Quick Answer

Start with your own baseline and choose by operating conditions, not product demos. Keep manual AP only when invoice volume is low, approvals are stable, and exceptions stay rare; move to selective automation when reconciliation and rework begin dominating team time; adopt broader automation when payout-heavy, cross-border flows strain controls. For marketplace operators, the decision turns on total process cost, ERP mapping quality, and whether API retries and webhook status updates stay traceable end to end.

AP automation vs manual processing for marketplace operations#

For marketplace operators, this is not a generic AP explainer. The real choice is whether you should stay with manual AP, move to rules-based automation, adopt AI-powered automation, or run a staged hybrid while volume, controls, and integrations catch up.

The goal is practical: you should leave with a cost-benefit method you can actually use, a few decision checkpoints that help you kill bad tool purchases early, and a sensible adoption sequence across finance, ops, and engineering. The right answer is rarely "automate everything now." In a marketplace, complexity shows up unevenly across approvals, payout handling, reconciliation, and exception queues. Your operating model has to match where the pain actually sits.

A simple starting rule helps. If your AP work is mostly clean invoices, predictable approvals, and low exception volume, manual steps may still be acceptable for a while. If your team spends more time chasing mismatches, rekeying data into ERP systems, or repairing approval gaps than reviewing spend quality, automation deserves a serious look. Automation usually delivers more value as complexity grows, but treat that as a directional signal, not proof for your marketplace.

Scope matters. Use your own baseline to test how invoice quality, exception rates, ERP fit, and cross-border compliance needs affect outcomes in your environment. A setup that looks efficient in a demo can fail in production if invoices arrive in inconsistent formats, approvers work outside the expected path, or ERP mapping is already brittle.

Before you trust any ROI claim, verify your own baseline from AP logs, ERP exports, and ledger journals. Check current cycle time, manual touches per invoice, rework hours, close delays, and the share of transactions that need human review.

The early evidence buyers see is mixed. TeamPay frames manual AP as inefficient, expensive, and error-prone. Infinite IT says the burden of manual AP rises as businesses grow. Latenode, in a comparison published on February 12, 2026, positions AI tools as better suited to diverse invoice formats than rigid templates. Ardent Partners is more useful as benchmark context, but even there the 2025 eBook is based on 212 AP professionals and explicitly discloses sponsorship.

That does not make the material useless. It means you should treat vendor and analyst content as directional input, then pressure-test it against your own data and approval reality.

Keep one red flag in mind from the start. Automating bad intake or weak ERP mappings can speed up the creation of cleaner-looking errors. If you cannot trace an invoice from receipt through approval to journal entry and payment status today, fix that visibility first. The next sections compare the three paths directly, then show how to model cost, control, and implementation risk without hand-waving.

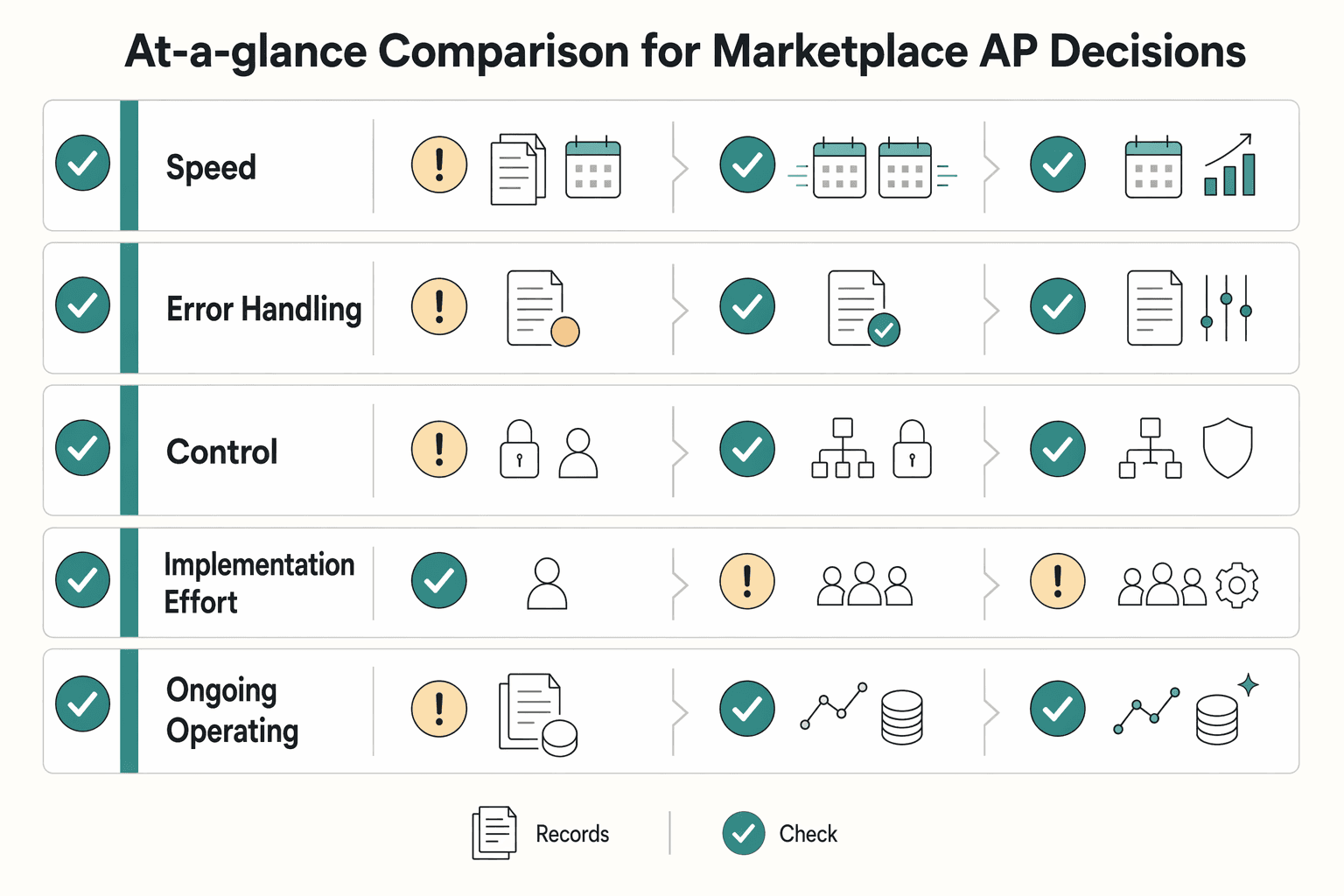

At-a-glance comparison for marketplace AP decisions#

For most marketplace operators, manual AP is only defensible when volume is low, approvals are simple, and exceptions stay rare. Rules-based automation is usually the first practical upgrade. AI is most useful when document variety and exception triage are the main bottlenecks.

| Decision area | Manual AP processing | Rules-based AP automation | AI-powered AP automation |

|---|---|---|---|

| Speed | Slowest when multiple sign-offs are required, especially when work moves across inboxes and spreadsheets. | Faster for structured intake, routing, and matching when fields and approval paths are predictable. | Fast on mixed-format intake and classification, if review rules are already clear. |

| Error handling | Humans can catch odd cases, but manual keying and duplicate checks weaken under load. | Built-in validation can catch errors before they escalate. | Better at reading varied documents, but low-confidence or policy-breaking items still need human review. |

| Control and approvals | Depends on team discipline and consistent recordkeeping. | Stronger when approval rules and validation checks run before posting to ERP. | Can expand coverage, but finance still needs clear exception ownership and review logic. |

| Implementation effort | Lowest upfront change, highest long-term staff effort. | Medium lift: rule design, ERP mapping, and exception ownership. | Highest lift: model behavior checks, confidence thresholds, and extraction-quality monitoring. |

| Ongoing operating load | High ongoing manual effort in chasing, rekeying, and cleanup. | Moderate: effort shifts to exception review and rule maintenance. | Moderate to high: fewer touches on clean items, but monitoring and drift review add work. |

| Payout complexity and payout batches | Often where manual systems break first as payout volume rises. | Works when payout files, approval logic, and reconciliation rules are structured. | Can improve intake quality, but does not replace payout execution controls. |

| Cross-border handling | Heavy manual burden for payee data completeness and jurisdiction-specific checks. | Better for required-field checks and routing incomplete submissions before payment. | Useful for document capture, but compliance outcomes still depend on explicit rules and review queues. |

| Traceability via ledger journals | Traceability is often reconstructed after the fact from multiple systems. | Better when approval/payment status is captured consistently and tied back to ERP records. | Same dependency, with more pressure on clear exception paths and auditability. |

| Engineering lift (API, Webhooks, idempotency, ERP connector depth) | Minimal integration lift, but weak system-to-system reliability. | Depends on API/Webhooks maturity and ERP connector depth; idempotency behavior should be verified for retries. | Same integration dependencies as rules-based, with tighter testing needs around retry safety and state sync. |

| Compliance pressure (KYC, KYB, AML, VAT, W-8/W-9/1099) | Highest manual burden for collecting and checking tax and compliance data. | Better for document presence checks, required-field gates, and policy routing. | Helps with intake, but legal responsibility remains with your process; requirements vary by jurisdiction and program. |

The main separator is not demo performance but whether your controls are structured enough to trust automation in production.

Two practical checks matter most. First, verify idempotency behavior on API paths that create or update payment records so retries do not create duplicates. Second, verify Webhooks push real-time status updates into the same records finance uses for reconciliation, without orphan states between provider events and ERP or ledger-journal entries.

Compliance load remains real after automation. Form W-9 is used to provide a correct TIN to payers filing information returns, Form W-8 BEN is submitted when requested by a payer or withholding agent, and Form 1099-NEC sits in the nonemployee compensation reporting path. Add VAT checks where relevant and beneficial-owner identification where CDD controls apply.

Use exception rate as a decision lens, not just cycle time. A cited Ardent summary reports 9% invoice exception rates for top-performing AP teams versus a 22% industry average.

Plain-language verdict: keep manual if your flow is still low-volume and stable. Automate selectively when pain is concentrated in intake, approvals, or reconciliation. Move toward full automation when document variability and recurring exceptions are high and your team can support reliable API, Webhook, and ERP alignment.

Related: MoR vs. PayFac vs. Marketplace Model for Platform Teams. If you want a quick next step, try the free invoice generator.

Where manual AP still works and where it breaks#

Manual AP is usually workable only in a narrow operating window: low invoice volume, low exception rates, simple approvals, and limited payout paths. If your team can receive invoices, verify details, and enter them into ERP without recurring rework, manual can still be a practical short-term choice.

| Signal | Condition in article | Article consequence |

|---|---|---|

| Low invoice volume | Manual AP is usually workable only in a narrow operating window: low invoice volume | Manual can still be a practical short-term choice |

| Low exception rates | Manual AP is usually workable only in a narrow operating window: low exception rates | Manual can still be a practical short-term choice |

| Simple approvals | Manual AP is usually workable only in a narrow operating window: simple approvals | Manual can still be a practical short-term choice |

| Status rebuilt from inboxes, spreadsheets, and ERP notes | Payment and approval status has to be rebuilt from inboxes, spreadsheets, and ERP notes | Manual work is already costing you twice |

| Cycle time toward a week or longer | If cycle time trends toward a week or longer | Manual is no longer the low-cost path |

| Close depends on spreadsheet rollups | If close depends on spreadsheet rollups | Manual is no longer the low-cost path |

It breaks when handling effort shifts from processing to chasing. Rising invoice variance, broader supplier mix, failed approvals, and delayed reconciliation turn basic entry into follow-up work. When payment and approval status has to be rebuilt from inboxes, spreadsheets, and ERP notes, manual work is already costing you twice, and spreadsheet-heavy controls add real output-error risk.

Use a simple decision rule: if exception handling and reconciliation consume more time than higher-value review and analysis, automate intake and approvals first. Track AP cycle time as the elapsed time from invoice receipt to payment transmission, and track how often work happens outside ERP. If your cycle time trends toward a week or longer, or close depends on spreadsheet rollups, manual is no longer the low-cost path.

Risk exposure also changes as you scale. Manual data entry is a common root cause of duplicate payments, and duplicated or erroneous disbursements are often cited in the 1% to 2.5% range annually. If you introduce event-driven updates later, treat duplicate delivery as expected behavior and design retries with idempotency keys plus deduplication controls.

Build a real cost-benefit model before you buy#

Build the model on total AP process cost per invoice, not a simple software-fees-versus-headcount comparison. For marketplace operators, the useful comparison includes implementation drag, exception handling, and the control work that remains after automation.

A practical starting point is that labor is often the largest AP cost bucket, and manual intervention is usually the driver. One benchmark puts labor at 62% of total AP costs, so focus on how many invoices still require human intervention after launch.

Build the TCO before the ROI story#

Start with a simple TCO structure, then pressure-test savings against it.

| Cost bucket | What to include | What operators often miss |

|---|---|---|

| Implementation | Vendor setup, internal project time, employee training, workplace disruption | Productivity loss while teams change approval flows and run interim processes |

| Integration | Process mapping, data migration, ERP integration, third-party connections, test cycles | Finance and engineering rework after go-live when mappings drift |

| Operations | Admin effort, queue monitoring, human review of low-confidence captures, supplier follow-up | Ongoing review cost when extraction cannot support straight-through posting |

| Exception rework | Missing fields, failed extraction, duplicate payment recovery work, approval retries | AP research and correction entries after payment or posting errors |

| Control and compliance | AML policy review, internal controls, independent testing support, VAT validation checks | Recurring policy and control labor after intake and approvals are automated |

Two lines need explicit treatment. First, extraction is probabilistic: confidence scores run from 0 to 100, so you need clear thresholds for auto-accept and a human-review path for low-confidence or missing-key outcomes. If you do not model that queue, labor just shifts; it does not disappear.

Second, compliance work changes shape rather than disappearing. AML remains risk-based and still requires formal controls and independent testing. For cross-border VAT checks, VIES is a search engine across national databases, so budget for failed checks, follow-up, and policy review.

Put uncertainty in the model on purpose#

A defensible model includes explicit unknowns. Add uncertainty lines for timeline risk, ownership gaps between finance and engineering, and data-quality constraints from the current manual process.

Before signing, verify whether your existing AP records can support the model inputs you are using, including receipt, approval, payment, exception, and posting signals. If that baseline is incomplete, increase the uncertainty buffer instead of forcing precision.

Validate savings against your own evidence#

Before approval, reconcile projected savings to baseline evidence from ledger journals and AP logs:

| Baseline measure | Definition in article | Evidence noted |

|---|---|---|

| Current cycle time | From invoice receipt to payment transmission | Ledger journals and AP logs |

| Rework hours | Exceptions, approvals, and reconciliation | Ledger journals and AP logs |

| Month-end close delays | Caused by off-ERP tracking | Ledger journals and AP logs |

| Low-confidence capture rate | Manual review volume from any pilot | Any pilot |

Manual invoicing can stretch to 90 days in some organizations, while others already run faster. Your baseline determines the upside. If savings do not map to fewer rework hours, shorter close delays, or fewer off-ERP touches, the case is not ready.

For a step-by-step walkthrough, see Comparables Analysis for Business Valuation in a One-Person Business.

Control and compliance tradeoffs operators cannot ignore#

Your cost-benefit model breaks if you underprice control work. For growing marketplace operators, policy-gated automation is usually stronger than pure manual approvals, but only when you design for evidence, exception handling, and clear compliance ownership instead of just faster payouts.

| Control area | Manual approvals | Policy-gated automation |

|---|---|---|

| Approval logic | Reviewer judgment sits in email, chat, and memory, so it is hard to prove why one payment passed and another did not. | Rules can enforce required fields, approval thresholds, and hold reasons before release, especially when each decision writes to audit logs and ledger journals. |

| Evidence trail | Records are often split across inboxes, spreadsheets, and ERP notes, making audit retrieval slow and incomplete. | Stronger model: one evidence chain linking source invoice, approval history, provider reference, and final journal entry. |

| Exception handling | Teams can catch unusual cases by feel, but queues become inconsistent as volume grows. | Strong when low-confidence, missing-tax-form, or failed-verification cases are routed to review; weak when exceptions are hidden or auto-cleared. |

The core tradeoff is control quality, not just speed. Manual review can work early, but it creates audit debt when evidence is fragmented. Automation can reduce that debt by keeping approval history, provider references, and ledger journals in one traceable path. Still, ledger immutability alone is not sufficient: you must retain supporting records long enough to substantiate income, deductions, and reporting.

Compliance work moves upstream, not away#

Automation does not remove AML duties where your program is tied to regulated banking or payout partners. CIP requirements are risk-based, and AML programs for covered banks still require internal controls, testing, compliance ownership, and training. If you onboard business payees, beneficial ownership verification for legal-entity customers can still apply. In practice, the work shifts from end-of-line manual checks to earlier identity, ownership, and policy gates.

| Requirement | What the article says | Scope |

|---|---|---|

| CIP requirements | Requirements are risk-based | Program tied to regulated banking or payout partners |

| AML programs | Still require internal controls, testing, compliance ownership, and training | Covered banks |

| Beneficial ownership verification | Can still apply | Legal-entity customers |

| Form W-9 | Used to provide a correct TIN for IRS information returns | Tax workflow |

| Form W-8 BEN | Used to certify foreign status when requested by a payer or withholding agent | Tax workflow |

| Form 1099-NEC | Obligations do not disappear because invoice intake is automated | Tax workflow |

| FBAR | A U.S. person may have a filing obligation if foreign accounts exceed $10,000 in aggregate during the year | Cross-border edge case |

| FEIE | AP software does not decide FEIE outcomes; the 2026 maximum exclusion is $132,900 per qualifying person | Cross-border edge case |

Tax workflows follow the same pattern. Form W-9 is still used to provide a correct TIN for IRS information returns. Form W-8 BEN is still used to certify foreign status when requested by a payer or withholding agent. Form 1099-NEC obligations do not disappear because invoice intake is automated. Cross-border edge cases remain: a U.S. person may have an FBAR filing obligation if foreign accounts exceed $10,000 in aggregate during the year, and FEIE outcomes are not decided by AP software even though the 2026 maximum exclusion is $132,900 per qualifying person.

Failure modes worth designing around#

The highest-risk setup is fast payout routing with weak gates. That is how payments move before a missing W-9, unresolved identity check, or ownership mismatch is reviewed. The second failure mode is a weak exception queue: cases age without clear ownership or release rules, and teams bypass controls to keep payouts moving.

Use a strict audit checkpoint. For a paid transaction, confirm you can retrieve the invoice, approval trail, provider reference, ledger journal, tax form on file, and exception disposition without rebuilding the timeline from email. If you cannot, the system is moving money faster than it is producing defensible evidence.

When volume expands across jurisdictions, prioritize control-first design over marginal speed gains. A one-day delay with a clean evidence pack is usually cheaper than a same-day payout you cannot defend.

Integration design choices that decide success or failure#

Integration depth usually determines whether AP automation stays reliable at scale. A shallow connector can work for simple invoice intake, approvals, and payouts. If you need dependable status sync, event tracing, and clean ERP posting, a deeper API integration is the stronger path.

Make the operating sequence explicit: invoice capture, validation, approval routing, payment execution, webhook status updates, then ERP reconciliation. Two checkpoints should happen before final posting: imported invoices should enter workflow routing, and pre-posting validation should run when your ERP supports it. In Dynamics 365 Finance, imported invoices can be auto-submitted to workflow and posting can be simulated before a vendor invoice is posted.

| Criteria | Shallow connector setup | Deeper API implementation |

|---|---|---|

| Time to launch | Faster when approval logic and ERP mappings are simple | Slower upfront because engineering must define request handling, event ingestion, and reconciliation logic |

| Retry safety | Limited visibility into retry behavior | Can use idempotent requests so retries do not create duplicate side effects |

| Status tracking | Basic sync may be enough at low complexity | Better when webhooks must keep local state aligned with provider-side events |

| Reconciliation quality | Can be acceptable for simpler payable flows | Stronger when you need event-level observability tied to ledger journals and ERP records |

| Operator fit | Early-stage or low-variance AP | Higher-volume or payout-heavy operations |

Architecture choices also shape outcomes. Virtual accounts, where supported, can be created by API to receive inbound funds and automatically route them to a parent account. On outbound flows, payout scheduling controls can support batch routing or timed releases, but schedule options can differ by account type and jurisdiction. If you use a Merchant of Record structure where enabled, the MoR is the entity legally responsible for processing customer payments, so your account and ERP mappings should reflect that legal setup.

Use strict verification checkpoints:

- No orphan states: For any paid transaction, confirm provider event status, local platform status, and ledger journal state all match.

- Deterministic retries: Retry the same payment request with the same idempotency behavior and confirm no second payout is created.

- Clear exception ownership: If webhook handling or journal creation fails, route the case to a named owner and queue.

If you cannot trace one payment from API request to webhook event to ledger journal without manual reconstruction, the integration is not ready for scaled automation.

What to execute in the first 90 days#

Do not treat AP automation as a big-bang cutover. Execute it in phases with explicit go/no-go gates. Start with baseline and design, run a controlled pilot, then scale only after production proof.

Use the documented seven-step implementation structure as a practical gate framework across three operating phases so finance, ops, and engineering stay aligned on what must be true before expansion.

| Phase | What you do | Primary owner | Go or no-go checkpoint |

|---|---|---|---|

| Baseline and design | Document current manual AP steps, approval rules, exception queues, and month-end evidence requirements. Define how API requests, Webhooks, and ERP posting are validated before live use. | Finance for policy and approvals, Engineering for technical design | Go only when approval rules are signed off, exception ownership is named, and retry plus deduplication behavior is testable |

| Controlled pilot | Run a partial, time-limited pilot with limited invoice and payout volume (canary-style), and compare outcomes against your baseline. | Ops for live handling, Engineering for reliability | Go only if manual touches decline, exception aging improves, close evidence is cleaner, and payout status tracking stays aligned |

| Scaled rollout | Increase exposure in tiers after the pilot proves itself in production. | Cross-functional | Go only when pilot metrics remain stable and no orphan states appear between provider events, local status, and ERP records |

Keep ownership explicit. Finance owns policy, approval rules, and close-evidence requirements. Ops owns exception SLAs, queue triage, and fallback handling when automation is paused. Engineering owns API and Webhook reliability plus ERP reconciliation, including protection against duplicate webhook deliveries and duplicate side effects from retried requests.

Define pilot acceptance criteria in operational terms: fewer manual corrections before approval or posting, faster exception resolution, cleaner close evidence linking invoice-to-approval-to-provider event-to-ERP entry, and stable provider/internal status sync.

Plan containment before launch. If the pilot shows duplicate state changes, reconciliation gaps, or payout status drift, stop expansion and route the affected cohort through a defined manual path. Document what pauses, what still posts, who reviews exceptions, and how already processed items are separated from items returned to manual handling.

Choose manual, selective automation, or full automation#

Choose based on operational risk, not preference: stay manual only while variance is low and controls hold, move to selective automation when exceptions and approval drag grow, and move to full automation when cross-border, payout-heavy complexity becomes the main failure point.

| Path | Choose it when | What must be true |

|---|---|---|

| Manual AP processing | You are early stage, invoice patterns are stable, and humans can still verify entries, approvals, and payment release without constant rework | Strict approval rules, documented payment-release steps, and month-end evidence that ties invoice, approval, and ERP posting |

| Selective automation | Variance is rising, approvals are slowing, or manual entry is creating avoidable errors | Automate intake and approval routing first, using strict rules and approval workflows before broader payment automation |

| Full automation | You are payout-heavy, operate across borders, or need programmatic money movement at scale | Deep integration, reliable ERP reconciliation, and clear exception ownership across finance, ops, and engineering |

Escalate immediately if any of these appear:

- repeated duplicate payments, especially if duplicate or erroneous disbursements are approaching the 1% to 2.5% band cited in AP guidance

- unresolved exceptions aging through close

- delayed close cycles where reconciliation is getting worse, not better

- weak audit evidence where you cannot quickly tie the invoice, approval record, provider reference or event, and ERP entry

Use a one-page decision check covering cost, control, integration readiness, compliance scope, and team operating maturity. If control or evidence is weak, do not push to full automation for speed alone. If your payout estate is cross-border, account for added complexity from currencies and regulations when deciding how far to automate.

For adjacent depth, review AP fundamentals, offshore payment constraints, and, if your UK service is in scope, the Online Safety Act UK compliance obligations, including Ofcom's three-month risk assessment timeline after launch.

Conclusion#

The right answer is rarely automation at all costs. For marketplace operators, the better choice is the one that improves control, reliability, and unit economics at your current stage, not the one with the cleanest demo or the lowest subscription price.

That is why the next move in this cost-benefit analysis should be discipline, not procurement. Build a real total cost of ownership (TCO) baseline first. TCO is a lifecycle measure, so your model should include setup, implementation, customization, data migration, integration with existing systems, and user training, not just license fees and hoped-for labor savings. If a vendor proposal skips those categories, your business case is probably understating cost and overstating speed to value.

Use your current AP metrics as the control group before you change anything. APQC benchmark tables are useful for orientation, but your own baseline matters more: for example, cycle time, rework hours, exception volume, and close delays. A practical checkpoint is simple: can finance and ops produce those numbers cleanly today, and can they trace them back to current AP logs or close records? If not, that is a red flag, because you will struggle to prove improvement later.

Do not commit on market coverage or compliance assumptions until you pressure-test them. Platform users often need to pass KYC checks before payment and payout activity, and those verification requirements can change over time as regulators update expectations. One failure mode is buying for invoice capture efficiency, then discovering late that onboarding, verification upkeep, or regional support creates manual work that was never priced in.

Your best next step is a scoped pilot, not a full cutover. Keep the pilot narrow, such as a limited invoice set or one department, and monitor it for accuracy, speed, and integration issues before expansion. The evidence pack for that pilot should be concrete: your TCO model, current KPI baseline, target approval and exception metrics, and a written list of integration and verification assumptions that must hold true before rollout.

If you are ready to move, talk to sales to confirm likely coverage by market and program, then verify the details in the docs and through that pilot. That sequence tells you more than a generic ROI promise. If you need a refresher on the operating model before that conversation, start with What Is AP Automation? A Platform Operator's Guide to Eliminating Manual Payables.

Related reading: A Freelancer's Guide to Business Process Automation (BPA).

Frequently Asked Questions

Is AP automation always cheaper than Manual AP processing for marketplace operators?

No. It depends on your baseline and how you model total AP cost. APQC’s AP cost-per-invoice measure includes outsourced, overhead, personnel, system, and other costs, so a tool that reduces data entry can still fail to lower total cost per invoice if other costs rise.

What costs are usually missed in an AP automation ROI model?

A common miss is treating ROI as labor savings only. You also need to price in overhead, system, outsourced, and other AP costs, plus the human work that remains around verification, matching, and exception handling before payment. Rework can also be undercounted when invoice formats are diverse or unstructured and extraction is less reliable.

How long does it typically take to see payback after moving from manual AP?

There is no universal payback window you can trust across all operators. The practical check is to baseline your AP cost per invoice, rework hours, and close delays before the pilot, then compare those same measures after go live. If a vendor gives you a fixed timeline without asking about your exception rate or invoice quality, treat that as a warning sign.

When should a marketplace keep some AP steps manual?

Keep manual review where the cost of a wrong approval or wrong payment is higher than the time you save. Supplier verification, matching, and exception handling are obvious cases, because approval operations still include those checks before payment. Even AI-oriented AP models still acknowledge that some steps continue to require human work.

How do AI-powered AP automation and Rules-based AP automation differ in day-to-day operations?

Rules-based automation can work well when invoices follow stable templates and fields appear in consistent places. AI-powered extraction is more useful when formats vary or documents arrive in messy, unstructured layouts, since traditional rule-based approaches struggle with that variety. The tradeoff is simple: AI reduces some extraction pain, but it does not remove the need for exception review.

What should finance and engineering verify before integrating AP automation with ERP systems?

Start with retry behavior in payment and API calls. Test that repeated requests using the same parameters and the same idempotency key execute only once, because that is the control that helps prevent duplicate execution on retries. Then confirm exactly where approval, verification, and exception handling sit before payment so the integration does not bypass controls finance still owns.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- bis.org/publ/bppdf/bispap167.pdftrusted

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/01trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalregister.gov/documents/2024/07/03/2024-14414/anti-money-l...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/forms-pubs/about-form-1099-nectrusted

- apqc.org/resources/benchmarking/open-standards-benchm...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

What Is AP Automation? A Platform Operator's Guide to Eliminating Manual Payables

AP stops feeling like a back-office admin task once your platform is processing more supplier and vendor payables. At that point, **ap automation for platform operators** is about controlling operational risk as much as efficiency. Manual AP is slower, more error-prone, and more expensive, and those weaknesses surface fast as volume rises.

Offshore Payment Processing for Platforms Under Regulatory Scrutiny

Offshore payment processing is a control decision first and a coverage decision second. For platform operators, the question is not just whether an offshore merchant account or gateway opens a new corridor. It is whether you can see activity clearly, prove approvals, and respond when issues cross jurisdictions.

UK Online Safety Act Compliance for Marketplace and Platform Operators

Treat the UK Online Safety Act as operating work now, not a policy debate. The most practical way to reduce uncertainty is to run an auditable implementation plan: make an initial scope call, stand up baseline controls, assign owners, and keep records you can defend if Ofcom asks questions.