Quick Answer

Build one country launch file before first payout: payer entity, recipient type, fund flow, payout rail, and named owners. Then run two separate gates: legal status (for example PSD2 authorization path or U.S. money-transmitter analysis) and operating proof (verification logs, sanctions results, approval trail, and exportable records). Treat unresolved registration, unknown filing owner, or inability to produce evidence on demand as a hard stop. Launch only when an independent reviewer can reconstruct the decision end to end.

What to check before launch in each country#

Treat each new payout country as a go or no-go decision. It may be blocked by law, blocked by operations, or cleared only with conditions. This guide helps compliance, legal, finance, and risk teams make that call early, assign ownership, and keep an evidence trail that holds up later.

Platform payout compliance turns on actual activity and fund flow, not business labels. Licensing, registration, AML, recordkeeping, and reporting obligations follow what your entities do in practice. In the EU, PSD2 requires authorization before providing payment services. In the U.S., money-transmitter status is a facts-and-circumstances determination. Outcomes can differ based on who holds funds, who instructs payouts, and the role your entity actually performs.

Country rules change the answer#

Use a country-by-country launch checklist, not a universal template. FATF explicitly recognizes that countries implement standards within different legal and operational systems, so triggers, registrations, and reporting expectations vary across corridors. A checklist that worked in one market can fail in the next if it ignores those differences.

Lower-risk corridors still need controls, just scaled to risk. FATF frames this as a risk-based approach, and U.S. MSB AML rules similarly require review scope and frequency to be commensurate with risk. In practice, you may simplify depth in a lower-risk launch, but you still need named owners, baseline checks, and records of what was done.

What "ready to launch" should mean#

"Ready" is not just a legal memo. Your launch file should let an independent reviewer reconstruct the decision: paying entity, recipient scope, corridor, required registrations, control approvals, and escalation triggers. If someone asks later why Country A launched and Country B did not, the rationale, approvals, and evidence should sit in one place.

Recordkeeping is central to that standard. Where PSD2 applies, payment institutions must keep appropriate records for at least 5 years. In the U.S., MSBs must keep records and file reports under BSA obligations. FinCEN registration can still be required even when state-licensed.

How to use this guide#

Work through each section in payout-lifecycle order and treat each as a gate. Use this sequence:

- Scope activity before debating labels. If you cannot clearly state who holds funds and who instructs payout, stop and resolve that first.

- Separate legal prerequisites from operational prerequisites. A corridor is not launch-ready if registrations are unresolved or controls exist only in policy text without operational evidence.

- Escalate ambiguity instead of normalizing it. Open counsel issues, unknown filing ownership, or missing on-demand evidence are launch blockers, not cleanup items.

The goal is not to make every corridor look the same. It is to make each corridor understandable, owned, and defensible. That means using one decision logic for facts, one operating standard for evidence, and one clear rule for escalation when something does not line up.

By the end, your teams should be able to answer the questions that matter most. What activity is happening. Which entity is doing it. What controls must exist before money moves. What filings or registrations apply. What evidence proves those controls ran. What conditions would force you to pause or reopen the launch decision. This checklist is meant to be risk-proportionate where possible, explicit where required, and documented closely enough to withstand scrutiny.

For a broader view of cross-border payout rail tradeoffs, see Cross-Border Payments Guide for Platform Operators: Rails Costs Compliance and Speed Compared.

Define payout scope and control owners before legal analysis#

Get the operating facts fixed before you classify the activity. FATF's risk-based approach starts with identifying and understanding the risks you are exposed to, so scope the real flow first and label it second.

Create a one-page scope note for each corridor: payer entity, recipient type (contractor, seller, creator), sending and receiving countries, payout rail, settlement model, who holds funds, and who instructs payout release. Use one checkpoint before moving on: can compliance, legal, finance ops, and product all describe the same flow in plain English? If not, pause and resolve the facts.

That one-page note matters because most later decisions depend on it. If the payer entity is unclear, your registration and reporting analysis can drift. If the recipient population is undefined, your KYC and monitoring design will be vague. If no one can explain who holds funds or who can change beneficiary details, both the legal analysis and the control design will be built on assumptions. Those are the assumptions that later cause launch files to fall apart under review.

Use this minimum scope and ownership checklist before you move forward:

- Name the payer legal entity that signs, funds, and approves payouts.

- Define the recipient population and relationship purpose for KYC and risk profiling.

- Map fund flow from collection through disbursement, including provider handoffs.

- Assign control owners for AML, sanctions screening, and reporting obligations.

Ownership is a control, not admin overhead. If a U.S. entity is in covered MSB scope, 31 CFR 1022.210 requires an effective AML program commensurate with risk and a designated person for day-to-day compliance. "Our processor handles it" is not enough by itself, and contractual allocation does not remove implementation responsibility from the MSB.

Set a simple RACI so approvals, exceptions, and regulator-facing responses do not fall between teams. A practical split is this: compliance owns AML, KYC, and sanctions decisions. Legal owns legal interpretation and counsel management. Finance ops owns reconciliations, evidence, and filing inputs. Product owns feature changes that affect controls. If no one can name who owns pre-payout sanctions screening or required reporting, stop launch work until ownership is explicit.

A good scope note should also make disagreements visible early. If legal thinks the platform never receives funds, but finance ops can show a settlement model where your entity sits in the middle, resolve that before anyone debates licensing. If product says beneficiary details are locked, but operations can still edit them through an exception path, that fact belongs in the note. If the intended payout rail changes the provider handoff or the evidence source, write that down too. The point is not to draft a perfect memo on day one. It is to create one version of the facts that every team can test.

Before you move on, ask four practical questions and answer each from the scope note and systems evidence:

- Can each team describe the same funds flow without relying on labels?

- Can you point to the system or contract that supports each key fact?

- Is every launch-critical control tied to a named owner?

- If something changes, do you know who must reopen the analysis?

If the answer to any of those is no, you are not ready for legal classification yet. You are still in fact-finding. That is a better place to pause than to keep building on an incomplete picture.

With scope and owners set, test whether your controls are real enough to support a first payout.

If ACH is part of your payout design, see International ACH Transfers: Complete Guide for Platform Cross-Border Payouts.

Establish minimum viable controls before first payout#

Set four controls as launch gates before first payout. If you cannot evidence them in logs and exports before go-live, treat that as an operational stop and fix the gaps first.

1. Gate payout creation on verification, not payout failure#

Verification should happen before a recipient is enabled for payout. In U.S. banking CIP language, identifying information is obtained prior to account opening. For covered MSBs, 31 CFR 1022.210 ties AML programs to customer identification verification and recordkeeping. The practical point is timing: run identity checks before a payee can be paid, not after a failed or flagged transfer.

Use one defensibility check: can you export recipient ID, collected data, verification result, decision timestamp, and the reviewer or ruleset that approved the account? If not, the control is weak in practice. If a "pending" payee can still enter the payout queue through exceptions, the gate is cosmetic.

The standard here is not just that verification exists somewhere in the system. It is that payout creation is actually blocked until the required verification outcome exists, and that you can show that block later. A policy that says verification comes first does not help if the product allows a pending recipient to be paid anyway.

2. Screen at onboarding and again before release#

For transaction-facing payout operations, screening only at onboarding leaves a known gap before funds move. UK guidance notes that businesses involved in transactions or financial services could deal with sanctioned individuals, and the UK Sanctions List reflects changes over time. Screening at onboarding and pre-disbursement is a practical minimum, while exact cadence and scope depend on your program and jurisdiction.

Evidence quality is the key output here. Store the list source, match outcome, timestamp, and who cleared or escalated potential hits. Without that, you cannot reliably show what happened between account approval and payment release.

This is where teams often confuse control design with a working control. If screening happens, but the system cannot show which list version was used or who resolved a potential hit, your evidence will be thin when someone asks what ran before payout release. The test is not whether the vendor says screening is enabled. It is whether your own records can prove what happened for a specific payee and a specific payout.

3. Monitor behavior, not just identities#

Once payouts are live, identity and sanctions checks alone are not enough. Under 31 CFR 1020.210, bank AML programs include ongoing monitoring to identify and report suspicious transactions and, on a risk basis, maintain and update customer information. For platform payouts, that means monitoring transaction behavior against the customer risk profile you defined earlier.

Start with scenarios analysts can explain and defend, such as payout velocity jumps, unusual corridor shifts for a recipient segment, and repeated beneficiary-detail edits before release. These are practical alerts, not universally mandated scenario lists. Ensure each alert has a disposition, reason code, and closure timestamp. Alerts closed without notes weaken your audit trail.

Keep the scenarios simple enough that operators can apply them consistently. A smaller set of explainable alerts with clear closure notes is stronger than a large set that no one can defend. Monitoring should reflect the flow you scoped at the start. If the recipient population or payout rail differs by corridor, scenario design and review depth may differ too.

4. Prove your privacy handling is deliberate#

If GDPR or CCPA applies to your data set or business, privacy controls belong in payout readiness. GDPR requires data minimization and appropriate security against unauthorized or unlawful processing. CCPA requires reasonable security and limits retention to what is reasonably necessary for disclosed purposes.

Run two checks. Confirm which recipient data is necessary for KYC, sanctions screening, and monitoring, and what should not be copied into support notes. Confirm retention windows and role-based access controls align to those purposes. A common failure mode is retaining full identity documents in shared ops tools after review, which raises privacy risk without improving AML control quality.

If these controls exist only in policy text, readiness is still incomplete. The minimum credible baseline is timestamped logs, exportable results, and written control descriptions that match actual product behavior.

A useful launch test is to walk a single recipient from onboarding through first payout. Can you show the verification decision, the screening results, the approval path, the release event, and any monitoring outcome using retained records rather than screenshots stitched together later? Can you show that only the needed data was available to the people who needed it? If not, your controls may exist conceptually but not operationally.

Once that baseline exists, assess the harder question of whether the corridor is legally launchable at all.

Use a country launch decision tree for licenses and registrations#

Do not treat labels like "marketplace," "platform," or "agent" as the legal answer. Build a country-by-country yes-or-no tree from actual fund flow and control points, and treat any unresolved branch as launch-blocking until legal and compliance close it.

Start with the facts that change legal classification#

Use the same four questions for each country and payout model:

- Does your entity accept funds or other value at any point?

In U.S. rules, "money transmission services" turns on accepting currency, funds, or other value that substitutes for currency, then transmitting it to another person or location. If your model matches that pattern, licensing and registration may apply even if payouts are only one part of your business.

- Who holds funds before payout?

In the UK, the FCA explicitly points to whether your business receives customer money before passing it to a seller. A "yes" answer pushes you toward a payment-services analysis.

- Who instructs payout, and who can change beneficiary details?

Map who controls release timing and destination data in practice. Test system behavior, not just commercial positioning.

- Are you relying on an exclusion or agency theory?

The UK commercial agent exclusion may apply in some cases, but not automatically. In U.S. MSB rules, agent status is fact-and-circumstances based, so contract labels alone are not enough.

A quick quality check helps here: your funds-flow diagram, contracts, and product walk-through should support the same branch outcome. If they conflict, your classification is not ready.

The decision tree should force clarity, not create a paper trail around uncertainty. If the answer to a branch depends on assumptions about how the system "normally" works, confirm that behavior in the product. If the answer depends on a provider step, identify exactly where that provider sits in the flow and what evidence you retain about the handoff. If the answer depends on contract language, compare that language against what operations and product can actually do.

Separate legal prerequisites from operational prerequisites#

Keep legal status and operational readiness as separate gates. Both must pass before go-live.

Legal prerequisites include required authorisation or registration, or a documented conclusion that the model is outside regulated activity in that country. For PSD2-related paths, authorisation or registration sits with national competent authorities, and required documentation varies by service type.

Operational prerequisites include AML, KYC, sanctions, monitoring, recordkeeping controls, and exportable evidence. In the U.S., if you are an MSB, FinCEN registration is required even if state licensing exists, and AML program obligations still apply.

| Branch outcome | Use it when | Required action |

|---|---|---|

| Launch blocked | Legal prerequisite unresolved, required registration incomplete, or facts too ambiguous to classify | Stop launch work for that country and escalate to counsel |

| Launch with conditions | Activity is permitted only within a constrained model you can enforce | Record enforceable constraints in product and ops, then test before go-live |

| Launch allowed with enhanced monitoring | Classification is cleared but close to a regulated boundary or exclusion argument | Increase review of payout changes, exceptions, and partner dependencies after launch |

The point of separating these gates is simple. A corridor can be legally possible and still operationally unready. It can also be operationally neat and still legally blocked. Keeping those decisions separate reduces the temptation to let a strong control environment excuse an unresolved registration question, or to let a good memo excuse weak evidence.

Put a counsel checkpoint at ambiguous forks#

Bring in counsel before launch when your branch depends on an exclusion, an agent theory, or a hybrid model where product behavior and contracts are not cleanly aligned.

Your review pack should include: country, payer and payee types, entities, rail, funds flow, who holds funds, who instructs payout, sample terms, and your proposed licensing or registration conclusion. For UK and EEA paths, name the authority route explicitly (FCA in the UK; relevant national competent authority under PSD2). If you are using UK FCA decision trees, keep local thresholds local. More than €3m projected monthly average payment transactions and more than €5m average outstanding e-money apply where relevant.

Document a dated rationale, named approver, and the facts relied on in the launch file. Reopen the branch when product behavior changes.

That last point matters. A decision-tree answer is only as durable as the facts behind it. If you change the payout rail, settlement model, beneficiary edit path, or provider handoff, you may have changed the legal answer too. The clean discipline is to treat product change as a reason to reopen the affected branch, not as a reason to assume the old conclusion still fits.

A decision tree is useful only if operators can actually use it, so the next step is to turn legal conclusions into an execution tool.

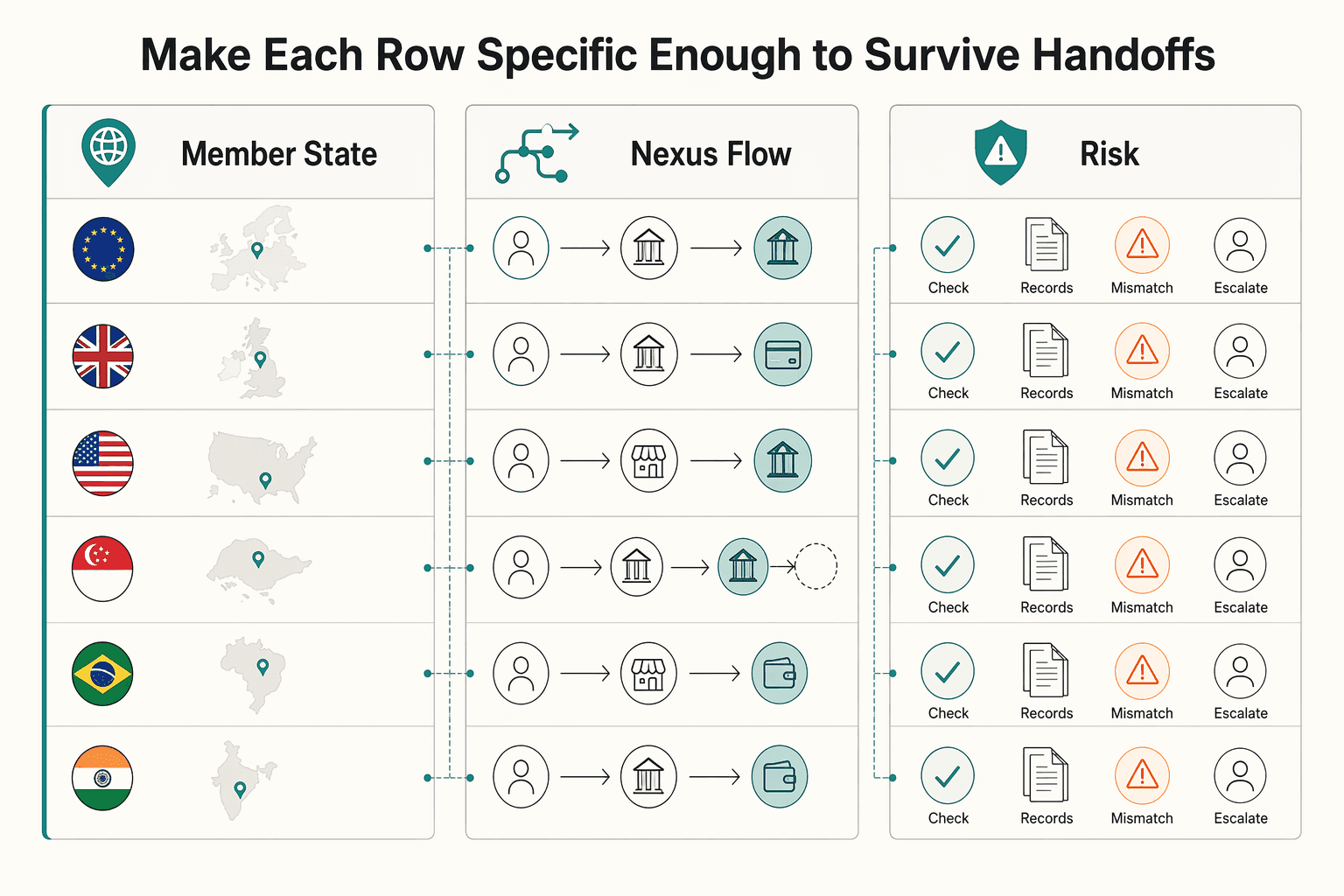

Build a jurisdiction matrix your operators can execute#

Turn each decision-tree outcome into an operator row, and treat unknown registrations or an unnamed filing owner as non-launchable until you resolve them.

A legal memo explains why launch may be allowed. The jurisdiction matrix defines what happens next, who owns it, and what evidence proves it. If those two artifacts conflict, reconcile them before launch.

Make each row specific enough to survive handoffs#

Use the real unit of risk in each row: country plus entity plus flow variant when fund flow or control points differ. A single country row can hide different compliance outcomes across payout models.

As an operating baseline, include required checks, filing owner, filing cadence, evidence source, escalation contact, implementation status, and a short applicability note.

| Matrix slice | What to capture in the row | Evidence source to name | Status use |

|---|---|---|---|

| EU Member State flow | PSD2 applicability note, provider-category mapping, home Member State competent authority, authorization or registration status | Public register check and dated launch-file record | Ready, blocked, conditional-launch |

| U.S. nexus flow | FinCEN or MSB applicability note, FinCEN Form 107 owner, initial filing deadline, renewal cadence, reporting-trigger note | Filed registration record and retained reporting records | Ready, blocked, conditional-launch |

| Country risk-control layer | Onboarding checks, pre-payout checks, transaction monitoring depth, post-payout recordkeeping owner | Exportable control logs and retained payout records | Designed, tested, live, gap open |

Put PSD2 and FinCEN in the row, not in a side document#

For EU flows, state whether PSD2 analysis applies to that entity and flow, and name the home Member State competent authority when a payment-institution authorization path is relevant. Keep authorization or registration status and the public-register check date in the same row.

For U.S.-nexus flows, avoid vague labels like "MSB maybe." If in scope, name FinCEN Form 107, the filing owner, and filing cadence. Include the initial 180-day registration window and the two-calendar-year renewal cycle.

Where applicable, include a concise SAR trigger note so compliance and operations can route cases consistently. Note the 30-calendar-day filing timeline from initial detection and the at-least-$2,000 condition.

Track control depth by country, not just legal status#

A row can be legally launchable but operationally unready. Show control depth in four stages: onboarding checks, pre-payout checks, ongoing transaction monitoring, and post-payout recordkeeping.

Calibrate depth by risk, not by one uniform template. If one corridor needs deeper controls, document that decision in the row and make sure evidence is exportable.

For each stage, name the record to retain or export, such as onboarding decision logs, screening results, monitoring case files, and payout records. If evidence cannot be produced outside a tool UI, treat that as a control gap.

This is where the matrix becomes more than a planning sheet. It becomes the operating version of the launch decision. A row that says a control exists but cannot name the record that proves it is not complete. A row that names a filing but not the owner is not complete. A row that is legally clear but shows untested monitoring is not ready.

Make status visible at a glance#

Use one status model so operators can see legal and operational readiness at a glance: ready, blocked, or conditional-launch at country level, plus designed, tested, or live for each control.

Keep the matrix strict. Unknown registrations, unknown owners, missing evidence sources, or untested monitoring should keep a row out of ready. That is what makes this a launch control rather than a planning artifact.

Once the matrix exists, you need the filing calendar and evidence pack that make those rows operational.

For a step-by-step walkthrough, see Cross-Border Freelancer Risk Mitigation Through Structure and Compliance.

Before you lock your country matrix template, map each control and evidence field to real payout statuses and exports so your operators can run it consistently: Read the docs.

Set a reporting calendar, audit evidence pack, and privacy controls#

Treat reporting as a deadline-driven control, not a side task. Once a country row is live, create a dated calendar entry with a named owner, backup owner, and trigger date. If you cannot prove when the filing clock started, that row is not launch-ready.

Keep this calendar tied directly to the jurisdiction-by-jurisdiction compliance matrix. For each entry, capture the country-row reference, filing type, triggering event, legal or internal deadline, primary owner, backup owner, and blockers, such as sanctions review completion, reconciliation, or case closure.

Build around the real filing clock#

Some obligations are recurring, but many are event-driven. Your calendar needs both fixed dates and trigger-based timers, and each timer should start from the underlying event.

| Jurisdiction or regime | Filing or notification | Filing clock to track | Owner dependency to name |

|---|---|---|---|

| U.S. | Currency transaction reporting | 15 days after the reportable transaction day | Finance ops data completeness and transaction classification |

| U.S. MSB / FinCEN | SAR | 30 calendar days after initial detection | AML case-open date, analyst disposition, filing owner |

| U.S. sanctions | OFAC initial blocking report | 10 business days from blocking date | sanctions screening hit validation and block timestamp |

| Canada / FINTRAC | Electronic Funds Transfer Report | 5 business days after initiating the transfer | payout initiation timestamp and reconciliation export |

| Canada / FINTRAC | Suspicious Transaction Report | as soon as practicable | investigator escalation and suspicion memo |

| EU / UK payments | major incident notification | without undue delay | incident severity decision and competent-authority or FCA contact owner |

Capture the trigger date from the underlying event, not from when someone starts working the case. For example, SAR timing runs from initial detection, and FINTRAC EFT timing runs from transfer initiation.

Define one evidence pack per filing type#

Do not assume every regulator wants identical artifacts, but do standardize an evidence pack per filing type so submissions are defensible and quick to assemble. For platform payouts, that typically includes KYC outcomes, sanctions screening results, the payout approval trail, and reconciliation exports.

Keep request ID and payout result or exception code in the same record path. You should be able to trace request to outcome without stitching screenshots across tools.

Use immutable timestamps as an internal control standard for regulator-facing artifacts, and preserve a clear chain from request creation to payout result. If timing or lineage can be edited after the fact, evidence quality is weak even when a filing appears on time.

Add verification checkpoints before deadlines#

Before any deadline, run at least two pre-deadline checks and record who performed them:

- Evidence completeness check

Confirm required artifacts are attached for that filing type, such as KYC decision, sanctions result, approval trail, and reconciliation export. Missing evidence should block readiness until fixed.

- Submission readiness check

Confirm filing owner, backup owner, trigger date, and retained-copy location. Keep retention rules explicit: BSA records have a five-year baseline, and OFAC blocked-property records can require availability for at least 10 years after unblocking.

Set retention schedules with both compliance and data-minimization in mind. Regulator-required records may need long retention, while duplicate working files should not be kept longer than necessary.

Tie every reporting entry back to the exact country, entity, and flow row in the matrix so reporting obligations stay auditable and operationally owned.

Classify privacy-critical data before it reaches operators#

Stop unnecessary personal data from spreading once your evidence pack is in place. For platform payouts, collect only what verification controls and payment execution require, and make everything else harder to view, harder to copy, and easier to delete on schedule.

Map fields across onboarding, review, and payout exceptions before they enter day-to-day workflows. Mark each field as required, optional, or prohibited in free text, and require a clear purpose and owner for anything collected.

Under GDPR Article 5, personal data should be limited to what is necessary, and CCPA notices must disclose both the categories collected and the purposes for collection or use. If you cannot state both for a field, remove it from the form.

Keep ops notes out of shadow-database territory. Notes should usually contain case ID, status, reason code, and a link to the source record, not copied identity documents, pasted payloads, or ad hoc screenshots.

Restrict access and copying to what the control actually needs#

Role-based access should match the purpose you already documented for KYC, sanctions screening, monitoring, and reporting. If a team only needs the case outcome, do not give that team more than the case outcome. If a reviewer needs the source document, keep the document in the source system and link to it instead of copying it into multiple tools.

This is where privacy and evidence discipline reinforce each other. The cleaner your record structure, the easier it is to produce what is required without creating duplicate stores of personal data. The more your teams rely on links, structured notes, and named evidence sources, the less likely they are to spread full identity documents into general operations tools.

Keep retention aligned to purpose, law, and the launch file#

Privacy controls do not replace recordkeeping duties, and recordkeeping duties do not justify keeping everything everywhere. Retain what law and control design require, keep retention windows explicit, and remove duplicate working files that do not improve the control.

For launch readiness, the key question is practical: can you show what was needed, where it was stored, who could access it, and how long it stays there? If the answer depends on habit rather than a documented rule, tighten it before go-live.

That same discipline should carry into sanctions and monitoring, because those controls only stay credible when they run as a repeatable operations loop.

Run sanctions, monitoring, and payout-rail choices as one operations loop#

Sanctions and monitoring are not one-time setup items. They are an operations loop that starts at onboarding, runs again before release, and continues after payout through alert review, filing decisions, and retained evidence.

The minimum pattern is already clear from the controls above: screen at onboarding, screen again before release, monitor behavior against the customer risk profile, and retain the records that show what happened. What changes by corridor is depth, ownership, and the exact evidence source. Lower-risk does not mean no loop. It means a scaled loop with named owners and auditable records.

Payout-rail choice belongs inside that loop because a rail can change the settlement model, provider handoffs, who holds funds, and where evidence lives. Those are not side details. They affect the same facts you used in the legal analysis and the same records you need for monitoring, reporting, and audit defense.

If a rail change means different beneficiary data, a different release point, or a different provider handoff, update the scope note, the decision tree, and the jurisdiction matrix. Do not treat the change as purely technical.

Use the same questions whenever a rail is selected or changed:

- Does this rail change who holds funds or who instructs payout release?

- Does it change who can edit beneficiary details?

- Does it change where sanctions and pre-payout evidence are generated?

- Does it change what reconciliation export or payout record you retain?

If the answer to any of those is yes, the corridor may need more than a product update. It may need a refreshed legal analysis, updated controls, and a revised reporting calendar entry.

This is also where partner dependence needs to stay explicit. A provider may perform a control step, but your launch file still needs to show who owns the outcome, what record proves it ran, and what happens when there is an exception. The standard remains the same: named owners, exportable evidence, and no hidden gaps between onboarding, release, and post-payout review.

Set escalation triggers before exceptions happen#

Do not wait for the first hard case to decide who must act. Define escalation triggers in advance, name the owner for each, and record where the decision and supporting evidence will live.

Some triggers are obvious launch blockers because they appear throughout this guide. Open counsel issues, unresolved registrations, unknown filing owners, and missing on-demand evidence are not cleanup items. They are reasons to stop launch work for that corridor until the issue is closed.

Other triggers appear once payouts start moving. Examples already built into the control design include potential sanctions hits, payout velocity jumps, unusual corridor shifts for a recipient segment, repeated beneficiary-detail edits before release, and monitoring alerts that require analyst review. Set the escalation path before those alerts appear, not after.

Use a simple rule. If the issue could change legal classification, stop payout expansion and reopen legal review. If the issue could affect whether a payment should be released, escalate before release. If the issue could affect a reporting clock, record the trigger date immediately and route to the filing owner and backup owner.

At minimum, define escalation for these situations before launch:

- facts in the funds-flow diagram, contracts, and product walk-through do not match

- a corridor depends on an exclusion or agency theory that is still unresolved

- a "pending" payee can still enter the payout queue

- sanctions screening produces a potential hit

- monitoring produces an alert without a clear disposition path

- required evidence cannot be exported outside a tool UI

- a product or rail change alters who holds funds, who instructs payout, or who can change beneficiary details

For each trigger, document the primary owner, backup owner, response expectation, and where the final disposition is stored. The operating standard should match the rest of the article: timestamp the trigger, record the reason, capture the decision, and retain the supporting artifacts in the same launch or case file.

The point is not to create a long exception manual. It is to eliminate ambiguity at the moments that matter most. When an exception arrives, people should already know whether to hold a payout, reopen legal analysis, start a filing clock, or block launch entirely.

Sanity checks before go-live and after first payout wave#

Before go-live, run a final pass that tests whether the launch file works as an evidence package rather than as a collection of good intentions.

Start with the simplest check: can compliance, legal, finance ops, and product still describe the same flow in plain English? If that answer has drifted since the first scope note, update the file before you launch. Then confirm the country row is actually in ready status, not conditional-launch with open gaps hiding in notes.

Next, test the controls with records, not screenshots. Pull a sample recipient and confirm you can export the verification result, screening result, decision timestamps, approval path, and payout outcome. Confirm the reporting calendar entry exists with a named owner and backup owner. Confirm the evidence pack for the relevant filing types can be assembled from retained records. Confirm role-based access and retention choices still match the data actually collected.

If the corridor is launch with conditions, test the conditions. Product and operations should be able to show that the constrained model is enforceable, not just described. If the corridor is launch allowed with enhanced monitoring, confirm who will review the added monitoring and where that review will be retained.

After the first payout wave, do not assume the live run proved everything. Use it to test whether the controls worked under production conditions:

- Did screening run at onboarding and again before release?

- Did any pending or exception path bypass the intended gate?

- Could you trace request to payout result without stitching together screenshots?

- Did monitoring alerts receive a disposition, reason code, and closure timestamp?

- Did any payout or alert expose a mismatch between product behavior and the launch file?

- Did the chosen rail create different evidence or handoff points than expected?

Review exceptions with the same seriousness as approvals. A clean first payout wave is useful only if you can explain why it was clean and produce the records that prove it. If the first live run shows that a control is weaker than expected, treat that as a reopening event for the matrix row and, where needed, the legal analysis.

The standard after go-live is the same as before go-live: facts stay aligned, owners stay named, controls stay evidenced, and changes do not get normalized without review.

Related reading: Healthcare Staffing Platform Payments Compliance for Safer Rollouts.

Conclusion#

A payout-country launch decision should be simple in structure even when the legal and operational work is not. First, fix the facts: entity, recipient scope, fund flow, payout rail, and control owners. Second, decide whether the corridor is legally launchable in that exact model. Third, prove the controls actually run with timestamped, exportable evidence. Fourth, tie reporting, privacy, sanctions, and monitoring back to named owners and a country row your operators can execute.

If you keep those steps separate and documented, you will make better go-or-no-go decisions earlier. More importantly, you will be able to explain them later. That is the real standard for payout readiness: not just that money can move, but that the corridor can stand up to review after it does.

If you are preparing a country rollout with unresolved registration or monitoring edge cases, confirm program fit and coverage assumptions before launch: Talk to Gruv.

Frequently Asked Questions

Do platform labels decide whether payout activity is regulated?

No. The article’s starting point is that compliance obligations follow actual activity and fund flow, not labels. Terms like “marketplace,” “platform,” or “agent” are not the legal answer by themselves. The decision turns on who holds funds, who instructs payout, whether your entity accepts funds or other value, and whether you are relying on an exclusion or agency theory that needs support.

Can we use one global launch template for every country?

No. You can use one operating method, but not one universal legal answer. FATF recognizes that countries implement standards within different legal and operational systems, so triggers, registrations, and reporting expectations vary by corridor. The consistent part is the discipline: scope the flow, run the legal decision tree, build the jurisdiction row, assign owners, and retain evidence.

If a corridor is lower-risk, can we skip some controls?

You can scale control depth to risk, but you should not treat lower risk as no control. FATF frames this as a risk-based approach, and the same practical rule runs through the guide: named owners, baseline checks, and records of what was done still need to exist. A lower-risk corridor may need less depth than a higher-risk one, but it still needs a defensible baseline.

Is a legal memo enough to say we are launch-ready?

No. “Ready” is not just a legal memo. The launch file should let an independent reviewer reconstruct the decision, including the payer entity, recipient scope, corridor, registrations or conclusions, control approvals, reporting ownership, and escalation triggers. A corridor is not launch-ready if legal prerequisites are unresolved or if controls exist only in policy text without operational evidence.

If our processor handles part of the flow, does that remove our compliance responsibility?

No. The article is explicit that contractual allocation does not remove implementation responsibility where your entity remains responsible for the activity. “Our processor handles it” is not enough by itself. You still need named owners, a clear understanding of what the provider does, and retained evidence showing how the control operated in practice.

When should we stop launch work and escalate?

Stop when the facts are not clear enough to classify the activity. Stop when a required registration or authorisation is unresolved, when owners are unknown, when evidence cannot be produced on demand, or when product behavior and legal assumptions do not match. Those are not items to clean up after go-live. They are launch blockers.

When should we reopen a completed country analysis?

Reopen it when product behavior changes. The article specifically calls out changes to fund flow, rail, who holds funds, who instructs payout release, and who can change beneficiary details. If those facts change, the legal answer, control design, reporting obligations, or all three may change with them.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/manual/OfficeOfForeignAssetsControl/01trusted

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/04trusted

- cppa.ca.gov/regulations/pdf/ccpa_statute.pdftrusted

- eba.europa.eu/publications-and-media/press-releases/eba-is...trusted

- eba.europa.eu/activities/single-rulebook/regulatory-activi...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fdic.gov/news/financial-institution-letters/2024/fil2...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platform Operators Choose Cross-Border Payout Rails by Corridor

The hard part is not choosing one "best" rail. It is choosing the right rail for each corridor and payout type, where cost, speed, access, and transparency pull in different directions. For any route, the practical question is simple: for this country pair, payout size, and recipient experience, which path gives you acceptable delivery, controllable cost, and audit-ready evidence?

When Platforms Should Use Wires vs Local Rails for Cross-Border Payouts

Treat rail choice as product logic, not team habit. No rail wins everywhere. SWIFT and local payment rails solve different payout risks, so your job is to route each payout by destination, currency, speed, and cost, not by whichever option sounds more global or more modern.

International ACH Transfers for Platform Operators

**International ACH can fit repeatable, non-urgent cross-border payouts when lower payout cost matters and you can still control approval, submission, recipient credit, and reconciliation.** For finance, ops, and product owners, this is less a payment-method debate than an ownership and control problem.