Quick Answer

Map each recurring B2C flow to Union, Non-Union, IOSS, or escalation before go-live. For platform operators using OSS after the 1 July 2021 changes, the direct win is one filing portal in a Member State of identification, but only for supplies that belong in the chosen scheme. Keep quarterly calendars for Union and Non-Union, monthly for import, and treat domestic VAT returns as a separate track with its own reconciliation.

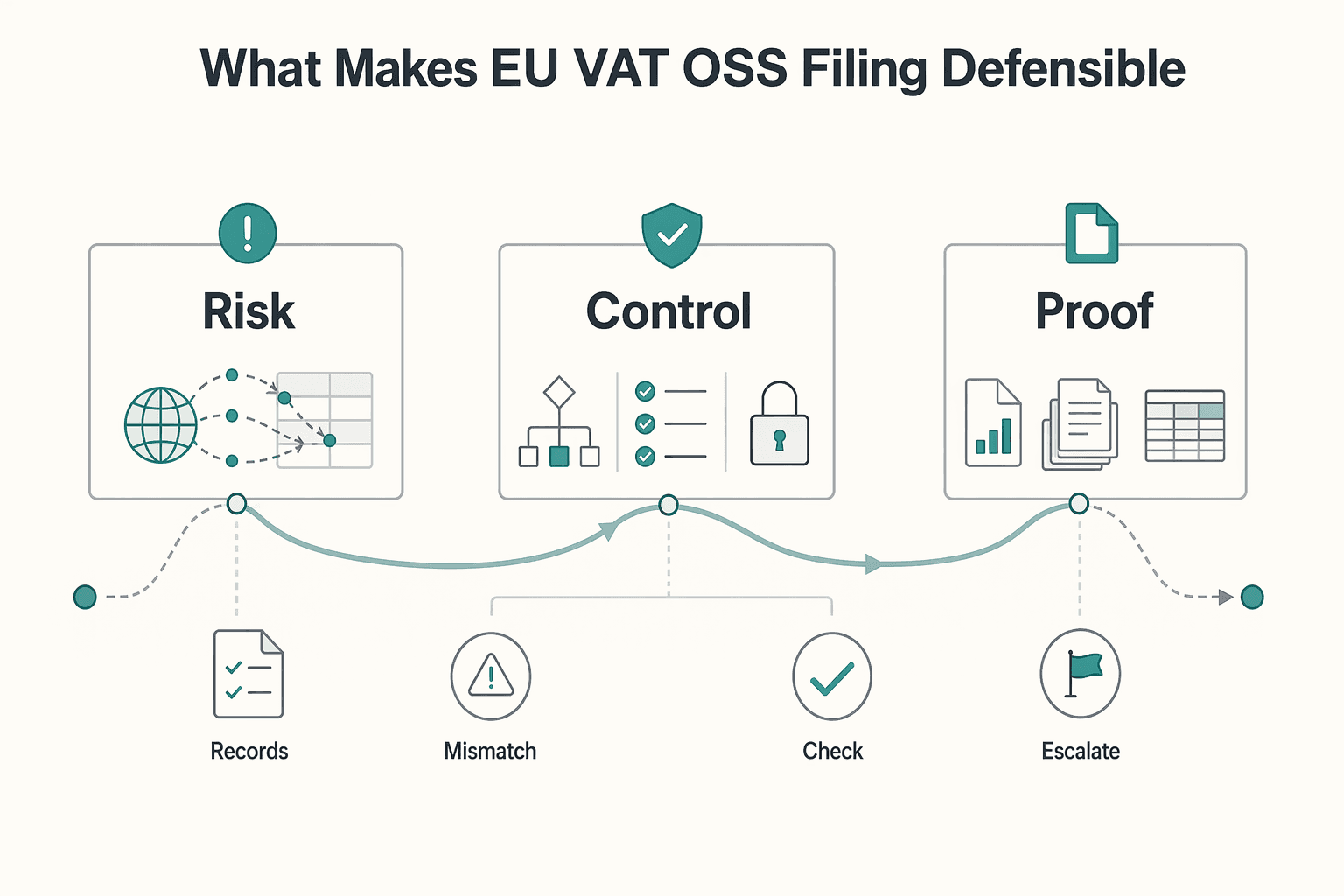

What makes EU VAT OSS filing defensible#

One Stop Shop (OSS) can simplify EU VAT filing for eligible transactions because you register in one Member State of identification and file the relevant OSS return there. That benefit depends on three things: transaction classification, scheme selection, and audit-ready records.

For compliance, legal, finance, and risk teams, the hard part is operational. Cross-border platform activity can look commercially similar but fall into different VAT treatments. Since 1 July 2021, that analysis has had to move into day-to-day execution, not just a year-end tax exercise.

OSS is not one bucket. The framework has three special schemes: Union, non-Union, and import. IOSS is the import track for distance sales of low-value imported goods not exceeding 150€. Union and non-Union returns are quarterly. Import returns are monthly.

Scope also needs to be set correctly early. OSS returns are additional and do not replace domestic VAT returns. If you choose an OSS scheme, supplies that fall under that scheme must be declared through that scheme's OSS return. Using one OSS portal does not remove the need to decide which supplies belong inside the scheme and which obligations remain outside it.

For platform operators, an early mistake is treating a cross-border payment flow as automatic OSS scope. Marketplace deemed-supplier treatment applies only in certain circumstances, and platforms can still have record-keeping obligations even when they are not deemed suppliers. Before you automate anything, confirm that each transaction ties to a specific VAT treatment with a documented rationale.

This article follows that sequence: key terms, scheme mapping, ownership and controls, filing execution, and evidence retention. Where classification remains unclear, escalate quickly and document the decision, including advance-ruling routes for complex cross-border VAT questions where appropriate.

For a step-by-step walkthrough, see How Platform Teams Accelerate MTD for UK VAT Without Control Gaps.

Start With the Terms That Drive Filing Decisions#

Get the label right first, because it drives the filing logic. EU VAT One Stop Shop (OSS) is the broader framework with three special schemes: Union, non-Union, and import. The import scheme is a separate track with a different filing cadence. Union and non-Union returns are quarterly, while import returns are monthly. If you collapse all cross-border consumer activity into one bucket, you can build the wrong reporting cycle from day one.

| Label | What the article says | Cadence/date note |

|---|---|---|

| OSS | Broader framework with three special schemes: Union, non-Union, and import | Union and non-Union returns are quarterly; import returns are monthly |

| Union scheme | One of the OSS schemes | Quarterly return |

| Non-Union scheme | One of the OSS schemes | Quarterly return |

| Import scheme (IOSS) | Track for distance sales of low-value imported goods not exceeding 150€ | Monthly return |

| MOSS | Legacy label for historical mapping only | Started 1 January 2015; extended into OSS from 1 July 2021 |

Keep scope decisions narrow at intake. Since 1 July 2021, the changes here focus on cross-border B2C e-commerce activities and distance sales of goods. Do not assume every transaction belongs in OSS by default. If you opt to use a scheme, declare all supplies that fall under that scheme through that scheme's OSS return. Where classification is unclear, hold and escalate rather than forcing a transaction into an OSS return.

Treat MOSS as a legacy label, not a current operating model. MOSS started on 1 January 2015 and was extended into OSS from 1 July 2021. Keep "MOSS" for historical mapping only, and relabel active controls to OSS scheme names so teams are working against the current filing framework.

For a deeper dive, read A guide to the 'One-Stop-Shop' (OSS) for VAT in the EU.

Map Each Transaction Flow to the Correct Scheme#

Map each recurring cross-border B2C flow to exactly one path: Union scheme, Non-Union scheme, Import One Stop Shop (IOSS), or paused for escalation before first filing. If a flow cannot be tied clearly to one scheme, keep it out of production filing logic until you resolve it.

Scheme mapping should follow the transaction and legal facts, not checkout labels or channel language. OSS schemes are optional, but if you use a scheme, you must declare all supplies that fall under that scheme in that scheme's OSS return. Filing cadence is scheme-specific: quarterly for Union and Non-Union, and monthly for import.

Use this table as a first scheme-routing check, not a complete eligibility matrix for every transaction type.

| Operational flow | First scheme path to test | Filing cadence | Minimum checkpoint before go-live |

|---|---|---|---|

| Flow already confirmed to fall under Union scheme | Union scheme | Quarterly | Mapping logic and return extraction both point to Union |

| Flow from a taxable person with no EU business or fixed establishment (with Non-Union conditions confirmed) | Non-Union scheme | Quarterly | One filing country is set |

| Imported B2C flow already confirmed as import-scheme eligible | IOSS | Monthly | Import flow is tagged separately from quarterly OSS traffic |

| Mixed, unclear, or conflicting flow | No scheme yet | None until resolved | Escalate before first filing |

Keep edge flows explicit#

Mixed goods and services, imported low-value consignments, and TBE services are common error points. Flag them as separate review paths. Use those flags to force a scheme decision or escalation, not to auto-assign treatment from partial signals such as shipping metadata alone.

For TBE services and intra-EU distance sales of goods, keep the EUR 10 000 EU-wide threshold visible in your review logic. A generic "digital" bucket makes later threshold and scheme checks harder to defend.

Separate channel labels from VAT outcome#

Channel labels help operations, but they are not the VAT conclusion. Online marketplaces and platforms facilitating supplies of goods can, in certain circumstances, be deemed to have received and supplied the goods themselves. Keep marketplace-facilitated flows distinct from direct seller flows so that analysis stays tied to the actual VAT outcome.

Escalate unresolved flows with scheme-specific evidence#

Set a hard rule: if you cannot clearly tie a flow to one scheme, pause automation before first filing. For Non-Union, confirm the filing country and, where applicable, the allocated individual VAT identification number format (EUxxxyyyyyz) before you enable filing logic.

Where treatment remains complex across borders, consider a VAT Cross-border Ruling request in the participating EU country where the taxable person is VAT-registered.

Related: The IRS 10-Return E-File Rule: What Platform Operators Must Change Before Filing Season.

Treat Deemed Supplier Status as a Risk Trigger#

For online marketplaces, treat deemed supplier status as a go-live risk trigger. It can change who is treated as making the supply for VAT purposes and shift VAT collection and reporting responsibilities. The Commission's baseline wording is narrow: platforms facilitating supplies of goods are, "in certain circumstances," deemed to have received and supplied the goods themselves. Use that standard, not product labels, as your decision point.

Why this fork matters#

If deemed supplier treatment is wrong, filing scope can be wrong with it. Where OSS is used, VAT is declared through the Member State of identification and transmitted to the relevant Member States of consumption. OSS returns are additional and do not replace regular domestic VAT returns. That makes the operational question twofold: scheme selection and party liability for in-scope supplies.

If you use an OSS scheme, all supplies that fall under that scheme must be declared in that scheme's OSS return. A deemed-supplier misclassification can therefore affect the full in-scope population, not just a few isolated lines.

Minimum checkpoint before go-live#

These roles are not prescribed by Commission text, but they are a practical minimum before automation goes live. Require one shared transaction map signed by all three owners:

- Legal interpretation owner: confirms whether the platform's actual role could create deemed supplier treatment for the goods flow.

- Tax sign-off owner: confirms reporting treatment, including which supplies enter OSS and which party is treated as responsible.

- Evidence owner: maintains the supporting records and can reproduce them for review.

Evidence and escalation#

Do not assume record-keeping duties disappear when a platform is not treated as a deemed supplier. Record-keeping requirements can still apply to facilitating platforms. Keep the legal and tax interpretation with the flow-routing evidence so the conclusion is defensible.

If cross-border treatment remains unclear, pause go-live and escalate. For complex cases, a VAT Cross Border Ruling (CBR) can be requested in the participating EU country where the taxable person is VAT-registered. Use the published Commission wording rather than relying on unattributed commentary.

Choose Your Filing Country and Registration Path Early#

Pick your filing country early and treat OSS registration as an implementation step, not a formality. OSS schemes are optional, but if you use OSS, you register in one single Member State and use that country's OSS portal. You declare and pay VAT due in Member States where you are generally not established.

Start with the legal rule, then use operational fit when there is a true choice#

For the Union scheme, the Member State of identification is generally where the taxable person has established its business. For the Non-Union scheme, an eligible taxable person can choose any Member State as its filing country. Start there. Sometimes the rule determines the country, and sometimes you have a real choice.

| Scenario | Filing-country rule | Note |

|---|---|---|

| Union scheme | Member State of identification is generally where the taxable person has established its business | Start with the legal rule |

| Non-Union scheme | An eligible taxable person can choose any Member State as its filing country | The filing country allocates an individual VAT identification number in the format EUxxxyyyyyz |

| Choice among multiple fixed establishments | If one country is chosen, that choice is binding | Current calendar year plus the two following calendar years |

Where you do have a choice, use operational fit to break ties: language, support process, and who can reliably access and run the portal day to day. That is not a legal test, but it is a practical control.

If you are choosing among multiple fixed establishments, treat that decision as sticky. The choice is binding for the current calendar year plus the two following calendar years.

Know what one registration does, and what it does not do#

OSS lets you declare and pay VAT due in other Member States through the web portal of your filing country. Return and payment data are then transmitted to Member States of consumption.

It does not replace domestic VAT returns. OSS returns are additional.

For the Non-Union scheme, the filing country allocates an individual VAT identification number in the format EUxxxyyyyyz. That number is limited to supplies declared under the Non-Union scheme.

Verify the registration path before the first return opens#

Before the first filing period, run one checkpoint and store the evidence with your scheme memo and transaction map. If any of these checks fail, pause and fix it before the first return window opens:

- Registration confirmation: confirm registration is active in the intended scheme and retain the confirmation and identifier.

- User access controls: verify who can log in, prepare data, and submit in the relevant portal.

- Calendar ownership: assign a named owner for filing and payment deadlines. Union and Non-Union returns are quarterly, and the import scheme is monthly.

Related reading: IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

Build VAT Classification and Rate Controls Before Filing Day#

Once registration is done, classification quality becomes a major OSS risk. Each transaction should land in the right Member State of consumption, with a VAT result your team can explain later. If you use a specific OSS scheme, all supplies that fall under that scheme must be declared through that scheme's OSS return. Classification gaps can become filing errors.

Put country and rate logic in one control table#

Use one shared control table for country and rate determination so tax decisions are visible before return preparation. Keep it in one place that finance, tax, and product can all review.

| Control element | What to store | What finance should check |

|---|---|---|

| Customer country signal | Country used for VAT determination, evidence source, capture timestamp | Signal exists, is plausible, and matches transaction facts |

| Rate source | Tax logic version or rule set used for the Member State of consumption | Applied version matches transaction date and supply type |

| Override rules | Reason code, impacted transactions, who changed outcome, when | Manual changes are limited, approved, and traceable |

| Approval trail | Reviewer, approval date, supporting memo/ticket | Material rule changes have clear ownership and support |

This table should let you answer one review question quickly: why was this transaction taxed in this country at this rate on that day?

Define the minimum data set before return prep#

Set an internal minimum that supports grouping, reconciliation, and explanation across Member States of consumption. Capture and retain at least:

- internal transaction ID

- transaction date

- supply type

- B2C flag

- scheme tag used for filing, for example Union or import where relevant

- Member State of consumption

- customer country signal and evidence reference

- taxable amount

- VAT rate applied

- VAT amount

- manual override flag and approver reference

- correction or cancellation reference when treatment changes

Keep OSS-scope flows separate from domestic VAT populations. OSS returns are additional and do not replace domestic VAT returns.

Make incomplete or conflicting country evidence an internal stop condition#

If country evidence is missing or conflicting, use an internal control to stop final tax determination until you resolve it. Do not let unresolved records flow into automated return population.

Before period close, run an exception report for:

- missing country signal

- conflicting country signals

- manual overrides without supporting record

Assign a named owner. Require resolution, documented deferral, or exclusion before draft OSS return sign-off.

Expect three failure modes#

Three failure modes are worth checking. First, wrong country mapping can happen when one signal is used even though stronger evidence points elsewhere. Test for this with sample review before the first filing cycle and again after major checkout or product-flow changes.

Another is stale tax logic. OSS in its expanded form applies from 1 July 2021, but your rule set can drift away from current operations as product scope or transaction flows change.

The third is mixed B2C treatment. Similar flows get split between in-scope and out-of-scope handling across teams. If you use a specific OSS scheme, supplies under that scheme must be declared in that scheme's return, so completeness checks matter just as much as rate checks.

Keep the evidence trail finance can defend#

Each filing period should leave three defensible artifacts, kept together in the file:

- audit logs for country and rate logic changes, including who changed what and when

- reconciliation outputs from transaction totals to return totals by Member State of consumption

- change history explaining why rules changed, who approved them, and which periods were affected

This matters because OSS returns and VAT paid are transmitted by the Member State of identification to Member States of consumption through a secure communications network. Your team should be able to recreate the path from transaction to return line without relying on memory.

Also keep detailed records even where a platform is not a deemed supplier, because record-keeping obligations can still apply. If treatment is genuinely unclear, escalate early and consider whether a VAT Cross-border Ruling is appropriate before filing on weak support.

If you are turning this control table into production workflows, review Gruv's integration patterns for traceable events, retries, and operational status handling in the developer docs.

Run a Predictable Filing Calendar Across OSS and IOSS#

Run OSS and the import scheme on a defined control calendar, not as ad hoc deadline work. Union and non-Union OSS returns are quarterly, and the import scheme is monthly. Once you use a scheme, you must declare all supplies that fall under that scheme in that scheme's OSS return, so period close should start with scope completeness.

Fix the order of operations before the first live cycle#

Set the sequence before the first live cycle and keep it stable:

- Close and freeze the in-scope transaction population for each scheme.

- Confirm scheme allocation across Union, non-Union, and import flows.

- Aggregate by Member State of consumption and prepare the electronic return.

- Reconcile draft return totals back to the frozen transaction set.

- Submit and pay through the Member State of identification, then retain filing and payment evidence.

This order matters because returns and payments submitted in the Member State of identification are transmitted to Member States of consumption through a secure communications network. Keep domestic VAT filing on its own track, since OSS returns are additional and do not replace domestic VAT returns.

Separate cadence and ownership by scheme#

Keep monthly and quarterly work separate so it does not blur into one queue. Assign clear accountability by filing rhythm. A practical model is preparer, reviewer, and submitter roles per cycle, with named backups.

| Scheme | Return frequency | Ownership focus |

|---|---|---|

| Union scheme | Quarterly | Complete inclusion of in-scope supplies and Member-State aggregation |

| Non-Union scheme | Quarterly | Complete inclusion of supplies that fall under that scheme |

| Import scheme | Monthly | Tighter close discipline and faster exception handling |

Make pre-submit evidence part of the filing package#

A mandatory tie-out or sign-off process is not prescribed here, so treat this as an internal control standard. Before submission, keep a reconciliation from transactions to return totals, an exceptions view that is either cleared or formally deferred, and approval evidence.

Store those records with the portal submission and payment confirmation so your team can reconstruct how the return was prepared and approved.

Give disputes their own lane#

Do not let complex corrections clog the normal filing queue. Route them through a separate exception lane with documented facts, ownership, and decision timing.

For genuinely complex cross-border VAT treatment, escalate early and consider requesting a VAT Cross-border Ruling in a participating EU country where you are registered for VAT.

We covered this in detail in How to Handle VAT on Platform Fees Across the EU: A Marketplace Operator's Guide.

Keep an Evidence Pack That Survives Audit Scrutiny#

If you cannot trace each filed figure back to the underlying transaction and decision path, your OSS process is unlikely to be audit-ready. For platform-facilitated sales, keep an evidence pack that reconstructs the transaction, the VAT logic, the scheme decision, and any later correction without relying on staff memory.

Official OSS materials cover records to be kept, invoices, and bad debt relief. They also note new record-keeping requirements for online marketplaces and platforms, including cases where they are not deemed suppliers. Your archive should support both the filed return and the commercial facts behind it.

Keep the transaction story, not just totals#

Build your filing file from transaction level up to the submitted OSS VAT return. Keep the source record for each in-scope sale, the country logic used, the VAT treatment selected, and the amount reported in the scheme return.

| Evidence layer | What to keep | Why it matters |

|---|---|---|

| Transaction record | Order or service ID, date, value, customer location data used, VAT charged, Member State of consumption | Traces each reported amount to an underlying supply |

| VAT decision record | Scheme classification (Union, non-Union, or import) and the rule applied | Shows why a transaction was reported in one route and not another |

| Change and correction history | Refunds, cancellations, bad debt adjustments, and reclassifications | Explains movement between original filing and later corrections |

| Filing support | Draft aggregation, reconciliation to source population, submitted return copy, and payment confirmation | Shows how totals were built and what was filed |

Use two checks every cycle: trace a filed line back to the included transactions, and trace a sampled transaction forward to either inclusion or a documented exclusion reason.

Separate scope evidence from filing evidence#

Keep scheme-scope reasoning separate from return assembly files. Preserve why a flow was treated as OSS in the first place, especially where platform involvement or deemed-supplier analysis affected the outcome.

This matters because filing happens in one portal country, while returns and VAT paid are transmitted to Member States of consumption through a secure communications network. If the process is reviewed later, you need to show both the numbers and the original scope decision. For unresolved complex cross-border VAT treatment questions, consider escalating through the VAT Cross-Border Rulings (CBR) path for an advance ruling.

Treat retention hygiene as an internal control standard#

The material provided does not set a specific immutable-timestamp rule or access-control design. Use those as internal control choices, not as stated legal requirements.

For each OSS VAT return, keep one final submission package, preserve a dated export of the underlying dataset, limit post-sign-off edits, and maintain clear correction history. This helps prevent silent overwrites and confusion between OSS returns and separate domestic VAT returns.

Include external shipping/import evidence when treatment depends on it#

When shipment or import facts drive VAT treatment, keep the operational records you relied on from postal operators, couriers, or related customs touchpoints. The official material places these parties in the affected e-commerce chain, so platform-only records can be insufficient for some treatments.

Keep the records that explain the treatment used, especially for import flows and low-value consignments under the import scheme scope for goods not exceeding 150€. If external evidence conflicts with internal order data, route it to the exception lane before the next filing cycle. For the full breakdown, read How Platform Operators Accept Payments Through QuickBooks.

Escalate Early When Signals Conflict#

Use the evidence pack to escalate as soon as a flow supports more than one VAT treatment. If the facts do not point clearly to a single route, pause automation and resolve it before filing or correcting anything.

| Conflict | What the article says | Immediate step |

|---|---|---|

| Deemed supplier signals do not line up | Contract flow and platform behavior point in different directions | Freeze classification and document the conflict in the file |

| Union and Non-Union scheme logic both seem plausible | This article does not provide a definitive tie-breaker for overlap cases | Escalate before registration |

| Import treatment starts drifting | A cadence mismatch is a practical warning sign: Union and non-Union returns are quarterly, while import returns are monthly | Escalate and assess whether a VAT Cross-border Ruling request is appropriate if unresolved internally |

When deemed supplier signals do not line up#

Escalate immediately when deemed supplier analysis is unclear because contract flow and platform behavior point in different directions. Online marketplaces and platforms can be treated as deemed suppliers in certain cases, but exact legal criteria for every fact pattern are not provided here, so conflicting signals should trigger tax and legal review.

Use one checkpoint for the same sample transaction: contract flow, customer journey, invoice presentation, and payment flow. If those items do not align, freeze classification and document the conflict in the file.

When Union and Non-Union scheme logic both seem plausible#

If a flow appears to fit both the Union and Non-Union schemes, escalate before registration. The OSS framework is split into non-Union, Union, and import schemes, and a definitive tie-breaker for overlap cases is not provided here.

For the Union scheme, the Member State of identification is where the business is established. If multiple fixed establishments exist and one country is chosen, that choice binds the current calendar year plus the next two calendar years.

When import treatment starts drifting#

Escalate when the same import flow is treated differently across countries or teams, including IOSS-related handling. A cadence mismatch is a practical warning sign: Union and non-Union returns are quarterly, while import returns are monthly.

For complex cross-border questions that remain unresolved internally, assess whether a VAT Cross-border Ruling request is appropriate in a participating EU country where you are VAT-registered. Submit it under that country's national VAT ruling conditions.

Know What OSS Simplifies and What It Does Not#

Once classification conflicts are resolved, set expectations clearly. One Stop Shop (OSS) simplifies filing mechanics, not VAT interpretation. It can centralize how you declare and pay VAT due in Member States, but it does not remove interpretation risk.

The scope is specific. OSS covers three schemes, non-Union, Union, and import, and participation is optional. If you choose a scheme, you must report all supplies that fall under that scheme through that OSS return.

The key tradeoff is straightforward: OSS returns are additional and do not replace your regular domestic VAT return. One portal does not mean all local obligations disappear.

Before go-live, run a simple tie-out:

- Confirm your filing country.

- Confirm which flows are inside OSS and which are outside.

- Reconcile one sample period from source transactions to both the OSS return and the domestic return.

- Keep records and invoices ready for audit, including cases where platform record-keeping obligations apply even if the platform is not a deemed supplier.

Treat simplification claims carefully. EU materials mention a potential red-tape reduction of up to 95%, but that is not a guaranteed result for every operator. Accept claims only when they are backed by reconciled returns and your actual filing obligations. Also plan for failure modes: OSS is optional, and a taxpayer or intermediary can leave or be excluded by the Member State of identification.

Turn One Portal Into Auditable Operations#

One portal works best when VAT treatment is settled before filing. Keep the sequence fixed: classify flows, map each flow to the correct OSS scheme, assign owners, run filing controls, and escalate unclear cases before submission.

OSS is optional, but scheme use is all-in for in-scope supplies. Once you use a scheme, you must report all supplies that fall under it in that scheme's return. Treat Union, non-Union, and import as tax-scope decisions, not convenience settings, to avoid reconciling mismatched channel labels, location evidence, and VAT treatment after filing.

Start with registration controls in your Member State of identification. Confirm registration is complete in the single Member State where you file, confirm portal access ownership, and confirm filing-calendar ownership. For non-Union registration, verify issued identification details, including EUxxxyyyyyz where applicable, and use that ID only for supplies declared under the non-Union scheme.

Then set ownership by filing cadence. Union and non-Union returns are quarterly, and import returns are monthly. Name clear owners for classification, return preparation, review and approval, and submission evidence so exceptions are resolved before filing, not after.

Do not treat OSS output as the whole VAT picture. OSS returns are additional and do not replace domestic VAT returns, so reconciliations need to show what was reported through OSS and what remained outside it.

Keep an evidence pack that lets another reviewer trace transaction facts, VAT treatment, registration confirmation, overrides or corrections, and submission records. Maintain that standard even when you conclude you are not a deemed supplier, because record-keeping duties can still apply to platforms.

Escalate early when signals conflict. If contract flow, platform behavior, and VAT mapping do not align, or establishment facts leave scheme choice unclear, pause automation and document a decision path. For complex cross-border treatment questions, evaluate a VAT Cross-border Ruling where national conditions allow.

Before the next filing cycle, run a short gap check on your OSS and import-scheme process:

- Which flows are still classified by commercial label instead of tax facts?

- Is Member State of identification setup verified, including access, registration confirmation, and scheme-specific ID controls?

- Do quarterly and monthly returns each have named preparer, reviewer, and submitter owners?

- Which unresolved classification questions require counsel or advance-ruling analysis before filing?

For Gruv's audience, the practical outcome is straightforward: this sequence can reduce filing surprises, support cleaner tax and finance reconciliations, and keep compliance decisions easier to defend under audit.

Before the next filing cycle, pressure-test your flow ownership, evidence trail, and exception handling with Gruv to confirm fit by market and program in a short implementation scoping call.

Frequently Asked Questions

What does EU VAT One Stop Shop actually simplify for platform operators?

It simplifies how you declare and pay VAT due in Member States where you are generally not established. You register in one Member State of identification and file through the relevant OSS scheme for in-scope supplies. OSS does not replace correct scheme mapping, and OSS returns are additional to your regular domestic VAT return.

When should a platform use OSS instead of Import One Stop Shop?

Use the scheme that matches the supply facts, not the label your team prefers. The import scheme is one of the three OSS schemes, and its return is monthly, while Union and non-Union returns are quarterly. If your facts do not clearly support scheme mapping, pause automation and resolve it before filing.

How do Union scheme and Non-Union scheme choices affect filing ownership?

They determine where filing is managed and which supplies must be reported once you opt in. If you use a scheme, you must declare all supplies that fall under that scheme through its OSS return. For non-Union registration, confirm the issued identification details, including the EUxxxyyyyyz format where applicable.

What changes operationally when destination-based VAT applies in Member States of consumption?

Your process needs records that support where VAT was declared and why. In practice, your filing data should consistently support the Member State where VAT was reported. If destination evidence is incomplete or conflicting, treat that as a filing risk to resolve before submission.

What records should platforms keep to satisfy OSS audit expectations?

There is no complete OSS record checklist to work from, but record-keeping obligations do apply. Keep enough transaction and filing records to support what you declared through OSS and regular VAT returns. For marketplace models, remember that record-keeping duties can still apply even when the platform is not a deemed supplier.

Does OSS remove the need for all local VAT registrations?

No. OSS can simplify part of cross-border VAT filing, but it does not remove all local VAT obligations. Treat “one portal means no local obligations” as a control failure until you test it against your actual flows.

When should a platform escalate deemed supplier questions to specialist counsel?

Escalate when contractual flow, platform behavior, and transaction mapping do not point to the same VAT treatment. Escalate also when your filing-country choice is made under a Union-scheme fixed-establishment scenario, because that choice can bind you for the decision year plus two following calendar years. For complex cross-border treatment questions, consider requesting a VAT Cross-border Ruling in a participating EU country where you are VAT-registered.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

When OSS VAT Applies and When Reverse Charge Handles EU Work

The mention of EU VAT can trigger invoicing anxiety, even for experienced international professionals. That reaction makes sense. The rules look dense, the acronyms pile up, and nobody wants a payment delayed over a tax setup issue.

The IRS 10-Return E-File Rule: What Platform Operators Must Change Before Filing Season

If you file **10 or more information returns**, the IRS requires electronic filing starting in **tax year 2023**. For many platform payout programs, that shifts filing from an admin task to a control decision.

How Platform Operators Choose Cross-Border Payout Rails by Corridor

The hard part is not choosing one "best" rail. It is choosing the right rail for each corridor and payout type, where cost, speed, access, and transparency pull in different directions. For any route, the practical question is simple: for this country pair, payout size, and recipient experience, which path gives you acceptable delivery, controllable cost, and audit-ready evidence?