Quick Answer

Starting in tax year 2023, if you file 10 or more information returns, you must file electronically. For platform operators, that means centralizing the return count, separating W-2 and W-2C filing through SSA BSO from other information returns filed through IRIS, securing an IRIS TCC if needed, and planning correction handling and evidence retention before filing season.

If you file 10 or more information returns, the IRS requires electronic filing starting in tax year 2023#

If you file 10 or more information returns, the IRS requires electronic filing starting in tax year 2023. For many platform payout programs, that shifts filing from an admin task to a control decision.

The practical question is not just how to send forms. It is which filing path you can defend if submissions, corrections, or timing are later questioned. The goal here is simple: help you choose the lightest setup that still gives you reliable execution and records you can stand behind.

The channel split is the first thing to get right. Many information returns now run through Information Returns Intake System (IRIS). It has two intake paths: the free web-based IRIS Taxpayer Portal and software-based IRIS Application to Application (A2A). Forms W-2 and W-2C still file through the Social Security Administration's Business Services Online (BSO), not IRIS, so you cannot treat ownership as one unified process.

Before filing season, confirm a few basics:

- If you plan to use the IRIS Taxpayer Portal, obtain an IRIS TCC first, the required 5-digit business identifier.

- Assign clear ownership for monitoring IRIS status during filing windows.

- Evaluate filing paths based on original submissions, IRIS-supported corrections, and automatic extensions, not just first-pass throughput.

If your plan still leans on FIRE for the long term, treat that as a migration risk now. The IRS targets tax year 2026 / filing season 2027 for FIRE retirement, so your operating model should still work as filing moves off FIRE.

The sections that follow rank the main options, spell out the tradeoffs, and give decision checkpoints for tax, compliance, finance, and operations owners.

You might also find this useful: Beneficial Ownership Verification: How Platforms Comply with FinCEN UBO Rules.

Selection criteria and who this list helps#

Use this list if you own reporting outcomes across teams and need a filing decision you can defend for Form W-2 and other information returns.

The standard is practical: choose the lightest path that still lets you prove two things at the entity level:

- how you determined whether e-filing was required

- how corrections will be handled once filing starts

This is written for the operator who has to reconcile tax, compliance, finance, and operations. Starting in tax year 2023, the IRS states that if you file 10 or more returns, e-filing is required. That includes Forms W-2 filed with the Social Security Administration. The split matters. W-2/W-2C go through Business Services Online (BSO), while other eligible information returns can be filed through IRIS.

Do not treat this section as legal advice for edge-case interpretations. The IRS points to T.D. 9972 for electronic filing requirements. If your issue turns on an exception or a disputed reading, escalate to counsel and, where needed, the IRS.

Rank options using these criteria:

- Control over threshold aggregation logic.

- Audit-trail quality, including retained filing-status records.

- Correction handling, including post-filing workflows.

- Dependency risk on vendors or fragile upload flows.

- Readiness friction around setup and access, including choosing an e-file option before applying for a TCC, obtaining the IRIS 5-digit TCC, and completing BSO registration for W-2/W-2C.

IRIS supports original filings, corrections, and automatic extensions, and it supports keeping records of completed, filed, and distributed forms. Keep one rule in mind for the rest of this list: if a path cannot show entity-level proof of threshold calculations and a clean correction trail for your electronic filing obligations, it is too thin even if it looks easier up front.

For a step-by-step walkthrough, see How to File a GST Return as an Indian Freelancer.

What the rule changes for platform operators#

The operational change is less about file format and more about control design. Before filing starts, you need one counting decision, clear channel ownership, and a plan for corrections.

- Centralize the count, even if filing is split

The IRS states that at 10 or more returns, e-filing is required. If tax, payroll, and ops teams count separately, you create room for inconsistent filing decisions. Use one documented owner for the filing count and keep the supporting records.

- Plan corrections in the channel that supports the form family

Do not leave corrections as a post-filing promise. IRIS supports corrections and automatic extensions for information returns, which matters for corrected information-return workflows. W-2C remains an SSA Business Services Online (BSO) process, so one shared correction queue may not be enough across payroll and nonpayroll reporting.

- Treat the channel split as a control requirement

IRIS has two intake paths, Taxpayer Portal and A2A, while W-2/W-2C routing is through SSA BSO. Keep separate access, ownership, and evidence procedures for IRIS and BSO. Before filing season, confirm your IRIS 5-digit TCC and check IRIS system status before you submit.

- Keep Form 940 and Form 941 separate from information-return workflows

Form 940 and Form 941 are in the 94x employment tax family and are received through Modernized e-File (MeF), not IRIS. Make that separation explicit in policy documents so routing and ownership do not get blurred.

For a deeper dive, read FTC Click-to-Cancel Rule: What Subscription Platforms Must Build Before the Deadline.

Build counting controls before choosing software#

Start with an owned count before you choose tools. Once you reach 10 or more returns, e-filing is required, and software will not rescue a weak counting decision.

| Control step | Grounded detail | Record to keep |

|---|---|---|

| Define counting boundary | Document who owns the return count and which families are in scope, including W-2/W-2C, multiple 1099 forms, and Form 1042-S | Owned count documented before vendor setup |

| Reconcile split workflows | If work is split across teams or providers, keep one internal aggregation record before submission so everyone uses the same totals and channel plan | One approved aggregation record across BSO and IRIS paths |

| Set a planning checkpoint | If the forecast is near 10 or more returns, decide the IRIS path early; choose the e-file option, then apply for a TCC | Forecast and channel-planning checkpoint |

| Plan for corrections and rejects | Publication 5718 calls out 6.1 Corrections Process, 6.2 Rejected Transmissions, and 6.3 Replacing an Original Transmission that Rejected | Dated count snapshots and a change log |

- Define your internal counting boundary first

Decide how your organization will track returns and who owns that number, then document it before vendor setup. Include the return families in scope (for example W-2/W-2C, multiple 1099 forms, and Form 1042-S) so channel decisions follow a known count rather than software defaults. Keep channel differences explicit: W-2/W-2C e-filing runs through SSA Business Services Online (BSO), while information returns can be filed through IRIS Taxpayer Portal or IRIS A2A.

- Reconcile split workflows into one approved record

If your filing work is split across teams or providers, keep one internal aggregation record before submission so everyone is working from the same totals and channel plan. The goal is one coherent filing decision across BSO and IRIS paths.

- Forecast early and set a planning checkpoint

Track counts during the year and set an internal checkpoint for channel planning. If the forecast is near 10 or more returns, decide the IRIS path early. IRS sequencing is straightforward: choose the e-file option, then apply for a Transmitter Control Code (TCC).

- Control for corrections and rejected transmissions

Build the process to handle post-submission changes, not just original filings. Publication 5718 calls out separate flows for 6.1 Corrections Process, 6.2 Rejected Transmissions, and 6.3 Replacing an Original Transmission that Rejected. Keep dated count snapshots and a change log so filing decisions remain traceable if counts change.

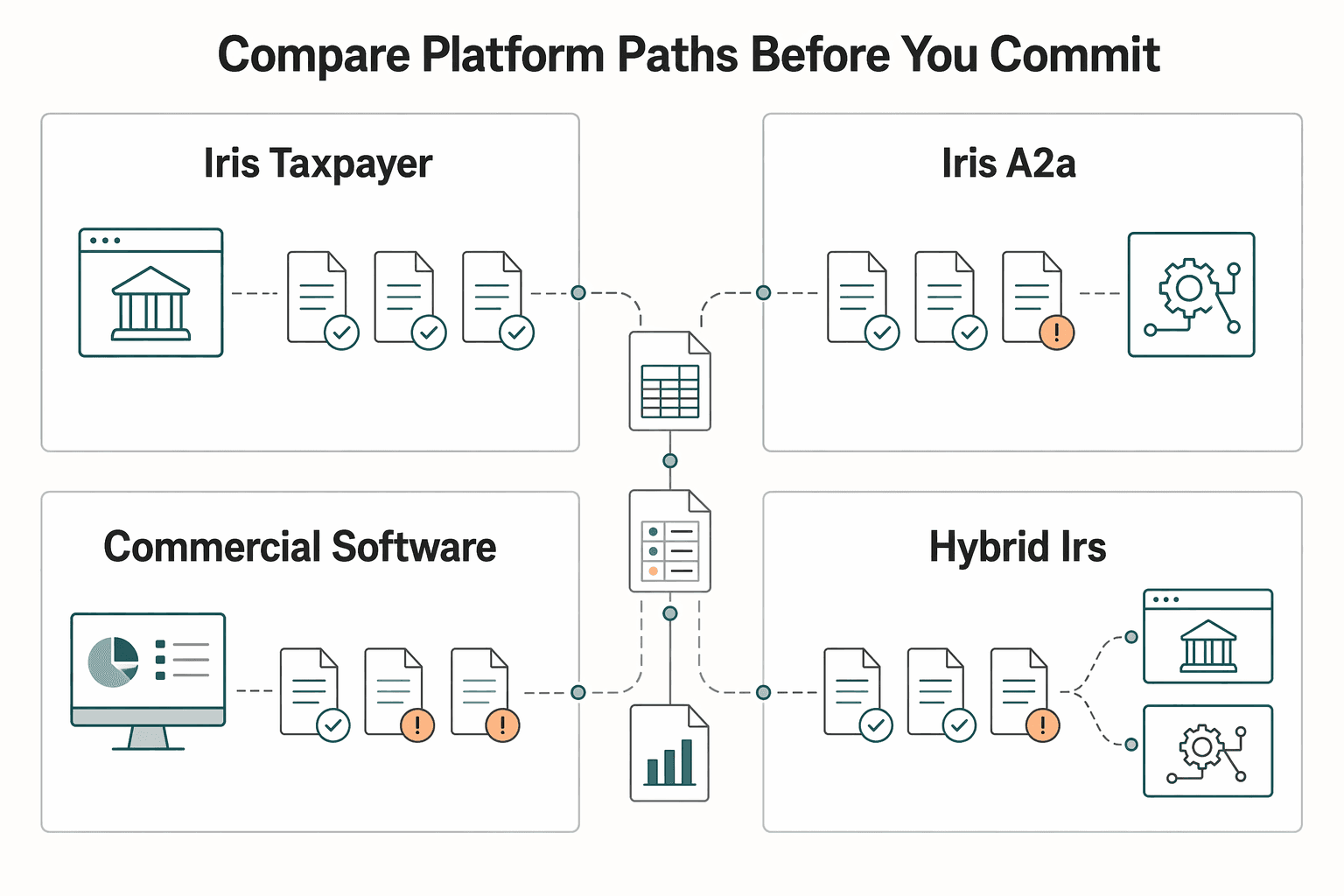

Compare platform paths before you commit#

If your control objective is system-to-system traceability and repeatable correction cycles, IRIS Application to Application (A2A) or a tightly governed hybrid are often a better fit. This choice is less about features and more about ownership, correction flow, and whether your evidence will still be clear months later.

Keep the channel boundary explicit. IRIS is for information returns through IRIS Taxpayer Portal and IRIS A2A, while Forms W-2/W-2C are filed through SSA Business Services Online (BSO).

| Path | Best for | Required credentials and setup (TCC, onboarding) | Correction handling | Dependency risk | Audit evidence quality | Channel split note |

|---|---|---|---|---|---|---|

| IRIS Taxpayer Portal | Lower-volume teams that want direct IRS filing with internal review | Portal access and an IRIS TCC. IRS describes this as a 5-digit code. Web entry or CSV upload, up to 100 returns at a time. | IRS states you can file corrections and request automatic extensions. Repeated correction cycles can become manual. | Lower vendor risk, higher person-and-process bottleneck risk | Strong when you retain CSV inputs, approvals, and IRS confirmations in one record | Information returns only. W-2/W-2C remain in SSA BSO |

| IRIS A2A | Teams that need software-based filing and repeatable machine workflows | Software onboarding plus clear ownership for submission and acknowledgement storage. Do not assume FIRE setup rules carry over. | Fits recurring corrections if you preserve original-to-correction linkage and acknowledgements | Higher engineering and release dependency than portal-only filing | Strong when source mappings, transmission logs, and acknowledgements are retained and retrievable | Still IRIS for information returns. Does not replace SSA BSO for W-2/W-2C |

| Commercial software | Teams that want a faster launch and packaged workflow UI | Setup varies. Confirm whether filing runs through IRIS Taxpayer Portal, IRIS A2A, or another layer, and whose transmitter profile is used. | Varies by vendor. Verify corrected-return and rejected-transmission handling before approval. | Vendor transparency and lock-in risk if filing logic is opaque | Acceptable only if acknowledgements, correction history, and user actions are exportable | Multi-form support can still require SSA BSO for W-2/W-2C |

| Hybrid (IRS channel + software assist) | Teams that want direct IRS control plus prep and QA support | Team owns IRS filing credentials and channel. Software assists preparation and validation. For portal use, confirm IRIS TCC and the correct tax-year CSV template. | Often a practical middle path when original-to-correction linkage is preserved | Medium. More moving parts than direct filing, less black-box risk than full outsourcing | Often strong when internal approvals and prepared files are paired with final IRS confirmations | Keep IRIS and SSA BSO evidence separate so information-return and W-2/W-2C records do not mix |

A FIRE-led roadmap should be a caution flag. IRS states IRIS will be the only intake system for information returns for filing season 2027, and lists tax year 2026 / filing season 2027 as the target for FIRE retirement.

Before approval, lock three items in one decision record: the exact channel by return family, credential and role ownership, including TCC where required, and the evidence standard for corrections, originals, acceptances, and rejections. For recurring filings, A2A or a governed hybrid is often a practical default. Use the portal when volume and reviewer controls can support its manual pace.

We covered this in more detail in When Platforms File 1099 for Foreign Contractors and When W-8 Applies.

If your decision hinges on system traceability and repeatable reconciliation, review Gruv's integration surfaces and operational patterns in the developer docs.

Best for low-volume direct filing with internal control#

Choose IRIS Taxpayer Portal when your volume is low enough to review each batch before filing and you do not need system-to-system throughput. For a lean team filing information returns for one entity, it can be a clean option. You file through a free IRS web channel and can avoid building an A2A integration.

Why this path works#

The main advantage is simplicity. IRS describes the portal as a free, web-based filing channel within IRIS. To use it, you need an IRIS Transmitter Control Code (TCC), which IRS describes as a 5-digit business identifier for e-filing.

The portal also has limits that fit lower-volume workflows. IRS states you can e-file up to 100 returns at a time. That can work for a single-entity cycle with CSV review and sign-off. As re-runs, recurring corrections, or multi-entity coordination increase, manual steps usually need tighter controls.

Where teams get the most value#

This path is strongest when the filing process is controlled and repeatable: one entity, manageable volume, and a documented QA step before submission. If you are below the 10 or more returns e-file trigger starting with tax year 2023, the portal can still be a sensible electronic default. If you are at or above that threshold, it can satisfy the electronic filing requirement without A2A build work.

IRS also states the portal lets you keep a record of completed, filed and distributed forms. Treat that as one checkpoint, not the full evidence set. Keep the source CSV, reviewer approval, submission confirmation, and acceptance or rejection outcomes together so the filing trail can be reconstructed later.

Tradeoffs to plan for#

Manual control is both the benefit and the risk. Reviewer checks can catch obvious issues before filing, but manual steps become more fragile during peak periods and repeated corrections.

CSV upload handling can be a friction point. IRS guidance notes refreshing and re-uploading if a file does not appear, so you need strict version control to avoid submitting an outdated file.

Decision rule and checkpoints#

Use the portal when these conditions are true and your team can keep the manual steps tight:

- You are filing information returns through IRIS for tax year 2022 and later, with clear owner and reviewer roles.

- Your batches stay within the 100-return upload limit and correction volume is expected to stay low.

- Your controls preserve a complete evidence chain from source file to IRS filing outcome.

Do not treat this as an all-forms channel. Forms W-2/W-2C are filed through SSA Business Services Online (BSO), not the IRIS information-return path.

This pairs well with our guide on When Platforms File 1099-K and 1099-NEC.

Best for high-volume systemized filing with engineering support#

Use an engineering-led filing model when volume and correction load are sustained, and tax ops plus engineering can jointly own requirements, validation, and evidence capture. IRIS Application to Application (A2A) is one path teams may evaluate, but channel-specific capabilities should be verified separately; control comes from the operating model, not the channel by itself.

When this path is worth it#

This path makes sense when multiple teams touch filing data and you need repeatable, auditable handoffs. If Form 1042-S is in scope, treat it as a first-class workstream from the start. IRS describes it as reporting income and amounts withheld, and the Form 1042-S page includes a 2023 electronic file requirement development entry dated 02-FEB-2024. Build shared validation and evidence standards first, then map each form family to its actual filing route.

What you need before engineering starts#

The real gate is a documented requirements pack, not code. At minimum, it should include:

- documented requirements for mappings, validations, correction handling, and acceptance criteria

- explicit requirements for data standards and compliance needs

- a test pack with known-good and known-bad records, including corrected-return scenarios

- an evidence specification for what is retained after submission, including source version, transformed output version, timestamps, and filing outcomes

If this package is not ready, the build is not ready.

The real tradeoff#

The upside can be more consistent policy enforcement before submission and a cleaner evidence trail after submission. The downside is delivery risk. Tax-technology programs can run into data, project-management, and leadership failure modes. Add an independent verification step, IV&V or equivalent, so automated errors do not become harder to detect than manual ones.

Decision rule#

Choose this path only when ownership is stable, requirements are documented early, and change control is realistic for filing season. Pass for now if tax ops and engineering cannot agree on requirements, correction ownership, or evidence retention before build work begins.

Need the full breakdown? Read Click-to-Cancel Subscription UX After the FTC Rule for Platforms.

Best for teams prioritizing speed and packaged features#

Choose packaged software when speed is the binding constraint, but keep filing policy and approval ownership in-house. For teams subject to the 10-or-more information return e-file rule, the real value is often faster execution on recurring filing cycles, not outsourced accountability.

Why this path makes sense#

IRS explicitly allows a software path through IRIS Application to Application (A2A), and says most information returns can be filed electronically through IRS systems. That can let you avoid building a full submission layer while reducing manual portal work.

This path is especially practical when manual operations become the bottleneck, including the IRIS Taxpayer Portal limit of up to 100 returns at a time. It can also reduce filing-season pressure when your team cannot absorb repetitive formatting and status tracking.

What to verify before you sign#

IRS sources confirm channels, prerequisites, and correction workflows. They do not confirm that a given commercial product includes TIN Matching, recipient delivery, or Backup Withholding handling. If those capabilities drive your decision, require explicit contractual language and clear post-filing record terms.

Before you sign, use this minimum verification pack and treat gaps as a control risk:

- filing-channel mapping by form family, including confirmation that supported information returns flow through IRIS A2A where applicable, and that Forms W-2/W-2C route through Business Services Online at SSA.gov rather than IRIS

- correction workflow detail, including how corrections are filed and how corrected records are documented in your process

- recordkeeping detail, including how your team will keep records of completed, filed, and distributed forms

- access prerequisites, including who owns IRIS TCC setup for IRIS Taxpayer Portal access

The tradeoff you are accepting#

Packaged tools can reduce setup time, but they can also reduce visibility into edge-case handling and correction lineage. Your team still needs defensible controls before submission and auditable records after submission.

Keep one internal sign-off on aggregation before filing. Starting with tax year 2023, the electronic filing trigger is 10 or more information returns, and that counting decision still belongs to you. If any process still depends on FIRE, plan migration now: IRS describes tax year 2026 / filing season 2027 as the targeted retirement window and indicates IRIS is planned as the only intake system for that season.

Best-fit use case#

This path fits a mid-sized platform with seasonal spikes that needs to get operational quickly without waiting for a full engineering build. Let the vendor handle interface and transmission while your team retains threshold counting, approval, and evidence retention.

Related: Taxes in Mexico for Expats Without Guesswork.

Best for mixed environments with legacy dependencies#

A mixed operating model can be useful when a legacy process is dependable and a digital process is still maturing. This can preserve continuity while you modernize, especially when checkpoints and owners are explicit.

For legal and compliance decisions, treat unofficial displays as reference material, not final authority. FederalRegister.gov states its Web 2.0 display is not an official legal edition and does not provide legal notice. Verify against the linked official govinfo.gov PDF before you finalize decisions.

The tradeoff is operational complexity. Running parallel paths can increase coordination overhead when responsibilities are unclear. Keep one accountable owner for final validation so transition speed does not weaken verification quality. This fits teams that need to preserve legacy strengths during transition and can enforce strict verification gates before relying on newer digital outputs.

Escalation points that should trigger counsel or executive review#

Escalate when an issue can change filing posture, required evidence, or your ability to hit fixed dates such as January 31 for Form 1099-K recipient copies.

- Disputed aggregation ownership across entities or vendors

Escalate immediately if return ownership disputes could move you above or below the 10 or more returns e-file threshold. If teams are relying on their own reading of T.D. 9972 to justify who owns the count, move it to counsel before filing decisions are finalized. In mixed operations, one team may file through IRIS Taxpayer Portal or IRIS Application to Application (A2A) while payroll files W-2/W-2C through Business Services Online (BSO). If no one owns the reconciled count across channels, your filing position may be difficult to defend. Require one written inventory by legal entity and form family showing who prepares, who transmits, and which channel is used.

- Any discussion of a waiver using Form 8508

Escalate as soon as waiver language appears. This section does not establish Form 8508 hardship criteria, evidentiary standards, or approval likelihood, so ops should not improvise the decision. Confirm whether the normal sequence was followed first: choose an e-file method, then apply for a Transmitter Control Code (TCC). If waiver talk starts because TCC, onboarding, or channel ownership slipped, counsel should review the full timeline. Include filing method, TCC status, blocked dependencies, and dated timeline evidence. For 1099-K, include calendar impact on January 31.

- A correction spike after submission

Escalate when corrections look patterned rather than isolated. Repeated W-2C or other corrected-return batches across entities or vendors can point to upstream control problems in source data, mapping, or review. You do not need a single numeric trigger to act. Recurring defects are enough for executive review. IRS processing and staffing strain can also increase downstream risk when correction cycles repeat. Compare corrected versus original filings by entity, form, and channel, then trace samples back to source records.

- Unresolved ambiguity on scope boundaries

If scope, filer ownership, or channel assignment is still unclear, do not file on unwritten assumptions. Document the assumptions and obtain written legal sign-off before execution. Keep the memo explicit: entities, forms, BSO/IRIS split, return count used for the 10 or more returns analysis, and the unresolved assumption. If your position depends on unofficial summaries or vendor interpretations of T.D. 9972, state that uncertainty directly and request confirmation of the authoritative basis.

Related reading: How to File a Defensible Final US Tax Return After Renouncing Citizenship.

Evidence package every platform team should produce#

Build one evidence package that shows why you filed the way you did, who approved it, and which channel handled each submission. Documentation can break down when TCC readiness is unclear, IRS and SSA evidence is mixed, or filed returns cannot be traced back to source records.

| Evidence item | Include | Purpose |

|---|---|---|

| Filing dossier | Whether filing volume reached the 10-or-more-return e-file requirement, approver names, selected e-file path, TCC status, submission confirmations, pre-transmission checks, and portal access controls | Shows why the filing path was chosen and keeps readiness steps explicit and dated |

| Per-return lineage file | Payer entity, internal payee identifier, source payout record or transaction group, field mapping, submitted values, and original-to-correction linkage | Lets a reviewer trace one filed return back to source data |

| Separate channel evidence | Separate IRIS and SSA/BSO submission logs, confirmations, access lists, and exception notes | Keeps information-return evidence separate from W-2/W-2C evidence |

| Reconciliation pack for Gruv-enabled programs | Ledger-based payout records and tax artifact exports mapped to submission evidence where supported | Helps a reviewer follow one chain from payee record to ledger entry to export artifact to submission evidence |

- Filing dossier

Keep one season-specific dossier for filing-readiness decisions, not just filed outputs. Include whether your filing volume reached the 10-or-more-return e-file requirement, approver names, selected e-file path, Transmitter Control Code (TCC) status, submission confirmations, pre-transmission data-verification checks, and portal access controls. Keep the readiness sequence explicit and dated: e-file option selected, then TCC application progress. If that sequence is missing, your filing position is harder to defend.

