091...trusted

- europarl.europa.eu/legislative-train/carriage/vat-in-the-digita...trusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- oecd.org/content/dam/oecd/en/publications/reports/202...trusted

- sec.gov/Archives/edgar/data/2024656/0001213900240899...trusted

- sec.gov/Archives/edgar/data/1370637/0001370637260000...trusted

- stripe.com/resources/more/selling-online-services-in-th...trusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: