Quick Answer

Start by confirming four points before claiming us-uk tax treaty royalties treatment: UK treaty residence, beneficial ownership, payment classification under Article 12, and no clear U.S. permanent-establishment trigger. Then file Form W-8BEN with details that match your contracts, royalty statements, and payer records. Keep the position maintainable by updating your file when travel patterns, contract authority, or UK filing status changes, including Self Assessment activity and UTR readiness.

For UK-based creative professionals, US-source royalty income can be a meaningful revenue stream. It also carries a familiar risk: the default 30% withholding tax. Many people treat Form W-8BEN as the whole answer, but that is too narrow. If you handle this as a one-off form task, you leave room for payment delays, incorrect deductions, and avoidable compliance stress.

A better approach is to treat this like a business decision. That means building a position you can explain and support, not just submitting paperwork and hoping the payer processes it correctly.

The practical sequence is simple. Validate, Execute, Defend. First confirm you are entitled to claim treaty benefits. Then file in a way that matches your documents and payment setup. After that, keep your facts clean so the position still holds if anyone asks questions later.

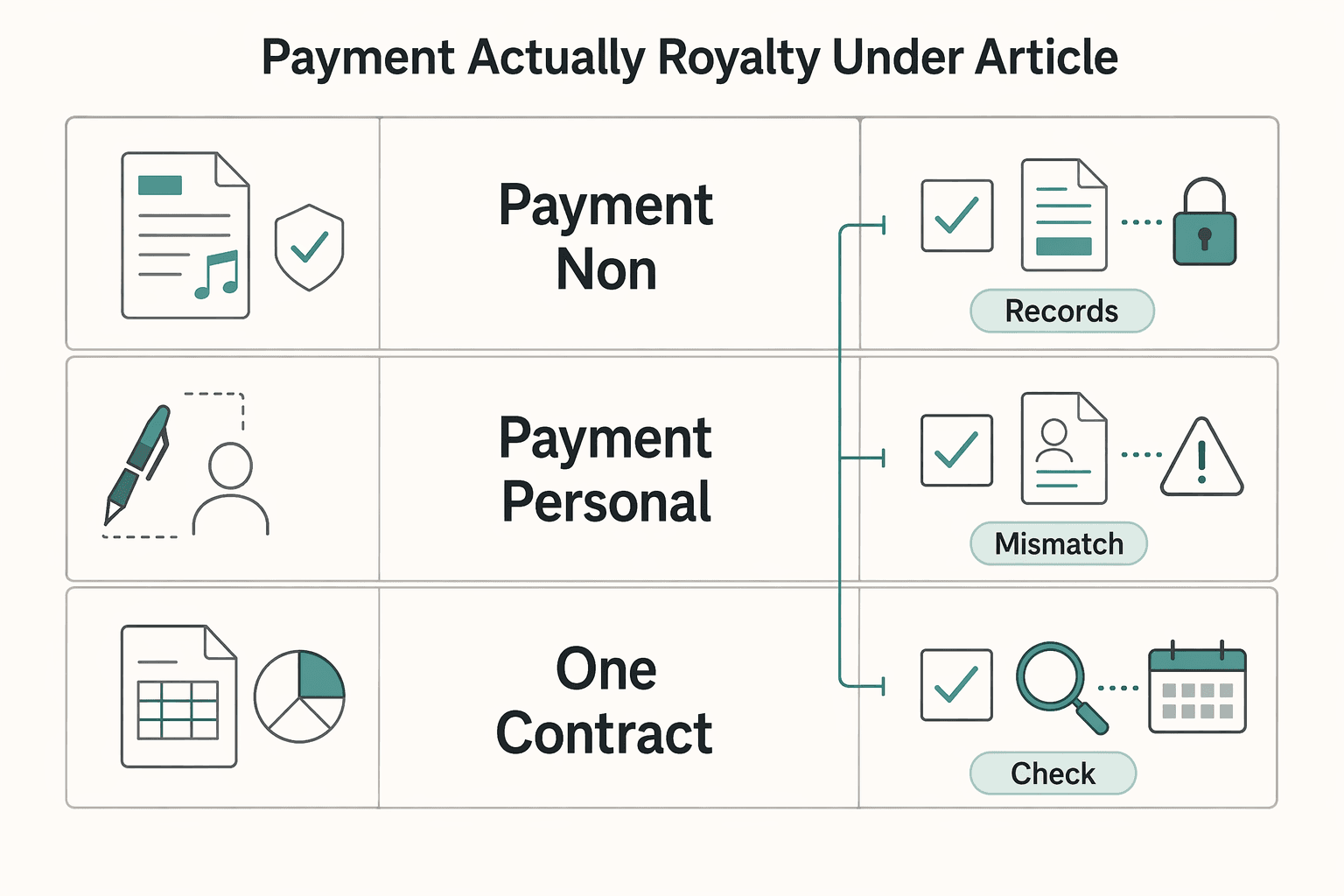

Stage 1: VALIDATE Your Eligibility#

Before you file Form W-8BEN, clear these four checks. If any answer is unclear, conflicted, or hard to prove, pause the treaty claim. A withholding agent can deny reduced withholding if they have reason to doubt your claim.

| Check | What to confirm | Evidence to keep |

|---|---|---|

| UK treaty residence for the royalty period | Residence for the period when the income arises; if facts are cross-border or mid-year, dual-residence outcomes require treaty tie-breaker tests in sequence | SRT day counts; travel log; records showing where you lived during the income period; documents supporting your UK tax-residence position |

| Beneficial owner of the income | You must be the beneficial owner of the income; if you are only collecting for someone else, the claim can fail | Signed publishing or license agreement; any IP assignment/amendment that changed ownership; royalty statements and payer notices; payment instructions and bank trail showing payer-to-owner alignment |

| Payment is actually a royalty under Article 12 | Not every author-related payment is a royalty, and classification affects the form path | Full contract and statement of work; work title(s) and payer identity details; invoices and royalty statements; any schedule that separates license fees from service fees |

| Early sign of a U.S. permanent establishment | Screen for a fixed U.S. place of business or a U.S.-based person who routinely concludes contracts that bind your enterprise | U.S. office/workspace records, if any; agency agreements; communications showing who can conclude contracts; records showing where core business activity occurs |

Are you a UK treaty resident for the royalty period?#

Start with residence for the period when the income arises. The treaty applies only to residents of one or both treaty states, and the Statutory Residence Test is the UK starting point for each tax year.

If your facts are cross-border or mid-year, do not assume the answer. Dual-residence outcomes require treaty tie-breaker tests in sequence.

Evidence to keep

- SRT day counts for the relevant tax year

- Travel log for the same period

- Records showing where you lived during the income period

- Documents supporting your UK tax-residence position

Are you the beneficial owner of the income?#

For a W-8BEN treaty claim, you must be the beneficial owner of the income. If you are only collecting for someone else, the claim can fail.

The paper trail matters. If the contract says one thing, the payment trail shows another, or ownership changed and the records were not updated, your claim may be challenged.

Evidence to keep

- Signed publishing or license agreement

- Any IP assignment/amendment that changed ownership

- Royalty statements and payer notices

- Payment instructions and bank trail showing payer-to-owner alignment

Is the payment actually a royalty under Article 12?#

Classification is the next checkpoint. Do not guess. Not every author-related payment is a royalty. Classification also affects the form path: IRS guidance points to W-8BEN for non-personal-services income and Form 8233 for personal-services income.

| Scenario | Likely treatment | What to do now |

|---|---|---|

| Payment is non-personal-services income | W-8BEN path | Continue treaty review |

| Payment is personal-services income | Form 8233 path | Review personal-services treaty path/form |

| One contract bundles rights-based payments and services | Mixed/unclear | Pause; classify before filing |

HMRC materials also note some author receipts can be treated like professional-service fees. If your contract is mixed, do not file on assumptions.

Evidence to keep

- Full contract and statement of work

- Work title(s) and payer identity details

- Invoices and royalty statements

- Any schedule that separates license fees from service fees

Is there any early sign of a U.S. permanent establishment?#

Before you file, do a quick PE triage. The treaty PE concept is a fixed place of business through which business is carried on. IRS practice guidance (non-binding) also flags dependent-agent contract authority in the U.S. as a risk indicator.

At this stage, you are not trying to resolve every edge case. You are screening for obvious triggers: a fixed U.S. place of business, or a U.S.-based person who routinely concludes contracts that bind your enterprise.

Evidence to keep

- U.S. office/workspace records, if any

- Agency agreements

- Communications showing who can conclude contracts

- Records showing where core business activity occurs

If all four checks are clean, move to Stage 2 for filing. If any check is disputed, mixed, or fact-heavy, treat it as risk triage now. Pause the claim, document the issue, and escalate to a qualified cross-border advisor before claiming treaty relief.

You might also find this useful: Tax Implications of Earning Royalties for a US Author Living in the UK.

Stage 2: EXECUTE the Paperwork Flawlessly#

Execution is mostly a consistency test. Your records and UK tax administration need to line up before you file.

Use current GOV.UK Self Assessment guidance as your source of truth. Before completing anything, assemble one working file with your HMRC registration/reactivation records, UTR details, and trading records.

Prepare inputs before completing the form#

Start by getting the basics aligned so you can file without avoidable delays.

| Input | What to confirm | Common error |

|---|---|---|

| Self Assessment status | Confirm whether you need to register for Self Assessment or reactivate an existing account | Trying to file without registering first, or filing from an inactive account |

| Tax identification readiness | Have your Unique Taxpayer Reference (UTR) available before using the online filing service | Reaching filing time without your UTR |

| Online filing scope check | Check whether your case fits the online filing service, including non-resident situations | Assuming the online route applies to every case |

| Recordkeeping | When you start trading, keep records from day one | Trying to rebuild records close to deadlines |

- Self Assessment status - Confirm whether you need to register for Self Assessment or reactivate an existing account.

- Tax identification readiness - Have your Unique Taxpayer Reference (UTR) available before using the online filing service.

- Online filing scope check - Check whether your case fits the online filing service, including non-resident situations.

- Recordkeeping - When you start trading, keep records from day one.

Resolve blockers early#

If something does not line up, fix it before a deadline is close.

| Scenario | Why it matters | What to do next |

|---|---|---|

| First-time Self Assessment filer with no UTR yet | You must register before first online filing, and the service requires a UTR | Register for Self Assessment, then proceed when your UTR is available |

| Previously registered but inactive Self Assessment account | HMRC states filing may be delayed without reactivation | Reactivate the account before filing |

| You need to complete a return for the previous year and have not told HMRC | HMRC requires notification by 5 October, and late notification can lead to a penalty | Notify HMRC as soon as possible and document the date |

| You plan to file online as a non-resident | The online filing service has scope limits, including non-resident cases | Check service eligibility before relying on online filing |

| You started trading and have not kept records | Recordkeeping is required when you start trading | Rebuild records now and keep ongoing records current |

Run the UK compliance timeline in parallel#

Do not leave the UK side to the last minute. Key checkpoints run on fixed dates.

| Checkpoint | Timing | Note |

|---|---|---|

| Tell HMRC if you need to complete a return for the previous year | 5 October | Late notification can lead to a penalty |

| File a return | On or after 6 April after the tax year ends | Filing starts after the tax year ends |

| Pay your tax bill | 31 January | Payment is due by 31 January |

| Review sole-trader registration requirements | If you earn more than £1,000 in a tax year | Review the requirements immediately |

If you need to complete a return for the previous year, you must tell HMRC by 5 October. GOV.UK's stated example is 5 October 2025 for the tax year 6 April 2024 to 5 April 2025, and late notification can lead to a penalty.

You can file a return on or after 6 April after the tax year ends, and you need to pay your tax bill by 31 January. If you start trading, you must keep records, and if you earn more than £1,000 in a tax year, review sole-trader registration requirements immediately.

Keep the file current with a control checklist#

Once filing is underway, keep one current file so future filings are easier.

- Keep HMRC registration or reactivation records together with your UTR details.

- Keep trading records up to date throughout the tax year.

- Recheck filing readiness before key dates (5 October, on or after 6 April, and 31 January).

- Update your file promptly if your filing status changes.

Keep your submission within what your records can support. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025. Before you submit, use the same details in one clean draft so everything stays consistent: W-8 Form Generator.

Stage 3: DEFEND Your Position Against Hidden Risks#

A treaty position stays strong only if your real U.S. operating facts stay outside permanent establishment exposure. Under the treaty, Article 12 royalty treatment can be displaced if royalties are attributable to a U.S. PE, so this stage is about controlling facts, not just filing forms.

Use two PE lenses in your self-audit: fixed place of business and dependent agent. Also keep this in view: a U.S. business touchpoint does not automatically create a PE, and IRS treaty practice guidance notes that limited preparatory or auxiliary activity may not. But those labels do not help much without records. Your file needs to show what actually happened.

Self-audit the fixed-place risk#

The key question is whether you have a fixed place of business through which your business is carried on. Focus on whether a U.S. location is fixed, available to you on an ongoing basis, and used to carry on business.

- Low risk signal: You take short, temporary trips, use changing locations, and do not have a dedicated U.S. office, studio, or desk available on an ongoing basis.

- Medium risk signal: You repeatedly use the same U.S. workspace or present a stable U.S. base in public materials even though your setup is meant to be temporary.

- High risk signal: You have a dedicated U.S. place continuously available and use it to carry on business, with contract and operating patterns reinforcing that setup.

Self-audit the dependent-agent risk#

You can create PE risk without a fixed office if someone in the U.S. acts on your behalf with meaningful contract authority.

- Low risk signal: You use a genuinely independent intermediary acting in the ordinary course of their own business, and they do not bind you.

- Medium risk signal: A U.S. representative negotiates key terms or presents deals as effectively final, while you formally sign.

- High risk signal: A U.S. representative can conclude contracts or approve core commercial changes such as pricing, renewals, amendments, or rights grants without your fresh review.

| U.S. activity pattern | Likely PE risk direction | Immediate mitigation action |

|---|---|---|

| Temporary travel for meetings/events and short-term work from changing locations | Lower signal if activity remains limited and temporary | Keep dated trip logs and purpose notes; avoid presenting any U.S. location as your operating base |

| Recurring use of one U.S. workspace | Rising signal due to continuity/availability pattern | Reduce repetition where possible; document temporary, non-exclusive use; remove standing-office signals |

| Contract-signing authority held by a U.S. representative | High signal under dependent-agent analysis | Revoke or narrow authority in writing; keep final approval/signature control with you outside the U.S. |

| Marketing with a U.S. address | Weak alone, stronger when it matches actual fixed-place use | Remove or correctly label U.S. address references; keep records showing no fixed place through which business is carried on |

Build an evidence file that matches reality#

This is where many people lose the thread. Intent is not enough if your contracts, travel pattern, and public-facing signals point in a different direction. Keep records that prove the limits in practice.

Review contract language for work location, signature authority, amendment authority, and anything implying a U.S. operating base. Keep written authority boundaries for any U.S. representative, including what they may do and what they may not do. Maintain a live travel and work-location log for each U.S. trip with dates, city, address used, purpose, whether the space was temporary or non-exclusive, and what activity occurred.

Keep supporting artifacts aligned with that log, such as calendar entries, bookings, workspace receipts if any, and public-facing profile or site snapshots.

At each operational change, such as a new agreement, renewed agreement, new U.S. representative, or repeated use of one U.S. location, reconcile the same day:

- Contract terms

- Authority boundaries

- Public location signals

- Travel/work-location log

If those four records conflict, fix the mismatch before the next payment cycle. Any treaty wording you use, including W-8BEN support language, should match facts you can document.

Know when to escalate#

Some issues are not worth trying to patch yourself. Escalate to a cross-border tax advisor when any of the following appears:

- You begin recurring use of one U.S. location.

- A U.S. person negotiates or signs in ways that may bind you.

- A payer challenges whether royalties are attributable to a U.S. PE.

- Your conclusion depends on an unverified threshold.

If a threshold is unclear, do not guess. Mark the current threshold as pending official tax or advisor verification before you rely on it.

Conclusion: You Are the CEO of Your Global Business#

Treat this as an operating discipline, not a one-time form task. Validate, execute, and defend your position with records you can actually prove. Specific US-UK treaty article details, withholding rates, and payer-form requirements should be verified against official tax records or advisor records before you act.

Validate: before the next payment, confirm your UK filing status and records still match your current facts. Execute: confirm your UK filing setup is active, including Self Assessment registration or reactivation if required. Defend: keep a current file that explains your payment treatment and supports your UK reporting if questioned later.

On the UK side, keep the process current. If you are filing for the first time, register for Self Assessment before using the online service. If you had an account that became inactive, reactivate it first, because filing without reactivation can delay your return.

Keep core records, such as bank statements or receipts, and keep UTR access ready for online filing. File on or after 6 April after tax year-end, and pay by 31 January. If you need to notify HMRC that you must file, verify the current 5 October deadline for your year before relying on an older example date.

| Reactive creator | Operator mindset |

|---|---|

| Waits until deadline pressure to check UK filing basics | Re-checks Self Assessment status and filing readiness before key dates |

| Treats recordkeeping as admin noise | Keeps bank statements or receipts and UTR access ready |

| Leaves UK filing prep to the deadline window | Keeps filing and payment dates current |

Keep that mindset with this quick checklist:

- Confirm your Self Assessment status (registration or reactivation) matches current facts.

- Keep core records and UTR access ready.

- Confirm filing and payment readiness for your tax year.

Escalate to a qualified tax professional when your business structure is changing, or when you cannot verify current requirements for treaty treatment, withholding, or payer documentation for your specific facts.

For related context, see A Deep Dive into the US-France Tax Treaty for Freelance Performers.

If you want this to stay low-stress year-round, keep residency evidence and renewal timing in one place, for example with the Tax Residency Tracker.

Frequently Asked Questions

Do you automatically qualify for the US-UK tax treaty royalties position just because you live in the UK?

No. First validate the Stage 1 facts: treaty residence under Article 4, income characterization under Article 12, and whether Article 5 (Permanent Establishment) could affect your position. If any of those points are unclear, pause before the next payment and verify your contract terms, payer classification, and residence records.

How should you complete Form W-8BEN for royalty payments?

Use the current IRS form and instructions, not an old example. In Stage 2, make sure what you claim matches your documented residence and treaty-position facts, then keep a copy plus payer confirmation in your file. If a payer asks for wording or identifiers you have not verified, note that the current form requirement must be checked against official IRS instructions, payer records, or advisor records before use.

What withholding rate should you expect?

Do not rely on a blog, a dashboard default, or an IRS bulletin synopsis. IRS bulletin synopses are not authoritative treaty interpretation, so get the payer’s written rate both before and after treaty-claim review. If the rate is still under review, mark the withholding rate as pending official tax or advisor verification before you rely on it.

Does temporary U.S. travel create permanent establishment risk under Article 5?

Permanent Establishment risk under Article 5 cannot be resolved from a short travel label alone. In Stage 3, document what actually happened and reassess when your operating pattern changes. | Situation | Risk direction | Next action | | --- | --- | --- | | Short, temporary U.S. travel | Cannot be determined from travel facts alone | Keep dated trip/location logs | | Repeated U.S.-connected activity | Cannot be determined from activity labels alone | Document the full fact pattern and review before the next payment | | Unclear or disputed operating facts | Higher uncertainty | Escalate for qualified advice |

Do you need a U.S. TIN, or will a non-U.S. tax number be enough?

Do not guess. Check the current form instructions and the payer’s onboarding requirements, then match the identifier to your legal and tax profile. | Payer request | What to do | | --- | --- | | Accepts a non-U.S. tax identifier | Confirm it matches current instructions and your records | | Requires a U.S. TIN | Ask for the requirement basis in writing; escalate if unclear before payment |

Do you still need HMRC filing steps if the payer is in the U.S.?

Yes. HMRC filing steps can still apply when you are required to file, and HMRC says you can notify by registering for Self Assessment. Keep core records, such as bank statements or receipts, file online on or after 6 April after tax year-end, and pay by 31 January. For year-specific cutoffs, verify the current HMRC notification deadline against official HMRC records or advisor records before you rely on it. If you are waiting for a UTR, reactivating an existing account, or your case includes non-resident-abroad facts, resolve that early or get qualified advice.

Try a related tool

A financial planning specialist focusing on the unique challenges faced by US citizens abroad. Ben's articles provide actionable advice on everything from FBAR and FATCA compliance to retirement planning for expats.

With a Ph.D. in Economics and over 15 years of experience in cross-border tax advisory, Alistair specializes in demystifying cross-border tax law for independent professionals. He focuses on risk mitigation and long-term financial planning.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment...trusted

- assets.publishing.service.gov.uk/media/5a81972ce5274a2e8ab54ce7/usa-consolida...trusted

- irs.gov/individuals/international-taxpayers/claiming...trusted

- irs.gov/businesses/international-businesses/united-k...trusted

- gov.uk/log-in-file-self-assessment-tax-returnexternal

- gov.uk/register-for-self-assessmentexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

How to Find the Best Deals on Flights

If you are planning a move or a long stay, the right way to find cheap flights is to choose the fare that supports the trip you are actually taking, not just the one with the lowest headline price. A cheap fare can still be the smart choice, but only if it gets you there on a schedule you can use, leaves you functional when you land, and gives you booking records you can work with later.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.