Quick Answer

Use a yes/no/escalate screen first for us-netherlands tax treaty lob. Confirm Article 4 resident status, match each income stream to Article 10, 12, or 13, and test Article 26 with the Convention text plus the IRS Netherlands treaty documents. If ownership records, operating-footprint evidence, or funds-flow support do not clearly back one LOB route, stop and escalate before requesting reduced withholding.

Make a defensible yes / no / escalate call on your LOB position#

Use this guide to make a defensible yes / no / escalate call on the Limitation on Benefits issue and leave with a document checklist you can actually use. The point is not to guess or claim treaty benefits based on a structure that only sounds plausible.

The U.S.-Netherlands Income Tax Treaty sets the framework for cross-border tax treatment, and Article 26 (Limitation on Benefits) is a gate, not a formality. The treaty package includes Article 26 by name, and the IRS publishes a full Netherlands treaty document set, not just a summary. One common failure mode for solo operators is assuming eligibility without a file that shows why.

What you should leave with#

By the end, you should have two things:

- A yes, no, or escalate decision on whether your facts are strong enough to keep testing treaty access.

- A documentation checklist you can share with a preparer or use to build your own treaty file.

The checklist is the main output. A treaty position is much easier to defend when you can point to the exact materials you relied on. Your file should include the Convention, the Protocol, and the IRS Technical Explanation, which the IRS describes as an official guide to the Convention and Protocol.

Why the gate matters#

Do not treat residency or a Netherlands entity as an automatic pass to benefits. The Convention signing date, December 18, 1992, the Protocol signing date, October 13, 1993, and the general effective date shown in the treaty PDF, 1 January 1994, are important context. They do not decide eligibility on their own.

The real question is whether your facts hold up against the full treaty package. That package spans more than one file and includes interpretive materials referenced alongside the Convention. Start with a basic control step: pull the documents from the IRS Netherlands treaty hub and confirm you can open them cleanly, because incomplete files and secondary summaries create avoidable errors.

What this article is and is not#

This is an operator-focused decision outline for freelancers and consultants who want a clean first pass before filing or briefing an advisor. It is meant to separate strong facts from weak assumptions where treaty access depends on records.

It is not individualized legal or tax advice. If your facts are messy, your ownership chain is hard to document, or the treaty materials do not clearly support your reading, escalate instead of improvising.

For a step-by-step walkthrough, see A Deep Dive into the US-Netherlands Tax Treaty for Independent Contractors.

Confirm treaty scope before you test LOB#

Before you touch Article 26, confirm scope: the right treaty, the right claimant, and the right income article. If that foundation is unclear, any LOB conclusion is guesswork. Work through this pre-screen in order:

| Check | What to confirm | Why it matters |

|---|---|---|

| Instrument and jurisdictions | Tax Convention with the Netherlands between the United States and the Kingdom of the Netherlands; Convention, Protocol, and Technical Explanation from the IRS treaty documents | Confirms the right treaty package |

| Claimant and residence | Who is claiming benefits and why that person or entity is a treaty resident under Article 4 (Resident) | LOB testing starts only after treaty residency is clear |

| Income article | Map the payment to Article 10 (Dividends), Article 12 (Interest), or Article 13 (Royalties), as applicable | Avoids testing treaty benefits in the abstract |

| PE vs. LOB | Keep Article 5 (Permanent Establishment) facts separate from Article 26 (Limitation on Benefits) | They answer different questions |

- Confirm the instrument and jurisdictions.

Verify you are working under the Tax Convention with the Netherlands between the United States and the Kingdom of the Netherlands. Pull the official IRS treaty documents and confirm the Convention, Protocol, and Technical Explanation are the package you are relying on.

- Identify the treaty claimant under Article 4.

Establish Article 4 (Resident) status before LOB testing. Treaty residency is determined under the treaty, so you should be able to state clearly who is claiming benefits and why that person or entity is the treaty resident.

- Map the payment to the relevant income article.

Do not assess "treaty benefits" in the abstract. Map the income to the article you are actually using, such as Article 10 (Dividends), Article 12 (Interest), or Article 13 (Royalties).

- Keep PE analysis separate from LOB entitlement.

Article 5 (Permanent Establishment) and Article 26 (Limitation on Benefits) answer different questions. PE analysis covers whether income is attributable to a permanent establishment. LOB analysis covers whether treaty benefits are available to the resident.

Two red flags should trigger a pause. First, a file that does not name the claimant, income article, and jurisdictions. Second, a file that relies on treaty tables without checking the treaty text. IRS guidance is to examine the specific treaty articles and check the relevant LOB text to see which tests are available.

Your output from this phase should be a facts-first brief with:

- claimant name and entity type

- residence position under Article 4 (Resident)

- payor country and recipient country

- income type and proposed article, for example Article 10, 12, or 13

- Article 5 (Permanent Establishment) facts listed separately

- documents reviewed from the official treaty set

If you cannot complete this brief without hedging, fix scope before you test LOB. Once scope is clean, you can move to a short Article 26 screen without mixing issues.

You might also find this useful: What is the 'Limitation on Benefits' (LOB) Clause in a US Tax Treaty?.

Run a one-sitting LOB pre-screen for a Dutch BV#

Use this first pass as a gate: either you have one clearly supportable basis under Article 26, or you mark the file escalate before any filing or withholding decision.

Keep it short and evidence-first. If you cannot answer basic ownership, claimant, and activity questions without a long explanation, treat that as a warning sign.

Start with inputs you can verify now#

Use only facts you can tie to documents:

- exact claimant and legal entity type (the Dutch BV claiming treaty benefits)

- ownership map from the BV through intermediate entities to ultimate owners

- income type and the treaty article already mapped in scope

- where relevant activity tied to the income happens

Your checkpoint is simple: can a third party understand who earns the income, who owns the claimant, and where the relevant activity happens from the file alone? If not, do not move to a confident yes.

Screen major LOB tests, then confirm in treaty text#

Use IRS treaty tables as a checkpoint so you do not skip a major LOB test. Table 4 is useful for that. But the IRS also says the tables are not a complete guide, so a table-only answer is not enough.

If anything is debatable, go back to the IRS Netherlands treaty documents page. Confirm against Article 26 (Limitation on Benefits) in the treaty text, and use the Technical Explanation where interpretation matters.

Build the yes/no/escalate grid#

Create a one-page grid with one row per LOB test you screened and these fields:

| LOB test screened | Result (yes / no / escalate) | One-sentence reason | Document relied on | Main open question |

|---|

Apply one strict rule: if your first pass cannot clearly support one basis under Article 26 from the treaty materials, mark escalate. A documented pause is safer than forcing a weak claim.

Compare qualifying routes and where solo operators usually fail#

Use the route you can prove now, not the one with the best-looking outcome. A defensible Article 26 path is safer than a fragile interpretation. If you cannot tie the claim back to treaty text and documents, treat it as an escalation case.

Do not confuse residency with access#

Article 4 residency is necessary, but it is not enough by itself. In treaties with an LOB article, you need both treaty residency and satisfaction of the LOB article. For U.S.-source dividends in these treaty materials, at least one Article 26 test must be met for the benefit claimed.

This is where files break. Residency is documented, but LOB eligibility is assumed instead of proven. A Dutch BV can be resident and still fail a treaty-benefit claim if no applicable Article 26 route is clearly supported.

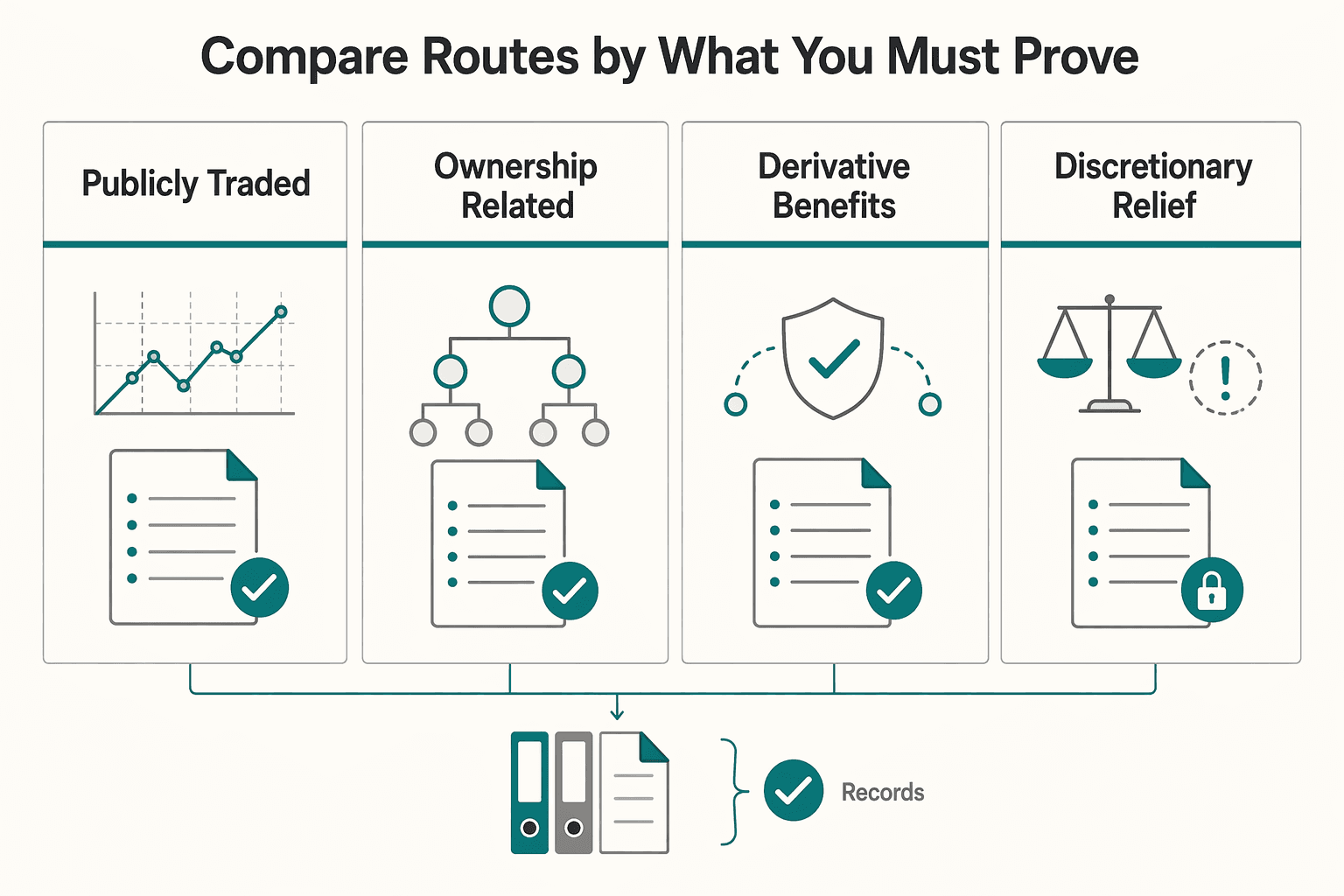

Compare routes by what you must prove#

| Route you are considering | What you need to verify now | Common failure to check |

|---|---|---|

| Publicly traded / recognized stock exchange route | The claimant's principal class of shares is substantially and regularly traded on one or more recognized stock exchanges | Group-level narrative is used instead of claimant-level share and trading evidence |

| Ownership and related listed tests under Article 26 | A clean ownership map plus support for required ownership and payment facts in treaty text | Verbal explanations are used instead of cap table, payment, and entity records |

| Derivative benefits route | Owner-level treaty-entitlement and ownership facts, checked against treaty text | Structure complexity can make the route hard to evidence clearly |

| Discretionary relief through U.S. Competent Authority | A documented request path when no applicable listed test is met | The path is treated as an informal backup instead of a formal escalation lane |

Listed routes are rule-based. You match facts to text. Discretionary relief exists, but it is not a self-proving filing position.

Where ownership complexity breaks the story#

Closely held does not automatically mean ineligible. It does mean you should be strict about any reliance on recognized-stock-exchange logic, which depends on specific trading criteria for the claimant's principal class of shares. If the claimant is privately owned, or you only have listing evidence for another entity in the chain, do not assume that route works.

A practical checkpoint is whether the claimant share register, current ownership chart, and any listing support make sense to a reviewer without oral explanation.

Use a hard stop when the route depends on exceptions#

If your route depends on exceptions you cannot evidence clearly, stop and document escalation. Record the Article 26 route considered, why it is not clearly met, what evidence is missing, and whether the next step is treaty-text review, Technical Explanation review, or advisor escalation.

IRS treaty tables are a guide, not the final authority. Before relying on any route, confirm the available tests and exact requirements in the treaty text itself. Once you know which path you are testing, the next question is whether your operating facts actually support it.

Apply the active business route without overreaching#

Use the active business route only when your file shows real operating activity tied to the income. If it does not, do not force an Article 26 (Limitation on Benefits) position.

This is a facts-first route, not a narrative rescue. A reviewer should be able to see what the claimant does, where it does it, and how that activity connects to the treaty claim without filling gaps by assumption.

Start with operating activity, not entity labels#

You are trying to show real operating activity, not just an entity that receives income. Labels like "consulting company" or "management company" are not proof on their own. Use three blunt checks as a practical screen, not as treaty thresholds:

- What recurring activity creates value?

- Who performs and controls that activity, and in which treaty jurisdiction?

- Which records support that story if challenged?

If the file mainly shows invoicing and cash collection while the real work sits elsewhere, treat the position as weak and escalate.

Use Article 5 facts to anchor geography#

Use Article 5 (Permanent Establishment) facts to anchor geography, then test the LOB claim under Article 26. Article 5 helps you describe where business presence and operations sit. It does not, by itself, satisfy Article 26.

The treaty materials confirm the Article 5 and Article 26 structure, but not the detailed mechanics of each Article 26 test. Keep the story consistent across your records. If the operating footprint changes depending on which document you read, stop and resolve that conflict before relying on this route.

Know the failure mode before review#

A common overreach is claiming active business while the records show detached income flows. A formal structure can look clean while operating activity is unclear or outside the claimant's actual footprint.

Treat that as a red flag, not a drafting problem. Build a short evidence pack against Article 5 and Article 26. If you cannot connect income to real operations in plain English, move to escalation.

Handle ownership, base reduction, and conduit risk in small-company structures#

Treat ownership and cash-flow proof as a go / no-go screen for Limitation on Benefits analysis. If you cannot explain ultimate ownership, economic benefit, and fund flows in plain language in under five minutes, treat the position as high risk and escalate.

Small-company claims can fail when the structure sounds clean at a high level but the ownership and payment record tells a different story. That gap is where treaty-shopping risk starts to appear, especially when a Dutch BV sits between U.S.-source income and someone outside the treaty-resident story.

Build an ownership evidence map, not a cap-table summary#

For base-reduction screening, do not rely on labels like "founder-owned." Build one map from the claimant to ultimate owners. Then overlay recurring outbound payments that reduce the local tax base.

Your map should align three answers at once:

- Who legally owns the shares.

- Who controls decisions.

- Who economically uses and enjoys the income after receipt.

If those answers come from different records, reconcile them before taking a treaty position.

| Check | What to verify | Red flag |

|---|---|---|

| Legal ownership | Current shareholder register, transfer records, voting rights, director appointments | Old cap table, nominee-style descriptions, or inconsistent ownership across documents |

| Economic outflows | Dividends, interest, royalties, service fees, management charges, related-party debt payments | Material recurring outflows with weak commercial support |

| Ultimate benefit | Who actually uses and enjoys the income, based on agreements, bank flows, and decisions | Income lands in the BV, then quickly moves to a person or entity outside the treaty-resident story |

This map helps you test ownership-side anti-abuse risk and expose hidden complexity. If the structure only sounds normal after a long explanation, treat that as a warning sign.

Stress-test the money trail for conduit risk#

Trace U.S.-source receipts into the BV, then trace material onward payments around those receipts. Focus on behavior, not labels.

A key anti-abuse signal in broader international tax analysis is near-total onward payment shortly after receipt to an entity that would not qualify for the same relief. Do not treat that standard as legally identical to treaty LOB rules, but use it as a conservative screening flag. If the BV looks like a short cash stop, treat the position as higher risk.

Use records that show timing and substance:

- bank statements around receipt and onward-payment dates

- intercompany agreements and invoices

- loan documents where interest is paid

- board approvals or minutes for distributions

- general ledger detail

- evidence of real local costs and expenditure

Substance should be visible in management activity, balance sheet reality, and cost structure tied to actual operations, not just formal legal steps.

Compare the two patterns before you decide#

A direct operating Dutch BV with retained substance is not automatically qualified, but it may be easier to defend. Income is earned, meaningful margin is retained, local costs are paid, and distributions are business decisions rather than automatic relays.

The higher-risk pattern is pass-through behavior. U.S. income arrives, then most of it is quickly paid out as royalties, interest, fees, or similar amounts, with little retained income and limited local activity. That pattern can draw challenge because it can look like indirect access to treaty benefits through an intermediate entity.

If facts are mixed, do not solve that with better wording. Build a short evidence pack and test it against the IRS Technical Explanation and companion treaty materials. That includes exchange of notes, the Memorandum of Understanding, and the Protocol's exchange of notes and Agreed Minutes. If ownership is not current through ultimate owners, or flow of funds shows rapid onward payments you cannot support with real business substance, escalate before making the claim.

We covered this in detail in A Deep Dive into the 'Dividend' Article of the US-Germany Tax Treaty for LLC Owners.

Flag edge cases you should not self-interpret#

Do not self-interpret this on a first pass when transparent entities or triangular facts are involved. When those patterns appear, treat your first read as preliminary and escalate for professional review.

Treat transparent entities as a caution zone, not an automatic yes or no. The outcome can depend on how the treaty text, Article 26 (Limitation on Benefits), and the interpretive materials apply to your exact entity and income item.

Treat triangular cases the same way. Avoid analogy-based conclusions and escalate when facts cross multiple jurisdictions.

Use this checklist before you rely on your initial reading:

- Open the full treaty package, not just the Convention text. The IRS materials describe the Technical Explanation as an official guide to the Convention and Protocol.

- Check the article discussion, not just the heading. The Technical Explanation says relevant portions of notes, the Memorandum of Understanding, and Agreed Minutes are discussed in the article discussions.

- Confirm you are using the current interpretive layer. Check the March 8, 2004 Understanding, which says it supersedes the earlier understanding tied to the 1992 Convention and 1993 Protocol notes.

- Treat unresolved ambiguity as an escalation item. Ambiguity is a stop signal.

For this edge-case check, confirm the Protocol to the Treaty, the Memorandum of Understanding of 13 October 1993, the U.S. Treasury Technical Explanation, and, where relevant, the March 8, 2004 exchange-of-notes Understanding, which is intended to guide both taxpayers and tax authorities. If your answer changes depending on which interpretive document you read, you do not yet have a filing position.

Build the evidence pack before you claim treaty benefits#

Before you file, build the evidence pack for your treaty position so your conclusion is traceable and reviewable. If your support lives only in memory, email threads, or IRS summary tables, treat the claim as incomplete.

| File element | What to include | Key reference |

|---|---|---|

| Treaty file | Tax Convention with the Netherlands, IRS Netherlands Tax Treaty Documents hub, Technical Explanation, and the exact PDFs used | IRS hub record marker: Page Last Reviewed or Updated 07-Aug-2025 |

| LOB support exhibits | Ownership and entity chart, business-activity summary, and support for the specific LOB test relied on | Article 26 (Limitation on Benefits) |

| Income map | Each payment type mapped to Article 10 (Dividends), Article 12 (Interest), or Article 13 (Royalties), with the underlying agreement or governing document kept in the same file | Applicable income article |

| Double-tax memo | For each relevant income item, state who taxes it, what relief is expected, and which assumptions the filing position depends on | Article 24 and Article 25 |

Start with the treaty file, not a rate table#

Your base file should include the Tax Convention with the Netherlands, the IRS Netherlands Tax Treaty Documents hub, and the Technical Explanation. Keep the Technical Explanation with the treaty text you relied on, because it is the official guide to the Convention and Protocol.

Save the exact PDFs you used and record the IRS hub version date you checked. The hub shows Page Last Reviewed or Updated: 07-Aug-2025, which is a useful record marker. Add a short memo titled "Applied reading of Article 26 (Limitation on Benefits)" that states your eligibility route, supporting facts, and any open uncertainties.

Use IRS treaty tables, including Table 4, as checkpoints only. They are not a complete guide, so your file still needs the treaty text and your reasoning.

Add eligibility exhibits that match your theory#

Your exhibits should match the LOB path you are claiming under Article 26. Use Table 4 as a checkpoint, then confirm your position in the treaty text and Technical Explanation. A practical set often includes:

- Ownership and entity chart

Show direct and indirect ownership, entity types, and jurisdictions for the claim period.

- Business-activity summary

Explain what the business does, where activity happens, and how the income connects to that activity.

- Support for the specific LOB test you rely on

Tie your records to the test you are using, and note any assumptions or open uncertainties.

If another reviewer cannot follow your chart and memo quickly, the file likely needs tightening before filing.

Map each income stream to the right article#

Create an income map for each payment type you are claiming under the treaty. Use Article 10 (Dividends), Article 12 (Interest), or Article 13 (Royalties) as applicable, and tie each stream to its treaty article and LOB analysis.

Do not rely on labels alone. Keep the underlying agreement or governing document for each mapped payment in the same file so classification can be checked.

Add a double-tax memo before filing#

Finish with a short memo anchored to Article 24 (Basis of Taxation) and Article 25 (Methods of Elimination of Double Taxation). For each relevant income item, state who taxes it, what relief you expect, and which assumptions your filing position depends on.

Keep it concise, but make sure the logic for why the same income is not taxed twice is explicit before the return is filed.

Before you lock your LOB position, centralize residency facts and timeline evidence with the Tax Residency Tracker.

Align filing positions and escalation steps with your advisor#

Align on the filing position early. If you and your advisor do not agree on Article 26 (Limitation on Benefits), pause and reconcile the facts before filing or claiming a treaty rate.

Bring a review-ready pack to your preparer before filing. Include your ownership chart, income map, applied reading of the Tax Convention with the Netherlands, and the exact treaty excerpts used from the IRS Netherlands Tax Treaty Documents page. Keep the full IRS document set available, including the Technical Explanation, Protocol, and exchange of notes, so your position is tested against the full context, not just selected text.

Pre-agree the escalation triggers#

Set specialist-review triggers in advance, and escalate if any of these apply:

| Trigger | Why it escalates | Named form or article |

|---|---|---|

| No clearly satisfied LOB test | The facts do not clearly satisfy at least one LOB test, even if the entity is a Dutch BV | Article 26 (Limitation on Benefits) |

| Incomplete withholding certificate file before payment | The withholding position relies on a withholding certificate and support file that were not complete before payment | Form W-8BEN or Form W-8BEN-E |

| Expected treaty-inconsistent taxation | The case may need Mutual Agreement Procedure assistance | Article 29 (Mutual Agreement Procedure) |

For MAP cases, treat timing and submission quality as part of the decision. The treaty labels Article 29 as MAP. IRS guidance says to read the MAP article before requesting assistance. Delays can reduce effective relief, and defective requests may be declined.

If operations and advisor narratives drift apart, do not smooth over the gap in return language. Update the facts memo, retest the treaty position, and then decide whether to file the claim, back off, or escalate.

Sanity checks before you rely on treaty benefits#

Run one final stop-or-go review before filing. If your facts changed and you have not re-tested your path under Article 26 (Limitation on Benefits), do not rely on treaty benefits yet.

- Reconfirm your claim path after any material fact change.

If key facts changed, recheck that your Article 26 position still matches the facts you can document.

- Check interpretation against current IRS treaty materials, not memory.

The Internal Revenue Service treats the Technical Explanation as an official guide to the Convention and Protocol, and its article discussions cover relevant companion materials. Your final review should use the treaty text, Technical Explanation, and current Protocol context together.

- Version-control the companion documents in your file.

Confirm your support file includes the Memorandum of Understanding (13 October 1993) and the attached Understanding dated March 8, 2004. Do not rely only on earlier 1992 or 1993 understanding materials, because the 2004 Understanding states it supersedes prior interpretive material.

- Make your file reviewable by a third party.

State both your eligibility logic and its limits in plain language, with no hidden assumptions, so a reviewer can trace the treaty text, your Article 26 position, and the supporting documents from start to finish.

Final checkpoint: if any key fact is unknown, say so clearly and escalate instead of claiming certainty.

Conclusion#

Use a strict end state: yes, no, or escalate. For this treaty, Article 26 (Limitation on Benefits) is the gate, and if you cannot identify and document the route you meet, you are not ready to claim benefits.

Treat this as two decisions, in order. First, confirm LOB eligibility under Article 26. Then align the claim mechanics with the treaty article for your income and, where relevant, Article 24 (Basis of Taxation) and Article 25 (Methods of Elimination of Double Taxation).

Before filing, lock these three items:

- Finalize your evidence pack

Keep the treaty text, IRS treaty materials, ownership map, activity memo if you are using an active trade or business route, and income-to-article mapping together. If you rely on a route like derivative benefits or discretionary determination, say so directly in your memo.

- Verify against primary treaty materials

IRS treaty tables can support documentation, but they are not a complete guide. Confirm your position against the treaty text, then check the Protocol and Technical Explanation where they affect your route, including the 2004 materials and any later updates.

- Match filing mechanics to the position

If you claim reduced withholding, notify the withholding agent of foreign status and provide Form W-8BEN or Form W-8BEN-E, as applicable. If ineligibility is known, the payor must not apply the treaty rate, so your memo and submitted forms need to align.

If you operate through a Dutch BV, use a conservative default: bring your yes / no / escalate worksheet and evidence pack to a qualified advisor before locking the filing position. The goal is not to maximize claims. It is to file a position you can support end to end with records.

If your final outcome is "claim," standardize payer paperwork early with the W-8 Form Generator.

Frequently Asked Questions

Who can qualify for benefits under the U.S.-Netherlands Income Tax Treaty LOB rules?

Article 26 is the gate. Treaty benefits are available only if the person fits a listed category or test. The text includes expressly listed persons such as individuals and states, plus qualifying routes for certain entities. For companies, residency alone is generally not enough without meeting at least one LOB test.

If I have a Dutch BV, do I automatically get treaty benefits in the United States?

No. A Dutch BV still has to satisfy Article 26 and identify at least one LOB route it actually meets. If you cannot clearly name the route and support it with current facts, treat the position as unresolved and escalate.

What is the fastest first-pass checklist for the qualifying person test?

Run three checks in order: confirm whether you are in an expressly listed Article 26 category, map direct and indirect ownership, and match that map to an actual threshold in the article. Company routes include thresholds such as more than 50% of vote and value, and one Dutch-company route references 30% and 70% ownership thresholds. Some tests also refer to five or fewer companies. If your ownership records are incomplete, stop and resolve that before relying on benefits.

What documents should I keep to support an active trade or business test position?

Keep a short memo that ties the entity’s operating activity to the specific income for which you are claiming benefits. Keep records that support that connection. If the fact pattern looks closer to investment management or otherwise not like active conduct of a trade or business, this route should be reviewed more closely.

When does derivative benefits test analysis become too complex for DIY?

It is usually beyond DIY once you cannot verify key ownership facts or assumptions cleanly. Even detailed practitioner flowcharts still require a full facts-and-circumstances review. If your explanation needs multiple caveats just to hold together, escalate.

How do transparent entities and triangular cases change the risk level?

They increase complexity immediately. The cited practitioner flowcharts explicitly say they do not address treaty eligibility for partnerships or other transparent entities, and they do not address triangular cases under Article 12 (interest) or Article 13 (royalties). That does not prove failure, but it does mean a simplified checklist is not enough.

What parts of my position must be confirmed in the Protocol to the Treaty or U.S. Treasury technical explanation?

First confirm the exact Article 26 route in the treaty text itself. Then confirm whether the Protocol and Technical Explanation clarify or affect how that route applies to your facts. The IRS describes the Technical Explanation as an official guide to the Convention and Protocol, so use the IRS treaty document set as your final checkpoint rather than relying on memory or a third-party summary alone.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Tbilisi Digital Nomad Guide for 2026 Long Stays in Georgia

Start with sequence, not excitement. If your income depends on delivering work on schedule, secure your legal footing, assemble your documents, and keep month one reversible before you optimize comfort.

What Is the Limitation on Benefits (LOB) Clause in a US Tax Treaty?

Treat the Limitation on Benefits, or LOB, article as an upfront eligibility gate, not post-signature fine print. In a U.S. income tax treaty, LOB is there to block treaty shopping. When a treaty includes it, benefits are available only if you satisfy one of that article's tests.