Quick Answer

Start with scheme and export classification, then file in sequence: GSTR-1 followed by GSTR-3B. For zero-rated services, confirm IGST Section 2(6) and file LUT in Form GST RFD-11 before supply when using the no-IGST-upfront route. Reconcile purchase claims against GSTR-2B, keep nil filing in mind where required, and pause any item with unclear place-of-supply or ITC support until reviewed by a CA.

For any serious professional, time is the one asset you cannot replenish. Yet for many Indian freelancers working with global clients, GST turns into a recurring admin drain that eats hours and attention. Treating it like a bureaucratic chore is a mistake.

A better way to look at it is this: GST is a system you can set up, run, and control. With the right foundation, a disciplined monthly rhythm, and a clean filing process, compliance stops being a source of stress. It becomes part of how you show professionalism, maintain financial control, and make life easier for better clients.

Step 1: Build Your Bulletproof GST Foundation#

Set your GST foundation before you file anything. Decide your scheme, confirm your export classification, choose your filing cadence, and lock your record process. If any of those facts are unclear, pause and verify them first, because filing errors often start earlier as classification errors.

1. Decide in this order#

The sequence matters. A lot of return problems start earlier, when decisions are made out of order and patched later.

- Choose your scheme first.

- Verify whether your overseas services meet export-of-services conditions under IGST Section 2(6) (including recipient location, place of supply, foreign-exchange receipt, and distinct-person test).

- Choose filing cadence only after scheme and eligibility are clear.

- Configure records so your books produce portal-ready numbers.

Use a CA early if you have mixed domestic and export supplies, unclear place-of-supply treatment, or unusual client or entity relationships. Those are not issues to leave for filing week.

2. Choose your scheme first#

This is the first real fork in the road. For many freelancer setups, the regular scheme is the practical default because it supports standard GST treatment and the normal return flow. Composition is usually the exception, not the starting point.

Use the regular scheme when you need standard GST treatment and the normal return flow. Choose composition only if you clearly qualify and accept its constraints.

| Criteria | Regular scheme | Composition scheme |

|---|---|---|

| Eligibility fit | Fits when you need normal return filing (GSTR-1, GSTR-3B) | Fits only if you qualify under current composition rules |

| ITC impact | Stays in normal ITC chain | Section 10(4): no input tax credit |

| Compliance load | Regular return cycle, including nil filing where required | CMP-08 quarterly statement + GSTR-4 annual return |

| Cash-flow effect | Tax handled through normal filing/payment cycle | Section 10(4): cannot collect tax from recipient, so pricing and tax absorption change |

| Current threshold/rate pending official GST portal or tax-advisor verification | Verify latest notification before relying on any threshold or rate figure | Verify latest notification before opting in |

If you need to collect GST from clients or claim ITC, validate composition very carefully before opting in.

3. Default to monthly filing; use QRMP only when it clearly fits#

For many freelancers, monthly filing is the safer operating choice because it keeps reconciliation tight and limits quarter-end surprises. QRMP can work, but only when eligibility is clear and your process can still support monthly discipline.

| Checkpoint | Applies to | Guidance |

|---|---|---|

| GSTR-1 due date | Monthly filing | By the 11th of the succeeding month; nil filing still applies. |

| GSTR-3B due day | Monthly filing | By the 20th of the following month; subject to notification-based extensions. |

| QRMP eligibility | QRMP | Includes PAN-based annual turnover up to ₹5 crore and filing the last due GSTR-3B. |

| Quarterly GSTR-3B due dates | QRMP | 22nd or 24th, based on State or UT. |

| IFF deadline | QRMP | Shown as the 13th of the next month. |

| Threshold verification note | Before switching cadence | Another GST help page still shows a Rs. 1.5 crore quarterly GSTR-1 threshold; confirm current eligibility in your GST account and current notifications before switching cadence. |

In practice, monthly filing is the safer default. It keeps reconciliation tight and reduces quarter-end surprises. QRMP can work when eligibility is clear and your workflow can still support monthly payments plus quarterly returns.

- Monthly guidance shown on GST help pages: GSTR-1 by the 11th of the succeeding month; GSTR-3B by the 20th of the following month (subject to notification-based extensions).

- QRMP guidance: eligibility includes PAN-based annual turnover up to ₹5 crore and filing the last due GSTR-3B; quarterly GSTR-3B due dates are 22nd or 24th (state or UT based); IFF deadline shown is the 13th of the next month.

- Important verification point: another GST help page still shows a Rs. 1.5 crore quarterly GSTR-1 threshold. Confirm current eligibility in your GST account and current notifications before switching cadence.

GSTR-1 is also required even in nil-activity periods.

4. Use LUT/Bond only after export status is verified, then make records filing-ready#

Do not treat LUT as the first paperwork step. First confirm that the supply actually qualifies as an export and that your place-of-supply conclusion holds. Then choose the route.

For zero-rated supplies, two legal routes exist:

- Supply without IGST payment under LUT/Bond and claim refund of unutilized ITC.

- Supply with IGST payment and claim refund of tax paid.

If your supply qualifies as export, complete LUT/Bond before export when using the no-IGST-upfront route. If export status or place of supply is unclear, get CA review before deciding the route. If your case involves mixed domestic or export flows or uncertain place-of-supply treatment, review place of supply rules before filing.

Once that route is clear, make your records usable for filing without rework:

- Classify each invoice as domestic taxable, export under LUT/Bond, or export with IGST payment.

- Capture customer location, invoice number and date, taxable value, and tax treatment consistently.

- Maintain purchase records with GST details to reconcile ITC against GSTR-2B before GSTR-3B.

- Keep export evidence (invoice, contract or scope, and payment proof in convertible foreign exchange).

Before you move to Step 2, your books should already produce the outward-supply totals you plan to report in GSTR-1, and your purchase records should reconcile to GSTR-2B. Once that is true, the monthly process becomes much lighter. Related: Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?.

Step 2: Master Your Monthly Workflow (The 15-Minute System)#

Once your scheme and filing cadence are set, keep the operating rhythm simple. Capture GST details when each transaction happens, then run one monthly review block. That turns return prep into a review task, not a reconstruction exercise.

1. Send the invoice as soon as the work is billable#

The best time to get GST data right is when you raise the invoice. Treat each invoice as a GST record created at source, not something you will clean up later. Run this pre-send checklist every time:

- Include the invoice details needed for your records and reporting.

- Confirm customer location and tax treatment are consistent with the treatment you chose in Step 1.

- Apply your internal service category tag consistently.

- Run a quick validation: taxable value, currency, tax line, and internal category tag all match.

If you cannot immediately map the invoice into your outward-supply reporting totals, fix it before sending.

2. Capture ITC evidence when the expense happens#

With expenses, speed matters. Save the document as soon as the cost happens, note the business purpose, and record the GST amount shown, if any. That gives you a usable audit trail before details go missing. Use this decision rule:

| Action | When it fits | Note |

|---|---|---|

| Capture now | Proper tax document, clearly business use, GST amount visible | This gives you a usable audit trail before details go missing. |

| Flag for review | Mixed personal or business use, incomplete document, unclear supplier treatment, or uncertain ITC eligibility | Do not assume every expense automatically qualifies for ITC. |

| Ask a professional | Large, unusual, or recurring items where eligibility is not clear | Use this path where eligibility is not clear. |

Do not assume every expense automatically qualifies for ITC.

3. Ring-fence tax cash when payments arrive#

Cash discipline matters as much as filing discipline. Move the tax portion out of your operating balance when client money arrives, so return-period payments do not compete with regular spending. A simple default playbook helps:

- Set a standing reserve rule in your process notes only after the current GST rate is verified from official GST portal guidance or a tax advisor.

- Tag invoice types separately in your books so monthly reconciliation is easier.

- For mixed invoice types, keep separate labels in books and bank notes.

- If payments are delayed, keep the reserve rule intact and reforecast cash instead of reducing the buffer.

4. Run one monthly operating rhythm#

You do not need constant GST admin. You need one clean rhythm: event-triggered execution during the month, followed by one recurring review block.

| When | What you do |

|---|---|

| As work happens | Issue invoice, save expense evidence, reserve tax cash, and tag each transaction correctly. |

| Monthly review block | Reconcile sales, purchases, and tax-payment records; review classification; verify documents for items you plan to claim; prepare draft return totals. |

If treatment is unclear during review, verify it with your tax advisor or on the official GST portal before filing.

If you use QRMP and currently qualify under the ₹5 crore cap, keep this monthly rhythm anyway. Quarterly filing changes filing frequency, not the discipline needed to stay accurate.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2026. Keep your monthly GST workflow clean by issuing invoices in one consistent format from day one: Generate a freelancer invoice.

Step 3: Execute the 30-Minute Filing Process#

By the time you reach filing, most of the work should already be done. The goal is to file from verified records in the Returns Dashboard, not to diagnose problems after submission.

1. Run the pre-filing gate#

Before you file anything, stop at one gate and make sure every number is traceable. This is where you prevent avoidable amendments and client-side corrections. Confirm these four checks first:

- Your invoice data for the period is complete and correctly tagged.

- Your sales totals in books reconcile with the outward-supply totals you plan to report.

- ITC entries are supported and align with Form GSTR-2B (auto-drafted; generated on the 14th day of the succeeding month for monthly filers, and on the 14th day of the succeeding month of the quarter for quarterly filers).

- Exceptions are identified now, not deferred until after filing.

Pause if anything cannot be traced to underlying records (invoice, note, voucher, or related document). Typical blockers: incorrect unregistered-customer address details, place-of-supply mismatch, or incomplete documents for ITC support.

2. File GSTR-1 first#

File GSTR-1 first because it is your outward-supplies statement and sets the base for the rest of the filing cycle. Use current-period invoice data and include relevant amendments within the normal return flow.

| Return | Main purpose | Key inputs | Common error points | Output artifact | Filing window check |

|---|---|---|---|---|---|

| GSTR-1 | Report outward supplies | Current-period invoice data, amendment entries, customer details, supply classification | Incorrect unregistered-customer address details, place-of-supply errors, missing invoice-level reporting where applicable for certain inter-State B2C invoices above Rs. 2,50,000 | Filed return PDF, ARN | Current filing window pending official verification |

| GSTR-3B | Declare summary liability and discharge tax | Auto-populated values, GSTR-2B reference for ITC, payment details, Table 3.2 details where applicable | Relying on auto-population without checks, ITC claimed without support, negative values shown as zero in some tables, Table 3.2 place-of-supply-wise reporting mistakes | Filed signed form, ARN | Current filing window pending official verification |

Before you submit, verify current due-date guidance on the portal. Do not assume old dates still apply. Nil filing still applies for GSTR-1.

3. File GSTR-3B second#

Once GSTR-1 is filed, move to GSTR-3B from Services > Returns > Returns Dashboard. GSTR-3B is a simplified summary return with auto-populated values, including references from system-generated GSTR-2B. This is where your reconciliation work needs to hold up.

Use a simple check order: confirm liability, then confirm ITC, then confirm payment. For monthly filers, the stated due day is the 20th of the following month. For quarterly filers, the stated due day is the 22nd or 24th (state or UT based), and notifications may extend dates. Nil filing is mandatory for GSTR-3B as well.

4. Pause and resolve exceptions before submission#

If something does not match, stop there. Filing with a known mismatch usually creates more work later than resolving it now. Use this path:

| Issue | Action | Limit or note |

|---|---|---|

| Same tax period invoice record issue | Review whether GSTR-1A (optional) fits your correction | Use this path when the issue is in the same tax period. |

| Earlier period record issue | Amend through a subsequent GSTR-1 | Subject to legal time limits. |

| Missing client details, unclear place-of-supply, or uncertain ITC support | Hold the affected claim until resolved | Consult a CA when ITC eligibility is unclear, support documents are incomplete, or classification or place-of-supply treatment remains uncertain after your internal review. |

Consult a CA when ITC eligibility is unclear, support documents are incomplete, or classification or place-of-supply treatment remains uncertain after your internal review.

5. Close the audit trail after filing#

Do this immediately after submission, while the filing set is still complete and easy to trace. Save a complete evidence set for that period:

- filed GSTR-1 PDF

- signed GSTR-3B form

- ARN for each filing

Store it with a consistent period label (example: GST/2026-27/Month/Filed Returns) and keep linked support in the same label set: invoices, credit and debit notes, vouchers, and reconciliation working papers. If your records are electronic, retain edit and delete logs so evidence continuity is preserved for reconciliation or notice response.

We covered this in detail in How to File a GST LUT Without Rework.

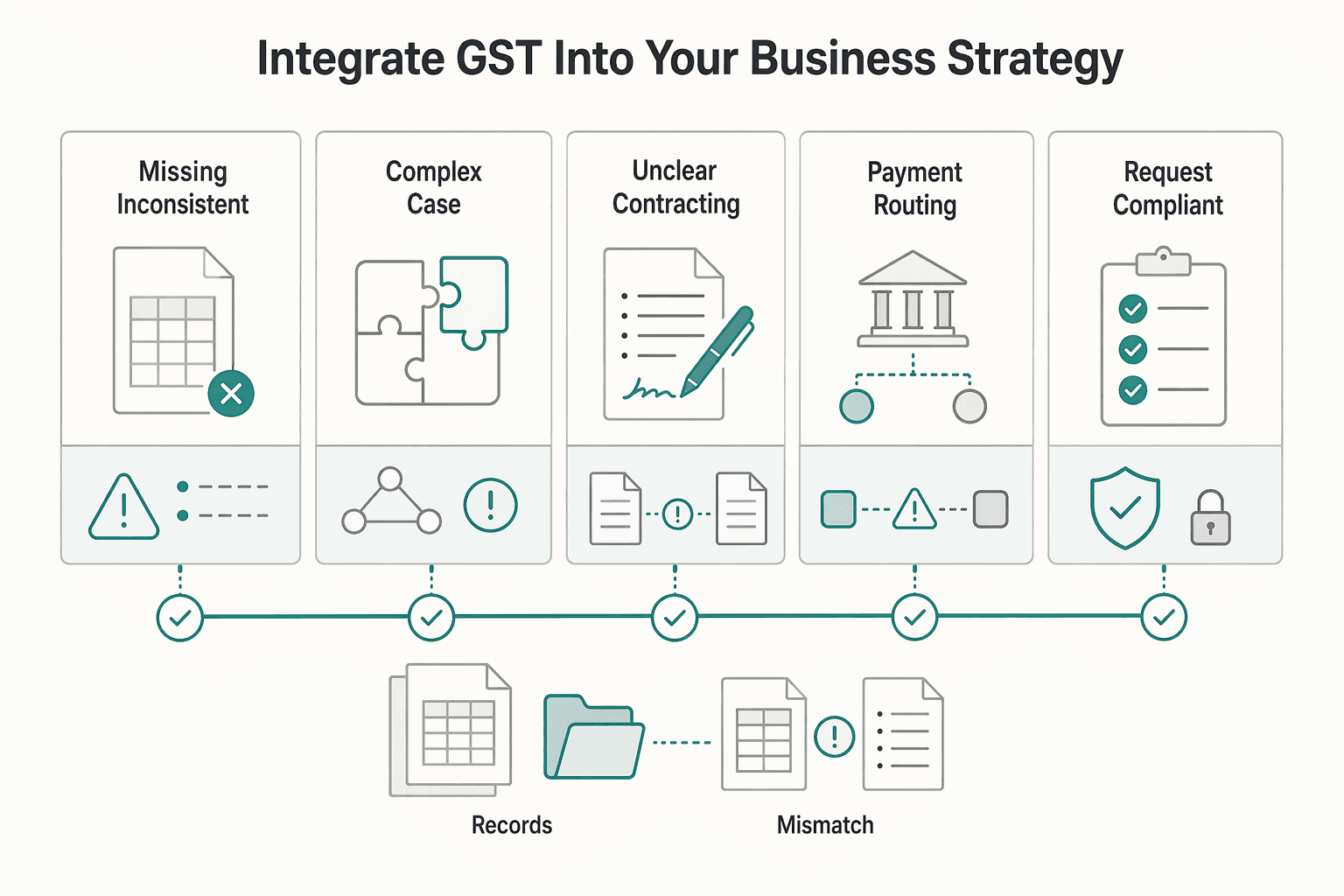

Beyond Filing: Integrate GST into Your Business Strategy#

Once your GSTR-1 and GSTR-3B process is stable, use the same discipline in pricing, onboarding, and delivery. That is where GST stops being just a filing task and starts shaping how your business runs.

1. Price with GST shown separately

Price with a tax-exclusive base fee and show GST as a separate line item. That keeps your commercial discussion clean and can reduce billing friction later. Use one format end to end: Professional fee: ₹X and GST: Current GST rate pending official GST portal or tax-advisor verification.

Keep the same structure in your proposal, contract, purchase order (if used), and invoice. Before you send any quote, verify the client legal name, billing entity, GSTIN (if applicable), and any billing details needed for correct invoicing. That way, your final invoice does not conflict with what was agreed.

2. Treat billing readiness as part of onboarding

Billing readiness is an onboarding issue, not just a finance issue. If a client cannot provide clean billing data, treat that as both a compliance risk and an operations risk.

Pause and clarify when you see red flags:

- missing or inconsistent legal name, billing address, or GSTIN

- requests to invoice outside the agreed contracting entity

- unclear contracting-party details

- payment routing that does not match contract terms

Action path:

- request compliant billing details in writing

- pause onboarding until records are complete

- escalate edge cases to a tax advisor when domestic versus overseas treatment is unclear

3. Use clean compliance habits to support better client work

Good compliance habits can support stronger B2B trust over time. A simple billing-readiness check helps:

- registration status is clear where applicable

- invoices are GST-compliant

- records needed for invoice reporting, tax payment, and ITC reconciliation are organized

This matters across both India-based and overseas client work, because accurate invoice reporting, tax payment, and ITC reconciliation all need to stay consistent. If you face ambiguous place-of-supply treatment, mixed domestic and export engagements, or unusual payment structures, get professional advice before you lock pricing or issue invoices.

You might also find this useful: How to Claim a GST Refund on Exports as an Indian Freelancer.

Conclusion: You're Not Just a Freelancer; You're the CFO#

GST works best as an ownership routine, not a filing-day scramble. Keep your setup records current, issue compliant invoices, file the returns that apply to you, and pause whenever a fact is unclear.

Foundation

Foundation is the record set you rely on every filing cycle. Keep your registration details, required registration documents, business identity data, and filing acknowledgements organized in one place.

Next, make sure your invoice and client data match that base record before you file. If core details are inconsistent or documents are missing, fix that first.

Workflow

Workflow is what keeps filing week quiet. Invoicing is part of GST compliance, so each transaction should leave behind usable records.

Run one fixed review for invoices issued, amounts received, tax collected, and expense records captured. That improves return readiness and makes client follow-up easier when invoice details have already been checked.

Execution

Execution is where your records turn into GST return filing. Rushed assumptions here can create rework and non-compliance risk.

File the return set that applies to your profile, verify figures against your records, and save acknowledgements with reconciliation notes. If something does not tie out, stop and resolve the exception before submission.

- Confirm setup: registration details, required documents, and current filing profile.

- Run the monthly process: invoice, capture records, and reconcile collections and expenses.

- File returns: submit applicable return or returns, then retain acknowledgements and payment proof.

- Review exceptions: mismatches, missing records, or transactions you cannot classify confidently.

- Escalate early: involve a qualified advisor when facts, documents, or portal treatment are unclear.

Use safe defaults, consistent execution, and clear evidence. That discipline can reduce avoidable risk and make each filing cycle easier to close.

For a step-by-step walkthrough, see How a German Freelancer Can Handle US Sales Tax with a US LLC. If you want a more traceable payment workflow as you scale cross-border client work, move to a workflow with clearer status visibility where supported: Explore Gruv for freelancers.

Frequently Asked Questions

Do I need GST for overseas clients?

If you are already registered and your service qualifies as a zero-rated export, you still report it in your GST returns. If you want to avoid paying IGST upfront on that supply, furnish LUT in Form GST RFD-11 before making the zero-rated supply. If your registration position is still unclear, resolve that first with A Guide to GST Registration for Indian Freelancers.

Should you choose monthly filing or QRMP?

Monthly filing is often the safer default when your clients are ITC-sensitive Indian businesses, because monthly outward reporting can support earlier recipient credit visibility. QRMP makes sense only if you are eligible under current portal rules and you can execute IFF for M1 and M2 consistently. If IFF is skipped or only partly used, the remaining invoices move to the next IFF or quarterly GSTR-1. Use this quick fit table to decide. | Option | Freelancer use case | Client ITC impact | Cash-flow effect | Poor fit when | |---|---|---|---|---| | Regular scheme with monthly returns | Regular B2B billing and predictable controls | Supports earlier recipient-side credit visibility through monthly outward reporting | More frequent return and payment checkpoints | You want minimum admin and clients are not ITC-timing sensitive | | Regular scheme with QRMP + IFF | Lower volume and you can run monthly payment + IFF in M1 and M2 | Can support recipient credit if IFF is filed reliably (typically by 13th of succeeding month) | Return cadence feels lighter, but monthly discipline is still required | You miss IFF, need clean month-end visibility, or serve ITC-sensitive procurement teams | | Composition levy (Section 10) | Limited cases after eligibility and commercial-fit check | Composition taxpayers cannot collect tax from recipients and cannot avail ITC | Simpler structure, but you lose ITC on your own inputs | You incur GST-heavy business costs or clients expect regular GST invoicing |

What dates matter most before you file?

For monthly filing, treat the 11th (GSTR-1) and 20th (GSTR-3B) as default anchors. For quarterly filing, one official FAQ shows GSTR-1 as the 13th day after quarter-end, while other official help text shows different quarterly cadence/eligibility details, so verify the current portal rule and latest notification before you submit. For quarterly GSTR-3B, due dates are 22nd or 24th based on your State or UT bucket.

How do you file LUT without rework?

File LUT before making a zero-rated supply, using Form GST RFD-11 via Services > User Services > Furnish Letter of Undertaking (LUT), and verify current menu labels in case the portal UI changed. Confirm eligibility first, including the prosecution condition linked to tax evasion of Rs 2.5 crore or above, and pause if that point is unclear. Treat LUT as an annual control because it is valid for the whole financial year in which it is tendered. A common failure point is filing after the zero-rated supply is made.

What happens if you file late?

Late filing creates two separate exposures: late fee under Section 47 and interest under Section 50 when tax payment is delayed. Statute text includes a baseline late fee of Rs 100 per day up to Rs 5000, and interest ceilings up to 18% and up to 24% for certain ITC cases, but verify current notified amounts, concessions, and applicability for your filing period before submission.

When should you claim ITC, and when should you wait?

Claim ITC only when the validation gates are met: tax invoice or debit note, receipt of goods or services, supplier-filed details reflected in GSTR-2B, tax payment, and your own return filing. Wait when records are incomplete or mismatched, and recheck GSTR-2B after the 14th of the succeeding month. Also screen for blocked credits under Section 17(5) and the 180-day supplier-payment condition before final claim.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- apa.ny.gov/meeting/2021/04/Planning/MA2019-01_FSEISAppe...trusted

- cbic-gst.gov.in/pdf/Circular-No-161-14-2021-GST.pdftrusted

- downloads.regulations.gov/USTR-2024-0002-0266/attachment_4.pdftrusted

- oecd.org/content/dam/oecd/en/topics/policy-issues/con...trusted

- oecd.org/content/dam/oecd/en/publications/reports/202...trusted

- sec.gov/Archives/edgar/data/1991261/0001493152230443...trusted

- tutorial.gst.gov.in/userguide/returns/Manual__Filing_Nil_Form_GS...trusted

- tutorial.gst.gov.in/userguide/returns/GSTR3B.htmtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Do I Have to Pay State Taxes While Living Abroad as a Digital Nomad?

Living abroad does not end `state income tax` exposure by itself. The first decision is practical: choose a filing position your facts can support, then build records that support the same story all year.

GST Registration Decisions for Indian Freelancers

This guide is for solo freelancers and independent consultants working from India, whether you bill Indian clients, foreign clients, or both. It focuses on practical GST registration decisions, not large-company structures, multi-entity planning, or product-heavy GST setups.