Quick Answer

Start by treating Singapore obligations as GST under OVR, not a standalone digital service tax. Classify each flow by supplier position, customer GST-registration evidence, and whether it is a remote service or low-value good, then monitor exposure using only validated rows. Keep ambiguous marketplace cases in an exception queue. Once in-scope exposure is likely, align checkout, invoicing, and ledger treatment and retain decision records for at least five years.

How Singapore GST OVR Applies to Platform Operators#

For platform operators, the real question is whether your Singapore-facing flows fall within GST under the Overseas Vendor Registration (OVR) regime, not whether there is a separate digital services tax. Get that call wrong, and downstream decisions drift with it: pricing, invoicing, registration planning, and customer messaging.

This guide is for compliance, legal, finance, and risk owners working with live onboarding and transaction data. The goal is practical: a defensible sequence to classify flows, monitor potential registration obligations, set charging controls, retain evidence, and escalate issues that public guidance does not fully resolve.

IRAS treats OVR as part of GST registration and reporting for imported remote services. Under the extended regime, imported B2C services can be in scope whether digital or non-digital when supplied and received remotely. Electronic marketplace operators may also be treated as suppliers when certain conditions are met.

Timing matters. Since 1 Jan 2020, OVR has applied to B2C digital services to customers in Singapore. From 1 Jan 2023, it extended to B2C non-digital remote services and to imported B2C low-value goods (LVG). If your internal logic still centers only on obvious digital products, you can miss exposure. Start with four concrete controls:

- Determine whether the customer belongs in Singapore.

- Determine whether the customer is GST-registered.

- Support refunds where GST was incorrectly charged to a GST-registered customer.

- Retain evidence for at least 5 years to substantiate GST collected and accounted to IRAS.

The rest of this article follows that sequence so you can decide where Singapore GST likely applies, what to monitor as obligations evolve, and when to escalate to specialist advice.

Start with the terms that change your liability#

Your liability turns on defined GST terms and customer GST-registration status, not on whether an account looks like a "business" account.

| Term | Plain-language meaning | Why it changes action |

|---|---|---|

| Remote services | Services the customer can consume without being physically present where the service is performed. | If a supply is remote and consumed in Singapore, you then classify it as B2C or B2B. |

| Digital services | A working label in this section, but the provided IRAS excerpt does not give a standalone formal definition. | Do not rely on internal product labels alone. Anchor classification to remote-services treatment and actual delivery model. |

| Low-value goods (LVG) | Qualifying imported goods delivered to Singapore by air or post, with value not exceeding S$400. | LVG is treated separately from remote services, so mixed marketplaces should classify goods and services in separate lanes. |

| B2C supplies | Supplies to non-GST registered persons, including individuals and non-GST registered businesses. | Under OVR, GST-registered overseas vendors must account for GST on relevant B2C supplies. |

| B2B imports | Supplies to GST-registered persons. | These may fall into reverse charge instead of an OVR charging path. |

The customer boundary that matters most#

The boundary that matters most is GST-registration status. A company can still fall into the B2C lane if it is not GST-registered, while B2B imports are supplies to GST-registered persons.

For certain GST-registered businesses, reverse charge means the customer accounts for GST as if it were the supplier. In practice, that creates different actions: B2C can require OVR charging, while eligible B2B imports can shift accounting to the customer.

Use a hard control here: store customer GST-registration status as a discrete transaction-level field. Do not infer B2B treatment from a company name, business email domain, or generic onboarding responses.

Read the right authority in the right order#

Use the IRAS guidance in this grounding for operational definitions and treatment of imported supplies. If you need legal interpretation, check the GST Act directly.

If commentary points to Section 21(3) of the GST Act, treat it as a signpost, not a complete answer. The grounding here does not include that section's full legal text or tests.

Do not assume when the fit is messy#

If a transaction does not clearly fit these terms, mark it unresolved and escalate. That usually means uncertainty about one or more of the following:

- whether the supply is truly remote

- whether the item is a service or LVG

- whether the customer is GST-registered at the point of supply

- whether your platform or another party is treated as the supplier for GST purposes

A held classification with a dated review note is usually more defensible than a fast but unsupported tax treatment.

Related reading: Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints.

Which platform operators are likely in scope under OVR#

If your platform facilitates remote services or low-value goods to non-GST registered customers in Singapore, start from the assumption that you may be in scope and narrow that position only after legal confirmation. Under OVR, exposure can arise in two roles:

- your entity acts as an overseas supplier

- your entity acts as an electronic marketplace operator supplying remote services or low-value goods on behalf of suppliers or merchants

Being "only an intermediary" does not end the analysis. The available guidance explicitly brings electronic marketplace operators into the OVR picture if certain conditions are met.

Separate your own supplies from marketplace supplies#

For each flow, split the analysis between:

- supplies where your entity is the supplier

- supplies where your platform facilitates a third-party supplier or merchant

This keeps the assessment tied to your role in each transaction, not to a single label applied across the whole product.

Use a hard evidence test before sign-off#

Do not sign off scope unless you can evidence, for each flow, the role your entity is playing and customer GST-registration status.

If your team cannot evidence the role on a flow, treat it conservatively as potentially in scope, mark it unresolved, and escalate for legal confirmation. Because the triggering conditions are not fully specified in the excerpt, legal confirmation is required before you lock scope decisions.

For a comparable registration analysis in another market, see Canadian GST/HST for Platform Operators: Registration Rules and the Digital Economy Tax.

Map every transaction type before you discuss registration#

Map transactions before you test thresholds. If you classify supplies after the fact, you can end up testing the wrong revenue base, mixing B2C and B2B flows, and missing where marketplace operator exposure sits.

IRAS routes imported consumption through two lanes: OVR for relevant B2C supplies and reverse charge for certain B2B imports. Since these regimes were implemented in 2020, with scope expanded in 2023, the first practical step is a row-by-row classification of supply type, customer type, and supplier role.

Build the table around treatment-changing decisions#

Build your working table around the decisions that actually change treatment. Use these columns:

- transaction type

- customer type

- supplier status

- customer location evidence

- likely lane

- working evidence (internal)

Keep the lane options simple: OVR regime, reverse charge, or pending review / not yet placed. Leave unresolved rows open. IRAS also notes its e-Tax guidance is not complete for every possible issue.

| Transaction type | Customer type | Supplier status | Customer location evidence | Likely lane | Working evidence (internal) |

|---|---|---|---|---|---|

| Remote services | B2C (non-GST registered persons) | Platform as supplier, or third-party supplier via platform | How you determined the customer belongs in Singapore (remote-services guide section 8 checkpoint) | Usually OVR if Singapore B2C and supplier role supports it | Contract terms, checkout terms, invoicing entity, customer GST status record |

| Digital services | B2C or B2B (kept separate as an operating row) | Same supplier-status split | Same customer-belongs test as remote services | May follow remote-services treatment; if scope is unclear, hold for review | Same evidence set, plus product description used in catalog classification |

| Low-value goods (LVG) | B2C or B2B | Platform as supplier, or third-party supplier via platform | Point-of-sale facts and whether goods meet LVG criteria, including value not exceeding S$400 | B2C may route to OVR; certain B2B imports may route to reverse charge | Merchant terms, checkout flow, invoicing entity, customer GST status, goods value evidence |

Separate rows for remote services, digital services, and LVG prevent service logic from leaking into goods, or the other way around. IRAS indicates digital services sit within remote-services scope, but the full definition text is not in this excerpt, so do not use "digital" as a catch-all label.

Supplier status is usually the highest-risk field for platforms#

For most platforms, supplier status is the field most likely to break the analysis. Map it explicitly as platform as supplier versus third-party supplier via platform. IRAS states that, under certain conditions, an electronic marketplace operator may be regarded as the supplier, and relevant B2C supplies made through the marketplace must be included for GST registration liability testing.

Do not rely on "we are only an intermediary." As an internal control, validate each row against the contract party, checkout terms, and invoicing entity. If those do not align, do not use that row for threshold counting.

Treat evidence as part of classification, not cleanup#

Evidence is part of classification, not something to collect later. For each row, capture:

- contracts or marketplace terms showing supplier role

- checkout terms showing what the customer was told

- invoicing entity details

- customer GST status evidence for B2C versus B2B routing

Customer status needs strict handling. IRAS distinguishes B2C as supplies to non-GST registered persons and B2B imports as supplies to GST-registered persons. If GST status cannot be verified, hold the row for review instead of auto-routing it to B2B.

Use this map before tools, returns, or filing cadence#

Most failures start with bad classification, not filing mechanics. Get the map right before you build tools, set return logic, or assign filing cadence.

The OVR thresholds, annual global turnover exceeding S$1 million and Singapore B2C remote services or LVG exceeding S$100,000 annually, are only reliable once rows are correctly classified. If a row lacks defensible customer type, customer-belongs-in-Singapore evidence, or supplier status, keep it out of automated registration calculations until Tax or Singapore counsel resolves it.

For a step-by-step walkthrough, see GST Digital Marketplace Platform Comparison for Australia, Canada, and India.

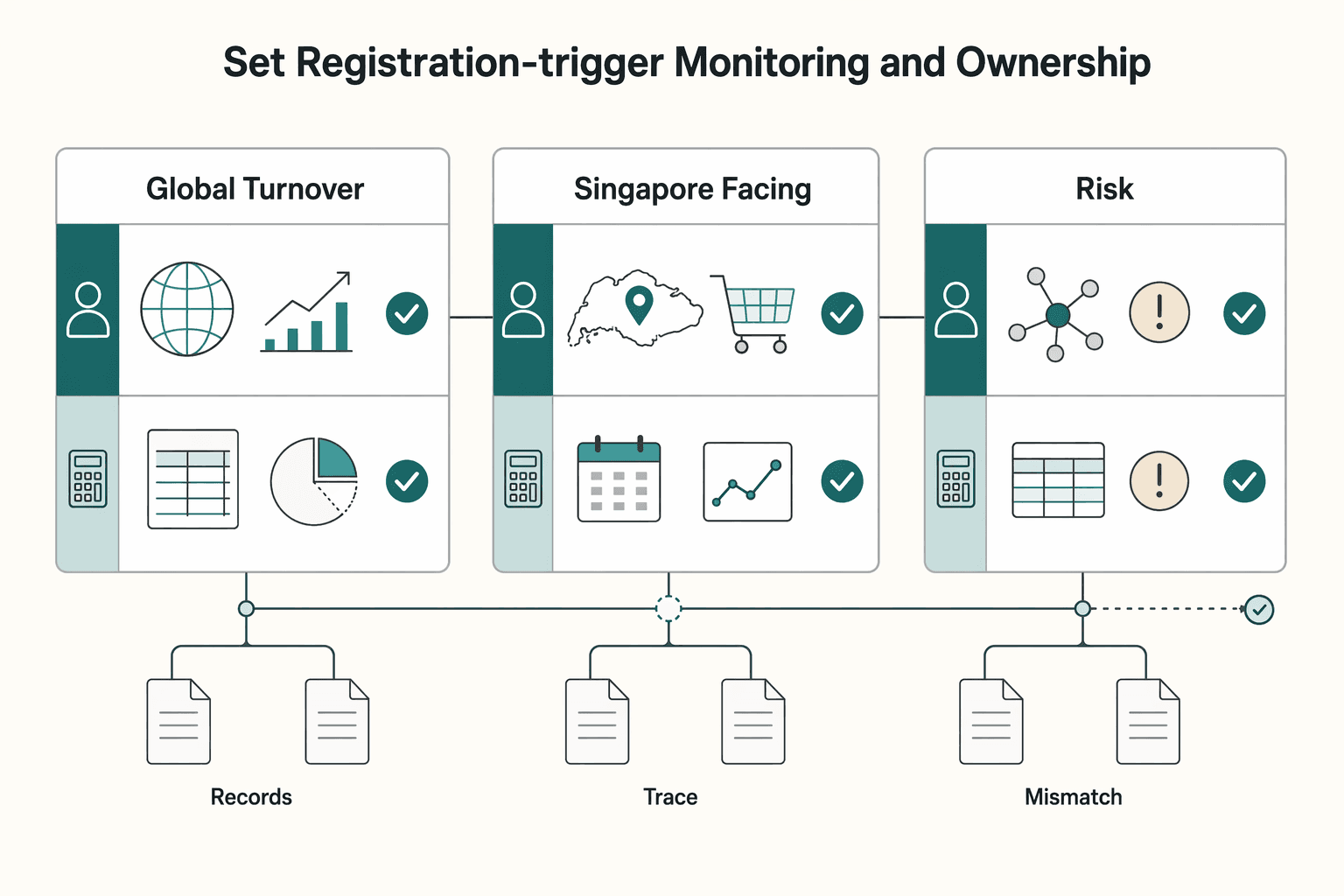

Set registration-trigger monitoring and ownership#

Once classification is in place, assign registration-trigger monitoring to both Tax and Finance. Tax should own scope decisions for relevant Singapore B2C supplies. Finance should own data completeness, close timing, and forecast tracking. A shared monitoring table is enough if it runs on a fixed cadence and ties back to source records.

| Monitoring item | What you are testing | Primary owner | Verification checkpoint | Escalation trigger |

|---|---|---|---|---|

| Global turnover test | The revenue base your internal policy uses to monitor potential overseas registration triggers | Finance, reviewed by Tax | Reconcile extracts to the ledger close and document exclusions | Unexplained variance, new product line, or policy gap |

| Singapore-facing B2C supplies test | Only transactions already classified as relevant Singapore B2C supplies | Tax, supported by Finance data | Tie totals back to the classification map and customer-status evidence | Ambiguous customer status, missing location evidence, or supplier-role uncertainty |

| Forecast breach risk | Whether run rate or pipeline may cross a trigger before the next close | Finance, with Tax sign-off | Maintain a dated forecast note with assumptions and sign-off | Likely trigger crossing before period close |

Tie the table to records, not manual cleanup#

For internal monitoring, use regular extracts from billing, order, or ledger systems, and route exceptions to review before finalizing the table. The key control is whether the extracted transactions match the classification map and whether unresolved rows are clearly excluded pending review. Require Tax and Finance sign-off after exceptions are resolved or explicitly parked.

Keep monitoring aligned to cited OVR scope changes#

Monitor against the cited scope changes, not legacy logic. Singapore implemented the OVR regime on 1 January 2020, and from 1 January 2023 the cited scope expanded so digital and non-digital B2C imported remote services are subject to GST. If your control logic still keys only to "digital services," your tested base may be too narrow.

| Date | Noted change or source |

|---|---|

| 1 January 2020 | OVR applied to B2C digital services to customers in Singapore |

| 1 January 2023 | OVR extended to B2C non-digital remote services and imported B2C low-value goods (LVG) |

| 30 July 2021 | Cited IRAS e-Tax guide published |

IRAS guidance should anchor interpretation. The cited IRAS e-Tax guide was published on 30 July 2021, but your team should confirm current IRAS positions before relying on older internal rules.

Treat the simplified pay-only regime as contingent#

If you model a simplified pay-only path, treat it as a planning scenario until eligibility is confirmed against current IRAS guidance. Confirm the eligibility tests with IRAS before you operationalize that path, and keep a dated IRAS-reference record and an internal decision note. If forecasts indicate a likely trigger crossing, start registration readiness immediately instead of waiting for period close.

Related: Brazil Digital Services Tax: CIDE and ISS Obligations for Platform Operators.

Build GST charging and invoicing controls that survive audit#

If registration exposure looks likely, make GST charging and invoicing controls deterministic now rather than relying on manual fixes later. When a GST-registered overseas supplier is in scope, checkout, invoice, and ledger should all produce the same GST outcome from the same transaction facts. The same applies when an electronic marketplace operator is treated as supplier under the Overseas Vendor Registration (OVR) regime.

The core control is the transaction decision key: who the supplier is, whether the customer is B2C or B2B, and what evidence supports the Singapore treatment. Once registered, overseas suppliers must charge and account for GST on relevant B2C supplies to Singapore, so supplier-role logic has to live in system records, not in offline notes.

Make charging logic depend on role and flow#

Channel is not the rule. Transaction role and flow are. Selling through an online channel does not by itself change GST treatment.

| Flow | Charging control | Record that must persist to invoice and ledger |

|---|---|---|

| B2C remote services supplied by an overseas supplier | Charge GST when the flow is in scope and you are registered | Supplier entity, customer-status result, service classification, tax amount |

| B2C supply through a marketplace where the operator is treated as supplier | Apply operator supplier logic, not seller default logic | Marketplace supplier-role flag, seller reference, customer-status result, tax amount |

| Goods flow | Separate local Singapore delivery, qualifying export, and outside-Singapore to outside-Singapore flows | Delivery path, goods classification (including low-value goods (LVG) where relevant), tax treatment, export-document reference where applicable |

For goods, keep the split explicit. Local delivery in Singapore should be standard-rated and GST charged. Outside-Singapore to outside-Singapore is out of scope. Exports can be zero-rated at 0% GST only when the required export documents are retained.

Require data that explains the result#

Your checkout and invoice records should preserve the data your team relied on for customer status and supply treatment. As a practical minimum, retain the legal supplier, customer-status outcome, location or delivery facts used, product or service classification, applied tax treatment, and tax amount posted to the ledger.

If a transaction is treated as B2B, retain the status evidence that supports that outcome. For B2B imports, certain GST-registered recipients may need to account for GST on imported services and LVG under reverse charge, so unsupported B2B treatment should be routed to review instead of defaulted.

Call out failure modes early#

Build explicit checks for these failure modes into release and close routines:

| Failure mode | Article signal |

|---|---|

| Treating sales channel (for example, online) as if it changes taxability by itself | Channel is not the rule. Transaction role and flow are. |

| Misclassifying customer status (B2C vs B2B) without supportable status evidence | Treat the B2C/B2B split as an evidence-based routing decision. |

| Missing supplier-role mapping where a marketplace operator may be treated as supplier | Supplier status is the field most likely to break the analysis. |

| Applying 0% export treatment without retaining the required export documents | Exports can be zero-rated at 0% GST only when the required export documents are retained. |

At close, reconcile charged GST to invoice totals and ledger postings, and investigate exceptions.

For marketplace reporting obligations across jurisdictions, see Digital Platform Reporting for Online Marketplaces: MRDP, DAC7, and UK HMRC Duties.

Keep the B2C and B2B boundary clean#

Treat the B2C/B2B split as an evidence-based routing decision, not just a customer label. In practice, each transaction should route to your internal treatment path, for example OVR-related, reverse-charge-related, or a review queue, based on what you can support at transaction time.

If your policy treats B2C and B2B scenarios differently, treat that as a controlled internal rule, then validate it against current official guidance rather than assumptions borrowed from other markets.

A useful control is to test the same service under two customer records:

- one record has only a free-text business name and weak status evidence

- one record has verifiable business details, a matched legal entity and invoice party, and reliable status evidence

Those transactions may share the same product code, but they should not be auto-classified the same way.

Use a strict gate: if customer status evidence is uncertain at transaction time, hold for review instead of defaulting to B2B. Keep the review pack dated and simple: declaration used, status-check result, legal entity name, invoice party, reviewer, and final treatment decision.

Finally, refresh policy on a recurring cadence. Singapore appears in current digitalized-economy indirect tax tracking, and those updates are produced monthly, so routing logic should be rechecked regularly.

For borderline B2C vs B2B cases, use a repeatable triage step before booking tax treatment, then sanity-check edge scenarios with the VAT reverse-charge checker.

Maintain an evidence pack regulators and auditors can follow#

Freeze the decision evidence at transaction time so another reviewer can reconstruct why a transaction was routed to a specific GST treatment or manual review. Treat this as an internal control standard.

Keep a minimum pack for every decision type#

| Evidence item | What to retain | Why it matters |

|---|---|---|

| Transaction classification output | Final treatment result, transaction ID, date, legal entity, product or service type, and whether it was routed to the selected GST treatment or review | Shows the decision that was actually applied |

| Customer-status evidence | Customer declaration used, business details collected, status-check result, invoice party, and timestamp | Supports the status call made at transaction time |

| Supplier-role rationale | Contracting party, invoicing entity, checkout terms, and a short rationale for who was treated as supplier in your process | Preserves the reasoning behind supplier treatment |

| Policy approval log | Policy version, approver, effective date, and scope of change | Shows which internal rule was in force when the decision was made |

A practical check is this: six months later, the file should still show the facts, the rule applied, who approved it, and any exception from the default rule.

Anchor each rule to a real source of truth#

Anchor rules to named IRAS guidance and the specific condition the rule is meant to apply. For edge cases, keep a dated decision memo with the fact pattern, chosen interpretation, approver, and next review date.

Where the transaction record alone is not enough, keep written reasoning. An outcome without a rationale is a control gap.

Add operating evidence, not just policy evidence#

Keep proof that controls actually operated in finance and operations, not just policy text:

- reconciliation files showing GST charged, invoice totals, and ledger postings for the review period

- exception-resolution records for ambiguous customer status or post-close corrections

- change logs for tax-rule updates, including effective date, owner, and what data or product mapping changed

Date-stamp each exception closure and link it to the policy version used so retired logic is not reused.

If a Singapore entity later claims input tax on local costs, the same pack should support that claim. IRAS conditions include being GST-registered, ensuring goods or services were supplied to or imported by the claimant and used for business purposes, and holding valid tax invoices or simplified tax invoices addressed to the claimant at claim time. Verify supplier GST registration details with the GST Registered Business Search, and claim in the accounting period tied to the invoice or import permit date.

Also check invoice-content failure points. For purchases above S$1,000, missing "tax invoice," customer name, or GST amount is an invalid-invoice scenario. For purchases at or below S$1,000, missing the GST amount or a statement that the price includes GST is also a failure mode.

Handle timeline and rate uncertainty without freezing execution#

Treat timeline and rate checks as recurring controls, not a one-time setup. The secondary materials here are explicitly time-bound, so they can support monitoring but not fixed assumptions in billing logic.

A practical freshness check from the excerpts:

| Source signal | What it tells you |

|---|---|

Date Written: April 15, 2025; Posted: 5 May 2025; Last revised: 12 May 2025 | This is dated context, not evergreen operational authority. |

updated as of February 2025, but there may have been regulatory changes since. | The publisher warns the summary may be stale. |

Every three years survey cadence across 18 different APAC markets | Broad regional surveys can lag market-specific changes. |

Use that as a governance rule: validate Singapore-specific rate and effective-date assumptions on a recurring schedule, and re-check before pricing, checkout, or invoicing-rule changes.

Keep a lightweight Tax/Legal change log so stale assumptions do not leak into production:

- rule area affected, for example tax scope, customer type, or marketplace treatment

- source checked, including any

last revisedorupdated as ofmarker - decision taken, effective date applied, owner, and linked approval or ticket

Escalate instead of guessing where the excerpts are incomplete: the exact "under certain conditions" test for marketplace deemed-supplier status, filing mechanics, and penalty specifics. If the source is not current and Singapore-specific, mark the rule provisional and route it for primary-law confirmation.

Execute in 30 60 90 days without overbuilding#

Use this 30 60 90 structure as an internal control plan: build enough to classify, monitor, charge, and defend decisions without automating unresolved judgments.

| Phase | Focus | Key actions |

|---|---|---|

| Days 1 to 30 | Visibility and ownership | Map transaction lanes; capture product or service as sold, customer type captured at checkout, invoicing entity and any seller-of-record field, likely supplier status, and evidence available now; assign owners across Legal, Tax, Finance, and Ops |

| Days 31 to 60 | Exposure monitoring for possible OVR risk | Review on a fixed cadence; keep treatments provisional where legal points remain open; create short evidence-pack templates; test exception handling on ambiguous supplier-status cases; label source quality explicitly |

| Days 61 to 90 | Dry-cycle close and reconciliation | Reconcile GST charged, invoice and checkout outputs, and ledger totals for the same period; investigate first if they do not tie; document unresolved items and escalation outcomes |

Days 1 to 30#

Start with visibility. Map transaction lanes using your current internal product and channel labels, and flag where OVR exposure may exist. Focus on visibility and ownership, not final legal conclusions drawn from secondary material.

For each lane, capture in one working table:

- product or service as sold

- customer type captured at checkout

- invoicing entity and any seller-of-record field

- likely supplier status, including unresolved marketplace-role treatment

- evidence available now, for example contract terms, checkout terms, billing records, customer-status data

Assign owners across Legal, Tax, Finance, and Ops so classification, monitoring, invoice outputs, and escalation do not fragment.

Days 31 to 60#

Once the map is in place, stand up exposure monitoring for possible OVR risk and review it on a fixed cadence. Where legal points remain open, keep treatments provisional and escalate rather than hardcoding uncertain rules.

Create short evidence-pack templates for each reviewed lane, including:

- classification output

- customer-status evidence available at transaction time

- supplier-role rationale

- dated source note

- approval or escalation record

Test exception handling on ambiguous supplier-status cases before scaling.

Also label source quality explicitly. Some materials in the excerpt set are not Singapore GST operational guidance, for example an old SEC filing artifact and academic program content, and one excerpt states that database inclusion does not imply endorsement. If those appear in decision records without clear labeling, your evidence position weakens.

Days 61 to 90#

Before you add more automation, run a dry-cycle close and reconcile for the same period:

- GST charged for transactions your team currently treats as in scope

- invoice and checkout outputs shown to customers

- ledger totals posted to Finance

If those do not tie, investigate first. Document unresolved items and escalation outcomes with owner, interim treatment, and date raised.

Pick the operating mode that matches risk#

Pick the operating mode that matches your actual risk profile. If volume is low and legal uncertainty is high, prioritize defensible manual review with tight exception handling and a documented hold path.

If volume is high, prioritize automation for clear cases and strict exception queues for anything below your evidence standard.

Close the cycle with a simple checkpoint: mapped, monitored, charged correctly, evidenced, and escalated where uncertain.

Conclusion#

For overseas platform operators, the sequence is simple: classify transactions correctly, monitor OVR exposure early, and only then scale automation.

Under Singapore GST, those classification calls drive everything downstream. Keep remote services and low-value goods separate, including LVG with a value not exceeding S$400 at point of sale, and keep B2C supplies to non-GST registered persons separate from B2B imports to GST-registered persons. In this IRAS framework, OVR applies to relevant B2C supplies and reverse charge applies to certain B2B imports.

Monitor registration exposure before it becomes urgent. In the IRAS framework here, the OVR test for overseas businesses includes annual global turnover exceeding S$1 million and B2C supplies to customers in Singapore exceeding S$100,000 annually. If you operate an electronic marketplace, include the value of relevant B2C supplies made through your marketplace when testing GST registration liability.

Once registered, the requirement becomes operational: charge and account for GST on in-scope B2C supplies to Singapore, and align invoicing and reconciliation workflows with that treatment. Reconcile charged GST and invoice totals against the same transaction population used for classification.

Where rules are explicit, standardize. Where guidance is conditional or incomplete, document assumptions and escalate quickly, especially for deemed-supplier exposure for electronic marketplace operators. If supplier role, customer GST status, or remote services versus LVG classification is not evidenced, route the case to exception review instead of forcing automation.

- Run a Singapore transaction-mapping table this week across all lanes, covering supplier role, customer status, product type, and required evidence.

- Assign named owners across Tax, Finance, Legal, and Ops for threshold monitoring, exception handling, and change control against current IRAS guidance.

- Validate unresolved legal points, especially marketplace deemed-supplier conditions and unclear B2B versus B2C facts, with Singapore-qualified tax counsel.

Related reading: DAC7 for Platform Operators: Scope, Seller Data, and Controls for EU and Non-EU Platforms.

If you want to operationalize this framework with policy gates, traceable records, and payout workflows where supported, talk to Gruv.

Frequently Asked Questions

Is Singapore digital service tax separate from Goods and Services Tax?

Based on the provided IRAS and secondary materials, these rules are framed within Singapore GST, including the OVR regime for imported B2C digital and non-digital services, rather than as a separate standalone digital services tax.

When does an overseas platform operator need to register under the OVR regime?

Registration is conditional, not automatic for every overseas platform operator. The supported position is that overseas vendors and electronic marketplace operators are required to register, charge, and account for GST if certain conditions are met. Use IRAS Annex B, "Determining whether the OVR regime applies to you," to test your facts.

Can an electronic marketplace operator be treated as the supplier for GST purposes?

Yes, OVR can apply to marketplace operators supplying remote services and low-value goods on behalf of suppliers or merchants. The full deemed-supplier tests should be confirmed with IRAS, so ambiguous cases should be escalated.

What counts as remote services versus low-value goods in Singapore GST rules?

IRAS treats remote services as a defined category, and that scope includes digital services. Low-value goods are a separate goods category with IRAS criteria at point of sale, including a value cap tied to the GST import relief threshold of S$400. Keep service and goods logic separate when classifying transactions.

How should teams handle B2C supplies versus B2B imports and reverse charge decisions?

Start by determining customer status. IRAS defines B2C as supplies to a non-GST registered person. The imported-remote-services guide includes a reverse-charge section, but the detailed B2B eligibility tests should be confirmed with IRAS, so unclear cases should be escalated instead of auto-classified.

What should a compliance team do first if key legal tests are still unclear?

Treat unresolved legal judgments as provisional and route them to manual review. Prioritize checks on supplier role and customer status, then validate against the latest IRAS material, especially Annex B and Annex C for straddling cases around 1 January 2023.

What evidence should we retain to defend GST treatment decisions during audit?

Retain records that support your classification, customer-status determination, supplier-role determination, and escalation decisions. IRAS also explicitly links zero-rating to keeping required export evidence. Do not rely on one guide alone, since IRAS states it is not intended to comprehensively address all possible tax issues.

Do the key dates matter for classification?

Yes, especially for historical and straddling transactions. The provided materials point to 1 January 2020 for imported B2C digital services, 1 January 2023 for imported B2C non-digital services and LVG, and 9% from 1 January 2024 in the newer secondary source. Date-stamp your treatment logic so you can defend why a rule was applied.

What is the quickest red flag that your treatment may be wrong?

A practical red flag is when you cannot clearly evidence supplier role, customer GST-registration status, and whether the supply is remote services or LVG. If those checks are not evidenced, route the case to exception handling instead of automation.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- curriculum.law.georgetown.edu/llm/llm-llm-programs/llm-general-individualizedtrusted

- govinfo.gov/content/pkg/CPRT-105JPRT46400/html/CPRT-105J...trusted

- iras.gov.sg/taxes/goods-services-tax-(gst)/gst-and-digit...trusted

- iras.gov.sg/media/docs/default-source/e-tax/gst-e-tax-gu...trusted

- oecd.org/content/dam/oecd/en/networks/global-forum-ta...trusted

- oecd.org/content/dam/oecd/en/publications/reports/200...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC7129073trusted

- sec.gov/Archives/edgar/data/1046126/0000950123050044...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Canadian GST/HST Registration for Platform Operators in the Digital Economy

If your platform touches Canadian customers, start by deciding whether Canada's digital-economy GST/HST measures may apply to each transaction flow. This is an operational question with real consequences. An affected business or platform operator may need to register for a GST/HST account and charge, collect, and remit tax under CRA-administered Excise Tax Act (ETA) rules.

Brazil Platform Operator Tax Controls for CIDE, ISS, and CBS/IBS Transition

You can make defensible tax decisions in Brazil now without pretending every open question is settled. Focus on confirmed CBS/IBS transition obligations, keep legacy taxes active during the overlap, and treat CIDE-related platform exposure as a monitored uncertainty that should be escalated, not guessed.

Making Tax Digital for Income Tax and UK Platform Operators: Confirmed Rules and Open Scope Questions

For platform operators, the first useful move is to separate confirmed HMRC and GOV.UK statements from scope assumptions. Most public guidance on Making Tax Digital for Income Tax is written for sole traders, landlords, and their agents, not for platform operators as a distinct audience.