Quick Answer

A defensible withholding engine automates payee routing, form validation, treaty-rate gating, and payout-level evidence, not just W-8 or W-9 collection. It should separate intake from rate decisions and reporting, keep non-treaty handling active when documentation is missing or unclear, and store the exact form, validation result, rule path, applied rate, and reporting path for each payout.

What a Global Tax Withholding Engine Needs to Handle#

A defensible global tax withholding engine w-8 w-9 treaty rate automation setup lives or dies on payout-level traceability, not just form collection. Collecting Form W-9 or Form W-8BEN is only the first control. You also need to show why a specific withholding rate, including any treaty rate, was applied.

Anchor the problem in withholding-agent obligations#

Start with your role. If your platform has control, receipt, custody, disposal, or payment responsibility over income paid to a foreign person, you may be acting as a withholding agent. Those payments may be subject to chapter 3 withholding, with chapter 4 potentially applying depending on the payment facts.

The operational risk is simple. Most types of U.S.-source income received by a foreign person are subject to U.S. tax of 30% unless a different outcome is properly supported, and some reportable payments to U.S. persons can require 24% backup withholding. Your control objective is to defend each rate outcome later, payment by payment.

Use an early checkpoint: for one historical payout, can your team retrieve the submitted form, its validation result, and the rule path that produced the withholding result? If not, your core gap is evidence, not speed.

Separate form collection from treaty-rate entitlement#

Treat forms as different controls, not interchangeable inputs. Form W-9 provides a correct TIN to payers filing IRS information returns. Form W-8BEN is for individuals to establish foreign status for U.S. withholding and reporting. Form 8233 is used by nonresident alien individuals to claim exemption from withholding on compensation for personal services because of an income tax treaty.

A treaty claim is not just a reduced percentage in a rate table. The payee must notify the withholding agent of foreign status to claim treaty benefits. If valid documentation cannot be reliably associated with a payment, presumption rules determine the withholding rate. When documentation is required, you cannot apply a reduced chapter 3 rate based only on presumed status.

Design against silent drift between documentation and payment events. If your engine cannot prove which document was active when a payout was made, the reduced-rate path is weak.

Define the outcome before deeper automation#

Set the target outcome before you add more logic: fewer withholding surprises, clear escalation points, and no automation where specialist judgment is still required. This guide is limited to U.S. withholding, treaty claims, and evidence retention in cross-border payout programs, not VAT or sales-tax design.

At minimum, your team should be able to answer four questions for any payout. Which form was submitted? Was it valid when payment occurred? Why was the applied rate treaty or non-treaty? Which reporting record does the decision feed? For foreign payees, that may include Form 1042-S reporting for certain income paid to foreign addresses and retention of Form 1042 records for the applicable statute-of-limitations period.

If you cannot answer those questions now, pause broader country and rate expansion and make each withholding decision explainable under pressure first.

For a narrower treaty example, see A Deep Dive into the US-France Tax Treaty for Freelance Performers.

What a defensible withholding engine actually automates#

A defensible engine automates three separate layers: what you collect, what rate you decide, and what you report. Keeping those layers distinct makes a payout's withholding outcome easier to explain later.

Separate intake from decisioning#

Treat Form W-9, Form W-8BEN, and Form 8233 as intake records, not rate outcomes. A W-9 provides a correct TIN for information returns. A W-8BEN documents foreign status with the withholding agent or payer. Form 8233 is for nonresident alien individuals claiming exemption from withholding on personal-services compensation because of a treaty or personal exemption amount.

Use a simple checkpoint: for any payout, can you show the exact form on file and that it was the form relied on when payment was made? If not, you have collection records, not defensible withholding logic.

Store the treaty decision, not only the percentage#

A reduced withholding tax rate is a separate decision layer. IRS treaty tables are useful summaries, but they are not a complete guide, and withholding agents are directed to consult treaty text when questions come up.

That is why "15%" is not enough. For defensibility, keep the treaty inputs behind each applied rate, not only the percentage itself. If you know, or have reason to know, eligibility is not met, the payor must not apply the treaty rate.

Keep reporting outputs downstream and explicit#

Once you have the decision, route the result into reporting obligations. That can feed Form 1099 reporting and backup withholding obligations where applicable. For foreign persons, Form 1042-S may be required even when withholding is not. If Form 1042-S is required, Form 1042 is also required.

The checkpoint here is straightforward: each payout should map to one withholding outcome and one reporting path, not a year-end reconstruction.

Fence off VAT and define manual review by policy#

Treat VAT and sales-tax logic as a separate domain from the U.S. withholding path. VAT is a consumption-tax regime with a different purpose, so mixing the two can blur control boundaries.

Just as important, define manual-review routes before they are needed. Treaty ambiguity, missing eligibility facts, or Form 8233 personal-services questions should escalate to named reviewers by policy, not after a payout deadline is already in play.

If you want a deeper dive, read Withholding Tax Rate Lookup: Interactive Guide to Treaty Rates for 100+ Country Pairs.

What to prepare before you build#

Before you build, lock four prerequisites: ownership, evidence, treaty scope, and sensitive-data boundaries. Ambiguity in any of those areas can create control gaps.

Assign named owners#

As an internal control choice, assign one named owner for each approval surface: IRS document policy, payout controls, and audit response. The goal is accountability when a Form W-9 issue, treaty-eligibility question, or external inquiry shows up.

One workable split is compliance for document policy, legal for treaty-lane policy, finance ops for payout holds and releases, and engineering for implementation and change control. Keep final approval points single-owner so exceptions stay traceable.

Define the evidence pack#

Require a complete evidence pack for each payee, not just a stored form. At minimum, retain the submitted Form W-9 or Form W-8BEN, the validation outcome, any TIN Matching result used, and timestamped change history.

Each record serves a different purpose. Form W-9 provides the correct TIN for information returns. Form W-8BEN certifies foreign status for U.S. withholding and reporting and is given to the withholding agent or payer, not sent to the IRS. TIN Matching validates name and TIN combinations before information-return submission.

Limit jurisdiction scope#

Set treaty coverage before you implement rate automation. Use U.S. withholding as the base, then enable only the country lanes your policy team has explicitly approved.

Treaty outcomes can be reduced or exempt, and IRS treaty tables are not a complete substitute for treaty text. Define each supported lane with its policy basis. Germany and France are examples of lanes with IRS-hosted treaty materials, not required starting points.

Separate sensitive-data storage and access#

If you also handle foreign-asset reporting artifacts, define storage and access policy up front. Form 8938 and FBAR are separate obligations, and filing Form 8938 does not replace FBAR.

Define access rules for these artifacts under your internal policy, including where each filing record is stored and who can review it. For context, certain U.S. taxpayers may need to report on Form 8938 when specified foreign financial assets exceed $50,000 (context-specific thresholds apply), while FBAR uses a $10,000 aggregate account-value test and is due April 15 with an automatic extension to October 15.

For related evidence issues, see Permanent Home Test in a Tax Treaty: Meaning, Evidence, and Tie-Breaker Rules.

Build payee routing rules before rate automation#

Set routing before rate logic. If intake classification is wrong, every later withholding and treaty decision rests on bad facts. That is how teams end up with avoidable manual escalations and potential exposure to 30% chapter 3 or 4, or 24% backup withholding, when valid forms are missing.

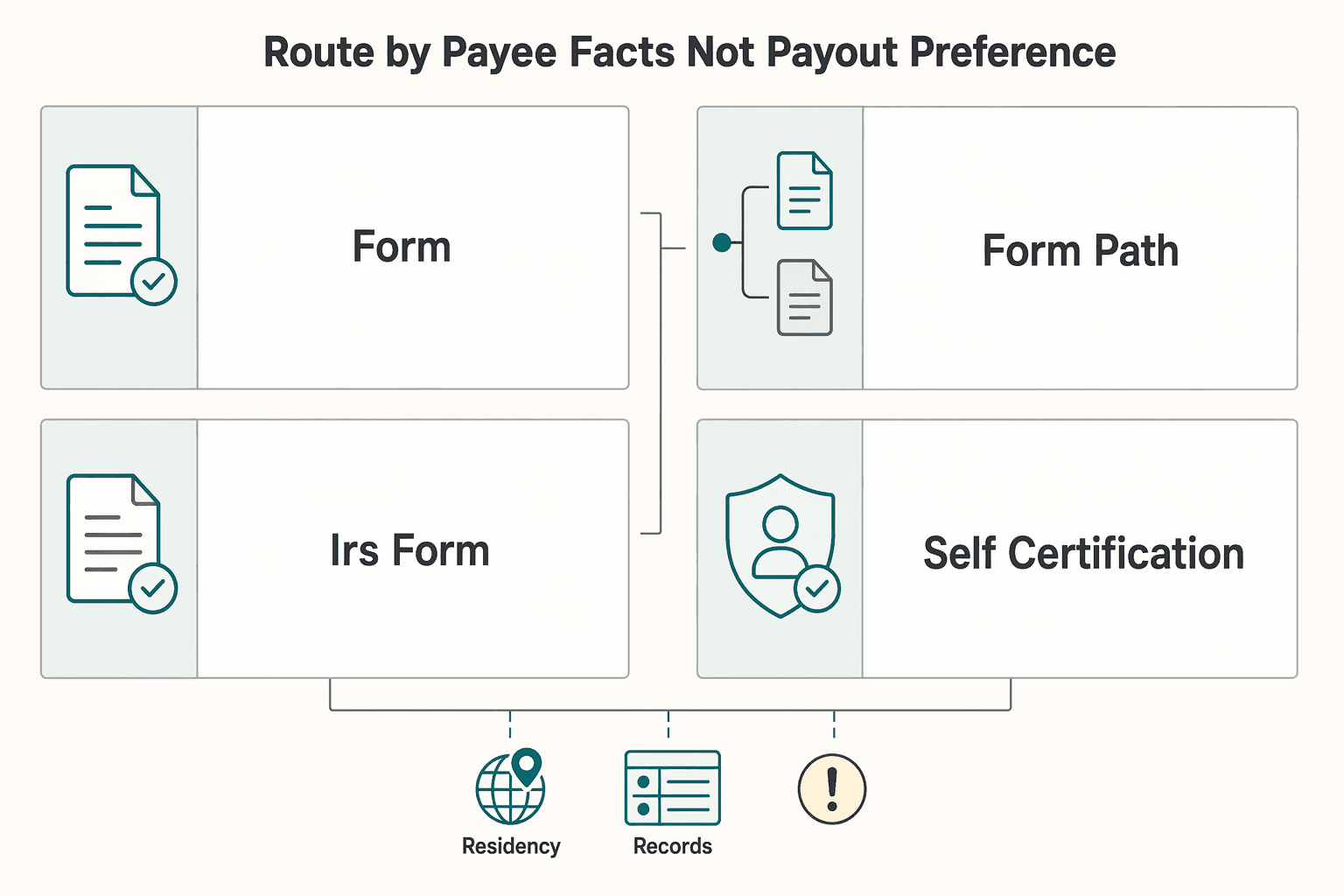

Route by payee facts, not payout preference#

Make the first decision deterministic. Assign one document lane before any rate logic runs, with one route reason and one exception owner. Use a practical starting rule set:

- Route to Form W-9 when you need a correct TIN for information returns and nothing supports a foreign-status lane.

- Route to Form W-8 when the payee is documenting foreign status for U.S. withholding. For a foreign individual, that commonly means Form W-8BEN.

- Route to IRS Form 8233 when a nonresident alien individual is claiming exemption from withholding on compensation for personal services.

- When additional self-certification is needed for facts IRS forms do not establish, such as local reporting or residency data, treat it as a separate legal artifact under applicable national law.

Before a payee becomes payout-eligible, the record should show the route code, submitted form type, and route-trigger facts.

Use this table as a policy template, not a complete IRS field or rejection list.

| Form type | Who uses it | Intake checkpoints (policy-defined) | Typical review flags | Escalation owner |

|---|---|---|---|---|

| Form W-9 | Payees in your W-9 lane where you need a correct TIN for information returns | Submitted W-9, legal name, TIN, timestamped submission and consent record | Missing TIN, name and TIN mismatch, incomplete submission, conflicting foreign-status claim elsewhere in profile | Compliance first, finance ops if a payout hold is needed |

| Form W-8 path, including Form W-8BEN for foreign individuals | Payees documenting foreign status for U.S. withholding | Submitted W-8, core identity fields, foreign-status claim, and treaty-claim fields if relied on | Missing foreign-status documentation, incomplete treaty fields, contradictions against profile or prior tax record | Compliance for document sufficiency, legal for treaty ambiguity |

| IRS Form 8233 | Nonresident alien individuals claiming exemption on compensation for personal services | Submitted 8233, identity fields, nonresident alien claim, personal-services compensation context, exemption-claim details used by policy | Used for non-service income, claimant not in the individual lane, missing exemption details, route chosen only to chase a lower rate | Legal or tax specialist, with compliance support |

| Self-certification | Payees who must provide additional residency or local reporting data outside IRS form content | Signed self-certification, residency declarations, linked payee identity, local-law basis for collection | Conflicts with W-8 or W-9 facts, unsupported residency claim, missing signature or required declarations | Legal or compliance, based on jurisdiction |

Block automated updates when validation fails#

On the W-9 lane, use TIN Matching before automated withholding updates or payout release. It is a pre-filing name and TIN validation step, and mismatches are a known trigger for later corrective handling.

Set an explicit rule. If required identity fields fail TIN Matching, do not auto-clear the profile and do not auto-update withholding treatment. Route the case to review, store the mismatch result, and let finance ops apply hold and release policy. This is a control choice, not a claim that every mismatch legally requires an immediate hold.

Store the validation record itself: submitted name, submitted TIN, outcome, timestamp, and any override. Reviewers need the full history, not just a final status.

Make treaty prerequisites visible gates#

Treaty-rate logic should be a visible gate, not an implicit code branch. The payee must notify the withholding agent of foreign status to claim treaty benefits, and if treaty eligibility is known to be unmet, the treaty rate must not be applied.

At minimum, require pass or fail checks for:

- Valid foreign-status documentation on file

- A treaty lane your policy explicitly approves

- Complete treaty-claim fields you rely on

If any check fails, keep the non-treaty path active and escalate instead of letting the engine guess a reduced rate. A stored W-8 alone is not the same thing as an approved treaty claim.

Keep self-certification separate and reconcile conflicts early#

If you collect self-certification for CRS or other local-law use, keep it separate from IRS form lanes and reconcile conflicts before changing payout eligibility. Self-certification must comply with applicable national laws, and it does not automatically answer the same withholding-document questions as W-8 or W-9.

Use a clear conflict rule: if self-certification conflicts with IRS-form residency or status facts, freeze automatic rate changes and route to compliance or legal by jurisdiction. Show both documents, the conflict flag, and current withholding treatment in the review queue.

For a related treaty-control example, see How to Make a Defensible LOB Call Under the US-Netherlands Tax Treaty.

If you are translating routing and escalation rules into production controls, map them to concrete API and webhook behaviors first: Review the implementation docs.

Design treaty rate logic that is reviewable under pressure#

Treat treaty-rate logic as a reviewed policy layer, not a hard-coded rate table. If eligibility inputs are incomplete or questionable, keep non-treaty withholding active, apply the default treatment your policy supports, and escalate rather than guessing a reduced rate.

That follows IRS standards. A withholding agent generally withholds 30 percent on amounts subject to withholding paid to a foreign person unless reliable documentation supports different treatment. The treaty rate must not be applied when ineligibility is known or suspected. The goal is a decision trail that still holds up under legal, compliance, or audit review.

Version treaty policy and keep rollback history#

Version treaty policy with named approvals and rollback history. IRS treaty tables are summaries, not full legal coverage, and IRS guidance says to consult treaty text when documentation is questionable.

For each supported lane, store:

- country pair and income category

- source treaty or protocol documents relied on

- policy version effective date

- legal or tax approvers

- rollback reference to the prior version

If you start with Germany and France, pin the exact document set in your record. The IRS Germany documents page lists core years 1989, 2006, and 2007. The IRS France page lists 1994, 2004, and 2009.

Start with narrow lane coverage and explicit eligibility gates#

Start narrow and make eligibility gates explicit. A practical first scope is US-Germany and US-France for a limited set of common income types, then expand after exception patterns stabilize.

Require the inputs your lane depends on, including foreign-status notification, treaty-country residency, beneficial-owner status, and U.S. or foreign TIN, subject to listed exceptions. Where applicable, include limitation on benefits checks. Keep form-path alignment explicit: IRS guidance points to Form W-8BEN for non-personal-service income and Form 8233 for personal services.

Use a default non-treaty rule when inputs are uncertain#

Use an explicit "if uncertain, hold default" withholding rule. Under Chapter 3 presumption rules, unreliable or contradictory documentation should not flow to a reduced treaty outcome.

When required inputs are missing, conflicting, or stale:

- Keep non-treaty withholding active, often the 30 percent Chapter 3 baseline unless another documented treatment applies.

- Route to review with missing fields, contradiction flags, and the current withholding result.

Defaulting withholding is the supported control here. Payout holds are a separate business policy decision.

Require rationale artifacts for overrides#

Require rationale artifacts for overrides. If a reviewer approves a treaty result the automated lane would reject, retain enough evidence so legal can defend the decision without reconstructing old logic.

Minimum artifact set:

- submitted form and fields relied on

- policy version used

- reviewer identity and timestamp

- short written rationale

- treaty-text reference when consulted because documentation was questionable

| Path | Speed | Risk posture | Evidence quality | Staffing impact |

|---|---|---|---|---|

| Automated path with complete eligibility inputs | Can be faster when inputs fit an approved lane | Can be lower only when documentation is reliable and gates pass | Strong if the record includes form, fields, policy version, and timestamps | Can lower work per case, with higher upfront policy setup |

| Manual review for incomplete or conflicting inputs | Can be slower per case | Often better for ambiguity because weak claims can be rejected | Strong only if reviewer notes and references are stored | Usually higher specialist time |

| Override of automated outcome | Often similar to manual for that case | Highest control need because baseline logic was bypassed | Defensible only with mandatory rationale artifacts | Can concentrate work on legal or tax approvers |

Also maintain a treaty-change watchlist outside code. Publication 901 reflects status changes, including U.S.-Hungary treaty termination effective for withholding taxes on or after January 1, 2024, and U.S.-Russia treaty suspension effective August 16, 2024.

Related: US-Germany Tax Treaty and Contractor Payments: Withholding Rates and Platform Obligations.

Add validation, renewal, and expiry controls that prevent silent failures#

Old or incorrect documentation should never keep driving withholding outcomes by default. Lifecycle controls are what stop stale records from quietly leaking into current payouts.

Use internal lifecycle states#

Use enforceable lifecycle states for Form W-8 and Form W-9, for example received, validated, pending correction, expiring soon, expired, and superseded. Treat these as internal control labels, not IRS terms.

For Form W-8BEN, calculate the standard validity end point from the signature date through the last day of the third succeeding calendar year, unless a change in circumstances makes the form incorrect earlier. Do not force one expiry rule across all W-8 records. IRS W-8 instructions also describe certain foreign-status documentation that can be indefinitely valid when the form and documentary evidence are provided within 30 days of each other.

For Form W-9, avoid unsupported "expiration date" logic. Track validation state, correction status, and whether a newer signed form supersedes the prior one.

Renew by policy, but decide by status#

Set renewal reminders by policy, but make withholding decisions depend on document status, not reminder delivery. If a W-8BEN is no longer valid, treat treaty-rate handling as unavailable and route the payee to default non-treaty handling until a new valid form is received and reviewed. IRS instructions say the beneficial owner must notify the withholding agent within 30 days of a change in circumstances and file a new Form W-8BEN or other appropriate form.

For W-9 flows, connect intake to backup-withholding controls where relevant. The backup withholding rate is 24%, and Publication 1281 says to stop backup withholding no later than 30 calendar days after receiving a signed Form W-9.

Log every validation event#

Log evidence for each validation event, not only the stored form, so decisions remain reviewable later. A practical evidence set can include:

- form version and signature date

- fields used for the decision

- calculated validity end date, when applicable

- rule tested and result

- reviewer override details and timestamp, if applicable

- TIN Matching result and check time for W-9 lanes that use it

Because TIN Matching is a pre-filing IRS service, logging the actual result and time checked is stronger than storing only a final pass or fail flag.

Handle delayed updates explicitly#

Handle delayed updates explicitly so stale records cannot leak into rate calculations. Require each calculation to read effective status as of a timestamp, not just the latest uploaded file. If a new W-8 or W-9 is pending review, restrict the prior record from new calculations. If a change-in-circumstances notice is received, remove treaty eligibility from automated processing until updated documentation is validated.

Related reading: How US Financial Consultants in Switzerland Use the Tax Treaty.

Connect onboarding decisions to payout execution and ledger evidence#

Your payout flow should use the tax status that is effective at payment time, not a stale onboarding snapshot. For each payment event, store the withholding decision used at that moment and the evidence needed to explain it later.

Bind the tax decision to the payment event#

Bind the tax decision to the payment event before funds move or income is otherwise realized. Withholding is required when payment is made, and for this purpose a payment event is not limited to cash transfer when income is realized. Tax logic cannot live only in onboarding records or settlement files.

For each payout, persist at least the payee ID, the tax form used for the decision (for example, Form W-9), decision timestamp, applied withholding result, and the supporting document record. If treaty treatment produces reduced or zero withholding for a foreign payee, retain a clear reporting indicator with that payment record. Some U.S.-source payments are still reportable on Form 1042-S even when no tax is withheld due to treaty treatment.

A useful check is one-view traceability: ledger entry, payout instruction, tax decision record, submitted form, and validation evidence.

Reuse the original outcome on retries#

Retries should reuse the original withholding outcome for the same payment event, not create a second one. The control objective: tax for one payment is withheld once, and duplicate reporting submissions are avoided.

This directly protects year-end reporting. Pub. 1220 warns against refiling the original file because duplicate reporting may result. If federal income tax was withheld, Form 1099-MISC filing is required regardless of payment amount.

Keep an end-to-end evidence chain#

Keep an end-to-end evidence chain that supports reporting and audit review. Recordkeeping must be sufficient to establish reported amounts, and exam guidance expects operating procedures for capturing and validating withholding-relevant payment and client information.

Your evidence set should connect:

- onboarding submission and stored tax documentation used for the decision

- validation outputs, including TIN Matching results where used for Form W-9 flows

- payout-time decision record and any reviewer override

- ledger posting for gross amount, tax withheld, and net paid

- downstream reporting references for Form 1042-S, Form 1042 aggregation, or Form 1099-MISC

Transaction-level Form 1042-S data should reconcile to annual Form 1042 totals due by March 15 of the following calendar year.

Recheck status before release or ledger posting#

Recheck tax status immediately before release or ledger posting so delayed updates cannot bypass controls. If status changed after payout creation, rerun the withholding decision before completion.

This does not require complex architecture. It does require one enforced final check that rereads effective status and blocks automatic completion when supporting documentation is no longer eligible.

Set exception queues and escalation triggers people can actually run#

Do not run exceptions through one generic review bucket. Split them by legal consequence, then make the payout-release decision explicit before cutoff.

Split exceptions by risk type, not by team inbox#

Use four queues: failed TIN Matching, missing treaty evidence, mismatched jurisdiction claims, and unresolved self-certification conflicts where self-certification rules apply. Keep missing TIN issues separate from incorrect name and TIN combinations so they do not share one resolution path.

| Queue | What puts a payment here | Default action | Who should clear it |

|---|---|---|---|

| Failed TIN Matching | Name and TIN fail pre-filing validation on a Form W-9 path | Block automated tax-status update and request corrected Form W-9 | Tax ops or finance ops |

| Missing treaty evidence | Form W-8 or treaty claim is missing required support, including TIN evidence where required | Do not apply treaty rate | Legal or tax owner |

| Mismatched jurisdiction claim | Country, residency, or form facts conflict enough to create reason to question the claim | Treat as unverified until new documentation is obtained | Legal or tax owner |

| Self-certification conflict | In workflows that use self-certifications, supplemental self-certification contradicts other collected data | Hold automated clearance and review reasonableness before use | Compliance owner |

Decision rule: if the issue affects whether documentation is reliable, it is not a clerical cleanup item.

Set escalation rules around payout cutoff and notice deadlines#

If an item is still unresolved before payout cutoff, hold release and notify the named legal or compliance owner. Do not let unresolved items clear by silence.

Before release, require these fields on every item: owner assigned, blocker reason selected, source documents attached, and next decision deadline. If any field is missing, keep the item blocked.

Keep a separate trigger for post-filing mismatch notices. For unresolved CP2100 or CP2100A First B-Notice cases, including cases where a signed W-9 response is not received, move to backup withholding no later than 30 business days after the notice date or receipt date, whichever is later. Where backup withholding applies, use the current 24 percent rate.

Batch mechanical fixes and require named review for treaty ambiguity#

Batch high-volume, low-judgment W-9 TIN corrections. The IRS TIN Matching tool supports interactive checks for up to 25 name and TIN combinations with immediate results and up to 999 requests per 24 hours. It also supports bulk checks for up to 100,000 combinations with results within 24 hours.

Do not batch-clear treaty ambiguity. Reduced treaty withholding depends on required documentation, including TIN evidence where required, and you cannot apply a reduced chapter 3 rate from presumed status when documentation is required. If eligibility remains unclear, require named reviewer approval or hold payout and apply the non-treaty outcome under your policy. Absent reliable documentation for different treatment, the chapter 3 baseline is 30 percent.

Escalate any item that changes form routing, treaty eligibility, or jurisdiction credibility. Batch only mechanical corrections.

Handle reporting and regulator requests without last-minute fire drills#

Your reporting handoff should preserve the same tax facts that drove each payout decision. If year-end reporting requires a manual rebuild of payee status, withholding treatment, or treaty logic, you create avoidable risk right when deadlines tighten.

Lock the year-end handoff to the original withholding decision#

Hand off a reconciled reporting file, not raw payout data. For U.S. information reporting, the package must support both IRS filing and recipient statements. For IRS filing, Form 1099-NEC is due January 31, and Form 1099-MISC is due February 28 for paper filing or March 31 for electronic filing.

Tie each reported amount to the tax classification in effect when the payment was made, not the payee's current profile. Before handoff, confirm whether the form path was W-9 or W-8, confirm any required 24% backup withholding on reportable U.S.-person payments is reflected, and confirm totals match the ledger after reversals and retries.

Where foreign-person withholding applies, keep Form 1042 aligned to payout-time withholding decisions rather than treating it as a separate cleanup cycle. Form 1042 is due March 15.

Make the IRS inquiry export complete enough to stand on its own#

If a rate is questioned, the record should be exportable without reconstruction. Include the submitted Form W-8 or W-9, form history, validation logs, decision timestamps, override approver identity, and the rationale for any treaty-reduced rate.

For chapter 3 outcomes, do not rely on treaty tables alone. They are not a complete guide, and when withholding is below 30% on Form 1042-S reporting, a chapter 3 exemption code is required. Keep the legal basis, exemption code, and supporting facts together, and retain any presumption-rule outcome when documentation was unreliable or conflicting.

Separate U.S. withholding outputs from FATCA, Form 8938, and FBAR tracking#

Keep U.S. withholding reporting separate from other disclosure regimes. Form 8938 and FBAR are separate obligations, Form 8938 does not replace FinCEN Form 114, and FBAR is filed electronically through the BSA E-Filing System rather than with the IRS. FBAR is generally due April 15, with an automatic extension to October 15.

If you track FATCA, Form 8938, or FBAR data, run that in a separate lane with separate owners, deadlines, and controls. Do not hardcode a single Form 8938 threshold. The IRS notes a general baseline above $50,000, with higher thresholds in some cases.

Run a monthly evidence-completeness review before deadlines get close#

Use a monthly review as an internal control so missing evidence is found before filing windows. This cadence is operational, not a stated IRS or FinCEN monthly mandate.

Check for missing form history, absent validation results, missing override approvals, and reduced-rate cases without treaty rationale or required exemption coding. The pass condition is simple: each reportable payee can be traced from source form to withholding result to reporting output. If not, remediate immediately or route the case back to exception handling.

For a focused royalty example, read How UK Authors Handle US-UK Tax Treaty Royalties Safely.

Common implementation mistakes and how to recover#

Many failures in global tax withholding engine W-8/W-9 treaty-rate automation come from weak evidence linkage, not missing features alone. A practical recovery step is to tighten documentation-to-decision traceability before expanding coverage.

Keep a decision record, not just a collected form#

A collected Form W-8 or Form W-9 is necessary but not sufficient for a withholding decision. Form W-9 provides a correct TIN for IRS information reporting, but you still need a payout-level record showing how documentation and validation produced the applied rate.

At minimum, keep the submitted form version, validation result, payout date, applied rate, and any override together. Test by sampling a payout and tracing form to withholding result without reconstruction. If you cannot reliably associate a payment with valid documentation, apply presumption-rule handling rather than treaty-reduction assumptions.

Publish country scope instead of implying global treaty coverage#

Treaty-rate automation is country-specific and income-specific, not global by default. A treaty with one country does not establish eligibility for another, and treaty tables describe income types that may qualify, not blanket approval.

Recover by publishing explicit supported-country and income-lane coverage, plus what stays manual or unsupported. As a control check, compare your supported list against the IRS treaty list, updated through September 26, 2025, and document gaps. If product language implies global treaty automation without lane-level coverage, narrow the claim.

Split VAT and sales tax out of withholding logic#

VAT, sales tax, and income-tax withholding are different tax domains and should not share one decision path. Mixing them can make withholding outcomes harder to validate and ownership less clear.

Recover by assigning separate owners, data fields, and approval paths for each domain. Verify that a withholding-rule change can ship without touching VAT or sales-tax logic. If it cannot, unwind the dependency first.

Default to non-treaty handling when treaty inputs are incomplete#

When treaty inputs are incomplete, unclear, or not tied to valid documentation, use the non-treaty path and escalate. For certain U.S.-source income, that usually means the 30% statutory rate unless a reduced rate or exemption applies. Documentation failures can also create 24% backup withholding exposure in some cases.

Recover by blocking automatic treaty-rate reduction when required inputs are missing, recording why the treaty lane failed, and routing to named review. Verify this with intentional incomplete-input tests and confirm the engine consistently falls back instead of silently applying a reduced rate.

For a step-by-step walkthrough, see How to Issue Compliant Tax Invoices in 50+ Countries as a Global Platform.

Conclusion#

Build the engine as a control system: automate only what you can prove, and gate what you cannot defend. If each withholding result is traceable from Form W-8BEN or Form W-9 intake through treaty decisioning to Form 1099 reporting evidence, you have an auditable control instead of a form collector. Use this closeout checklist before expanding coverage:

- Confirm routing before rate logic.

Route Form W-9 when you need a correct TIN from a U.S. person or resident alien for information returns. Route Form W-8BEN when a foreign individual is establishing foreign status and, if applicable, claiming treaty relief. Route IRS Form 8233 for nonresident alien individuals claiming exemption on personal-services compensation. If you collect self-certification for non-IRS fields or non-U.S. obligations, keep it separate from the IRS form's purpose.

- Gate payout on TIN and form-validity controls.

Use TIN Matching as a pre-filing control on the W-9 path, since it validates name and TIN combinations before information-return submission. On the W-8BEN path, track validity through the last day of the third succeeding calendar year, unless a change in circumstances makes the form information incorrect. Before release, confirm form status, validation outcome, and any expiry or correction flags.

- Version treaty logic and block weak claims.

Treaty relief is a documented eligibility decision, not a country picklist. The payee must notify the payor, as withholding agent, of foreign status to claim treaty benefits, and if you know or have reason to know a claim is wrong, you must not apply the treaty rate. Keep approval records, effective dates, and rollback history for treaty-rule changes.

- Tie reporting outputs to the source decision.

For U.S. reporting, keep each payout tied to the form path and validation result that drove withholding. Form 1099-NEC reports nonemployee compensation. Form 1099-MISC includes thresholds such as at least $10 in royalties and at least $600 for listed categories like rents, prizes and awards, and other income payments. Evidence exports should include the submitted form, validation history, payout date, applied rate, and any manual override approval.

- Define exception ownership and hold rules upfront.

Failed TIN Matching, missing treaty support, mismatched foreign-status claims, and unresolved self-certification conflicts need named owners and explicit hold and release rules. Record why each exception was cleared or denied. If the decision cannot be explained from stored evidence, the process is not audit-ready.

Before finalizing your withholding-control rollout, confirm market coverage and program-specific compliance gates for your payout lanes: Discuss your setup with Gruv.

Frequently Asked Questions

What does a global tax withholding engine automate beyond collecting Form W-8 and Form W-9?

It automates the decision and reporting layers, not just document intake. That includes validating inputs, using TIN Matching on W-9 lanes where applicable, routing treaty versus non-treaty handling, and recording the withholding result with each payout. If a payment cannot be traced to the form, validation outcome, and applied rate, the control is incomplete.

When should a payee be routed to Form W-9 instead of Form W-8 or IRS Form 8233?

Use Form W-9 when you need a correct TIN for IRS information reporting and nothing supports a foreign-status lane. Use Form W-8BEN for foreign individuals documenting foreign status for non-personal-services income, and use Form 8233 when a nonresident alien individual is claiming exemption on compensation for personal services. If the income type is unclear, route the case to review.

What controls are required before auto-applying a treaty rate?

Confirm treaty-country residence, beneficial-owner status, and valid supporting documentation for the approved lane before applying a reduced rate. Keep a decision record with the form used, validation result, income type, payout date, and applied rate. If required treaty inputs are missing, use the non-treaty path and escalate.

When should treaty-rate decisions be blocked and escalated to legal or tax specialists?

Block and escalate when you know, or have reason to know, a treaty claim is incorrect. Also escalate when country, residency, income lane, or beneficial-owner facts do not align, or when treaty effective-date changes may affect eligibility. If policy coverage and rule tables are out of sync, pause automated treaty treatment until that gap is resolved.

How should teams handle expiring forms without stopping all payouts?

Track Form W-8BEN validity through the last day of the third succeeding calendar year and prompt renewal before expiry. If a replacement is not on file, stop using the expired form for treaty treatment and route the payee to the non-treaty path where policy allows. Capture change-in-circumstances updates within 30 days.

What evidence should be stored to defend withholding decisions during an IRS review?

Store the submitted form version, validation results, change history, payout date, and applied rate. Keep TIN Matching results where used and retain any reviewer override, rationale, and timestamp. For foreign-payee reporting, tie the payment and withholding record to Form 1042-S and the Form 1042 workflow.

How do you separate withholding tax logic from VAT and sales tax obligations?

Treat withholding and VAT or sales tax as separate tax domains. Give them separate owners, data fields, decision paths, and outputs so a withholding-rule change does not require a VAT or sales-tax change. This keeps control boundaries clear and makes withholding outcomes easier to validate.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: