Quick Answer

Build an internal payment audit trail by starting with a narrow, retrieval-focused baseline that lets non-engineers produce one evidence set for a payout or policy change. Log approvals, policy edits, access changes, exception overrides, and linked payout events with actor, action, timestamp, object, before-and-after state, and approval chain, then preserve corrections as append-only amendments and make exports reviewable without screenshots or ad hoc SQL.

Build a compliance ready payment audit trail without overbuilding#

In the first implementation phase, stand up a narrow, retrieval-focused audit trail baseline. You are not building a complete control program yet. The goal is a shared operating model so compliance, legal, finance, and risk can answer the same questions from one evidence set: who approved what, what changed, and how quickly you can produce it.

Define the phase-one outcome#

Set a modest target: a baseline that can hold up in internal review and early diligence without engineering having to reconstruct the story by hand.

Test it with one payout and one policy change, retrieved by someone outside engineering. They should be able to show actor, action, timestamp, affected object, approval path, and before-and-after state from one evidence set. If they still need screenshots, Slack messages, or ad hoc SQL, you have logs, not an audit trail.

Design for retrieval that stands up to scrutiny, not maximum logging#

The real tradeoff is speed versus evidence quality. Payouts still need to move, but the record also needs to hold up to regulatory and diligence scrutiny.

Design for retrieval under pressure. SEC electronic recordkeeping expectations focus on maintenance, preservation, and prompt production of records. For in-scope firms using third-party recordkeepers, examination access and prompt furnishing matter too.

Keep the scope honest. Rule 17a-4 electronic recordkeeping requirements apply to broker-dealers and related SEC categories, not automatically to every U.S. payments platform. If your model could fall into an SEC-regulated category, bring in counsel early. If not, build to a comparable evidence standard anyway.

Treat overwrite-only history as a red flag. The SEC's audit-trail alternative requires a method that permits recreation of the original record if it is modified or deleted.

Set U.S./Europe boundaries before building controls#

If you operate across the United States and Europe, settle the boundary questions early or you will redesign controls later. This guide is practical for multi-market platforms, but final control design still needs specialist legal review.

In Europe, directives set outcomes and are transposed by Member States, so local implementation can change how controls are interpreted and evidenced. PSD2 provides an EU-wide payments foundation, but not one unchanged implementation path.

For phase one, build to a common denominator: clear decision history, retention intent, and prompt exportability across markets. Then use legal review to add stricter country-specific or entity-specific controls where required.

Use SEC staff FAQs for orientation, not as final authority. They do not have legal force, so validate the final design against binding rules, your entity structure, and counsel guidance.

For control design, see Internal Controls for Payment Platforms: Segregation of Duties Dual Approval and Audit Trails.

Set prerequisites and owners before you touch a single log line#

Set accountability and scope first or your evidence will fragment and retrieval will fail when you need it most.

Name accountable owners and split sensitive duties#

Assign accountable owners for control areas such as approvals, policy changes, access administration, and record custody, and involve compliance, legal, finance, and engineering as needed. Keep senior ownership explicit, even when operators handle the day-to-day work.

For sensitive actions, apply segregation of duties and dual control so one person cannot request, approve, and implement the same change. Use a payout-limit change as a quick test: you should be able to show a requester, a separate approver, and a reviewer. If one admin can edit policy, grant access, and release funds, treat that as a control gap before you worry about logging.

Confirm entity and program scope first#

Before you design controls, define which legal entities, products, and payment programs are in scope for phase one. Then resolve one legal scoping question early: does any activity look like broker or dealer activity?

This matters because a broker is in the business of buying or selling securities for others, while a dealer buys or sells securities for its own account. If any program is close to that line, pause and document counsel's decision. Do not assume that "we only handle payouts" keeps you outside broker-dealer scope.

Freeze a practical phase one perimeter#

Keep the first boundary narrow, for example payouts, policy changes, and access changes. This is a practical build boundary, not a regulator-mandated list.

Hold that scope through the first audit drill where possible. Expanding too early into disputes, onboarding, and exceptions can create inconsistent fields and weak reviewer chains.

Choose one evidence home and export authority#

Choose one primary audit log system. Then define who can export, who approves exports, and what format exports must take. A useful test is whether someone outside engineering can retrieve one complete evidence package without screenshots, ticket archaeology, or ad hoc SQL.

If SEC or FINRA books-and-records obligations may apply, confirm retention and accessibility at design time. Some SEC Rule 17a-4 records require 3-year or 6-year preservation, with the first 2 years easily accessible. Records and audit trails may also need to be furnished in a reasonably usable electronic format.

Related reading: How to Build a Payment Sandbox for Testing Before Going Live.

Define the event catalog your compliance audit trail must capture#

Build the catalog around control decisions, not screens. If an event can change who may move money, what policy applied, who got access, or why a transaction monitoring case was closed, it belongs in phase one.

That turns the scope from the last section into a usable event matrix so compliance, finance, and engineering can retrieve the same record set under pressure.

Build the event families around control decisions#

Start with five families: payment approvals, policy edits, role and access changes, exception overrides, and case outcomes from transaction monitoring. That set is often enough for a phase-one baseline covering the points where control intent and operational reality diverge.

| Event family | Decision points to log |

|---|---|

| Payment approvals | approval action, not only final payout state |

| Policy edits | draft submission; approval; publication; rollback |

| Role and access changes | grants; removals; privilege changes; break-glass access |

| Exception overrides | bypassed rule; approver; expiry |

| Monitoring cases | alert disposition; reviewer; escalation decision; closure reason |

Log the decision points shown above, not just end states. If an event changes money movement, decision authority, or the evidence chain, include it. If it is only a UI convenience event, leave it out.

Require the same core fields on every event#

Standardize the schema early. Use one core set of fields across families: actor, action, timestamp, object, before state, after state, and approval chain. If a producer cannot emit those fields, fix the producer instead of creating schema exceptions.

Be strict about attribution. The actor should be a named person or a distinct approved account identifier, not a shared admin label. The object should be explicit, such as payout ID, policy version, role assignment, or case ID. Before and after state matters most for policy edits, role changes, and overrides.

Entity-specific books-and-records rules reinforce this approach. Where applicable, Advisers Act Rule 204-2 requires records that are true, accurate, and current, including person-level attribution and core trace fields for certain order records. Even outside adviser activity, that is a practical standard for usable evidence.

Tag records for scope, retention, and export at write time#

Tag records as they are written so retrieval does not depend on later interpretation. At minimum, tag legal entity, program, rule reference, retention bucket, export destination, and control family.

Do not treat SEC Rule 17a-4 as universal. It is scoped to specified securities entities, with some categories retained for 6 years and others for 3 years, with the first 2 years easily accessible. Advisers Act Rule 204-2 is also scoped and includes 5-year retention for cited records, with the first 2 years in an appropriate adviser office.

Use tags to reflect applicability, not assumptions, such as rule_reference=17a-4, retention_bucket=6y, or rule_reference=204-2, retention_bucket=5y. Where the SEC audit-trail alternative is relevant, preserve enough version detail to recreate the original record after modification or deletion.

Reconcile finance and compliance events before launch#

Before launch, make sure finance and compliance are looking at the same underlying trail. Include Accounts Payable and payout batch events in the same catalog, even if the exports differ. Finance typically needs batch creation, approval, release, voids, reissues, and journal or cash-disbursement references. Compliance needs the linked control chain.

Run one pre-launch check: for one payout batch, one policy change, and one access change, confirm that a reviewer outside engineering can retrieve the full chain from the authoritative log and finance export without screenshots.

| Event family | Primary owner | Retention expectation | Export destination |

|---|---|---|---|

| Payment approvals | Compliance plus finance operations | Map to entity-specific record class; if Rule 17a-4 applies, use the relevant 3-year or 6-year bucket with first 2 years easily accessible | Authoritative audit log and audit packet export |

| Policy edits | Compliance owner with legal reviewer | Preserve version history; where SEC electronic recordkeeping rules apply, keep enough detail to reconstruct the original if modified or deleted | Audit log and policy archive export |

| Role and access changes | Security or admin owner with compliance review | Apply the retention class tied to the in-scope entity and keep the approval chain intact | Audit log and access administration export |

| Exception overrides and monitoring case outcomes | Risk or compliance owner | Keep according to the applicable entity rule set; preserve reviewer decision, reason code, and closure record | Case export and audit log |

| AP and payout batches | Finance owner | Internal finance schedule plus any entity-specific books-and-records duty for in-scope activities | ERP or AP export plus audit log |

If you have to be strict in only a few places, be strict on attribution, versioning, and stable linkable IDs.

Related: What Is an Audit Trail? How Payment Platforms Build Tamper-Proof Transaction Logs for Compliance.

Lock approval authority and change governance before launch#

Lock approval authority before launch so no single person can change rules, expand payout authority, grant exceptions, and hide the evidence. That is the point of segregation of duties: split administration so critical actions cannot be fully controlled, or concealed, by one actor. Where applicable, pair it with dual control procedures.

Build a decision table before anyone gets change rights#

Publish approval authority in a decision table, not in chat history or memory. For each high-impact change, name the requester, first approver, second approver where required, and escalation path.

| Change type | Minimum approval pattern | Separation rule | Escalate when |

|---|---|---|---|

| Policy changes | Operations or policy owner requests, compliance approves, second approver for material edits | Requester cannot be final approver | Version conflict, unclear rationale, or broad user impact |

| Payout limit changes | Operations requests, finance or risk reviews, second approver for threshold increases | Person changing limits cannot release payouts under the new limit alone | Increase affects many users, entity exposure, or payment velocity |

| Onboarding exceptions | Operations or risk requests, compliance approves | Exception requester cannot clear their own case | Missing case notes, missing evidence, or repeated exceptions for the same rule |

| Emergency overrides | Named emergency group member requests, separate approver authorizes, post-hoc reviewer validates | Override executor cannot be sole reviewer afterward | Override touches audit records, disables a control, or lacks attributable identity data |

Keep this table aligned with the event catalog. If the log shows action=policy_publish or action=override_granted, a reviewer should be able to confirm approved authority quickly.

Increase approval depth when risk and impact both rise#

Approval depth should increase as criticality and sensitivity rise. Low-risk operational edits should not move through the same path as changes that alter payout authority, control logic, retention behavior, or approval authority across many users or an entity.

Use one launch rule: if change risk is high and user impact is broad, require additional independent approval, not just operations.

If you operate in a broker-dealer context, apply FINRA Rule 3110 where it is in scope. Covered transactions require registered-principal review evidenced in writing. Do not extend that requirement beyond the activities it governs.

Define hard escalation triggers and log them as exceptions#

Some conditions should force escalation instead of routine queue handling. The underlying rules do not prescribe your exact trigger list, so define it in policy and record each trigger event as a control exception.

Escalate immediately when:

- approver identity is missing, shared, or not attributable to a named person or approved account identifier

- the approving event references a conflicting or unpublished policy version

- an emergency override affected a compliance audit-trail record and has not yet received post-hoc review

Where the SEC 17a-4 electronic alternative applies, evidence quality depends on complete time-stamped change history and actor identity. If identity or version lineage is broken, record quality may be degraded.

Define the emergency path and post-hoc review window in writing#

Emergency action is acceptable only if the emergency path is defined in advance. Name the emergency group ahead of time, and require post-implementation evaluation and documentation review as soon as possible after implementation.

Set a written post-hoc review window by severity and staffing. There is no universal 24-hour or 48-hour deadline for this, so use an internal standard and treat misses as exceptions.

Record the full post-hoc outcome in the audit log: emergency reason, authorizer, control bypassed or changed, start time, restoration time, reviewer conclusion, and remediation decision. If segregation of duties was not feasible during the incident, require independent review afterward.

For a step-by-step walkthrough, see How to Launch a Legal Compliance Platform for Freelancers and Handle Their Payments.

Need to turn your authority matrix into an implementable workflow? Use the Gruv docs to map policy gates, event logs, and export-ready evidence paths.

Design the log data model so evidence is retrievable under pressure#

A log model is only good enough if a reviewer can rebuild one clear story from request to payout outcome quickly. Treat linkage and preservation as evidence requirements from day one, not as reporting polish you add later.

Assign canonical trace IDs across the full payment path#

Use one canonical trace key from intake through provider action and ledger impact. Each relevant audit log record should carry consistent linkage keys, such as your internal request ID, the provider reference, and the ledger posting ID when it exists. That lets a reviewer follow the path without manual stitching.

That mirrors the retrieval principle in SEC Rule 613's CAT model, where lifecycle events are linked for timely, accurate retrieval. Keep the scope clear: Rule 613 applies to U.S. NMS securities activity, not to all platform payouts.

Verification point: sample one completed payout and one failed payout. Confirm you can traverse request creation, approval, provider submission, provider response, ledger posting, and any reversal using IDs already in the trail.

Split mutable business records from immutable evidence records#

Keep business objects editable when operational correction is needed, but preserve evidence records as append-only. Approval event, policy version reference, approver identity, timestamp, and exception decision should not be silently rewritten.

Where SEC electronic recordkeeping rules apply, immutability alone is not enough. If you use the audit-trail alternative, the system must preserve enough history to recreate the original record after modification or deletion.

Record corrections as append-only deltas, not replacements#

When a policy, approval, or escalation record needs correction, write a new event that references the original event ID. Do not replace the original record in place.

This matters most if SEC Rule 17a-4 is in scope for your entity, because that rule covers certain exchange members, brokers, and dealers. Under the audit-trail alternative, the preserved record must maintain a complete time-stamped trail of modifications and deletions. The amendments were effective January 3, 2023, with a May 3, 2023 compliance date for amendments to 17 CFR 240.17a-4.

Add export-ready fields before the first audit request arrives#

Build evidence records so audit packets can be produced without reconstruction work. Include fields like reviewer notes, exception reason codes, attachment pointers, policy version, approval chain, and export timestamp if those are part of your control process.

The SEC does not mandate those exact field names. But where its electronic recordkeeping rules apply, firms must furnish the record and audit trail, if applicable, in a reasonably usable electronic format. Use durable attachment references so the exported packet still works when it is reviewed later.

Choose immutable and editable boundaries with explicit decision rules#

Set one boundary rule and keep it simple: approvals, denials, and escalation outcomes are evidence, so they belong in an immutable audit trail with append-style change history. Allow corrections only for limited display or reference fields, and only through traceable amendments in the audit log.

This boundary is about defensibility, not developer convenience. If a field can change and you cannot prove who changed it (if applicable), when, and what changed, treat it as immutable by default.

Classify records by evidentiary value first#

Start with the records you will need to answer audit, incident, or dispute questions. Approval result, denial result, exception disposition, escalation outcome, policy version used, approver identity, and timestamp should stay on the immutable side.

Keep editable fields narrow, such as display-name corrections, internal case-title cleanup, or supplementary statements tied to personal data. In Europe, GDPR Article 16 supports rectification without undue delay, but that does not require you to overwrite approval evidence.

Set one hard default for uncertain fields#

Use a single rule in your boundary register: if you cannot produce actor identity (if applicable), action timestamp, original value, amended value, and reason for change, the field stays immutable.

For U.S. entities where SEC Rule 17a-4 applies, electronic recordkeeping must meet either WORM or the audit-trail alternative that allows recreation of the original record after modification or deletion. If you cannot reconstruct the original, your boundary is too permissive.

Document U.S. and Europe tradeoffs explicitly#

Write the tradeoff into policy: where you accept slower correction in exchange for stronger evidence, and where you allow controlled amendments to preserve personal-data accuracy.

- United States (SEC-scoped entities): Bias decision records toward immutability. Preserved records and audit trails may need to be furnished in a reasonably usable electronic format. Depending on record type, retention can be 3 years or 6 years under Rule 17a-4, with the first two years easily accessible.

- Europe (personal-data correction context): Allow traceable amendments to personal display fields or supplementary statements, but do not rewrite the underlying approval, denial, or escalation evidence.

One avoidable failure mode is storing customer-facing edits and decision evidence in the same mutable object.

Tie the boundary to incident response and legal defensibility#

This boundary has to hold during an incident, not just during a clean audit sample. Logs should help reveal compromise scope and be protected from unauthorized access or deletion. Review the boundary with compliance, legal, and security, not engineering alone.

Verification point: in staging, correct one editable field on a completed payout case and confirm the audit log captures original value, amended value, actor identity (if applicable), timestamp, and any required reason-for-change field. Then attempt to edit an approval record in place and confirm the system blocks it and writes a new event instead.

Implement logging in the real order operations happen in Gruv#

Log each payment action under one parent trace with explicit timestamps and sequence markers: request received, policy gate decision, provider response, ledger posting, webhook transitions as they arrive, then export snapshots into the audit trail. That keeps retries, async updates, and manual reviews understandable without making one action look like multiple approvals.

Record the request exactly once#

Write a request-received event before any downstream call for payouts or Virtual Accounts. Include internal request ID, actor, target account, amount, currency, destination details, and idempotency key when used.

Keep the same idempotency key on retries. Replays with the same key can return the same result, including prior 500 responses. That is what lets you prove retry versus duplicate approval attempt.

Verification point: submit the same request twice with the same key and confirm one request event plus one replay marker, not two approval candidates.

Attach the policy gate result before the provider call#

Log the policy decision between request receipt and provider submission: allowed, denied, or held, plus policy version, rule outcome, override reviewer if any, and reason code.

For KYC or AML-related holds, link the payout action to the transaction monitoring case ID when one exists. If a review escalates into suspicious-activity handling for an MSB-scoped program, keep supporting notes and attachments tied to the case record.

Verification point: place one payout on hold in staging and confirm payout ID, hold reason, policy version, and case reference are retrievable in one trace.

Separate provider acceptance from ledger posting#

Do not collapse provider acceptance and ledger posting into one event. A successful API response may mean only that the instruction was accepted while backend completion is still pending.

Log the provider response with provider reference, raw status, and receipt timestamp. Log ledger posting only when Gruv books the financial effect. Where FX is enabled, include quote ID, quoted rate, expiry window, and whether approval happened within the valid window of 5 minutes, 1 hour, or 24 hours.

Verification point: test an expired-quote path and confirm the trace shows quote expiry and no ledger posting.

Persist webhook transitions before processing#

For asynchronous flows, webhook updates are part of the evidence chain. Accept webhook delivery with 2xx, store the message, then process downstream.

Keep an immutable receipt record for each webhook event: provider event ID, provider event time if supplied, receipt time, payload hash or pointer, and internal object updated. Do not assume events arrive in business-process order; key status transitions to provider reference plus event ID so retries and replays do not look like duplicate approvals in the audit log.

Verification point: replay one webhook payload twice and confirm the second receipt is marked duplicate with no new approval or ledger event.

Snapshot an export-ready record after material state changes#

After each material milestone, create an export snapshot into the compliance audit trail: policy decision, provider acceptance, final status resolution, and manual exception closure.

Each snapshot should be investigator-ready. Include request ID, actor, approval chain, policy version, payout or Virtual Account reference, provider reference, ledger reference, webhook chain, case IDs, FX quote details where relevant, and attachment pointers. Keep records retrievable within a reasonable time period and aligned to your retention baseline.

| Step | What can fail | Evidence that proves control | Who gets paged |

|---|---|---|---|

| 1 Request | Retry creates a second logical request | Same request ID and same idempotency key mapped to one parent trace | API/on-call engineer and payments ops |

| 2 Policy gate | Hold exists but cannot be tied to case review | Policy outcome, rule code, reviewer, and case reference on the payout trace | Compliance reviewer and risk ops |

| 3 Provider and ledger | Provider success logged as final completion | Separate provider-response and ledger-posted events with distinct timestamps | Payments engineering and finance ops |

| 4 Webhook | Replay looks like a second approval | Stored webhook receipt, duplicate marker, no new approval event | Integration/on-call engineer |

| 5 Export snapshot | Records exist but cannot be retrieved quickly | Export manifest with all linked IDs and attachment pointers | Compliance operations and data owner |

Build escalation logic and exception handling that auditors can follow#

Once you can reconstruct the payment trace, the next question is when a gap becomes an exception and who owns it. In the audit trail, classify missing records, broken approval chains, and unexplained log gaps as named exception types with a severity tier, owner, and documented timing expectation.

