Quick Answer

Yes - verify vat number vies by checking the client ID on the European Commission VIES page before finalizing invoice treatment. Use the returned status as your decision trigger: valid means you can continue, while invalid means pause and correct client details first. Save the dated result immediately, since the lookup is point-in-time evidence you rely on for billing and compliance records.

Why VIES Verification is Your First Line of Defense Against Compliance Anxiety#

Run a VIES check before work starts, and make your VAT call from that result, not from assumptions. VIES is the European Commission's VAT validation web tool. It queries national VAT databases to show whether a number is recorded for cross-border EU trade. The operating rule is simple: if the result is Valid, move to the next compliance step. If it is Invalid, treat the VAT number as unconfirmed and resolve it with the client before deciding invoice treatment.

| Decision point | If you verify | If you skip |

|---|---|---|

| Payment flow | You issue the invoice with a checked VAT status, which can reduce avoidable finance-team back-and-forth on tax details. | You increase the chance of delays while tax details are clarified or corrected. |

| VAT treatment | You decide from a same-day VIES result, Valid or Invalid. If invalid, you pause and clarify before applying reverse charge. | You risk applying cross-border treatment on an unconfirmed VAT number. If that assumption is wrong, supplier-side VAT may still apply. |

| Client trust | You can show a clear compliance process and keep records to support your invoice position. | You can create avoidable friction and look less reliable on cross-border invoicing controls. |

Read Valid and Invalid narrowly, but take them seriously. VIES tells you only whether the number is recorded in the relevant national database. If you get Invalid, re-check the number with the client before assuming bad intent. Simple entry mistakes and database timing issues happen. VIES also depends on national databases, and only national tax administrations can update that data.

Your internal rule should still be firm. In cross-border cases where reverse charge is relevant, VAT ID validity affects who accounts for VAT. Commission guidance states that if the customer does not have a valid VAT number, the supplier charges VAT. Tax authority guidance also warns that wrong VAT ID assumptions can lead to additional assessment and fines, and you may still owe VAT on supplies made without charging it.

Capture proof when you run the check. VIES confirms status for the current day only and cannot confirm historical validity, so save the result immediately with the check date in the client file. Also keep the UK edge case straight. Since 01/01/2021, VIES no longer validates UK GB VAT numbers.

Once that rule is in place, the next step is operational: collect and verify the right information from each EU client during onboarding. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Protocol Step 1: Vet Every EU Client with Pre-Contract Due Diligence#

Treat VAT identity checks as a pre-contract control. Do not finalize scope, kickoff, or invoice setup until you have either a clear verification result or a documented escalation decision. Use this sequence every time:

- Collect the billing identity pack. Get the legal entity name, Member State, VAT number, and a billing contact who can correct tax details quickly.

- Run the check on an official EU page. Use a page on the

europa.eudomain, then store the check date and result in the client onboarding file. - Apply one internal handling rule. Treat missing clarity as unresolved, not "probably fine."

| Check outcome (internal handling) | Working assumption | Next action |

|---|---|---|

| Verified on an official EU page | Usable for today's onboarding decision | Proceed with signature and invoice setup; keep the dated result on file |

| Not verified yet | Not confirmed yet | Request corrected VAT details and written confirmation; re-check before proceeding |

| No result yet | No verification outcome yet | Retry later and document an escalation decision before moving forward |

Keep your judgment practical. A non-match may be administrative: a typo, an outdated detail, or a delayed update. Treat risk as higher when issues repeat, entity details conflict, or the client pushes to proceed before tax details are resolved.

If a client says they are using the cross-border SME scheme, ask for confirmation of prior notification in their Member State of establishment and whether the EX number has been granted. Use of the exemption starts from that grant date. The registration process should not take longer than 35 working days, but it can run longer when authorities need extra anti-evasion checks.

If the treatment is structurally complex, escalate instead of guessing. For complex cross-border VAT transactions, a VAT Cross Border Rulings request can be made in the participating EU country where the requester is VAT-registered. If details fail the first pass, use this short follow-up:

Hi [the client's name],

As part of onboarding, I need to confirm your billing VAT details before we finalize scope and invoice setup. The details I have are not currently verified, so please send the corrected VAT number, legal entity name, and confirmation of cross-border SME status (if applicable). Once received, I will re-check and move us forward.

For a step-by-step walkthrough, see How to Obtain a 'VAT Number' as a Freelancer in the Netherlands.

Protocol Step 2: Move from Verification to a Bulletproof Invoice#

If the client's VAT status is not documented as valid, do not send a reverse-charge invoice. Send only after you have a current verification result on file and the invoice clearly shows both VAT IDs and an explicit reverse-charge note.

Step 1. Make a send or no-send decision first#

Make the send decision as soon as you have the check result:

- Valid: move to invoice build.

- Invalid: no-send. At the time of the check, that number is not registered in the relevant national database. Ask the client to correct the details or verify with their tax office, then re-check.

Before you draft anything, confirm that the billing identity still matches what you validated, including the entity name and VAT number. Also keep the UK and NI rule straight: GB numbers are not validated in VIES, and Northern Ireland numbers use the XI prefix.

A valid result supports your process, but it does not by itself determine VAT treatment. The invoice treatment still has to match the transaction.

Step 2. Build from a fixed template#

Consistency matters more than creativity here. Use one EU B2B invoice template so the required fields stay in the same place and nothing material gets dropped under time pressure. That template should include:

| Template area | What to include | Note |

|---|---|---|

| Supplier block | Your VAT ID | Plus other supplier details required in your jurisdiction |

| Customer block | Verified customer VAT ID | Plus other customer details required in your jurisdiction |

| Tax note area | Explicit reverse-charge wording | Reverse-charge wording to add after verification |

| Tax amount lines | No VAT amount shown | Where reverse charge applies, local rules may require this |

If you build from a saved template, you are less likely to miss a VAT ID or the reverse-charge note when billing gets rushed.

| Invoice outcome | What it shows | Action |

|---|---|---|

| Compliant | Your VAT ID, customer VAT ID, explicit reverse-charge note | Ready to send |

| Missing VAT ID | One VAT ID missing or mismatched | Hold and correct before sending |

| Missing reverse-charge statement | Both VAT IDs shown, no clear reverse-charge note | Hold and revise before sending |

Step 3. Run a pre-send QA check#

The last check should compare the issued invoice against the onboarding record you relied on. This is where you catch avoidable mismatches before the client's AP team does. Before sending, confirm:

- Client VAT ID matches exactly

- Your VAT ID is visible

- Reverse-charge note is present

- No VAT amount is shown where reverse charge applies

If the issued VAT details are wrong, correct them through the proper process, including a credit note and revised invoice where required. In some jurisdictions, if VAT is shown incorrectly, you can remain liable until it is corrected. Related: The Silent Profit Killer: How to Stop Margin Erosion in Your Freelance Business.

Before you send, do one final treatment check with the VAT Reverse Charge Checker so your invoice language and VAT handling stay consistent.

Protocol Step 3: Systematize Your Protocol for Flawless Execution#

If you want fewer billing errors and fewer invoice delays, treat this as a gated process rather than a memory task. Work should move forward only when each VAT control is complete and documented.

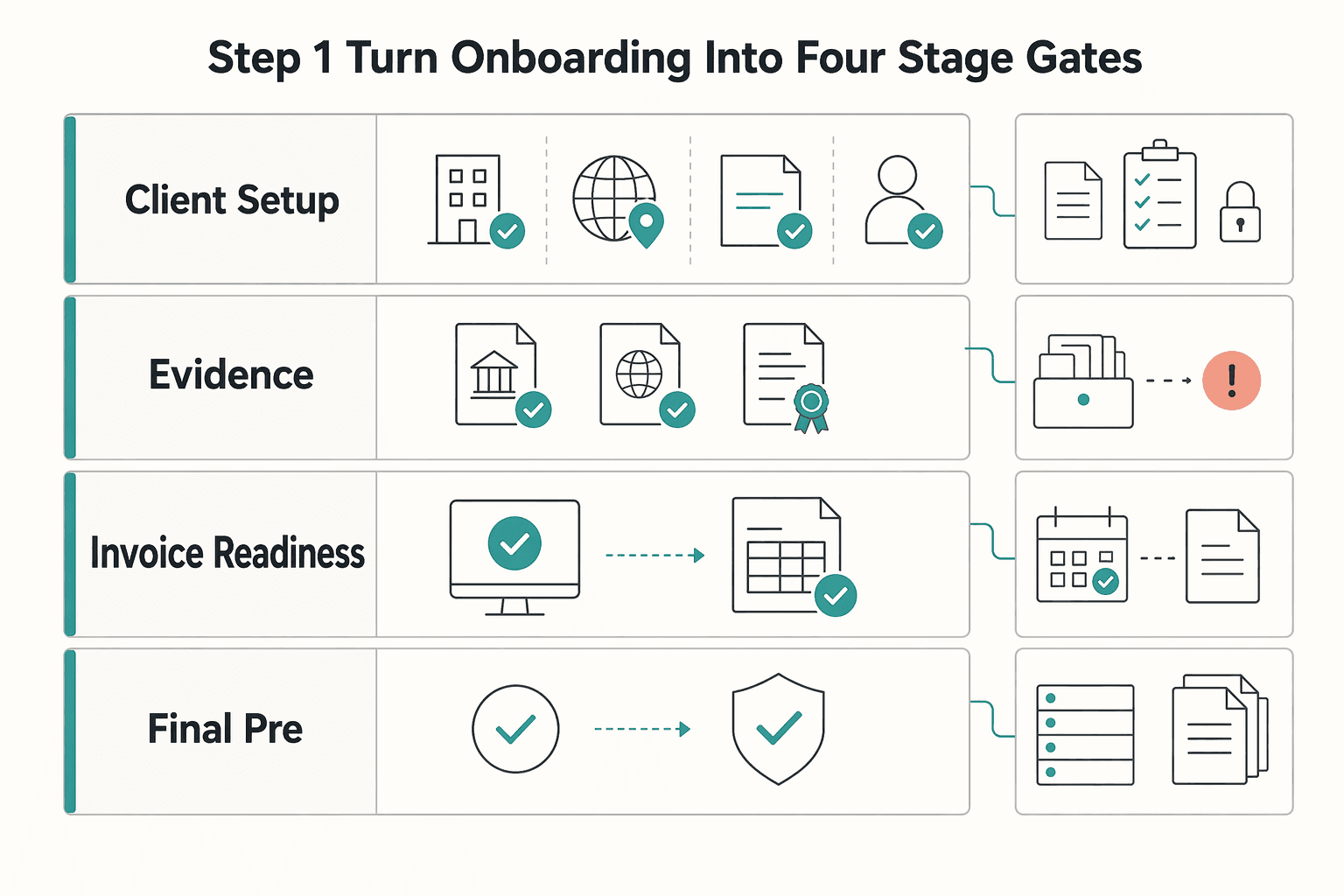

Step 1. Turn onboarding into four stage gates#

| Stage gate | Required action | Gate |

|---|---|---|

| Client setup | Capture the client legal entity, country, VAT number, and billing contact before work starts | The contract entity and the billing entity match |

| VAT verification evidence | Run the VIES check before preparing a reverse-charge invoice, and save the result | You have a dated record of the VAT number checked and the result returned |

| Invoice readiness | Build the invoice only after the verification record exists | Invoice identity matches the validated record, reverse-charge legal text is present, and tax treatment matches the verified setup |

| Final pre-send compliance check | Re-compare the contract, validation record, and final invoice right before sending | No mismatch in entity, VAT number, or invoice treatment |

- Client setup

Capture the client legal entity, country, VAT number, and billing contact before work starts so the contract entity and the billing entity do not drift apart.

- VAT verification evidence

Run the VIES check before preparing a reverse-charge invoice, and save the result so you have a dated record of the VAT number checked and the result returned.

- Invoice readiness

Build the invoice only after the verification record exists, then make sure the invoice identity matches the validated record, reverse-charge legal text is present, and tax treatment matches the verified setup.

- Final pre-send compliance check

Re-compare the contract, validation record, and final invoice right before sending. This final gate helps catch a known AP rejection trigger: invalid VAT details on the issued invoice.

Step 2. Standardize your record protocol#

Your records should allow immediate retrieval, not turn into a scavenger hunt later. For each reverse-charge client, keep one consistent evidence set. Save the VIES result output, the check date, the VAT number checked, the client legal name used for contracting, and who ran the check. If there is a mismatch or correction cycle, store that trail in the same client record.

Keep everything in one place with a fixed structure such as Contract, VAT Verification, and Invoices. Use predictable file names like ClientName_VATcheck_YYYY-MM-DD. Link the verification record directly to the signed contract and the first invoice that relied on it so you can retrieve the full trail quickly.

Step 3. Pick your control level#

The right control level depends on volume and handoffs. The goal is not sophistication for its own sake. It is reducing misses and making the evidence easy to retrieve when someone asks how the VAT decision was made.

| Control level | What it looks like | Main risk | Best use case |

|---|---|---|---|

| Manual memory | You remember checks and updates yourself | Highest miss risk and weak audit retrieval | Very low volume only |

| Checklist-driven | Required onboarding and pre-send checks block progress | Depends on consistent execution | Minimum standard for solo operators |

| Tool-assisted automation | System supports VAT validation, invoice rules, and record retention | Misconfiguration can scale mistakes; exceptions still need review | Frequent EU invoicing or shared billing work |

Checklist-driven should be your baseline. Tool-assisted controls make sense as soon as billing volume or team handoffs increase.

Step 4. Add automation for specific failure points#

Choose tools based on what they actually control, not how they are marketed. Focus on VIES-based VAT validation support, reverse-charge text handling in templates, document retention tied to client records, and a clear exception path when checks fail.

| Control | What it does | Limitation |

|---|---|---|

| Verify VAT Numbers feature | Uses VIES and updates the Intra-Community Valid status for eligible cross-border contacts | Gives a clear pass or fail checkpoint |

| VAT format check by country | Checks VAT format by country even without live VIES verification | Helps catch formatting errors but is not the same as a live validity result |

| Human exception path | Hold issuance, re-check, document the reason, and treat any manual override as an internal record | Not automatic proof of final tax treatment |

In Odoo, the Verify VAT Numbers feature uses VIES and updates the Intra-Community Valid status for eligible cross-border contacts, giving you a clear pass-or-fail checkpoint. Odoo also checks VAT format by country even without live VIES verification, which helps catch formatting errors but is not the same as a live validity result. For edge cases, including newly created companies whose VAT may not yet appear in VIES, keep a human exception path: hold issuance, re-check, document the reason, and treat any manual override as an internal record, not automatic proof of final tax treatment.

For a related US scenario, see How a US graphic designer should handle VAT when invoicing multiple EU clients.

Conclusion: Transform Anxiety into Agency#

The practical order is straightforward: Vet, Build, Systematize for every EU client engagement. That sequence gives you a repeatable path for onboarding, recordkeeping, and reverse-charge handling.

- Vet before you commit. Confirm the client's legal entity, country, and communicated VAT identification number, then check it in VIES before relying on cross-border B2B treatment.

- Build from verified details. Issue the invoice after the check is documented, and include "Reverse charge" where the customer is liable for VAT.

- Systematize the process. Make validation, record saving, and the final pre-send check part of your normal process, not something you try to remember.

For each client and invoice, keep a minimum evidence set together in one place:

- Client legal name, country, communicated VAT identification number, contract entity, VIES result, [check date], and [who ran the check]

- Saved lookup proof, such as the PDF or screenshot filename

- Final invoice PDF, [invoice number], [invoice date], and reverse-charge wording where used

- Any correction trail when VAT number, entity details, or billing details change

Keep one escalation guardrail. If VIES returns invalid, pause. If name or address association needs national confirmation, pause. If the client says they are VAT-registered but still cannot produce a valid result, pause. VIES depends on Member State databases, so failures can reflect activation issues as well as data errors. Ask the client to verify with their tax office, and for urgent matters, contact local tax administration.

On your next client cycle, run the check first, save proof immediately, and build the invoice from that verified record. Calm, repeatable execution is what reduces compliance anxiety.

We covered this in detail in How a UK LTD Should Invoice an EU Business on VAT Post-Brexit. To keep this process repeatable for every new EU client, run each VAT ID through the VAT Number Validator and archive the result with your invoice records.

Frequently Asked Questions

What are the consequences of not verifying a VAT number?

If you have not checked the VAT number in VIES, pause before treating the invoice as cross-border. You are missing a core verification point on whether the business is registered to trade cross-border within the EU. Decision: pause and verify before issuing the invoice.

Is a VIES check enough for a compliant EU invoice?

No. A valid VIES response means EU VAT information is displayed, but it is only one part of your compliance checks and does not guarantee every VAT outcome on its own. Verify first, document the result in your process, then invoice using the verified VAT number. If local wording or checks are unclear, talk to a VAT professional before you proceed.

When should you verify the client’s VAT number?

Run the check during onboarding, before you rely on cross-border treatment in your contract or invoice. VIES retrieves data from national VAT databases at query time, so the timing should match the billing decision you are making. Decision: proceed only after you have a current result for the VAT number you will invoice.

What is the difference between a local VAT number and a VIES-valid number?

A client can share a VAT number that still returns invalid in VIES. Invalid can mean the number does not exist, is not activated for intra-EU transactions, or the registration is not yet finalized. Decision: pause and verify by reconfirming the legal entity and number, then asking the client to request tax-office verification if they claim they are registered.

What should you do if the result is invalid or the VIES service is unavailable?

Treat these as different paths. For invalid, pause, re-check client legal details, and use national-level verification when you need confirmation of VAT validity or name and address association. For unavailable, treat it as no result, retry later, and do not issue the invoice on that basis yet. Decision: pause and verify in both cases, and escalate to your local tax administration or a VAT professional when the case is urgent or remains unclear.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ec.europa.eu/taxation_customs/vies/checkVatService.wsdltrusted

- ec.europa.eu/taxation_customs/viestrusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- europa.eu/youreurope/business/taxation/vat/cross-borde...trusted

- irs.gov/pub/irs-pdf/p1500.pdftrusted

- sme-vat-rules.ec.europa.eu/sme-scheme/cross-border-sme-scheme_entrusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- taxation-customs.ec.europa.eu/taxation/vat/vat-directive/persons-liable-va...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Stop Freelance Profit Margin Erosion Before It Hits Cashflow

Revenue can hold steady while the business underneath it gets weaker. What comes in matters, but what you keep after the work is delivered is the clearer signal of health.

How a US graphic designer should handle VAT when invoicing multiple EU clients

---