Quick Answer

Treat offshore payment processing as a control program before a growth project. Approve it only after legal ownership is named per jurisdiction, provider evidence is retrievable on demand, and transaction-to-ledger traceability is proven. The article highlights FATCA pressure, including a potential 30% withholding on US-sourced payments tied to non-compliant foreign financial institutions. Use narrow pilots when obligations are still unclear, and scale only after dispute handling, reconciliation, and escalation ownership are functioning in production.

What Offshore Processing Means for a Platform Under Scrutiny#

Offshore payment processing is a control decision first and a coverage decision second. For platform operators, the question is not just whether an offshore merchant account or gateway opens a new corridor. It is whether you can see activity clearly, prove approvals, and respond when issues cross jurisdictions.

Offshore finance means conducting business in a foreign jurisdiction rather than your home country. That can be legal, but it can also attract regulatory scrutiny, and compliance obligations can vary across jurisdictions and institutions. A practical starting posture is to treat offshore as an accountability problem before you treat it as a growth lever.

This guide is for compliance, legal, finance, and risk owners scaling cross-border payouts or collections. If you are evaluating an offshore processor, merchant account, or multi-provider routing layer, your job is to define what you will approve and what evidence you need before launch. You also need to define what you will monitor and which events trigger escalation.

Offshore structures sit inside modern reporting and transparency expectations. FATCA, implemented in 2010, and CRS increased offshore reporting pressure and cross-border information sharing. FATCA can impose a 30% withholding tax on U.S.-sourced payments for non-compliant foreign financial institutions. Offshore does not mean invisible, and undocumented assumptions can create costs well outside the payments team.

Before you scale, verify two basics in writing:

- Who owns legal interpretation in each active jurisdiction, with exact responsibility boundaries if a provider is involved.

- What evidence the provider can produce on demand, including transaction records and reporting data tied to balances, transactions, and earnings where applicable.

The tradeoff is potential broader reach versus heavier oversight. Different legal frameworks can create compliance hurdles, and higher-risk payment contexts can include fraud and chargebacks that contribute to losses and account closures. If your team cannot clearly explain the path from transaction request to provider record to internal reconciliation, pause rollout and reduce scope.

The goal is practical: help you decide what to approve, what to monitor, what to document, and when to escalate. Rules vary by jurisdiction and provider setup, so use this as an operator guide and confirm legal specifics locally. Start by defining the stack you are actually approving.

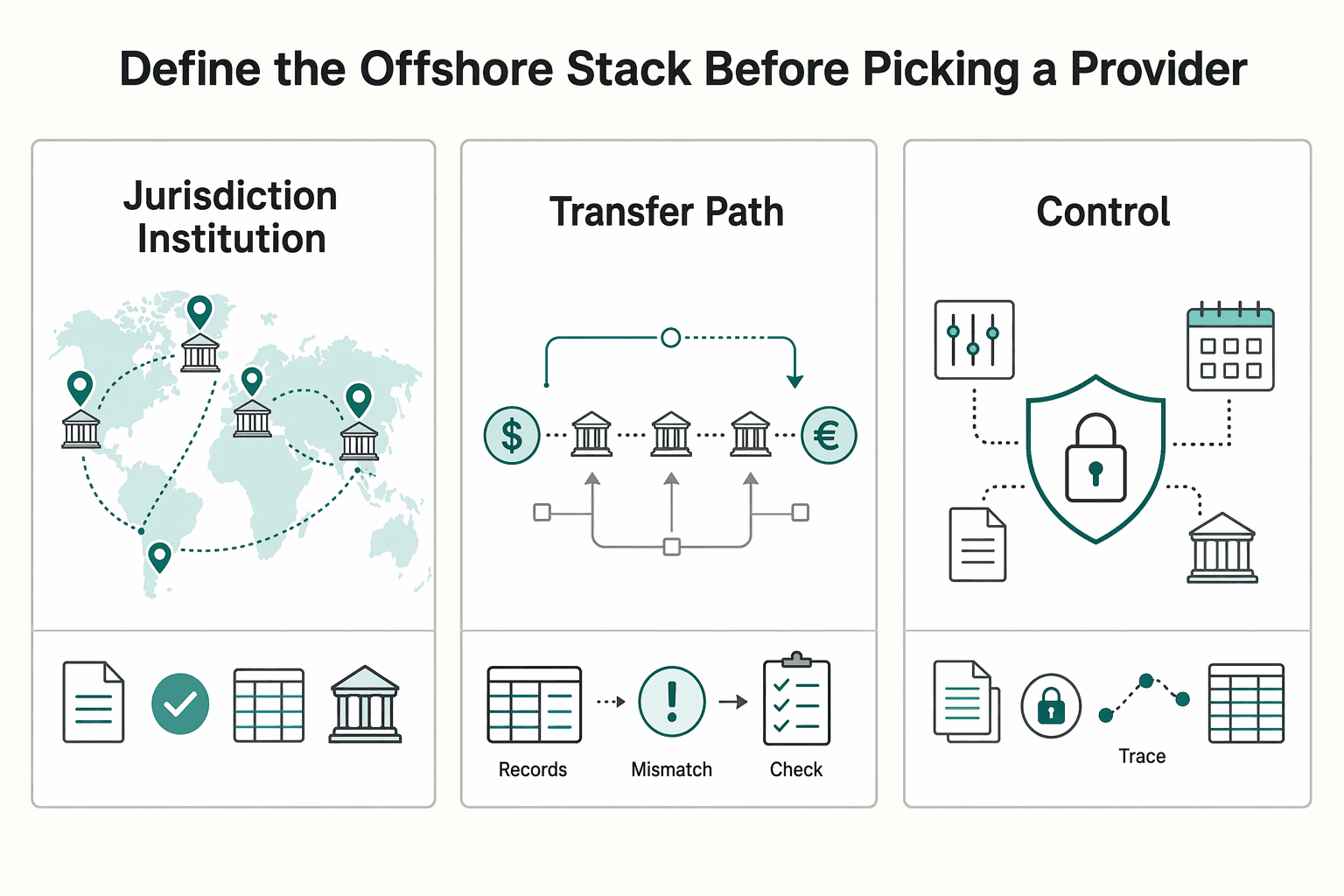

Define the offshore stack before picking a provider#

Start by splitting offshore decisions into three practical approvals: jurisdiction and institution map, transfer path, and control ownership. If you skip that split, a clean front-end flow can still leave a settlement path that is hard to audit later.

| Approval area | What to define |

|---|---|

| Jurisdiction and institution map | Document which regulatory jurisdictions and financial institutions are involved in each cross-border flow |

| Transfer path | Map how funds move across partner banks, including correspondent-bank relationships and any nostro/vostro settlement points where relevant |

| Control ownership | Assign who verifies recipient details, who reviews exchange-rate assumptions, who initiates the payment, and who tracks the transaction |

Keep those three approvals separate during review. Cross-border payments typically involve currency conversion and coordination across multiple institutions and jurisdictions, with familiar friction around costs and processing delays. Breaking the stack apart also reduces surprises when FX movement creates cost variance during reconciliation.

Use the same six-step checkpoint for every option: payment type, exchange rate, recipient details, verification, initiation, and tracking. Ask for one sample transaction mapped across all six steps, including which institution handles each step. If that path is unclear, pause approval. Related: How to Respond to a Regulatory Audit as a Payment Platform.

When offshore is the right move for a platform#

Use offshore when it solves a defined operating constraint and you can staff the compliance work that follows. If your current setup already meets your needs, simpler governance is usually the better call.

| Check | Requirement |

|---|---|

| OSS selection | OSS is optional, but once selected, all supplies covered by that scheme must be declared through OSS |

| Domestic VAT returns | OSS returns are additional and do not replace domestic VAT returns |

| Return cadence | Union and non-Union OSS returns are quarterly; the import scheme return is monthly |

| EUR 10 000 threshold | Where relevant, ownership for monitoring the EUR 10 000 EU-wide threshold must be named |

| CBR requests | If several companies are part of a CBR request, one company should file on behalf of the others |

Europe is a useful example because the documentation is public and the operating implications are concrete. EU VAT e-commerce rules affect marketplaces and platforms inside and outside the EU, and a platform can be treated as a deemed supplier in some cases. For cross-border B2C activity, tie the go or no-go decision to VAT administration readiness. That includes whether OSS is appropriate and whether a complex transaction chain warrants an advance CBR request.

OSS can reduce administrative friction by allowing eligible taxable persons to register in one Member State for covered cross-border supplies, but it is not a free simplification. Keep the checks in the table explicit, and name an owner for thresholds, filings, scheme scope, and exception handling.

If several companies are part of a CBR request, one company should file on behalf of the others. If ownership is still unclear for filings, thresholds, scheme scope, or exception handling, pause rollout or reduce scope before launch. Member States can exclude a taxable person from OSS, and some Member State of identification choices can bind the business for the current calendar year plus the next two.

Related reading: How to Expand Your Subscription Platform to Europe for Payment and VAT Readiness.

The benefits that matter at platform scale#

At platform scale, the benefit is specific. Offshore can open payment access you cannot get through your current domestic setup, but only if you can control the added operational risk. The goal is not more payments in the abstract. It is usable coverage with clear ownership.

The strongest case is practical: an offshore merchant account may be the only way to accept card payments when domestic approval is unavailable, and it is often used by businesses expanding internationally. In that setup, payments move through a foreign bank before transfer to your merchant account, and currency conversion may be part of the path.

Where the upside is real#

The upside is broader access, not automatic conversion or performance gains. If a provider claims multi-currency acceptance, define exactly how funds move before you treat it as a real benefit:

- payments are processed through a foreign bank before transfer to your account

- currency conversion may occur before funds are remitted to you

- transfer timing and settlement details are documented up front

Those details drive different reconciliation and support implications.

Do not assume routing or resilience#

Do not treat an offshore structure by itself as proof of better routing, failover resilience, or lower concentration risk. The evidence supports offshore access options, not guaranteed architecture outcomes. Validate the result in your own environment.

Before rollout, require written policies and procedures, plus a provider decision checklist that records process and basis for decision. For overseas providers, run this through a vendor risk management program because third-party offshore arrangements carry inherent risks and unknowns.

The tradeoff appears first in operations and cost#

The tradeoff usually shows up first in operations and cost: heavier documentation, delayed fund transfers, possible foreign-country incorporation requirements, and the risk of unnecessarily high international payment fees. Offshore can be the right move when domestic paths are blocked, but only if you can show the benefit and absorb the oversight burden. If you cannot do that while maintaining control of fees, documentation, and provider oversight, it is not the right move.

Map the full risk surface before go live#

If you cannot map risk by payment flow and assign a clear control owner, you are not ready to launch. Build the map around where money and messages move: onboarding, transaction screening, settlement, payouts, dispute handling, and reconciliation.

Use one shared table so teams can see handoffs, alerts, required actions, and retained evidence in one place. Visa's April 2021 Payment Facilitator and Marketplace Risk Guide is a useful anchor because it treats operational risk, regulatory and compliance risk, and credit settlement risk as distinct categories.

| Flow | What can go wrong | Minimum control check before launch | Evidence to keep |

|---|---|---|---|

| Onboarding | Weak onboarding review lets bad actors enter the platform | Confirm who performs screening, what data is required before activation, and how escalations are handled | Policy version, approval record, exception log |

| Transaction screening | Fraudulent or suspicious activity passes because rules are too thin | Verify velocity checks, fraud detection, and suspicious transaction monitoring are active and tested | Rule inventory, test results, alert samples |

| Settlement | Settlement breaks create unresolved differences across provider files, internal ledger, and bank receipts | Reconcile provider settlement files to internal ledger and bank receipt path | Settlement reports, bank confirmation, variance log |

| Payouts | Payout control gaps can send funds to the wrong party and make recovery difficult | Hold back first-release cohorts, verify beneficiary controls, and document reversal limits | Payout approval records, beneficiary change log, failed payout reports |

| Dispute handling | Chargebacks are routed late or to the wrong queue | Test dispute intake, ownership, response timing, and ledger impact handling | Chargeback notices, response files, aging report |

| Reconciliation | Duplicate postings, missed events, or FX mismatches distort balances | Confirm idempotent posting logic, replay handling, and daily exception review | Reconciliation output, event replay log, unresolved breaks report |

Treat faster rails as a different fraud problem#

If your review only models card-not-present fraud, it may be incomplete for your payment flows. For faster or low-friction flows, define which detection controls must run before release versus after settlement, then test that design.

Add acceleration scenarios to your risk table, including account takeover, merchant cloning, and enumeration or account testing. Visa explicitly flags enumeration or account testing schemes, force-post fraud, account takeovers, and merchant cloning, so include them even when the product is marketed as low-friction or instant.

Operational breaks need explicit testing too#

Operational breaks should be treated as launch-critical. Test these four failure modes before launch:

- Duplicate postings: retries or replayed events create a second ledger impact.

- Missing webhook events: provider status changes but your platform does not record the event.

- Stale FX assumptions: assumed and realized conversion outcomes diverge across authorization, settlement, or remittance.

- Delayed chargebacks: a transaction appears settled, then a later dispute changes balances and margin.

Require at least one simulated failure in each category. Ask the provider to show duplicate-event behavior, retry fields, exception reporting, and where delayed chargebacks appear in exports. Visa's "Exception Reporting and Investigations" control area is a useful checkpoint. If the exception path is unclear, launch risk is still high.

Make the evidence pack part of launch, not audit cleanup#

The table only helps if it produces an audit-ready record. For each flow, retain the owner, trigger, action taken, and supporting records.

Require a named Risk Monitoring Policy and attach the flow table to it. This makes controls testable and keeps tradeoffs explicit. The BIS notes tradeoffs across stability and integrity, competition and efficiency, and consumer protection and privacy. Treat faster payouts with lighter checks as a risk decision, not just a feature decision.

Do not copy another platform's controls and assume they fit. The New York Fed's broader liquidity guidance is that responses are institution-specific. If onboarding, screening, settlement, payouts, disputes, and reconciliation owners cannot sign one shared risk map, pause launch and narrow scope.

Set a minimum regulatory baseline and country-variance checks#

Set a written regulatory baseline before you scale by country. If control scope, ownership, escalation paths, and logging expectations are still informal, you are not launch-ready.

Lock the baseline first#

Treat these as launch artifacts, not intentions:

- Control scope clarity: Document what is in scope, what is out of scope, which provider controls you rely on, and who revalidates scope when the product changes.

- Policy ownership: Assign one owner, keep policy versions controlled, and record exception approvals when you add a corridor or entity.

- Escalation path: Define the route from alert to decision, including who can pause activity, who handles escalation, and how evidence is retained.

- Logging expectations: Define which systems log onboarding decisions, screening hits, settlement changes, beneficiary updates, and manual overrides, then get legal and security sign-off on the approach.

A data reconciliation framework should connect those controls to transaction, settlement, and payout records. If data is not traceable and usable, controls can look complete on paper and fail under review.

Build a jurisdiction matrix that separates knowns from unknowns#

Once the baseline is set, use one matrix for active corridors and planned entities, for example the United States, Europe, APAC, and options like Ireland, Gibraltar, or Malta. The goal is to show what is confirmed, what is still unknown, and who can sign legal interpretations.

| Market or entity | Must be known before launch | Unknowns to flag | Who signs interpretation |

|---|---|---|---|

| United States | Licensing and reporting position for your model and corridors | Open legal or tax treatment questions for the planned structure | Named internal legal owner, with outside counsel if needed |

| Europe | Country-by-country obligations for served markets | Assumptions that one answer covers all countries | Regional legal and compliance owners |

| APAC | Country-specific permissions, reporting, and partner dependencies | Gaps tied to local supervisory or enforcement capacity in some markets | Local counsel or market specialist plus program owner |

| Ireland, Gibraltar, Malta | Entity role, contracting chain, reporting responsibilities | Assumptions that incorporation or provider access equals operating permission | Group legal, finance or tax, and business sponsor |

Marking an item as unknown is acceptable. Hiding it as assumed is not.

Use a launch gate, not a promise#

Use one hard rule: if jurisdiction obligations are still unclear close to launch, limit the rollout to pilot corridors and defer full expansion. Keep scope narrow until legal and reporting interpretations are signed.

Policy and standards material can inform your checklist, but it is not binding local law by itself. A matrix without signed interpretations, supporting legal notes, or a reporting calendar is a red flag. Narrow the release instead of scaling uncertainty.

Choose providers with evidence, not sales claims#

Once your jurisdiction matrix is signed, choose the provider that can prove controls in documents and test outputs, not in sales language. If a gateway or processor cannot show how it routes, reconciles, escalates, and handles failures, treat that as a risk issue.

Third-party processors are intermediaries, so diligence is not just about integration quality. It also covers contract terms, hidden fees, and the operational tradeoffs that surface during exceptions.

Ask for evidence you can inspect#

Request a compact diligence pack your risk, finance, and compliance owners can verify.

| Area | Evidence to request | What to verify |

|---|---|---|

| Routing controls | Demo or product documentation with routing and fallback logic | Why a transaction took a route, and how overrides are logged |

| Disputes and exceptions | Dispute tooling walkthrough, sample case data, status exports | End-to-end traceability from provider reference to your ledger or reporting |

| Reconciliation exports | Sample daily exports plus field definitions | Match quality for payouts, fees, reversals, returns, and adjustments |

| Compliance and risk | Evidence of compliance monitoring, risk-control coverage summary, named escalation contacts | Clear ownership for compliance and risk escalation, and control coverage for your flows |

| Incident management | Contract terms and incident-management process language | Clear severity definitions, notification paths, and responsibility boundaries |

Prioritize the sample export test before you sign. If finance cannot reliably tie provider references, internal IDs, amounts, and exception codes, the operational cost will show up later.

Test by rail, not by brochure#

Run scenarios across the payment rails relevant to your model. Test normal approvals and failure cases, including reversals, returns, and dispute-related exceptions, then confirm:

- which event the provider sends

- what lands in reconciliation exports

- who is alerted for manual review

Providers that are clear on successful flows but vague on exceptions usually create the most downstream work.

Treat opacity as a red flag#

Do not treat offshore opacity as a benefit. Financial institutions routinely share account information with tax authorities, and FATCA and CRS reporting expectations mean offshore structures still face scrutiny. If a provider is evasive about entity structure, licensing or registration posture, or reporting responsibilities, reject it.

Risk controls also affect market access. Payment systems rely on access limits, compliance monitoring, and penalties for noncompliance. Weak control handling can lead to market rejection.

Practical decision rule#

If coverage is similar, choose the vendor with the cleaner evidence trail: clearer reconciliation exports, named escalation contacts, and transparent handling for returns, reversals, and dispute exceptions. That usually reduces avoidable risk and rework.

For the controls and reconciliation side, see How to Build a Deterministic Ledger for a Payment Platform.

Design controls before scaling volume#

Before you scale volume, make sure your controls can handle higher-risk activity, retries, and exceptions without creating accounting noise. Use a risk-based approach: identify and understand the ML or TF risk in the activity you enable, then scale preventive controls to that risk.

Gate higher-risk flows with customer due diligence and suspicious-activity monitoring tied to access controls and exception routing. Keep the decision rule explicit:

- elevated risk or incomplete due diligence: restrict access or hold for review

- expected profile and behavior: standard path

- unresolved alerts or mismatches: route to a named exception owner

In payment orchestration, design event handling to be idempotent so retry paths are less likely to create duplicate outcomes. Treat that as an engineering control, then test retry scenarios and verify one intended business outcome with a complete event trail.

Design traceability so teams can investigate decisions and payment movements through to reconciliation. Low observed losses are not proof that controls are sound, and weak controls can still lead to market rejection.

If a control is manual for now, assign an owner, define the evidence it must produce, and set a review checkpoint before expanding into new corridors.

For buyer protection and risk controls, see Payment Guarantees and Buyer Protection for Platform Operators.

If you are turning these controls into implementation requirements, use the API and webhook references to map idempotency, status handling, and reconciliation flows: Read the Gruv docs

Build the reporting pack your auditors will ask for#

Build a regular, versioned evidence pack that lets a reviewer trace what happened, who approved it, and whether controls were applied consistently. The exact fields can vary by platform, reviewer, and jurisdiction, so keep the format explicit and repeatable.

Use one structure every cycle:

- Operating outcomes: the key risk and control metrics your team tracks.

- Breakdowns: segment views that match how your risk and finance teams monitor changes, so local shifts do not get buried in blended totals.

- Trace records for each metric: source export, reconciliation to finance reporting, and reviewer sign-off.

- Material-change detail: when a change happened, which provider or process triggered it, and how it was recorded.

- Exception detail: age, owner, and current disposition, not just a count.

- Control evidence: retained documentation that shows who participated, how the review was performed, and what terms/acronyms mean for consistent interpretation.

This matters because Treasury's 2024 National Money Laundering Risk Assessment identifies third-party payment processors as a risk area. It also flags inconsistent compliance with domestic obligations and inconsistent implementation of international AML/CFT obligations as vulnerabilities. In practice, reviewers will focus on whether your pack shows consistent execution over time and clear audit traceability.

For a step-by-step walkthrough, see KYC Best Practices for Reducing Money Laundering Risks: A Payment Platform Compliance Guide.

Define escalation triggers and stop-ship thresholds#

Define escalation triggers before volume scales so your team is not making governance decisions in real time. Set clear rules for what escalates, who decides, and when onboarding or payout expansion pauses because control exceptions are outpacing review capacity.

Use your monthly reporting pack to detect sharp changes from your own recent baseline. Prioritize three triggers: sudden chargebacks spikes, unexplained approval volatility, and repeated reconciliation breaks.

| Trigger | First verification check | Primary owner | Immediate containment action |

|---|---|---|---|

| Sudden chargebacks spike | Reconcile provider data with ledger and dispute exports | Risk | Review routing and exposure before adding volume |

| Unexplained approval volatility | Check provider, corridor, and payment-method cuts | Ops with Risk | Pause discretionary routing changes until cause is clear |

| Repeated reconciliation breaks | Verify source exports, ledger postings, and settlement files for the same period | Finance with Ops | Pause new payout or onboarding expansion until breaks are cleared |

Assign ownership explicitly so investigation and decision authority do not blur. Risk investigates patterns and abuse signals, legal assesses jurisdiction impact, finance approves liquidity actions, and ops executes routing changes.

When legal interpretation is part of an escalation, verify against official legal sources where relevant. FederalRegister.gov XML is informational and should be checked against an official Federal Register edition, because the XML version does not itself provide legal or judicial notice.

Set stop-ship rules around control capacity, not only risk appetite. Manual operations can create compliance blind spots and slow decision-making when speed matters most. If exceptions no longer have clear owners, current disposition, and consistent evidence of policy application, pause expansion until control discipline is restored.

Route incidents through a documented incident response plan, and use regular security audits and penetration testing to confirm that trigger logic, ownership handoffs, the legal verification path, and containment controls still work under time pressure.

Execute in a 90-day sequence with verification checkpoints#

Treat this 90-day plan as a control-proof window, not a growth sprint. If the core evidence pack is not complete by day 30, keep scope narrow and delay broader rollout.

| Phase | Focus | Checkpoint |

|---|---|---|

| Days 1 to 30 | Finalize the jurisdiction matrix, the provider due diligence file, and a compliance accountability map | If the core evidence pack is not complete by day 30, keep scope narrow and delay broader rollout |

| Days 31 to 60 | Pilot one corridor and one fallback route with controlled volume | Confirm that both routes can run the same six-step flow reliably |

| Days 61 to 90 | Expand only after checkpoints hold against your own recent baseline for timing, reconciliation, and exception handling in the same reporting period | Do not let volume growth mask unresolved timing breaks or unexplained variance between provider records and your books |

Days 1 to 30#

Finalize three artifacts before live expansion: the jurisdiction matrix, the provider due diligence file, and a compliance accountability map. Start here because cross-border payments involve currency conversion and coordination across multiple institutions and jurisdictions, and compliance interpretation can still vary across markets.

Build the due diligence file so it can be rechecked, not just approved once. Include offshore entity review documents and the operating evidence needed for rechecks and escalation. If beneficial ownership is hard to verify because registry data is limited, request supporting records such as a certificate of incumbency. Then confirm notarization or apostille handling where relevant and verify the notary. Treat incomplete, altered, or forged documentation as an immediate escalation signal.

Days 31 to 60#

Pilot one corridor and one fallback route with controlled volume. The goal is to confirm that both routes can run the same six-step flow reliably: payment type, exchange rate, recipient details, verification, initiation, and tracking.

Compare primary and fallback behavior using operator-facing checks for settlement visibility, tracking quality, and reconciliation readiness. If fallback performance depends on manual exception handling, it is not ready to scale.

Days 61 to 90#

Expand only after checkpoints hold against your own recent baseline for timing, reconciliation, and exception handling in the same reporting period. Do not let volume growth mask unresolved timing breaks or unexplained variance between provider records and your books.

Cross-border expansion can support growth, but it can also add cost and processing-delay tradeoffs, so expansion should follow evidence. The end state is leadership sign-off that controls, evidence, and escalation paths are operating in production, not sitting in draft or depending on one person.

Conclusion#

Offshore expansion is worth pursuing only when it solves a clear business need and you can run it with documented controls.

Use disciplined sequencing: define the operating model, confirm how cross-border data and contracts change your legal exposure, test controls in a limited pilot where practical, then scale. Offshore setups can create upside, but unmanaged legal and operational risk can rise quickly when data and responsibilities span jurisdictions.

Before go-live, require evidence you can inspect:

- cross-border data handling is mapped, with applicable privacy obligations addressed, such as GDPR or CCPA where relevant

- contracts include Data Processing Agreements, confidentiality terms such as NDAs, and clear arbitration and termination procedures

- partner screening is completed for security, financial, and compliance risk

- ownership is named for exceptions, disputes, and ongoing control reviews

If any of these points are still unclear, delay expansion. Recurring compliance audits and contract updates are part of the operating model, not post-launch cleanup. They are what keep offshore from turning into a fragile exception path.

Before rollout, confirm market coverage, policy gating, and operating ownership with your risk and finance leads: Talk to Gruv

Frequently Asked Questions

What are the main benefits of offshore payment processing for platform operators?

A primary benefit is broader payment acceptance beyond your registered country. Offshore merchant accounts are positioned for global acceptance, and for some high-risk merchants they may be the only workable path to card processing when domestic approval is hard. For platform operators, that value is strongest when offshore meaningfully expands coverage instead of duplicating a domestic setup.

What are the biggest risks beyond processing fees?

Key risks include regulatory scrutiny and added operational complexity in fund movement. Offshore flows can include foreign-bank transfer steps and currency conversion exposure, and providers may require heavier documentation, delayed transfers, or foreign incorporation. These are control and execution risks, not just pricing tradeoffs.

What compliance baseline should we require before launch?

Set a baseline of verified due diligence rather than assumptions. At minimum, confirm the provider’s technical and pricing details and document how you will handle scrutiny and operational exceptions in practice. Do not assume PCI DSS, KYC, or AML obligations are automatically satisfied just because the setup is offshore.

How should we evaluate an offshore payment gateway or processor?

Start with risk-control capability, not volume promises. Require evidence of advanced fraud detection and prevention, configurable risk settings, and real-time reporting and analytics. Then complete due diligence on technical and pricing details before launch.

When should we use offshore as a strategic setup versus a temporary fallback?

Use offshore strategically when it solves a persistent access problem, such as ongoing limits in domestic approval or the need for cross-border acceptance. Treat it as a temporary fallback when you need continuity but still have unresolved operational or compliance questions. The difference is whether the model is proven and sustainable for your risk posture.

What data is still unknown before go-live, and how do we close those gaps safely?

Unknowns often center on documentation burden, transfer timing, incorporation requirements, currency-conversion exposure, and how much scrutiny the structure will face. Close those gaps through structured provider due diligence that validates technical, pricing, and risk-control details before broad rollout. If those points are still unclear, treat the uncertainty as a launch blocker rather than a minor follow-up item.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bclawreview.bc.edu/articles/51/files/639aa9015bca3.pdftrusted

- bis.org/cpmi/publ/brief4.pdftrusted

- bsee.gov/sites/bsee.gov/files/tap-technical-assessmen...trusted

- federalregister.gov/documents/2025/01/17/2025-00708/cybersecurit...trusted

- federalregister.gov/documents/2024/09/04/2024-19260/financial-cr...trusted

- ferc.gov/sites/default/files/2020-08/20160303130808-T...trusted

- home.treasury.gov/system/files/136/2024-National-Money-Launder...trusted

- law.georgetown.edu/international-law-journal/wp-content/uploads...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Expand Your Subscription Platform to APAC: Payment Methods Currency and Regulatory Landscape

Asia-Pacific (APAC) expansion requires country-by-country launches, not one regional motion. This guide helps you decide with payment, currency, and regulatory evidence so you do not mistake a strong regional headline for real launch readiness in your subscription platform.

Responding to a Regulatory Audit as a Payment Platform

Use a short initial response structure, not a giant audit program. In the early phase, focus on reducing surprises: define what is in scope, freeze the right evidence, and avoid building process the regulator did not ask for.

ACH Payment Processing Platforms for U.S. Collections and Payouts

Start with the outcome, not the feature label. You may need a setup that collects money in and sends money out over the U.S. banking network, not just a generic bank-transfer option. In practice, that often means ACH debits for collections and ACH credits for payouts, with controls your product, engineering, and finance teams can run in production.