Define severity tiers by evidence risk#

Set tiers based on how much the gap weakens auditability, not how noisy it is operationally. A delayed export is friction. A payout with no approver identity or no policy decision is a control failure. Treat the timing expectations below as internal policy choices, not regulator-mandated SLAs.

| Severity | Typical trigger | Primary owner | Example internal time expectation | Why it matters |

|---|---|---|---|---|

| Tier 1 | Single missing non-decision record, recoverable from source logs | Engineering or data owner | Same business day triage | Prevents retrieval issues from spreading |

| Tier 2 | Broken approval chain, missing reviewer identity, unresolved override, or repeated log-gap pattern | Compliance plus engineering | Immediate assignment, tracked to closure | Weakens supervisory evidence and exception reporting |

| Tier 3 | Gap that may affect regulator-facing obligations, possible books-and-records issue, or suspected unlogged approval/change | Compliance and legal, with engineering support | Escalate through incident path per policy | May require FINRA/CFTC reporting or recordkeeping analysis |

Use FINRA Rule 3120 as a control-design anchor for FINRA-supervised programs. Supervisory controls should test and verify procedures, and significant exceptions and procedure changes should be documented. Your tier definitions should already state reviewer ownership, update cadence, and required documentation in the audit log.

Verification point: stage three failures, missing webhook receipt, payout with no recorded approver, and manual override with no reason code, and confirm each maps to the expected tier and owner.

Route FINRA/CFTC-relevant findings before normal defect flow#

If your program has obligations associated with FINRA or CFTC oversight, route high-risk exceptions to compliance and legal as soon as the facts indicate reporting or recordkeeping risk. Do not wait for a full root-cause writeup before notification.

For FINRA members, covered events must be reported promptly and no later than 30 calendar days after the firm knows or should have known. For CFTC matters, timeliness and completeness affect mitigation credit in self-reporting evaluations. If a gap affects your ability to prove who approved, what changed, whether a record was corrected, or whether records remain authentic and reliable under 17 CFR 1.31, escalate first and investigate in parallel.

The practical goal is accountability without waiting so long that the record degrades or the response becomes harder to defend. A failure mode to guard against is repairing missing approval data and closing the issue as "fixed" without preserving the original gap, the correction or amendment record, and who authorized the repair.

Require a closure packet before marking resolved#

Do not mark an exception resolved in the audit log until all three are present:

- Closure notes: what failed, impact window, affected objects, and whether reporting analysis was required.

- Named remediation owner: the person accountable for the code, process, or supervisory change.

- Verification evidence: proof the fix works, such as a replay test, recovered trace, corrected linkage evidence, or export retrieval proof.

If the issue touched a FINRA-supervised process, record whether supervisory procedures were amended and whether inclusion in annual Rule 3120 reporting is needed. If it touched a CFTC-relevant books-and-records path, preserve original and corrected records plus related electronic metadata for not less than five years, where that rule applies.

Verification point: sample exceptions marked resolved in the last month and confirm an independent reviewer can understand the full timeline without asking the original engineer.

Build the audit request pack before anyone asks for it#

Once closure packets exist, package retrieval so an audit request is routine instead of a scramble. Build one evidence pack that answers the first round of questions on its own, then map only the records that actually have U.S. or Europe regulatory relevance.

Assemble a one-screen evidence pack#

Start with a compact export from the audit log that a reviewer can scan in one sitting. Keep these five sections together for the same object or time window: approval history, policy version history, exception register, access change log, and an export manifest. Treat these as internal pack components, not regulator-mandated named fields in SEC Rule 613 or MiFIR Article 26. The manifest should show what was pulled, from where, for which dates, and by whom.

| Pack section | What it should show |

|---|---|

| Approval history | approval path |

| Policy version history | which policy version applied |

| Exception register | linked exception status |

| Access change log | whether admin access changed at the same time |

| Export manifest | what was pulled, from where, for which dates, and by whom |

If a reviewer needs a second tool to confirm who approved, which policy version applied, or whether admin access changed at the same time, the pack is not ready. Use stable identifiers across all sections so the records line up without manual joins. The export manifest matters because it proves retrieval scope and timing, not just the underlying events.

Verification point: pick one payout and one policy change from a recent period and confirm an independent reviewer can reconstruct the approval path, linked exception status, and related admin changes using only this pack.

Add regulatory context only where it applies#

Do not tag every record as regulator-facing. Add a context column that states which control the record may support and under which business model.

For U.S. securities activity, SEC Rule 613 is the anchor for CAT context. It defines the data to collect and when it is reported to a central repository, including order lifecycle events such as origination, modification, cancellation, routing, and execution. Use this mapping only where your entity or affiliate is actually in scope for covered securities-order handling. If your team has no such order flow, do not imply CAT coverage just because your payment logging is strong.

A practical risk is over-tagging ordinary payout evidence with SEC or FINRA labels, which can create false urgency and confused retention assumptions.

Create a jurisdiction tab for United States and Europe differences#

For market-expansion work, add a narrow jurisdiction tab that flags where evidence handling changes.

| Jurisdiction context | Reporting or preservation point to flag | Why your pack should show it |

|---|---|---|

| United States broker-dealer records | SEC Rule 17a-4 preservation for not less than 6 years, first two years in an easily accessible place | Retrieval speed matters, not just retention |

| U.S. CAT-relevant activity | Rule 613 data and reporting timing, including next-day reporting context (by 8 a.m. Eastern Time the following trading day) | Lifecycle events must be easy to isolate |

| Europe investment services context | MiFIR Article 26 requires complete and accurate transaction details by close of the following working day | Timestamps and completeness checks matter |

| Europe personal data handling | GDPR storage limitation requires identifiable data not be kept longer than necessary | Avoid over-exporting personal data into long-lived packs |

This tab helps prevent cross-border mistakes, such as copying U.S. retention behavior into Europe without checking data minimization and access controls.

Schedule routine exports before an incident forces them#

Set monthly, quarterly, and incident-triggered exports as internal operating routines. These cadences are operating choices, not regulator-set frequencies in the sources here.

- Monthly: export a sample pack for recent approvals, policy changes, and access changes to confirm fields still populate.

- Quarterly: pull a broader pack and verify that preservation and accessibility expectations still hold for older records.

- Incident-triggered: export immediately when an exception reaches escalation, before repair work changes how records are viewed.

Check the last three exports for missing sections, date-range mismatches, or records that cannot be tied back to the original object ID. If those basics fail, the trail may still help operations, but it is not ready for scrutiny.

For the ledger side of the audit trail, see How to Build a Deterministic Ledger for a Payment Platform.

Pressure test the system with retrieval and integrity drills#

Do not assume retrieval will hold under pressure. Prove it with drills that can fail. If the audit trail shows timestamps but cannot show key context like ownership, approval path, or change reason, treat that as a control gap.

Run a mock request against two recent records#

Run a no-notice mock request for two recent records (for example, one payout and one policy change), and retrieve the evidence chain using only the designated audit sources. Measure completeness, not just speed. A reviewer should be able to follow object ID, actor, action, before-and-after state, approval path, linked exceptions, and related access changes from the same retrieval set. Then have a second person reconstruct the sequence without follow-up questions.

Test lifecycle linkage where regulatory context exists#

Where your activity is actually in scope for U.S. securities reporting, run the same drill on CAT-related references. In that context, Rule 613 focuses on linking reportable data through an order lifecycle and reporting certain data to a central repository by 8 a.m. Eastern Time the following trading day. If CAT-Order-ID, surveillance references, or internal event IDs cannot be linked reliably without extra reconciliation, record that as a weakness.

Fail hard and log remediation#

Fail the drill when key context is missing, even if timestamps exist. This aligns with integrity expectations around authenticity, reliability, and the ability to re-create records after modification or deletion. Log the drill date, sampled records, gaps, remediation owner, and re-test result in the audit log so the drill history itself demonstrates control improvement.

Avoid common build failures and recover without weakening controls#

Teams often hit the same four failure modes: noisy logs, shared admin power, silent edits, and mixed-up rule scope. The recovery path is not to log everything or expand admin access. It is to improve retrieval design, approval governance, evidence integrity, and rule mapping.

Trim logging to evidence you can retrieve and export#

Over-logging is still a control gap if reviewers cannot find the decision trail. Keep the data you actually need, and make sure it is searchable and exportable in a usable packet.

For payment operations, prioritize approvals, denials, policy edits, role and access changes, exception overrides, and linked payout events. Use one fixed export template across operations and compliance so both teams review the same fields: object ID, actor, action, timestamp, before and after state, approval chain, exception reason, and attachment pointer.

Test it by exporting one payout and one policy change, then handing the packet to someone outside the build team. If they cannot reconstruct the sequence without extra joins or screenshots, the event design still needs work.

Separate admin duties and require compensating control where needed#

Shared admin privileges quickly undermine audit credibility. Apply segregation of duties where you can, and use dual approval as a compensating control when staffing limits full separation.

Do not allow one role to grant access, change approval rules, and approve the resulting high-impact change alone. For high-impact changes where dual approval is part of your control design, record two distinct identities in the audit log, even if one approver sits outside engineering.

Validate this with a permissions test, not with policy text alone. If one admin role can change payout limits or policy settings and self-approve, treat that as an abuse path. If an emergency override occurs, log it, escalate it, and capture the post-hoc decision.

Handle corrections as append-only amendments#

Silent retroactive edits weaken defensibility. If approvals, policy versions, or escalation outcomes can be rewritten without preserving the original, the evidence chain is fragile.

For broker-dealer records, Rule 17a-4 pathways include WORM and an audit-trail alternative that supports recreating the original after modification or deletion. In practice, keep the audit trail append-only for approvals, denials, and escalation outcomes, and store corrections as amendment records linked to the original record ID with reason, actor, and timestamp.

Your pass condition is simple: a reviewer can reconstruct the original and amended states from the export alone.

Map controls to the correct entity and rule scope#

Jurisdiction confusion creates preventable control errors. Rule 17a-4 covers certain exchange members, brokers, and dealers, while Rule 204-2 covers investment advisers under the Investment Advisers Act.

That scope difference changes retention and retrieval design. Some Rule 17a-4 categories require preservation for not less than 6 years, with the first 2 easily accessible. Others require not less than 3 years, with the first 2 easily accessible. Rule 204-2 includes records kept for not less than five years, with the first 2 in an appropriate office of the adviser.

Before you standardize one export policy, annotate each control with entity, activity, rule basis, and retention expectation. Keep a control register that labels each log family as broker-dealer relevant, adviser relevant, or operational only, and route unclear mappings to legal review before implementation.

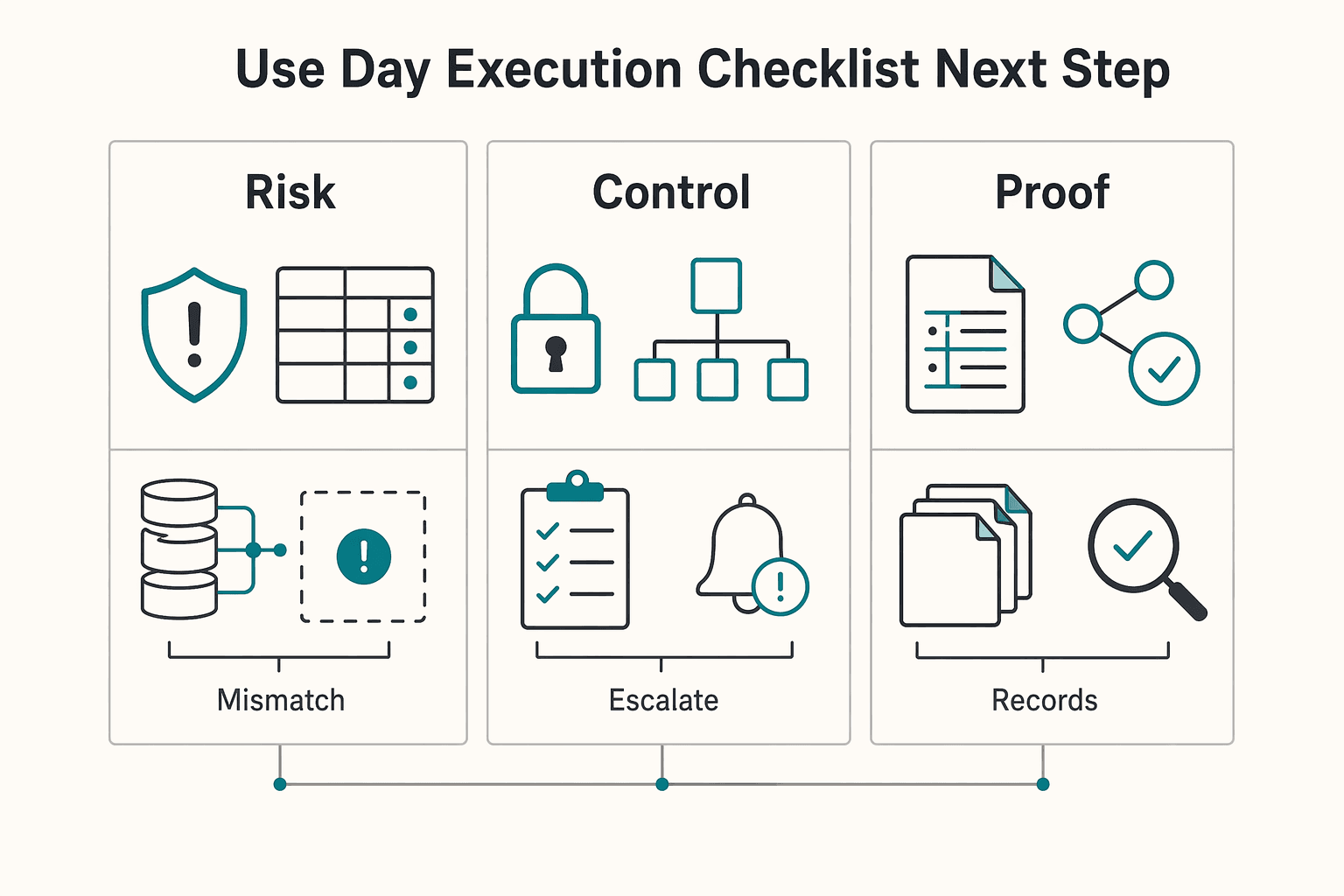

Use this 30 day execution checklist as your next step#

Use this 30-day plan to make your controls reviewable, not to claim full compliance by day 30. The target is clear authority, durable evidence, reliable retrieval, and explicit escalation that can stand up to supervisory scrutiny without making operations brittle.

| Week | Focus | Key step |

|---|---|---|

| Week 1 | Lock authority before log design | Test three high-impact actions and confirm that one person cannot complete the full chain |

| Week 2 | Publish the event catalog and data model | Export one policy edit and verify that one packet shows original state, amended state, editor, reason, and timestamp |

| Week 3 | Wire logging and test retrieval | Ask someone outside the build team to reconstruct one payout and one override from the audit log alone, including approvers and the applicable policy version |

| Week 4 | Run a drill and formalize governance | Build evidence packs for one payout and one policy change with approval history, policy version history, exception register, access-change log, export manifest, and linked payout records |

Week 1. Lock authority before log design

Week 1 is authority design: confirm scope, owners, and the authority matrix before log design. Freeze phase-one scope to high-evidentiary-risk areas such as payouts, policy changes, and access changes. Assign named owners across compliance, finance, engineering, and legal, and define who can request, review, approve, export, and escalate each action.

Lock segregation of duties and dual-control rules up front. One person should not be able to create a sensitive change, approve it, and export the evidence alone.

Checkpoint: test three high-impact actions and confirm that one person cannot complete the full chain. If one person can, fix authority design first.

Week 2. Publish the event catalog and data model

Week 2 is evidence design: publish the event catalog and data model. For each event family, define preserved fields, actor, action, timestamp, object ID, before and after state, approval chain, reason code, and attachment pointer, plus retention owner and export destination.

Set clear preservation boundaries for the audit trail at the evidence layer. Approvals, denials, escalation outcomes, and exception decisions should remain reconstructable after changes. If broker-dealer scope applies and you rely on the SEC audit-trail alternative, the system must support recreation of the original record after modification or deletion.

Checkpoint: export one policy edit and verify that one packet shows original state, amended state, editor, reason, and timestamp.

Week 3. Wire logging and test retrieval

Week 3 is end-to-end implementation: wire logging across payout, policy, and exception paths, then test retrieval under pressure. Cover the full log lifecycle, not just capture, and link events with canonical IDs so reviewers can reconstruct the chain without manual joins.

Checkpoint: ask someone outside the build team to reconstruct one payout and one override from the audit log alone, including approvers and the applicable policy version. If linkage breaks, fix identifiers and joins before expanding scope.

Week 4. Run a drill and formalize governance

Week 4 is proof and governance: run a drill, package evidence exports, close gaps, and document escalation triggers for steady-state operations. Build evidence packs for one payout and one policy change with approval history, policy version history, exception register, access-change log, export manifest, and linked payout records.

Define escalation paths explicitly to management and, as appropriate, board-level governance. Escalate gaps that affect evidentiary trust, including missing approver identity, broken approval chain, unexplained log gaps, or corrections that block reconstruction of original records.

If broker-dealer scope applies, prove that you can furnish a record and its audit trail in a reasonably usable electronic format. Also prove that you can retain records for the required category, for example, SEC Rule 17a-4 categories that require 6 years with the first 2 easily accessible, or 3 years with the first 2 easily accessible. Close the month by assigning each gap an owner, due date, and verification evidence, and keep the defect history intact.

If your team is finalizing a cross-market control design and wants to confirm program-specific coverage, contact Gruv.

Frequently Asked Questions

What is an internal payment audit trail and what fields are mandatory in every record?

An internal payment audit trail records who did what, when, and why across approvals, changes, and exceptions. There is no single mandatory field list for every platform and regulatory perimeter. A practical baseline is actor, action, timestamp, object ID, before-and-after state for changes, approval chain, exception reason, and pointers to supporting records.

Which approval and change events must be logged first if we are resource constrained?

If resources are limited, log the events that prove authority and impact first. Start with approvals and denials, policy or permission changes, exception overrides, and the related payout event. Then export one payout and one policy change to confirm someone outside the build team can reconstruct the sequence without screenshots or manual joins.

What makes an audit trail compliance ready versus just operationally useful?

A compliance-ready audit trail is not just useful for debugging. It also preserves authenticity, reliability, retention, accessibility, and retrievability for the required period. If you cannot produce a reviewable packet that shows what changed over time, it is still operational logging, not compliance-ready evidence.

Should we make everything immutable or allow some edits with controls?

Do not make every field immutable by default. Keep decision records such as approvals, denials, and escalation outcomes append-only where possible, and allow limited corrections only when the original record can still be recreated after modification or deletion. If you cannot prove the original state and correction history, treat the field as immutable.

Who should own approval controls across compliance, legal, finance, and engineering?

Use split ownership with clear accountability. Compliance defines control intent, finance validates payout evidence, engineering implements and exports records, and legal handles scope and defensibility questions. Keep segregation of duties and dual control so the same person is not preparing and deciding on the same high-impact outcome.

What should be included in an audit request evidence pack for regulators or banking partners?

Include approval history, policy version history, exception records, and linked payout records. For corrected records, include the original state, amended state, and when and how the record was modified. The pack should let a third party reconstruct the decision chain from the export alone.

When should we escalate a gap instead of fixing it quietly in normal operations?

Escalate when the gap affects evidentiary trust, not just convenience. Missing approval artifacts, unexplained log gaps, or edits that prevent recreation of the original record should go through formal governance tracking instead of a quiet fix. Record the deficiency, owner, corrective action, and verification evidence.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/0...trusted

- bsaaml.ffiec.gov/docs/manual/06_AssessingComplianceWithBSAReg...trusted

- cftc.gov/PressRoom/PressReleases/9054-25trusted

- csrc.nist.gov/pubs/sp/800/92/r1/ipdtrusted

- ecfr.gov/current/title-17/chapter-II/part-240/subpart...trusted

- ecfr.gov/current/title-17/chapter-II/part-275/section...trusted

- fdic.gov/news/financial-institution-letters/2024/upda...trusted

- federalregister.gov/documents/2022/11/03/2022-22670/electronic-r...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: