Quick Answer

Start by separating initiator, approver, releaser, and reconciler duties, then enforce those boundaries in UI and API permissions before adding more approvers. Use dual authorization for high-risk batches and AML-flagged exceptions, and verify each approval event captures actor, outcome, timestamp, reason code, provider reference, and linked ledger journals. Run a weekly SoD conflict query on payout batches and escalate confirmed breaches through compliance, legal, or risk with documented retesting.

What Auditors Need to See#

If you own payout risk, start with a short control set you can operate, verify, and defend when a payout is challenged by compliance, finance, legal, or audit. This ranked list of seven controls aims to reduce real release risk without adding approval theater. It is not a claim that seven controls are always enough.

Use a practical standard for each control. Identify the problem it prevents, the speed or staffing cost it adds, and the evidence that shows it actually ran. Controls that exist in policy but are hard to prove in operations rarely hold up in internal review.

The design follows established control expectations. FFIEC guidance on segregation of duties describes SoD as requiring more than one person for critical or sensitive tasks. FFIEC BSA/AML materials also pair dual controls with SoD to the extent possible. The same guidance expects mechanisms to escalate compliance issues to management and the board, or a committee, as appropriate. In practice, approvals, SoD, and escalation are usually stronger when designed as one control system rather than as separate topics.

The right design also varies by risk profile and market. FFIEC states BSA/AML programs should be commensurate with ML/TF and related risk. FATF similarly says implementation should be adapted to each country's legal and operational circumstances. A payout flow that is acceptable for one program, region, or payee type may need different gates elsewhere. Before you compare controls, align scope on documentation:

- Identity and entity checks are not interchangeable. KYC, entity verification, beneficial ownership, and AML checks may sit on the same payout path, but they serve different purposes. For legal-entity customers, FFIEC materials treat beneficial-owner identification and verification as a defined compliance requirement.

- Tax forms depend on payee status. Form W-9 is used to provide a correct TIN to payers required to file information returns. Form W-8BEN is used by foreign individuals to establish foreign status for U.S. withholding and reporting. If you pay independent contractors, Form 1099-NEC may be required.

- Some obligations are eligibility- or threshold-based. FEIE applies only if requirements are met. FBAR is an annual report for qualifying U.S. persons, triggered when aggregate foreign financial accounts exceed $10,000 at any time during the calendar year, due April 15 with an automatic extension to October 15.

That scope check is operational, not administrative. If your team handles domestic contractors, foreign individuals, and legal entities across multiple markets, weak intake documentation can surface later as manual overrides, rushed approvals, and audit gaps. The controls that follow focus on what to review weekly, the tradeoffs involved, and the evidence you need to show each control is operating as designed.

How to choose controls that actually reduce risk#

Choose controls by asking two questions: what risk do they prevent before funds move, and what evidence can you produce later. For cross-border payouts and payout batches, including Merchant of Record setups, prioritize enforcement, segregation of duties, and ledger-linked records before you add more approval layers.

- Enforcement strength

Prioritize controls that block risky actions before release, especially on higher-risk transfer paths. If someone can bypass a block through a manual side channel, the control is likely weak regardless of policy wording.

- Audit trail quality

Use controls that leave verifiable, transaction-linked evidence. For payout batches, you should be able to show who initiated it, who approved it, when, and which transaction or journal record it maps to. If that evidence sits in unlinked email, chat, or spreadsheets, the trail is already degrading.

- SoD coverage

Separate critical functions where possible, and require independent review where full separation is not feasible. Dual controls help, but they do not replace SoD design. If one person can initiate, approve, and reconcile, enforce role boundaries first or apply compensating controls such as dual approvals plus independent review and escalation to management.

- Ledger-journal verification

Prefer controls you can test against ledger support, not policy text alone. Approval events should map to general-ledger artifacts, including dual-signature style evidence where relevant.

This framework does not replace jurisdiction-specific legal advice. Implementation should be adapted to local legal and operational context, so treat counsel review as a separate step. If your team is small, start with system-enforced controls, a documented independent-review path, and clear escalation mechanisms before you add more manual approvers.

For a step-by-step walkthrough, see How to Build a Deterministic Ledger for a Payment Platform.

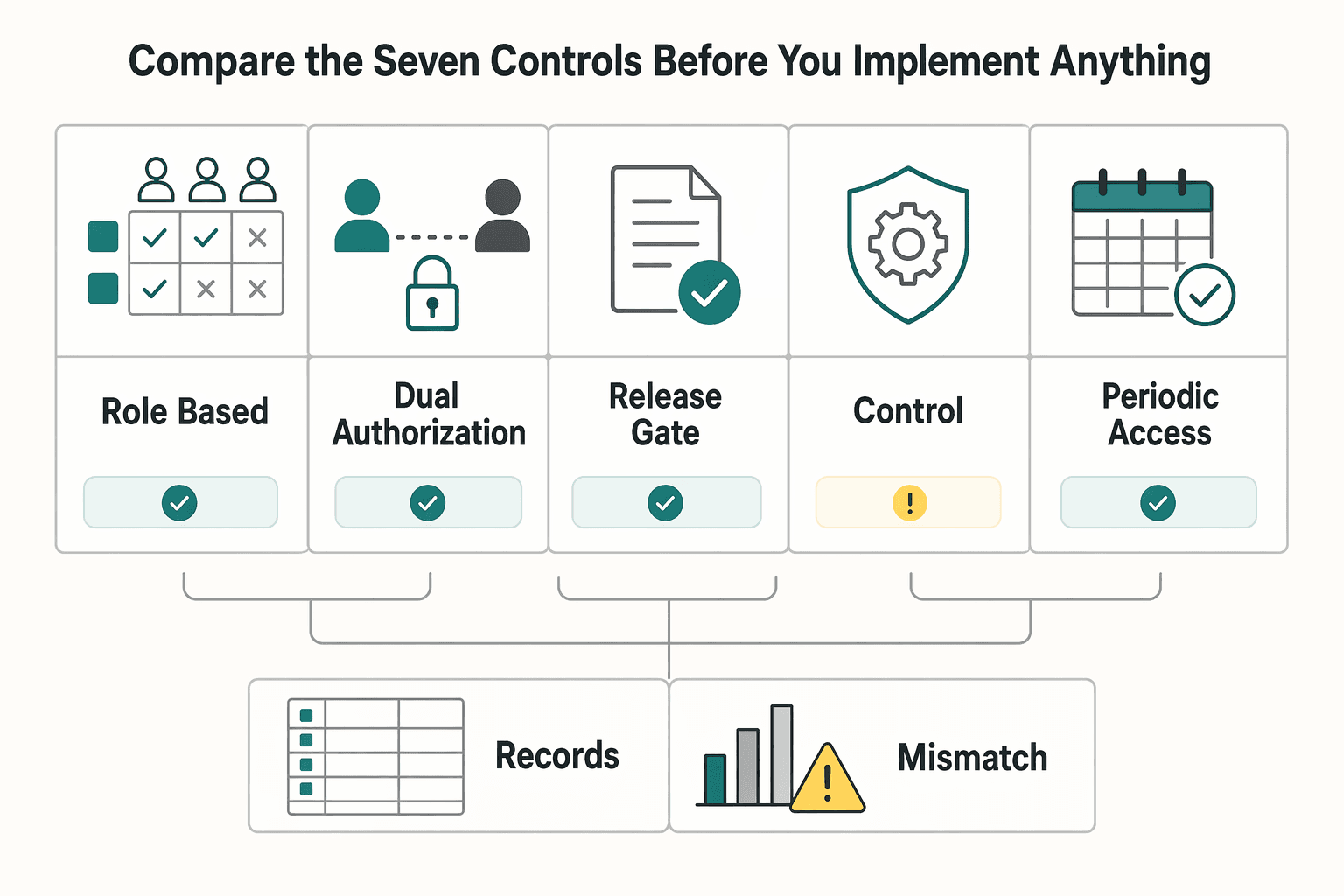

Compare the seven controls before you implement anything#

Compare all seven controls first, then implement them in dependency order so they are enforceable and your records can show they operated as designed.

| Control | Best for | Control owner | Implementation effort | Failure mode prevented | Required evidence artifact | Review cadence | Decision checkpoint |

|---|---|---|---|---|---|---|---|

| Role-based access matrix | Teams separating initiator, approver, and reconciler duties for payouts | Security or IAM with finance ops sign-off | Medium | One person can both originate and approve, or approve and reconcile | Approved role matrix, entitlement export, role change ticket, named incompatible duties | After role changes and periodic separate evaluation | Implement now |

| Dual authorization | High-risk or exception payout batches where one approver is not enough | Finance ops with compliance or risk approver | Medium | Single-user release of a sensitive payout | Approval log with two distinct user/process identifiers, timestamps, decision outcome, and payout or batch reference | Per high-risk batch, plus periodic sample review | Use only for high-risk payout batches |

| Approval thresholds | Programs where escalation should vary by policy-defined risk level or exception type | Finance policy owner | Medium | Senior review missing on higher-risk payouts, or ad hoc escalation with no rule | Threshold policy, exception register, approval outcome records, override approvals | After policy updates and periodic exception review | Phase after policy gates stabilize |

| System-enforced controls | API-first platforms that need prevention, not detective cleanup | Product or engineering with security ownership | High | Self-approval paths or manual bypass of required checks | Permission configuration record, blocked-event logs, success/fail outcomes, user/process identifiers, change ticket | Ongoing monitoring plus periodic separate evaluation | Implement now |

| Periodic access reviews | Organizations with frequent team moves or privileged-access sprawl | Security or IAM with business owner attestation | Medium | Stale access and hidden SoD conflicts stay active | Account inventory, reviewer sign-off, remediation tickets, removal confirmation | Organization-defined periodic frequency, and after org changes | Implement now |

| Compensating controls | Lean teams that cannot fully separate duties yet | Risk or compliance owner | Low to Medium | No independent check when staffing cannot support full SoD | Documented alternative control, independent review record, reconciliation evidence, follow-up ticket | Temporary use with a defined re-review date | Implement now |

| SoD violation testing | Teams that want proof controls still work in live activity | Risk, internal audit, or control testing owner | Medium | Policy says duties are separated, but activity records show conflicts | Test query or report, exceptions log, escalation record, closure evidence, retest result | Ongoing monitoring or periodic separate evaluation | Phase after policy gates stabilize |

A sensible default sequence is: role-based access matrix, system-enforced controls, periodic access reviews, then dual authorization for high-risk batches, then approval thresholds, then SoD violation testing. This aligns with the control logic reflected in GAO Principle 10, FDIC wire guidance, NIST AC-2, and NIST AU-3.

Before each rollout gate, test one recent payout batch. Confirm your platform records can show who initiated it, who approved it, and whether the action succeeded or was blocked. If that evidence is incomplete, fix access design and system enforcement before you add more approver layers.

Keep compensating controls narrow and explicit. Use them when full SoD is impractical, define the independent check, document exception handling, and set a re-review date. If compensating reviews keep surfacing the same override pattern, treat that as a design issue and move it into the next control hardening cycle.

This sequence can support a cleaner audit trail and a more defensible control story for finance, risk, and audit review.

Before you assign control owners and review cadence, map each control to how payouts, approvals, and evidence records will be implemented in your stack: Review implementation docs.

Role-based access matrix with hard SoD boundaries#

Implement this when one user can initiate, approve, and reconcile the same transaction. A hard SoD boundary means one person should not control a transaction across initiation, authorization, recording, and reconciliation.

Use a written role assignment plan and separate duties across recording, approval, custody, and reconciliation. In practice, that means defining who can do each stage and who is explicitly blocked from combining incompatible duties.

What the matrix should separate#

- Initiator: creates or submits a payout or funding request

- Approver: performs pre-approval or post-entry review, but does not submit or reconcile the same item

- Reconciler: validates outcomes against reports and transaction records, but did not post the transaction

- Custody/release role: where relevant, controls release authority and stays separate from origination and reconciliation

Why this control matters#

A clear matrix gives you defensible ownership and cleaner exception handling. It also gives auditors a direct evidence path: the approved role matrix, current entitlements, and activity records showing different people performed the separated steps.

Use a practical checkpoint before you move on. Test one recent transaction batch and one recent reconciliation cycle. Confirm the initiator, approver, and reconciler are different users, and confirm the actions are traceable in your transaction and reconciliation records.

Where teams get stuck#

The common failure point is overlap in live access, not policy wording. Teams can assign different titles while one person still has overlapping entitlements, or the reconciler may be reviewing reports they effectively created.

If full separation is not practical, document the exception and apply compensating controls with independent review rather than leaving role overlap informal.

Dual authorization and approval thresholds that match risk#

Once hard role boundaries are in place, use dual authorization where single-approver risk is unacceptable. The goal is not two approvals for everything. It is a risk-based gate for the transactions most likely to cause loss, fraud, or control failure.

NIST treats the two-person rule as dynamic separation of duty, and Nacha describes dual control as requiring more than one individual to initiate a payment. In practice, this complements your role matrix. The matrix separates standing permissions, while dual authorization adds a second authorized reviewer on specific live transactions before release.

Where this control earns its keep#

Dual authorization is often most useful for higher-risk cases, such as high-value payouts, exception-heavy payments, and AML-flagged items that need closer scrutiny. This fits a risk-based approach and guidance for higher-risk money-laundering relationships to be independently challenged and escalated to senior management or committees.

Keep the rule simple. When a payout is AML-flagged, linked to a high-risk country context, or outside policy gates, route it to a defined second approver. If those exceptions start rising, escalate the pattern to compliance review rather than piling on ad hoc overrides.

Set thresholds by risk, not by habit#

There is no universal approval amount that fits every platform or market. Approval limits are configurable, and control depth should scale to your size and operational complexity. A workable threshold model is:

| Payment tier | Approval path | When it applies |

|---|---|---|

| Standard payments | single approval only | beneficiary, corridor, amount range, and policy checks are within normal bounds |

| Elevated-risk payments | dual authorization | higher values, new beneficiaries, manual edits, failed or overridden policy gates, or AML-review flags |

| Exceptional or high-risk cases | multi-level approval or compliance escalation | risk is outside normal appetite, especially where enhanced due diligence is already required |

If you operate in a U.S. ACH context, this direction is consistent with 2026 risk-management tightening: March 20, 2026 is a major effective date, followed by broader applicability in June 2026. Phase-1 thresholds such as 6 million (2023 annual ACH origination volume) and 10 million (2023 annual ACH receipt volume) are ACH-specific. They should not be treated as global payment thresholds.

The main tradeoff to watch#

A common breakdown is poor threshold tuning or thin approver coverage, even when policy wording looks fine. Thresholds set too low create queues and bypass pressure. Thresholds set too high let risky items pass as routine.

Use a simple evidence check on a recent high-value payout, one AML-flagged payout, and one threshold exception. Confirm that different users initiated and approved, the trigger for second approval is visible, and any compliance or senior escalation is documented with the decision and timestamp. If that evidence is unclear, the control is not audit-ready.

System-enforced controls that block self-approval paths#

If you want prevention instead of cleanup, enforce separation and release gates in the product. Users should not be able to approve their own payouts or release transfers when program-required checks are still unmet. This is especially important in API-first payout flows, where weak permission design can scale quickly.

| Control | Rule | Operational check |

|---|---|---|

| Actor lockout | Make it technically impossible for the same user to initiate and approve, or prepare and release, the same payment | Records should show separation across created_by, approved_by, and released_by where policy requires it |

| State-based release gates | Keep the transfer non-releasable until the relevant gate state changes | For example, beneficiary verification, KYB review, or AML review where the program requires it |

| Permission and integration change control | Permission bundles, API scopes, and admin exceptions need formal change control | After each permission change, test at least one UI path and one API path end to end |

- Actor lockout

Make it technically impossible for the same user to initiate and approve, or prepare and release, the same payment. FFIEC's control direction supports this approach: dual controls and segregation of duties where feasible, including avoiding preparer-and-decider overlap.

Each action should tie to a unique user identity, not a shared login, and access should follow business need-to-know. Your records should show separation across created_by, approved_by, and released_by where policy requires it. If one technical identity can submit and approve through an API path, you still have a self-approval gap.

- State-based release gates

Treat holds as system rules, not reviewer discretion. For checks your program requires, for example beneficiary verification, KYB review, or AML review, keep the transfer non-releasable until the relevant gate state changes.

Scope this to obligations that actually apply to your product and market. Do not assume a universal rule that every payout must wait for every KYC, KYB, and AML check. In U.S. bank-regulated contexts, CIP requires risk-based identity-verification procedures and minimum identifying information before account opening, and beneficial-owner handling has changed in practice with reported FinCEN exceptive relief effective Feb. 13, 2026, so gate logic should match current program requirements.

- Permission and integration change control

Role and integration changes need the same control rigor as initial design. Permission bundles, API scopes, and admin exceptions need formal change control so system modifications stay aligned with the information security program.

After each permission change, test at least one UI path and one API path end to end. If one principal can edit beneficiary data, submit payout, clear hold, and approve release, your segregation boundary has collapsed. Also avoid giving approvers the ability to clear AML or KYB holds themselves; that turns extra approvals into control theater.

PCI DSS also emphasizes tracking and monitoring access activity, so your evidence should show who attempted actions, which rule allowed or denied them, and when gate states changed. That makes the control easier to defend in an internal payment audit.

Audit trail records that stand up in an internal payment audit#

A defensible payment audit trail lets a reviewer reconstruct who did what, when, from where, and with what result without guesswork. If your evidence depends on screenshots, chat messages, or memory, control operation is harder to prove during review.

1. Capture approval events, not only final status#

For each approval action, record core fields consistently: actor identity, event type, date and time, outcome, source or origination context, and the affected payment data.

For dual authorization, log each approval as a separate event. A final approved=true state alone does not show that two authorized people approved.

2. Preserve segregation-of-duties evidence in the record#

Your records should show person-level separation for critical steps, not just that multiple actions happened. Use distinct identities for roles such as created_by, approved_by, and, where applicable, released_by. When one person must perform multiple functions, record the independent review or approval as a separate event.

3. Add decision context that makes review practical#

Beyond the core audit fields, keep enough operational context for a reviewer to trace the decision and downstream impact. A practical evidence set may include actor, action, decision, timestamp, reason code, policy gate result, provider reference, and linked ledger journals. Treat these as operator-grade review fields, not a universal legal minimum.

4. Set retention and retrieval as testable controls#

Retention only helps if the records are available when you need them. Use the PCI baseline as a minimum reference point: retain audit trail history for at least one year, with at least three months immediately available for analysis. Then test retrieval regularly for both recent and older approval events.

5. Re-validate logging coverage after permission or integration changes#

After material role, API, admin-tool, or processor-integration changes, re-test logging coverage. Confirm that appropriate directories, files, security controls, and events are being monitored. Confirm both UI and API paths produce the same minimum record quality: actor, event type, timestamp, outcome, source context, and affected payment reference. Then verify that your operational context fields are present where applicable.

This reduces review friction, with the tradeoff of stricter logging and retention governance.

Periodic access reviews and fast conflict remediation#

Periodic access reviews matter most when role changes can outpace your permissions model. The objective is to find stale access, expose segregation-of-duties conflicts, and remove or reassign privileges before they become control gaps.

1. Set a defined cadence and clear trigger rules#

Use an organization-defined review cadence, with explicit ownership for each review set. For higher-risk roles, you may choose a tighter cadence, but that is an operating decision, not a universal requirement.

Do not rely on the calendar alone. Run off-cycle reviews when someone is terminated, transferred, or their need-to-know changes so stale entitlements do not remain active after personnel moves.

2. Test access against SoD control points, not titles alone#

Review entitlements against your access matrix and the control points that matter most in your workflow. SoD is meant to reduce abuse of authorized privileges and lower collusion risk, so focus on combinations that could let one person bypass dual control where dual control applies.

As a practical check, confirm that privileged users' current roles, active permissions, and recent approval activity align. If self-approval is prohibited in your matrix, the review should show that the path is not available.

3. Remediate by removing the conflict and confirming closure#

After review, the required action is to remove or reassign unnecessary privileges. If temporary elevated access is still needed, define how it is controlled and when it ends, then verify that excess access is revoked.

Avoid sign-off without cleanup. Assign remediation ownership, confirm closure, and recheck affected users in the next cycle so the same exception does not keep returning.

Compensating controls when full SoD is not feasible#

If you cannot fully separate initiator, approver, and reconciler duties yet, use compensating controls as a documented bridge when constraints are legitimate, not as proof the risk is solved. They can reduce exposure while operations continue, but they do not replace preventive segregation because many compensating checks are detective and happen after the fact.

This often comes up in lean teams, where concentrated responsibilities are structural rather than a policy failure. A practical response is to add independent review on key processes until stronger control design is feasible. If full role separation is not possible now, document the constraint, define the alternative checks, and set a trigger for moving to stronger controls.

What counts as a credible compensating control#

A credible package usually has three parts:

| Component | Review action | Focus |

|---|---|---|

| Post-payment review | Someone independent of payout initiation reviews completed payout activity after release | exceptions and unusual approval paths |

| Independent reconciliation | A separate person compares payout records, provider records, and linked ledger journals | investigates and resolves discrepancies rather than only confirming totals |

| Enhanced audit trail review | The reviewer checks audit-trail details | verify who initiated and approved actions and whether self-approval or override paths appeared in practice |

The key differentiator is review independence, even when full role separation is not possible. Dual control and segregation should be applied to the extent feasible so one person does not create, approve, and reconcile the same batch end to end.

Where teams get this wrong#

A common failure mode is treating detective review as a substitute for system-enforced preventive controls. Preventive controls should be prioritized where appropriate, and detective controls are for discovering and correcting issues after they occur. If a self-approval path is known to exist, later review should not be treated as an indefinite substitute for stronger preventive design.

Another failure mode is using compensating controls only after a miss. They are intended for legitimate, documented constraints, including legacy process limits, not retroactive coverage for past gaps.

What to document and when to escalate#

Your evidence pack should show the constraint, alternative review steps, control owner, and the records checked for each payout batch. Tie review output to the audit trail and ledger journals, and log discrepancies through closure, since reconciliation only works when discrepancies are identified, investigated, and resolved.

If reviews repeatedly surface the same override pattern, treat that as a sign that current controls may be insufficient. Strengthen role design or system-enforced preventive controls, and escalate to senior management and the relevant governance or compliance owner. Related reading: Continuous KYC Monitoring for Payment Platforms Beyond One-Time Checks.

SoD violation testing and escalation rules you can run weekly#

Run this as a weekly evidence check. If one person appears to initiate, approve, release, or reconcile the same payout batch across incompatible steps, treat it as a potential control issue until you validate it against your role matrix and approved exceptions.

A compensating-control setup stays credible when you test it regularly, route issues through established reporting lines, and document corrective action plus retesting.

- Detect the conflict in the audit trail

Use query logic to flag the same actor across incompatible actions on the same payout batch. Focus on actual behavior in logs, not just assigned permissions. Check records for actor, action, approval decision, timestamp, and reason details.

- Validate against the role-based access matrix

A log match is not automatically a breach. Compare each event to the current, date-effective role matrix and any documented exception path. Use this step to distinguish an approved design choice from an internal control deficiency in design, implementation, or operating effectiveness. Where decisions are more critical or sensitive, approval depth should be higher. If the approval path is thinner than your matrix allows, treat it as a control issue.

- Quantify impact on payout batches

After validation, scope the issue: identify affected batches, their current status, and whether the same user could both perform and conceal activity. Document enough detail for review without rework: batch IDs, impacted users, timestamps, approval path, exception rationale if any, and reconciliation status.

- Escalate, correct, and retest

Route issues through established reporting lines on a timely basis. Some issues can stay in routine remediation, but suspected fraud, potentially illegal conduct, or management-conflict cases should move beyond routine line remediation to compliance, legal, or risk ownership, and may require external reporting when obligations apply. Corrective action should be explicit, documented, and completed promptly, then followed by retesting in the next cycle. If you cannot show detection, validation, escalation, corrective action, and clean retest evidence, control health is not yet demonstrated.

Conclusion#

The durable outcome is not a thicker approval stack. It is a risk-based control design you can enforce in the platform and prove with evidence.

- Define separated roles clearly

Make it explicit who can initiate, approve, release, and reconcile payouts so one person cannot control a transaction end to end. If your access matrix allows repeated initiator-approver overlap, redesign roles instead of layering on extra reviewers.

- Apply dual authorization where risk is highest

Use two authorized approvers for actions with the highest loss or compliance exposure, and use added approval levels only where the sensitivity justifies the delay. If low-risk work is repeatedly stuck in approval queues, adjust thresholds or approver coverage before teams resort to exceptions.

- Enforce controls in the system, not only in policy

Enforce separated duties and approval rules across UI, admin, and API-connected flows where applicable. The key test is operational: prohibited actions should be denied consistently.

- Maintain an evidence-grade audit trail for transaction activity

Keep logs that show who acted, what they did, when it happened, and the outcome, with enough context to reconstruct events and support accountability. Linking audit events to payment and ledger records can improve investigations and internal audit readiness. For implementation detail, see How to Build an Internal Payment Audit Trail: Logging Approvals and Changes for Compliance.

Tailor this control set to your platform's risk profile rather than copying a generic checklist. Make escalation paths explicit so compliance issues reach management and, when appropriate, the board or a board committee.

If you want to pressure-test this control design against your markets, policy gates, and audit requirements, get a practical implementation review: Talk with Gruv.

Frequently Asked Questions

What are the minimum internal controls a payment platform should implement first?

Start with control design that separates responsibilities, dual authorization for execution, and an audit trail that captures who acted and what happened. Together, those controls reduce single-person abuse risk, add a two-person execution check, and create evidence you can test. If full segregation of duties is not yet feasible, use independent review as a compensating control.

What is the practical difference between Segregation of duties (SoD) and dual authorization?

SoD is a role-design control that separates responsibilities to reduce abuse risk without collusion. Dual authorization is a transaction-execution control that requires two authorized individuals to approve execution. Dual authorization helps, but it does not replace broader segregation of duties.

When should we use multi-level approvals instead of simple dual authorization?

Use multi-level approvals when decisions become more critical or sensitive. FFIEC guidance supports adding approval levels as criticality and sensitivity increase. Define those escalation points in policy so higher-risk items route consistently rather than ad hoc.

When are compensating controls acceptable for a small team?

Compensating controls are acceptable when full SoD is not currently practical and you require independent review of the activity. Keep that review independent and documented. Without documented independent review, the SoD gap remains unmitigated.

What must an Audit trail include to support an internal payment audit?

At minimum, records should show the identities associated with the event and the event outcome. Outcome detail should include whether actions succeeded or failed and any event-specific result needed to interpret the control evidence. If those basics are missing, internal audit support will be weak even when a control appears to have run.

How often should periodic access reviews happen, and what should trigger an emergency review?

There is no universal review cadence for all platforms; NIST leaves frequency organization-defined. In PCI-scoped environments, a commonly cited interpretation is at least once every six months for account-access review, subject to assessor or acquirer interpretation. Trigger emergency reviews when audit findings, security incidents or breaches, or legal and regulatory changes indicate your current access model may no longer be appropriate.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/0...trusted

- bsaaml.ffiec.gov/manual/AssessingComplianceWithBSARegulatoryR...trusted

- bsaefiling.fincen.gov/docs/FinCENFBARHelp.pdftrusted

- csrc.nist.gov/CSRC/media/Projects/risk-management/document...trusted

- csrc.nist.gov/pubs/sp/800/53/r5/upd1/finaltrusted

- fdic.gov/risk-management-manual-examination-policies/...trusted

- fdic.gov/resources/supervision-and-examinations/exami...trusted

- federalreserve.gov/supervisionreg/interagencyguidelines.htmtrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: