Quick Answer

Start with per-flow role mapping under the Excise Tax Act, then choose registration only after that map is stable. For canadian gst hst platform operators registration digital economy tax decisions, the main operational risk is applying one platform-wide label even though CRA indicates a business may be affected by multiple measures. Hold automation for disputed classifications, and require written tax, product, and finance approval before launch.

GST/HST Registration Basics for Platform Operators#

If your platform touches Canadian customers, start by deciding whether Canada's digital-economy GST/HST measures may apply to each transaction flow. This is an operational question with real consequences. An affected business or platform operator may need to register for a GST/HST account and charge, collect, and remit tax under CRA-administered Excise Tax Act (ETA) rules.

This guide is for compliance, legal, finance, and risk owners, and for the product and payments teams supporting them. The practical job is to map your platform role and supply type by transaction leg, identify which obligations may attach, and know when to escalate instead of relying on assumptions.

You cannot treat timing and scope as optional. The ETA digital-economy amendments took effect on July 1, 2021. CRA guidance also says a business may be affected by more than one measure at the same time. In practice, that means you should assess the combined impact across flows instead of applying one blanket treatment.

Start with role mapping before you touch registration mechanics. At minimum, confirm:

- which legal entity is in scope

- what the platform is doing in the transaction

- whether there is a taxable supply in Canada

- who is expected to handle collection and remittance

- whether your data and records can support that position, including notification and information reporting needs

This article is an operational interpretation aid tied to CRA guidance and the ETA, not legal advice. The excerpts behind this guide are directionally clear but not complete for every edge case, threshold scenario, or role-classification dispute, so uncertain cases should be escalated early. CRA also indicates a prospective compliance approach except for egregious non-compliance. Treat that as context for escalation planning, not as a reason to defer core controls.

For the reporting side of marketplace compliance, see Digital Platform Reporting for Online Marketplaces: MRDP, DAC7, and UK HMRC Duties.

Start with the terms that control liability#

Liability often turns on role classification. Under the ETA, a registrant making a taxable supply in Canada must collect GST/HST from the recipient and remit it.

Before you design registration or tax logic, map each transaction leg to the legal entity making the supply, the entity facilitating it, and whether that leg is a taxable supply in Canada. Since the digital-economy measures took effect on July 1, 2021, those labels can change who may need to register, charge, collect, and remit.

- Non-resident supplier: a named category generally covered by Canada's digital-economy GST/HST provisions.

- Non-resident vendor: a non-resident seller of taxable digital products or services.

- Distribution platform operator: a platform operator that facilitates certain supplies through a platform, including specified cross-border digital supplies.

- Accommodation platform operator: relevant to short-term accommodation situated in Canada where the operator meets specified conditions, such as controlling or setting essential transaction elements.

These labels are not cosmetic. CRA guidance indicates that a business may be affected by more than one measure at the same time. Customers may also pay GST/HST to a distribution platform operator or accommodation platform operator rather than the underlying supplier.

Use a simple control check now: document role by transaction leg, product line, and legal entity, then test each leg for a taxable supply in Canada. If one global label is being applied to the whole platform, treat that as a classification risk.

Map your platform role before touching registration#

Map role by transaction leg before you choose any GST/HST registration path. CRA guidance under the ETA says a business can be affected by more than one digital-economy measure depending on its supplies, so a single platform-wide label can misstate obligations.

A role matrix helps you separate who makes the supply from who collects GST/HST. CRA also notes that even if an underlying supplier is not required to register and collect, customers may still pay GST/HST to a distribution platform operator or accommodation platform operator.

| Role | Supply type | Customer type | Collection owner |

|---|---|---|---|

| Non-resident supplier | Supplies made directly by that entity, including affected cross-border digital products or services | Varies by supply; for affected cross-border digital products or services, CRA points to Canadian consumers and Canadian entities not registered under the normal GST/HST regime | For taxable supplies in Canada made by a registrant, that registrant generally collects and remits; in some cases customers may pay GST/HST to a distribution or accommodation platform operator |

| Distribution platform operator | Platform-facilitated supplies covered by digital-economy distribution-platform measures | Customers purchasing through the platform | The platform operator may charge and collect GST/HST for affected supplies |

| Accommodation platform operator | Platform-facilitated supplies covered by digital-economy accommodation-platform measures | Customers booking through the platform | The platform operator may charge and collect GST/HST for affected supplies |

If your platform is both facilitator and direct seller, split the analysis by transaction leg instead of using one global tax assumption.

Use this contrast to keep the rule set narrow:

- Cross-border digital services: test whether the supply is in scope and confirm customer status, including Canadian consumers and Canadian entities not registered under the normal regime.

- Other taxable supply flows: re-test who is making the taxable supply in Canada and who owns collection for that specific leg. Do not assume the same customer test or collection outcome applies.

If a transaction cannot be explained in one matrix row (role, supply type, customer type, and collection owner), pause registration and configuration until classification is resolved.

For a comparative view of platform-operator indirect tax rules, see Singapore GST for Platform Operators: OVR Regime and Digital Service Tax Compliance.

Compare standard and simplified registration paths#

Treat the registration path as a control decision, not just an admin step. It affects business-customer treatment, reconciliation, and confidence in downstream Input tax credit (ITC) outcomes.

CRA confirms two relevant lanes in public digital-economy guidance: a Simplified GST/HST registration, reporting and remittance regime for certain non-resident vendors and platform operators, and the normal GST/HST registration regime. Those excerpts are high level, so eligibility edges, B2B edge cases, and ITC outcomes are not fully resolved there.

| Decision area | Standard GST/HST registration regime | Simplified GST/HST registration regime | What this article cannot confirm from public excerpts |

|---|---|---|---|

| Who typically uses it | Businesses whose facts place them in the normal GST/HST registration regime. | CRA says this is applicable to certain non-resident vendors, non-resident digital platform operators, and distribution platform operators for covered digital-economy activity. | The excerpts do not fully set out all statutory conditions, exceptions, or whether a platform can choose between paths in a specific fact pattern. |

| Return and remittance expectation | Regular GST/HST account administration under the normal regime. | CRA explicitly frames this as simplified registration, reporting, and remittance. | The excerpts here do not provide filing frequency, return fields, deadlines, or penalty detail for either path. |

| Business-customer treatment and ITCs | Often the path teams assess when business-customer treatment and tax-credit recovery are central to the model. | CRA frames this lane as simplified, but practitioner guidance warns some simplified-regime invoice scenarios can leave tax paid but not recoverable through an ITC. | CRA excerpts used here do not confirm universal ITC outcomes or full evidence standards for each B2B treatment path. |

| Core control implication | Better fit when your teams need invoice, customer-status, and reconciliation logic tied to regular GST/HST account processes. | Better fit when in-scope activity matches simplified rules and customer-status handling is reliable. | Public excerpts remain high level on invoice content, customer evidence standards, and treatment detail when a buyer presents business registration information. |

A practical tradeoff is this: simplified is designed to simplify registration, reporting, and remittance, but weak customer-status logic can create cleanup later.

Use one verification checkpoint before you commit#

If simplified appears in scope for your facts, require proof that product can capture and retain the customer tax data needed for tax decisions and reporting. A practical checkpoint from practitioner guidance is whether a buyer's GST/HST registration number can be entered in billing or account settings and actually flows through your tax logic. If that data only lives in notes or tickets, your controls are not ready.

Some commercial summaries say simplified-regime B2B treatment may allow 0% tax when a buyer provides a 9-digit BN. Treat that as a review trigger, not production logic. The CRA excerpts here do not confirm the full conditions, validation standards, or audit evidence requirements.

Put ownership in the right seats#

Keep ownership split across functions. Tax sets the position under the ETA and CRA guidance. Product implements invoice and tax logic, including capture and transfer of customer registration details. Finance validates reconciliation outputs, remittance support, and exception reporting under the chosen path.

If those three owners cannot explain the same transaction the same way, pause registration and configuration until classification and controls align.

Related reading: DAC7 for Platform Operators: Scope, Seller Data, and Controls for EU and Non-EU Platforms.

Use a registration checkpoint sequence before go-live#

Use this as an internal launch control pattern, not a CRA-prescribed GST/HST legal checklist. The public excerpts used here do not establish a required four-step digital-economy GST/HST go-live order.

Move in dependency order#

If you use a checkpoint sequence, tie it to control dependencies and document where assumptions are still provisional.

- Confirm the role assumptions your workflow relies on.

- Confirm how your rule logic is classified and documented.

- Validate the customer-status assumptions that affect treatment.

- Assign clear ownership for filing and remittance tasks.

If one step is unresolved, treat downstream setup as provisional.

Escalate mixed or disputed classification before launch#

The excerpts do not set a GST/HST-specific escalation rule. As an internal risk control, consider escalating mixed or disputed classifications before go-live and avoid fully automating that segment until interpretation is resolved.

Require explicit interpretation sign-off#

The excerpts do not establish a formal compliance-and-finance sign-off duty for digital-economy GST/HST measures. If useful, add written interpretation approval as an internal control to reduce silent production drift.

Gate launch on reporting readiness#

For Notification and information reporting, the excerpts do not confirm a GST/HST-specific launch duty. They do show a useful CRA verification posture in the 2026-2028 Accessibility Plan: "fewer actions but a greater focus on measurement." The checks listed there include "including persons with disabilities in user testing." Apply that posture to your launch outputs. Verify they are consistently generated, owner-reviewed, and understandable to real users before go-live.

For a step-by-step walkthrough, see GST Digital Marketplace Platform Comparison for Australia, Canada, and India.

Before launch, align your checkpoint owners and evidence handoffs with systems that support policy gates, traceable records, and controlled retries in the Gruv docs.

Handle business-customer cases without breaking ITC logic#

Business-customer treatment should follow evidence, not just account labels. CRA's digital-economy GST/HST guidance frames the Simplified GST/HST registration regime around Canadian consumers and Canadian entities not registered under the normal regime. Customer registration status can therefore change which path applies.

That decision affects Input tax credit (ITC) outcomes downstream. Under the ETA framework, registrants may generally recover GST on purchases or imports to the extent they relate to commercial activities. If your platform applies one rule to all business-looking customers, you can create a mismatch. What was charged, what the customer expected from its GST/HST account status, and what finance has to defend later may no longer line up.

Where the operational risk starts#

The break point is often evidence handling. A customer provides GST/HST registration details, but the platform ignores them, stores them without checks, or switches treatment without enough support. In digital-economy flows, that can move a transaction between a simplified-regime lane and a normal-regime assumption.

You should also expect mixed exposure. CRA notes a business may be affected by more than one digital-economy measure and should assess combined impact. If you operate across multiple roles or customer types, avoid one global rule for every transaction.

Minimum controls worth building#

Use a minimum evidence standard before you change treatment:

| Control | Keep | Article detail |

|---|---|---|

| Capture tax ID plus customer assertion together | Submitted registration number, entity details, channel, and timestamp | Keep them together before you change treatment |

| Apply a validation step before switching treatment | Structured identifier data and a clear customer representation | Not free-text notes alone |

| Store transaction-level evidence | Original submission, edits, customer-facing tax output, and the tax-rule version used at pricing | Retain at transaction level |

| Version tax determination rules | Effective dates, approvers, and impacted transaction types | When logic changes |

Those four controls do most of the work. The practical test is whether finance can reconstruct why GST or HST was or was not charged on a specific order without engineering log forensics.

Failure mode and the right bias#

One error scenario is charging GST/HST under the wrong registration path and finding it later. That can create additional review, reconciliation, and audit-trail cleanup work.

The opposite error is also risky: suppressing collection on weak evidence. If evidence is incomplete, low quality, or changed after purchase, prefer escalation over automated non-collection. A short manual review step can be safer than unwinding a disputed tax position tied to customer status and ITC expectations.

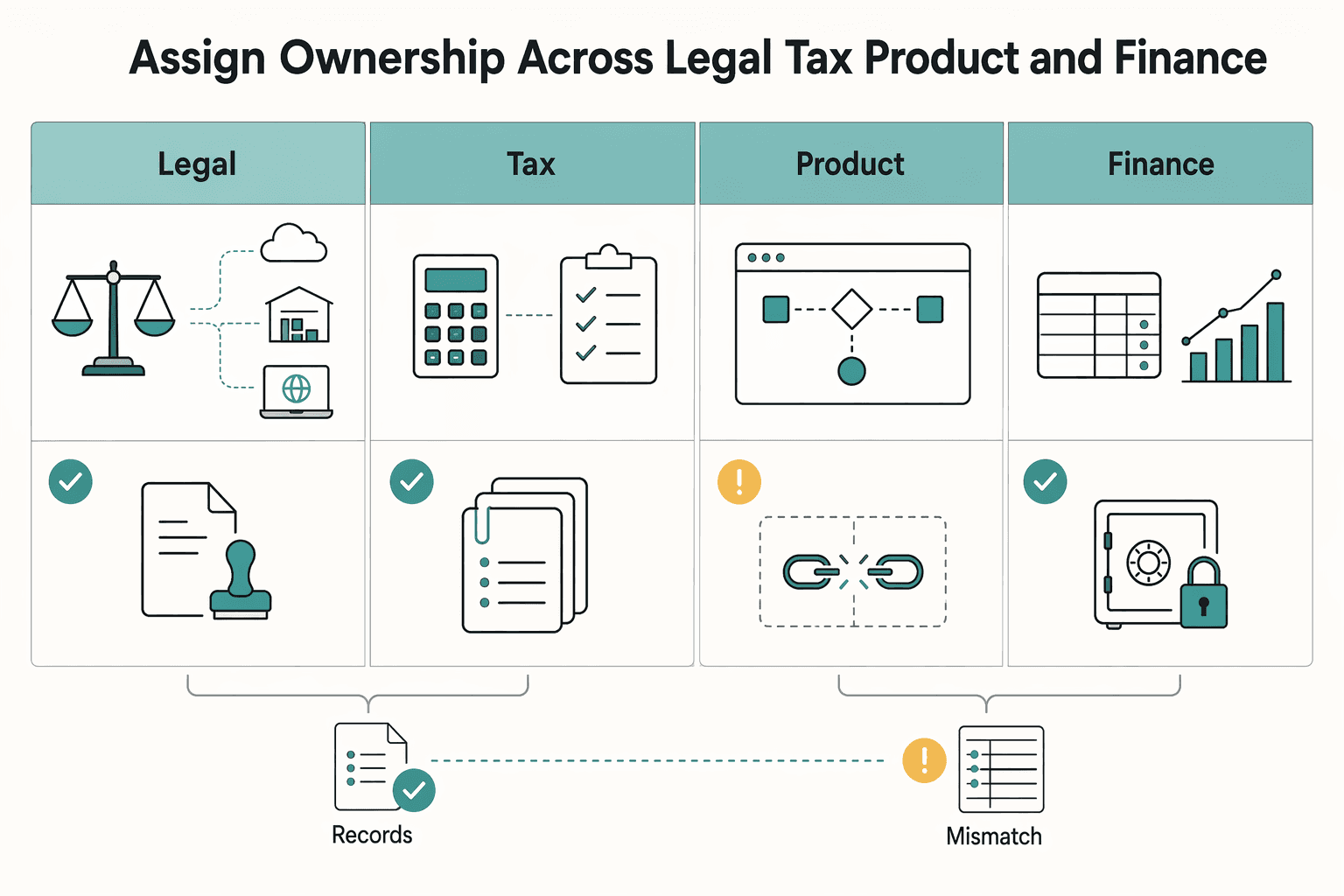

Assign ownership across legal, tax, product, and finance#

When registration path and supply type can change tax treatment, unclear ownership becomes a filing risk. Assign one accountable owner per decision point, and route production rule changes through a defined approval path.

| Function | Owns the decision | What they should produce | Release checkpoint |

|---|---|---|---|

| Legal | Interprets scope and classification questions | Position note on platform role, supply type, and whether activity fits a Distribution platform operator context | Open interpretation issues resolved or escalated |

| Tax | Signs collection, remittance, and regime logic | Decision record for Simplified GST/HST registration, reporting and remittance system versus normal GST/HST rules, plus documented treatment exceptions | Written tax approval before production change |

| Product | Implements tax rules in the platform | Rule specs, effective dates, test evidence, release records, rollback plan | Test evidence and release records complete |

| Finance | Owns reconciliation and filing support | Traceable exports from transaction outcomes to filing-support totals for GST/HST workflows | Finance impact review completed before launch |

Legal should handle interpretation, especially where flows differ between digital supplies and goods linked to Canadian fulfillment warehouses under normal rules. Tax should then convert that interpretation into collection and remittance logic, including what evidence is required before treatment changes.

Finance should be involved before release, not after month-end. Covered businesses may need to register, collect, and remit GST/HST on taxable sales. Distribution platform operators can also have CRA-facing information obligations on third-party vendors. If finance only sees aggregate totals, reconciliation risk increases.

Use controls that support review as well as deployment: approvals, policy gates, audit logs, and traceable exports. These are operational controls, not statutory requirements, but they can reduce avoidable failures and make incident recovery safer.

Keep a strict internal handoff rule: no production tax-rule change without tax and product approval, plus finance impact review. Keep the evidence trail together. CRA can request supporting documentation to substantiate eligibility conditions, and documentation-heavy requests can become administratively burdensome and may involve sensitive information. One complete record set is easier to defend than scattered tickets and inbox history.

Build the evidence pack CRA reviewers expect#

Once ownership is clear, build one reproducible record set for each GST/HST decision path, anchored to the Excise Tax Act (ETA) first and then to the guidance you used. RC4022 can support interpretation, but it is plain-language guidance and does not replace the law.

| Evidence item | What to keep | Article detail |

|---|---|---|

| Small-supplier status | Registration analysis showing how you assessed small-supplier status | Treat registration basis as a separate checkpoint |

| Thresholds applied | CAD30,000, or CAD50,000 for a public sector body or charity | Record the thresholds you applied |

| Threshold exceptions | Notes on any exception where a threshold-only check was not enough | Keep exception notes in your records |

| Registration records | Submitted documentation such as RC1 where relevant | Keep core registration records together |

| Voluntary registration | Decision record when registration was voluntary | Include it in the registration basis record |

Keep the registration basis as its own checkpoint. Your record should show how you assessed small-supplier status, which thresholds you applied (CAD30,000, or CAD50,000 for a public sector body or charity), where exceptions mattered, what was filed such as RC1 where relevant, and whether registration was voluntary.

The provided excerpts do not set a CRA-mandated evidence-pack checklist, transaction-level traceability standard, or specific retention period. Document those controls under your internal policy and legal/tax review.

Execute a 30 60 90 day implementation plan#

Use an internal 90-day rollout to validate classification and collection controls before scaling. If role analysis is still disputed or the evidence pack is incomplete, hold that segment instead of automating on assumptions.

| Phase | Focus | Outputs |

|---|---|---|

| Days 0 to 30 | Role mapping and a draft registration position before invoice configuration | One file per treatment path with entity, rule basis, customer-status assumptions, and open issues |

| Days 31 to 60 | Invoice logic, exception queues, and reconciliation design after the role and registration draft is stable | Separate checkpoints for registration, collection, and place-of-supply logic |

| Days 61 to 90 | Stress-test before cutover | Parallel validation on samples and at least one remediation drill |

This phase turns your evidence pack into production controls that can handle real invoice volume, exceptions, and ownership handoffs.

Days 0 to 30#

Start with role mapping and a draft registration position before invoice configuration. For each product line and transaction leg, map your reasoning to the Excise Tax Act (ETA) first, then to the CRA guidance used for interpretation, and record guidance versions, for example, RC4022(E) Rev. 25 and RC4027(E) Rev.23, in your control file.

For each legal entity and product line, create a short memo. It should cover who is supplying, whether the supply is taxable, whether resident or non-resident status affects treatment, which role is being assumed for that leg, who would own collection and remittance under that draft, and what is still unresolved. Keep these conclusions explicitly marked as draft where fact gathering is still open.

By day 30, you should have one file per treatment path with entity, rule basis, customer-status assumptions, and open issues. If that file set is not complete, you are not ready for rule coding.

Days 31 to 60#

Do not move to invoice logic, exception queues, and reconciliation design until the role and registration draft is stable. Tax, product, and finance must use the same field definitions for customer status, supplier identity, and supply classification, or rule behavior will drift.

Use separate checkpoints for registration, collection, and place-of-supply logic. Keep approvals separate as well, so scope decisions, invoice outcomes, and location-driven treatment are not collapsed into one uncontrolled rule set.

Build exception queues early for unclear resident or non-resident status, missing customer evidence, and role mismatches between product flow and legal memo. Each queued item should record why it was held, who reviews it, and what evidence clears it, with that evidence fed back into your pack.

Reconciliation should verify traceability, not only totals. Source inputs, rule version, invoice result, and expected filing or remittance owner should be traceable without manual reconstruction.

Days 61 to 90#

Use the final month to stress-test before cutover. Run parallel validation on samples, either against current production behavior or against manual review, to catch classification drift before filing impact.

Prioritize mixed-role, cross-border, and role-sensitive flows, including transactions that may be misclassified between non-resident supplier treatment and other role assignments. Confirm each sampled audit trail is complete enough to support CRA review.

Run at least one remediation drill using a realistic misclassification scenario. Validate who halts rules, who quantifies impact, who updates decision records, and how finance reflects corrections.

Launch criteria#

Do not go live until all gates are met:

- evidence pack completeness is confirmed for each active treatment path

- finance signs off that reconciliation outputs support filing and remittance ownership

- escalation paths are tested with real scenarios

- unresolved legal edge cases are closed or explicitly excluded from automation

If role classification or scope is still disputed late in the cycle, hold and escalate. CRA guides are informational and do not replace law, and CPA materials are not a substitute for specialized professional advice in specific fact patterns.

Plan for mistakes, remediation, and escalation#

Treat remediation as a controlled process. Pause the affected path, work from transaction facts and internal records, and avoid changing production behavior from generic summaries alone.

Common misses are often operational:

- role drift after product, pricing, or checkout changes

- incomplete evidence at invoice time

- over-reliance on high-level summaries when facts are mixed or disputed

Use this remediation order as an internal control sequence, not as a CRA-prescribed method:

- Stop the affected rule path.

- Quantify exposure by entity, period, invoices, and tax impact.

- Correct treatment prospectively and validate before restart.

- Assess historical correction separately with specialist input.

Keep knowns and unknowns separate in every escalation file:

- Known from the provided excerpts: clearer expectations and fact-supported decision records can improve compliance outcomes.

- Unknown from the provided excerpts: GST/HST thresholds, edge-case role tests, full penalties and interest outcomes, and complete correction mechanics.

Escalate when ambiguity is material or facts remain disputed after initial remediation. Require a complete, detailed, fact-supported escalation pack. If facts are still thin, hold the segment instead of automating through uncertainty.

Related reading: Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints.

Conclusion#

Start with role classification, then choose the registration path, then build controls and evidence. Reversing that order can create extra process work without adding certainty.

That sequence matters because Canada's digital-economy GST/HST measures have been in effect since July 1, 2021, and many non-resident businesses and platform operators had to reassess obligations. A recurring operational risk is treating the business as one global role when transaction paths differ.

Keep a high-value checkpoint at the transaction level. If you facilitate short-term accommodation in Canada, ask whether you control or set the essential elements of the transaction between supplier and recipient. That can affect accommodation platform operator treatment. Also keep in mind that CRA glossary language is a plain-language aid, not legal text, so final positions should be validated against the Excise Tax Act and escalated where needed.

The tradeoff is straightforward. Underbuilding controls can increase surprise risk in filing and remittance operations, while overbuilding before role clarity can automate the wrong owner, logic, or evidence flow. Precision first is often cheaper than rework later.

Also avoid relying only on legacy physical-presence instincts. One advisory source indicates these rules may apply even without physical presence in Canada and even without carrying on business under older concepts, so offshore status alone is not, by itself, a reliable screen.

Your next step this quarter:

- Run a role matrix across top transaction types by volume and revenue.

- Apply registration checkpoints to each transaction path separately.

- Escalate mixed-role, accommodation, and business-customer edge cases early.

- Get tax, product, and finance sign-off before changing live GST/HST logic.

The goal is a defensible position matched to the right regime, with evidence that supports your treatment decisions if reviewed later.

If your team needs to validate scope, controls, and market-specific rollout constraints before implementation, contact Gruv.

Frequently Asked Questions

Who must register under Canada’s digital-economy GST/HST rules?

At a high level, the Excise Tax Act digital-economy rules generally apply to non-resident suppliers, distribution platform operators, and accommodation platform operators. CRA also indicates one business may be affected by more than one measure, so a single-role assumption can fail. If your facts span multiple roles, assess each transaction path separately.

What is the simplified GST/HST registration regime for platform operators?

The simplified GST/HST regime is a separate registration, reporting, and remittance path for certain digital-economy cases. CRA’s registration guidance states that, for cross-border digital products and services, registration is required under the simplified regime. Treat simplified as its own regime choice, not as a shorter version of normal registration.

How is the standard GST/HST registration regime different in practice?

The standard path is the normal GST/HST account, and it is not interchangeable with simplified registration. CRA states you cannot be registered under both at the same time, and for supplies of qualifying goods, simplified is not available and normal registration is required. CRA also states a business otherwise required to use simplified may be able to apply voluntarily for normal registration if certain conditions are met, but those conditions are not detailed in the excerpts here.

When can GST/HST treatment differ for business customers?

Treatment can differ when your tax logic depends on whether the customer is a business registrant. One non-CRA summary says simplified-regime GST/HST charged to Canadian business registrants may not be ITC-recoverable, but that point is not confirmed as a settled CRA position in the excerpts here. Where that distinction affects pricing or invoicing, get specialist review before automating exceptions.

What changed when Canada introduced the digital-economy GST/HST measures?

Canada’s digital-economy GST/HST measures are already in effect. CRA states they took effect on July 1, 2021 through ETA amendments that generally apply to the operator categories above. CRA also notes that even if a supplier is not required to register and collect, customers may still pay GST/HST to a distribution platform operator.

What evidence should a platform retain for CRA review?

The clearest operational checkpoints are in the registration flow: prepare the full submission before starting because CRA says the online process cannot be saved and times out after 30 minutes of inactivity. After submission, keep the CRA reference number for status follow-up.

What details are still unknown from high-level public summaries and require specialist advice?

Several items require specialist advice. That includes full legal conditions for voluntary normal registration, definitive ITC outcomes across all simplified-regime scenarios, specific penalties or interest, full retention periods, and complete edge-case role definitions. If your decision depends on those points, or on mixed-role facts, escalate for specialist advice before shipping tax logic.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- oecd.org/content/dam/oecd/en/publications/reports/202...trusted

- oecd.org/en/publications/consumption-tax-trends-2024_...trusted

- stripe.com/ae/guides/understanding-the-tax-obligations-...trusted

- canada.ca/en/revenue-agency/services/tax/businesses/to...external

- canada.ca/en/revenue-agency/services/tax/businesses/to...external

- chamber.ca/wp-content/uploads/2025/09/Proposed_Resoluti...external

- connectcpa.ca/blog/the-simplified-gst-hst-regime-for-digit...external

- dgchait.com/en/publications/new-gst-hst-rules-for-digita...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Singapore GST OVR Compliance Decisions for Platform Operators

For platform operators, the real question is whether your Singapore-facing flows fall within GST under the Overseas Vendor Registration (OVR) regime, not whether there is a separate digital services tax. Get that call wrong, and downstream decisions drift with it: pricing, invoicing, registration planning, and customer messaging.

Making Tax Digital for Income Tax and UK Platform Operators: Confirmed Rules and Open Scope Questions

For platform operators, the first useful move is to separate confirmed HMRC and GOV.UK statements from scope assumptions. Most public guidance on Making Tax Digital for Income Tax is written for sole traders, landlords, and their agents, not for platform operators as a distinct audience.

EU DAC7 Directive for Freelancers Using Digital Platforms

Treat the EU DAC7 Directive as an execution problem, not a theory exercise. Your job is to do three things early: identify which income channels need review, set up one record routine you can actually maintain, and escalate complex cross-border cases before they turn into year-end guesswork.