Quick Answer

Start with a narrow scope test: treat an entity as BOIR-in-scope only when it is foreign formed and registered to do business in a U.S. state or tribal jurisdiction through a filing. Then apply ownership checks by risk, not as default collection for every U.S.-created entity. Keep a dated decision packet with formation evidence, registration proof, reviewer, and source version, and route conflicts or material changes to escalation before release.

Beneficial Ownership Verification for Platform Teams in 2026#

In 2026, the practical approach is to separate BOI filing scope from ownership-risk controls. Many entities created in the United States are exempt from BOI reporting, but that does not automatically remove ownership-review controls in risk-based onboarding.

This guide is for compliance, legal, finance, and risk owners managing cross-border contractor, seller, or creator payouts. FinCEN, a bureau of the U.S. Department of the Treasury, narrowed BOI reporting scope in its March 26, 2025 interim final rule to entities previously defined as foreign reporting companies. That leaves you with an operational choice: avoid under-controlling higher-risk entities while also avoiding blanket BOI collection from entities now exempt.

- The legal scope moved, but your control design still needs discipline.

Beneficial ownership information, or BOI, covers information about the entity, its beneficial owners, and in certain cases company applicants. When reporting is required, teams file a BOIR. What changed is who is in scope. FinCEN's BOI E-Filing alert says entities created in the United States, including those previously known as domestic reporting companies, are now exempt from BOI reporting. BOI filing scope now centers on foreign-formed entities registered to do business in a U.S. state or tribal jurisdiction by filing with a secretary of state.

- The common failure is stale scope language in live onboarding flows.

Older BOIR filing instructions still use broader wording, and that same document tells teams to check the latest FinCEN BOI information. Check your first checkpoint against two facts: where the entity was formed, and whether it registered to do business in a U.S. state or tribal jurisdiction by filing the required document. Keep your record audit-ready by saving the reviewer, date, and source documents used for that determination.

- "No BOIR required" is not always the same as "no ownership review needed."

BOI reporting and CDD obligations are different regimes. Current eCFR text still requires covered financial institutions to maintain written procedures reasonably designed to identify and verify beneficial owners. Even when a BOIR is not required, teams may still apply ownership-verification controls based on risk. The useful operating standard is to trigger screening only when it is actually needed so onboarding speed and compliance defensibility can coexist.

From there, we recommend a straightforward path: pick one operating model, define checkpoint triggers for deeper review, and document escalation paths that will hold up under audit. A defensible minimum evidence pack includes an as-of date, the reporting-company determination, and the documents used to reach it.

For the broader payout-platform context, see Beneficial Ownership Verification for Platforms: UBO Rules and Why They Matter for B2B Payouts.

How to pick the right UBO model for your platform#

Start with the lightest UBO model that still classifies whether an entity is a reporting company, and not exempt, correctly. Add automation only after that classification is stable.

- Use this model set when your onboarding mix is complex.

These models fit multi-entity platforms onboarding contractors, sellers, or creators across mixed U.S. and non-U.S. populations, especially when some entities may be foreign reporting companies. A practical split at intake is simple: is the entity formed in the U.S., or foreign-formed and registered to do business in the U.S.?

- Skip heavy design when your population is narrow.

If your flow is single-entity, domestic, and has no cross-border exposure or realistic foreign-reporting-company intake, a heavy UBO model is usually unnecessary under current BOI rule text. The common mistake is applying broad BOI logic from older guidance to an onboarding population that never reaches a BOIR decision point.

- Evaluate every model with the same four criteria.

Score options on scope accuracy under the Corporate Transparency Act framework as implemented by FinCEN, operational burden, operational impact, and audit defensibility. Put scope accuracy first. FinCEN's March 26, 2025 interim final rule narrowed BOI reporting to foreign reporting companies, while some federal pages still use broader language and direct BOI questions to FinCEN. For defensibility, capture formation jurisdiction, U.S. registration status, reviewer, as-of date, and source document for each decision.

- Let legal stability set your automation ceiling.

If your internal interpretation of reporting-company status is unstable, use stronger legal escalation gates instead of deeper automation. FinCEN's filing instructions are explanatory and may be revised, so edge cases need controlled review. Keep event-driven triggers explicit. When required information changes, BOI updates run on a 30-calendar-day clock.

For a step-by-step walkthrough, see How to Transfer Ownership of an LLC.

Compare the five UBO operating models before you choose#

Choose the lightest model that keeps each BOIR trigger defensible under the March 26, 2025 interim rule. Add complexity only where your onboarding mix actually requires it.

The core scope test is straightforward. BOI reporting turns on foreign reporting company status, which means the entity is foreign-formed and registered to do business in the U.S. by filing with a secretary of state. Entities previously treated as domestic reporting companies are exempt under that interim rule, and U.S. persons are exempt from providing BOI to a foreign reporting company. Keep one caveat in view: FinCEN filing instructions are explanatory only, while some official pages still use broader language that may need legal reconciliation.

| Model name | Best for | BOIR trigger logic | Dependence on FinCEN BOI FAQs | Payout friction | Legal review load | Failure mode |

|---|---|---|---|---|---|---|

| Reporting-only minimum | U.S.-heavy platforms with limited foreign-entity intake | Trigger only when legal confirms foreign-formed + U.S.-registered status | Low when anchored to rule text and filing instructions | Low | Low to medium | Stale rule assumptions can leave a foreign entity unflagged if intake misses U.S. registration evidence |

| Risk-tiered onboarding | Mixed-geography onboarding with some higher-risk cases | Baseline checks for all; BOIR branch only for foreign-formed + U.S.-registered entities or truly ambiguous cases | Medium, because tier logic often borrows FAQ examples | Medium | Medium | Over-collection from U.S. persons or exempt U.S.-created entities if tiers are too broad |

| Event-driven reverification | High-velocity programs where entity or ownership facts change after onboarding | Recheck status on key data changes; if previously submitted required information changes, updates run on a 30-calendar-day clock | Medium, because event definitions are interpretation-heavy | Medium to high | Medium to high | Noisy triggers delay payouts, while weak detection can miss 30-day update filings |

| Jurisdiction-split handling | Platforms with meaningful foreign incorporation plus U.S. registration activity | Separate U.S.-created and foreign-formed paths; make BOIR decisions only on the foreign path after U.S. registration is proven | Low to medium, because classification relies on formation and registration facts | Low to medium | Medium | Missed foreign-entity filings in the FinCEN BOI E-Filing System when formation country is captured but U.S. state filing is not |

| Hybrid managed controls | Larger platforms with delegated ops teams and frequent edge cases | Automation proposes scope; counsel review is required when logic conflicts with prior determinations, filing instructions, or other official-page language | Medium to high by design | Medium to high | High | Reviewer bottlenecks, stale exceptions, or over-collection from U.S. persons if the exemption is not encoded clearly |

| Recommendation band: low complexity | Mostly domestic entities with rare foreign-registration cases | Start with reporting-only minimum | Keep FAQ dependence low | Keep friction low | Escalate only edge cases | Main risk is missing the few foreign-reporting-company cases present |

| Recommendation band: medium complexity | Mixed onboarding with some cross-border entity volume | Start with jurisdiction-split handling; add risk-tiering only when justified | Moderate | Moderate | Moderate | Main risk is broad UBO collection without a real BOIR trigger |

| Recommendation band: high complexity | Cross-border onboarding plus frequent pre-payout profile changes | Start with jurisdiction-split + event-driven checks, or hybrid managed controls when scope disputes are frequent | Medium to high | Medium to high | High | Main risk is silent misclassification if escalation gates are too weak |

Two operator controls matter whatever model you pick. First, complete the decision packet before deciding "BOIR required" or "not required." Include formation jurisdiction, evidence of U.S. registration filing, reviewer, and as-of date. Second, set your filing method early. We recommend deciding upfront whether your team will use PDF BOIR upload or online filing, because the online flow is real-time and you cannot save it for later. Handoff-heavy teams usually need tighter process control.

Keep BOIR scope separate from broader UBO data collection for internal or partner needs. If your main risk is legal scope, start with reporting-only minimum or jurisdiction-split handling. If your main risk is post-onboarding change, add event-driven checks. If guidance drift and edge cases already consume legal capacity, hybrid managed controls are usually justified.

Model 1 Reporting-only minimum#

Choose this model when your onboarding is mostly U.S. companies and you want a narrow, defensible BOIR gate. Do not start a BOIR process unless legal confirms the entity is a foreign reporting company under the March 26, 2025 interim final rule.

Where this model fits#

This is the default for low-complexity teams with limited foreign-entity onboarding, especially when over-collection is the bigger risk. FinCEN narrowed CTA BOI reporting to entities previously defined as foreign reporting companies. Entities previously treated as domestic reporting companies are exempt and do not need to report, update, or correct BOI to FinCEN.

What you actually verify#

For this model, your decision point is legal classification, not where the customer operates or gets paid. Ask a narrower question: does legal conclude the entity is a foreign reporting company, including registration to do business in a State or Tribal jurisdiction by filing with a secretary of state or similar office?

Keep the edge-case packet compact, with formation jurisdiction from formation documents or a registry extract, proof of U.S. registration filing if any, reviewer name and as-of date, and the final classification of reporting company or not.

If legal confirms reporting-company status, file the Beneficial Ownership Information Report through FinCEN's BOI e-filing site. For entities that become reporting companies on or after March 26, 2025, the filing window is 30 calendar days.

Why teams choose it and where it breaks#

The advantage is low operational overhead and a clean control narrative tied to current BOI scope. The tradeoff is weaker internal signal for non-reporting but higher-risk entities. You can still miss cases if ops shortcuts on customer location instead of checking formation and U.S. registration evidence. Keep the boundary clear: this BOIR gate does not replace separate written-procedures duties that may apply to covered financial institutions under 31 CFR 1010.230.

Model 2 Risk-tiered UBO collection at onboarding#

This model fits when you need more than a reporting-only gate, but full owner-level review for every entity would over-collect. Keep baseline entity checks for all onboarding, then require deeper Ultimate Beneficial Owner evidence only when facts indicate real BOI exposure or higher risk for your program.

Why this model fits#

This model works when you need more signal than Model 1 but still want to control collection. As of the March 26, 2025 interim final rule, FinCEN narrowed BOI reporting to entities previously defined as foreign reporting companies, while entities previously defined as domestic reporting companies are exempt. So your onboarding logic should classify first, not assume every incorporated business has a BOI reporting obligation.

What the tiers should do#

A tiered design works best when each lane has one job.

| Lane | Trigger | Action |

|---|---|---|

| Baseline entity lane | Every entity | Collect core classification facts, including formation jurisdiction and whether the entity is registered to do business in the U.S. by filing with a Secretary of State or equivalent office. |

| Enhanced UBO lane | Entity is foreign formed and appears registered in the U.S. by filing with a Secretary of State or equivalent office | Collect deeper UBO evidence and route for reporting-company analysis. |

| Legal escalation lane | Documents conflict or registration status is unclear | Pause and resolve classification before continuing collection. |

The key checkpoint#

Do not tier on payment destination, operating country, or founder location. Tier on the narrower BOI scope question: was the entity formed under foreign law, and registered to do business in the U.S. through a filing with a Secretary of State or equivalent office?

Keep the evidence pack compact and tied to the decision record: formation document or registry extract, proof of U.S. registration filing if any, reviewer name, and as-of date.

Where teams miss#

The first failure is treating all non-U.S. entities as reportable, which is broader than the current BOI scope. The second is collapsing CTA scope and customer due diligence into one decision. For covered financial institutions, 31 CFR 1010.230 requires identifying beneficial owners of legal entity customers at account opening and verifying identity with risk-based procedures.

Recommendation#

Make escalation mandatory for foreign-formed entities with incomplete U.S. registration evidence. That one control helps prevent both high-cost errors: missing a real foreign reporting company and over-collecting from exempt domestic profiles.

Model 3 Event-driven reverification before payout release#

Pick this model when you need a payout-time control that rechecks ownership only after meaningful changes, not on a fixed calendar. It fits high-velocity programs where ownership or control can drift between onboarding and disbursement.

If Model 2 established the initial classification, this model adds a second gate only when new facts make the original owner record less reliable.

Why this model works#

This model works when time-based review creates more noise than protection. Current CDD text in 31 CFR 1010.230 still ties beneficial-owner identification to new account opening for covered financial institutions. It allows reliance on customer-supplied ownership data only until facts reasonably call reliability into question. FinCEN's CDD framework also describes ongoing, risk-based maintenance and updates of customer information, including beneficial-owner information for legal entity customers.

So the trigger is the changed fact, not time elapsed. It also stays aligned with post-March 26, 2025 BOI scope: entities previously defined as domestic reporting companies are exempt from BOI reporting, while foreign reporting companies still have BOIR obligations.

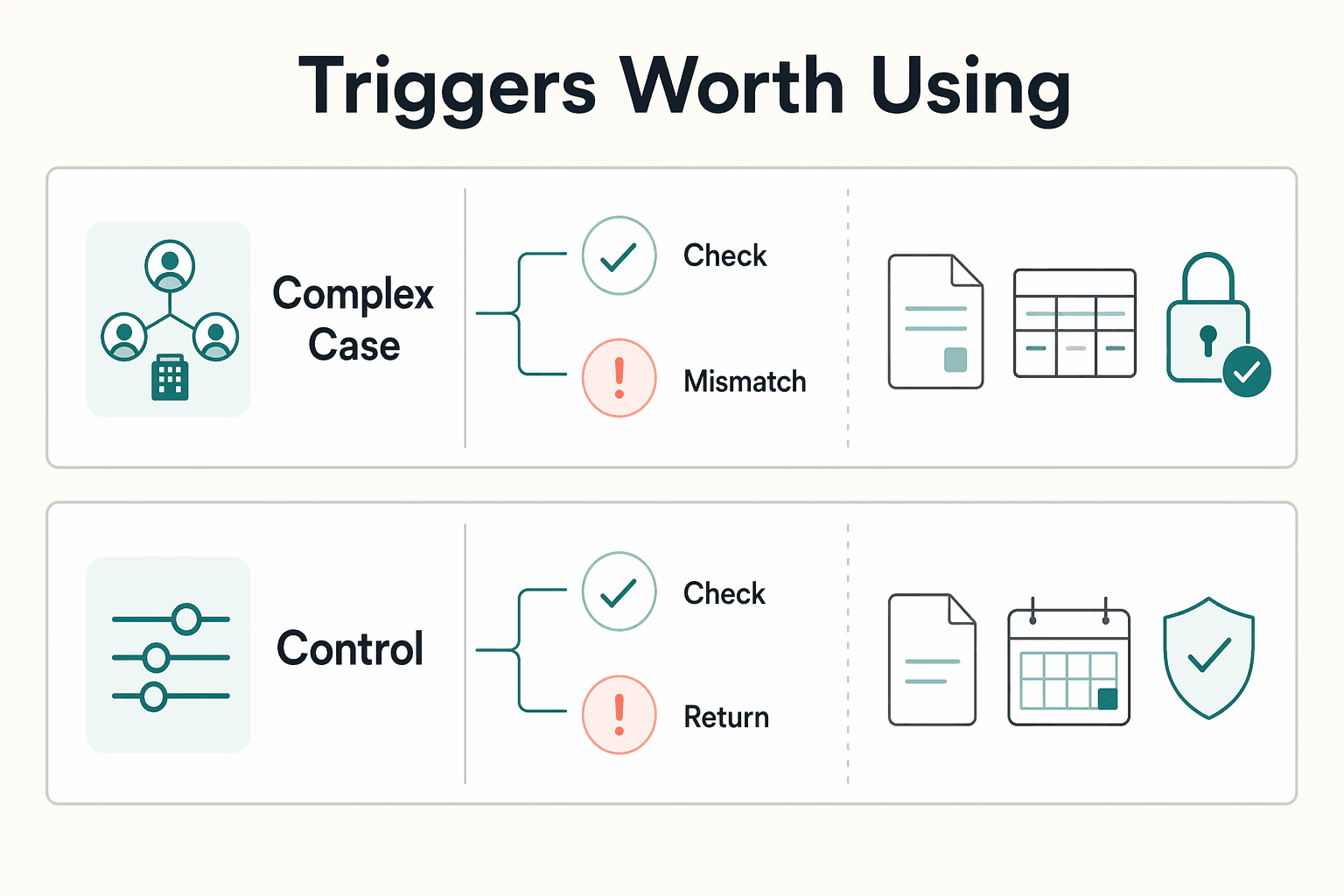

Triggers worth using#

Use narrow, auditable triggers tied to BOI scope or ownership reliability:

| Trigger | Examples | Review implication |

|---|---|---|

| Legal entity profile changed | Formation jurisdiction, legal name, or U.S. registration status changed | Recheck whether the entity still appears to fall within foreign reporting company scope |

| Ownership or control details changed | A new control person, a revised beneficial-owner declaration, or a material risk-score change tied to entity data | If BOI scope is uncertain, consider pausing release and routing the case to legal before final payout approval |

| Prior filing data no longer matches | The entity previously provided a FinCEN ID, claimed a BOIR filing, or referenced the BOI E-Filing System | Current facts no longer match |

Keep triggers tight. If cosmetic profile edits cause payout stops, teams get noise instead of risk control.

What should release the hold#

Release criteria should be short and documentable: current registry extract or formation record, updated UBO or control-person attestation, reviewer name, and as-of date. Where relevant, include BOIR filing-status review and any FinCEN identifier used by the individual or reporting company.

Also check timing when it matters. For entities that become reporting companies on or after March 26, 2025, the initial BOIR deadline is 30 calendar days from registration notice or public notice. BOI changes to previously submitted information also carry a 30-calendar-day update deadline.

Treat secondary reporting about possible February 13, 2026 CDD relief as non-final until legal confirms the current primary text that applies to your program.

For BOI filing requirements and definitions, see this practical guide to FinCEN's Beneficial Ownership Information (BOI) Reporting.

Model 4 Jurisdiction-split handling for foreign entities#

Choose this approach when you onboard meaningful cross-border entity volume and need a clear BOIR decision path from day one. Split intake by jurisdiction so you do not collect BOI data from entities previously defined as domestic reporting companies while still catching foreign reporting company cases that require action.

The core judgment is two-step under the March 26, 2025 interim final rule. First, determine whether the entity is U.S.-created or foreign-formed. Second, for foreign-formed entities, determine whether they are registered to do business in the United States by filing with a Secretary of State or equivalent office. That registration fact is the key BOIR scope checkpoint.

| Entity path | Practical treatment | Key checkpoint |

|---|---|---|

| U.S.-created entity | Do not route into BOIR collection based only on domestic formation | Record that entities previously defined as domestic reporting companies are exempt from BOI reporting under the March 2025 rule |

| Foreign-formed, no U.S. registration filing identified | Hold BOIR-specific steps unless later facts show U.S. registration | Verify whether any U.S. registration filing with a Secretary of State or equivalent office exists before closing scope |

| Foreign-formed, registered via Secretary of State or equivalent office | Route to foreign reporting company review and BOIR decisioning | Confirm filing path, registration date, and whether any exception needs legal review |

Why this model earns its keep#

This model earns its keep when one intake population contains genuinely different legal paths. A U.S. LLC and a Cayman company qualified to do business in Delaware should not follow identical BOI logic. Forcing one intake path usually causes over-collection from exempt domestic entities or missed follow-up on foreign entities that meet the U.S. registration condition.

It also makes your controls easier to defend because the decision record ties to a specific fact pattern, not a broad "non-U.S. equals high risk" assumption.

What to verify before you ask for anything else#

Before you request UBO or BOIR evidence, build a short jurisdiction file with the country of formation, whether the entity is registered to do business in the United States through a filing with a Secretary of State or equivalent office, the filing office name, and the effective date or notice date of that registration.

The date matters. For entities that become reporting companies on or after March 26, 2025, 31 CFR 1010.380 sets a 30-calendar-day filing timeline.

The failure mode to guard against#

Do not treat every foreign business as a foreign reporting company. In this model, a non-U.S. entity is generally a BOIR candidate when the U.S. registration element is present, and edge cases should go to legal.

Also watch for source drift. The BOI E-Filing System is the filing channel, but its broader CTA wording can read differently from the March 2025 interim final rule. If that conflict shows up in operations, pause classification and get legal confirmation on the governing text.

How to document it so it holds up later#

For each foreign-formed entity, store the registration evidence, reporting-company determination, reviewer name, and as-of date. If you move the case to filing review, capture whether the customer submitted a Beneficial Ownership Information Report through the BOI E-Filing System and any confirmation reference the customer provided.

For ownership structure choices tied to platform operations, see Merchant of Record for Platforms and the Ownership Decisions That Matter.

Model 5 Hybrid managed controls with legal escalation gates#

This model makes sense when a wrong scope call is more expensive than moderate onboarding friction. It can fit larger platforms that want routine BOI handling automated, with legal escalation for ambiguous reporting company decisions.

This model works best after Model 4's jurisdiction split is already in place. Once U.S.-created and foreign-formed entities are separated, define who decides edge cases and what evidence is required before classification is finalized.

Why this model is worth the extra cost#

The main benefit is defensibility. You can automate standard intake, including entity facts, ownership data, and registration details, and require legal review when current classification logic conflicts with prior determinations.

That matters under the March 26, 2025 interim final rule. Current BOI reporting scope was narrowed to entities previously defined as foreign reporting companies, while entities previously defined as domestic reporting companies are exempt from BOI reporting, updates, and corrections. A hybrid design also fits the CDD expectation of risk-based, written verification procedures rather than a one-size-fits-all rule.

The escalation gate that matters most#

Make legal review mandatory as an internal control when a new classification would reverse a prior determination based on older BOI FAQs, IRS page text, or earlier internal memos. The point is to prevent silent reclassification and preserve a clear decision record when source language drifts.

A practical escalation gate should cover cases where:

- an entity was previously marked out of BOIR scope but current review suggests foreign reporting company treatment

- a foreign-formed entity has incomplete or inconsistent U.S. registration evidence

- ownership analysis raises uncertainty around substantial control or the 25% ownership threshold

- customer-provided government page text conflicts with your current reading of 31 CFR 1010.380 and the March 2025 interim final rule

If legal confirms filing is required, route to the FinCEN BOI E-Filing System and log the BOIR submission confirmation in the case record.

What operations should verify before escalation#

Send legal a compact evidence pack, not a generic ticket. Include country of formation, U.S. registration filing evidence, registration notice or public notice date, prior classification record, current classification reasoning, and the beneficial owner list used for the determination.

Timing is a control point, not a detail. If an entity becomes a reporting company on or after March 26, 2025, the initial BOIR filing window is 30 calendar days. Updates for changes to previously submitted required information also follow a 30-calendar-day window.

The main failure mode#

The common failure is resolving contradictions by treating whichever public page appears newest as controlling. For example, an IRS page still states that certain U.S.-created entities must report BOI, last reviewed 19-Feb-2026, which can conflict with current interim-final-rule scope language.

Use this model when regulatory-change risk is high and multiple teams touch the same entity record. The extra operating cost can help reduce silent misclassifications and support stronger audit-ready decision logs.

Related reading: Stripe Identity User Verification Without Repeat Reviews.

Build the evidence pack auditors and counsel will actually need#

Build each entity file so you or an independent reviewer can reconstruct the BOI decision, timeline, and action without relying on email threads. The goal is not more paperwork. It is a file that makes the classification, filing decision, and timing obvious to someone who was not in the original conversation.

| Artifact | What it answers | What to keep |

|---|---|---|

| Internal scope determination memo | Why you classified the entity that way | Preserve the interpretation used at decision time and tag it by source type |

| Beneficial ownership data record | Whose ownership or control data you used | Include FinCEN ID where available |

| Filing decision | What action followed | No BOIR, initial BOIR, update, or correction |

| BOI E-Filing System submission evidence | What was submitted | Submission confirmation details and downloadable BOIR transcript |

- Require four artifacts for every entity.

Keep a standard packet: internal scope determination memo, beneficial ownership data record, filing decision, and any FinCEN BOI E-Filing System submission evidence. Each artifact should answer a different question: why you classified the entity that way; whose ownership or control data you used, including FinCEN ID where available; what action followed, whether no BOIR, initial BOIR, update, or correction; and what the customer or your team submitted, including submission confirmation details and downloadable BOIR transcript. The submitter's certification is that the filing is true, correct, and complete.

- Version the interpretation, not just the customer data.

FinCEN states filing instructions may be revised, so preserve the interpretation used at decision time and tag it by source type, such as a FinCEN release, BOI FAQs update, or internal legal opinion. For each interpretation note, log the source, as-of date, rule summary, and whether it changed a prior position. If classification changes later, keep both versions and record the delta instead of overwriting history.

- Capture review checkpoints that show the decision path.

Record who approved the classification internally, when your team reviewed it, what sources you checked, and what changed from the prior determination. Federal sources do not require that exact approver-field format, but it is a high-value internal control for defensibility. Tie each checkpoint to a trigger, such as new registration evidence or ownership or control changes, and align the review date, action date, and filing evidence. For foreign reporting companies, the interim final rule extended initial, update, and correction timelines to 30 days from publication, and the BOI E-Filing alert listed April 25, 2025 for most existing foreign companies after that update. For covered financial institutions, 31 CFR 1010.230 requires written beneficial-ownership identification and verification procedures in the AML compliance program. Use that as the benchmark for documentation rigor.

- Add boundary notes so BOI is not mixed with FBAR or FATCA.

Include a short boundary note in each entity file when adjacent tax-reporting issues appear, and state why they are separate from BOI scope. Use exact labels: FBAR is filed on FinCEN Form 114 when aggregate foreign account value exceeds $10,000 during the year, due April 15 with automatic extension to October 15, and it is not filed with the IRS. Form 8938 is an IRS filing for specified foreign financial assets above reporting thresholds, including references to at least $50,000 for certain U.S. taxpayers. Form 8938 does not replace FBAR, and neither replaces a BOIR.

Turn your memo, approval, and change-log requirements into an implementation checklist with Gruv docs.

Run change control so search-snippet drift does not break compliance#

Rule drift is a control risk, so treat BOI logic as dated legal guidance and anchor decisions to current FinCEN primary sources. This is where good teams separate a filing rule from a search result and keep routine work moving while edge cases go to review.

| Control step | What to do | Record or check |

|---|---|---|

| Monitor official sources | Base each check on FinCEN releases, the BOI E-Filing alert page, filing instructions, and the underlying rule text | Flag conflicts across official pages |

| Stamp every interpretation | Include the exact source set and an as-of timestamp | Verify the timestamp predates approval and matches the saved source version in the entity file |

| Pause ambiguous edge cases | Pause new edge-case classifications while legal reviews revised criteria and keep routine cases moving where criteria are still clear | Log the trigger that caused the pause |

| Track operational fallout separately | Separate reclassifications, pending BOIR tasks, and internal payout-hold decisions into distinct queues | Record the new classification, whether BOIR action is required, and who cleared or maintained any hold |

- Monitor official sources and flag cross-source conflicts.

Base each check on FinCEN releases, the BOI E-Filing alert page, filing instructions, and the underlying rule text, not reposted summaries. As of March 26, 2025, FinCEN narrowed reporting to entities previously defined as foreign reporting companies, while the IRS BOI page still described broader reporting language for some U.S.-created or registered entities. Flag conflicts across official pages, not just edits within a single page.

- Stamp every interpretation with an as-of date.

Every BOI or UBO interpretation used by onboarding, risk, or payouts should include the exact source set and an as-of timestamp. FinCEN's filing instructions state they may be revised and direct users to the latest BOI page, so undated interpretations become weak evidence when guidance changes. Verify that the timestamp predates approval and matches the saved source version in the entity file.

- Pause ambiguous edge cases when guidance conflicts.

If new guidance conflicts with current logic, consider pausing new edge-case classifications while legal reviews revised criteria. Keep routine cases moving where your criteria are still clear. Freeze only the ambiguous queue and log the trigger that caused the pause.

- Track operational fallout separately from BOIR filing triggers.

Separate reclassifications, pending BOIR tasks, and internal payout-hold decisions into distinct queues. Under 31 CFR 1010.380, an updated BOIR is due within 30 calendar days when previously submitted required information changes, so confirm whether a filing trigger exists versus an internal policy cleanup. For each affected entity, record the new classification, whether BOIR action is required, and who cleared or maintained any hold.

Choose the lightest model that is still defensible#

Start with the rule that exists now, then add controls only where the risk justifies them. In practice, we recommend getting entity scope right under current FinCEN BOI rules before you add heavier pre-payout checks.

1. Reporting-only minimum#

Use a reporting-only minimum when entity classification is stable and your onboarding mix is mostly low-complexity. Under the March 26, 2025 interim final rule, BOI reporting was narrowed to entities previously defined as foreign reporting companies (with limited exceptions), while entities previously defined as domestic reporting companies were exempted.

The key control is a documented scope decision for each entity, not broader data collection. Keep the formation or registration facts reviewed, the approver, and the as-of date of the rule text in the record. If the entity is in scope, file through the FinCEN BOI E-Filing System.

2. Add pre-payout escalation only where timing risk is real#

If you onboard entities that may fall within foreign reporting company scope, or the facts are unclear, add an escalation gate before payout release. This keeps controls light while still covering short filing windows. Entities that become reporting companies on or after March 26, 2025 have a 30-calendar-day initial filing window, and required BOI changes have a 30-calendar-day update window.

Use a clear trigger: if scope or filing status cannot be confirmed before release, pause payout and escalate. Your evidence pack should show what changed, when it changed, who reviewed it, and whether BOIR was filed or not required.

3. Version the rule baseline because it can move#

Keep this control set adaptive. The March 2025 revision was issued as an interim final rule with a request for comments. Your process should include versioned source capture and periodic review, not a one-time interpretation.

A lean, defensible package should include the entity-scope memo tied to current FinCEN rule text, the BOIR decision and, if filed, the filing confirmation reference, the escalation trigger used before payout release, and a dated change-review note when FinCEN guidance or counsel interpretation changes.

If you are deciding between models, choose the smallest one that can prove three points on demand. It should show why the entity was in or out of scope, whether any 30-day filing or update window applied, and who had authority to stop payout when the answer was unclear.

When your final model depends on release holds and escalations, align it with compliance-gated disbursement workflows in Gruv Payouts.

Frequently Asked Questions

Do U.S.-created entities still file BOI with FinCEN?

Confirm whether U.S.-created entities must file BOI with the relevant authority. What is confirmed separately is FBAR timing: certain U.S. individuals with signature authority but no financial interest have an extended FBAR due date of April 15, 2027, while other individuals with FBAR obligations remain due April 15, 2026.

Which entities are still likely to have BOI obligations after the 2025 rule changes?

BOI scope decisions after the 2025 rule changes require legal/compliance review. Confirm which entities have ongoing BOI obligations with the relevant authority.

Where do teams file a Beneficial Ownership Information Report in practice?

Confirm BOIR filing channels and submission procedures directly with FinCEN.

Why can Google snippets disagree with live FinCEN guidance?

This grounding pack does not address search snippets or BOI guidance-indexing behavior, so no conclusion is supported here.

What should a platform verify even when BOI reporting is not required?

Define platform UBO verification requirements and BOI-exemption documentation standards through internal policy and legal/compliance guidance.

When should legal escalation be mandatory for UBO scope decisions?

No regulator-defined mandatory UBO escalation trigger is supported in this grounding pack. For questions tied to the FinCEN notice in scope here, the notice points to fincen.gov/contact for the FinCEN Regulatory Support Section.

How often should compliance teams re-check BOI rules and internal decision logic?

No BOI review cadence is provided in this grounding pack. Do not treat any specific cadence as regulator-set based on this material.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- boiefiling.fincen.gov/resources/BOIR_Filing_Instructions.pdftrusted

- boiefiling.fincen.govtrusted

- bsaefiling.fincen.govtrusted

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalregister.gov/documents/2025/03/26/2025-05199/beneficial-o...trusted

- federalregister.gov/documents/2022/09/30/2022-21020/beneficial-o...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Beneficial Ownership Verification for Platforms and UBO Rules That Control B2B Payout Risk

Treat UBO verification as part of payout release, not as a compliance file that gets archived after onboarding. If you pay contractors, sellers, or creators across markets, the wrong ownership model can create two immediate problems: higher AML/CFT risk and payout delays when an entity cannot be explained well enough to pass review.

Beneficial Ownership Collection in Marketplace Onboarding Without Conversion Loss

For **beneficial ownership collection in marketplace onboarding**, the real question is not whether you need one more form. It is whether you can explain who owns or controls the business before you activate it, enable payouts, or defend the decision later. If you treat ownership data as only a filing issue, you will either slow down good users with unnecessary asks or approve risky ones without a clean evidence trail.

Beneficial Ownership Reporting in 2026 for FinCEN BOI Decisions

Use this as an execution guide, not a legal memo. Your job is to make a current BOI decision, document why you made it, and avoid cleanup later. The outcome is straightforward: confirm whether your entity is in scope, prepare what you need if it is, and keep dated proof of the basis you used.