Quick Answer

Use a three-layer sequence: lock kickoff behind a signed agreement and named SOW, send invoices that meet AP requirements with verified jurisdiction wording, then choose liability ownership before volume grows. For cross-border Payment Protection & Finance, connect each invoice to a deliverable, approval record, and acceptance evidence in your project file. That sequence cuts preventable rejections, shortens collection delays, and gives you a clearer escalation path when approvals or funds stall.

Why Traditional 'Payment Protection' Fails the Modern Professional#

Traditional payment protection is often too reactive for cross-border independent work. The real risk is usually operational: late or missing payment, invoice-validity issues, payment-rail friction, and fees that reduce your margin after settlement.

For many independent professionals, that is not an edge case. In EU commercial transactions, one out of two invoices are paid late or not at all, and one in four bankruptcies are linked to invoices not being paid on time. Legal remedies can matter, but they still come after the delay has already affected cash flow. For example, UK statutory late-payment interest (8% plus the Bank of England base rate) applies only after a payment is late.

| Question | Legacy protection approach | Revenue security operations |

|---|---|---|

| Main trigger | Reacts after loss or non-payment | Reduces risk before work starts and at each billing point |

| Coverage gap | May not address invoice-quality failures, rail delays, or fee stack | Depends on your process discipline and payment design |

| What you can control | Limited once the problem appears | Contract execution, invoice quality, payment rail choice, and fee-aware pricing |

If you run a multi-client pipeline, you can deliver on time and still be paid late. Delays can stem from invoice handling, processing constraints, or cross-border friction around cost, speed, access, and transparency. In EU B2B workflows, invoices are generally required for VAT purposes, and invoice quality affects tax treatment, so this is a control point, not just admin polish.

Fee drag is another operational risk. Card and processor pricing can include base fees plus international and currency-conversion add-ons, so headline project price is not the same as settled net. Treat payment protection as a three-layer approach you control, not a fallback product you reach for after the damage is done.

Layer 1: Forge Your Contractual Armor#

Start at signature stage: make required documents and payment terms explicit before work starts.

1. Get commitment before kickoff#

Define kickoff conditions in writing and place them in the signed contract set. In regulated contexts, a missing required document can cause a formal failure outcome, so treat required items as true gates.

Use plain language such as: "Work begins only after the signed agreement is returned and all required start conditions are met, including any agreed start payment."

This material does not support a standard freelancer deposit percentage, so set that amount separately based on your policy and jurisdiction.

Before you schedule production, confirm you have:

- signed agreement

- named SOW version

- proof that any contract-required start condition was met

2. Define scope so billing triggers are unambiguous#

A vague SOW creates vague billing rights. Write it like an execution record, not a promo summary.

FAR Part 52 highlights a core control: clauses and provisions should be clearly incorporated and modified through explicit procedures. In private contracts, mirror that discipline by naming exact documents, versions, and trigger language.

At minimum, specify:

- deliverables by name and format

- approval points tied to deliverables

- how contract terms are incorporated (document name/version)

- how updates are documented when terms change

If you bill by milestone, define the trigger and invoice event in the same clause. This material does not provide freelancer-specific milestone wording, so your exact phrasing remains policy-specific.

| Weak contract language | Protective contract language |

|---|---|

| "Website design project." | "Deliverables are those listed in SOW v3 dated [date], incorporated into this agreement." |

| "Payment due during the project." | "Invoice events occur only at the written triggers defined in the incorporated SOW." |

| "Extra terms are in email." | "Only terms included in the signed contract set apply to this project workflow." |

| "We can adjust scope later." | "Scope changes require a written change record before related work starts." |

3. Control change orders before work expands#

Scope change is normal. Unpriced, undocumented scope change increases delivery and billing risk. Use one rule: anything outside the current SOW needs a written change record that states scope and timing effects; include fee impacts if your policy requires it.

Keep a single audit-trail folder with:

- signed agreement

- current SOW version

- approved change records

- delivery records

- approval messages

In practice, if a clause or required document is not clearly incorporated, treat it as missing.

4. Run a pre-sign check#

Use a formal checklist before kickoff, similar to a compliance-worksheet discipline: required documents, incorporated versions, and trigger conditions should all be verifiable.

| Check | What to confirm |

|---|---|

| Client legal name and billing contact | Correct client legal name and billing contact |

| SOW title and version date | Attached SOW title and version date |

| Start conditions | Explicit start conditions |

| Invoice triggers | Invoice triggers that can be verified |

| Approval points and approver | Approval points and approver |

| Method for documenting scope changes | Written method for documenting scope changes |

Use the table above as your pre-sign checklist. If any item is unclear, fix it before work starts. This layer helps reduce preventable disputes by making required terms explicit and verifiable. Next, make sure your invoice reflects these terms exactly.

Layer 2: Engineer a Bulletproof Invoicing Engine#

A clear contract does not save an invoice that AP cannot process. Your invoice should execute the deal you already protected in the contract.

1. Start with compliance checks#

For cross-border B2B work, build one master template. Then verify legal and tax details before each send instead of filling them from memory.

| Invoice item | Verify before send |

|---|---|

| Your legal business name and address | Your legal business name and address |

| Client legal entity name and billing address | Client legal entity name and billing address |

| Unique invoice number and invoice date | Unique invoice number and invoice date |

| Service period or delivery date | Service period or delivery date |

| Deliverable reference that matches the signed SOW version | Deliverable reference that matches the signed SOW version |

| PO number, vendor number, or internal billing code | If required |

| Tax registration fields | After jurisdiction check |

| Jurisdiction-specific invoice wording | Wording pending contract and tax review |

| Payment method details | Exactly as the client must use them |

| Billing contact and AP submission route or portal | Billing contact and AP submission route or portal |

Use the table above as your pre-send checklist. If you invoice into the EU, use the European Commission eInvoicing Implementation Checklist as a checkpoint, then verify jurisdiction-specific legal and tax wording before you send.

2. Tie each invoice to proof#

Bill against evidence, not vague phases. Each invoice should map to one deliverable, one approval event, and one payment trigger.

Use this structure:

- Invoice 1: kickoff; payment split pending signed agreement verification; trigger is signed agreement + final SOW attached.

- Invoice 2: named interim deliverable; payment split pending signed agreement verification; trigger is written approval in email or your project system.

- Invoice 3: final handoff; payment split pending signed agreement verification; trigger is delivery of the agreed final files/package.

| Common invoice rejection reason | Preventive fix you control |

|---|---|

| Client name does not match legal entity or vendor record | Copy legal entity details from signed agreement or vendor onboarding record |

| Missing PO number, vendor code, or AP route | Confirm AP submission instructions before kickoff and store them with project docs |

| Description is too vague | Reference exact SOW version, deliverable name, and service period |

| Tax text or registration detail is incomplete | Keep tax wording pending review, then replace it with verified jurisdiction wording before send |

| Payment details are unclear or outdated | Maintain one approved payment block in your template and re-confirm before issuing |

3. Run a receivables cadence#

Collections slow down when reminders depend on memory. Use a fixed sequence: pre-due reminder, due-date reminder, overdue escalation, then pause or escalate if unpaid. Keep reminders neutral and in the same thread as the original invoice.

Assign one owner to each stage. Handoff gaps are a common failure point, and poor coordination can turn into month-end blame instead of mid-week fixes.

As volume grows, look for receivables tools with capabilities such as Collections Automation, Payment Portal, Automatic Reconciliation, and Dashboard & Reporting.

4. Do a final readiness check#

Before sending, confirm:

- invoice matches the signed SOW version and milestone trigger

- client legal name, PO details, and AP route are correct

- jurisdiction-specific tax wording is verified or clearly flagged for hold

- payment instructions are current

- delivery and approval evidence is saved in the project folder

If any item is missing, hold and correct it before sending. Once invoices are reliable, the next question is resilience: how much damage can one slow payer or one bad cycle actually cause?

Layer 3: Construct Your Financial Moat#

A solid invoice gets one payment through. This layer helps keep one late payer, one tax cycle, or one dispute from destabilizing your business. Run three controls in parallel: client concentration limits, cash-account rules, and a clear liability model for transactions.

1. Set a client concentration policy#

Set the rule before any single client becomes too large. Review it monthly.

- Maximum share per client: threshold pending owner policy review, measured against trailing 12-month revenue.

- Early-warning trigger: set a lower internal alert point you watch before the cap. For context, 20%+ from one customer is often treated as high concentration risk, and 10% appears in public-company disclosure guidance, but neither is a universal operating cap for your business.

- Required action at trigger: pause open-ended scope, tighten billing terms (shorter milestones or stronger upfront terms), and run a 30-day replacement pipeline plan.

Track both trailing 12-month revenue and committed next 90 days. Concentration risk can spike when one client expands while smaller projects roll off.

2. Separate cash and automate the first move#

Cash discipline works best when the first move is automatic, not ad hoc.

Use this implementation sequence:

- Keep business and personal accounts separate.

- Maintain at least one business operating account plus a separate tax-reserve account; add owner-pay and reserve or profit accounts if useful.

- Set automatic allocation when revenue clears: tax, owner pay, operating, and reserve or profit allocations pending financial review.

- Review on a fixed cadence: weekly transfer reconciliation and monthly balance check against real obligations.

If U.S. estimated taxes apply, anchor reviews to April 15, June 15, Sept. 15, and Jan. 15 (following year). If you expect to owe $1,000 or more at filing, estimated payments generally apply, and underpayment can trigger penalties. Also monitor deposit concentration: FDIC coverage is $250,000 per depositor, per FDIC-insured bank, per ownership category for insured deposits.

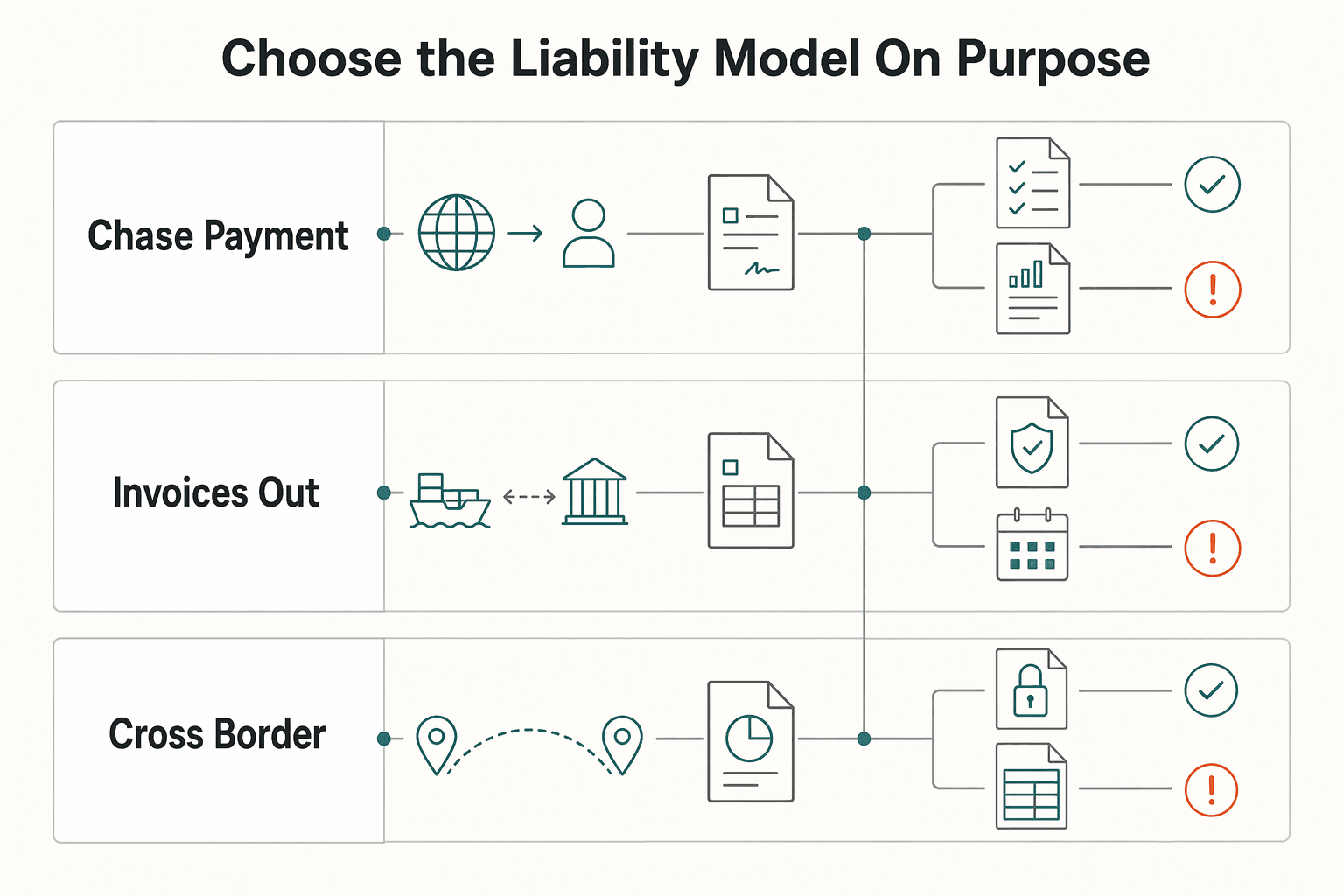

3. Choose who owns transaction liability#

Do not treat DIY billing, a payment processor, and a Merchant of Record (MoR) as interchangeable. Your actual risk profile depends on who is legally responsible for tax, compliance, refunds, and chargebacks.

| Model | Tax handling | Liability ownership | Dispute risk | Operational overhead |

|---|---|---|---|---|

| DIY | You determine tax obligations and handle collection/reporting/remittance where required | You | You handle refunds and chargebacks | Highest (in-house) |

| Payment processor | Processor handles payment flow; tax responsibility still depends on which entity is liable and your setup | Varies by contract and model | Varies by contract and model | Medium (varies) |

| MoR | MoR typically handles tax-compliance operations for the sale | MoR carries transaction-level financial, legal, and compliance liability | MoR typically handles refunds and chargebacks | Lower admin, higher platform dependence |

Validate this from contracts, not product pages. Confirm which entity must collect and report tax, and who handles refunds and chargebacks. If you sell through a facilitator model, check whether you are still treated as the MoR for those transactions. A MoR can materially reduce your operational burden, but it does not remove all regulatory or conduct risk.

Moat health check (monthly)#

| Monthly check | Confirm |

|---|---|

| Client share is within your policy cap | Trigger breaches have written actions |

| Cleared payments were allocated by rule | No undocumented tax-reserve reversals |

| Estimated-tax deadlines | Scheduled and funded if applicable |

| Current model (DIY, processor, or MoR) | Matches your actual contract terms on tax, refunds, chargebacks, and legal responsibility |

Use the table above as your monthly review.

Conclusion: You Are the Architect of Your Financial Security#

If you want more control over when you get paid, treat this as a three-part operating decision: tighten your contract, tighten your invoicing process, and choose your cross-border compliance route on purpose. In practice, this is less about one tool and more about reducing ambiguity, reducing payment friction, and checking responsibilities early, especially when requirements vary by jurisdiction.

Tighten the contract before work starts#

Write contracts that remove guesswork before work starts. Name the client entity, define the deliverable or milestone in plain language, state the invoice trigger, and include a pause-of-work right if approvals or payments stall. Use this checkpoint: a neutral third party should be able to read the signed agreement and identify when you can invoice, what counts as approval, and who can authorize changes.

Make invoicing easy to process and defend#

Match every invoice to a dated contract event, keep the invoice log current, and keep your evidence pack complete: signed agreement, current SOW, approved changes, delivery record, and acceptance email (or equivalent). For cross-border work, do not improvise tax or legal wording. Keep jurisdiction-specific requirements pending until seller entity, tax treatment, and invoice language are confirmed.

Choose the liability model on purpose#

Choose the payment-liability model for the work you do, not just the fastest setup. Direct invoicing can give you more control while often leaving more operational burden with you. A processor may make collections smoother, but contract and tax responsibility can still remain with you depending on terms and jurisdiction. A Merchant of Record may reduce transaction-handling work, but responsibilities are not automatic or universal, so verify contract boundaries, payout timing, refunds, disputes, and any remaining obligations.

| Reactive workflow (before) | Controlled workflow (after) |

|---|---|

| You chase payment after confusion appears | You set triggers, approvals, and escalation points before kickoff |

| Invoices go out when work "feels done" | Invoices map to documented milestones or acceptance events |

| Cross-border responsibility is assumed | Seller, refund/dispute handling, and jurisdiction-specific requirements are checked up front because requirements vary by jurisdiction |

Your next move should be small and concrete:

- Update contract terms so payment triggers, approvals, and pause-of-work rights are explicit.

- Tighten your invoice process so every invoice has matching delivery and acceptance evidence.

- Choose your cross-border route now: direct invoicing, platform, or Merchant of Record, then verify which liabilities remain with you.

Frequently Asked Questions

How do you lower non-payment risk before work starts?

Confirm the legal client entity, billing contact, approver, PO requirements, and first payment trigger before you reserve production time. Tie invoices to clear start, milestone, or acceptance events you can evidence later, and include a pause-of-work rule if approvals or payments stall. For cross-border work, keep jurisdiction-specific tax wording pending contract and tax review, and escalate before kickoff if entity details are unclear, scope is open-ended, or the client requests tax language you cannot verify.

Which billing route should you choose for a cross-border project?

Start with direct invoicing for known-client custom work, and move to a platform or MoR when operational load is the real bottleneck. Before you choose, confirm which entity is the seller, who issues invoices, who handles refunds and disputes, and who owns jurisdiction-specific tax and invoice obligations. Escalate when seller identity, tax handling, or chargeback responsibility is vague across jurisdictions.

What contract terms matter most if your goal is simply getting paid on time?

Make payment timing, milestone definitions, late-payment response, and change approvals clear enough to read once and execute. Keep a file that can support a good-faith review of your numbers and approvals: signed agreement, current SOW, approved changes, invoice log, delivery evidence, and acceptance records. Use that as a process checkpoint, and verify current requirements before relying on older PPP-era guidance. Escalate if redlines on ownership, termination payment, or governing law change your collection position.

How do you handle scope creep without turning it into an argument?

Classify each request as included, deferred, or billable, and confirm it in writing before you start the extra work. Define deliverables, revision limits, approval authority, and a short change-order path that updates price and timeline. Include jurisdiction-specific tax wording only after scope changes, tax treatment, and invoice obligations are confirmed, and escalate when changes affect usage rights, sublicensing, reseller treatment, or the client disputes a conflicting SOW.

Should you use milestone billing or one final invoice?

Use milestones when delivery spans multiple cycles, depends on approvals, or carries revision risk, so you do not hold all timing risk to the end. Define each milestone by a visible output or approval event, set invoice timing to that event, and state what happens if the client goes silent after delivery. For a concrete structure, see How to De-Risk a Fixed-Price Project with a Phased Payment Schedule. Escalate if acceptance criteria are subjective, retroactive, or dependent on third parties outside your control.

Do U.S. debt-collection or BOI rules change how you chase payment?

Do not assume FDCPA consumer-debt protections apply to your B2B unpaid invoice, because the FTC states business debts are not covered. If your business is foreign-formed and registered in a U.S. state or tribal jurisdiction, verify whether you are in FinCEN's March 26, 2025 reporting-company scope. Covered foreign reporting companies registered before March 26, 2025 had an April 25, 2025 deadline, and those registered on or after that date generally have 30 calendar days after registration is effective. Escalate if guidance conflicts, especially where older FinCEN FAQ text differs, since FinCEN says FAQs are explanatory only and parts may not be fully updated.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- ec.europa.eu/digital-building-blocks/wikis/display/DIGITA...trusted

- home.treasury.gov/system/files/136/Paycheck-Protection-Program...trusted

- irs.gov/faqs/estimated-tax/individuals/individuals-2trusted

- irs.gov/irm/part5/irm_05-015-001trusted

- taxation-customs.ec.europa.eu/taxation/vat/vat-businesses/invoicing_entrusted

- gov.uk/late-commercial-payments-interest-debt-recov...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: