Quick Answer

Build the decision in order: classify the payment, confirm U.S.-sourced FDAP status, and verify foreign-status or treaty-claim documentation before any reduced withholding. If any item is unresolved, keep baseline withholding or hold-for-review instead of releasing on a UK profile label. Require one file that links authority, payment characterization, reviewer outcome, and expected Forms 1042/1042-S treatment so a second reviewer can reproduce the decision.

US-UK withholding errors usually come from control gaps, not missing treaty awareness#

For US-UK contractor payouts, the main risk is usually not a lack of treaty awareness. Your team creates risk when it approves reduced or zero withholding before you confirm income source, payment type, and treaty-status documentation. A UK label on its own does not support the treatment.

The IRS also draws a line between orientation material and legal authority. Its withholding-agent FAQs are useful for baseline awareness. But the IRS says those Q&As "do not constitute legal authority and may not be relied upon as such." If your team is approving treatment from summary notes alone, the control chain is already weak.

Start with a Chapter 3 lens, not a country-label lens. The IRS frames withholding and reporting responsibility around U.S.-sourced FDAP payments to a foreign person. Your first gate is straightforward: what is being paid, is it U.S. sourced, and is foreign-status or treaty-claim documentation complete? If those inputs are incomplete, stop the approval path.

This is also the right way to choose controls for your platform size and risk. We recommend that you choose them for defensibility, operational fit, and auditability, not for how smooth the payout flow looks on the surface. For contractor payouts where U.S.-sourced income and country-of-residence claims affect release decisions, a controlled decision has a simple sequence:

- Classify before you exempt

Classify the payment from the contract and payout context before treaty logic runs.

- Document status before treatment changes

The IRS explicitly points withholding agents to documenting foreign status or treaty claim. If the file is incomplete, do not auto-apply relief.

- Keep one audit trail per decision

Your classification, documentation, and withholding outcome should reconcile to the transaction record in one traceable chain.

A few recurring mistakes explain why teams get tripped up even when they know a treaty exists. A Stanford independent personal services treaty table lists the United Kingdom with article citation 7 and "--" in threshold fields. That is a prompt for further review, not proof that all UK contractor payments qualify for blanket treaty treatment.

Teams also tend to overread FAQ language in edge cases. The IRS withholding-responsibility Q&A section is marked updated April 18, 2024, and it points to Treas. Reg. Sec. 1.1441-2 for exceptions even on U.S.-sourced payments. In practice, your process should capture whether an exception was considered and why it did or did not apply.

Keep taxpayer filing topics in a separate lane. This is not personal filing guidance for FBAR, FinCEN Form 114, FATCA, Form 8938, or Schedule SE. Form 8938 is a specified foreign financial asset reporting form. It is attached to an annual return and filed by that return's due date, including extensions. Filing Form 8938 also does not remove any FinCEN Form 114 filing requirement. That separation matters because taxpayer reporting may be relevant to the payee, but it does not decide your platform's withholding control path.

The practical priority is simple: force source checks, payment classification, treaty-claim documentation, and audit-ready approvals before funds move. If that chain is unclear, tighten the hold point before adding more automation.

1) Use official treaty authority before any withholding exemption decision#

Make this the first control. Before any withholding exemption is approved, require a documented citation to official U.S. government material and the internal policy that applies it. If that record is missing, do not treat the payment as exempt.

This belongs first because it forces source discipline before case-by-case interpretation starts. IRS Publication 515 explicitly identifies the withholding agent role and separately flags Forms 1042 and 1042-S reporting obligations. Your team should document both the release decision and the reporting consequence.

Before release, the minimum decision file should include:

- the exact official U.S. source used for the decision

- the internal policy language mapped to that source

- payment classification, payee identity, and reviewer decision (approve or escalate)

- the expected Forms 1042 and 1042-S reporting treatment

The check is simple: another reviewer should be able to reopen the file later and see exactly what authority was used and how the policy was applied. If the file depends on a memory, a chat thread, or a general sense that "this is a UK contractor," it is not ready.

This is basic, but it is where many teams drift. The common failure mode is speed. Teams operationalize summaries from blogs, decks, or internal chat as if they were authority. A second failure is mixing UK taxpayer process with U.S. withholding authority. HMRC Self Assessment recordkeeping and timing may matter for the contractor, but they do not determine whether a U.S. payment should be released under a withholding exemption.

In practice, this control works best when it is narrow and mandatory. Do not ask reviewers to assemble authority after they have already decided the outcome. Require the authority record before the release decision is even available. That reduces hindsight reasoning and keeps the decision anchored to the source that actually supports it.

It also creates a cleaner link between withholding and reporting. If your team cannot identify what it expects to do for Forms 1042 and 1042-S, that is a useful signal that the underlying release decision is still underdeveloped. The reporting consequence should not be an afterthought. It should appear in the same decision file as the authority and the classification.

The tradeoff here is slower setup, because legal and ops need to align before automation ships. The payoff is a defensible record and fewer reversals when reporting obligations are reviewed. If you want a payout process that survives second review, reconciliation, and later audit work, this is the place to be strict.

Related: US-India Tax Treaty and Contractor Payments: Royalty and Fee Withholding for Platforms.

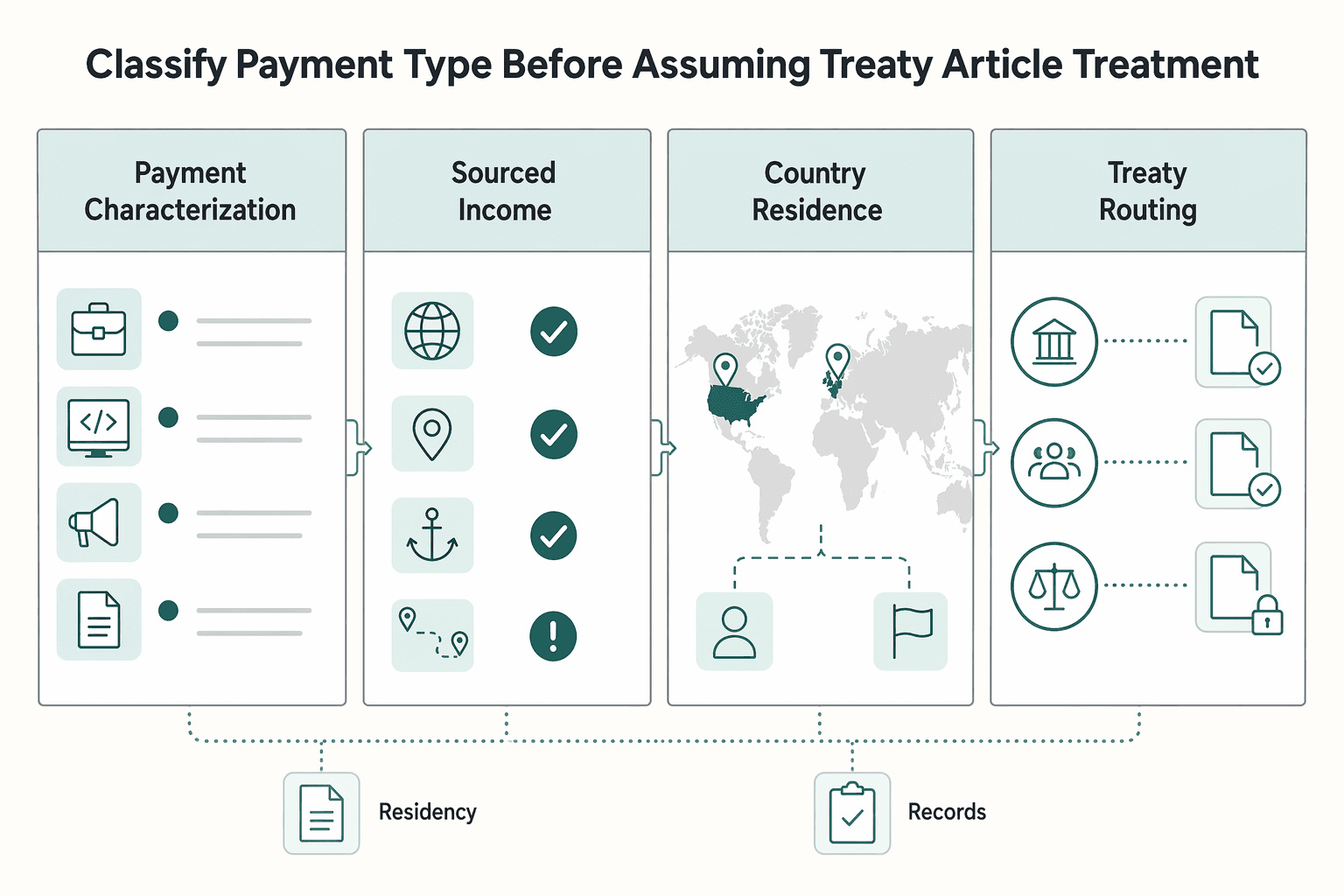

2) Classify payment type before assuming Treaty Article 7 treatment#

Classify the payout before treaty routing. If you skip classification, Article 7 turns into a catch-all and you increase the risk of applying relief to the wrong payment type.

Start with a narrow intake gate. If your policy still uses an Independent Personal Services branch, keep it explicit instead of folding those cases into Article 7 by default. The point is not to create more labels than you need. It is to make sure treaty analysis starts from what the payment actually is, not from the country in the profile.

Before treaty logic runs, the gate should capture the following:

| Gate field | Capture | Review trigger |

|---|---|---|

| Payment characterization | Exact contract or invoice wording for what is being paid | Services and usage/license language both appear |

| U.S.-sourced income status | Marked by policy as yes, no, or unresolved | Source is inferred from profile details instead of case facts |

| Country of residence | Claimed residence and whether evidence is on file | Residence is assumed from banking/contact metadata |

| Treaty routing | Selected article or escalation path | Article 7 selected before the first three fields are complete |

The control is in the sequence. Classify first, then decide whether treaty analysis is appropriate.

This is also the right place to be skeptical of shortcuts. A Stanford independent personal services treaty table listing the United Kingdom with article citation 7 and "--" in threshold fields can be useful as a pointer. It is not proof that every UK contractor payment belongs in a single treaty lane. A table entry is a prompt to review the real decision file, not permission to bypass it.

The same goes for profile data. Country-of-residence claims matter, but residence should not be inferred from banking or contact metadata. If the system is turning a bank country, mailing country, or general UK label into treaty routing, then the control is backwards. Residence evidence belongs in the file. It should not be guessed from adjacent fields.

Keep UK filing administration separate from U.S. payout classification. GOV.UK notes Self Assessment mechanics such as UTR use, possible account reactivation, and recordkeeping like bank statements or receipts. It also notes filing limitations in some non-resident scenarios. Treat those as payee administration signals, not as evidence of payment type for U.S. withholding decisions.

A useful rule for unclear files is simple: when characterization is unclear, do not auto-apply treaty relief. Route the payout to your policy default, for example baseline withholding or hold-for-review, until classification is resolved and documented. That protects the process from being pushed forward by urgency alone.

If your team remembers only one thing from this section, make it this: Treaty Article 7 is not a substitute for classification. It comes after classification, not before it.

You might also find this useful: Non-Resident Withholding on Contractor Payments: Platform Guide to the 30% Rule and Treaty Reductions.

3) Apply treaty relief only when eligibility evidence is complete#

Apply treaty relief only after the eligibility file is complete. Keep default U.S. withholding tax in place until the record is complete enough that a second reviewer could reach the same outcome from the file alone.

That second-reviewer standard is useful because it forces clarity. A reviewer should be able to answer, without guessing:

- who the payee is

- whether there is liability for tax

- the amount to withhold

- when to withhold

If any point is unresolved, do not move the payment to treaty treatment under the U.S.-UK Income Tax Treaty. UK residence on its own is not a release trigger.

For operations, define "complete" narrowly as one transaction file that ties together:

- final payment classification from the prior control

- payee identity and residence evidence on file, not inferred from profile or banking metadata

- treaty basis note and reporting consequence for Forms 1042 and 1042-S

If the team cannot state how the payment will be handled for Forms 1042 and 1042-S reporting, the approval record is not complete.

That standard matters because incomplete files often look better than they are. A file may have a UK address, a UK bank account, a contract that sounds service-based, and a reviewer note that says "treaty." That does not mean the eligibility record is complete. The question is whether the file actually ties identity, residence evidence, payment classification, treaty basis, and reporting consequence into one coherent packet.

This is also where teams need to resist substituting UK admin proof for U.S. withholding eligibility. A UTR, Self Assessment status, or HMRC timing points such as 31 January, first-time registration, or account reactivation can be valid payee admin details, but they are not U.S. withholding eligibility proof by themselves. If status is unclear, hold to your default review path until eligibility evidence is complete.

Keep the release rule simple:

- do not release on a country label alone

- do not release on contract language alone

- do not release because the payee says they are UK resident if the evidence file is incomplete

- do not release because someone believes Forms 1042 and 1042-S can be sorted out later

Instead, use a hard release gate. Either the file is complete enough for a second reviewer to reach the same result, or it is not. If it is not, the payment stays in the default path.

That may feel conservative, but it solves a real operational problem. Most payout mistakes are not driven by sophisticated treaty interpretation. They are driven by releasing a payment before the file is complete enough to support the decision. A hard gate fixes that earlier than any downstream cleanup can.

Related reading: Choosing 1099 Filing Ownership for Platform Contractor Payments.

4) Build a minimum evidence pack that survives audit and reconciliation#

Build one repeatable packet per payout. It should include both payment records and tax-admin context that another reviewer can follow without guessing.

Keep decision notes separate from underlying records. Internal notes help consistency, but they do not replace records. The core record set should include concrete payment evidence, for example receipts or bank-linked records, because HMRC guidance emphasizes keeping records so a return can be completed correctly. When records, status notes, and reviewer decisions are split across tools or inboxes, reconciliation risk rises quickly because someone later has to reconstruct what happened.

A practical minimum packet to keep for each payout looks like this:

| Packet item | What it supports | Common failure if missing |

|---|---|---|

| Payment record (receipt, bank-linked evidence, or ledger-linked transaction record) | Confirms what was paid and provides retainable evidence | A decision exists, but cannot be tied back to the actual payout |

| UK tax-admin status note (registering for Self Assessment, already registered, or reactivation needed) | Clarifies the payee's filing-admin path | Team assumes readiness when registration or reactivation is still pending |

| Date checkpoint note (for the stated HMRC scenario: tax year 6 April 2024 to 5 April 2025, notify by 5 October 2025, pay by 31 January) | Anchors timeline-sensitive follow-up | Timeline discussions stay vague and become hard to verify |

| Exception note for unclear status or filing route | Captures uncertainty and next action | Ambiguous cases get forced into a clean decision without escalation |

That packet does not turn UK filing administration into the legal basis for U.S. withholding. It does something narrower and more useful: it preserves the context that affects timing, follow-up, and review discipline, while keeping that context separate from the actual withholding decision.

Log known failure modes explicitly in the same packet. Note that filing without reactivating an existing account can delay a return, and that some cases require commercial software or other forms when standard online filing is unavailable. If a payee is unsure whether they are trading, note that uncertainty and route it to your exception path rather than closing the case as if status were settled.

This packet also gives you a practical reconciliation advantage. If a payout later needs to be reviewed, do not leave one team holding the contract excerpt, another team holding the bank evidence, and a third team holding the reviewer note about treaty routing. You want the entire decision traceable from one place:

- what was paid

- what the payment was classified as

- what status and residence evidence were on file

- what authority and policy were used

- what reporting consequence was expected

- whether the file was approved or escalated

That is what survives real audit and reconciliation work. Not because it is fancy, but because it reduces ambiguity. A good evidence pack does not rely on institutional memory. It lets another reviewer follow the same path without filling in gaps.

If you already have most of this information but it lives across different systems, the fix is not to collect more information. It is to create one repeatable packet structure and require that every payout decision resolve into that structure before funds move.

For a step-by-step walkthrough, see How to Build a Global Tax Withholding Engine: W-8 W-9 and Treaty Rate Automation.

If you are converting this evidence-pack checklist into enforceable workflow rules, map each control to statuses, approvals, and audit events in Gruv Docs.

5) Escalate edge cases early instead of forcing deterministic automation#

When core facts conflict, escalate early instead of forcing automation to produce a clean answer from an incomplete file. This matters most when residency, source-of-income facts, or treaty support are unclear. The tradeoff is a larger manual queue, but it cuts the risk of miswithholding and weak audit support.

Use the payout evidence packet from the prior section as the escalation checkpoint. If the packet shows unresolved facts, missing support, or conflicting signals, that should trigger review before release.

1) Conflicting residency signals#

Escalate when residency signals conflict for the same period. A single profile field is not enough when other records point elsewhere, because residency can be fact-and-circumstance based rather than determined by one input.

If a file includes a UK residency claim but also shows unresolved California ties or a disputed relocation window, route it to review. In the exception note, record the exact conflict, the period in dispute, and the named resolver before release.

The key here is not to settle the conflict by choosing whichever field is easiest for the system to read. If the evidence packet shows two different stories for the same period, your process should acknowledge that directly and stop auto-release.

2) Unclear U.S.-sourced income status#

Escalate when you cannot clearly support where services were performed. California guidance is explicit that services physically performed in California can create California-source income. So mixed-location work should not be auto-classified as fully outside the United States without support.

Use allocation evidence as a practical checkpoint:

CA Workdays / Total Workdays = % Ratio% Ratio x Total Income = CA Sourced Income

If workday support is missing, inconsistent, or not tied to the payment period, escalate.

This is a good example of why source should not be inferred from profile details. Source depends on case facts. If the file does not support those facts, then the file is not ready for a deterministic outcome.

3) Missing treaty support for a proposed reduced-treatment decision#

Escalate when proposed treaty treatment is not backed by a clear document reference in the file, including cases labeled with Treaty Article 7. Missing citation does not, by itself, decide the legal outcome, but it does mean the file is not ready for release.

Flag the missing support in the packet, log the disputed point, and require a named reviewer to attach the document reference before final decision.

Keep the trigger set narrow enough to use#

Escalation works only if the trigger set stays short enough that teams actually follow it. You do not need a giant exception catalog to get value from this control. You need a small set of mandatory triggers that reflect the real failure points already identified in the process:

- residency signals conflict for the same period

- source-of-income facts are unclear or unsupported

- treaty support is missing for a reduced-treatment decision

- the evidence packet is incomplete

- the reporting consequence for Forms 1042 and 1042-S is still unclear

Once one of those triggers appears, the system should stop pretending the file is clean. Assign a named reviewer, record the unresolved point, and hold the release path until the issue is closed. That is slower than forcing a deterministic result. It is also more defensible.

6) Configure policy gates in payouts so treaty logic is enforceable#

Policy is not enough if the payout flow can bypass it. Configure policy gates in the payout process so treaty logic is enforceable, not merely documented.

| Gate | Trigger | System result |

|---|---|---|

| Authority gate | The file is missing the exact official U.S. source or the internal policy language mapped to it | No withholding exemption decision moves forward |

| Classification gate | The payment is not classified from the contract and payout context | No treaty routing occurs |

| Source gate | U.S.-sourced income status is marked unresolved | No reduced-treatment decision occurs |

| Evidence-completeness gate | Payee identity, residence evidence, treaty basis note, and expected Forms 1042 and 1042-S treatment are not complete in one file | No treaty relief is applied |

| Escalation gate | Residency signals conflict, source facts are unclear, or treaty support is missing | The payout routes to hold-for-review rather than auto-release |

The easiest way to think about this is to turn the earlier controls into release conditions. If a payout can move forward without satisfying those conditions, then your policy is advisory rather than operational.

A workable gate sequence follows the order already established:

- Authority gate

No withholding exemption decision moves forward unless the file includes the exact official U.S. source and the internal policy language mapped to it.

- Classification gate

No treaty routing occurs until the payment is classified from the contract and payout context.

- Source gate

Do not make a reduced-treatment decision if your team marks U.S.-sourced income status as unresolved.

- Evidence-completeness gate

Do not apply treaty relief until payee identity, residence evidence, treaty basis note, and expected Forms 1042 and 1042-S treatment are complete in one file.

- Escalation gate

If residency signals conflict, source facts are unclear, or treaty support is missing, the payout routes to hold-for-review rather than auto-release.

That is what "enforceable" looks like in practice. The control does not depend on a reviewer remembering to be careful every time. It depends on the payout state itself.

A good configuration also keeps default paths explicit. Earlier sections already point to baseline withholding or hold-for-review as examples of the default path when classification or eligibility is unclear. Keep that same discipline in the payout system. The safest automation is often not an automated exemption. It is an automated stop.

A few implementation habits make the gate structure stronger without adding new legal complexity:

- store the classification, documentation status, and withholding outcome against the transaction record

- require the reviewer decision to be visible in the same chain as the payout record

- prevent Article 7 selection before the first classification fields are complete

- require the expected Forms 1042 and 1042-S treatment to be stated before final approval

Those steps are not about making the interface nicer. They are about making the decision traceable. If another reviewer cannot tell why the payout was released, the gate design is too weak.

This is the right place to separate payee administration from withholding logic. UK Self Assessment notes, UTR status, reactivation issues, and HMRC date checkpoints can live in the file because they help with context and follow-up. But they should not unlock treaty relief on their own. The release gate should remain tied to authority, classification, source, evidence completeness, and reporting consequence.

If your team wants more automation, use gates first. Automation that respects hold points is usually safer than automation that tries to infer a clean answer from messy facts.

We covered this in detail in IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

7) Pick a control model with explicit tradeoffs before scaling to new corridors#

Pick a control model deliberately instead of drifting into one.

For US-UK payouts, the draft record already shows the core tradeoffs. Stricter front-end controls mean slower setup. Manual review queues may get larger. More files may pause at hold-for-review. But those costs buy something specific: a defensible record, clearer reporting treatment, and fewer reversals when someone later asks how the withholding decision was made.

At a minimum, your model should answer three operational questions:

- what happens when classification is unclear

- what happens when evidence is incomplete

- what happens when treaty support is missing

If the answer to any of those is effectively "the system releases anyway," then you do not have a defensible model yet.

A practical way to choose among control approaches is to decide how much uncertainty you are willing to let automation absorb.

Review-first model#

In a review-first model, files move to a reviewer whenever your team still has unresolved authority, classification, source, or evidence-completeness questions. The advantage is stronger decision quality and a cleaner audit trail. The cost is a larger manual queue and slower payout operations.

Rules-with-hard-stops model#

In a rules-with-hard-stops model, automation does the routing, but only within a narrow set of clean cases. If your team has not classified the payment, if someone selects Article 7 too early, if the evidence file is incomplete, or if the reporting consequence is not clear, the system blocks release. The advantage is consistency. The cost is that you have to invest in gate design before scale.

Faster-flow model with default fallback#

Where teams prioritize speed, the only defensible version is one that still falls back to baseline withholding or hold-for-review when the file is unclear. The advantage is a smoother path for straightforward cases. The cost is that teams must resist broadening the "straightforward" category until it silently absorbs edge cases.

The important thing is to choose the tradeoff explicitly, especially before scaling to new corridors. If your US-UK process already depends on country labels, incomplete files, or summary materials treated as authority, adding more corridors will multiply the same weaknesses. If your US-UK process instead relies on a clear order of operations, an evidence pack, narrow escalation triggers, and enforceable payout gates, you have a stronger base before adding more corridors.

If your US-UK flow still has edge-case exceptions after baseline controls, validate rollout scope and policy-gate design with Gruv.

Frequently Asked Questions

What is the first control in a US-UK treaty withholding review?

Start with payment classification and source before you consider treaty relief. Your team should confirm what is being paid, whether the payment is U.S. sourced, and whether the supporting documentation is complete before any reduced-withholding decision moves forward.

Can we apply Treaty Article 7 as soon as a contractor says they are in the UK?

No. A UK residence claim alone does not complete the control chain. Your file still needs a payment-type classification, source support, and a documented basis for the proposed treatment before you let the payout move past review.

What evidence should sit in the file before reduced withholding is approved?

Keep one packet that shows the payment classification, residence evidence, authority reference, reviewer decision, and expected Forms 1042 and 1042-S handling. If those items are scattered across systems or still incomplete, your team should hold the release path.

When should a payout route to manual review instead of auto-release?

Route the case to review when residency signals conflict, U.S.-source facts are unclear, the evidence packet is incomplete, or treaty support is missing. In those cases, a clean automated answer is usually less defensible than a documented hold-for-review decision.

Do HMRC self-assessment records decide our U.S. withholding outcome?

No. They can help with follow-up context, but they do not replace the U.S. withholding controls in your payout process. Keep payee-administration items in the file, but do not let them unlock treaty relief on their own.

How should you configure the default path when the file is incomplete?

Use baseline withholding or hold-for-review as the default path when authority, classification, source status, or evidence completeness is unresolved. If you want more automation, build gates that stop release instead of asking the system to infer a clean answer from messy facts.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

US-Germany Treaty Withholding Decisions for Contractor Platform Payouts

For U.S.-Germany contractor payouts, the safest starting point is simple: do not force a single withholding answer when payment characterization or treaty access is unclear. The hard part is usually not finding treaty text. It is deciding what your team can defend before funds move in a platform-mediated payout.

US-India Contractor Payment Withholding Decisions for Platforms

US-India withholding failures often start with misclassification, not rate selection. When contractor services, royalties, and fees for included services are treated as interchangeable, the payout file can carry the wrong payment character before anyone applies a rate.

Non-Resident Withholding on Contractor Payments: Platform Guide to the 30% Rule and Treaty Reductions

Start with the default. If a payment is in scope for NRA withholding and you cannot support reduced treatment, withhold 30% and escalate unresolved cases before release.