Quick Answer

Run a disputed-payout reconstruction test first, then set control depth from scope and risk. For card environments, PCI DSS Requirement 10 requires attributable access records, protected audit logs, and anomaly review, not just stored events. Build around append-only history, dual approval for beneficiary, amount, or routing changes, and exception cases with linked closure evidence. If key records live in chat threads or spreadsheets, the audit trail is not defensible.

Why Audit Trails Matter for Payment Platforms#

For payout risk owners, a useful audit trail is one you can replay under pressure: who acted, what changed, when, and why it was allowed.

- Who this guide is for

This guide is for compliance, legal, finance, and risk owners managing contractor, seller, or creator payouts across markets. In NIST terms, a log is a record of events in computing assets, and log management covers the lifecycle from generation through disposal. In payout operations, evidence often sits across multiple records. The real test is whether one payout can be reconstructed end to end.

- What you will get from this guide

You will get practical direction on what to log, what to review, and when to escalate so you reduce surprises without overbuilding. The focus is on operational controls you can produce as evidence: routine review to detect anomalies, as reflected in PCI daily log-monitoring guidance from May 2016, and access tracking for card environments under PCI DSS Requirement 10 where card scope applies. Keep two limits in view from the start. Tamper-proof logging helps oversight but does not, by itself, prove compliance. Log data still has to meet privacy and data-minimisation requirements.

- Where this guide stops and where to escalate

Treat this as an operator guide, not a legal determination. Control depth can vary by market and system function. FATF materials updated in October 2025 note that countries cannot all take identical measures, and PCI's July 2025 FAQ, Article 1252, states that PCI DSS applicability depends on system function, with any non-applicability decision supported by documented evidence. If a logging control is being marked out of scope, pause until that evidence exists. Escalate early when card scope, privacy limits, or legal interpretation is in question.

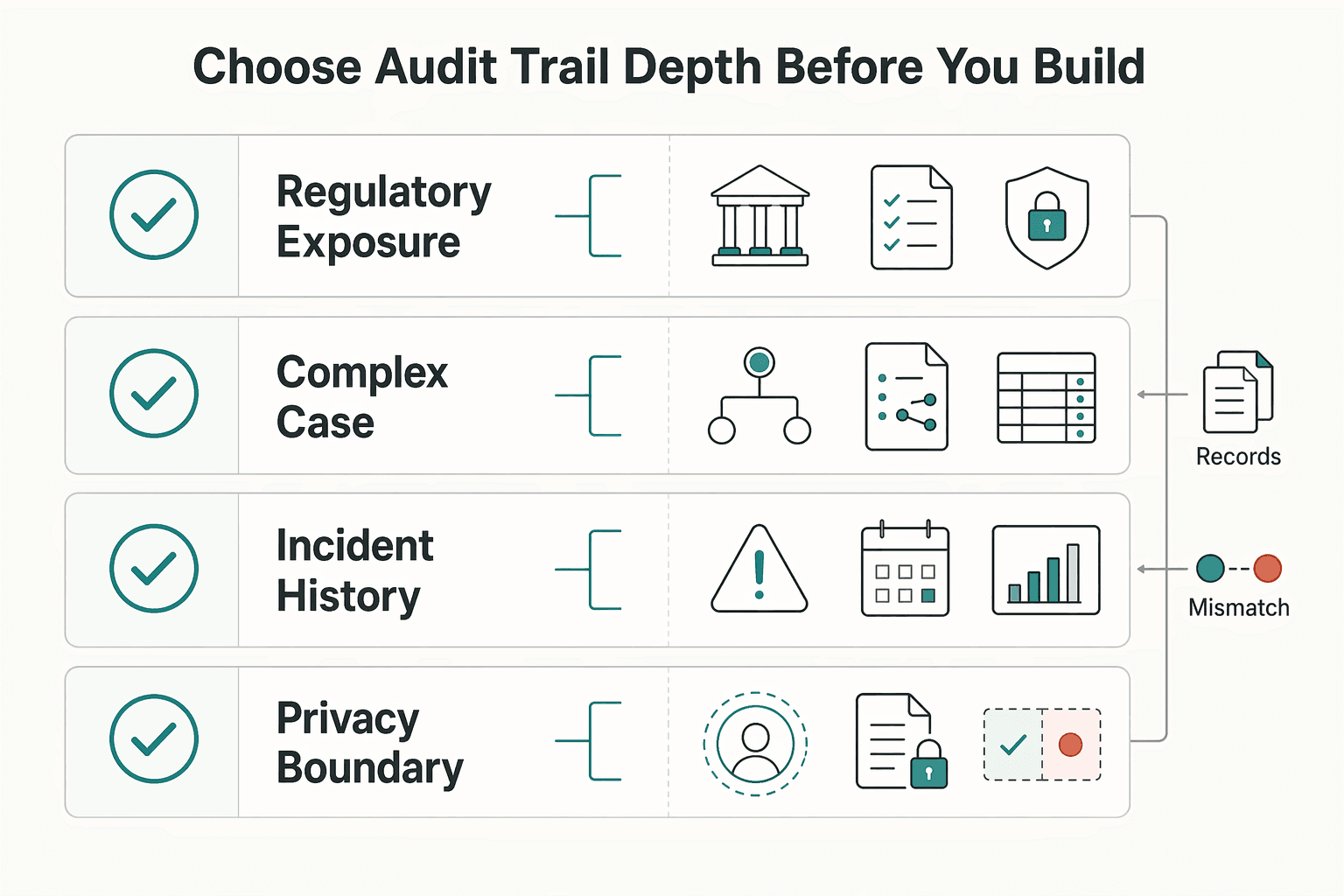

How to choose audit trail depth before you build#

Choose audit-trail depth before you choose tooling. The right depth comes from regulatory exposure, investigation needs, and privacy limits, not just from whatever your systems already happen to emit. This is a control-sizing step, not jurisdiction-specific legal advice.

| Factor | What to examine | Why it affects depth |

|---|---|---|

| Regulatory exposure | PCI DSS Requirement 10; SOX Section 404 when payout activity feeds financial reporting | Requirement 10 requires tracking and monitoring access to network resources and cardholder data, and SOX Section 404 raises control expectations |

| Operational complexity (volume and handoffs) | Trace one payout across approvals, provider updates, reversals, and manual interventions | If reconstruction depends on CSV exports, inbox searches, or chat screenshots, defensibility may be weaker |

| Incident history and prioritization | Use dispute and investigation history; check for status timestamps with no durable approval, override, or exception rationale | Controls can be prioritized by expected risk reduction versus time and resources |

| Privacy boundary | Keep operational facts, but minimize personal data fields where masked identifiers and restricted access still meet the control objective | More logging is not automatically better |

Start with a reconstruction test on one disputed payout. Can you assemble who acted, what changed, when it happened, where the action occurred, and why it was allowed from durable records such as event history, approvals, and reconciliation or exception notes?

- Regulatory exposure

If you accept or process payment cards, PCI DSS applies. Requirement 10 requires tracking and monitoring access to network resources and cardholder data, so shallow logging is hard to defend in card scope. If payout activity feeds financial reporting, SOX Section 404 also raises control expectations because management must report on internal control over financial reporting.

- Operational complexity (volume and handoffs)

Volume and handoffs are not legal triggers by themselves, but they increase the chance that records fragment across systems. Trace a single payout across approvals, provider updates, reversals, and manual interventions. If reconstruction depends on CSV exports, inbox searches, or chat screenshots, defensibility may be weaker.

- Incident history and prioritization

Use your own dispute and investigation history to set depth. NIST log-management guidance supports prioritizing controls by expected risk reduction versus time and resources, especially where logs support investigations and retention outcomes. One gap to check for is status timestamps with no durable approval, override, or exception rationale.

- Privacy boundary

More logging is not automatically better. GDPR Article 5(1)(c) requires personal data to be adequate, relevant, and limited to what is necessary, and ISO/IEC 27701 emphasizes accountable privacy management. Keep operational facts, but minimize personal data fields where masked identifiers and restricted access still meet the control objective.

If you want a deeper dive, read How to Build an Internal Payment Audit Trail: Logging Approvals and Changes for Compliance.

Minimum viable vs mature controls at a glance#

Build these controls in phases, but do not confuse a phased build with an adequate stopping point. If you are in PCI DSS Requirement 10 or SOX 404 scope, minimum viable controls are hard to defend unless you can show reviewer ownership, escalation paths, and retention evidence on demand.

That framing matches the underlying control guidance. NIST SP 800-92 treats log management as end to end, from generation through disposal. NIST AU controls support defined review frequency, named reporting roles, and time-correlated trails. PCI DSS Requirement 10 requires protecting audit logs from destruction or unauthorized modification and reviewing logs for anomalies or suspicious activity.

| Lifecycle stage | Minimum viable controls | Mature controls | Best for | Cost of getting this wrong |

|---|---|---|---|---|

| Initiation | Create an immutable event for each payout request with actor, timestamp, amount, payee reference, and source action. Keep a basic retention register showing storage location and access ownership. | Maintain a time-correlated, system-wide trail that links request creation to upstream trigger, service or device identity, and later field changes without overwriting history. Add replay capability for the exact initiation state. | Teams moving from ad hoc exports or mutable rows to durable records. | Weak opening records make every later review harder to defend. |

| Approval | Capture reviewer identity, decision, and decision time in the same durable trail. Define escalation destinations for out-of-policy approvals. | Enforce named reviewer ownership by approval type, dual review for high-risk actions, and evidence that approval rules were current at decision time. | Smaller teams with manual approvals and clear accountability. | If approval ownership is unclear, authorization evidence is hard to prove. |

| Screening | Log screening outcome, rule or list version, and whether the payout was cleared, held, or escalated. Use case references for exceptions, not only status flags. | Preserve full screening history, including re-screens, analyst rationale, and linked case outcomes so you can replay why a payout advanced or stayed blocked. | Programs with basic screening and manageable exception volume. | Status-only logs are difficult to defend in investigations. |

| Execution | Record provider submission, provider response, internal status changes, and failure codes as append-only events. Protect logs from unauthorized modification or deletion. | Correlate internal execution events with provider callbacks, retries, reversals, and batch identifiers across services for a single timeline. | Platforms integrating one or two payout rails. | Disputed timing and missing handoffs create costly reconciliation and investigation work. |

| Reconciliation | Keep dated reconciliation outputs, unmatched-item logs, and reviewer signoff. Show periodic review at an organization-defined frequency. | Link reconciliation exceptions back to initiation, approval, and execution events, with aging, owner, closure evidence, and retained review history. | Finance teams that need weekly or monthly close support before full automation. | If reconciliation cannot be traced to source events, evidence credibility drops. |

| Correction | Never overwrite the original event. Log corrective action, approver, reason, and related transaction reference. | Use explicit correction classes, such as reversal, reissue, and manual adjustment, with required rationale, approvals, and linked outcome evidence. | Teams handling occasional operational fixes that still require auditability. | Silent edits break replay traceability and raise tampering concerns. |

What separates viable from mature#

The difference is not log volume. It is whether the records remain usable across generation, storage, access, review, and disposal. Minimum viable controls establish durable facts. Mature controls add ownership, exception discipline, and replay traceability so the evidence still stands up months later.

Use a simple checkpoint: pull one corrected payout and request the initiation event, approval record, screening result, execution handoff, reconciliation line item, and correction rationale. If any piece exists only in email, chat, or spreadsheet attachments, the control state is still fragile.

When minimum viable is enough for now#

Minimum viable can be acceptable as a phase, but only when review and escalation are actually operating. NIST AU-6 supports defined review frequency and named recipients for findings. PCI's prioritized approach supports phased risk reduction, but no single milestone equals full compliance, and full PCI DSS compliance still requires meeting all requirements.

So keep early scope tight, but do not skip tamper protection, periodic evidence review, or escalation ownership. If these controls sit inside a broader internal-control program, use this operating evidence to support that wider control set.

Weak recordkeeping can carry material downside. In 2024, the SEC announced combined civil penalties of $392.75 million in a recordkeeping action set. Different fact patterns do not change the lesson: if you cannot show ownership, retention, and reconstruction, control risk rises quickly.

Related: Music Royalty Tax Compliance: How Platforms Handle 1099-MISC vs. 1099-NEC for Artist Payments.

If you are mapping ownership, evidence artifacts, and escalation paths, use Gruv's docs to align API events, payout states, and reconciliation outputs with your control matrix.

Control 1: Immutable event ledger for transaction truth#

If payout history is editable in place, fix this first. An immutable, append-only ledger becomes essential when payouts move through multiple steps and webhook updates can arrive asynchronously, be retried for up to three days, or appear more than once.

What it is#

The rule is simple: append events, do not overwrite them. Each material action becomes a durable record with its own timestamp, actor or service identity, transaction reference, and outcome. That gives you a replayable history instead of one mutable current-status row.

This matters quickly in payment operations. Duplicate or delayed messages can blur sequence when handlers update records in place. Stripe notes that webhook endpoints might receive the same event more than once, and some fulfillment logic can run multiple times, possibly concurrently, for the same session.

Why it earns its keep#

This pays for itself during reconstruction. In a payout dispute, you need to line up approval time, provider submission time, callback or status-update time, and ledger posting time without relying on edited records or backfilled notes.

It also aligns with established expectations. NIST log guidance treats log management as a lifecycle and calls for protecting audit information from unauthorized modification or deletion, with synchronized timestamps for reliable correlation. PCI DSS Requirement 10 focuses on tracking and monitoring access, and PCI guidance ties logging to forensic effectiveness. For SOX 404-scoped programs, the same ledger can help management show how financially relevant transactions moved through internal control points without silent edits.

What to record#

At minimum, append each event with:

- Internal transaction reference

- Event type and outcome, for example approval granted, provider submitted, callback received, or reversal initiated

- Actor or service identity

- Provider event ID, callback ID, or batch reference when available

- Timestamp from a synchronized clock

- Link to the related prior event or correction record, not a replacement

Use one practical test: reconstruct a payout older than 30 days without depending on provider event-list APIs. Stripe's event listing window is 30 days, so your own retained records have to carry the long-term trail.

Where teams stumble#

The hard part is correction design. In append-only systems, corrections have to be reversible business actions, not silent edits to the original rows.

Watch for mutable side paths in spreadsheets, chat, or admin tools, and for deduplication rules that remove retry evidence. When duplicates occur, retain the original provider event IDs and record the processing decision instead of deleting duplicate records.

For a step-by-step walkthrough, see Transaction Monitoring for Platforms: How to Detect Fraud Without Blocking Legitimate Payments.

Control 2: Approval chain integrity with SoD and Dual Approval#

If an action can change beneficiary, amount, or routing, a strong default is Segregation of Duties (SoD) plus Dual Approval by two different authorized users. If you allow an exception, record it when the change happens, with the reason.

What this control is really doing#

The point is simple: one person should not be able to misuse a sensitive process alone. NIST defines SoD that way, and describes the two-person rule as a dynamic SoD pattern where the second authorized user is different from the first.

That is why approval-chain integrity is more than a role setting. You need a durable record linking request, review, and execution. A second click by the same person, a shared admin account, or one service identity acting for both steps is not meaningful separation.

Where to apply it#

Apply dual approval to actions that can cause direct financial loss or misdirection, not to every routine task. That usually means:

- Beneficiary changes, including payout destination or recipient identity

- Amount changes, threshold overrides, or manual release of held funds

- Routing changes, such as provider selection or payout path edits

- Privileged admin actions that can bypass normal approval logic

For lower-impact actions, document why single approval is acceptable and keep that rule in policy. A key risk is inconsistency across paths, especially in emergency flows.

Evidence that stands up#

For PCI DSS Requirement 10, focus on accountability in the logs. The requirement set covers defined and documented logging processes in 10.1. It also covers capture of admin actions in 10.2.1.2, and protection of audit logs from unauthorized modification or destruction in 10.3. For a privileged payout-rule change, logs should show requester, approver, affected object, and execution time.

For SOX 404, the link is strongest when payout approvals affect internal control over financial reporting (ICFR). Section 404(a) requires management assessment and reporting on ICFR effectiveness, and 404(b) requires auditor attestation for in-scope companies. If your organization is not clearly in SOX scope, do not assume the label applies.

What to verify before you trust it#

Before you rely on this control, spot-check a recent sensitive change. Confirm:

- Requester and approver are different users

- The affected data, system, or component is explicitly identified

- Before and after values are visible where available

- Approval evidence is linked to the final execution event

A practical failure mode to watch for is split evidence: approval in chat or email, execution in an admin console, and only the final state retained. If you need deeper implementation patterns, see Internal Controls for Payment Platforms: Segregation of Duties Dual Approval and Audit Trails. That guide goes further on ownership and enforcement.

Control 3: End-to-end payment state logging across money movement#

If you cannot reconstruct a payment after it leaves your app, the control is incomplete. For cross-border flows that can include states like invoice, conversion, payout, return, and reversal, keep one linked history of state transitions so reconciliation does not depend on disconnected tools.

This matters most when outcomes are asynchronous. Payment providers note that in many integrations, final status is not known at API request time, and webhooks deliver later state changes. For review, the evidence should cover the original request, each external status update, and the internal action triggered by each update.

What to capture end to end#

Treat the control object as transaction lineage, not a single payout row. For one payment, keep a chain from invoice confirmation or payable creation through FX conversion (if any), payout submission, provider acknowledgment, batch update, and any return or reversal.

| Lifecycle point | What to log | Why it matters |

|---|---|---|

| Initiation | internal transaction ID, payer or payee reference, amount, currency, creation timestamp | anchors business intent before movement starts |

| External processing | provider event ID, webhook event type, delivery timestamp, resulting status | preserves asynchronous changes not known at request time |

| Cross-border tracking | message reference such as UETR where available, route or rail used, settlement currency | improves traceability across providers or jurisdictions |

| Correction events | return reason, reversal trigger, linked original payment ID, operator or automated actor | preserves why funds moved back, not only that they moved |

In SWIFT or Fedwire mapping contexts, UETR is a practical tracking key. Fedwire market practice states specified notifications must include UETR, and it can be up to 36 characters including dashes. Do not treat UETR as universal across all cross-border payments, but where available, store it early and carry it through downstream events.

Why this stands up better in reviews#

The value here is a usable reconstruction path, not just more log volume. PCI DSS describes a baseline for protecting payment account data, and Requirement 10 is about tracking and monitoring access to network resources and cardholder data. A linked state history is not explicitly mandated as one chain, but it makes Requirement 10 evidence more useful when reviewers ask how external updates and internal actions led to the final outcome.

It also fits the log-management discipline described in NIST SP 800-92 and gives you a cleaner review narrative.

What to verify before you trust it#

Test one recent payment whose status changed after the initial API call. Confirm the internal transaction ID links to provider event IDs, webhook timestamps are preserved, and any return or reversal links back to the original payment.

Watch for two common gaps: state views that only show current balances, and webhook-driven handling without reconciliation. Stripe retries live-mode webhook deliveries for up to 3 days and allows querying missed events over a selected period. If you cannot show which events were replayed or recovered, the timeline is incomplete.

Related reading: SOC 2 for Payment Platforms: What Your Enterprise Clients Will Ask For.

Control 4: Exception queue and investigation trail#

Once you can reconstruct payment state changes, abnormal events that can affect fund movement or compliance should go through a documented investigation case, not informal messages. For teams dealing with unmatched deposits, compliance holds, provider failures, or stale quote rejects, this is what turns recurring noise into accountable handling.

The key point is process, not tool choice. NIST log-management guidance frames logs as a full lifecycle discipline and ties them to incident investigation and retention. In practice, each exception needs an owner, a timeline, and linked evidence.

Four parts that make the queue defensible#

| Queue stage | What to record | Why it matters |

|---|---|---|

| Detect and classify | Internal transaction ID, provider event or reference ID if available, detection timestamp, trigger source, current payment status, and initial severity or queue tag | The case needs to tie back to the transaction lineage |

| Freeze or contain when risk justifies it | Why the hold was applied, what clears it, who applied the hold, when, what it covered, and what report or escalation followed | Shows why funds were paused and what happened next |

| Assign one owner and capture decision rationale | One accountable owner, who reviewed what, which artifacts were checked, whether legal or compliance was consulted, and why the final decision was made | Keeps accountability clear even when multiple teams contribute |

| Close with resolution artifacts linked to the audit record | Reconciliation output, provider confirmation, reversal records, sanctions reporting evidence, or approval to release funds | Creates one reviewable history of event trail, investigation trail, and closure evidence |

- Detect and classify

Open the case from a specific anomaly, not a vague complaint. Capture the internal transaction ID, provider event or reference ID if available, detection timestamp, trigger source, current payment status, and initial severity or queue tag.

The test is linkage: if the case cannot tie back to the transaction lineage from the prior control, the investigation trail is incomplete.

- Freeze or contain when risk justifies it

Not every exception should pause funds, but some should. If the pattern suggests blocked property, sanctions exposure, or suspicious activity, consider a temporary hold while the case is reviewed under your legal and compliance policy.

Record why the hold was applied and what clears it. For OFAC-relevant scenarios, 31 CFR 501.603 covers reporting tied to holding, unblocking, or transferring blocked property. So the case record should show who applied the hold, when, what it covered, and what report or escalation followed.

- Assign one owner and capture decision rationale

Assign one accountable owner per case, even when multiple teams contribute. NIST SP 800-61 Rev. 3, with Rev. 2 withdrawn on April 3, 2025, describes incident handlers as responsible for verifying incidents, analyzing evidence, and prioritizing response across shared roles.

Capture who reviewed what, which artifacts were checked, whether legal or compliance was consulted, and why the final decision was made. In banking contexts, SAR obligations and related FAQs reinforce that even a decision not to file should be documented.

- Close with resolution artifacts linked to the audit record

A case is closed only when final resolution evidence is attached to the same transaction and investigation chain, not when someone says it is fixed. Artifacts can include reconciliation output, provider confirmation, reversal records, sanctions reporting evidence, or approval to release funds. That gives you a reviewable history in one place: event trail, investigation trail, and closure evidence.

What usually goes wrong#

The common failure is resolving in chat, email, or calls and never linking the outcome back to the case and audit record. Standards may not ban those channels, but they do require incidents to be tracked, documented, and reported, and they emphasize correlating audit review and response for suspicious or unusual activity.

The second failure is queue sprawl. Without clear ownership, aging review, and closure standards, items sit unowned even when they affect fund release, reversals, or sanctions and suspicious-activity decisions.

What to verify before you trust it#

Test one closed case and one open case. For the closed case, confirm the anomaly trigger, containment action if any, owner, rationale, and final artifact are all present and tied to the same transaction. For the open case, confirm active ownership and that interim actions, including holds, escalations, and updates, are logged as they happen.

If you keep one rule, use this: when a decision can change whether money moves, record that decision in the case before funds are released or a hold is lifted.

Control 5: Retention, minimization, and access boundaries#

This control works best when you do three things together: keep evidence of what happened, minimize personal data around that evidence, and restrict access by role.

Keep the evidentiary core, minimize personal data around it#

Your trail should preserve the operational facts needed to explain decisions and money movement while limiting personal data to what is necessary for that purpose. Under GDPR data minimisation, personal data should be adequate, relevant, and limited to what is necessary.

In practice, keep event history usable while limiting exposure of sensitive personal fields. Reviewers should be able to verify what happened from limited personal-data views, while only roles with a clear need can access raw sensitive details. In payment environments, PCI DSS remains a baseline framework for protecting payment account data.

Use a simple test: can a reviewer reconstruct what happened from a minimized record? If not, minimization went too far. If unrestricted sensitive data is broadly visible, it did not go far enough.

Set retention by record class, not one blanket period#

Retention should be purpose-based and justifiable, not one global timer. Storage limitation requires that personal data is not kept longer than needed, and you should be able to justify retention periods.

Use a documented policy with standard periods where possible, then review data and erase or anonymise it when no longer needed. Apply those rules by record class where purpose and obligations differ, rather than treating all nearby records the same. Log-management expectations also include storing records for their required period, so retention belongs inside the control design.

Watch for both extremes: indefinite retention of everything, or aggressive purging that removes context needed for later review. If legal, tax, or regulatory holds apply, document them so routine deletion does not remove required evidence.

Enforce role-based access and prove it#

Access boundaries should be role-based and formally assessed. Access control guidance emphasizes assigning appropriate access rights and restricting sensitive systems to roles that require privileged access.

Operationally, this usually means tiered visibility: limited-data access for most users, narrower case-linked detail for specific roles, and tightly approved access to raw sensitive records. ISO/IEC 27701 can support a structured privacy management approach, and role boundaries still need to be explicitly defined by your organization.

Validate this control with sampling: compare role definitions to real permissions and verify that privileged access activity is logged. If the model depends on broad just-in-case production access, the privacy risk is too high for the evidentiary benefit.

Control 6: Audit-ready evidence pack for reviews and regulator requests#

Do not wait for an auditor, legal team, or regulator to ask. Build one repeatable evidence-pack format and refresh it on your review cycle. The goal is a complete, understandable record that shows how decisions were made, how money moved, and how controls were reviewed.

A credible pack is more than raw log exports. It should show that logs support detection and forensic analysis, are protected from unauthorized change or destruction, and are actively reviewed. For SOX 404-scoped processes, include evidence of management responsibility for ICFR and management's effectiveness assessment.

What the pack must contain#

Use the same checklist every cycle so reviewers can confirm completeness quickly. At minimum, the pack should contain:

| Artifact | What to include | Primary owner | Why it matters |

|---|---|---|---|

| Event history | Time-bounded export of payout lifecycle events, linked IDs, status changes, and source systems | Ops | Reconstructs who did what, when, and in what order |

| Approvals evidence | Approval records for high-risk actions, approver identity, timestamps, rationale, delegated authority if used | Compliance | Shows decision ownership and supports control design |

| Change logs | Configuration or rule changes affecting beneficiary, amount, routing, thresholds, or review logic | Ops | Shows whether a later issue came from a process change |

| Exceptions and investigations | Open and closed exception cases, case notes, linked underlying transactions, closure decision | Compliance | Helps keep exception handling in the official record |

| Reconciliation outputs | Period-end reconciliations, breaks, resolution notes, and follow-up evidence | Finance | Connects transaction history to financial reporting and settlement outcomes |

| Retention and review proof | Evidence records are stored for required periods, plus review records with reviewer, findings, and follow-up | Compliance | Shows logs are governed, not merely stored |

| SOX 404 artifacts where applicable | Management responsibility statement, effectiveness assessment, and external auditor attestation report for annual SOX work | Finance | Supports ICFR evidence for SOX-scoped processes |

| Tax-adjacent reporting artifacts where applicable | Classification memo, filing extracts, and recipient statement examples for Form 1099-NEC or Form 1099-MISC | Legal or Finance | Supports payout reporting without unnecessary payee-data exposure |

Who owns what#

This control often fails when ownership is implied instead of assigned. Documented responsibilities prevent familiar gaps such as missing change logs, incomplete review records, or exceptions that do not map back to payouts.

One workable split is this. Ops owns event history and change logs. Compliance owns approvals, exception-case quality, and log-review records. Finance owns reconciliation outputs and SOX 404 linkage. Legal owns retention holds, regulator-response review, and disputed tax-classification positions. If delegated authority exists, document that too.

What makes the pack immediately usable#

A pack is audit-ready when a reviewer can resolve a disputed payout without hunting for missing context. For each artifact, label the reporting period, source system, owner, and covered population.

For review evidence, include who reviewed, what they checked, what they found, and whether follow-up was opened. Common failure modes are disconnected exports and proof of log existence without proof of tamper resistance or review.

Handling 1099 evidence without leaking more PII#

Include only what you need to support reporting treatment: classification evidence, filing extracts, and recipient-statement samples with identifiers masked where possible. Truncated taxpayer identification numbers on payee statements can reduce identity-theft risk.

Keep classification evidence explicit, because some payment card and third-party network transactions are not reported on Form 1099-NEC or Form 1099-MISC. If 1099 reporting is in scope, keep filing-calendar evidence on file. That includes January 31 for Form 1099-NEC, February 28 for paper or March 31 for electronic filing of Form 1099-MISC, the 10-return aggregate e-file threshold effective for returns filed on or after January 1, 2024, and the tax year 2026 and filing season 2027 IRIS intake transition.

Control 7: Escalation triggers you should not handle as routine ops#

Use your evidence pack to decide when to stop routine handling and escalate. If a payout case includes unexplained audit-log gaps, signs that audit trails may have been altered, or conflicting timestamps on financial actions, treat it as a control-integrity event first and an ops issue second.

| Escalation trigger | What to do first | Why it is not routine ops |

|---|---|---|

| Unexplained missing log entries, signs of audit-trail alteration, or conflicting times for the same payout action | Preserve the original state, check clock-synchronization controls, and confirm whether the issue touches payout initiation, approval, execution, or reversal | These conditions can undermine the reliability of the record itself |

| Logging-control failure in PCI DSS scope or a SOX-linked ICFR process | Route the case immediately to finance, compliance, and internal-controls owners | A potential material weakness is escalation-grade, not routine ops work |

| Unclear breach-notification or disclosure obligations | Escalate to counsel and specialist advisors before sending remediation messaging | Timing rules are framework-specific |

Log gaps, audit-trail integrity, and timestamp conflicts#

Escalate immediately when any of these signals appears: unexplained missing log entries, signs of audit-trail alteration, or conflicting times for the same payout action. These conditions can undermine the reliability of the record itself, not just how it looks in a report.

Before any remediation note, preserve the original state and check whether the affected systems were under clock-synchronization controls. Then confirm whether the issue touches payout initiation, approval, execution, or reversal. Under PCI DSS Requirement 10, synchronized clocks, protected audit trails, and anomaly review support reliable investigation sequencing.

When this becomes a PCI DSS or SOX 404 matter#

Escalate faster when the control failure is in PCI DSS scope or affects a SOX-linked ICFR process. Unresolved logging-control failures in PCI scope should not sit in routine queues.

For ICFR-linked processes, ask directly whether the deficiency could affect management's ICFR conclusion. If the answer may be yes, route the case immediately to finance, compliance, and internal-controls owners. A potential material weakness is escalation-grade, not routine ops work.

If legal meaning is unclear, pause the messaging#

If breach-notification or disclosure obligations are unclear, escalate to counsel and specialist advisors before sending remediation messaging. Timing rules are framework-specific. GDPR Article 33 uses a 72-hour window after awareness in relevant cases, while SEC Form 8-K Item 1.05 uses four business days after a materiality determination.

Keep escalation handoffs in one documented case trail, not fragmented across chat, email, and separate tickets. Record, at minimum:

- who handled the case or asset

- date and time of transfer

- purpose of transfer

That chain-of-custody detail keeps the escalation defensible. If the handoff trail breaks, the integrity risk becomes part of the incident.

Common mistakes that make audit trails look strong but fail in practice#

Once your escalation criteria are clear, do not assume the trail you already have is stronger than it is. In practice, audit trails often fail not just from missing events, but from weak attribution, weak governance, and unnecessary data collection.

- Calling storage "tamper-proof" and stopping there

Storage-only controls are incomplete. NIST defines log management as a full lifecycle: generating, transmitting, storing, accessing, and disposing of log data. Review the whole operating model, not just immutability at rest: access, administration, monitoring, and retention. Otherwise, you can have immutable files while collection, forwarding, or review gaps persist.

- Recording events but not decisions and outcomes

Event logs alone are not enough for investigations. You need the decision trail too: who acted and what the investigation concluded. PCI DSS Requirement 10 requires tracking and monitoring access, and PCI DSS 10.1 ties audit trails to each individual user. A practical test is whether one disputed payout can be reconstructed end to end from the available trail.

- Leaving controls undocumented or ownerless

Ownerless controls produce weak evidence. Under Section 404 and SOX 404 reporting expectations, management must report on internal control over financial reporting, and unclear ownership makes control operation hard to defend. If teams give conflicting answers on who reviews logging exceptions, treat that as a control failure, not a communication issue.

- Collecting more sensitive data than the purpose requires

Over-collection creates avoidable privacy risk. Regulation (EU) 2016/679 requires personal data to be adequate, relevant, and limited to what is necessary, with storage periods limited to a strict minimum. If you align with ISO/IEC 27701, accountability for PII processing reinforces that discipline. Keep the operational facts you need, but restrict sensitive fields and set retention by record class instead of one catch-all bucket.

Conclusion#

A strong payment audit trail is not the one with the most records. It is the one that can reliably reconstruct a transaction, show who approved what, and document how exceptions or control failures were handled without relying on memory, chat, or spreadsheet backfills.

- Prove transaction truth first.

Start with records that answer the core dispute question: what happened, in what order, and what is the durable source of truth. Log management is a full lifecycle, not just storage, so the real test is reconstruction quality. If one payout can be pulled with initiation, approval, execution status, exception notes, and reconciliation output in one evidence pack, your controls are more likely to hold up.

- Make ownership explicit where money or reporting can change.

Clear decision ownership is operationally necessary and important to SOX 404 accountability. A defensible standard is attributable approval, not a status field that only says "approved." Keep owner identity, timestamp, role context, and override rationale in the same case history so authority and control decisions are verifiable later.

- Mature controls in risk order, not log-volume order.

After the core proof points are stable, prioritize improvements by risk. PCI DSS is a baseline, and the PCI SSC Prioritized Approach is a roadmap for sequencing work, not a substitute for full compliance. Benchmark your process against the comparison table and evidence checklist, then fix the first two gaps most likely to reduce regulatory surprise, often around exception linkage and retention or review evidence. If PCI DSS is in scope, verify current version requirements. Older quick-reference checks, including daily critical log review, one-year retention, and three months immediately available, are still useful for direction.

Final rule: do not add more logs until a single sample transaction can already prove truth, ownership, and escalation. If you want a practical review of your current payout audit-trail controls and escalation design, contact Gruv.

Frequently Asked Questions

What is an audit trail in a payment platform, in plain terms?

An audit trail is the record of who accessed the system and what they did, so you can reconstruct what happened later. In payment operations, it should let you follow activity across the full flow, not just confirm that a payout occurred. That can include the approval path, status changes, exceptions, and reconciliation outcome in the same case history.

What makes a transaction log tamper-evident instead of just “stored”?

Tamper-evident means changes can be detected, not that changes are impossible. A stronger setup protects audit information and logging tools from unauthorized access, modification, and deletion, and alerts when logging fails. A practical check is whether you can quickly detect and investigate events such as capture failures, unauthorized record changes or deletion, or storage capacity being exceeded.

Which compliance regimes are most relevant to payment audit logging?

PCI DSS is a core baseline when payment account data is in scope because it sets technical and operational requirements for protection. Its log guidance points to daily review for critical systems and retaining audit trails for at least one year, with at least three months immediately available for analysis. If your operations affect financial reporting, SOX 404 and related SEC ICFR expectations may also apply.

What is the minimum evidence pack an internal audit or regulator will expect?

Start with the AS 1215 structure: what was planned and performed, which procedures were used, what evidence was obtained, and what conclusions were reached. In payment investigations, that typically means records of the event history and procedures performed, the evidence reviewed, the conclusions reached, and evidence that access and retention controls were applied. If pulling one sample transaction still requires stitching together chat and email, the pack is not yet reliable.

How do we choose between minimum viable controls and mature controls?

Use risk as the decision rule. AS 1105 states that as risk increases, the amount of evidence should increase as well. If risk is higher, move beyond minimal logging toward stronger attribution, review, and exception linkage. If risk is lower, minimum viable controls can be acceptable when ownership, retention, and escalation are operating consistently.

When should compliance or legal be escalated immediately instead of handled by operations?

Escalate immediately when the audit logging process fails. NIST 800-171 treats failures such as capture breakdowns, software or hardware errors, and storage capacity exhaustion as alert-triggering events. Also consider immediate escalation when a control issue could affect PCI DSS scope or materially affect an ICFR process.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- csrc.nist.gov/CSRC/media/Projects/risk-management/document...trusted

- csrc.nist.gov/glossary/term/audit_trailtrusted

- fdic.gov/news/financial-institution-letters/2025/freq...trusted

- govinfo.gov/content/pkg/GOVPUB-C13-PURL-LPS69969/pdf/GOV...trusted

- irs.gov/instructions/i1099mectrusted

- irs.gov/government-entities/federal-state-local-gove...trusted

- sec.gov/files/rules/final/33-8238_0.htmtrusted

- sec.gov/newsroom/press-releases/2024-98trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Internal Controls for Payment Platforms That Hold Up in Audit

If you own payout risk, start with a short control set you can operate, verify, and defend when a payout is challenged by compliance, finance, legal, or audit. This ranked list of seven controls aims to reduce real release risk without adding approval theater. It is not a claim that seven controls are always enough.

Internal Payment Audit Trail for Platform Compliance

In the first implementation phase, stand up a narrow, retrieval-focused audit trail baseline. You are not building a complete control program yet. The goal is a shared operating model so compliance, legal, finance, and risk can answer the same questions from one evidence set: who approved what, what changed, and how quickly you can produce it.

Music Royalty Tax Compliance: How Platforms Handle 1099-MISC vs. 1099-NEC for Artist Payments

This is an operating-model decision, not a year-end form choice. A team can ship quickly and still end up with misclassified payouts, correction cycles, and filing risk if the classification logic is weak. If you run creator payouts, you need the classification rule before your first batch, not after your first correction cycle.