Quick Answer

Use compatible or bridging software first, then move to direct HMRC API work once your controls survive period close. The immediate goal is compliant filing for VAT-registered businesses under Making Tax Digital for VAT, which has applied to all VAT-registered businesses since April 2022. Build one period file with reconciliations, approver actions, filed values, and HMRC receipt confirmation. Since 1 November 2022, quarterly and monthly returns cannot go through the old VAT online account.

Why MTD for UK VAT Needs Both Speed and Control#

If you operate a platform and need to automate UK VAT reporting, the practical path is usually staged. Get MTD-compliant filing working first with compatible software. Then add deeper automation once you can show your digital records tie to submitted VAT return totals.

HMRC's baseline is clear. Making Tax Digital for VAT requires VAT-registered businesses to keep VAT records digitally and file VAT Returns using software. HMRC policy wording says that since April 2022, all VAT-registered businesses have been required to keep digital records and file through MTD-compatible software. From 1 November 2022, quarterly or monthly VAT returns could no longer be sent through the old VAT online account.

- Start from the legal minimum

You do not need to begin with a custom HMRC API build to be compliant. HMRC allows either compatible software or bridging software that connects non-compatible tools, including spreadsheets, to HMRC systems.

- Plan for multi-owner accountability

This guide is for compliance, legal, finance, risk, and engineering owners who must ship automation and explain it to internal reviewers. A practical failure mode is not "the return would not send," but "the return sent and the team cannot show how totals were derived, who approved them, or what changed after an exception."

- Move from manual returns to checkpointed automation

This is an operating recommendation, not an HMRC rule. Start with a testable checkpoint: can you trace source transactions to return-ready totals and retain filing confirmation from your software? Then define exception handling. When totals do not reconcile or a submission is rejected, is there a named owner, a documented fix, and a record of what changed before resubmission?

Official wording is not perfectly aligned across pages. A UK government API catalogue page says below-threshold businesses can use VAT MTD voluntarily, while HMRC policy and collection pages say all VAT-registered businesses should now be signed up for Making Tax Digital for VAT and file through compatible software.

This article takes the conservative operator view. If you are VAT-registered and automating UK VAT, design for MTD compliance and keep evidence that your software path is compatible with HMRC's digital reporting route.

The upside is practical. HMRC's policy note says users of compatible software have reported faster VAT return preparation and greater confidence in getting their tax right. The tradeoff is equally practical. Filing software can speed submission without fixing weak record-keeping, missing approvals, or poor exception handling. The sections that follow focus on the lightest path to compliance without creating hidden control risk.

How to choose an MTD acceleration path#

Choose the path that closes your immediate compliance risk first, then expand. In practice, that often means getting UK VAT filing working through MTD-compatible software, then deepening automation once the records and approvals are defensible.

- Set scope before choosing tooling

Separate two jobs: filing VAT returns under Making Tax Digital for VAT (MTDfV), and improving upstream VAT record-keeping. HMRC frames MTDfV as both digital record-keeping and return filing, so a clean submission layer does not fix weak records. If your immediate requirement is UK MTD filing, keep phase one narrow: compliant software filing, digital records for the UK VAT scope in question, and retained filing evidence.

- Choose by constraints, not preference

The available routes are compatible software, bridging software, and software that interacts directly with HMRC via the MTD APIs. HMRC allows hybrid setups across multiple products if they are digitally linked. Direct API integration is valid when your team can build and test against HMRC's developer flow, but it increases operational ownership. Also assign ownership for software access renewals, since authority can lapse after 18 months.

- If lineage is weak, start software-led

If you cannot clearly trace submitted totals back to source transactions, a direct API build is usually better as a later phase. A software-led route can limit initial build complexity while you fix traceability, approvals, and exception handling. This is also practical because, since 1 November 2022, regular VAT returns cannot be filed through the old VAT online account and must follow a supported software route.

- Be explicit about who this is not for

This path is not for teams seeking a one-off filing fix with no ongoing owner. Automation only holds if someone owns recurring review, exceptions, and evidence retention. Confirm scope before building: MTDfV includes defined exemptions in some cases, including insolvency procedures.

For a step-by-step walkthrough, see How Platforms Automate Pre-PO Approval with Purchase Requisitions.

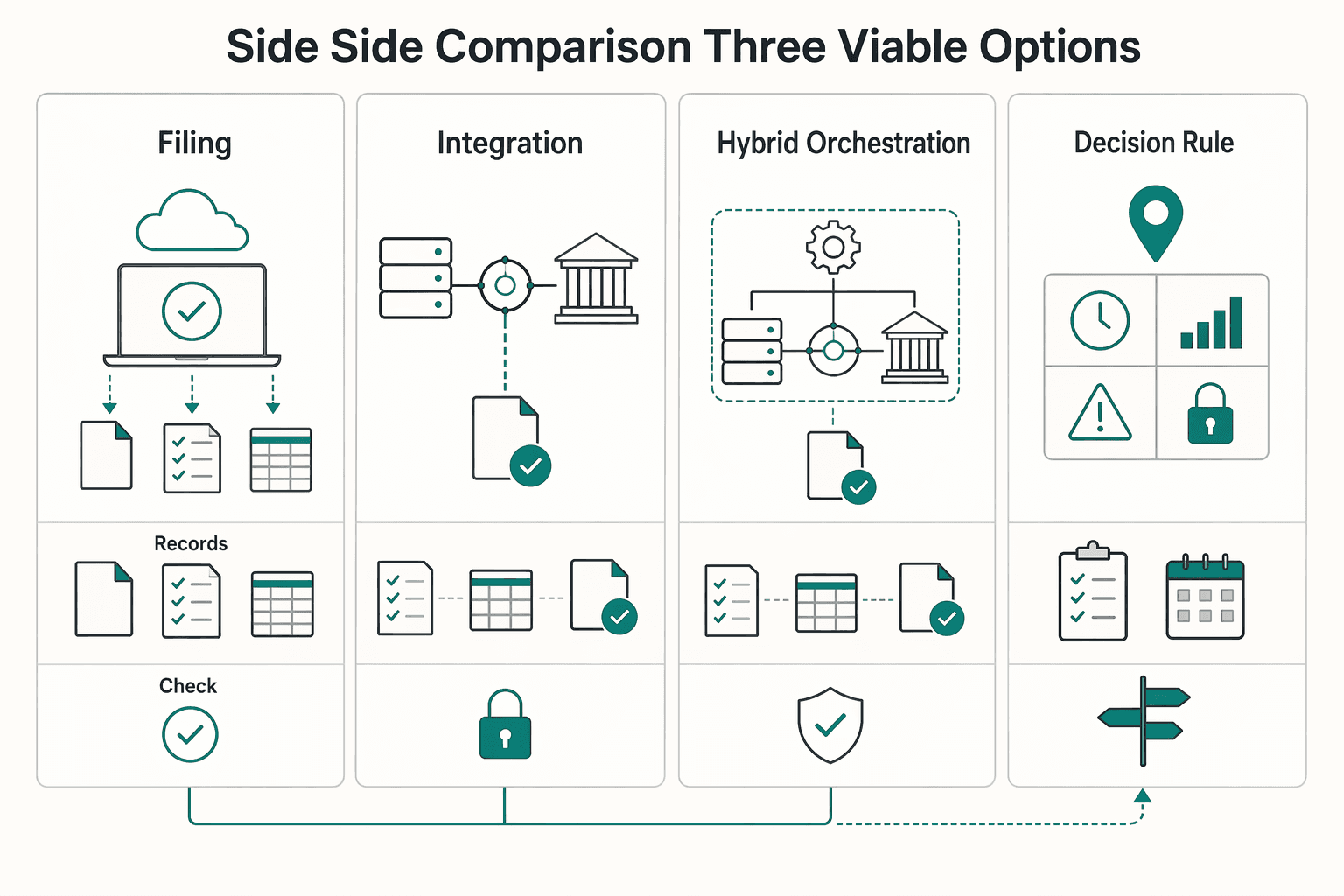

Side by side comparison of the three viable options#

For UK VAT filing under Making Tax Digital for VAT (MTDfV), choose the route based on ownership as much as tooling. A software-led or bridging route can be practical when filing continuity is urgent and controls are still maturing. Direct API or hybrid can fit teams that want more internal ownership and can operate it reliably.

HMRC's baseline stays the same across routes. Businesses in scope must keep digital VAT records and file VAT Returns using software, including software that communicates with HMRC through its API platform. What changes is who owns validation, exception handling, and audit evidence assembly.

| Option | Best for | Control depth | Implementation effort | Failure visibility | Dependency risk | Audit evidence quality for MTDfV |

|---|---|---|---|---|---|---|

| Off-the-shelf filing software | Teams that need a compliant filing path within vendor workflows | Vendor-defined controls, plus your internal review steps | Product setup, process design, and evidence export procedures | Usually clear submission status in-product; external lineage depends on exports | Vendor dependency | Strong when you retain submission confirmations, return outputs, and approval records |

| Direct HMRC API integration | Engineering-led teams that want custom validation, routing, and telemetry | Defined by what you design, monitor, and enforce | Build, test, operate, and evidence-capture responsibilities stay in-house | Strong only if requests, responses, errors, and reconciliations are fully instrumented | Internal ownership dependency | Strong only if payload lineage, approvals, and HMRC outcomes are archived together |

| Hybrid orchestration | Teams that need compliance now with phased internal control expansion | Split across vendor and internal components | Ongoing alignment across two operating layers | Split unless tool events and internal checks are joined per filing period | Dual dependency (vendor + internal) | Strong only when cross-system evidence is tied to the same period record |

| Decision rule | If filing continuity is urgent and controls are still maturing, a software-led route is often practical; API or hybrid can fit teams that want more internal ownership. | Match route to current control maturity | Do not build past your ability to support period close | Visibility matters only if exceptions are reviewed each period | Accept dependency only with explicit ownership | Evidence quality depends on process discipline, not product label |

1. Off-the-shelf filing software#

Use this route when finance needs a predictable filing path this period and engineering capacity is limited. HMRC's software guidance (last updated 1 May 2025) describes compliant routes as a compatible software package or bridging software, so this is often a practical path to MTDfV filing operations.

Sage is a representative software-led pattern because its public guidance shows a concrete "Creating and submitting an MTD for VAT Return using Sage Accounting" flow. Deloitte ITC is another representative pattern. Deloitte describes ITC as MTDfV-compatible and states it runs 40 standard data tests, with 35+ embedded quality checks cited elsewhere in Deloitte materials.

Checkpoint: confirm you can retrieve period figures, submission confirmation, and approver trail without manual reconstruction. A common gap is treating a vendor "submitted" status as complete evidence when reviewers still need traceability back to digital records.

2. Direct HMRC API integration#

Use direct API when you need to own validations, exception routing, and observability instead of relying on a vendor-defined submission flow. HMRC's API page states software can "interact directly with our systems via the MTD APIs," so this is a valid path when you can support the operational controls around it.

The key tradeoff is ownership, not automatic quality. You control how returns are assembled, what checks run, how failures are escalated, and what evidence is retained. richpeck/vat-mtd on GitHub is a representative code-level pattern because it is described as a "Ruby implementation of HMRC's VAT (MTD) API," but it is not official product guidance.

Checkpoint: prove a clean chain from source totals to submission artifacts and HMRC outcomes. The common failure mode is building the submission call but underbuilding the review and evidence layer.

3. Hybrid orchestration across software and API#

Use hybrid when you need near-term filing stability and a staged move to more internal controls. HMRC explicitly includes a bridge-style path via "bridging software to connect non-compatible software (like spreadsheets) to HMRC systems," which supports split operating models.

The practical advantage is phased ownership. Keep vendor-led filing for current cycles while moving higher-risk checks, reconciliations, or approval logic into internal systems over time.

Checkpoint: stitch evidence across systems for each VAT period so tool output, internal validation results, and HMRC acceptance clearly map to the same filing record. The common failure mode is split visibility, where teams see different statuses and cannot prove which approved figures were filed.

Option 1 Use MTD software first#

Use this option when your immediate goal is a compliant MTDfV filing process through an existing software workflow, rather than building and operating your own HMRC API integration.

- Best fit

HMRC's baseline is fixed: all VAT-registered businesses should now be signed up for Making Tax Digital for VAT, and VAT Notice 700/22 requires digital record-keeping and software-based VAT Return filing. If you need an operating route now, software-first can be a practical starting point.

- What this route includes

HMRC's compatible software guidance (last updated 1 May 2025) sets out two paths: a compatible software package or bridging software for non-compatible tools such as spreadsheets. That means you may be able to run MTDfV without rebuilding your full tax data stack first, provided you keep a clear chain from digital records to the filed return.

- Representative patterns

Sage is a filing-led example: its VAT page says you can "Submit your VAT return directly to HMRC." Deloitte ITC is a tax-compliance-led example: Deloitte states ITC is compatible with MTDfV and runs 40 standard data tests.

- Control checks before you commit

A prebuilt software route can reduce implementation work for filing to HMRC. You still need to verify that review, exception handling, and evidence capture fit the product's operating model. Before you commit, verify in the live product that you can:

- Retain or export the period figures that were filed.

- Preserve HMRC acceptance or rejection outcomes.

- Show approver actions without reconstructing from side channels.

- Manage HMRC software authorisation renewal, which HMRC says lasts 18 months.

One risk is treating a vendor "submitted" status as complete evidence. Keep a single period file that ties reviewed figures, approvals, filed values, and HMRC outcome to the same VAT period.

Option 2 Build direct HMRC API integration#

Choose direct HMRC API integration when you need more control over how VAT filings are prepared and submitted in your own systems. Under Making Tax Digital for VAT (MTDfV), VAT-registered businesses must keep records digitally and file VAT Returns using software, and that software communicates with HMRC through its API platform.

- Best fit

This route can suit teams that want clearer internal evidence of how filed figures were produced, checked, approved, and submitted. Since 1 November 2022, HMRC says routine quarterly or monthly VAT Returns can no longer be sent through the old VAT online account, so software-based filing is the operating path.

- Reference implementation only

Use richpeck/vat-mtd on GitHub as a reference point for request flow and client structure. Treat it as an example implementation, not evidence of HMRC approval or production readiness for your environment.

- What production design should include

HMRC provides a sandbox endpoint (https://test-api.service.hmrc.gov.uk) and a production endpoint (https://api.service.hmrc.gov.uk), with guidance to integrate and test in sandbox before live use. In practice, teams often include:

- Environment separation: isolate sandbox and production credentials, endpoints, and logs.

- Submission evidence: retain filed figures, approver record, and HMRC acceptance or rejection outcome for each VAT period.

- Fraud-header handling: capture and transmit all available fraud header information with related tax information, as required by HMRC's direction.

- Failure traceability: record validation failures, API errors, and resubmissions so finance and engineering can trace each return period.

- Main tradeoff

The advantage is greater control in your own process design. The tradeoff is ongoing ownership: API maintenance, compliance review, and period-close evidence retention need clear accountable owners before go-live.

Related reading: India Equalisation Levy: What Foreign Platforms Must Pay on Digital Advertising Services.

Option 3 Run a hybrid model#

A hybrid model can be a practical path when you need MTDfV filing live soon but want stronger in-house controls over time. Start with software-led submission, then move high-risk controls, such as validation, exception routing, and evidence capture, into your own HMRC API layer as operations stabilize.

HMRC's baseline does not change in this model. VAT-registered businesses must keep records digitally and file VAT Returns using software, and that software communicates digitally with HMRC through the API platform. Hybrid changes where controls sit first, not the requirement itself.

- Use compatible or bridging software as the submission shell

Use a compatible software package, or bridging software if finance still prepares figures in spreadsheets. HMRC allows both routes, which lets you meet filing requirements while upstream data and process controls are still maturing. Deloitte's MTDfV options page shows this spreadsheet-retention pattern, but it is dated 13 Mar 2019, so treat it as an example pattern, not current product validation.

Track software authority as an operational control: HMRC states the authority lasts 18 months. If that authority lapses, submissions may be interrupted even when figures are correct.

- Migrate high-risk logic before final filing

Once submission is stable, move the controls most likely to create filing risk into your own application layer first, such as validation rules, reconciliations, exception categorization, and approval evidence. Use HMRC Developer Hub materials and reference implementations like the Ruby-based richpeck/vat-mtd repository to understand API flow, while software continues to submit live returns.

Avoid split-truth operations. For each VAT period, define one source of truth and keep one evidence pack: source totals, adjustments, approver record, software output, and HMRC acceptance or rejection outcome.

- Treat governance as the main hybrid cost

Hybrid can reduce cutover risk, but it adds governance overhead across compliance, finance, and engineering. If ownership is unclear, you can end up with two partial processes and weak auditability.

Also handle scope decisions carefully. The API Catalogue says below-threshold use is voluntary, while HMRC VAT guidance says VAT-registered businesses below the threshold also had to follow MTD rules from 1 April 2022. Resolve that conflict against current guidance and take specialist advice where needed.

Control checkpoints before you automate filing#

Do not enable automated filing until three checks pass: accountability, data lineage, and go/no-go gates. Under Making Tax Digital for VAT, VAT-registered businesses must keep records digitally and file VAT returns using software that communicates with HMRC through the API platform. Since November 2022, MTD software has been the only VAT filing portal route, so control weaknesses can quickly become operational risk.

| Checkpoint | What to confirm | Key detail |

|---|---|---|

| Accountability | Show who prepares figures, who approves the return, who can stop submission, and who retains period evidence | Assign responsibility for VAT record-keeping quality, draft return quality, and submission operations. |

| Data lineage | Run an end-to-end walkthrough from source transactions to return totals and back again | Digital link requirements applied for VAT periods beginning on or after 1 April 2021, and HMRC says you cannot manually transfer linked VAT data, including copy-paste, between software. |

| Go/no-go gates | Do not auto-submit when reconciliation does not tie, material exceptions remain unresolved, or period records cannot be produced digitally | Confirm the filing method returns HMRC receipt confirmation and store it with period evidence. |

- Set a minimum accountability layer before the first live return

The cited HMRC guidance does not prescribe a specific internal org chart, but you still need clear ownership, approval, and evidence retention before automation starts. If you cannot show who prepares figures, who approves the return, who can stop submission, and who retains period evidence, you are not ready.

Keep the model practical: assign responsibility for VAT record-keeping quality, draft return quality, and submission operations, including engineering or external tooling where relevant. One person can hold multiple roles in smaller teams, but approval should still be explicit and documented.

Retention should cover both records and decisions. Records in the electronic account must be kept digitally in functional compatible software, and they should be complete, up to date, and sufficient to calculate VAT correctly. For each period, you should be able to retrieve return-ready totals, reconciliation output, approver records, and software receipt confirmation.

- Prove data lineage from source transaction to VAT return totals

Before automating, run an end-to-end walkthrough from source transactions to return totals and back again. This is the control that separates "we can submit" from "we can explain the submission."

Use a representative sample and trace where data enters the chain, how VAT treatment is applied, how adjustments are made, and how values flow into return totals. Test both directions: transaction-to-box total and reported total-to-source records.

Be strict on transfer method. Digital link requirements applied for VAT periods beginning on or after 1 April 2021, and HMRC says you cannot manually transfer linked VAT data, including copy-paste, between software. If your process depends on manual rekeying or disconnected spreadsheet steps, fix that first.

- Define go/no-go gates before live submission starts

Write submission gates before deadlines create pressure. HMRC does not publish a universal numeric threshold for unresolved exceptions or reconciliation breaks, so set internal tolerances and apply them consistently.

At minimum, do not auto-submit when reconciliation does not tie, material exceptions remain unresolved, or period records cannot be produced digitally. Define "material" in advance and document it.

If a gate fails, use controlled manual review: named reviewer, correction within the compatible software chain, rerun reconciliation, and record the reason for change. Avoid workaround filing through final manual copy steps.

Include one technical gate: confirm the filing method returns HMRC receipt confirmation and store it with period evidence. Software should provide receipt confirmation after filing, and that evidence should remain retrievable for compliance checks. If underpaid tax is identified, payment can be required within 30 days.

Tighter gates may slow early automated periods, but loose gates create higher risk: faster filing with weak evidence. If reconciliation breaks or exceptions accumulate, pause automation for that period and revert to controlled manual review.

Before you lock in software, API, or hybrid, map your approval gates and evidence flow first, then pressure-test implementation paths in the Gruv docs.

Operating sequence for each VAT period close#

Use a repeatable close sequence: fix the period scope, reconcile first, run explicit approvals, submit, then confirm receipt before the usual deadline of one calendar month and 7 days after period end.

| Step | Action | Record or note |

|---|---|---|

| Lock the period | Record the cutoff time, included ledgers or exports, and any items held for review | If you are VAT-registered, you still submit a VAT Return even when there is no VAT to pay or reclaim. |

| Reconcile first | Tie source transactions to the VAT account, review adjustments, and only then generate the draft in functional compatible software | If you cannot explain return totals back to source records, stop and resolve that gap first. |

| Role gates | Define an internal role model and apply it consistently before submission to HMRC | A practical split is finance for numbers and reconciliation, compliance for VAT treatment or policy alignment, and a tooling owner for submission-path integrity. |

| Verify acceptance and archive | Confirm the software receipt that HMRC received the return, then archive the period evidence | Keep the archive practical: submitted return, approved draft, reconciliation outputs, approval record, receipt confirmation, and correction notes. Preserve VAT records for the required period, which can run up to 6 years. |

- Lock the period before anyone builds the return

Start with a real cutoff for which transactions are in scope for that VAT period. HMRC does not require a step named "freeze period inputs," but your records still need to be complete, up to date, and sufficient to calculate VAT correctly under Making Tax Digital for VAT (MTDfV). Record the cutoff time, included ledgers or exports, and any items held for review.

Include nil periods in the same control path: if you are VAT-registered, you still submit a VAT Return even when there is no VAT to pay or reclaim.

- Reconcile tax-relevant transactions before generating draft VAT returns

Reconcile before you optimize filing mechanics. Tie source transactions to the VAT account, review adjustments, and only then generate the draft in functional compatible software. If you cannot explain return totals back to source records, stop and resolve that gap first.

Keep records and filing in compatible software through to final submission.

- Use role gates before the HMRC submission step

The submission step requires an explicit declaration that the return is correct and confirmation to submit to HMRC. HMRC does not prescribe your internal role model, so define one and apply it consistently.

A practical split is finance for numbers and reconciliation, compliance for VAT treatment or policy alignment, and a tooling owner for submission-path integrity via your filing software connected to HMRC's MTD APIs.

- Verify acceptance, then archive enough to defend the period

After submitting, confirm the software receipt that HMRC received the return, then archive the period evidence. Do not treat "sent" as complete until receipt is confirmed.

Consider setting named owners and internal SLAs for rejected submissions, mismatched totals found before filing, and errors found after filing. For post-filing errors, move to the formal correction process. Leaving errors uncorrected can create penalty and interest exposure.

Keep the archive practical: submitted return, approved draft, reconciliation outputs, approval record, receipt confirmation, and correction notes. Preserve VAT records for the required period, which can run up to 6 years.

Red flags that mean you should slow down#

If any of these are true, pause acceleration. These are UK VAT control risks, not just tooling gaps.

- You cannot trace return totals back to source records

Stop if you cannot explain a VAT return number from source transactions through to the submitted return. MTDfV requires digital VAT records and digital links from sales or purchase ledger data to VAT Return submission, so broken lineage can mean reconciliation is not ready for more automation.

Quick test: take one box total and rebuild it from the period data and adjustments used for that return. If the trail breaks, fix lineage before increasing HMRC API submission volume.

- Your team treats software output as final

Slow down when draft output is accepted without challenge before submission. Functionally compatible software can prepare and submit, but the submitter still has to declare the information is correct and confirm submission to HMRC.

Responsibility also stays with the business even if an agent files on your behalf.

- Exceptions are piling up and nobody can size the exposure

A growing exception queue is a filing-risk signal when no owner can quantify which periods or returns may be affected. Pause, assign ownership, and quantify impact before scaling automation.

Since 1 January 2023, late VAT returns add penalty points (annually 2, quarterly 4, monthly 5), and reaching the threshold triggers a £200 penalty. Since 1 November 2022, the existing VAT online account cannot be used to submit quarterly or monthly VAT returns.

- You are expanding markets and reusing UK logic by default

Treat this as a stop signal: this MTDfV guidance is UK HMRC-specific. If you expand into other jurisdictions, do not assume the same record rules, submission path, or evidence expectations apply unchanged.

Reuse architecture where it helps, but validate legal and reporting controls market by market.

Evidence pack to keep for audits and internal risk review#

Keep an evidence pack as a live filing control. The material here supports Self Assessment filing operations, not a full VAT/MTD evidence standard, so use it as a practical minimum set.

- Period file tied to each filing

Create one file for each return cycle and update it during preparation and submission. Include the underlying records used to prepare the return, such as bank statements or receipts, plus artifacts from the online service such as prior returns and tax calculation outputs where available.

- Route and access decisions log

Record any filing-route exceptions that change how you submit, including when the online service cannot be used and commercial software or other forms are required. Also log account-access issues that can delay filing, such as needing to reactivate an existing account.

- Deadline and penalty risk notes

Keep a clear record of the relevant filing and payment dates in your workflow, and note that missing the return deadline can lead to penalties. Where official pages show timing differences, for example references to filing after 5 April versus on or after 6 April, flag that for verification before relying on one date in controls.

If you can only improve one thing this quarter, make the period file complete and repeatable first. For related context, see HMRC Reporting Rules for Platforms for UK Marketplace Operators.

Conclusion#

Choose the route that matches your current control maturity, not the one that looks most advanced. For MTDfV, HMRC's baseline is digital VAT records and VAT Returns filed through compatible software, including software that connects through HMRC APIs.

- Start with compliance you can evidence

If you still rely on manual reconciliation, copy and paste between tools, or person-specific handoffs, a software-led route can be a practical first step. The key test is not technical ambition. It is whether you can show a clean, reproducible path from source records to submitted VAT figures.

- Deepen automation after filing is repeatable

A staged sequence is often practical: stabilize filing, prove controls, then expand automation where volume and risk justify it. HMRC's final evaluation (published 27 February 2025) reported that around 60% found their first MTD submission easy, rising to over 70% for ongoing submissions. That supports a measured ramp, not a forced big-bang rebuild.

- Use period evidence as the go/no-go check

Before adding complexity, make sure each period leaves a defensible record: reconciliation, approval, submission event, and software confirmation of receipt. HMRC states that after submission, confirmation is provided through the software. If you cannot reliably reproduce how totals were prepared and accepted, keep strengthening controls before moving to deeper integration.

HMRC phased mandation from April 2019 for VAT-registered businesses at or above the £85,000 taxable turnover threshold, then from April 2022 for VAT businesses below that threshold. The operating question now is how much of the digital filing chain you should own directly, and when.

If you want to turn this staged VAT control model into an executable rollout plan with clear ownership, start with a focused implementation discussion.

Frequently Asked Questions

What does Making Tax Digital for VAT (MTDfV) require from platform operators in practice?

If you are VAT-registered, HMRC says you should now be signed up to MTD for VAT. In practice, that means keeping VAT records digitally and filing VAT Returns through software that communicates with HMRC via API. If you use more than one product, the transfer between them must be a digital link, not manual copy and paste.

What is usually the fastest compliant route for UK VAT reporting: software, HMRC API, or hybrid?

There is no public HMRC benchmark proving one route is fastest for every platform. If your immediate gap is compliant filing, a common route is compatible software, including bridging software where appropriate, and the old VAT online account route for quarterly or monthly returns ended on 1 November 2022. Direct API or hybrid routes are planning choices, not publicly benchmarked speed winners.

Which controls are mandatory before automating VAT returns?

The legal baseline is digital records, software-based filing, and digital links where multiple tools are used. You should also be able to trace return totals back to source records and reproduce that path, because HMRC may check records to confirm the right tax was paid. If reconciliation cannot be reproduced, your control position may be weak even if a return was submitted.

Who should own each step of submission, approval, and exception handling?

HMRC does not prescribe a fixed internal ownership model, so you need to define one and keep it stable. At minimum, assign clear owners for preparation, filing approval, and exceptions such as rejected submissions, broken digital links, or software authority issues. Track software authority status as an operational control, since HMRC says that authority typically lasts 18 months.

What should trigger escalation to specialist VAT counsel instead of internal handling?

Escalate when the issue depends on legal scope, exemption, or conflicting HMRC statements rather than routine filing operations. Typical triggers include applying for an MTDfV exemption because digital tools are not reasonable or practical, or relying on mandation wording that differs across sources. If you apply for an exemption, continue filing as usual until HMRC sends its decision.

What evidence should we retain to defend our HMRC filing process?

Keep the digital records used for the return, the reconciliation to VAT figures, approval records, submission confirmations, and software sign-up or authority records. Retention should align with VAT record-keeping expectations, which are generally at least 6 years. Your strongest pack shows the full digital path from source data to submitted return, especially when multiple systems are involved.

Which claims about implementation speed, integration depth, and effort are still unknown from current public sources?

Public sources do not provide definitive delivery-time benchmarks across compatible software, direct HMRC API builds, and hybrid models. They also do not provide reliable fixed estimates for engineering effort or failure rates by route. Open-source examples such as richpeck/vat-mtd should be treated as exploratory references, not production benchmarks.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- api.gov.uk/hmrc/vat-mtdtrusted

- accountingweb.co.uk/tax/business-tax/mtd-digital-links-mandated-...external

- deloitte.com/uk/en/services/tax/research/what-are-my-mtd-...external

- deloitte.com/uk/en/services/tax/services/indirect-tax-com...external

- github.com/richpeck/vat-mtdexternal

- gov.uk/guidance/find-software-thats-compatible-with...external

- gov.uk/government/publications/vat-notice-70022-mak...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Making Tax Digital for Income Tax for UK Freelancers: Who Needs It and When

Making Tax Digital for Income Tax is moving into mandatory rollout, not just sitting on the list of future admin changes. Some sole traders and landlords must use it from **6 April 2026**. Your immediate job is to confirm whether you are in scope, get your digital records into shape, and avoid a rushed software switch.

Making Tax Digital for Income Tax and UK Platform Operators: Confirmed Rules and Open Scope Questions

For platform operators, the first useful move is to separate confirmed HMRC and GOV.UK statements from scope assumptions. Most public guidance on Making Tax Digital for Income Tax is written for sole traders, landlords, and their agents, not for platform operators as a distinct audience.

VAT for UK Freelancers Without Filing Surprises

If you want a low-stress approach to **vat for uk freelancers**, start with an HMRC-first baseline. Think of compliance as a series of decisions backed by records, not a setting inside your invoicing tool.