Quick Answer

Start by classifying the payment type, assigning withholding ownership, and testing treaty access before funds move. In this corridor, the material does not support one universal contractor-service rate under the U.S.-Germany treaty, so unclear files should be paused and sent for specialist review. Use Article 14, Article 28 (LOB), and Article 29 as structured checkpoints, and keep documentation that links contract scope, approval, and final payout instruction.

How Platforms Should Assess US-Germany Treaty Withholding#

For U.S.-Germany contractor payouts, the safest starting point is simple: do not force a single withholding answer when payment characterization or treaty access is unclear. The hard part is usually not finding treaty text. It is deciding what your team can defend before funds move in a platform-mediated payout.

The treaty structure supports that caution. In the excerpted convention, contractor services appear separately under Article 14 (Independent Personal Services), while Article 28 covers Limitation on Benefits (LOB) and Article 29 covers Refund of Withholding Tax. In this material, there is no single contractor-service withholding rate shown that you can apply across all fact patterns. Treat those articles as intake checkpoints, not just references:

- classify the payment type before mapping withholding logic

- test treaty access under LOB instead of treating residency or entity status as a simple checkbox

- preserve a case record that can support a later refund path if withholding is disputed

Classification risk goes beyond rate selection. German contractor arrangements can trigger strict false self-employment (Scheinselbstständigkeit) scrutiny, so a defensible file should include contract terms and working-pattern indicators of independence, such as autonomous work arrangements and evidence of multiple clients. If those facts are missing or contradictory, escalate classification before payout release.

This article stays narrow by design: German withholding-tax decisions for contractor-linked payouts with incomplete or mixed intake facts. Where outcomes change by income type, entity form, or treaty eligibility, the goal is to mark the decision point, not force false precision.

Start with payment type before you discuss rates#

Classify the payment first. Until you do that, any rate discussion is not defensible. In this corridor, Independent contractor service payments need their own analysis, separate from Dividend withholding tax and Royalty withholding tax, even when the same payee appears in multiple payment flows.

IRS Publication 515 reflects that sequence by separating Identifying the Payee, Determination of amount to withhold, and When to withhold. For platform operations, start by confirming who is being paid and what is being paid for. Then map withholding treatment and any applicable treaty analysis.

Mixed contracts need extra discipline. Where a contract bundles services and IP rights, split the analysis before you apply any Treaty relief claim logic. Do not let one vendor label decide treatment for every line item.

Before you release payout, use a quick classification checkpoint:

- contract or statement of work

- invoice wording and line-item descriptions

- clauses that assign or license IP rights

If those inputs conflict, pause payout and escalate classification. That matters even more in Germany, where false self-employment, Scheinselbstständigkeit, is a known misclassification risk area with penalty exposure.

Before release, lock the payment-type decision into the case record. Keep, at minimum, a short classification note, reviewer, approval timestamp, and the source documents used. That will support later withholding reporting reviews, including Form 1042 and 1042-S contexts.

See IRS Form 1042-S for Platform Operators: How to Report and Withhold on Foreign Contractor Payments for a step-by-step walkthrough.

What current Germany-focused evidence does and does not answer#

Current Germany-focused evidence helps set boundaries, but it does not decide German WHT for contractor payouts on its own. It supports documentation process context and income-type separation. It does not provide a specific German withholding result for U.S.-Germany independent contractor services or clearly assign which platform party must withhold.

Treaty analysis can vary by income category, and solidarity surcharge appears in German tax context. For this operator use case, the sources still do not resolve contractor-service withholding treatment end to end.

| Income type | What current sources clearly cover | What remains unknown for operator execution under German WHT |

|---|---|---|

| Dividend withholding tax | Dividend-focused treaty commentary appears as a separate category, which supports category-by-category analysis. | Whether dividend treatment can be reused for contractor payouts, whether solidarity surcharge changes your contractor outcome, and who on-platform owns withholding execution. |

| Royalty withholding tax | Royalty-focused commentary is also separated from services, reinforcing the need to split IP-related lines from pure services before treaty analysis. | Treaty treatment in the provided material for mixed service-plus-IP payments, the exact German WHT result for platform payouts, and claim-handling steps for treaty relief. |

| Independent contractor service payments | The sources support high-level treaty and documentation context only: DTAs exist, and the IRS certification lane includes Form 8802, Processing Time Limits, and a Three-Year Procedure. | A specific German withholding rate for U.S.-Germany contractor services, Germany-side claim forms and timelines for this fact pattern, and exact platform withholding obligations across payer, marketplace, and managed payout models. |

| Do not assume | Dividend- or royalty-focused treaty commentary is not an automatic proxy for contractor-service payouts. | Any contractor-service rate, exemption, or filing step that is not directly supported by payment-type-specific source text. |

The IRS material is a U.S. certification process for reduced treaty rates, not a Germany contractor-withholding rate table. If Form 8802 is the only support in the file, the withholding decision is still open until payment-type-specific, country-specific treatment support is documented.

Apply the same filter to adjacent Germany tax commentary. Corporate tax updates, including references to below 25% by 2032 and local trade-tax variability, are not operational withholding instructions for contractor payouts. They also do not assign payer-versus-platform responsibility.

The practical risk is false confidence from adjacent sources. If your support is only a general treaty reference, a residency certification document, or dividend or royalty commentary, do not force a contractor-service WHT result. Route it for specialist review until you have payment-type-specific authority and a documented withholding owner.

If you want a deeper dive, read US-UK Tax Treaty and Contractor Payments: What Platforms Should Know About Withholding.

Why dividend treaty outcomes cannot be copied into contractor payout logic#

Do not reuse a dividend outcome for a contractor payout. Dividend authorities may be useful background, but once the payment is a service fee, the legal category changes and dividend logic stops being a direct withholding answer.

Entity characterization changes the framing, not the service-fee result#

Entity characterization can change how you frame the analysis and what documents you collect. It does not, by itself, resolve whether a cross-border service fee triggers withholding, at what rate, or who in the payment chain is responsible.

Form 8802 marks the same boundary. It is used for U.S. residency certification, but it does not convert a service payment into a dividend case or supply a contractor-service withholding result on its own.

Dividend-fund fact patterns are structurally different#

The BFH matters here involve dividend withholding and nonresident fund fact patterns (French FCP and Luxembourg SICAV), not contractor payout fact patterns. Dividend settings turn on ownership and distribution rights. Contractor settings can turn on contract scope, invoice language, and payment characterization.

If your fact pattern is a contractor service payment, dividend or fund cases are context, not a reusable answer. Follow the payment characterization in the transaction, and escalate before analogizing from dividend outcomes.

BFH judgments are persuasive signals, but still fact-specific#

The BFH judgments published on 22 August 2024, I R 2/20 and I R 1/20, addressed dividend withholding for nonresident fund fact patterns, French FCP and Luxembourg SICAV. They support a dividend-discrimination analysis, not a general rule for contractor fees.

Those decisions also show why legal signals have to be matched to facts. The court held the withholding treatment discriminatory in that setting, but remanded to the lower tax court to determine exact refund and interest amounts. Even strong authority remained fact-specific at the amount level.

What to confirm before anyone borrows dividend logic#

Before anyone tries to analogize from dividend treatment, make sure the file supports a service-fee analysis on its own. At minimum, confirm the following:

- The contract and invoice describe services, not an equity distribution.

- The counterparty is acting as a vendor or contractor in this transaction, not as a shareholder or fund investor for this payment.

- The file includes payment-type classification support, not only residency support such as Form 8802.

When withholding is applied unlawfully, refund-plus-interest exposure can follow. For platform operations, if your support is dividend, fund, or shareholder authority and your payment is a contractor fee, escalate instead of analogizing.

Related: US-India Tax Treaty and Contractor Payments: Royalty and Fee Withholding for Platforms.

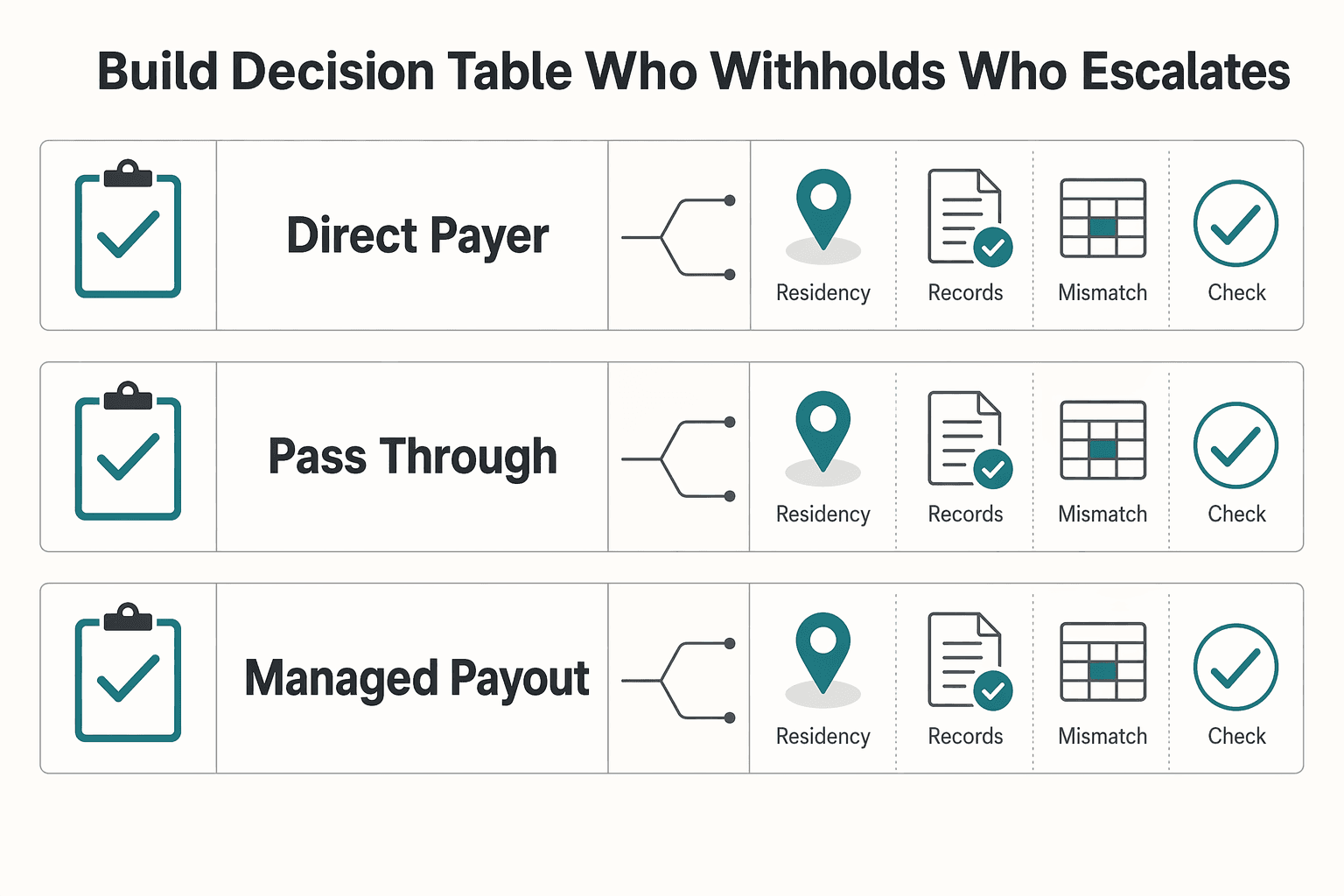

Build a decision table for who withholds and who escalates#

Once you classify a payment as a contractor service fee, decide ownership and escalation before you start debating rate outcomes. Do not hard-code one party as always responsible across models. Assign a starting owner, require minimum evidence, and keep an explicit unknown/needs counsel lane.

| Payout scenario | Starting point for withholding ownership review | Evidence required before release | If X, do Y | Main risks | Unknown or needs counsel |

|---|---|---|---|---|---|

| Direct payer model | Use the entity that signed the contractor agreement, books the expense, and instructs payment as the initial routing owner. If the platform is only software, treat it as a data collector first until withholding ownership is confirmed. | Payee tax profile, cross-border tax residency indicators, signed contract, invoice wording, payment classification note, and treaty-review flags (including LOB: needs review where relevant). | If contract or invoice language suggests IP rights, royalties, or mixed deliverables, pause auto-release and route to specialist review before any treaty-relief claim. | Under-withholding from misclassifying services; over-withholding from forcing service fees into a royalty bucket; payout delays from missing documentation. | Whether these facts create a German-source collection obligation, and whether treaty relief can be applied at source or only later. |

| Pass-through marketplace model | Start with the party legally in the supplier payment chain, then test marketplace contracts against the actual flow of funds. If the marketplace sets terms, touches funds, or appears on invoices, escalate to determine whether ownership shifts or splits. | Payee profile, onboarding tax forms, marketplace terms, vendor agreement, invoice path, residency support, LOB review flag, and a clear role map (merchant/agent/paymaster). | If legal documents do not match money flow, pause automated payout and escalate before assigning withholding ownership. | Under-withholding from treating a marketplace as a pure intermediary when it operates deeper in the chain; over-withholding from duplicate controls; contractor friction from repeated document requests. | Whether the marketplace is only a facilitator or has a tax-collection role in this corridor and program design. |

| Managed payout model | Start with the operator that controls fund release and payout rules, then verify what the contract actually delegates. Operational control is not the same as legal liability. | Payee file, funding and settlement agreements, managed payout terms, evidence of who approves tax treatment, residency indicators, contract scope, and treaty-review flags (including LOB review status). | If delegated tax logic exists but legal responsibility is unclear, hold payout and obtain legal or tax signoff before invoking treaty treatment. | Under-withholding if teams assume the payout provider owns the decision when it does not; over-withholding from blanket holds or deductions; support load because contractors see only the platform. | Exact liability allocation among platform, payout provider, and underlying payer in cross-border service flows. |

Use the table as a release gate, not a shortcut#

Use the table to assign who investigates first and who approves release once the file is complete. Keep payment classification and treaty eligibility in separate fields, because clean residency support does not fix unclear income characterization.

For a treaty-relief claim tied to U.S. residence, Form 8802 is a core residency-certification checkpoint. Mirror the IRS control posture in your own file: payment validation, clear responsibility, confirmation-number traceability, and a retained certification record.

What to verify before release#

Residency is not a single-box check. Confirm that legal name, address, tax form, invoice country, and residency support tell the same country story. If they conflict, hold payout and escalate.

Read contract scope and deliverables for characterization triggers, especially usage-rights, license, or bundled-rights language that can shift the analysis. If status or income type is unclear, do not automate payout.

Also screen for a separate risk track: Germany's false self-employment, Scheinselbstständigkeit, exposure. If the profile looks employee-like, escalate beyond treaty and withholding review.

Keep the unknown lane visible#

Keep an explicit unknown/needs counsel field and route those cases without forcing precision the record cannot support. A short payout delay is usually lower risk than under-withholding exposure, over-withholding disputes, and an audit file that cannot explain why funds were released.

If you want this decision table to map directly to payout states and approval gates, review how Gruv Payouts handles controlled release workflows.

Define the minimum evidence pack before funds move#

If the file cannot explain the payout decision from start to finish, do not release funds. Your minimum evidence pack should let a second reviewer trace the path from contract scope to withholding decision and final payout instruction without extra context.

What must be in the pre-payout file#

At minimum, keep these items in the pre-payout file:

| File item | What it should show |

|---|---|

| Signed contract or statement of work | Scope and any rights granted |

| Payment-classification memo | Chosen treatment or needs escalation |

| Treaty-position note | Whether treaty treatment was considered, relied on, rejected, or left open pending review |

| Payout instruction details | Payee, amount, invoice reference, and release approval |

In the classification memo, capture the facts that drove the decision so the rationale is reproducible.

Tax documents and downstream reporting flags#

Tax forms help, but they are not the whole answer. If your program collects tax forms (for example, W-8 or W-9), store the version used for that payment and tie it to the payee record as of the approval date. Treat those forms as inputs, not as a complete answer on treaty entitlement, reporting, or withholding ownership.

Where facts make it relevant, add tracked follow-up items for Form 8938 and FBAR (FinCEN Form 114) with a named owner. Keep these as case-specific downstream flags, not a blanket conclusion that the platform must file in every case. For Form 8938, keep the core guardrails explicit in the file notes:

- it is attached to the annual return and filed by that return's due date, including extensions

- filing Form 8938 does not remove any separate FinCEN Form 114 (FBAR) requirement

- for certain specified domestic entities, thresholds include

$50,000on the last day of the tax year or$75,000at any time during the year - some accounts are excluded, including accounts maintained by U.S. payers

- if no income tax return is required for the year, Form 8938 is not required

Approval metadata and overrides#

Approval metadata is not optional. Require three fields on every case: reviewer name, approval timestamp, and reason code for any withholding override. If you release funds with missing or unresolved items, the override reason must say why.

For U.S. residence-based treaty positions, record whether residency certification is on file, pending, or not requested, and track any Form 8802 application status when your program uses that path.

The record should read as one continuous chain: payment intent, contract scope, classification memo, treaty note, tax-document artifacts, reviewer approval, any override rationale, and final payout instruction.

This pairs well with our guide on A Freelancer's Guide to the US-Germany Tax Treaty.

Set hard escalation triggers so teams stop guessing#

Ambiguity needs a real stop state. If the file is inconsistent, unclear, or producing the same exception pattern over and over, pause and escalate instead of pushing the payout through. Prioritize escalation where potential impact is highest: taxpayer rights, number of taxpayers affected, and financial impact.

| Trigger | When to escalate | Stated action |

|---|---|---|

| Mixed service and IP cases | The contract and payment record can reasonably support more than one tax characterization | Pause the payout, separate the facts, and route for specialist review |

| Treaty eligibility uncertainty | The file does not establish specific US-Germany contractor-withholding criteria, LOB pass/fail tests, or required residency-document workflows | Keep the decision open and send it to specialist review |

| Repeated exceptions | The same exception pattern recurs by corridor or entity type | Track the cases with reason codes and escalate recurring patterns for policy/process review |

Mixed service and IP cases#

Escalate when the contract and payment record can reasonably support more than one tax characterization. If service scope and rights language point in different directions, do not force a single label just to keep funds moving. Pause the payout, separate the facts, and route for specialist review.

Treaty eligibility uncertainty#

Escalate when treaty treatment is unclear from the existing file. The provided evidence does not establish specific US-Germany contractor-withholding criteria, LOB pass/fail tests, or required residency-document workflows. Keep the decision open and send it to specialist review rather than resolving it by analyst discretion.

Repeated exceptions are a policy signal#

Repeated exceptions should be treated as a potential systemic problem by corridor or entity type, not just one-off handling. Track these cases with reason codes and escalate recurring patterns for policy or process review so the same issue does not keep coming back.

Run payout operations in a fixed sequence from onboarding to post-payment review#

Once a case clears escalation, run it through a defined eight-step sequence so decisions stay consistent and auditable. The point is not more process for its own sake. It is making sure similar files are handled consistently.

Steps 1 to 3 before money moves#

The first three steps are mandatory before release: classify, verify documents, and set a preliminary tax-handling posture.

- Classify the payee and payment facts first.

Clarify who is being paid, in what role, and what the payment is for. Treat status determination as a required checkpoint, not a formality.

- Validate documentary completeness.

Confirm the file is internally consistent across payee profile, intake records, contract or statement of work, and payment description.

- Assign a preliminary tax-handling posture.

Record the current view, the basis, and whether the case can proceed, needs conditional handling, or stays paused for specialist review.

If contract scope and payout description do not match, treat it as a classification break and stop for review.

Steps 4 to 6 at execution#

Execution should start only after policy gates pass and decision records are complete.

- Apply policy gates.

Block progression when required fields are missing, contract terms changed, or the payment method no longer matches the approved model. Expect cross-team input where ownership is split across tax, legal, and operations.

- Execute payouts under approved routing only.

Use only the approved payment type, entity path, and tax-handling posture tied to that exact record. Do not carry forward old treatment when scope, deliverables, or rights language changed.

- Log decision metadata for audit and reconciliation.

Keep change history with core fields such as timestamp, reviewer, evidence version, tax-handling posture, override reason, and payout event reference.

Steps 7 to 8 after payment#

Post-payment controls should surface repeat failure patterns, not just close tickets.

- Run post-payment exception review.

Review disputes, returns, over-withholding complaints, and reconciliation breaks to identify where sequence controls failed.

- Tune rules on a recurring cadence.

Use at least a monthly review cycle, with annual checkpoints, to tighten only the controls that are repeatedly failing. Avoid one-size-fits-all rules when a scenario is not broadly applicable.

Monthly control test checkpoints#

- Confirm sampled payouts had status and payment classification completed before release.

- Confirm sampled files include consistent contract or SOW and payment descriptions.

- Reconcile approved tax-handling posture to executed payout and ledger treatment.

- Verify overrides include approver, timestamp, and reason code.

- Test for stale classifications: where scope or rights language changed, confirm a fresh classification was performed.

- Log recurring exception patterns and route fixes to policy, intake design, or specialist guidance.

For a related operating model, see How MoR Platforms Split Payments Between Platform and Contractor.

Prevent the most common operator mistakes in US-Germany withholding#

Focus on classification and evidence before you make a withholding decision.

Mistake 1: Treating all cross-border payouts as one tax bucket#

Do not treat different cross-border payout types as interchangeable categories. Use a strict classification checkpoint before release, and do not reuse a prior conclusion from a different payment type without a fresh review.

Mistake 2: Using VAT sources as if they decide income-tax withholding#

VAT process materials are the wrong source for a U.S.-Germany income-tax withholding decision. A VAT Cross Border Ruling (CBR) addresses VAT treatment of foreseen transactions and follows national VAT ruling conditions in the filing country. One Stop Shop (OSS) is an optional VAT scheme with its own registration and return mechanics. It includes Member State of identification and additional OSS returns, not an income-tax withholding determination.

Treat these as red flags:

- citing OSS status, deemed supplier treatment, or VAT e-commerce changes from 1 July 2021 as the basis for an income-tax payout release

- presenting the EC Parent/Subsidiary Directive or EC Interest and Royalties Directive as automatic answers for platform contractor payment facts

Mistake 3: Building justification after payout#

Set the decision record before payment, especially when the available support is VAT-only. If the file lacks non-VAT support for an income-tax withholding outcome, pause and escalate instead of treating VAT process rules as a final answer.

Mistake 4: No formal path for ambiguity#

Ambiguous files need a visible hold-and-escalate state. If facts are mixed, support is VAT-only, or the reasoning is copied from another income category, pause and escalate instead of using silent manual workarounds.

See Non-Resident Withholding on Contractor Payments: Platform Guide to the 30% Rule and Treaty Reductions for a related workflow.

Implement controls in Gruv without overbuilding#

Start narrow. Put in only the controls that block unsupported payouts and preserve decision evidence for each U.S.-Germany case. Once the hold-and-escalate path exists, resist full automation until exception patterns are clear.

Turn legal checkpoints into product gates#

Turn the legal checkpoints into explicit product gates for treaty-position decisions on payouts. At minimum, require payment type, payee tax profile, country pair, treaty-position status, and a flag for mixed service or IP facts before a payout can move forward.

A practical state model is usually enough:

| State | When used |

|---|---|

| Draft | Intake with missing facts |

| Ready for review | Only after required fields and documents are complete |

| Approved for payout | Only after named reviewer approval and timestamp |

| On hold for escalation | When treaty eligibility, residency, or income characterization is unclear |

Make the payout-release gate strict: if there is no documented treaty position, or the file reuses reasoning from a different income category, do not release payment.

Build one linked case record, not scattered notes#

Use one case record per payout, or payout batch, and link the request, decision, payout event, and reconciliation artifact. Even when steps are manual, the record should show what facts existed before payment, who approved, and which ledger event was posted.

Anchor this in artifact discipline, not free-text notes. IRS residency-certification operations use named Program Controls and specific checkpoints. If a position depends on U.S. residency certification, store the concrete document reference, for example the Form 8802 path, instead of summary text alone.

Add a stable payout reference for reconciliation. IRS materials describe researching payment confirmation numbers in the USRC database. Apply the same control idea so finance can match records without reopening legal analysis.

Design for exceptions early#

Exception handling should be a core control, not cleanup work. If a payout reference does not match the approved case, route it back to review. Do not allow off-platform fixes to become the system of record.

Also define a visible path for misdirected payments or misapplied records. IRS operations explicitly include an exception path for Checks not Belonging to USRC, which is a practical model for your own hold-and-return flow.

Include one time-based recheck rule. The IRS workflow includes a Three-Year Procedure, which supports periodic revalidation instead of treating documentation as permanently reusable.

Roll out narrowly, then generalize#

Launch this control set for the U.S.-Germany corridor first, review exception patterns, then expand. That sequence gives you real operating evidence before you generalize controls to other corridors.

Keep capability language exact. Describe controls as available only where supported and aligned to market or program coverage. For a deeper buildout, see How to Build a Global Tax Withholding Engine: W-8 W-9 and Treaty Rate Automation.

Conclusion#

The through line is straightforward: classify first, document the basis, assign the owner, then release funds. For U.S.-Germany contractor-payment flows, speed is not a substitute for a documented income characterization, treaty-eligibility check, and named approval owner.

The materials here do not support a single treaty withholding rate you can apply across all contractor fact patterns. If characterization is unclear, documentation conflicts, or a conclusion is borrowed from a different income category, hold the payout and escalate instead of improvising.

Keep one pre-payout case file that explains what is being paid, why the classification was chosen, and who approved the withholding posture. Where your position depends on U.S. residency certification, keep the IRS certification trail together with the payout record. That includes Form 8802 support, related control checkpoints, processing time limits and payment validation, and payment-confirmation tracking from the USRC database.

Treat evidence gaps as a control failure, not a drafting inconvenience. If a source is inaccessible or cannot be verified, record the uncertainty, document assumptions, and route to specialist review rather than auto-processing.

If you need one immediate next step for this corridor, do this:

- Implement documented decision criteria, an evidence pack, and hard escalation triggers before release.

- Enforce a stop state for unclear characterization, unclear treaty eligibility, or incomplete evidence.

- Review exceptions regularly so recurring edge cases become written policy and tighter intake rules.

When you are ready to translate this US-Germany control framework into implementation details, start with the Gruv docs and validate market/program coverage before rollout.

Frequently Asked Questions

Does the U.S.-Germany treaty itself provide a clear withholding rate for contractor service payments in all platform scenarios?

No. The materials here do not establish a single treaty withholding percentage for independent contractor service payments across all platform models, and they do not provide one article-and-rate combination to apply mechanically. If the payment cannot be tied to a clearly supported income category, treat the rate as uncertain and route it for review rather than guessing.

What withholding rates are clearly discussed in current Germany-focused materials, and which income types do they apply to?

The BZSt Section 50a EStG source is procedural guidance, not a treaty rate table for contractor services. The ESMA material is explicitly about withholding tax on dividends, not contractor service payouts. The numeric rates shown here are DST examples from CRS, such as 3% in Spain and a planned 3% in the UK, and those are revenue-tax examples, not U.S.-Germany contractor withholding rates.

Can a platform reuse dividend treaty outcomes for contractor payouts if the same payee is involved?

No. The ESMA material here is framed around dividend withholding and withholding-tax reclaim-scheme risk, not contractor service payouts. Do not assume a dividend outcome can be reused for contractor service payments, even when the payee is the same.

What should we do operationally when rate applicability is unclear at payout time?

Use a hold-and-review path before release when rate applicability is unclear. Where the process falls under Section 50a EStG, a concrete checkpoint is that withholding tax returns must be submitted electronically via the BZStOnline-Portal. If a representative is filing, BZSt asks for the original power of attorney to be sent to BZSt.

Which facts usually trigger escalation instead of automated treatment under a treaty claim?

The excerpts do not provide a definitive escalation-trigger list for U.S.-Germany contractor-service treaty claims. Treat unresolved income characterization or unverified execution details as review-required rather than auto-processing. One explicit BZSt process risk is that a local tax-office SEPA mandate does not automatically apply to BZSt, so a separate BZSt mandate is required.

What minimum records should we keep to defend a withholding decision during audit or dispute?

The provided excerpts do not define a complete minimum-record standard for contractor-service treaty decisions. If Section 50a EStG applies, retain evidence of BZStOnline-Portal submission, the separate BZSt SEPA direct debit mandate where used, and the original power of attorney when a representative acts. Keep these with your internal decision record so the file reflects what was known and approved at payout time.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- census.gov/programs-surveys/brds/about/brdshelp.htmltrusted

- congress.gov/crs_external_products/R/PDF/R45532/R45532.2.pdftrusted

- congress.gov/event/110th-congress/senate-event/LC9658/texttrusted

- downloads.regulations.gov/USTR-2025-0016-0053/attachment_1.pdftrusted

- esma.europa.eu/sites/default/files/library/esma70-155-10272...trusted

- govinfo.gov/content/pkg/FR-1974-04-23/pdf/FR-1974-04-23.pdftrusted

- govinfo.gov/content/pkg/CHRG-118shrg54561/html/CHRG-118s...trusted

- irs.gov/pub/irs-trty/germany.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

US-UK Tax Treaty Withholding Controls for Contractor Payment Platforms

For US-UK contractor payouts, the main risk is usually not a lack of treaty awareness. Your team creates risk when it approves reduced or zero withholding before you confirm income source, payment type, and treaty-status documentation. A UK label on its own does not support the treatment.

US-India Contractor Payment Withholding Decisions for Platforms

US-India withholding failures often start with misclassification, not rate selection. When contractor services, royalties, and fees for included services are treated as interchangeable, the payout file can carry the wrong payment character before anyone applies a rate.

Non-Resident Withholding on Contractor Payments: Platform Guide to the 30% Rule and Treaty Reductions

Start with the default. If a payment is in scope for NRA withholding and you cannot support reduced treatment, withhold 30% and escalate unresolved cases before release.