Quick Answer

Start with the lookup as triage, then make a controlled decision before release. Map payer jurisdiction, payee residence, income type, and entity type, verify claimant documentation, and confirm the treaty basis in your file. For U.S.-linked flows, keep Form 1040-NR Schedule OI context and residency-certification support aligned with the case record. If the evidence set is incomplete, hold the statutory rate; if treaty interpretation remains unclear, escalate to tax or legal review.

Why this guide exists for payment operators#

Use the rate lookup for triage, not as permission to apply a reduced rate. The real operating decision is whether the country-pair direction, payment type, and document trail support anything other than the domestic default. If they do not, hold at the statutory rate and escalate.

This usually matters most for cross-border payouts to contractors, sellers, and creators, where small fact changes can change treatment. Payment direction, payer jurisdiction, and the payee's claimed tax residence and entity status can affect the outcome. A generic country list is too blunt, so this guide stays focused on direction-specific country pairs and the records needed to defend each decision.

The promise of this guide#

The goal is practical: use an interactive lookup to find a candidate rate quickly, then run a short decision sequence before money moves. You are not turning each payout into a legal memo. You are separating routine cases from cases where treaty eligibility, missing documents, or conflicting facts mean you should pause.

That balance keeps queues moving without turning chart outputs into approvals. Fast screening handles volume, and a documented sequence helps prevent reduced-rate errors.

Why a chart alone is not enough#

For U.S.-linked payments, IRS materials make clear that withholding decisions involve more than a rate lookup. Publication 505 (2025) includes dedicated navigation for "Nonresident aliens." It also separately flags "Final regulations on income tax withholding," which is a cue to verify current-year changes before relying on prior assumptions.

| Source item | Stated point | Control takeaway |

|---|---|---|

| Publication 505 (2025) | Includes dedicated navigation for "Nonresident aliens" | Withholding decisions involve more than a rate lookup |

| Publication 505 (2025) | Separately flags "Final regulations on income tax withholding" | Verify current-year changes before relying on prior assumptions |

| Form 1040-NR instructions (2025) | Require completing applicable Schedule OI items and including Schedule OI with the return | Documented facts should be strong enough to hold up later |

| Form 1040-NR instructions (2025) | Note that additional schedules may be required in more complex cases, including U.S.-source income not effectively connected with a U.S. trade or business | Quick triage still needs a defensible file |

The filing path points the same way. The 2025 Form 1040-NR instructions require completing applicable Schedule OI items and including Schedule OI with the return. They also note that additional schedules may be required in more complex cases, including U.S.-source income not effectively connected with a U.S. trade or business. Even when payout-time triage is quick, the documented facts should be strong enough to hold up later.

Use a simple control test here: can another reviewer follow your decision from the payment record alone? If your reasoning depends on side messages, tribal knowledge, or unlabeled screenshots, the process is not ready for reduced-rate decisions at scale.

What this guide is trying to help you produce#

The outcome is an audit-ready operating approach, not a perfect answer to every treaty question. In practice, that means doing three things consistently:

- Screen the country pair and payment type to identify a candidate treatment.

- Decide whether the available documents and facts are strong enough to apply it.

- Record why the case was applied, held, or escalated.

One clear failure mode is document mismatch. The Form 1040-NR instructions explicitly warn not to use Schedule A (Form 1040-NR) with Forms 1040 or 1040-SR. For operators, that is not just clerical noise. It can be an early signal that the case facts or payee setup need review.

Use the lookup for speed and the document check for control. That is how you reduce surprises without overbuilding the process.

If you want a deeper dive, read US-Germany Tax Treaty and Contractor Payments: Withholding Rates and Platform Obligations.

Define the terms before you compare rates#

Before you compare rates, separate three decisions: the domestic withholding rule, any claimed reduced treatment, and who is legally responsible for withholding. If those blur together, a lookup becomes an approval.

| Term or check | What the article says | File implication |

|---|---|---|

| Domestic withholding rule | In the FIRPTA context, a foreign person's disposition of a U.S. real property interest is generally subject to 15% withholding on the total amount realized | Use as the baseline before any reduced outcome is considered |

| Amount realized | Includes cash, the fair market value of other property, and liabilities assumed | Keep the withholding base explicit in the file |

| Claimed reduced treatment | Belongs in the file as a candidate outcome, not proof of eligibility | Separate rate screening from eligibility validation |

| Withholding agent | In most FIRPTA cases, the buyer (transferee) is the withholding agent, and when a U.S. business entity disposes of a U.S. real property interest, the business entity itself is the withholding agent | Define responsibility early |

| Liability check | If the transferor is foreign and withholding is missed, the transferee may be held liable for the tax | If checks are incomplete, hold to the domestic rule and escalate |

In the FIRPTA context, the domestic rule is explicit: a foreign person's disposition of a U.S. real property interest is generally subject to 15% withholding on the total amount realized. For this purpose, the amount realized includes cash, the fair market value of other property, and liabilities assumed.

Treaty or other reduced-rate lookups belong in the file as candidate outcomes, not proof of eligibility. This section does not establish Chapter 3 or treaty-qualification mechanics. It separates rate screening from eligibility validation.

Define withholding agent early. In most FIRPTA cases, the buyer (transferee) is the withholding agent, and when a U.S. business entity disposes of a U.S. real property interest, the business entity itself is the withholding agent.

Before you treat any reduced outcome as applicable, run two checks:

- Verification check: confirm who the transferor is and whether the transferor is a foreign person.

- Liability check: if the transferor is foreign and withholding is missed, the transferee may be held liable for the tax.

If those checks are incomplete, hold to the domestic rule and escalate.

Map each payment as a direction-specific country pair#

Map each payment as one specific cross-border path before you screen any treaty rate. Do not start from a generic country list. Capture the core inputs consistently.

| Field | What to capture | Why it matters |

|---|---|---|

| Payer jurisdiction | The payer-side jurisdiction for the transaction | Withholding is applied when businesses make in-scope payments, so payer-side context anchors where withholding obligations start |

| Payee tax residence | The residence being claimed | Treaty-rate processes include residency certification checkpoints, so the claimed residence should be explicit |

| Income type | Payment character | Withholding rates vary by payment type and location, so one pair can screen differently across income streams |

| Legal entity type | Individual vs entity claimant | Set this early so your review lane and documentation checks stay consistent from triage onward |

Direction is mandatory data. "U.S. and Germany" is not one lookup until you specify who pays and who receives. The provided evidence does not establish symmetry by direction, so evaluate each direction separately and keep the income type attached to that direction-specific pair.

A good way to test your mapping is to use concrete corridors such as U.S.-Germany and U.S.-France before you scale. The point is not to predict a final rate from memory. The point is to confirm your team captures the same payer jurisdiction, payee residence, income type, and claimant type every time.

Keep the risk signal visible while mapping. OECD highlights that withholding differences across payment types and locations can affect financing decisions, and withholding can raise cross-border repatriation costs. A weak map is therefore a control failure, not just a lookup typo.

If your process includes U.S. residency certification evidence, flag that early as part of the pair record. IRS operations include Form 8802, Form 8802 payment validation, and payment-confirmation research in the USRC database. Unresolved residence support should keep treaty relief provisional until the record is complete.

Compare lookup sources by what decision they can support#

For U.S.-linked withholding, match the source to the decision stage: quick screens for triage, IRS materials for operating support, and treaty text when you need legal confirmation.

| Source | Decision it can support | Confidence label | Practical limit |

|---|---|---|---|

| IRS IRM: United States Certification for Reduced Tax Rates in Tax Treaty Countries (including Form 8802 and processing-time steps) | Building a defensible operating process with roles, checkpoints, and timing | Operational support | Not a shortcut to treaty-article interpretation |

| IRS nonresident guidance + Publication 519 (2025) | Rule checks and exception awareness in U.S. nonresident treatment | Operational support | General rules can have treaty exceptions (for example, India Article 21) |

| Publication 4152 (Rev. 9-2025) | Escalation and risk signals, including unique treaty provisions and failure-to-file consequences | Operational support | Flags risk, does not replace article-level treaty reading |

| PwC WHT Quick Charts / WWTS and Deloitte DITS Treaty Rates | Preliminary corridor screening before IRS/treaty confirmation | Quick screen | Treat outputs as provisional pending verification |

| Treaty text sources | Final confirmation when eligibility, scope, or unique provisions drive the outcome | Legal confirmation required | Slower and easier to misread without specialist review on hard cases |

Use one rule across the lane: if you are deciding where to look, quick-screen sources are fine. If you are applying a U.S. position, move to IRS operating materials. If the outcome depends on treaty-specific language, confirm in treaty text and escalate when interpretation is not clean.

That distinction prevents false confidence. IRS guidance pairs broad rules with treaty-specific exceptions, so a neat summary rate is still only a screen until your file supports the article basis, residency certification status, and control checkpoints.

We covered this in detail in Non-Resident Withholding on Contractor Payments: Platform Guide to the 30% Rule and Treaty Reductions.

Test treaty eligibility before applying any reduced rate#

A treaty rate stays a candidate until your file shows the treaty basis, the payment characterization, and the supporting records for the claimant. If any of those are unclear, keep the case open and resolve the gap before treating the reduced rate as decision-ready.

Quick lookup outputs are useful for triage, not final eligibility. The real test is whether the record you retain can support the claim.

Build one eligibility gate before payout release#

Use one repeatable checkpoint table so every reviewer tests the same items:

| Checkpoint | What to verify | Why it matters | Evidence to retain |

|---|---|---|---|

| Treaty source and status | You are using a current, official legal source for the relevant country pair | Summary pages can be incomplete or out of date for final decisions | Source used, review date, reviewer |

| Claimed treatment fit | The payment type is matched to the claimed treaty treatment with a short rationale | Clear characterization and rationale help avoid preventable errors | Reasoning note, source text used |

| Eligibility conditions in source text | Any stated eligibility conditions are reviewed for the claimant fact pattern | Skipping conditions can leave eligibility unclear | Condition review note, escalation flag if unclear |

| Claim documentation set | Claimant identity, residence claim, and supporting forms or records are internally consistent | Inconsistent files weaken defensibility | Document list, validation checks, decision timestamp |

In U.S.-linked cases, keep the legal hook and file trail explicit#

For U.S.-linked withholding decisions, keep a short record of the treaty text relied on, the legal basis used, the payment type, and the document set reviewed. This is a control choice. It prevents "treaty rate applied" from becoming an unsupported label.

The same documentation-first pattern shows up in IRS process design. The IRS has a dedicated U.S. certification track related to reduced treaty rates, and Form 8802 is a named document in that workflow. The practical takeaway is simple: reduced-rate outcomes should be tied to traceable documents and review steps.

Escalate ambiguity early instead of guessing#

When sources conflict or interpretation is not clean, escalate to specialist review instead of inferring from a nearby country pattern or a commercial summary. Also treat unofficial legal-text renderings carefully. FederalRegister.gov explicitly notes that users should verify against official editions and that some rendered formats do not provide legal or judicial notice.

Use interactive lookup tools to narrow work queues, then close decisions only when the file can answer three questions clearly: what treaty, what legal basis, and what evidence.

For a step-by-step walkthrough, see US-UK Tax Treaty Withholding Controls for Contractor Payment Platforms.

Use a decision table for apply, hold, or escalate outcomes#

Once you have checked treaty source, article fit, and file support, route every case to one explicit outcome. Apply the treaty rate, hold at the statutory rate, or escalate for legal or tax review.

This split helps prevent a common failure in cross-border withholding: treating "not fully proven" as "approved." If source confidence is high but eligibility evidence is weak, hold. If eligibility evidence is strong but treaty interpretation is unclear, escalate.

| Outcome | Use it when | What the reviewer must retain | Owner and timing rule |

|---|---|---|---|

| Apply treaty rate | Treaty source is current, income-article fit is documented, and claimant evidence supports the claim | Treaty or article note, source used, document list, decision timestamp, reviewer | Payments ops can release only after a named reviewer approves and a documented timing checkpoint is met |

| Hold statutory rate | Default rate is clear, but eligibility evidence is missing, incomplete, or inconsistent | Gap note, request for missing items, current rate basis, recheck date | Payments ops owns follow-up; case stays in queue with a named owner and a documented recheck date |

| Escalate for legal or tax review | Treaty text, article mapping, or interpretation is ambiguous even if the file is otherwise strong | Issue summary, conflicting-source note, documents reviewed, escalation timestamp | Tax or legal owner must accept the case and set the next timing checkpoint |

Make the choice mechanically, not by instinct#

Use two separate tests: source confidence and eligibility evidence. A reliable source does not justify a reduced rate if the claimant record cannot support the claim. In that case, hold at the statutory rate.

The reverse case matters just as much. You may have a strong document set and still face an article-interpretation question or a conflict between summary materials and treaty text. That is an escalate case, not a call for operator guesswork.

Use one short reason code in the case record, such as evidence gap, entity type mismatch, or article interpretation conflict. This keeps later audits workable and approvals out of free-text debates.

Add owners and timing so cases do not disappear in batch queues#

Name an owner for each state. "Escalated" is a status, not ownership. A payments ops analyst can own hold follow-up, while tax or legal owns interpretation questions.

This fits the same control discipline reflected in IRS process design concepts like Roles and Responsibilities, Program Controls, and Processing Time Limits. The IRS certification workflow also includes Form 8802 and uses the USRC database for payment recording and confirmation-number research. You do not need to copy that process. The useful lesson is simpler: named step, named owner, dated record.

Reopen the case when a material fact changes#

Do not treat the first decision as permanent. Add a recheck trigger for material changes, especially new or corrected claimant documentation, entity-type updates, or internal treaty-interpretation updates.

That matters because some cross-border tax outcomes remain uncertain and may depend on later specifics and domestic implementation choices. Your table only works if apply, hold, and escalate are living states with clear reopen rules.

Before you approve any reduced rate, standardize claimant documentation checks with the W-8 Form Generator.

Catch the failure modes competitors rarely spell out#

After you set an apply, hold, or escalate path, the next risk is false confidence. A common failure mode is treating quick references or reporting forms as if they were approval evidence for withholding outcomes.

| Failure mode | What it looks like | Required response |

|---|---|---|

| Quick chart only | The file has a chart percentage and no case-specific support | Keep the case in hold or escalate |

| Direction read in reverse | "Same countries, same result" is assumed without separate direction-specific support | Treat as unresolved until source and case align |

| Reporting forms used as support | Form 8938, FBAR, or a generic FATCA note is used to support a reduced withholding rate | Treat as a scope-boundary error and do not use it alone to approve withholding outcomes |

| Treaty outcome asserted without support | Treaty outcome language is asserted, but no separate treaty support is in the file | Do not approve pending cleanup; move the case to hold or escalate with a reason code |

Quick charts are screening tools, not approval support#

The Form 8938 and FBAR materials in scope do not validate any reduced withholding rate on their own. If a file only has a chart percentage and no case-specific support, keep it in hold or escalate it.

Use a simple file check. If you cannot show payment direction, the named country pair, and the internal support used for the decision, this is not an apply case.

Keep a short checkpoint note with source name, capture date, payment direction, and what still needs proof. A note that only says "rate per quick chart" is not decision-grade support.

Do not read a country pair in reverse#

These excerpts do not provide treaty article outcomes or reverse-direction rate support. If a file assumes "same countries, same result" without separate support, treat that as unresolved.

Force direction into the record every time: payer jurisdiction first, payee residence second, then income type and entity type. If the reference does not clearly match that direction, hold or escalate until the reference and case align.

A practical red flag is any note like "same treaty, should be same rate" that does not state who is paying whom.

Keep reporting forms out of withholding decisions#

Form 8938 is a reporting form for specified foreign financial assets when the applicable reporting threshold is met. It must be attached to the annual return and filed by that return's due date, including extensions, and it must identify the applicable calendar or tax year.

Filing Form 8938 does not remove the separate FBAR (FinCEN Form 114) filing requirement. Also, some accounts maintained by a U.S. payer are outside Form 8938 reporting scope, and Form 8938 is not required when no income tax return is required for the year.

So if a file uses Form 8938, FBAR, or a generic FATCA note as support for a reduced withholding rate, treat that as a scope-boundary error. Keep reporting records if needed, but do not use them alone to approve withholding outcomes.

Red flags worth adding to your review step#

Use a short red-flag pass before release:

- Support relies on Form 8938, FBAR, or FinCEN reporting artifacts instead of withholding evidence.

- Support relies on a quick chart percentage without case-specific backing.

- Source material does not clearly state payment direction.

- Treaty outcome language is asserted, but no separate treaty support is in the file.

If any red flag appears, do not approve pending cleanup. Move the case to hold or escalate with a reason code.

Build the evidence pack that survives audit questions#

If you expect to defend a decision later, build the file so another reviewer can reconstruct the path without guessing: what you used, what changed, and what action you took. A practical pattern visible in durable public records is a step trail, a latest-action entry, and a formal identifier.

Use a compact, time-ordered record for each decision:

| Evidence item | What to capture | Why it matters |

|---|---|---|

| Source snapshot | The exact page, screen, or PDF reviewed, plus capture date and source name | Recreates what the reviewer actually saw |

| Decision basis note | The specific internal rationale used for this case, tied to the status checkpoint used at review time | Shows how the decision matched the record available at that point |

| Document status | The status step and latest-action entry used at review time, with an internal document ID if available | Preserves traceability without duplicating full files |

| Approval event | Internal reviewer role and decision time, if your process records them | Creates accountable decision history inside your workflow |

| Execution link | The internal record reference tied to the executed outcome, if applicable | Connects the decision record to the resulting action |

Keep the record minimal and retrievable based on your internal policy.

Do not rely on text extracts alone when format details matter. Official text renders can omit graphics or visual context, so retain the original snapshot alongside any extracted notes.

Finally, link request, decision, and execution records with durable IDs. That small structure is often the difference between a fast audit response and manual forensics.

Implement controls in your payouts and reconciliation stack#

Treat withholding as a release control, not a post-payment note. If documentation, review, or exception handling is incomplete, your payout should not move.

That approach aligns with IRS operating guidance, including named control steps such as Program Controls and payment validation. In practice, the withholding decision should determine payout movement, not sit alongside it as optional context.

Gate payout release on decision status#

Use a strict release state before funds move from approved to released. The decision should be complete, traceable, and linked to the payment record.

A practical rule is simple:

- if a case has a candidate rate but no completed review state, keep it unreleased

- if data conflicts or authority is unclear, route to escalation instead of bypassing the gate

- if a lookup tool informed the review, store it as supporting input, not stand-alone authority

Make retries repeat the same decision#

If a payment is retried, keep the same decision and payment reference so the record remains traceable and consistent.

Keep one accounting truth, then derive ops views#

Keep one authoritative record for withholding actions and payment confirmations. Operations-facing views can still exist, but as derived views rather than separate edit points.

This is a control design choice that improves traceability: one durable record for what was recorded, when, and under which reference. Where possible, tie tax document collection state, payout status changes, and finance or compliance export artifacts to that same record so reconciliation stays reviewable instead of becoming forensic.

Also keep an explicit exception lane for misrouted items, and escalate unclear cases for specialist review. Summary guidance is not exhaustive or a substitute for law, so controls should stop uncertain payouts rather than force a guess.

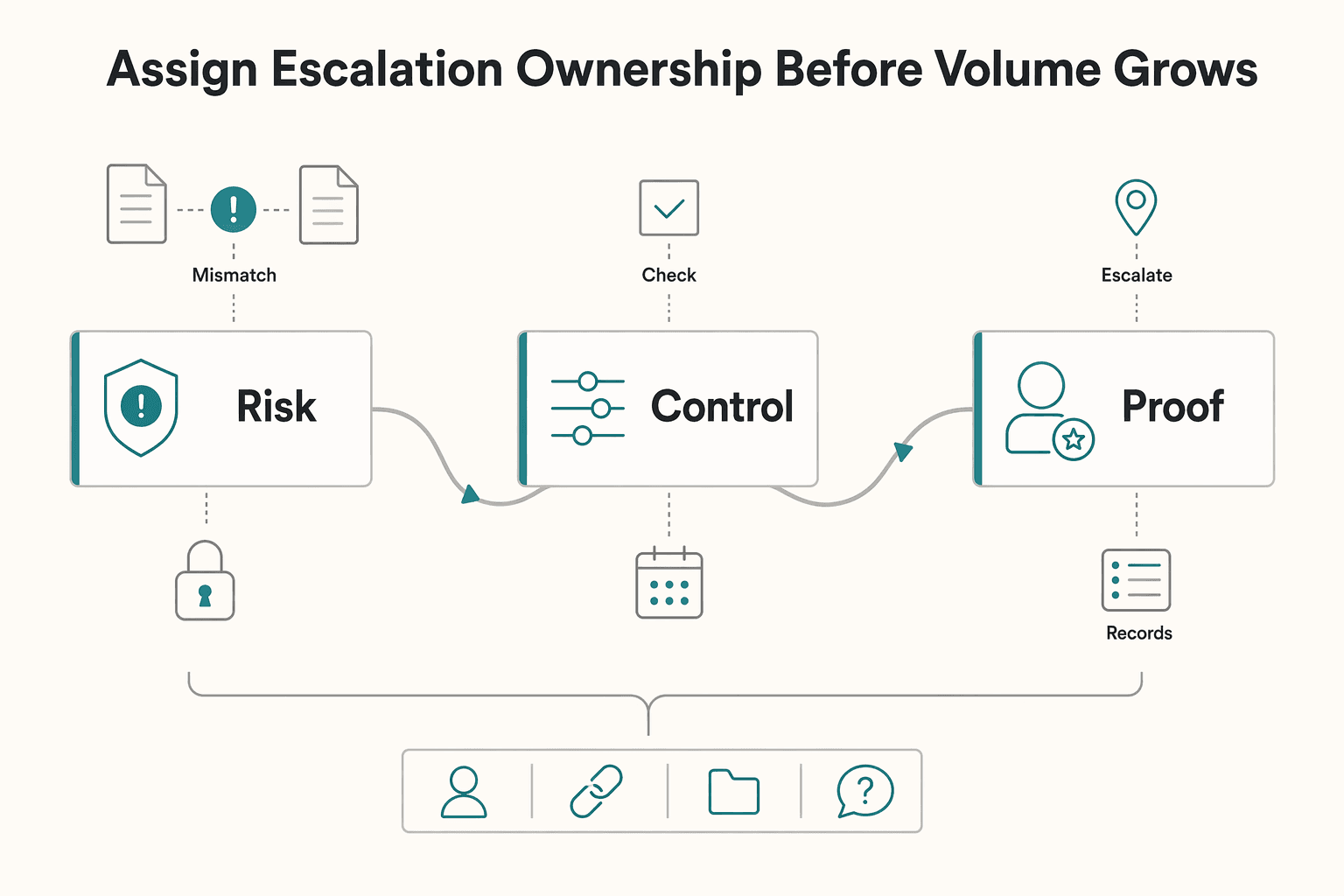

Assign escalation ownership before volume grows#

Once payout gates are in place, assign escalation ownership before volume turns uncertainty into backlog. If evidence is weak or missing, keep the case in hold. If judgment is unclear, route it to a named reviewer instead of leaving it with the last operator.

Define clear owners for each state: apply, hold, and escalate. For each handoff, capture a minimum record: decision owner, payment reference, case context, and the exact question to resolve. That helps keep escalations reviewable and more consistent.

Write escalation triggers before exception volume rises. Trigger escalation when interpretation is unresolved, when processing time limits are at risk, or when exception paths repeat, for example partial payments, multiple payments, or checks that do not belong to USRC. Before routing, confirm the case file includes the screening basis and the linked payout reference so the reviewer can issue a usable decision.

Use the IRS control pattern as a model for process discipline, not structure. IRM 21.8.4, "United States Certification for Reduced Tax Rates in Tax Treaty Countries," explicitly covers Roles and Responsibilities, Program Controls, and Processing Time Limits. It also treats recordkeeping and misroutes as operating steps, including USRC database research and a separate path for items that do not belong there. In practice, that means giving every exception a named owner, a time checkpoint, and a searchable record.

For complex corridors, start with specialist review. Once outcomes are stable and defensible, codify that logic into your decision table.

Make the lookup your first step, not your final answer#

Use the lookup for speed, then switch to decision controls. The practical sequence is fast rate discovery first, evidence and eligibility checks second, and escalation when facts still do not line up.

That split matters because speed and rigor solve different problems. A lookup helps you triage quickly once you have mapped payer jurisdiction, payee residence, income type, and entity type. The withholding decision needs a higher bar: enough support that another reviewer can see why you applied a reduced rate, or why you held the statutory position.

Separate triage from decision#

The problem is not using a lookup. The problem is treating a candidate rate as an approved outcome.

Keep each step narrow:

- Triage question: what rate should we investigate for this country pair and payment type?

- Decision question: are we comfortable applying it now, or do we hold the statutory position until the file is complete?

Separating those steps helps reduce two common failures: under-checking risky files and overbuilding full legal review for ordinary payments.

Verify the document path, not just the number#

For U.S.-linked cases, IRS IRM 21.8.4 is a useful operating model because it is specifically about U.S. certification for reduced tax rates in treaty countries. The workflow includes checkpoints around Form 8802, payment validation, and recording payments in the USRC database.

Apply the same discipline internally. When a reduced rate is in play, you should be able to point to the country pair, the income characterization used, the treaty support reviewed, and the claimant documentation on file. If that support package cannot be identified quickly, the rate may be discoverable, but it is not ready to apply.

Know the common break points#

A frequent break point is scope confidence. A treaty-style answer can look clean in a summary view while the tax at issue may fall outside treaty scope. The cited discussion of France's 3 percent digital services tax shows this risk: it is described as outside treaty scope because it is a consumption tax. Different fact pattern, same control lesson: if characterization is wrong, the lookup result does not protect the decision.

Another break point is evidence confidence. If the source looks clear but residence, entity details, or supporting documents are incomplete or conflicting, hold the statutory position. If documents look strong but treaty applicability is still ambiguous, escalate instead of guessing.

Build three things before you expand#

Do not start by operationalizing every corridor. Prove the sequence on one country pair first:

- One decision table with three outcomes: apply treaty rate, hold statutory rate, escalate.

- One evidence-pack template with lookup snapshot, treaty support reviewed, document status, approver, and timestamp.

- One escalation path with a named owner for unclear characterization or treaty applicability.

If those three pieces work for one corridor, expansion is usually cleaner.

Related: How to Build a Global Tax Withholding Engine: W-8 W-9 and Treaty Rate Automation.

When you are ready to operationalize this framework, map your controls to Payouts so apply, hold, and escalate decisions stay traceable from review to execution.

Frequently Asked Questions

What is the difference between statutory withholding tax and treaty withholding tax in practice?

Statutory withholding is the domestic rate set under a country’s own law for an income type. A treaty rate is a possible reduction from that statutory rate, sometimes to zero, but only when treaty conditions and required proof are met. If eligibility or procedure is not established, use the statutory position as the operating fallback.

Can we apply treaty rates directly from an interactive lookup tool without further checks?

No. A lookup tool is a screening aid, not final authority. You still need to verify the relevant facts and required residency evidence, then follow the jurisdiction’s process. Some countries allow treaty-rate withholding at source, while others withhold at statutory rates first and handle refunds later.

What minimum checks should be completed before claiming a reduced treaty rate?

Confirm the payment is in scope for withholding and that a treaty reduction is available for that situation. Confirm you hold the residency proof the paying country requires and that you are following that country’s procedure for applying the rate. Where U.S. residency certification is required, a concrete checkpoint is whether certification has been requested through Form 8802.

Are treaty rates always reciprocal between two countries in both payment directions?

Do not assume reciprocity. A treaty relationship does not guarantee identical outcomes in both payment directions. If a summary view looks symmetric, treat that as a prompt to verify, not a final conclusion.

If a treaty does not specify a rate for an income type, what default rate may apply and who decides?

If treaty text or official guidance does not clearly provide a reduced rate, do not infer one from a lookup summary. Treat it as a hold-or-escalate decision pending jurisdiction-specific tax or legal review.

Which sources are best for quick lookup versus final compliance determination?

Use interactive tools and summary tables for triage and prioritization. For final determinations, rely on treaty text, relevant government guidance, and the claimant’s supporting documentation or residency certification. OECD withholding-tax material is useful context, but not transaction-level legal authority for a specific file.

What records should a platform retain to defend withholding decisions in an audit?

Keep the documentation that supports the rate applied, especially the residency evidence or certification used. If U.S. residency certification is part of the basis, retain records tied to the Form 8802 certification process and related processing controls. The goal is a file another reviewer can reconstruct without assumptions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

US-Germany Treaty Withholding Decisions for Contractor Platform Payouts

For U.S.-Germany contractor payouts, the safest starting point is simple: do not force a single withholding answer when payment characterization or treaty access is unclear. The hard part is usually not finding treaty text. It is deciding what your team can defend before funds move in a platform-mediated payout.

How to Build a Global Tax Withholding Engine: W-8 W-9 and Treaty Rate Automation

A defensible **global tax withholding engine w-8 w-9 treaty rate automation** setup lives or dies on payout-level traceability, not just form collection. Collecting Form W-9 or Form W-8BEN is only the first control. You also need to show why a specific withholding rate, including any treaty rate, was applied.

A Deep Dive into the US-France Tax Treaty for Freelance Performers

Your biggest risk here is operational, not theoretical. You finish a gig in France, payment arrives short, cash flow gets squeezed, and no one can tell you whether the withholding was required, avoidable, or recoverable.