Quick Answer

A resilient payment compliance system in 2026 is an evidence-driven control framework that runs while money moves. It should combine identity gates, transaction screening, third-party oversight, ledger-first audit evidence, escalation paths, tax and invoicing checks, jurisdiction mapping, and continuity testing. The goal is to make hold, release, reversal, and escalation decisions traceable, consistent, and defensible under stress or review.

Why Resilient Controls Matter in 2026#

Payment compliance in 2026 needs to operate as a system, not just a document set. A practical test is whether your controls run while money moves and whether you can show who checked what, when it changed, and who approved the decision.

That expectation is clear in current legal signals. U.S. AML program rules require a system of internal controls for ongoing compliance, plus ongoing monitoring to identify suspicious transactions and, on a risk basis, maintain and update customer information. In the EU, DORA (Regulation (EU) 2022/2554) sets uniform ICT security and resilience rules for financial entities, and harmonized ICT risk-management requirements apply from 17 January 2025.

The same pattern shows up in adjacent payment and reporting frameworks. The GENIUS Act became law on 07/18/2025 as Public Law 119-27, and its text states that it provides for the regulation of payment stablecoins. The European Commission states that ViDA was adopted on 11 March 2025 and will roll out progressively until January 2035, while still allowing EU countries that choose to implement national digital reporting systems for domestic trade.

That is why this article is organized control by control. The point is to make each decision clear, surface the tradeoff, and define the evidence you will need when time is short.

What matters in this list#

Each item is built around three operator questions that keep the list practical:

- Control value: does it materially reduce exposure across KYC, AML, third-party dependency, tax, invoicing, or operational continuity?

- Escalation point: when should team discretion stop and legal, compliance, or leadership step in?

- Evidence pack: what records prove the control actually ran?

Treat evidence as part of the control, not cleanup after the fact. For held, released, reversed, or blocked payouts, a defensible answer typically depends on linked records: screening result, reviewer action, timestamp, rule version, and final disposition.

Scope and jurisdiction#

The examples here reference DORA, the U.S. GENIUS Act, and e-invoicing frameworks because they are concrete signals, not interchangeable rules. Applicability still varies by product, entity, and jurisdiction.

That matters in multi-market operations. ViDA includes EU-level direction but leaves room for domestic digital reporting choices, and e-invoicing practice remains jurisdiction-specific as adoption expands. The Inter-American Development Bank reports that nearly 90 countries are rolling out e-invoicing.

Use this list to decide what to build, monitor, and evidence continuously, then localize the legal interpretation where market rules change the answer. If a control decision depends on jurisdictional scope, escalate to counsel before you standardize behavior.

Selection criteria and who this list is for#

Use this list if you run multi-market payouts and need controls that keep working during stress, dependency failures, and regulatory review. If a step slows payouts but clearly reduces AML or KYC exposure, add that friction at the highest-risk points first, then relax only when your own evidence supports it.

Who should use it#

- Multi-market payout owners

Compliance, legal, finance, and risk teams handling contractor, seller, or creator payouts across multiple jurisdictions.

- Teams with operational dependencies

This list fits programs that rely on banks, processors, sanctions data, or identity vendors and need continuity, not just policy coverage. DORA applies from 17 January 2025 and focuses on resilience to ICT disruption.

- Operators who must explain decisions under pressure

Use it when you need to reconstruct why a payout was held, released, reversed, or blocked with a defensible audit trail.

When not to use it as written#

This is not a substitute for local legal analysis. FATF emphasizes that countries do not apply identical AML/CFT measures and that controls should reflect national legal and regulatory frameworks. Two cases need escalation before you use this list as written:

- Single-country edge cases

Do not treat this as legal advice where jurisdiction-specific interpretation changes the outcome.

- Conflicting perimeter or product questions

Escalate to counsel when DORA, the U.S. GENIUS Act, local AML duties, or payment-service perimeter issues create uncertainty. The GENIUS Act became Public Law 119-27 on 07/18/2025 and addresses payment stablecoins, but product-specific licensing and control questions can still require jurisdiction-specific legal or compliance advice.

How each control made the list#

Each control earned its place for one reason: it reduces surprise when conditions are messy, not just when operations are normal. That shows up in three filters:

- Measurable reduction in regulatory surprise

Priority goes to controls that make ongoing due diligence and suspicious-activity monitoring easier to demonstrate.

- Operational continuity under failure

A control belongs here only if it still runs during outages, data delays, or incident escalation, not only in normal conditions.

- Defensible audit trail quality

We prioritize controls that leave clear, reconstructable decision records rather than controls that are hard to verify after the fact.

For a step-by-step walkthrough, see Device Fingerprinting Fraud Detection Platforms for Payment Risk Teams.

Control 1 identity gates before money moves#

A practical default is to hold the first payout until KYC clears, then use risk-based step-up checks for later payouts when signals change. This is often the cleanest place to add friction because it can catch avoidable AML issues before funds move and leave a clearer decision trail.

This control fits platforms that onboard new payees quickly across markets. The tradeoff is straightforward: stronger first-line risk reduction, but more onboarding friction and more false positives if screening is too blunt.

What the gate should actually do#

Do not treat the gate as only "upload ID and wait." Keep three decisions separate:

- Collect minimum identifying data before account opening.

- Verify identity using reliable, independent documents, data, or information.

- Decide first-release eligibility based on risk and review outcome.

Where your program applies U.S. CIP/CDD standards, that separation matters. CIP is written and risk-based, and CDD is broader than ID capture alone.

For legal-entity payees, include ownership checks where applicable. Under the U.S. CDD ownership prong, beneficial owners include individuals with 25 percent or more equity ownership, so a company name by itself is not enough for first release.

The practical release rule#

Use a simple default where this control fits your program: keep the first payout on hold until KYC passes. Later payouts can run with lighter checks unless risk changes. That puts the heaviest friction at the point of highest uncertainty, then steps up only when needed.

Common step-up triggers include material profile changes, ownership changes, verification mismatches, or suspicious activity signals. Avoid a one-size-fits-all queue that treats missing data, failed verification, and elevated risk as the same problem.

Operator checkpoint#

Document four states with named owners, escalation paths, SLA targets, and defined evidence requirements so release decisions stay consistent and auditable:

| State | Definition |

|---|---|

| Hold | Required fields or documents are missing, or identity is not yet verified. |

| Review | Information exists, but mismatches or risk signals need human decision. |

| Release | Checks passed and required review outcomes are recorded. |

| Offboard | Repeated failure, non-cooperation, or risk findings make the payee ineligible. |

What to verify in the record#

A second reviewer should be able to reconstruct the decision from the file alone. For each first payout, keep the collected identity fields, verification outcome, source documents or data used, beneficial-owner record where relevant, reviewer decision, and timestamped rationale for hold, release, or offboard.

Do not treat onboarding as the end of due diligence. Ongoing monitoring and risk-based updates to customer information should stay active after first release.

Control 2 transaction screening that matches payment speed#

For real-time payments, screening is typically tiered and run before release. High-confidence hits can be held immediately, while lower-confidence flags can follow a monitored review or controlled release path. That lets you interrupt AML and fraud risk early without pushing every alert into one manual queue.

As settlement gets faster, there is less time to intervene after release. Instant payments are received immediately, at any time, with near-real-time interbank settlement, and they clear transaction by transaction rather than in predictable batches. That is why controls need to trigger early in the payment flow.

How to tier screening without breaking payout speed#

Use segmentation, not a single alert policy for every payee, rail, and payment context. Enhanced measures belong on higher-risk scenarios, with lighter treatment reserved for lower-risk ones.

| Screening tier | What it is | Default action | Key differentiator |

|---|---|---|---|

| High-risk or high-confidence hit | Strong match or strong suspicious pattern on a payment that may not be suitable for auto-release | Immediate hold before release | Stop first, investigate second |

| Mid-risk or ambiguous flag | Partial match, conflicting signal, or pattern needing more context | Monitored review or controlled release path, based on policy and jurisdiction | Preserve speed for some legitimate payments while keeping a review record |

| Lower-risk or known-good pattern | Lower alert confidence and no material risk-profile change | Pass with logging and post-event monitoring | Reduce friction by segment, not by weakening core AML logic |

This is a design choice, not a universal legal template. If false positives rise and payout latency worsens, review segmentation before loosening core AML rules. A practical split is instant versus non-instant rails, new versus established payees, and strong versus weak alert confidence.

Where the legal detail actually matters#

Scope matters in Europe. For instant euro credit transfers, payment service providers must verify periodically, and at least daily, whether payment service users are subject to targeted financial restrictive measures. That is a specific requirement for a specific lane, not a blanket rule for every rail and jurisdiction.

Timeline matters too. The regulation was adopted on 13 March 2024. Its euro-area deadlines are listed as 9 January 2025 for receiving instant payments and 9 October 2025 for sending instant payments. If you serve Europe, your design should explicitly link instant-payment handling, sanctions-check cadence, and release decisions.

The UK gives a different signal. The Payment Services (Amendment) Regulations 2024 came into force on 30 October 2024 and allow delays of up to 4 business days to investigate suspected APP fraud. But the bar is objective: reasonable grounds to suspect fraud or dishonesty, not mere speculation.

What to verify before you tune anything#

Before you tune the rules, confirm that your records can explain why one payment was held and another was released on a monitored path. If every alert collapses into one queue, low-confidence flags can delay legitimate payments while urgent hits wait beside them.

Keep a minimum evidence pack for each screened payment decision so tuning stays defensible:

- alert timestamp and payment rail, especially for real-time payments

- rule or model version that generated the hit

- hit type and confidence category used in policy

- status decision, whether hold, review, or release

- objective facts supporting any delay or hold

- reviewer notes, override reason if any, and final timestamped disposition

That evidence makes tuning easier to defend, especially at higher volume. The goal stays the same: strengthen fraud prevention while minimizing impact on legitimate payments.

For a deeper look at sanctions and risk-screening decisions, see OFAC, PEP, and Adverse Media Screening Decisions for Payment Platforms.

Control 3 third-party and payment intermediary oversight#

Use this control when a third party runs a step you cannot easily replace, because you still own the outcome if that control fails. It helps address concentration and blind-spot risk, but it adds real overhead in procurement, contract discipline, and ongoing monitoring.

After screening, this is the next handoff to lock down. Outsourcing a critical control does not outsource accountability, which is consistent with European oversight framing, including EBA outsourcing guidance that covers payment and electronic money institutions.

Score the relationship by what would break#

Rank third parties by control impact, not by spend or brand. The useful question is simple: if this provider fails, what payout, screening, or evidence path breaks with it?

| Factor | Assessment |

|---|---|

| Control dependency | Whether the provider performs or materially affects release-blocking steps, for example KYC checks, sanctions screening, routing, or exception handling. |

| Incident history | Outages, data-quality failures, delayed files, or unresolved control failures that required manual workarounds. |

| Evidence quality | Current, dated proof of controls, continuity arrangements, escalation contacts, and change notices. |

Use a risk-based approach across the full relationship life cycle: planning, due diligence, contract negotiation, ongoing monitoring, and termination. Then set review cadence by tier. The cadence itself is a policy choice, but critical-control providers with weak evidence should get shorter review cycles and tighter change approval.

Put the contract where the risk is#

For critical providers, contract terms are part of the control. At minimum, the agreement should clearly assign incident-notification and continuity responsibilities; where relevant, it should also define data return or extraction rights, subcontracting limits, and termination support.

If a provider cannot show who does what during an outage, or how you can retrieve the data needed to continue or reconstruct payment decisions, treat that as a control risk.

Verify fallback before renewal#

Before renewal, require a documented fallback path for every critical provider. You should know whether you can switch providers, move to a controlled manual process, or pause the lane with a defensible communication path. Ask for evidence you can verify:

- fallback owner and current escalation contacts

- data fields required to recreate open payment state

- most recent fallback test or walkthrough date

- concentration view, including hidden dependencies on shared underlying providers or feeds

In Europe, dependency and third-party concentration are explicit resilience concerns under DORA (adopted 14 December 2022). In the UK RPSO/SSP perimeter, the Bank of England's updated statement was published on 18 March 2026 and takes effect on 18 March 2027. It expects written coverage of core areas for material outsourcing and an annual register to the Bank. If a provider performs a critical compliance step and cannot show a tested fallback path, do not renew by default.

For the operating model behind ongoing reviews, see Continuous KYC Monitoring for Payment Platforms Beyond One-Time Checks.

Control 4 ledger first audit evidence you can actually defend#

If you need to defend a payout decision under pressure, your ledger should answer first, and every other log should support it. This control is worth the engineering cost when finance and compliance need to reconstruct holds, releases, and reversals across asynchronous systems without debating which screen is correct.

The upside is stronger reconstruction and faster investigations. The cost is stricter posting discipline, cleaner event design, and less room for manual fixes that never enter the audit trail.

Put the decision in the ledger, not just the payment processor log#

When processor status, webhook history, and internal case notes all act as separate truths, audit and investigation work gets messy fast. You need one record that shows what was decided, when, why, and what changed.

Use a simple rule: every payout-affecting decision posts a ledger event. That includes compliance holds, manual-review releases, sanctions or KYC-related reversals, cancellations, and retries after failure. If a decision changes, append a new linked entry instead of overwriting prior state.

In adjacent regulated recordkeeping contexts, this standard is explicit. SEC Rule 17a-4 amendments adopted on October 12, 2022 allow either WORM storage or an audit-trail approach that can recreate an original record after modification or deletion. CFTC Rule 17 CFR 37.205 requires data sufficient to reconstruct activity, including timing and sequencing, and to track an order from receipt through execution. These rules are not automatically applicable to every payment platform, but they are practical references for defensible reconstruction.

What the entry needs to prove#

Each ledger entry should stand on its own so someone outside the original team can follow the decision chain. For each payout decision, capture at least:

- unique ledger event ID and sequential ordering field

- event time, posting time, and source event or request ID

- decision type, such as hold, release, reverse, or cancel

- actor and origin, whether automated rule, user action, or third-party trigger

- reason code and linked case, policy, or review reference when relevant

Timing and sequencing matter most when multiple services can update status, so you need a clear authoritative order of events. A practical check is to pick one disputed payout each month and rebuild it from ledger events alone. If you still need app-table forensics, webhook dashboards, or analyst memory to explain the result, the ledger is not yet your source of truth.

Design for replay, delay, and duplicate delivery#

A credible audit trail breaks when retries create duplicate effects or missing evidence. Stripe states webhook endpoints can receive the same event more than once. PayPal states non-2xx responses can trigger up to 25 retries over 3 days.

So the answer is replay-safe posting, not webhook avoidance. Use idempotent writes for every state-changing request and store the dedupe key with the ledger event. Stripe describes idempotency keys as the control for safe retries without duplicate operations, and notes keys can be removed once they are at least 24 hours old. If your reconciliation window is longer than 24 hours, keep dedupe history longer than that vendor minimum.

A common failure mode is surface mismatch: late or duplicate webhook delivery collides with manual action, and internal versus processor states diverge. Prevent that by defining posting precedence and reconciliation rules up front. Decide which source can create ledger events, which can only annotate, and when a late event must be logged as non-financial context rather than new money movement.

What to recommend in practice#

Start with payout holds, releases, and reversals before you try to ledger every operational detail. Those are often the first decisions challenged and the ones leadership must explain quickly.

If engineers can edit historical payout status in place without a reversing or superseding ledger entry, fix that first. An append-first audit trail, combined with replay-safe posting and routine reconciliation, gives you evidence you can defend when scrutiny increases.

Related: What Is an Audit Trail? How Payment Platforms Build Tamper-Proof Transaction Logs for Compliance.

Control 5 escalation paths that trigger before incidents spread#

Define escalation paths before incidents happen. Set scenario-based triggers, assign named owners, and tie each trigger to a real reporting clock or incident-classification rule. That helps prevent avoidable delay when AML, KYC, operations, and legal teams are under pressure.

This control matters most when escalation still depends on judgment calls in the moment. It can improve containment speed and accountability, with the tradeoff of more process design, training, and testing.

Use scenario triggers, not vague severity labels#

"Escalate if serious" is not operationally reliable. Triggers should let an analyst act without debating severity on the fly. A practical trigger set can include:

- repeated AML alerts on the same customer, corridor, or beneficiary within one reporting period

- unresolved KYC exceptions that keep a payout on hold past your internal review target

- third-party outages that affect screening, payment execution, or required customer data

- recurring ICT incidents that may meet DORA major-incident criteria in Europe

Treat thresholds as policy choices, not universal legal rules. If repeated high-severity signals are a known failure pattern in your environment, set an automatic escalation path to compliance leadership and legal rather than relying on ad hoc discretion.

Tie escalation to real clocks and named accountability#

Escalation design should follow actual filing clocks. For U.S. suspicious activity reporting, the baseline is 30 calendar days from initial detection. An additional 30 days is allowed when no suspect is identified, and there is no delay beyond 60 calendar days from initial detection.

Ownership should be explicit. AML program rules require designated day-to-day compliance responsibility and ongoing monitoring, so each trigger should name a primary receiver, a backup, and a clear point for legal or senior compliance escalation.

Split ownership can become a failure mode: operations sees payout impact, compliance sees alerts, and vendor teams see outages, but no one owns the escalation decision. That is how incident exposure can accumulate across teams.

Build around DORA and third-party lifecycle risk#

If you operate in Europe or depend on providers there, map your matrix to DORA Article 19 (major ICT incidents and significant cyber threats) and Article 23 (operational or security payment-related incidents for relevant payment entities). In policy, reference Delegated Regulation (EU) 2024/1772 so incident classification and materiality thresholds are concrete.

Give third-party incidents their own escalation path. Interagency guidance covers the full lifecycle of third-party relationships, and outsourcing does not remove your responsibility, so escalate based on your service impact, control gaps, and reporting obligations.

What to verify before you trust this control#

Run a case test for each trigger scenario. The evidence pack should show the trigger event, initial-detection timestamp, recipient, decision, and whether the case was linked to SAR review, legal assessment, or DORA classification.

If those records exist only in chat threads or inboxes, the control is not reliable yet. Missed escalations should produce corrective action, such as policy updates, retraining, or tighter thresholds.

If third-party oversight is part of your control set, see Vendor Risk Assessment for Platforms: How to Score and Monitor Third-Party Payment Risk.

Control 6 tax and invoicing controls that prevent downstream rework#

Stop payouts early when required tax records or invoice evidence are missing instead of repairing failures at year end. Use the same hold-and-escalate discipline from Control 5 here, so exceptions route to named owners before they become filing or reporting problems.

For US-connected creator or contractor lanes, tie payout eligibility to tax profile completeness on reportable flows. In practice, collect Form W-9 so you have a correct TIN for information-return reporting. Then route missing or incorrect TIN cases to an exception queue or payout hold where your policy requires it. This helps avoid cleanup work when backup withholding risk applies, including the IRS backup withholding rate of 24 percent.

Gate tax data before release, not after payout#

Make the release check explicit for each payee on a US-reportable lane: tax profile status, form on file, for example Form W-9, collection date, payout ID, and hold or release decision. If those records sit across tools without a shared identifier, rework is built in.

For 2026 automation, keep threshold logic as a verification point until you confirm current IRS primary instructions. Secondary sources conflict on 1099-NEC threshold values, so do not hard-code a universal threshold assumption.

Separate reporting tracks before filing season#

Do not run Form 1099-NEC and Form 1099-MISC through one generic "1099" workflow. They cover different reporting contexts, and where applicable, 1099-K logic should stay separate because some payments are not reportable on 1099-NEC or 1099-MISC.

| Form | Filing timing (year after tax year) |

|---|---|

| 1099-NEC | January 31 |

| 1099-MISC (paper) | February 28 |

| 1099-MISC (electronic) | March 31 |

If your platform handles mixed income types, classify at the payment or contract level, not in a year-end spreadsheet. For creator-heavy mixes, this breakdown of 1099-MISC vs. 1099-NEC can help operationally.

Pair tax checks with invoice validity rules#

Tax checks alone are not enough in Europe or Latin America. Release logic should also validate invoice requirements for the lane. Accepting any uploaded PDF without lane-specific checks can create avoidable post-payment disputes.

| Lane | Release check | Detail |

|---|---|---|

| US-connected creator or contractor lanes | Tax profile completeness on reportable flows | Collect Form W-9 so you have a correct TIN for information-return reporting; route missing or incorrect TIN cases to an exception queue or payout hold where your policy requires it; IRS backup withholding rate is 24 percent. |

| Europe | Invoice validity for the lane | ViDA was adopted on 11 March 2025; EU communications set 1 July 2030 as the DRR start point for cross-border B2B transactions; compliant e-invoices should not depend on recipient acceptance. |

| Latin America | Jurisdiction-specific e-invoicing checks | Argentina requires electronic invoicing or fiscal controller coverage for domestic operations, and Mexico uses CFDI. |

In Europe, ViDA was adopted on 11 March 2025, and EU communications set 1 July 2030 as the DRR start point for cross-border B2B transactions. EU law text also states compliant e-invoices should not depend on recipient acceptance, so workflow design should not rely on buyer acceptance as a precondition for invoice validity.

In Latin America, treat e-invoicing as jurisdiction-specific. Argentina requires electronic invoicing or fiscal controller coverage for domestic operations, and Mexico uses CFDI. The control adds data-handling burden, but it can reduce correction work on reporting and invoice evidence after funds are released.

Related reading: Goodwill and Intangible Assets on a Balance Sheet for Payment Risk.

Control 7 jurisdiction mapping for cross-border change pressure#

After tax and invoice gates, a common risk is jurisdiction drift. The fix is a living jurisdiction matrix by market, product lane, payment method, and provider type, not a one-time country sheet. When a local rule is stricter than your global default, keep the baseline and tighten that lane.

Build the matrix by lane, not just by country#

A country-only map is too coarse for cross-border payouts. FATF is clear that countries adapt implementation to local legal and operational context, and its risk-based approach means AML/CFT controls should follow actual risk rather than a single global template.

That is even more important for digital assets or stablecoins where supported. FATF updated Recommendation 15 in 2019 to bring virtual assets into AML/CFT scope. Its 9 July 2024 update says implementation is still lagging, with 75% of jurisdictions only partially or not compliant. That is a practical reason to avoid one generic crypto row.

| Lane key | Minimum fields to map | Why it needs its own row |

|---|---|---|

| Europe fiat payout via bank or non-bank PSP | AML/CFT requirements, provider type, operational continuity obligations, tax and invoice dependencies | FSB calls for more consistent treatment of bank and non-bank cross-border PSPs, and has highlighted cross-jurisdiction gaps and inconsistencies |

| Europe crypto-asset or stablecoin transfer | transfer-information checks, asset type, wallet or provider model, effective-date tracking | EBA Travel Rule Guidelines show application date 30/12/2024, and MiCA stablecoin-related titles applied from 30 June 2024 |

| Crypto tax-reporting lane in CARF-committed jurisdictions | reportable asset category, customer tax fields, reporting owner, exchange timeline | OECD reports 58 Global Forum members intend to begin CARF exchanges in 2027 |

Put dates, owners, and evidence in every row#

A matrix is only useful if each row is auditable. Include, at minimum, rule owner, last review date, effective date, exception approval path, and an evidence pack showing that the control is live. For lane-level rules, that usually includes the legal interpretation note, policy text, product configuration or screening setting, and a sample hold or release case.

Use a simple checkpoint: if a row has no effective date or named owner, treat it as unapproved. You should be able to explain lane-specific friction by pointing to trigger date, control change, and release condition without rebuilding the history from chat threads.

Localize the stricter rule when defaults collide#

Use a hard rule: never weaken the baseline to accommodate one market. If an EU crypto transfer lane has transfer-information checks effective from 30/12/2024, add those checks in that lane rather than lowering global AML collection.

Apply the same logic to operational continuity. DORA applies from 17 January 2025, and ESMA notes it covers 21 types of financial entities. If a lane is in scope, map the continuity obligations and key provider dependencies explicitly.

The downside is ongoing maintenance. Rules keep moving, especially for stablecoins and cross-border crypto reporting, and FSB continues to highlight jurisdictional gaps and inconsistencies. In practice, a common failure mode is stale mapping: a new payout route inherits the wrong default, and the row is corrected only after an incident or audit.

Control 8 resilience and continuity testing under real stress#

If your controls exist only in policy text, treat them as unproven until scenario testing shows they hold under disruption. This control works best after lane mapping, because then you can test whether continuity actually holds when a provider is unavailable, sanctions data updates are delayed, or settlement timing is disrupted.

The standard is not "we have a plan." FCA rules require testing severe but plausible disruption, with scenarios that vary by nature, severity, and duration. With DORA applying from 17 January 2025, prioritize the lane that would create the highest customer or regulatory impact over a generic incident drill.

Pick scenarios that break the service, not just the tool#

Start with scenarios that expose different failure paths. Provider downtime tests whether a critical third party can fail without taking your important service down. Sanctions data lag tests whether controls still implement list changes without delay when updates are missed or late. A delayed-settlement scenario can test whether holds, releases, and escalations still work when final settlement is late.

Do not stop at alerting checks. Trace the full path: trigger time, queue behavior, hold decision, manual override, release condition, and customer outcome.

Make pass or fail explicit#

Define pass-fail criteria before each test and tie them to impact tolerance for the important service. At minimum, record:

- the important service being tested

- the impact tolerance for that service

- the disruption window and scenario assumptions

- the exact pass-fail criteria

- the remediation owner and target date if it fails

The key checkpoint is whether the service stayed within impact tolerance. If testing is outsourced, accountability stays with your firm. Keep an evidence pack with timestamps, decision logs, screen captures or ledger extracts, and clear senior ownership of remediation so the result can stand up in audit.

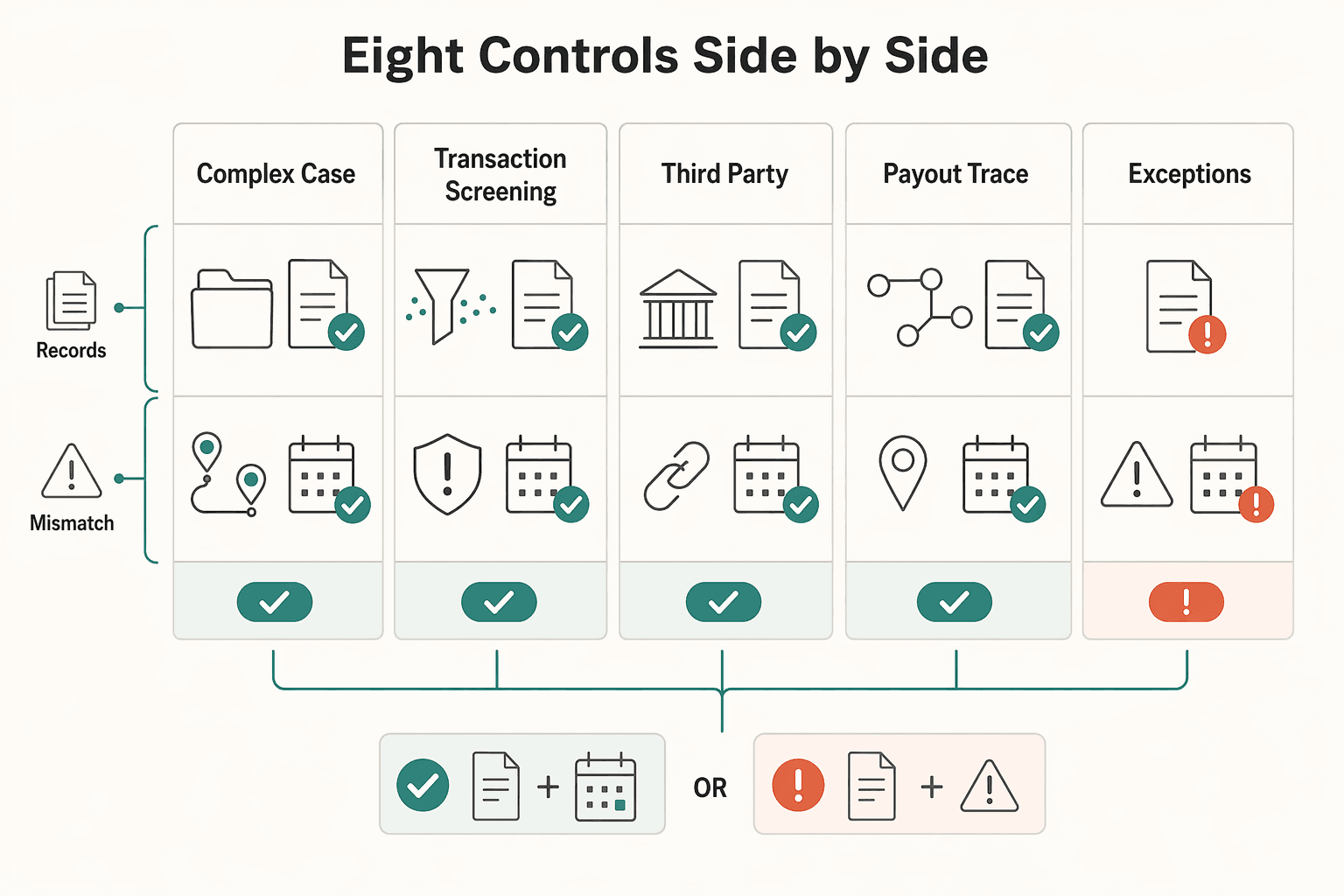

Compare the eight control systems and phase implementation#

Do not implement all eight controls at full depth at once. Build the evidence-critical ones first, then increase automation once you can reliably prove who was paid, why a payout was held, and who approved an exception.

Use the 30/90/later sequence as an operating heuristic, not a universal regulatory template. The right rollout depends on your products, lanes, jurisdictions, and risk exposure.

Eight controls side by side#

| Control system | Best for | Required systems | Typical failure mode | Key evidence artifact | Owner | Escalation trigger |

|---|---|---|---|---|---|---|

| 1. Identity gates before money moves | New payees and first payout release; stronger AML/CFT control, but slower onboarding if queues back up | Identity verification workflow, beneficial ownership procedures for legal entities, case queue, payout hold logic | One-time verification treated as permanent, or manual release with weak records | Identity verification decision record, beneficial owner check result, hold/release log | Compliance onboarding lead | Unresolved identity exception before first payout, or suspicious facts that may start a SAR clock |

| 2. Transaction screening matched to payment speed | Real-time and instant payments, where risk exposure may differ from legacy methods; more payout delay if tuning is blunt | Screening engine, risk segmentation, alert queue, release controls, ongoing CDD monitoring | Rules copied from slower rails, causing avoidable holds and latency | Alert history, analyst disposition, release rationale, screening change log | AML operations lead | Repeated suspicious activity, or alert patterns that may require SAR filing within 30 calendar days of initial detection |

| 3. Third-party and intermediary oversight | Multi-provider stacks; more vendor flexibility, but more third-party exposure | Provider inventory, due diligence file, contract register, incident monitoring, fallback path | Critical dependency with no tested backup or weak termination planning | Due diligence memo, contract controls, incident log, fallback test result | Vendor risk manager with payments ops | Critical provider outage, monitoring evidence gap, or control dependency with no viable fallback |

| 4. Ledger-first audit evidence | Teams that must reconstruct decisions under audit or investigation; stronger accountability, but tighter engineering discipline | Ledger event store, reconciliation logic, idempotent posting, decision event mapping | Replay or delay creates duplicate or missing records across systems | Reconstructable event chain, reconciliation report, decision timestamp history | Finance systems lead and compliance data owner | Inability to reconstruct a hold, release, reversal, or customer-impact event quickly |

| 5. Escalation paths before incidents spread | Firms with inconsistent legal or risk escalation; faster containment, but more training and ownership discipline | Severity matrix, named approvers, contact tree, incident log | Teams wait for ad hoc judgment and lose reporting time | Escalation log with timestamps, decision owner, legal or CCO notification record | CCO or legal ops lead | Reportable suspicion, unresolved high-severity case, or pressure against SAR clocks (30/60 calendar days, where applicable) |

| 6. Tax and invoicing controls | US-connected payouts and multi-market operations; clearer filing readiness, but more data collection and PII handling | Tax profile collection, form logic, invoice status checks, payout block rules | Payout released with missing tax form or invalid invoice | Tax form receipt, block/release record, filing calendar | Tax operations lead | Missing tax data before release, or filing windows like January 31 (1099-NEC) and February 28/March 31 (1099-MISC) |

| 7. Jurisdiction mapping for cross-border change pressure | Cross-border operations; clearer local-rule handling, but ongoing maintenance cost | Market rule matrix, lane register, counsel review queue, change log | Global default overrides a stricter local rule | Versioned jurisdiction matrix, counsel sign-off, change approval trail | Legal and compliance policy owner | Rule change, new market launch, new payment method, or local-versus-global control conflict |

| 8. Resilience and continuity testing | Important services needing disruption readiness evidence; stronger resilience evidence, but real test overhead | Service map, scenario tests, incident metrics, provider fallback, remediation tracking | Tests validate alerting only and skip customer impact or pass-fail criteria | Test script, timestamps, decision logs, remediation owner sign-off | Operational resilience lead | Important service exceeds impact tolerance, or DORA test failure for an in-scope entity after 17 January 2025 |

A control is not live unless two things are true: the evidence artifact is easy to retrieve, and the escalation trigger points to a real deadline or harm condition. If either is missing, you have policy text, not an operating control.

Phase implementation without overbuilding#

| Phase | What to implement | Verification checkpoint | Avoid overbuilding |

|---|---|---|---|

| First 30 days | Identity verification and beneficial ownership controls, baseline AML screening, ledger-first audit trail, escalation paths | For every blocked or released payout, you can retrieve the decision, timestamp, and accountable owner | Do not prioritize model nuance or edge-case localization before end-to-end reconstruction works |

| Next 90 days | Third-party lifecycle oversight, jurisdiction mapping, tax/invoicing controls, risk-based ongoing CDD | Provider oversight is tiered by risk and complexity; jurisdiction changes are versioned; tax blocks align with filing timelines | Do not assume DORA scope by default; verify in-scope status for your entity mix |

| Later optimization | Deeper screening segmentation, stronger provider fallback, broader resilience testing program | Automation improves speed without degrading evidentiary quality for suspicious activity, outages, or overrides | Do not tune only for fewer holds before proving clean capture of decisions and incidents |

Implement evidence-critical controls first, especially identity verification, AML controls, and audit-trail reconstruction, then optimize automation depth. If identity, decisioning, and reconstruction are defensible, faster payout operations can be safer to scale.

If you are turning this matrix into operating policy, use the Gruv docs to map controls to compliance gates, ledger evidence, and payout status flows.

Conclusion#

Run compliance as a continuous system, not a policy library. The throughline across these sources is consistent: FATF centers AML/CFT on a risk-based approach, U.S. AML/CDD expectations include internal controls for ongoing compliance and ongoing monitoring, and DORA expects documented, monitored, incident-ready ICT risk management.

Controls can fail at handoffs, not just in policy text. A payout may be held without a named owner, a screening hit cleared without a recorded rationale, or a provider outage may leave no usable fallback evidence. If you cannot reconstruct who decided what, when, and why, your audit trail is not yet defensible.

Priority order matters more than policy volume. Start with KYC, AML, third-party risk, and operational continuity so you focus resources on higher-risk exposure instead of spreading effort evenly. That aligns with FATF's risk-based model and with U.S. CDD expectations for ongoing monitoring and updates, not one-time onboarding checks.

For EU entities in DORA scope, anchor on Regulation (EU) 2022/2554 (14 December 2022). Maintain a sound, complete, well-documented ICT risk management framework. Continuously monitor ICT security and operations, and detect, manage, record, and notify ICT-related incidents. Resilience is credible only when those actions are traceable to named owners and dated records.

Third-party oversight belongs in the same first wave. U.S. interagency guidance finalized on June 6, 2023 treats third-party risk as a full lifecycle discipline. If a partner or vendor performs a critical compliance step, verify both the evidence you receive and the fallback path if that evidence stops.

For a practical closeout, do three things:

- Map the article's control set to operations. For each control, name the owner, key evidence artifact, and escalation point.

- Find the highest-risk evidence gap. Start where an auditor or investigator is most likely to get an incomplete story.

- Fix that gap before adding policy text. Add the missing timestamp, decision rationale, fallback path, or review record first.

If you do one thing next week, pick one recent payout or incident and rebuild its full history from your records. That test can be a faster signal of control quality than another policy revision.

When you need to confirm jurisdiction coverage and rollout constraints for your control plan, talk with Gruv.

Frequently Asked Questions

What is a resilient risk system for payment platforms in 2026?

A resilient risk system is a coherent control framework you can defend with evidence. It combines risk-based AML/CFT controls, ongoing monitoring, and escalation paths to accountable owners. A practical test is whether you can retrieve who made a hold or release decision and when.

Which controls are table stakes for cross-border contractor and seller payouts?

The baseline is ongoing monitoring, clear escalation ownership, and reconstructable evidence. For U.S.-connected payouts, tax-data completeness should align with filing pressure points such as January 31 for Form 1099-NEC and February 28 or March 31 for Form 1099-MISC. If intermediaries are involved, documented oversight and fallback planning are also table stakes.

How often should compliance controls be monitored and reported to leadership?

There is no single universal reporting cadence in this article for every control type. For EU entities in DORA scope, the ICT risk management framework must be documented and reviewed at least once a year, with management responsible for implementation oversight. Keep dated reviews, remediation ownership, and version history so leadership reporting reflects operating evidence.

What events should trigger immediate escalation to legal or the CCO?

Escalate immediately when suspicious facts may start a SAR timeline in U.S.-applicable contexts. Also escalate major ICT-related incidents where EU reporting rules apply, and any event that breaks decision traceability or ownership. The main trigger is time-bound reporting exposure combined with risk severity.

How do you reduce regulatory surprises without adding unnecessary payout friction?

Use a risk-based approach so controls match measured ML/TF risk instead of adding the same friction to every lane. Reserve heavier checks for higher-risk scenarios and keep lower-risk flows more efficient. That reduces broad delays while still addressing the highest-risk exposure.

How should teams handle jurisdiction differences across Europe and Latin America?

Treat jurisdiction mapping as a living control because countries do not apply identical legal and operational measures. In Europe, VAT direction includes real-time digital reporting based on e-invoicing, while Latin America uses jurisdiction-specific e-invoicing practices. When local rules are stricter than your baseline, localize that lane and document the variance.

Where do stablecoins and digital assets fit in a compliance-first payment stack?

Stablecoins and digital assets should sit inside AML/CFT and jurisdiction-mapping controls, not outside them. FATF extends AML/CFT measures to virtual assets and virtual asset service providers, and the EU framework covers crypto-asset service providers and relevant token issuers. Before launch, confirm scope and make sure screening, evidence capture, and escalation controls still work end to end.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/bill/119th-congress/senate-bill/1582/texttrusted

- congress.gov/bill/119th-congress/senate-bill/1582trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fdic.gov/news/financial-institution-letters/2023/fil2...trusted

- federalregister.gov/documents/2023/06/09/2023-12340/interagency-...trusted

- federalregister.gov/documents/2016/05/11/2016-10567/customer-due...trusted

- irs.gov/instructions/i1099mectrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: