Quick Answer

Yes - treat the us-france tax treaty for performers as a documentation workflow, not a headline rate. Verify the current Article 17 position with the payer before payment, confirm the base they will use, and provide the residency documents they request. Keep one complete file with contract, invoice, settlement record, payment proof, and tax emails so any withholding can be traced and reviewed. If active thresholds, rates, or form names are uncertain, pause and get case-specific advice before acting.

The CEO's Guide to the US-France Tax Treaty: A Playbook for Performers#

Your biggest risk here is operational, not theoretical. You finish a gig in France, payment arrives short, cash flow gets squeezed, and no one can tell you whether the withholding was required, avoidable, or recoverable.

Start from a cautious default. Treat any specific rate, exemption threshold, expense-inclusion rule, form, or deadline as unconfirmed until you verify it in current official materials or with a qualified advisor.

Start with working definitions#

Use these as internal operating terms for this article, not as verified treaty text:

| Term | Meaning |

|---|---|

| Performer income scope | payments tied to your France performance activity or paid because of it |

| Gross receipts | pre-tax total used for risk tracking before withholding, commissions, processor fees, or other deductions |

| Reimbursed expenses | costs paid back to you, or paid on your behalf, such as travel, lodging, local transport, or production items |

| Withholding | tax held back by the payer before funds reach you |

| Treaty relief path | any process, if available, to reduce withholding before payment or deal with it afterward |

Keep these labels consistent across your contract, invoice, settlement records, and tracker. If you cannot show the current rule text, the payer's stated position, and your supporting document trail, you do not have a tax plan yet.

What to verify before you trust any number#

Do not start with a headline rate. First confirm the payment base and document expectations in writing. Ask the payer three questions before you invoice or perform:

- What do you plan to withhold?

- What payment base are you using?

- What documents do you need from me to support the treaty position you are applying?

Then build one evidence pack: signed contract, invoice, settlement statement, payment advice, expense records, and tax-treatment emails. If a dispute comes later, clean records usually determine whether you can fix it quickly or spend months reconstructing the file.

A practical classification table#

Use this as internal triage, not a legal ruling. Treaty treatment for these items is unverified.

| Payment type | Working classification | Why it sits there |

|---|---|---|

| Performance fee or guarantee from the promoter | Confirm with the relevant authority | It is tied to the engagement, so confirm treatment before relying on any assumption. |

| Box office bonus or backend in the same settlement | Confirm with the relevant authority | It may affect the payment base, but treatment is not verified here. |

| Cancellation fee linked to the booked appearance | Confirm with the relevant authority | It is connected to the engagement; confirm handling with a qualified adviser. |

| Refund of a security deposit you originally paid | Confirm with the relevant authority | It may be a return of funds or a compensating amount depending on facts. |

| Pure pass-through funds with matching records | Confirm with the relevant authority | Documentation and legal characterization determine treatment. |

| Travel reimbursement paid to you | Confirm with the relevant authority | Confirm expense treatment with the relevant authority. |

| Hotel, flights, or local transport paid on your behalf | Confirm with the relevant authority | Treatment may differ by structure, so verify current rules. |

| Per diems, stipends, or production allowances | Confirm with the relevant authority | Labels alone do not settle treatment; verify substance and current guidance. |

| Merch income, licensing, or media rights bundled into one deal | Confirm with the relevant authority | Bundling can obscure treatment, so itemize before taking a treaty position. |

Main red flag: bundling. If one contract mixes fee, travel, buyout, merch, and media rights into one number, break it out before payment.

Once you have a working view of what may be in scope, put the engagement in the right stage so the next move is clear.

Pick your stage#

| Stage | Context | Priority |

|---|---|---|

| Stage 1 | Planning or contracting | Verify current rules, align on payment base, and build the document trail before funds move |

| Stage 2 | In-country execution or imminent show | Confirm payer actions, reconcile invoice to settlement, and save every supporting record |

| Stage 3 | Post-payment cleanup | Identify what was withheld, by whom, and on what base, then assemble records for the next recovery or credit decision |

Choose the stage based on where the money and documents sit right now. For the rest of this guide, keep treaty mechanics provisional until verified, and treat documentation plus cash-flow controls as non-negotiable.

Related: Tbilisi, Georgia: The Ultimate Digital Nomad Guide (2025).

Stage 1: Pre-Tour Strategy - Designing Your Success Before You Land#

Your pre-tour job is simple: prevent avoidable withholding and assign responsibility before any service is delivered or paid. For the treaty rules that matter to performers, outcomes are often driven more by the contract, the document handoff, and year-to-date receipts tracking than by a headline summary.

Article 17 is the starting point for performer income and overrides the general independent-services and employment framing for this income type. That means a generic contract is not good enough. It should say who handles treaty paperwork, when documents move, and what happens if paperwork is incomplete when payment is due.

Lock the contract before the show#

This is the moment to remove ambiguity. If the contract leaves tax handling vague, the payer may default to its own protection. Use this checklist before signature:

| Contract point | What to specify |

|---|---|

| Treaty reference | Cite the U.S.-France treaty and Article 17, then keep the current exemption rule and withholding treatment pending treaty, tax authority, and advisor verification. |

| Filing ownership | Name who prepares, submits, and tracks the treaty-relief package with the French payer or withholding side |

| Document handoff timing | Set dates for your Form 6166 delivery, any French residence-attestation paperwork such as Form 5000-SD, and payer acknowledgment |

| Payment terms | State whether payment is gross if relief is accepted, or net if withholding is applied, and require a settlement statement showing the payment base used |

| Fallback language | If paperwork is late or rejected, require written notice before payment, the withholding basis used, and remittance or filing evidence |

In practice, name the filing owner, set document deadlines, and require written notice if the packet is late or rejected.

Also get the actual withholding contact, not just "accounts." IRS instructions for Form 6166 say it should go to the foreign withholding agent or other appropriate person. IRS also warns that some countries withhold first at statutory rates and process refunds later.

Start residency paperwork early. Form 8802 is required to request Form 6166, and IRS instructions say to mail it at least 45 days before you need to submit Form 6166 abroad.

Finally, verify treaty text together with protocol text. For France, the protocol entered into force on December 23, 2009. IRS Table 3 lists Jan. 1, 2010 as the protocol date to check in planning.

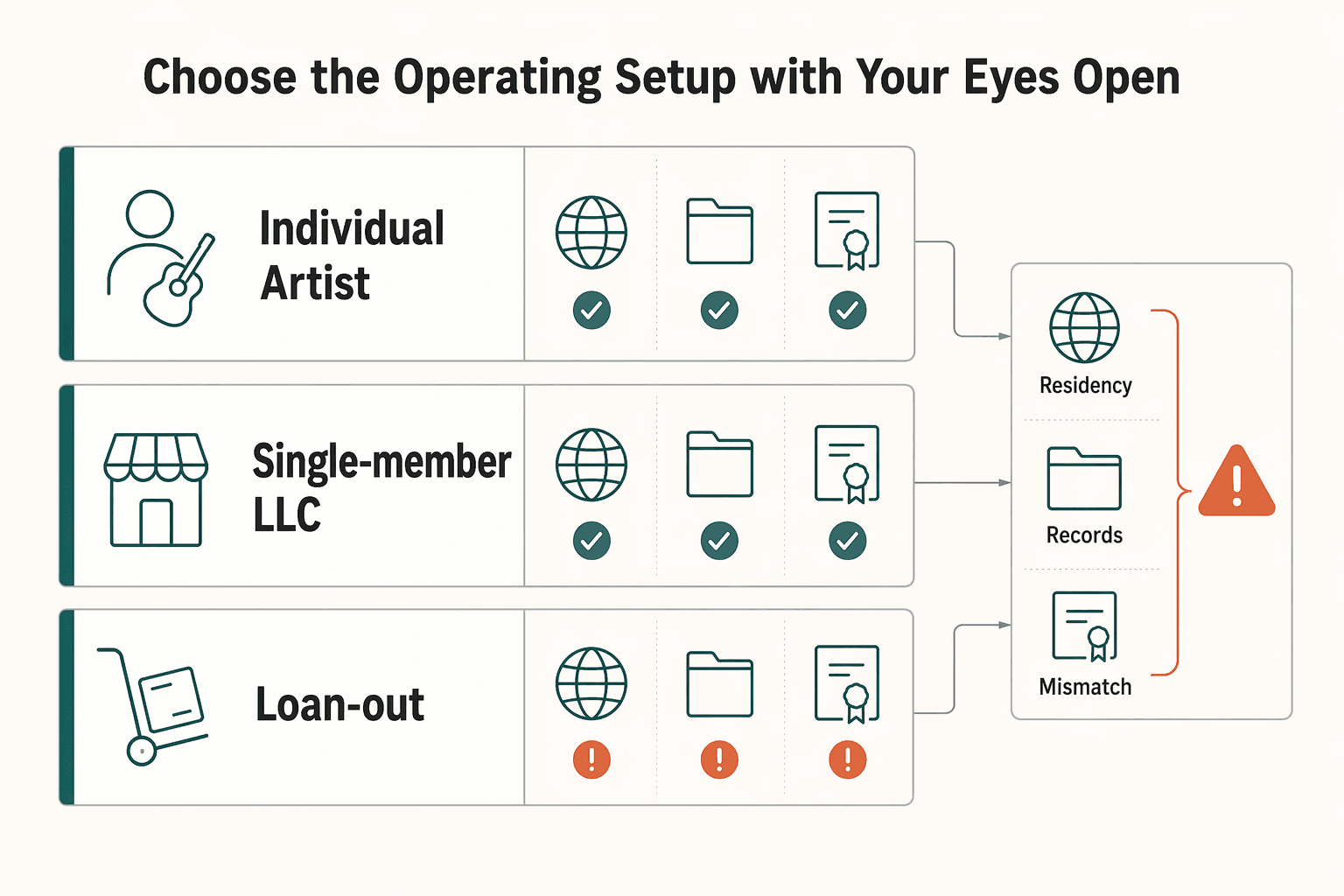

Choose the operating setup with your eyes open#

No common setup automatically fixes Article 17 issues, so treat the entity choice for what it is: a risk-allocation decision, not a shortcut.

| Setup | Stage 1 implication | Main risk | Specialist review trigger |

|---|---|---|---|

| Individual artist | Often the cleanest document chain for residency and treaty paperwork | You carry classification and recordkeeping risk directly | Mixed income streams, multiple French payers, or possible permanent professional establishment facts |

| Single-member LLC | Can be workable, but payer acceptance of tax and ownership facts must be explicit | Structure confusion can lead payer to default withholding | Contract, invoice, banking, and treaty claimant details do not align |

| Corporate loan-out | Requires careful analysis of who earns income and who claims treaty treatment | Mismatch risk across performer, entity, and documents | Strongly recommended for setup and contract review |

If the contract name, invoice name, and residency certificate owner do not match, you can face friction and possible withhold-now treatment.

Model the year, not just the gig date#

A one-show view is where teams get surprised. Build your pre-tour model around cumulative France receipts, including reimbursed expenses or amounts borne on your behalf, and test that against the verified rule text.

| Scenario | Pre-tour choice | Promoter communication | Cash-flow planning |

|---|---|---|---|

| Clearly below the verified threshold | Push early treaty-relief processing and keep categories itemized | Confirm required documents, owner, and timing in writing | Plan for gross settlement path, but keep fallback records ready |

| Near the verified threshold | Re-check each reimbursement or allowance classification before signature | Require explicit base-of-payment and treatment confirmation | Keep contingency for either gross or net settlement |

| At or above likely threshold | Assume higher withholding risk unless confirmed otherwise | Request detailed settlement or remittance support before payment | Budget for potential net payment and later recovery work |

Bundled contracts can create avoidable ambiguity. Break out performance pay, reimbursements, licensing or media, merch, and production items before signature.

Escalate early when facts are not clean#

Some fact patterns are not worth forcing through a standard process. Bring in a specialist before the tour starts if you have:

- multi-entity arrangements or split payment instructions

- mixed income streams, including performance plus licensing, merch, sponsorship, or media rights

- unclear reimbursement or allowance classification

- uncertain treaty eligibility or protocol-adjusted treatment

- uncertain fit with the nonresident-artist fact pattern, including possible permanent professional establishment issues in France

You might also find this useful: A Guide to France's Micro-Entrepreneur Regime for Freelancers.

Stage 2: On-the-Ground Execution - Your France Compliance Checklist#

Once the trip is live, the goal shifts from planning to clean execution. Compliance drift usually comes from process gaps: late documents, mismatched payer and payee details, or promoter workflows that were never checked against Article 17 and current tax-office instructions.

Get the order and ownership right#

The fastest way to lose control is to assume the promoter knows who should receive what. Confirm responsibilities in writing before invoicing. Ask the promoter who receives treaty paperwork, whether they require a French residence-attestation form such as Form 5000-SD, and what they treat as sufficient proof before payment approval.

For U.S. residency proof, file Form 8802 to request Form 6166, and budget for the Form 8802 user fee. Filing lead time is pending IRS/source verification, so confirm the active timing before setting the internal deadline. Before submission, verify that the contract, invoice, vendor record, and Form 6166 details match by name, address, and taxpayer identity to reduce rejection or withholding risk.

If the promoter's instructions conflict with treaty text or French guidance, stop there. Request the instruction in writing, capture which office or team issued it, compare it against official treaty documents, and escalate to an advisor before funds move.

Build the minimum viable proof packet#

A thin file is fine until something goes wrong. Keep one payment-defense folder per tax year and event, with scanned copies plus retained originals or certified copies where relevant.

| Document | Owner | Purpose | Storage location | Failure risk if missing |

|---|---|---|---|---|

| Signed performance contract | You and promoter | Confirms payee, service date, and payment terms | Year folder, event subfolder | Hard to prove who earned the income and what payment covers |

| Form 8802 filing proof | You | Shows Form 6166 request was filed (with required fee) | Residency subfolder | Hard to explain missing or late Form 6166 |

| Form 6166 | You (issued by IRS) | U.S. residency certification for treaty-benefit claims | Originals file plus scanned PDF | Promoter may reject treaty treatment or hold payment |

| Form 5000-SD (if requested) | You complete your part; promoter routes per their process | Residence-attestation support used in some French workflows | Event folder, with retained record copy | Packet may be treated as incomplete |

| Promoter acknowledgment, settlement statement, or withholding or remittance evidence | Promoter | Shows accepted treatment and withholding basis, if applied | Correspondence folder | Weak support for later reconciliation, refund, or credit work |

Practical caveat: retrieved Form 5000 guidance is framed around dividends, interest, and royalties appendices, not explicitly performer fees. If requested, treat it as process-specific documentation, not automatic proof that it is the definitive performer packet.

Track totals while the tour is live#

This is where a simple tracker earns its keep. Use one row per payment event and keep categories separate so you can spot threshold and classification issues before the next invoice goes out.

Track these items for each event:

- promoter and event name

- service date and payment date

- fee income

- reimbursed costs

- amounts paid on your behalf

- treaty-relevant total for that event

- cumulative treaty-relevant total for the year

- document status (

requested,sent,accepted,questioned) - trigger note: re-check the current cumulative threshold rule and expected withholding treatment after treaty, tax authority, and advisor verification

If cumulative totals approach your verified rule, or the promoter changes withholding treatment, stop auto-pilot and re-check before issuing the next invoice.

Exception path when something breaks#

Problems are common. Force the issue into writing while the facts are still fresh.

- Late paperwork: Plan for the possibility that payment is processed with withholding. Ask whether payment can be held pending review. If not, require a written settlement statement showing the basis used. Consult advisor now when the amount is material or multiple French payers are involved.

- Rejected residency proof: Ask which exact field failed (for example, identity or address details), correct it, and resubmit. Do not replace requested formal residency certification with informal letters.

- Mismatched payer/payee details: Pause payment release, reconcile contract entity, invoice issuer, and bank beneficiary, and request payer remittance evidence if withholding is applied. French payer-side withholding declarations, including Form 2494-SD, are payer-oriented and include quarter-based remittance timing.

For a step-by-step walkthrough, see A Deep Dive into the US-Israel Tax Treaty for Tech Freelancers.

Use a single log for travel days, contracts, and payment evidence so your treaty file stays consistent from booking to filing: Tax Residency Tracker.

Stage 3: Post-Tour Reconciliation - The Safety Net for Your US Tax Return#

Treat year-end as a decision point, not as admin cleanup. If withholding or treaty questions come up, flag them for professional review instead of assuming one filing route is automatically correct.

Do not file from net cash alone. Reconcile contract and settlement records to the gross amounts you plan to report, then map those amounts into your return workpaper. If any key element is weak or missing, mark it for verification before filing. Keep current credit-limit mechanics and form-handling nuance pending official source and advisor verification before use.

Reconciliation pack that actually holds up#

At this stage, weak records are usually more dangerous than an unfavorable answer. Build the pack so a reviewer can follow the payment from contract to return without guessing.

| Required record | Why it matters | Common mismatch risk | Corrective action |

|---|---|---|---|

| Signed contract and final invoice | Anchors payee, service date, and billed amount for reconciliation | Invoice entity does not match contract or bank beneficiary | Reconcile names, addresses, and taxpayer identity before filing |

| Payer settlement statement or withholding document | Supports withholding/tax reporting review | Only net payment proof exists, with no tax breakout | Request written remittance detail from payer |

| Payment proof and bank records | Shows what was received and when | Payment timing differs from service or invoice timing | Add a dated memo that explains timing differences |

| Return workpaper with open tax-treatment questions | Keeps unresolved items visible until verified | Key assumptions are undocumented | Add explicit verification notes and advisor follow-up items |

Your year-end close checklist#

Keep the Digital Shoebox, but run it like a close:

- Confirm each payment event has contract, invoice, payment proof, and any withholding document you received.

- Flag inconsistencies in payee identity, dates, and billed-versus-paid amounts.

- Trigger advisor handoff when multiple payers are involved, withholding support is missing, or treaty/credit treatment is unclear.

- Archive one locked year folder with scans plus retained originals or certified copies where relevant.

Final return checkpoint: if your filing uses Form 1040-NR, complete the applicable items on Schedule OI (Form 1040-NR) and include it with the return. More complex returns may require additional schedules, and e-file software will generally determine which ones are needed. Also avoid a common mismatch: Schedule A (Form 1040-NR) is not used with Forms 1040 or 1040-SR.

If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Conclusion: You Are the CEO of Your Career#

For lower-drama cross-border work, act like the person responsible for the whole machine: process over improvisation, records over memory, and documentation over assumptions.

The three-stage model stays simple so it still works under pressure:

- Stage 1, pre-tour strategy: verify live treaty materials before relying on them, especially Article 17, then set up documents early: Form 6166 requested through Form 8802, and confirm whether Formulaire 5000-SD is needed on the France side. Outcome: fewer preventable withholding surprises and a usable position before contracts are signed or payments are released.

- Stage 2, on-the-ground execution: keep contract, invoice, settlement records, and payment proof aligned on payee identity, dates, and amounts, with records the IRS would recognize. Keep performance income clearly separated from other line items. Outcome: fewer classification disputes and a defensible evidence pack if questions come from a payer, preparer, or tax authority.

- Stage 3, post-tour reconciliation: if withholding occurred, move from prevention to recovery using Article 24 as a relief anchor, supported by tax-paid documentation and the U.S. filing path (including Form 1116 for foreign tax credit claims). Outcome: lower double-tax risk and a cleaner route to claim relief on your U.S. return.

Final rule: re-check current treaty text and administrative practice before relying on any rate or exemption claim. Current withholding and exemption references remain pending official source and advisor verification.

Escalate to a qualified cross-border tax professional when your case includes an entity, mixed income types, uncertain treaty treatment, unclear state-tax interaction, or complex foreign tax credit questions.

For a related treaty workflow example, see A Deep Dive into the US-Ireland Tax Treaty for Tech Consultants.

If your performer income, reimbursements, and entity setup create edge cases, get a pre-filing review so your compliance plan is clear before year-end: Contact Gruv.

Frequently Asked Questions

How do I prove my treaty position or any threshold-based claim?

The provided treaty excerpts do not set out proof standards or threshold mechanics. Build a complete record set and verify current documentation requirements before relying on a treaty position. If key records conflict or are missing, treat that as a professional-review trigger.

What counts as performer income, and what about reimbursements?

Use Article 17 as the treaty anchor for performer-related questions. The provided excerpts do not confirm how reimbursements are treated for withholding or thresholds. Keep reimbursements separately itemized until that treatment is verified from current official guidance.

Which forms and documents should I map?

Start with the treaty article map, then verify current form names, filer responsibility, and timing before relying on any document set. | Scenario | Form or document | Who files or prepares it | When to prepare | | --- | --- | --- | --- | | Treaty analysis for performer income | Treaty article map (Articles 17, 24, 30; Article 29(2) checkpoint) | Verify for your case | Verify for your case | | France-side relief before payment | Current France-side treaty-relief forms pending source verification | Payer versus performer responsibility pending source verification | Timing requirements pending source verification | | Residency support for treaty position | Current residency-support documents pending source verification | Responsible filer or preparer pending source verification | Timing requirements pending source verification | | U.S. return and double-tax relief path | Current U.S. forms pending source verification | Responsible filer or preparer pending source verification | Timing requirements pending source verification | | Evidence pack for reconciliation | Contract, invoice, settlement records, payment proof, residency file | Each party maintains its records | Keep updated through close |

Which forms matter most?

The treaty article anchor and the admin form workflow are separate decisions. Use the treaty map to frame the position, then verify active form names, filer responsibility, and timing from current official instructions before relying on them. If the active form set is still unclear, escalate to a qualified reviewer.

Does my LLC or company change treaty eligibility?

Possibly. The provided excerpts confirm Article 30 (Limitation on Benefits) as a relevant checkpoint, but they do not provide entity-specific outcomes for this scenario. If entity and residency facts do not line up cleanly, escalate for case-specific review before payment.

What if withholding happened, treaty relief was missed, or I also sold merchandise?

Use Article 24 as the treaty anchor for relief-from-double-taxation questions. The provided excerpts do not include the procedural steps, form sequence, or deadlines for a specific relief path, so verify those items before acting. Keep performance and merchandise lines clearly separated in contracts and invoices to reduce ambiguity during later review.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

How Freelancers Can Decide on France’s Micro-Entrepreneur Regime

Low-stress compliance starts with one question: does the Micro-entrepreneur regime match your real setup right now? It is often presented as a simplified option for lower-revenue activity, so use it as a fit test, not a shortcut.