Quick Answer

Map the invoice-to-cash path as named states before scaling automation. Start with DSO, unapplied cash aging, dispute cycle time, and manual touches per invoice, then enforce a strict matching order: exact invoice reference, buyer-plus-amount, then manual review. Require one timestamp, one source record, and one owner for each state from invoice issued to payout eligibility. Expand buyer cohorts only after consecutive periods show lower manual handling and a smaller unapplied backlog.

Why Enterprise Buyer Collections Get Hard at Scale#

Enterprise AR teams are being asked to improve cash conversion and cut manual work at the same time. That sounds reasonable until you're collecting from buyers on terms like 0-90/other days. In that environment, weak AR operations do more than consume staff time. Manual, error-prone workflows can create bottlenecks that delay cash conversion.

The point of AR automation is not just to send invoices faster. It is to collect cash with fewer manual touches and clearer ownership when something breaks.

Start from the operating problem#

Accounts receivable automation uses software and automation to remove repetitive AR work, but the first gain is usually control, not magic. B2B collections are hard in part because extended payment terms push cash receipt further out. Even a healthy customer can look late from your side of the ledger. One invoicing guide notes that 86% of invoices are paid late in its comparison set. Treat that as a reminder that lateness is common, not as a benchmark for your board deck.

If you want this project to work, define your current AR process clearly and mark the manual handoffs. You should know who creates the invoice, how payment details are captured, and who resolves exceptions when payment and invoice data do not match. Use a simple checkpoint: can your team trace a single invoice from issue to payment application without pulling evidence from scattered inboxes, spreadsheets, and side chats? If not, you are still in discovery, not implementation.

A common failure mode is automating the visible front end while leaving manual handoffs in the middle untouched. Teams send invoices faster, but payment application and exception handling still rely on manual review. The result is predictable. More volume enters the pipe, but bottlenecks and delayed cash conversion do not improve enough.

Treat forecasts as background#

You will see plenty of market optimism around AR automation. Treat forecasts as background context, not as the decision signal. Market growth does not tell you whether your process is clearly defined, whether manual handoffs are shrinking, or whether collectors are spending hours each week on avoidable exceptions.

This guide stays focused on operator questions market reports usually skip: what to standardize first, where manual handoffs create risk, which checkpoints prove progress, and what evidence you need before rolling changes out broadly. If you are evaluating AR automation at scale, the real test is not feature count. It is whether your process still holds when payment terms are long and exceptions have clear owners.

The bias here is toward proof. If manual touches fall, matching gets cleaner, and exceptions become traceable, you are moving in the right direction even before every headline metric improves.

For a step-by-step walkthrough, see Accounts Payable vs Accounts Receivable for Freelancers.

Define success before you automate anything#

Define success before rollout by locking the scorecard first; otherwise, automation can look busy without improving operations.

Set the baseline measures before rollout#

Lock four baseline measures and their definitions before launch: Day Sales Outstanding (DSO), unapplied cash aging, dispute cycle time, and manual touches per invoice. DSO measures the average number of days it takes to collect payment after a sale, but it should not stand in for the whole outcome.

Use one scope for all four metrics: same buyer population, same time window. If you measure post-launch manual effort across all invoices but track DSO only on a smaller enterprise cohort, you can create false progress.

Use one decision rule for phase one#

Use one rule up front so phase-one results are clear: if DSO is flat and manual touches drop, treat that as operational progress; if both DSO and manual touches worsen, pause rollout and fix process design before scaling volume.

Keep market momentum in context. External coverage may cite AR automation growth from $3.40 billion in 2025 to $6.57 billion by 2031, but that is context, not proof your operating model is working.

Segment targets by buyer behavior#

Segment targets by buyer behavior instead of relying on one blended average. If cohorts such as BFSI and non-BFSI follow different approval paths, payment timing, or remittance quality, track them separately so you do not compare unlike payment behavior.

A practical checkpoint is trend consistency: the same segment should show fewer touches and cleaner unapplied cash aging across consecutive periods. If the blended number improves while a high-volume enterprise segment worsens, treat that as a red flag.

We covered this in detail in Subscription Billing Platforms for Plans, Add-Ons, Coupons, and Dunning.

Prepare the prerequisite evidence pack and owners#

Do not start build work until the evidence pack exists and named owners accept it. If invoice logic, tax artifacts, and exception rules are scattered across tools, you will automate ambiguity and spend launch untangling it.

Gather the minimum evidence pack#

Build one ledger-linked source of truth before anyone writes rules for e-invoicing or cash application. At minimum, include:

| Artifact | What to keep | Required controls |

|---|---|---|

| Current invoice schema | A real example | Current version; named owner; last-updated date; ledger event it affects |

| Standard payment terms | A real example | Current version; named owner; last-updated date; ledger event it affects |

| Dispute reason list | A real example | Current version; named owner; last-updated date; ledger event it affects |

| Remittance formats you actually receive | A real example | Current version; named owner; last-updated date; ledger event it affects |

| Current API-driven cash application logic | A real example | Current version; named owner; last-updated date; ledger event it affects |

For each artifact, keep a real example plus basic controls: current version, named owner, last-updated date, and the ledger event it affects.

Assign accountable owners before launch#

Set one accountable owner each for e-invoicing, reconciliation, and exception handling. The exact team split can vary, but unresolved ownership is a launch blocker.

Use a short owner matrix so decision rights are explicit for dispute reason changes, remittance parsing behavior, and exception closure evidence.

Confirm policy and tax gates up front#

Confirm which policy gates your program applies by market, who approves changes, and what ledger or audit-trail event proves the gate was met. If you track KYC, KYB, AML, VAT, or audit-log retention controls, document them as implemented in your flow instead of relying on assumptions.

For tax artifacts, document handling for W-8, W-9, Form 1099, FEIE, and FBAR where enabled. FEIE should not sit as a loose checkbox: IRS guidance says a person may qualify only when specific requirements are met, including having a tax home in a foreign country. One route uses the physical presence test of 330 full days during a 12-month period. Those 330 days do not have to be consecutive, the physical presence test applies to U.S. citizens and U.S. residents, and FEIE still requires filing a U.S. tax return reporting the income.

Keep yearly FEIE limits in your evidence model instead of hardcoding a single value: 2025 is $130,000 per qualifying person and 2026 is $132,900 per person, with annual inflation adjustments.

Map the current collection sequence and failure points#

With the evidence pack in place, map the real order of operations before you automate anything else. If Finance Ops cannot show exactly when a transaction moved from invoice issued to payment received, applied, posted, exported, and cleared for payout, AR automation will hide delays instead of fixing them.

Step 1: Trace the sequence as state changes, not team handoffs. Write the path in the same terms your ledger, payment provider, and reconciliation outputs use. Accounts receivable software is meant to manage the journey from invoice creation to cash in the bank, so your map should not end at "buyer paid."

| State | What must be captured | Common break signal |

|---|---|---|

| Invoice issued | Invoice ID, issue timestamp, buyer entity, payment terms, invoice reference sent to buyer | Invoice exists, but the reference format does not match what the buyer returns in payment or remittance |

| Payment received | Payment timestamp, amount, payer identifier, bank or provider reference | Funds arrive with no usable remittance advice or unclear buyer identity |

| Cash application | Match result, applied amount, unapplied balance, reason code if manual review is needed | Partial remittance, short pay, overpay, or ambiguous match in API-driven cash application |

| Ledger posting | Journal reference, posting timestamp, settlement status if relevant | Cash is applied operationally but not posted, or posted to the wrong receivable bucket |

| Reconciliation export | Export file ID, generated timestamp, record count, downstream destination | Applied cash does not appear in the reconciliation export used for close or reporting |

| Payout eligibility | Eligibility status, hold reason if any, release timestamp | Receivable looks complete, but payout is blocked by unresolved exceptions or missing controls |

Your verification checkpoint should stay simple: each state needs one timestamp, one source record, and one accountable owner. If two systems disagree on whether a payment is "applied" or "posted," treat that as a design gap, not a reporting nuisance.

Step 2: Mark where enterprise buyers break the flow. Do not use one generic "exception" bucket. Partial remittance, short pay, overpay, missing remittance advice, and delayed approvals in API-driven cash application create different recovery paths and evidence needs.

A short pay with a clear dispute note is not the same as a short pay with no context. An overpayment should not automatically close multiple open invoices unless buyer instruction is explicit and your accounting treatment is approved. If a buyer repeatedly pays without remittance advice, avoid widening fuzzy matching until it seems to work. That usually trades a visible exception for harder cleanup later.

Annotate the map with the first point where each break becomes visible and the first point where it can actually be resolved. Missing remittance may appear at payment receipt, but resolution may depend on buyer outreach or controlled manual review during cash application. Delayed approvals may sit in the matching layer even after funds are received, which is how teams end up escalating blind.

Step 3: Identify asynchronous points explicitly. If your process relies on provider events and internal updates that do not occur at the same time, document event order from your own logs and reconciliation outputs. Do not assume one clean payment moment.

For unmatched-deposit investigations, require a small evidence pack: provider event or bank reference, account identifier, amount, received timestamp, suspected buyer, and final resolution note. Without that pack, Finance Ops will chase the same item across support, treasury, and engineering.

Step 4: Add checkpoint timestamps that let you prove root cause. DSO measures the average number of days it takes to collect payment after a sale, and high DSO can signal AR process inefficiencies. It will not tell you whether the delay sat with buyer approval, remittance capture, cash application, or ledger posting. State-change timestamps will.

Record when each item entered and exited every key state. Then test the map with a recent sample of successful payments and a recent sample of broken ones. If Finance Ops cannot reconstruct the timeline without asking Engineering to inspect raw logs, your checkpoint design is still too weak.

Related: Finance Automation and Accounts Payable Growth: How Platforms Scale AP Without Scaling Headcount.

Choose the right collection architecture for enterprise buyers#

Choose the architecture that lowers exception cost in your real flow, not the one with the broadest feature list. If remittance quality is weak, tighten controlled rails and reconciliation keys before adding more channels.

Compare models against your failure map#

| Model | Choose when your current map shows | What it can improve | Main tradeoff | Verification checkpoint |

|---|---|---|---|---|

| Direct invoicing plus payment links | Buyers follow invoice instructions and return usable references | Cleaner invoice-to-payment flow and simpler payer path | Faster onboarding can increase exceptions if intake controls are loose | Prove invoice ID, payment reference, and payer identifier remain intact from issue to posting |

| Virtual Accounts | Bank-transfer-heavy behavior and frequent matching ambiguity in your current process | Stronger matching discipline when account assignment and event handling are controlled | More operational setup and review discipline | Test sample deposits and confirm each maps to one buyer record without fuzzy fallback |

| Merchant of Record (MoR) | Your commercial or compliance structure requires a different merchant/seller boundary | Clearer ownership boundaries when responsibility must be separated | More parties and policy gates can increase dispute and settlement complexity | Verify who invoices, who collects, and which records prove the chain end to end |

Do not default to the fastest intake path. Lighter controls up front often shift work to cash application, dispute handling, and close.

Score each option on downstream controls#

Use the same criteria across options: reconciliation completeness, dispute traceability, compliance gating (KYC/KYB/AML), and cross-border readiness (including North America and Asia-Pacific contexts). Keep the scoring method consistent so tradeoffs are visible.

Recent 2026 comparison content is useful for market scanning, but it is not architecture proof. For example, one guide frames 5 solutions, another shows 12 platforms, and comparison formats include dimensions like implementation timelines and speed to value. That helps scope options; it does not validate outcomes for your buyer mix.

Prioritize reconciliation completeness first. If you cannot reliably connect payment to buyer, invoice, and ledger records, scale will amplify exceptions.

Keep unknowns explicit#

Document three unknowns early: vendor-level win rates, verified implementation timelines, and ROI comparability. The cited comparison excerpts do not establish those as audited, like-for-like results.

Final check: run recent successful payments and recent exceptions through the proposed model on paper. If you cannot show the full path from invoice to payment, application, posting, and compliance-cleared status with named records, the architecture choice is not ready.

If you want a deeper dive, read Accounts Receivable Management for Platforms: How to Collect from Buyers While Paying Sellers Fast.

Implement step 1 with invoice and payment capture controls#

After you choose the collection model, lock invoice and payment-capture controls before expanding buyer coverage. If references do not persist from invoice creation to ledger posting, automation scales exceptions instead of collections.

| Step | Focus | Checkpoint |

|---|---|---|

| Step 1 | Standardize invoice creation and payment intent capture | Each invoice should trace to its payment event and posted ledger entry without manual reconstruction |

| Step 2 | Enforce single-outcome handling for retries and late confirmations | Replay the same confirmation in non-production and verify there is no duplicate cash posting, no second invoice closure, and no duplicate journal entry |

| Step 3 | Add pre-send acceptance checks for e-invoicing and remittance readiness | Keep an audit trail for failed acceptance checks, including payload, buyer account, rejection reason, and corrected resend record |

| Step 4 | Publish a daily control report and phase by buyer volume | Run a daily control report by enterprise account for failed payment captures, missing references, and invoice-payment-ledger status mismatches |

- Step 1 Standardize invoice creation and payment intent capture

Use one required record path from the signed commercial record to invoice, payment request, cash application record, and final journal entry. The same buyer identifier and invoice reference should carry through the contract-to-cash flow without spreadsheet rekeying. If your CRM-to-ERP flow still depends on exports, fix that handoff first, because integration depth and ERP compatibility affect outcomes.

Check it with a recent sample: each invoice should trace to its payment event and posted ledger entry without manual reconstruction.

- Step 2 Enforce single-outcome handling for retries and late confirmations

Set the operating rule early: one business event should produce one posting outcome, even when confirmations arrive late, duplicated, or out of order. In non-production, replay the same confirmation and verify there is no duplicate cash posting, no second invoice closure, and no duplicate journal entry.

This is where early control discipline matters: status mismatches across invoice, payment, and ledger records create avoidable manual cleanup.

- Step 3 Add pre-send acceptance checks for e-invoicing and remittance readiness

Before scaling sends, verify each buyer cohort can accept your e-invoicing output and return usable remittance detail. Focus on preventing predictable rejects by checking required invoice data and reference fields before send, especially for high-volume enterprise accounts.

Keep an audit trail for failed acceptance checks, including payload, buyer account, rejection reason, and corrected resend record.

- Step 4 Publish a daily control report and phase by buyer volume

Run a daily control report by enterprise account for failed payment captures, missing references, and invoice-payment-ledger status mismatches. Use it as the step-1 operating checkpoint.

If capacity is limited, roll out controls to highest-volume buyer cohorts first rather than the most vocal internal stakeholder.

Related reading: Best Platforms for Creator Brand Deals by Model and Fit.

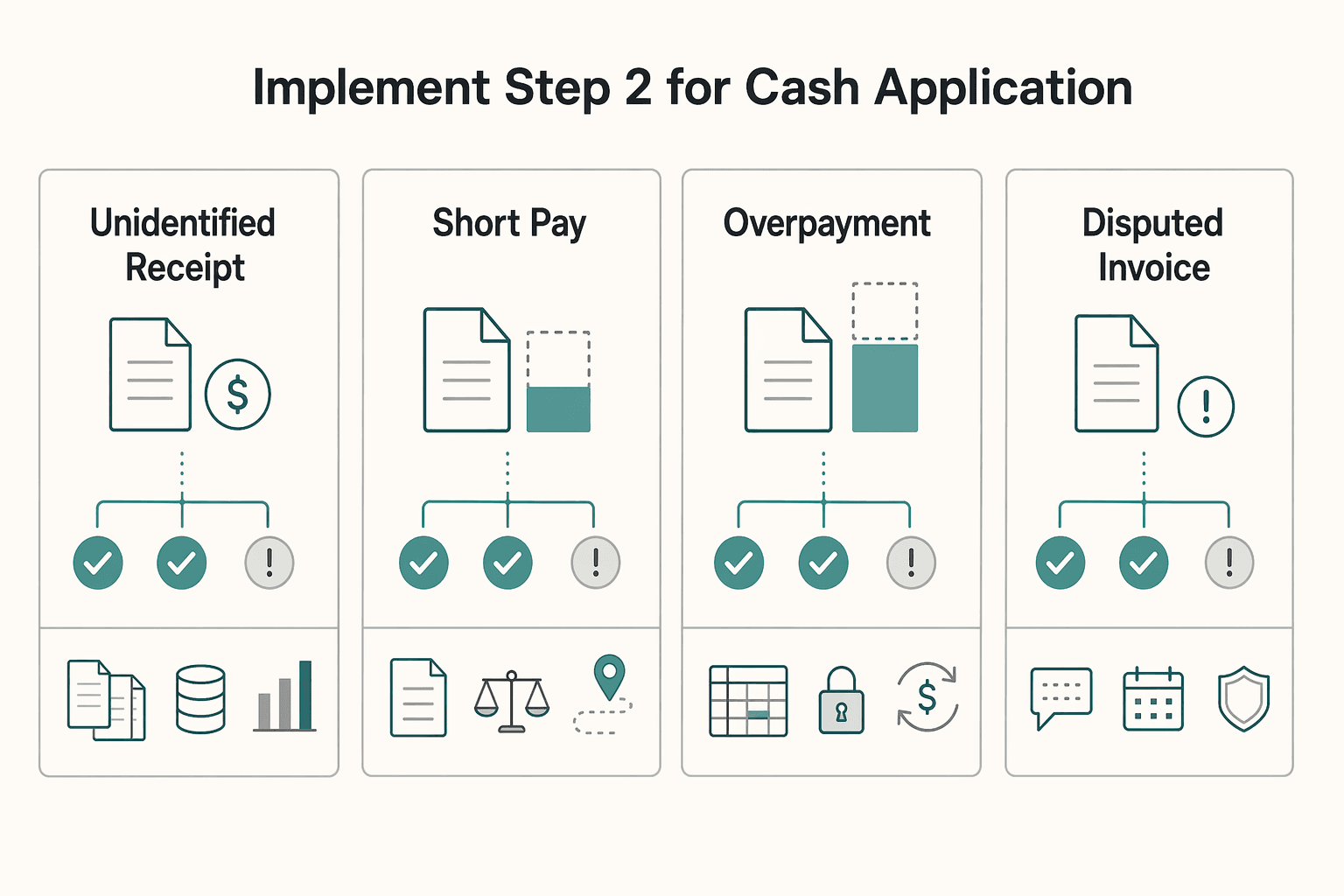

Implement step 2 for cash application, reconciliation, and exception queues#

Step 2 should make cash application explainable at scale: keep auto-matching strict, define exception handling clearly, and avoid moving downstream settlement faster than receivable states can support.

Step 1. Set a strict auto-match order before automated posting. Use one clear hierarchy for API-driven cash application: exact invoice reference first, buyer account plus amount second, then manual review. Treat unapplied cash as safer than a confident misapplication, and log the match reason so operators can verify why each receipt posted.

Step 2. Define exception classes with clear recovery paths. AR automation works best when repetitive work is automated and exceptions are easy to action.

| Exception class | Owner | SLA basis | First recovery action | Closure evidence |

|---|---|---|---|---|

| Unidentified receipt | Finance Ops cash application | From receipt credit date | Check invoice reference, buyer account, and remittance details; keep unapplied if unresolved | Supporting remittance or buyer confirmation, posted application entry, closed investigation note |

| Short pay | Collections or dispute owner | From variance detection date | Compare payment to invoice, terms, credits, and deductions; request buyer reason | Approved deduction or correction record, updated balance, dispute/adjustment record |

| Overpayment | Finance Ops with accounting approval | From overage detection date | Check for related open invoices before carry-forward or refund | Reallocation or refund approval, ledger entry, buyer communication record |

| Disputed invoice | Collections or account owner | From dispute intake date | Pause collection pressure and gather invoice/approval/delivery records | Dispute outcome, corrected invoice or reinstatement, auditable approval trail |

Route these queues through systems tied to your ERP, CRM, and payment flow so reporting and accountability stay intact.

Step 3. Reconcile payment, application, and ledger views on a fixed cadence. Reconcile wallet or payment-rail credits against cash application status and ledger postings daily if your operating model can support it. Track timing gaps separately from true breaks, and flag unresolved gaps before month-end close.

Step 4. Gate payout execution on receivable finality. Use Payout Batches only when receipt application and key exception states are resolved enough to avoid cascading corrections. If cash is still in exception review, keep it out of downstream payout logic.

Step 5. Hold a scale gate before expanding buyer coverage. Expand only when unapplied cash backlog and manual-touch rates trend down across consecutive operating periods. If either metric stalls or worsens, fix matching or exception design before adding volume.

You might also find this useful: Accounts Receivable Turnover for Platforms: How to Measure Collection Efficiency.

Implement step 3 for compliance, tax, and payout dependencies#

Do not release payouts until both compliance status and tax readiness are clear in the payout record. Cash can be fully applied in AR and still be blocked for valid compliance or tax reasons, so treat these as payout dependencies, not cleanup tasks.

Gate payout on named compliance states#

If your program uses identity reviews, AML checks, or market-specific policy controls, connect those statuses directly to payout eligibility. Keep the hold reason code, opened timestamp, current owner, and last review action in the same record as the payout decision.

Use a simple control test: for any blocked payout, the reason should be visible without email, chat, or side spreadsheets. If Finance sees funds as ready while Compliance tracks an unresolved hold elsewhere, your control is not reliable.

Validate tax readiness with current-year FEIE checkpoints#

Do not mark a payee as tax-ready from old onboarding data alone. Where FEIE-related handling applies, keep the IRS checkpoints explicit in your workflow.

| FEIE checkpoint | What to verify in operations |

|---|---|

| Qualifying basis | The person is treated as a qualifying individual with foreign earned income and a foreign tax home. |

| Reporting rule | Excluded foreign earned income is still reported on a U.S. tax return. |

| Physical presence test | 330 full days in a 12-month period; qualifying days do not have to be consecutive. |

| Current-year limit use | Use current limits: $130,000 (2025) and $132,900 (2026) per qualifying person. |

| Housing limitation reference | Generally 30% of the FEIE maximum; IRS cites $39,000 (2025) and $39,870 (2026). |

If you also collect W-8/W-9 documents or track Form 1099, keep them in the same readiness check, but do not treat document collection as a substitute for eligibility review.

Route blockers to named owners and confirm coverage before promising timing#

When collection-to-payout flow stops, route by blocker type with named owners and documented turnaround expectations. Define recheck triggers so holds reopen only when new evidence arrives.

For global programs, confirm market and program coverage before committing to payout timing. Extending a stated timeline is usually cheaper than unwinding funds after a late compliance or tax failure.

Conclusion#

AR automation can pay off when you treat it as an operating change, not a market story. The category is growing in multiple forecasts, but forecast inputs vary across providers. Your go or no-go decision should rest on process evidence: can you move from invoice generation through payment collection, cash application, and reconciliation with fewer errors and fewer manual touches?

| Checklist item | What to confirm | Warning sign |

|---|---|---|

| Confirm baseline metrics | Every metric needs a named source, refresh cadence, and owner | You cannot reproduce the baseline two weeks later from the same records |

| Finalize the evidence pack | Trace a single payment end to end and confirm the same references survive each handoff | Invoice data sits in one tool, remittance arrives by email, and reconciliation logic lives in a spreadsheet no one formally owns |

| Validate the architecture before you buy the narrative | Test payment identification or routing options against actual remittance samples and bank statement patterns | A faster launch path can create more unmatched cash and more operator rework later |

| Deploy in phases and protect the ledger | Start with a defined buyer cohort, ideally one with meaningful volume and known payment behavior | Expanding before clear posting controls and exception handling are in place |

| Hold the scale gate until the trend is real | Wait for consecutive operating periods where reconciliation accuracy is improving and manual workload is falling | Unapplied cash grows, billing mistakes rise, or payment tracking gets harder |

Use this as your final launch checklist, and do not move to broad rollout until each step has evidence behind it.

- Confirm baseline metrics.

Lock your starting numbers for DSO, unapplied cash aging, manual touches per invoice, and dispute cycle time. The checkpoint is simple: every metric needs a named source, refresh cadence, and owner. If you cannot reproduce the baseline two weeks later from the same records, you are not ready to judge improvement.

- Finalize the evidence pack.

Gather invoice schemas, buyer reference fields, remittance formats, payment terms, dispute reasons, and the ownership map across Finance Ops, Product, and Engineering. A useful verification step is to trace a single payment end to end and confirm the same references survive each handoff. A practical risk is fragmented evidence, where invoice data sits in one tool, remittance arrives by email, and reconciliation logic lives in a spreadsheet no one formally owns.

- Validate the architecture before you buy the narrative.

Decide how invoices are issued, how payments will be identified, and how reconciliation will work when data is late, partial, or missing. If you are considering different payment identification or routing options, test them against actual remittance samples and bank statement patterns rather than vendor positioning. The tradeoff to watch is speed versus cleanup cost: a faster launch path can create more unmatched cash and more operator rework later.

- Deploy in phases and protect the ledger.

Start with a defined buyer cohort, ideally one with meaningful volume and known payment behavior. Put clear posting controls and exception handling in place before you expand, because manual AR is already associated with slow payment cycles and tracking errors. If you work across markets, also check e-invoicing requirements early; Mordor notes mandatory rules are active in more than 80 jurisdictions, which can affect invoice acceptance before collections even begin.

- Hold the scale gate until the trend is real.

Expansion should wait for consecutive operating periods where reconciliation accuracy is improving and manual workload is falling. DSO may lag, and that is not automatically failure. But if unapplied cash grows, billing mistakes rise, or payment tracking gets harder, pause and fix the design before you add more volume.

That discipline matters more than any headline about AR automation at scale. The practical win is not that the market is expanding. It is that your team can prove cleaner collections with evidence, not hope.

Frequently Asked Questions

What improves first in enterprise AR automation: DSO, manual workload, or both?

There is no universal sequence. Teams often target both manual workload and DSO, but which one moves first depends on where delays actually sit, including internal processing versus buyer payment behavior.

Why do many teams rate AR automation as critical but still remain early-stage?

Because the pressure is real, but the hard work sits in integration and ownership. Billtrust cites research showing 95% of leaders feel more pressure than ever to ensure steady cash flow, and its buyer guidance focuses on AI maturity, ERP compatibility, and integration depth because those factors can affect outcomes. For enterprise organizations with 500+ employees, a common red flag is stitching together disconnected point solutions and ignoring gaps in ERP-native tools.

Which manual bottlenecks show up most often across invoicing, collections, payments, and reporting?

This grounding pack does not rank a universal list of bottlenecks across those workflows. What it does support is that ERP-native gaps and disconnected point solutions create manual handoffs and rework, so those are practical places to inspect first.

How should we interpret different market forecasts from Grand View Research, Mordor Intelligence, and MarketsandMarkets?

Do not rely on those forecast comparisons as the core approval case here. The stronger lens is criteria-based: AI maturity, ERP fit, integration depth, and total cost of ownership beyond license fees.

When should we choose Virtual Accounts versus standard invoice payment links?

This research set does not provide a neutral head-to-head result, so avoid a blanket recommendation. Choose based on your own payment mix and reconciliation pain, then validate with internal exception data before committing.

How much AI in AR is deployed versus still being evaluated, and what does that mean for rollout plans?

Do not assume mature AI is already standard across the market. For rollout planning, verify each vendor's current AI maturity, ERP compatibility, and integration depth, then scale based on what is proven in your environment.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- congress.gov/bill/119th-congress/senate-bill/1071/text/eahtrusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- leginfo.ca.gov/pub/03-04/bill/sen/sb_0551-0600/sb_600_bill_...trusted

- obamawhitehouse.archives.gov/sites/default/files/omb/assets/egov_docs/fea...trusted

- reginfo.gov/public/jsp/Utilities/FEA_CRM_v23_Final_Oct_2...trusted

- sec.gov/Archives/edgar/data/1607939/0001607939260000...trusted

- billtrust.com/resources/blog/what-are-the-best-accounts-re...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Accounts Receivable Management for Platforms: How to Collect from Buyers While Paying Sellers Fast

**Treat AR for a platform as a payout control problem, not just a collections task.** If you separate buyer collections from seller payouts, you risk releasing funds based on a status your ledger cannot actually support.

How Platform Teams Scale AP Volume Without Adding Headcount

Use this as a decision list for operators scaling Accounts Payable, not a generic AP automation explainer. In these case-study examples, invoice volume can grow faster than AP headcount when the platform fit is right, but vendor claims still need hard validation.

Accounts Receivable Turnover for Platforms to Measure Collection Efficiency

Accounts receivable turnover can help a platform measure collection efficiency, but only when you read it against cash timing. A higher [`Accounts Receivable Turnover Ratio`](https://www.netsuite.com/portal/resource/articles/accounting/accounts-receivable-turnover-ratio.shtml) usually points to faster collections and stronger cash flow. On its own, though, it does not tell you everything about collection health.