Quick Answer

To file a defensible final U.S. tax return after renouncing citizenship, build Form 8854 support first, confirm five tax years of compliance, and file the expatriation-year package with the correct status, labels, and attachments. If dual-status applies, use Form 1040-NR for the nonresident segment, report only U.S.-source income there, avoid the standard deduction, and keep every material figure tied to records, valuations, and ownership support.

The Expatriation Playbook: A Three-Stage Guide to a Flawless U.S. Tax Exit#

Start with Plan before you schedule paperwork. Good sequencing lowers filing risk because it lets you confirm Form 8854 support and screen for covered-expatriate issues before your expatriation-year return is due. It also keeps you from locking in an expatriation date while key records, valuations, or prior-year filings are still unresolved.

| Stage | When to do it | Main control point |

|---|---|---|

| Plan | Before expatriation date | Build the Form 8854 file, verify 5 tax years of compliance support, and screen covered-expatriate exposure |

| Execute | In the expatriation year | File the dual-status package correctly if it applies, label it properly, and attach Form 8854 on time |

| Manage | After expatriation | File Form 1040-NR only when income is subject to U.S. tax and keep withholding records current |

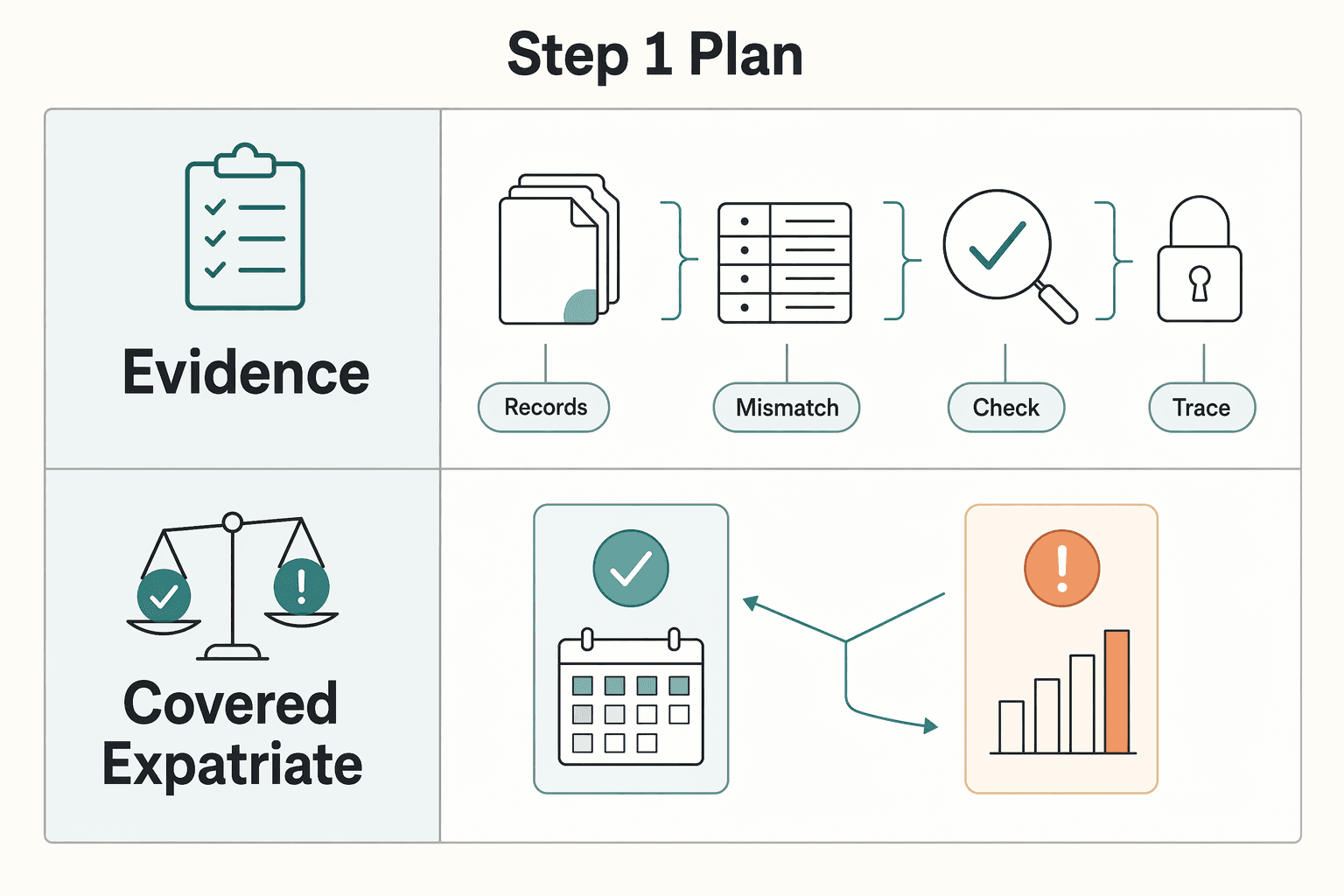

Step 1 Plan#

Build your file around Form 8854 before you lock your expatriation date. That form is where you certify compliance for the 5 tax years before expatriation, and failure to certify is itself a covered-expatriate trigger. A covered expatriate is someone who meets any of the covered-expatriate tests under the expatriation rules.

| Control | What to confirm | If unclear |

|---|---|---|

| Records readiness | Each of the last five years is supportable with filed returns, amendments if any, and settlement support | Pause before filing Form 8854 if a year is missing or unresolved |

| Covered-expatriate exposure | Check each applicable test using the current Form 8854 instructions, including net-worth and average tax-liability thresholds | Escalate if the result depends on uncertain valuations, unresolved amendments, or assets that are hard to price |

| Asset documentation | For each material asset, keep dated support for ownership, valuation method, and the figure reported on Form 8854 | Treat it as not filing-ready if you cannot trace a reported number |

The practical decision at this stage is simple. Decide before exit whether you are on a routine expatriation-year path or one that needs deeper IRC 877A analysis. If the five-year compliance file is clean and the covered-expatriate screen is straightforward, the rest of the project is mostly execution discipline. If either point is shaky, the right move is usually to pause before the expatriation date is fixed.

Before you move forward, use this checklist:

- Confirm records readiness. Make sure each of the last five years is supportable with filed returns, amendments if any, and settlement support. If a year is missing or unresolved, pause before filing Form 8854. The standard is not just that something was filed. The standard is that the year can be followed from return to final outcome without gaps you would struggle to explain later.

- Screen covered-expatriate exposure. Check each applicable test using the current Form 8854 instructions, including net-worth and average tax-liability thresholds. Use the current year-sensitive amount instead of carrying forward an older number. If the result depends on uncertain valuations, unresolved amendments, or assets that are hard to price, treat that as a sign to escalate rather than assume it will sort itself out.

- Set an asset documentation standard. For each material asset, keep dated support for ownership, valuation method, and the figure reported on Form 8854. If you cannot trace a number, treat it as not filing-ready. In practice, you should be able to point from the reported amount back to the supporting file without rebuilding the logic from scratch.

A simple way to keep this manageable is to organize the file by issue, not by inbox or download source. Put each prior year in one place. Keep amendments with the year they affect, and keep each material asset with its ownership and valuation support. That makes the final reconciliation faster and reduces the chance that a number on Form 8854 is technically correct but unsupported in your working file.

Once the file is built, the next risk shifts from eligibility to execution. That is where status, labels, and attachments matter more than theory.

Step 2 Execute#

This is where filing mechanics matter most. If you were a U.S. resident for part of the year and a nonresident for part of the year, you are a dual-status individual. The nonresident segment is the nonresident part of that year, and during that segment you are taxed on U.S.-source income only. If you end the year as a nonresident, the IRS filing framework centers on Form 1040-NR.

Before filing, use this control table:

| Task | Common failure | How to verify before filing |

|---|---|---|

| Label the return | Dual-status label is missing | Confirm "Dual-Status Return" appears across the top of the return |

| Attach Form 8854 | Form 8854 is prepared but not attached, or copy filing is missed | Confirm the initial Form 8854 is attached to the income tax return for the year that includes the expatriation date, and calendar copy filing by the return due date, including extensions |

| Keep forms consistent | Non-U.S.-source amounts appear in the nonresident segment | Confirm the nonresident segment reports only U.S.-source income |

| Reconcile reported figures | Form 8854 figures do not tie to support files | Tick-and-tie each material figure to valuation and underlying records |

Then run these final checks before filing:

- Do not claim the standard deduction on a dual-status return.

- Do not treat Form 8854 as optional.

- If your expatriation date is on or after June 17, 2008, IRC 877A applies. Pause and escalate if covered-expatriate screening, sourcing, or valuation support is unclear.

The safest review sequence is mechanical, not intuitive. First confirm filing status. Then confirm the package label. Then confirm attachments. Then review the income lines for sourcing. Finally, tie Form 8854 back to the support file. That order matters because a technically correct number can still sit in the wrong package, on the wrong form, or in the wrong segment of the year.

This is also the stage where small mismatches create avoidable trouble. Check that names, dates, and status assumptions are consistent across the return and Form 8854. If one document reflects the expatriation date differently from another, treat it as a filing issue, not a cosmetic one.

If the expatriation-year filing is clean, the ongoing job gets narrower. After that, you are managing nonresident obligations, not rebuilding the exit file every year.

Step 3 Manage#

After expatriation, the right posture is ongoing nonresident control. Form 1040-NR is filed only when you have income subject to U.S. tax. Effectively connected income (ECI) is U.S.-source income connected with a U.S. trade or business and is taxed on a net basis at graduated rates.

| Task | What the article says | Follow-up |

|---|---|---|

| Monitor U.S.-source income | Form 1040-NR is filed only when you have income subject to U.S. tax | If the facts are unclear, review them before deciding not to file |

| Use Form W-8BEN when requested | A foreign individual uses Form W-8BEN to establish foreign status and, if eligible, claim treaty withholding relief | Keep a copy of what you provided and note which payer received it |

| Keep a records log | Maintain filed returns, Form 8854, W-8BEN submissions, withholding documents, and notes supporting source and taxability decisions | A short year-by-year memo is often enough if it clearly shows income, withholding, and why a return was or was not required |

| Escalate early when facts change | Get help if a payer rejects your W-8BEN, withholding does not match your treaty position, or your activity may be treated as a U.S. trade or business | If residency assumptions are part of the issue, review them with a conservative framework |

Your job here is to monitor U.S. taxable income, handle withholding documentation correctly, and keep a clear record trail for each file-or-no-file decision.

- Monitor U.S.-source income each year. If no income is subject to U.S. tax, Form 1040-NR may not be required. If the facts are unclear, review them before deciding not to file. Make that decision from the year's actual income and withholding facts, not from what happened the year before.

- Use Form W-8BEN when requested. A foreign individual uses Form W-8BEN to establish foreign status and, if eligible, claim treaty withholding relief. It supports withholding treatment but does not by itself remove filing obligations. Keep a copy of what you provided and note which payer received it.

- Keep a records log. Maintain filed returns, Form 8854, W-8BEN submissions, withholding documents, and notes supporting source and taxability decisions. A short year-by-year memo is often enough if it clearly shows what income you had, whether withholding occurred, and why you concluded a return was or was not required.

- Escalate early when facts change. Get help if a payer rejects your W-8BEN, withholding does not match your treaty position, or your activity may be treated as a U.S. trade or business. If residency assumptions are part of the issue, review them with a conservative framework in 183-Day Rule Explained.

The post-expatriation mistake to avoid is treating nonresident compliance as automatic. It is narrower than before, but it is still a live control process. Payer paperwork, withholding, and the character of your U.S. income can all affect whether you file, what you report, and what records you need to keep.

For a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide. Before you file, you can also prefill your payer paperwork so your post-expatriation withholding setup is clean: Generate your W-8 package.

Conclusion: Take Control of Your Financial Future#

Close this out like an operator: Organize, Confirm, Notify. The standard is straightforward: defensible records, one internally consistent filing package, and documented payer updates after renunciation.

| Action | Key items | Check |

|---|---|---|

| Organize | CLN, records supporting the 5-year compliance certification on Form 8854, and the basis, valuation, ownership, and income records used in the expatriation-year package | Check date consistency across the CLN, Form 8854, and the return package |

| Confirm | Attach the initial Form 8854 to the expatriation-year return and file by the applicable deadline | If dual-status applies, include the dual-status statement, use Form 1040-NR for the nonresident segment, limit that segment to U.S.-source income, and do not use the standard deduction |

| Notify | Update U.S. payers or withholding agents that still need non-U.S. documentation; for foreign individuals, that is often Form W-8BEN provided to the payer when requested and not filed with your return | Keep a log of what you sent, when, and to whom, and monitor whether later-year Form 1040-NR filing is required based on income subject to U.S. tax |

- Organize your evidence pack now.

Gather the records that control the filing: your CLN (Certificate of Loss of Nationality), records supporting the 5-year compliance certification on Form 8854 (including filed returns where applicable), and the basis, valuation, ownership, and income records used in the expatriation-year package. Check date consistency across the CLN, Form 8854, and the return package so your expatriation date aligns with IRS relinquishment-date rules. As a practical matter, keep the core file in one place and make sure each material number can be traced without searching across separate folders, email threads, or old downloads.

- Confirm the package before filing.

Treat this as one package, not a set of separate tasks. Attach the initial Form 8854 to the expatriation-year return and file by the applicable deadline. If your facts require dual-status treatment, label the return "Dual-Status Return," include the required dual-status statement, use Form 1040-NR for the nonresident segment, and verify that segment is limited to U.S.-source income and does not use the standard deduction. Final check: names, dates, status labels, sourcing, and attachments should match across documents. If a figure is correct but unsupported, or supported but inconsistent with the rest of the package, it is not ready to file.

- Notify payers and monitor post-filing obligations.

Update U.S. payers or withholding agents that still need non-U.S. documentation. For foreign individuals, that is often Form W-8BEN, provided to the payer when requested and not filed with your return. Keep a log of what you sent, when, and to whom. Then monitor whether later-year Form 1040-NR filing is required based on income subject to U.S. tax. Keep the same discipline after the exit year that you used during it: document the facts, save withholding records, and note the basis for each filing or non-filing decision.

Bring in cross-border tax or legal support when ownership runs through entities, partnerships, trusts, or intermediaries. Do the same when sourcing is unclear, or when treaty residency or withholding treatment is uncertain. If dual-status mechanics are still the weak point, review Filing a Dual-Status Alien Tax Return Without Mismatched Forms.

If you also want process context, see How to Renounce US Citizenship: The Process and Tax Implications. If your exit includes entity structures, mixed income sourcing, or cross-border payout complexity, get an implementation read on controls and coverage: Talk to Gruv.

Frequently Asked Questions

What does Form 8854 actually do?

Form 8854 is where you certify five tax years of U.S. federal tax compliance and report the information used to determine covered expatriate status. It should be attached to the income tax return for the year that includes the expatriation date. A defensible Form 8854 also ties each material figure to filed returns, valuations, and ownership records.

How do you know if you will be a covered expatriate?

You are a covered expatriate if any listed test applies, including the net-worth test, the average annual net income tax liability test, or failure to certify five tax years of compliance on Form 8854. Check each year-sensitive amount using the current Form 8854 instructions. If the result depends on uncertain valuations or unresolved amendments, escalate before filing.

What is the biggest mistake people make on the final tax return after renouncing citizenship?

The biggest mistake is usually filing mechanics, not arithmetic. Common failures are wrong status, mismatched forms, missing attachments, or incorrect dual-status labeling. If dual-status applies, use Form 1040-NR for the nonresident segment, limit it to U.S.-source income, and do not use the standard deduction.

How does the exit tax work if you are a covered expatriate?

If you are a covered expatriate, Section 877A generally applies mark-to-market treatment, so property is treated as sold the day before expatriation for fair market value. The main filing risks are basis, valuation method, and ownership support, especially for private, illiquid, or cross-border assets. Each material asset should have dated valuation support and defensible basis records.

Do you still have to file an FBAR after renunciation?

Possibly. FBAR is a separate filing and is not submitted with the income tax return package, so filing Form 1040-NR or Form 8854 does not satisfy it if your facts still trigger an FBAR obligation for that calendar year. Review full-year account balances and file electronically through FinCEN BSA E-Filing by the current deadline if required.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

183-Day Rule Tax Myths That Trigger Residency Filing Mistakes

If you are a mobile freelancer or consultant, start here: the "183 day rule tax" idea is not a single universal test. It is a shortcut phrase people use for different residency rules that do not ask the same question. If you mix federal and non-federal residency logic, you can create filing risk even when your travel calendar looks clean.

Renounce US Citizenship With a Clear CLN and Tax Closure Plan

If you plan to **renounce US citizenship**, treat it as a sequence, not a single embassy appointment. In practice, you are managing three checkpoints: the consular renunciation act abroad, State Department approval reflected in a Certificate of Loss of Nationality (CLN), and tax-compliance follow-through with the IRS.