Quick Answer

Prioritize intake classification, document validation, and controlled release gates in that order to reduce withholding errors in US-India flows. Treat W-8BEN or W-8BEN-E quality as a pre-release condition, use a deterministic rule table for withhold versus reduced versus escalate outcomes, and hold payouts when payment character is unclear or file data conflicts across contract, onboarding, and payout records.

How platforms should approach US-India withholding decisions#

US-India withholding failures often start with misclassification, not rate selection. When contractor services, royalties, and fees for included services are treated as interchangeable, the payout file can carry the wrong payment character before anyone applies a rate.

That matters because the withholding obligation sits with the payer, including resident or non-resident payers, when specified payments are credited or paid. Before money moves, the practical question is simple: what are you paying for, what in the file supports that label, and what happens when the facts are incomplete or contradictory?

This article ranks eight controls to put in place before payout. It is for compliance, legal, finance, and risk teams that need a workable order of operations under the US-India Income Tax Treaty and shifting domestic-rule conditions: classify the payment, validate documentation, choose a withholding path, and stop payments that need review.

Start with one checkpoint that is easy to test and costly to miss: a valid W-8BEN. In the platform excerpt used here, a missing valid W-8BEN can lead to 24% backup withholding or up to 30% on certain income, so reduced withholding should never rest on incomplete paperwork.

Capture sourcing and rights facts at intake, not after a payout exception. The same excerpt notes that services performed entirely in India are foreign source, and the India summary also states that royalty includes consideration for use of, or right to use, computer software. Those facts can change whether a payment stays in the standard flow or moves to escalation.

Finally, treat rules and thresholds as moving parts, not a one-time configuration. PwC notes Finance Act 2025 threshold amendments effective 1 April 2025, and its tables show category-specific threshold and withholding differences. Your controls need upkeep as the rules change, not a single hard-coded build.

You might also find this useful: Non-Resident Withholding on Contractor Payments: Platform Guide to the 30% Rule and Treaty Reductions.

Choose controls by risk exposure, not by feature volume#

Set your minimum controls by exposure first, especially where residency and source-income errors create filing and tax risk.

If you are deciding where to invest first, start with intake evidence, not automation breadth. Residency is a facts-and-circumstances determination, part-year residents are taxed on worldwide income during resident periods, and nonresidents are taxed on California-source income. For service payments, treat physical work location as a key signal, because services physically performed in California create California-source income exposure.

Apply that same discipline here: get the source facts right before you rely on downstream logic. Prioritize controls in this order: capture residency and source facts, apply a repeatable sourcing method (for example, CA Workdays / Total Workdays = % Ratio, then % Ratio x Total Income = CA Sourced Income), and route required California-source compensation to the Form 540NR filing path. Keep an escalation lane for borderline cases, since FTB does not issue written residency opinions for specific periods.

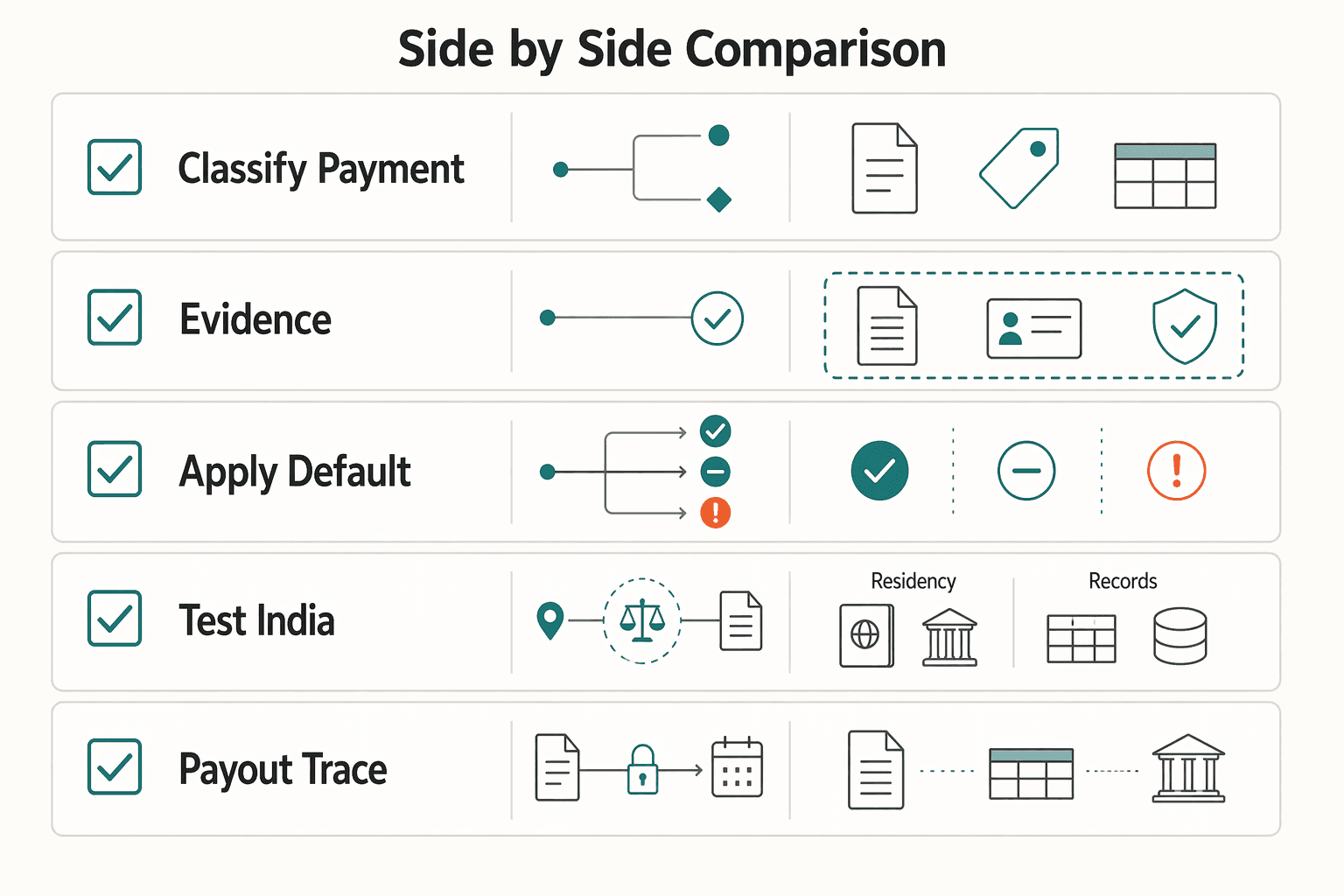

Compare the eight controls before implementation#

Compare the controls before implementation so you can see which one blocks a bad payout, which one creates audit evidence, and which one surfaces only after reporting breaks.

For a US-India payment flow, anchor the comparison to the IRS checkpoints in Publication 515: Identifying the Payee, Determination of amount to withhold, When to withhold, and Forms 1042 and 1042-S Reporting Obligations. Keep treaty interpretation under Article 12 and Article 15 separate from the execution controls the withholding agent can enforce.

Side by side comparison#

| Control | Best for | Required evidence | Blocker condition | Escalation trigger |

|---|---|---|---|---|

| 1) Classify payment character at intake | Platforms paying for services, licenses, content use, or mixed invoices | Contract extract, statement of work, invoice line detail, product metadata showing what was sold or licensed | Payment character is too unclear to choose a treatment path | Facts could fit both Article 12 and Article 15, or one line item mixes services and IP rights |

| 2) Validate treaty-claim documentation before payout release | Teams relying on a treaty position and document-based onboarding | Tax documentation on file, payee name and country data, onboarding profile, internal treaty-claim checklist | Missing file, stale file, or mismatch between tax form and onboarding data | Residency or payee identity is unclear, or the form conflicts with the contract counterparty |

| 3) Apply a default-and-override withholding decision tree | High-volume payout operations that need consistent withholding tax (WHT) outcomes | Decision table, rule version, case log with chosen branch, override reason if manual | No deterministic branch exists for the fact pattern | Manual override is requested because classification, documentation, or amount-to-withhold logic does not fit the table |

| 4) Test India domestic rules against treaty position before final rate lock | Teams with India-side tax exposure or nonresident digital revenue steps | India-side tax memo or issue note, treaty position summary, transaction facts, local-law review flag | India-side position is not assessed before payout release | Nonresident digital-services pattern appears, or local-law and treaty assumptions point in different directions |

| 5) Gate payout execution with approvals and traceable events | Ops teams that need hard release controls, not policy stored in slides | Approval record, timestamped system event, release log, batch ID tied to case | Classification, document check, or rate approval is incomplete | Manual release is requested outside the normal approval path |

| 6) Build an exception lane for mixed contracts and late corrections | Marketplaces with contract amendments, recoding, or disputed withholding outcomes | Exception ticket, legal or tax notes, revised coding, correction approval, payout hold reason | Exception handling is happening in email or chat with no case record | Retroactive reclassification, post-invoice amendment, or partner dispute on withholding |

| 7) Keep an audit file that survives regulator and partner scrutiny | Teams that need to defend decisions months later | Contract extract, classification memo, tax form, decision record, payout trace, reconciliation export, reporting mapping | File is too incomplete to reconstruct who decided what and when | Broken link between payout, withholding decision, and Forms 1042 or 1042-S reporting |

| 8) Run quarterly governance checks and treaty-change monitoring | Leaders trying to catch drift before it becomes a batch issue | Quarterly attestation, control testing notes, change log, repeat-exception report, legal refresh log | Controls run on stale assumptions with no review trail | Repeated overrides, rising exception volume, or a treaty/local-guidance change affects a decision branch |

What matters most in practice#

Control 1 is the origin point. If intake classification is wrong, later controls can look clean while still producing the wrong outcome. A practical checkpoint is whether the contract separates license or use rights from service delivery. If that boundary is blurred into one line item, pause before rate logic.

Controls 2 and 3 are where teams often overtrust paperwork. A tax form on file is not, by itself, a payout decision. Confirm that the tax form payee, contract counterparty, and platform account all align to the same person or entity.

Use the grid to phase implementation#

If you are the withholding agent, treat Controls 1, 2, 3, and 5 as phase-one release gates because they map most directly to payee identification, withholding amount, and withholding timing. Controls 6, 7, and 8 are durability controls for exceptions, evidence retention, and drift detection.

Control 4 needs a dedicated escalation lane. USTR describes India's Digital Services Tax as a 2% revenue-based tax on specified digital services that applies to non-residents, and notes compliance-cost and double-taxation risk. That does not make DST a withholding rate for contractor payments, but it is a clear reason to flag India-specific nonresident digital fact patterns for specialist review instead of forcing them through a generic payout rule.

Use this table to assign ownership, define blocker conditions, and set required evidence before money moves. Borderline legal interpretation issues should go to escalation, not get resolved informally in operations.

For a step-by-step walkthrough, see IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments.

Turn this comparison into an execution checklist by mapping each control to approval gates and release states in Gruv Payouts.

1) Classify payment character at intake before any rate logic#

Classify payment character before any withholding-rate logic, or a clean-looking file can still produce the wrong payout outcome.

For a withholding agent, that sequence aligns with IRS Publication 515: Identifying the Payee, then Determination of amount to withhold, then When to withhold. In a US-India flow, this control keeps different payment categories on separate tracks early instead of asking payout rules to infer intent from vague invoice text.

What good intake needs#

You do not need a full treaty memo at onboarding, but you do need structured facts that prevent obvious miscoding:

- contract extract showing what was sold, licensed, or delivered

- statement of work or order form when services are involved

- invoice line detail, not only a gross total

- product or platform metadata showing whether the payment is for service delivery, use rights, or both

- payee and counterparty identity details tied to the payout account

Free-text labels like "consulting," "creator payout," or "platform fee" are usually too broad when the same platform also pays for content use, software access, or monetization rights.

Operator rule for mixed facts#

If a contract includes both license or use rights and services, do not force one undifferentiated category just to keep the batch moving. Split line items at intake when the documents already separate them. If the contract and invoice are blended, route the case to legal or tax review before release.

If facts are mixed, pause automation. This is an operational control, not a treaty conclusion.

Checks before advancing the case#

Before amount-to-withhold logic runs, confirm:

- a second reviewer can explain, from the contract extract plus invoice lines, what was bought or licensed

- the contract payee, receiving platform account, and onboarding profile point to the same person or entity

This step also protects downstream reporting. Publication 515 separately flags Forms 1042 and 1042-S Reporting Obligations and Form 1099 reporting and backup withholding, so early miscoding can show up later as reporting or reconciliation issues.

Tradeoff#

The cost is tighter intake design, better document linking, and more QA, with more cases stopped for review. The benefit is avoiding harder post-release reclassification work.

Where India-related nonresident digital revenue facts appear, early flagging is especially important. USTR states India's Digital Services Tax applies to non-residents, imposes a 2% tax on revenue from a broad range of digital services offered in India, and notes compliance-cost and double-taxation risk for affected companies. That does not determine payment character here, but it is a practical reason not to bury these cases under a generic "services" label.

2) Validate treaty-claim documentation before payout release#

Do not release a treaty-reduced payout unless the file supports the claim from start to finish. For a withholding agent, this is a pre-release control, not post-payment cleanup.

Treat the treaty-document set as a release condition: collect the applicable W-8 form (for example, W-8BEN or W-8BEN-E), confirm payee identity across contract, onboarding, and payout records, and document the treaty-eligibility review point before rate lock. Publication 515 helps here because Identifying the Payee comes before withholding decisions, and weak documentation creates downstream Forms 1042 and 1042-S Reporting Obligations risk.

| Checkpoint | Verify before release | Blocker condition |

|---|---|---|

| Payee identity | Contract payee, onboarding profile, and receiving account match | Name/entity mismatch or unclear payee record |

| Treaty form | Applicable W-8 form is on file and tied to the same payee record | Missing form, wrong form, or form linked to another profile |

| Residency consistency | Residency details align across tax form and case file | Conflicting residency data |

| Reporting readiness | File can support 1042/1042-S treatment | Missing source documents or no traceable decision basis |

| India domestic inputs | Payment category + recipient/year aggregation fields captured | One uniform threshold rule used across different categories |

Apply a clear hold rule: if there is no usable W-8 form for the claim or the residency data conflicts, route the case to the default withholding path until file quality is fixed. This adds onboarding friction and can delay payouts, but it prevents unsupported treaty outcomes.

Capture India-side domestic-law inputs before release where relevant. The cited India notes indicate withholding obligations can apply when specified payments are credited and/or paid, thresholds are aggregated by recipient and tax year, and categories use different threshold limits. The same notes show category-specific entries such as INR 50,000 and 10% (professional service), INR 50,000 and 2% (technical service), INR 50,000 and 10% (royalty), and 0.1% (certain e-commerce participant payments via digital platform), with amendments effective 1 April 2025. Do not universalize those figures across all non-resident cases. Use them to trigger the right domestic-law check and escalation path.

Related: US-Germany Tax Treaty and Contractor Payments: Withholding Rates and Platform Obligations.

3) Apply a default-and-override withholding decision tree#

Use a strict default: if required documentation is incomplete, withhold. Allow reduced withholding only through a documented override path. This keeps decisions consistent and defensible across treaty-claim and backup-withholding scenarios.

A withholding agent should get the same output for the same file state every time, with a decision log that explains why a payout was released at a reduced rate or held at default withholding.

Make the baseline strict and machine-readable#

If the payee is foreign and no valid W-8 is on file, route to default withholding. In the source materials used here, that means a flat 30% default withholding.

Keep form handling precise:

- W-8BEN for individuals; W-8BEN-E for entities

- forms are provided to the withholding agent, not filed with the IRS

- your internal file must show the signed form, payee linkage, and final withholding decision basis

| Input state | Minimum evidence on file | Output | Why |

|---|---|---|---|

| Foreign payee, no valid W-8BEN/W-8BEN-E | Basic payee setup only | Withhold | Default 30% branch for missing W-8 documentation |

| Valid W-8, identity match, treaty claim appears supportable | Signed W-8, matching payee record, complete tax profile | Reduced | Reduced treatment can be considered only after complete documentation and eligibility review |

| Valid W-8, but identity/residency/beneficial-owner/payment-character conflict | Conflicting onboarding/contract/payout records | Escalate | Prevent unsupported treaty treatment on ambiguous files |

| Backup withholding indicators present | Reporting indicators | Escalate or separate branch | Publication 515 treats backup withholding as a distinct decision area |

Publication 515 separately lists "Form 1099 reporting and backup withholding" and "Forms 1042 and 1042-S Reporting Obligations." Keep those tracks distinct in the tree.

Treat treaty relief as an override, not an automatic result#

A signed W-8 is a core checkpoint for claiming treaty benefits, but it is not automatic entitlement to reduced withholding. Sources note possible reduced outcomes like 10% or even 0% in some scenarios. Do not hard-code those rates across all payment types.

Open the reduced branch only after key fields align, for example payee name, form type, country claim, and contract party, and a validity check passes. Source phrasing differs on validity, "three years from the date of signing" versus "3 calendar years from the date of signing," so include a renewal checkpoint and force re-review before expiry.

Keep a controlled manual override lane#

A rigid tree needs a clean stop point. Route to escalate when the file is reviewable but not clean enough for auto-routing, including:

- W-8 present but linked to the wrong profile

- identity, residency, or beneficial-owner details conflict across records

- payment characterization is unresolved for treaty analysis

- backup withholding or 1042/1042-S treatment is unclear

Log override decisions with Publication 515-style checkpoints: determination of amount to withhold and when to withhold. Keep the first version narrow with three outputs only: withhold, reduced, escalate.

We covered this in detail in How to Build a Global Tax Withholding Engine: W-8 W-9 and Treaty Rate Automation.

4) Test India domestic rules against treaty position before final rate lock#

Do not lock a reduced rate until your India domestic-law view and treaty view are tested side by side for the same payment. If they do not align, route the file to tax counsel before release as an internal control.

A treaty can allocate and limit taxing rights, but the practical outcome still depends on how treaty provisions compare with each country's domestic law. Treaty analysis is necessary, but not sufficient on its own.

- Write the treaty position first.

Define the payment characterization, the facts supporting it, and the documents those facts come from.

- Write the India domestic-law position separately.

Keep it distinct from treaty reasoning so a reviewer can clearly see whether characterization, scope, or source treatment matches or conflicts. If key India-side withholding details are not established in the materials in scope, mark them as unknown and escalate.

- Check expected double-tax relief before final approval.

Where relevant, confirm whether relief in the residence country is expected through a credit or an exemption, and record that expected path.

If treaty and domestic positions diverge, pause the rate lock, attach both analyses, and require counsel sign-off before payout release. This adds friction to close cycles, but it reduces the risk of operationalizing a rate that is supportable under only one side of the analysis.

5) Gate payout execution with approvals and traceable system events#

Treat payout release as a control decision, not an ops shortcut. Execution should stay blocked until required statuses are true in system state and the checks are traceable. In Gruv Payouts, that means keeping batch execution blocked until required compliance and documentation statuses are recorded as satisfied.

The benefit is enforceability. If a decision lives only in tickets, chat, or email, it can be bypassed under deadline pressure. A release gate turns that decision into a required step before money can move.

Make the stop/proceed logic explicit#

Use a simple sequence: blocker raised, verification performed, then proceed allowed. A historical formal-record pattern shows the logic clearly: a quorum concern was raised, roll call verified participation, and only then did proceedings continue. That does not establish US-India tax-control specifics; it simply shows the value of explicit stop/proceed states.

For payout batches, ask:

- Was a blocker raised?

If any required status is missing or pending, the batch should enter a hard-stop state.

- Was the blocker formally verified?

Record a verification event against current records, not memory.

- Was proceed status earned?

Only enable execution after all required statuses are confirmed as satisfied.

Record a sequence of events, not just a final green check#

Keep an audit trail that shows how release became valid:

- Blocker event

Capture why execution is blocked, plus batch ID, timestamp, and actor or service.

- Verification event

Capture which statuses were checked and their exact values at verification time.

- Release event

Capture who authorized release, when status changed, and which verification event the release relied on.

Machine-readable records are more durable than ad hoc notes in this flow. Structured event data with IDs, status values, and timestamps is easier to review and test later than scattered free text.

Related reading: How MoR Platforms Split Payments Between Platform and Contractor.

6) Build an exception lane for mixed contracts and late corrections#

Use a dedicated exception lane when a case cannot be resolved cleanly in the normal payout flow. For mixed contracts, retroactive recoding, and disputed outcomes, that lane should have explicit entry rules, evidence requirements, and re-release approval.

Define what belongs in the lane#

Keep criteria narrow so the lane does not become a backlog. Route cases into exceptions when they involve:

- Mixed contract character

Services and licensing or other rights are bundled, and existing coding no longer matches the documents on file.

- Late-breaking changes

An amendment, legal note, or dispute arrives after classification or withholding treatment was approved.

- Post-decision correction

You are revising a recorded decision that already affected payout, reporting, or both.

If a change would alter payment character, withholding treatment, or the stored decision rationale, route it to exceptions instead of editing in place.

Preserve the original decision before correcting it#

Do not overwrite the initial record. IRS Information Returns Processing guidance includes a dedicated correction procedure and a specific subsection on Invalid Correction Attempts (IRM 3.12.8.2.10), which is a useful operational model: not every attempted fix is a valid correction.

Keep a case file with the original classification, original approval event, triggering document, proposed revised coding, and why the first decision is no longer reliable. If tax or legal provides input, store it in the case record.

Make re-release stricter than first release#

A corrected payout should generally have an explicit second approval tied to the correction case ID and the exact fields changed. Use machine-readable events with timestamps and actor or service identity.

Avoid correction patterns that can look resolved but are hard to verify later: cancel-and-reenter workarounds, free-text-only reasons, or rate changes without corresponding classification updates.

Keep one queue, split triage and resolution#

Use one exception queue, but separate intake from final resolution. Triage can confirm the case belongs in exceptions, validate triggering evidence, and pause further payout changes until review is complete. Resolution then assigns ownership and records the final corrective decision.

For a mixed service-and-licensing invoice, a clean flow is: auto-route to exceptions, attach the relevant contract or amendment, record review notes, store revised coding, and require re-release approval before funds move again.

7) Keep an audit file that survives regulator and partner scrutiny#

Your file is audit-ready only if a reviewer can reconstruct one payment from facts to withholding outcome to cash movement without guesswork.

- Anchor the file to the payment's actual character.

Keep the underlying description, supporting evidence, and internal classification rationale together so the reasoning is visible, not just the final code. For India-related analysis, make sure the description and evidence support the conclusion, including any "make available" analysis when relevant.

- Freeze the decision-day record, not just the latest record.

If your reasoning references treaty positions, retain the exact memo and supporting onboarding and approval records used at release, with version history. Keep any conflict-resolution follow-up with that same snapshot.

- Keep identifiers, approvals, and payout traces in structured fields.

A strong case file links reasoning to execution through decision records, approver identity, payment trace, and reconciliation details for the exact release. Where present in your records, preserve tax identifiers as distinct fields, for example an I.R.S. Employer Identification Number, so review does not depend on screenshots or email threads.

- Add a consistency check across related tax positions.

Before closing the file, confirm the withholding position does not conflict with related TP, PE, or GST fact patterns documented elsewhere. A short consistency note is usually enough to show that linked positions were reviewed and aligned, especially when relief depends on documented conditions.

Keep one owner accountable for file completeness after payout. If core artifacts for description, evidence, decision records, identifiers, and payment execution cannot be produced quickly, the control is not complete.

8) Run quarterly governance checks and treaty-change monitoring#

Use a recurring governance check to keep withholding decisions aligned with current guidance instead of stale assumptions. The practical win is fewer surprises, but only if ownership and review cadence are explicit.

What to check each quarter#

Focus on whether your current decision branches still match how payouts are actually handled.

- Review IRS Publication 515 sections

Future Developments,What's New, andForms 1042 and 1042-S Reporting Obligations; if anything changed, log the branch, form, or reporting output that needs an update. - Confirm sampled payments still have a complete internal evidence pack (for example, contract extracts, classification notes, W-8BEN, decision records, payout traces, and reconciliation outputs).

- Verify the withholding outcome and 1042/1042-S reporting treatment still match the stored decision record for each sampled branch.

What to refresh annually#

Run a legal and control refresh across withholding decision branches, mapped to the exact branch labels your operations team uses. Keep tax and sanctions monitoring as separate checks: OFAC states prohibitions vary by program, and an OFAC FAQ update date, for example August 21, 2024, is a sanctions recency signal, not a treaty-update signal.

Escalation triggers that should pause payout#

Pause payout when the compliance position is unresolved in the file, not merely uncertain. For United States-to-India flows, unresolved treaty assumptions should trigger a hold. The compliance-default examples below come from press-release material, so use them as risk signals and corroborate before locking policy.

Ambiguous payment character#

Stop when the contract, invoice, and product facts do not support one consistent treatment. If those records can reasonably support more than one path, do not let batch operations guess.

Use a simple control: if your process includes a contract extract, decision memo, and invoice coding, they should align. If they do not, route the case out of normal processing.

Unclear treaty-claim file#

Pause when the claim depends on documents or statements that do not line up. You do not need a long memo for every payout, but you do need one coherent and defensible record.

As a practical check, the claim record, decision record, filing/payment status, and payout trace should tell the same story. If core signals conflict, treat that as a stop signal, not a later cleanup item.

Treaty and domestic results point in different directions#

Pause when competing analyses lead to different practical outcomes and the file does not document why one position controls. If the case record shows competing answers, escalation is safer than choosing the operationally convenient one.

Also force review when ongoing compliance is not current. Monthly payments alone may be insufficient, and even a single missed return or unpaid current-year balance can create default risk; once defaulted, collection activity can resume quickly. If release logic also depends on stale assumptions while cross-border tax rules are shifting, hold for review.

Conclusion#

The practical close is sequence, not guesswork: classify first, validate the rule path, then release only with traceable approval.

- Classify the payment before setting any rate.

Use the contract and invoice together to identify what the payment is. That first call matters because India withholding obligations sit with the payer when specified payments are credited or paid, and threshold checks can depend on the total paid to one person in a tax year. For platform teams, rights language is a key intake check: the cited India context states that royalty includes consideration for use of, or right to use, computer software.

- Validate the decision path and keep it auditable.

A rate by itself is not a control. As an internal control, document the facts, the classification, and the approval path. India's withholding table explicitly includes payments to e-commerce participants through digital platforms, with a rate-column value shown as 0.1, so platform payouts should not automatically be handled as a single generic contractor bucket. If the classification path does not lead to a clear operational result, pause and escalate.

- Keep the model practical and refresh it on a fixed cadence.

Automate clean, repeatable cases and reserve specialist review for ambiguous or mixed fact patterns. Then review rule logic on a schedule so controls do not go stale when statutes change. One example is a threshold amendment to INR 50,000 effective 1 April 2025, which is exactly the kind of change that can break an otherwise stable workflow.

Before rollout, validate your classification, document, and escalation workflow against the integration and control patterns in the Gruv docs.

Frequently Asked Questions

What should a platform do first for US-India withholding compliance?

Start with classification at intake before requesting treaty forms or setting a rate. Confirm worker-status and payment-character facts early, because withholding decisions depend on that sequence. If the contract and invoice do not support one clear payment character, pause release instead of letting operations guess.

Does `W-8BEN` automatically reduce withholding for every payout type?

No. W-8BEN and W-8BEN-E support foreign-status and treaty claims, but they do not automatically reduce withholding across all income types. One operational source says services performed entirely in India with a valid W-8BEN usually move to zero withholding, which is conditional rather than universal. These forms are provided to the withholding agent, not filed directly with the IRS, and are stated to remain valid for 3 calendar years from signing.

How should we distinguish contractor services from royalties and fees for included services?

Use the contract and invoice as an initial screen for payment character. Bundled or unclear line items are a red flag because they can hide different treatment within one payout. The source documents here do not provide a complete legal test for treaty classification, so borderline cases should be split or escalated, not forced into a default bucket.

When does India domestic law override or conflict with treaty expectations in practice?

Treat this as a payout-control issue: do your India domestic-law and treaty analyses support the same operational result. If signals in the file point to different payment-character outcomes, do not finalize the rate. When domestic and treaty analyses diverge, escalate to tax counsel before release.

What evidence should sit in the file before approving payout release?

Keep one coherent case file with the signed W-8BEN or W-8BEN-E, contract extract, short classification memo, decision record, and payout trace. Verify that payee name, country, and beneficial-owner statements align across the form and vendor record, and confirm the form is within the stated 3 calendar year validity window. Secure form collection and strong record-keeping are core controls because a technically correct tax position does not erase penalties, back-taxes, or audits if the file cannot support it.

Which scenarios require escalation to tax counsel instead of operations review?

Escalate when the issue is legal interpretation, not missing admin data. That includes mixed or unclear contracts, conflicting residency or beneficial-owner signals, disputed payment character, or files where treaty and India domestic analyses point to different outcomes. Escalate no-documentation baseline disputes as well, since the non-authoritative excerpts conflict between 24% backup or up to 30% for some income and a flat 30%.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- acquisition.gov/far/part-52trusted

- congress.gov/crs-product/R45186trusted

- das.nebraska.gov/materiel/purchasing/contracts/pdfs/59912(o4)...trusted

- ftb.ca.gov/file/personal/residency-status/part-year-and...trusted

- ftb.ca.gov/forms/misc/1100.htmltrusted

- govinfo.gov/content/pkg/GPO-CRECB-1929-pt2-v71/pdf/GPO-C...trusted

- govinfo.gov/content/pkg/CRPT-113erpt7/html/CRPT-113erpt7...trusted

- irs.gov/publications/p515trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

US-UK Tax Treaty Withholding Controls for Contractor Payment Platforms

For US-UK contractor payouts, the main risk is usually not a lack of treaty awareness. Your team creates risk when it approves reduced or zero withholding before you confirm income source, payment type, and treaty-status documentation. A UK label on its own does not support the treatment.

US-Germany Treaty Withholding Decisions for Contractor Platform Payouts

For U.S.-Germany contractor payouts, the safest starting point is simple: do not force a single withholding answer when payment characterization or treaty access is unclear. The hard part is usually not finding treaty text. It is deciding what your team can defend before funds move in a platform-mediated payout.

Non-Resident Withholding on Contractor Payments: Platform Guide to the 30% Rule and Treaty Reductions

Start with the default. If a payment is in scope for NRA withholding and you cannot support reduced treatment, withhold 30% and escalate unresolved cases before release.