- Per-return lineage file

Keep return-level lineage for each in-scope information return (including applicable 1099 series forms and Form 1042-S) from source data to submitted output. Record the payer entity, internal payee identifier, source payout record or transaction group, field mapping, and submitted values. For corrections, link the corrected return to the original filing and show exactly what changed. The control goal is simple: pick one filed return and trace it back to source data without guesswork.

- Separate channel evidence

Keep IRIS evidence separate from SSA/BSO evidence in both folder structure and status logs. IRS systems handle most information returns, while W-2/W-2C filings route through BSO at SSA. Store separate submission logs, confirmations, access lists, and exception notes by channel. Clear routing labels prevent avoidable ambiguity during review.

- Reconciliation pack for Gruv-enabled programs

For Gruv-enabled workflows, map ledger-based payout records and tax artifact exports to filing evidence where supported. This is an operator control, not an IRS filing rule, and it improves audit and correction readiness. A reviewer should be able to follow one chain from payee record to ledger entry to export artifact to submission evidence. If that chain breaks, reconciliation becomes slow and fragile.

Conclusion#

The lightest defensible path is usually the right one, but only after you centralize the count, assign channel ownership, and decide how corrections and evidence will be handled. For low-volume direct filing, IRIS Taxpayer Portal can work well. For sustained volume and repeatable machine workflows, A2A or a governed hybrid is often stronger. If you use packaged software, keep threshold counting, approvals, and evidence retention in-house. Whatever path you choose, keep IRIS and SSA BSO evidence separate and make sure the model still works as filing moves off FIRE.

Frequently Asked Questions

What is the IRS 10-Return E-File Rule in one sentence?

Starting in tax year 2023, filers with 10 or more information returns must file electronically. The IRS also states this includes Forms W-2, even though W-2s are e-filed with the Social Security Administration.

Is the threshold calculated per form type or across all covered information returns?

The provided IRS excerpts do not give a per-form counting formula. They state "10 or more information returns" and explicitly include W-2 filings with SSA. If your program spans multiple form families, document your approach and get tax or legal review before filing.

If different vendors file different forms, does the filer still have to aggregate totals?

This guide does not answer that directly. Treat split-vendor filing as a legal and tax review point, not a safe assumption. Document your filing position and get sign-off before submissions begin.

Do corrected returns need to be filed electronically when originals were e-filed?

The materials here focus on the correction channel rather than a separate paper fallback. IRIS supports corrections for information returns, and W-2C remains an SSA Business Services Online process. Plan corrections in the channel that supports the form family and do not leave correction handling as a post-filing promise.

How should teams choose between IRIS Taxpayer Portal and IRIS Application to Application (A2A)?

Use the IRIS Taxpayer Portal when your volume is low enough to review each batch before filing, your batches stay within the 100-return upload limit, and correction volume is expected to stay low. Use IRIS Application to Application when you need software-based filing, repeatable machine workflows, recurring corrections, and clear ownership for submission and acknowledgement storage.

What should be set up first before filing season: counting controls, Transmitter Control Code (TCC), owner assignment, or software?

Start with counting controls and ownership. Build an owned count before you choose tools, assign clear ownership for monitoring filing status, decide the e-file option early, and then apply for a Transmitter Control Code where required.

Which issues are still ambiguous enough to require formal legal review before filing?

Formal legal review is warranted when aggregation ownership across entities or vendors is disputed, when an exception or disputed reading of T.D. 9972 affects the filing position, when waiver discussions using Form 8508 begin, or when scope boundaries, filer ownership, or channel assignment are still unclear. The same is true if your position depends on unofficial summaries or vendor interpretations rather than an authoritative basis.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: