Quick Answer

Yes - most Canadian freelancers should keep a Canadian Stripe account, add a USD-denominated Canadian bank account, and map USD payouts there first. This avoids Stripe’s +2% conversion charge when conversion is required and keeps operations lighter. Consider a U.S. LLC and U.S. Stripe account only when you can document recurring payment or onboarding friction, or a client requirement that truly depends on U.S. account-country access, and you can sustain ongoing filing work such as Form 5472 where applicable.

The Default Path to Profit: Mastering USD Payments with Your Canadian Stripe Account#

Start with your Canadian Stripe account if your goal is to protect margin without adding U.S.-entity complexity. It is often the simpler path, and with the right payout setup you can receive USD without forcing immediate conversion.

The definitions below show where margin can slip:

- Settlement currency: the currency your destination bank account receives from Stripe payouts.

- Payout currency: the currency set in Stripe payout settings. It must match your linked bank account currency.

- Automatic conversion: when charge currency and your default settlement setup do not match, Stripe converts funds before payout.

Here is the practical flow. If a client pays you in USD, USD is the presentment currency. Stripe supports charging in over 135 currencies. It also documents that incoming funds are automatically converted to your home-country default currency unless an alternate settlement setup is in place. If Stripe performs that conversion, it charges a currency conversion fee. On Stripe's Canada pricing page, this is listed as +2% if currency conversion is required. Stripe also states conversion is generally based on a mid-market source, and the conversion cost can appear either as an adjusted rate or as a separate fee line item. Verify current fee behavior before you rely on it.

| Flow | Control | Cost visibility | Operational burden |

|---|---|---|---|

| Default CAD payout flow | Low. USD is converted if settlement remains CAD. | Lower. FX cost may be embedded in rate or shown as a separate fee. | Lowest day-to-day, but margin loss is easier to miss. |

| USD hold-and-convert-later flow | Higher. You can receive USD payouts and decide when to convert. | Better. Processing and FX timing are easier to evaluate separately. | Slightly higher. You need a USD-denominated bank account and matching payout settings. |

Decision checkpoint: confirm your linked bank account is USD-denominated and your Stripe payout currency matches it. If not, USD client payments can still end as CAD payouts with conversion fees. If your main objective is preserving margin with minimal compliance overhead, fix this Canadian-account setup before you consider U.S.-entity complexity.

If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

The Default Path: Mastering USD Payments in Canada#

If you stay on the Canadian path, the work is mostly configuration. If USD settlement is available in your Stripe settings, set the account up so USD charges pay out to a USD account, not CAD. In practice, you do three things in order: open a Canadian USD business account, add it in Stripe, and confirm USD payout routing.

Three terms keep this setup clear:

- USD settlement: you receive funds in USD because settlement and payout account currency are aligned, so Stripe does not need to convert that flow.

- Payout routing: Stripe sends each currency balance to the bank account configured for that same currency.

- Conversion event: FX happens when the starting currency and destination currency are different.

The key distinction is simple: card processing fees and currency conversion costs are not the same line item. Stripe's Canada pricing page lists 2.9% + CA$0.30 per successful domestic-card transaction, while currency conversion is a separate add-on when conversion is required. When you hold USD in a matching USD payout account, you decide when conversion happens instead of triggering it automatically. Verify any current fee or spread comparison before you make this your operating assumption.

| Action | Where to do it | What to confirm | Common setup error |

|---|---|---|---|

| Open a USD business account | Your Canadian business bank | The account is USD-denominated and usable for business payouts | Opening an account that still settles Stripe payouts in CAD |

| Add the USD account in Stripe | Stripe Dashboard, under settlement currencies and bank accounts / payout bank account settings | The added payout bank account currency is USD | Adding the bank account but leaving payout currency on CAD |

| Route USD payouts to USD | Stripe payout configuration for USD balance | USD payouts are assigned to the USD bank account | Assuming routing is automatic without checking the currency assignment |

Step 1: open the USD business account. RBC, TD, and CIBC each advertise USD business banking options for businesses receiving U.S.-dollar payments. The goal is straightforward: you can receive and hold USD within your Canadian banking setup.

Step 2: add it in Stripe and check the currency match. Stripe guidance points to Settlement currencies and bank accounts. Stripe support states accounts opened in Canada can use USD-denominated bank accounts, and Stripe docs require payout bank-account currency to match payout-settings currency. Stripe support also says you can have one payout bank account per currency.

Step 3: verify with an actual payout trail. Stripe typically schedules the first payout 7 to 14 days after the first successful live payment, so check payout records and your bank statement together. The result you want is simple: USD charge, USD payout, and no forced conversion event in that flow.

Use the U.S.-presence path only when these become recurring blockers:

- Payment-method friction tied to currency or account mismatch patterns (for example, delayed failures on wrong-currency PAD debits).

- Integration-specific limits for U.S. payment methods that persist after troubleshooting (for example, ACH setup issues documented in some third-party integrations).

- Reconciliation friction that remains high even after using Stripe's reconciliation tooling.

If these issues are occasional, keep the Canadian setup and tighten the checks above. If they are persistent, that is the point where a U.S. presence becomes a real decision rather than a hypothetical upgrade.

Related: Ho Chi Minh City, Vietnam: The Ultimate Digital Nomad Guide (2025).

The Power Play: When and How to Establish a U.S. Presence#

Move to a U.S. setup only if your Canadian setup is still causing persistent payment friction. If the issues are occasional, keep your Canadian stack. Stripe treats a U.S. account as a full local setup, not a shortcut.

Use this trigger: proceed only when your current account-country setup keeps blocking payment methods you need, creates repeat checkout or client-onboarding friction, or a client requires a U.S.-registered vendor. Stripe states that payment-method support varies by country and currency, and opening in another country requires more than company formation.

| Aspect | Canadian-only stack | U.S.-presence stack |

|---|---|---|

| Payment acceptance fit | Works when your Canadian Stripe account plus USD settlement matches client and payment-method needs | Better fit when required payment methods, client onboarding, or account-country expectations require a U.S. entity |

| Operational overhead | One Stripe country, one primary banking base, fewer moving parts | Separate U.S. entity, U.S. banking, separate Stripe account, more account management |

| Documentation burden | Canadian business records plus payout-routing checks | U.S. registration, tax ID, local-presence evidence, linked U.S. bank account, Stripe verification details |

| Support complexity | Simpler support path in one account country | Higher complexity in cross-country operations, often with multiple accounts |

Before you start, define the pieces clearly. An LLC is a U.S. state-law business entity. A Registered Agent receives legal and official documents in the state. An EIN is the federal business tax ID. A U.S. Stripe account must meet U.S.-specific business and verification requirements.

Entity setup#

Start with the legal entity first. Every downstream record depends on it. Your inputs are your state filing details, final legal business name, and Registered Agent. You are not really ready until the entity is formed and the legal name and details are finalized for IRS, bank, and Stripe use.

| Stage | Needs | Ready when |

|---|---|---|

| Entity setup | State filing details, final legal business name, Registered Agent | Entity is formed and the legal name and details are finalized for IRS, bank, and Stripe use |

| Tax identity | Finalized entity details, responsible-party details from the IRS application | EIN is issued and state registration, EIN record, bank records, and Stripe profile use the same legal name and entity type |

| Banking readiness | Approved entity, EIN, required business docs, U.S. bank account that can receive payouts | Account is open, active, and intended for this U.S. operation long term |

| Stripe onboarding | U.S. registration, legal entity name, entity type such as LLC, EIN, business address, representative tax identity details, phone number, government-issued ID, working website, physical location, confirmed U.S. bank account | Verification has passed and payouts are linked to the confirmed U.S. bank account |

Treat formation as only one part of the project. Stripe's cross-country requirements include a legal entity, tax ID, physical location, phone number, government-issued ID, working website, and a physical bank account in that country. A Registered Agent helps with state registration, but it does not satisfy the full local-presence package.

Tax identity#

After formation, get the EIN. Stripe onboarding for U.S. accounts can include EIN verification, and U.S. tax administration uses this identifier. The inputs are your finalized entity details and responsible-party details from your IRS application. For some international applicants, IRS Form SS-4 instructions list the EIN phone channel at 267-941-1099, 6:00 a.m. to 11:00 p.m. ET, Monday-Friday.

The main control here is exact record matching. Your state registration, EIN record, bank records, and Stripe profile should all use the same legal name and entity type. You are only ready when the EIN is issued and those details align across records.

Banking readiness#

Set up banking before Stripe onboarding. Stripe requires a linked bank account for payouts, and for this setup Stripe says the bank account cannot be a virtual bank account. You need the approved entity, EIN, required business docs, and a U.S. bank account that can receive payouts.

Ready means the account is open, active, and intended for this U.S. operation long term. A common failure is assuming any fintech account qualifies, then discovering it does not meet Stripe's country requirements. Keep this distinction clear: Stripe's Canada exception for USD-denominated bank accounts is not the same as qualifying for a U.S. account.

Stripe onboarding#

Onboard only after the entity, EIN, and bank account are in place. Stripe states that registered businesses need U.S. registration for a U.S. account, and verification can include legal entity name, entity type such as LLC, EIN, business address, and representative tax identity details. Stripe also lists broader local-presence requirements for cross-country accounts, including phone number, government-issued ID, working website, and physical location.

Two operator checks matter most. First, account country is effectively permanent after activation, and using Stripe in another country generally requires a separate account. Second, ready does not just mean opening the account. It means verification has passed and payouts are linked to the confirmed U.S. bank account.

Final checkpoint: if you cannot maintain ongoing filings, records, and documentation hygiene, do not proceed. The next section explains why that matters, including the Form 5472 regime that can apply to some foreign-owned U.S. structures with reportable transactions, where filing can involve a pro forma Form 1120 attachment and the IRS states a $25,000 penalty for failure to file when required. Verify current eligibility and compliance details before you act.

You might also find this useful: How to Open a Stripe Account for a Non-US Business.

The Compliance Trap: The Hidden Costs of a U.S. LLC#

If you open a U.S. LLC, a major risk is the ongoing execution: accurate records, clear categorization, and follow-through year after year.

For exact U.S.-LLC forms, deadlines, and penalties, treat the details as rule-dependent and verify them before filing.

What you actually need to manage#

Separate the work into distinct buckets and assign an owner for each one. Even when a rule still needs confirmation, ownership should be explicit.

| Obligation | Who handles it | Frequency | What breaks if missed | Cost type |

|---|---|---|---|---|

| Potential U.S.-specific filing requirements (scope to be confirmed) | Advisor confirms current requirement; you provide complete records | Verify current rule | Filing can be late, incomplete, or based on the wrong requirement | Variable professional cost + admin time |

| Expense tracking | You maintain records; advisor reviews as needed | Ongoing (at least monthly) | Tax work gets harder and operational surprises increase | Admin time |

| Expense categorization | You categorize before accounting/tax handoff | Ongoing | Transactions can be misclassified and harder to review | Admin time |

| Compliance-relevant labels (for example, Taxes and licenses) | You keep labels explicit in your categories | Ongoing | Important compliance costs can disappear into generic lines | Admin time |

The exact filing requirements depend on current rules and your fact pattern. Do not guess. Verify each bucket and assign a named owner.

The real failure mode is weak bookkeeping#

The practical protection is strong expense tracking and categorization. Clean books make taxes easier, reduce avoidable surprises, and speed up review.

Use clear categories before year-end handoff. Keep compliance-relevant labels explicit, for example Taxes and licenses, so these costs do not disappear into generic admin lines.

Your records should answer, quickly:

- Is this revenue, reimbursement, transfer, or business expense?

- Which account cleared it?

- Do invoice, receipt, and bank activity match the same event?

Manual tracking is a common failure point because it adds time drag and error risk. A simple system is fine. Memory-based bookkeeping is not.

Before you file anything#

Set controls before the first filing cycle:

| Control | What to include | Note |

|---|---|---|

| Monthly evidence pack | Statements, invoices, major receipts, contracts, official notices | Monthly |

| Label transfers and reimbursements | Labels added when they happen | Do not leave ambiguous descriptions |

| Compliance calendar | Deadlines, reminders, named owners | One calendar |

| Month-end close | Revenue, expenses, transfers, unresolved items | Basic month-end close |

| Advisor handoff | Categorized transactions, statements, summaries, open questions | Clean package |

Proceed only if you can fund and operate this compliance work consistently. If not, simplify first and avoid adding avoidable compliance complexity.

We covered this in detail in A German Freelancer's Guide to Permanent Establishment Risk in the US.

The Decision Framework: Is a U.S. LLC Worth the Cost?#

By this point, the question is no longer whether a U.S. entity sounds useful. It is whether a verified U.S.-access constraint is costing you enough to justify the added compliance load. If your issue is mainly FX handling, payout control, or settlement flow, Stripe already supports multi-currency settlement and charging in over 135 currencies, so a U.S. entity may not be your first fix.

Define the decision criteria before you score them#

Compliance burden is the ongoing filing and deadline workload created by your structure. In practice, that means recordkeeping, calendar control, and required returns. For a foreign-owned U.S. disregarded entity, that includes Form 5472 attached to a pro forma Form 1120, and a missed required filing can trigger a $25,000 penalty.

| Criterion | Meaning | Key note |

|---|---|---|

| Compliance burden | Ongoing filing and deadline workload, including recordkeeping, calendar control, and required returns | For a foreign-owned U.S. disregarded entity, this includes Form 5472 attached to a pro forma Form 1120; a missed required filing can trigger a $25,000 penalty |

| Payment friction | Payout timing, settlement constraints, or payment-rail mismatch that keeps delaying money movement | Track actual incidents and separate structural friction from normal onboarding timing; initial payouts are typically scheduled in 7 to 14 days after the first successful payment |

| Client concentration risk | Exposure from relying on too few clients | One major client change in procurement, payout rules, or tax-document requests can disrupt a large share of income |

| Strategic access | Confirmed access to capabilities gated by country or account setup | Treat this as a verification item, not an assumption |

Payment friction is day-to-day cashflow drag: payout timing, settlement constraints, or payment-rail mismatch that keeps delaying money movement. Track actual incidents and patterns, and separate structural friction from normal onboarding timing. Stripe notes initial payouts are typically scheduled in 7 to 14 days after your first successful payment.

Client concentration risk is exposure from relying on too few clients. If one major client changes procurement, payout rules, or tax-document requests, a large share of your income can be disrupted.

Strategic access is confirmed access to capabilities gated by country or account setup. Treat this as a verification item, not an assumption.

Use a practical decision matrix#

| U.S. revenue band | Compliance load | Payment friction | Client pressure | Expected upside | Default move |

|---|---|---|---|---|---|

| Low U.S. revenue band | Heavy relative to current scale | Occasional or unclear | Low, mixed, or one-off requests | Limited unless a verified gated capability is blocking deals | Improve Canadian USD workflow first |

| Medium U.S. revenue band | Material but potentially manageable | Recurring issues with payouts, rails, or settlement control | Moderate, especially if a few clients drive revenue | Real if friction is documented and repeated | Wait unless multiple triggers persist |

| High U.S. revenue band | Still significant, but easier to operationalize | Frequent and costly | High procurement or onboarding pressure | Meaningful if verified access improves collections or retention | Consider moving forward after verification |

A potential false trigger is client documentation pressure. If a client asks for Form W-9, do not assume you need a U.S. LLC. IRS instructions indicate a foreign person may not provide Form W-9. Confirm whether Form W-8BEN is the correct document, since failure to provide W-8BEN when requested may lead to 30% withholding.

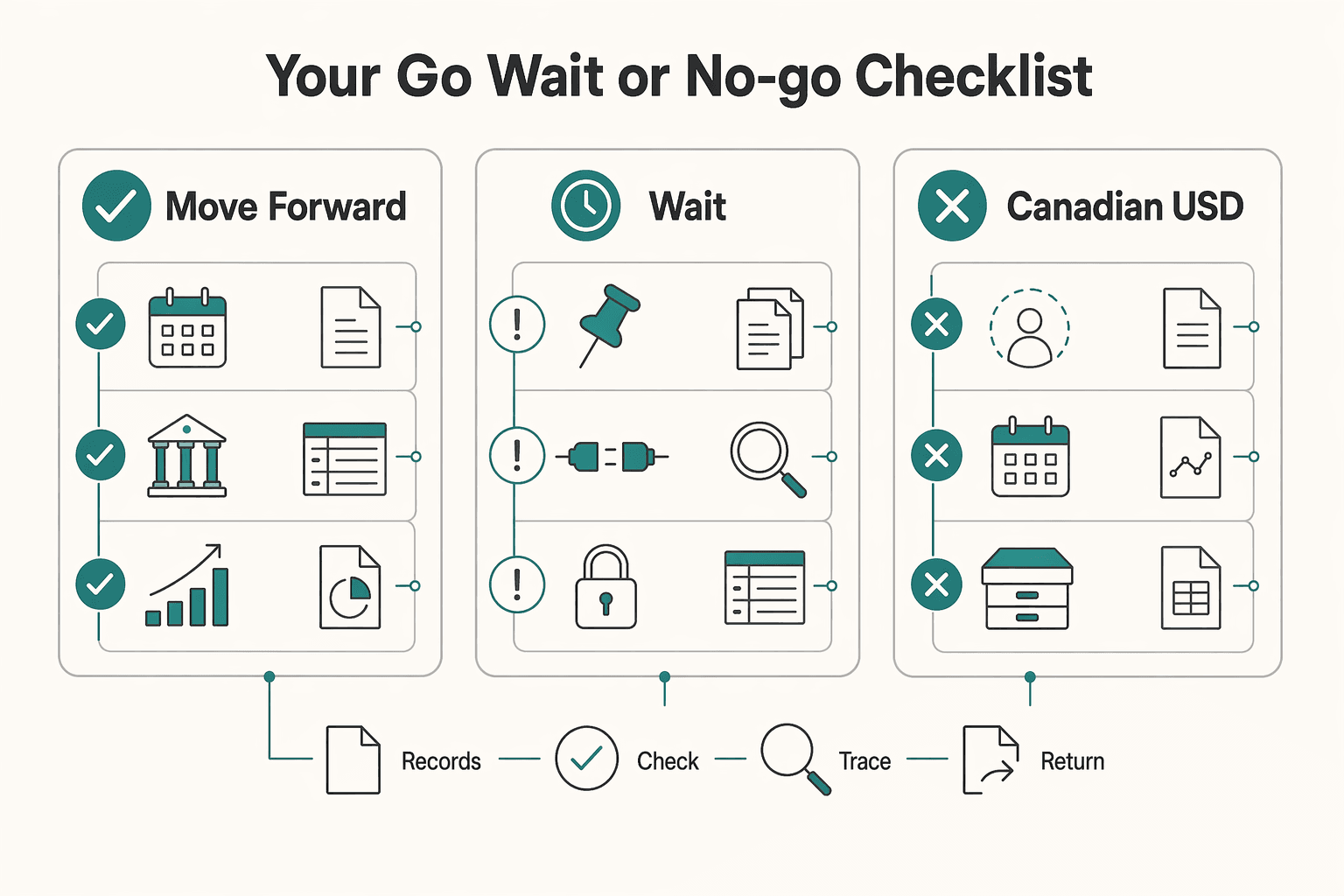

Your go, wait, or no-go checklist#

-

Move forward only if

-

you have recurring, documented payment or onboarding friction - you can run the ongoing filing workload consistently with clean books and evidence - the upside still holds after compliance and admin effort are included

-

Wait if

-

the issue is isolated to one client or a short period - you have not fully tested Canadian USD settlement and payout options - your bookkeeping is not ready for recurring U.S. filing execution

-

Improve your Canadian USD workflow first if

-

your main problem is conversion timing or FX control - clients can already pay you, but money movement is inefficient - you do not have a verified need for a separate U.S. Stripe account

Use access as the final tie-breaker. Verify the exact capability first, for example whether ACH Direct Debit is the feature you actually need and whether it depends on customers with a U.S. bank account. Then confirm current Stripe eligibility and account constraints before committing. U.S. registered businesses must be registered in the U.S., Stripe verifies entity and tax details, and you cannot change account country after activation, so country changes require a new account. Verify current product and country eligibility before you commit.

This pairs well with our guide on The Best Way to Invoice a Canadian Client from a US LLC to Minimize Fees.

Before you pick a structure, run your real client mix and fee flow through this payment fee comparison tool so your decision is based on net cash retained, not headline rates.

Conclusion: Choose Control, Not Complexity#

The throughline here is simple: optimize your Canadian Stripe setup for USD first, and treat a U.S. LLC plus U.S. Stripe account as an escalation only when your current setup cannot meet a specific operational need.

Start with configuration discipline. Stripe supports collecting, accruing, and paying out in non-default currencies when set up correctly, and each enabled payout currency needs its own payout bank account. If you enable USD settlement, confirm that USD has its own payout bank account in your Dashboard and verify your payout routing with a real test payout.

Do not treat a U.S. account as a simple upgrade. After activation, Stripe account country cannot be changed, and using Stripe in another supported country requires a new account with that country's requirements: entity, tax, address, identity, and banking footprint. For U.S. Stripe use, Stripe requires a verifiable TIN and SSN details for associated individuals, so missing or inconsistent records may delay verification.

| Feature | Path A: Canadian Stripe with Canadian USD payout setup | Path B: U.S. LLC and U.S. Stripe account |

|---|---|---|

| Primary Benefit | Keeps USD handling inside your current operating setup with less structural change | Can provide a true U.S. account footprint when a client, platform, or banking requirement clearly needs it |

| Annual Cost | Verify current bank-account and account-maintenance costs before relying on them | Verify current entity, registered-agent, tax, accounting, and banking costs before relying on them |

| Primary Risk | Misconfigured settlement or payout settings can still create avoidable friction | U.S. filing exposure may apply, including Form 5472 scope for foreign-owned U.S. disregarded entities. Verify current penalty exposure before relying on it. |

| Best For | You want cleaner USD collection with lower admin load | You have confirmed U.S.-specific constraints and capacity for ongoing compliance work |

If you escalate, treat compliance as core operating work. A foreign-owned U.S. disregarded entity can fall within Form 5472 scope, and if that filing applies and you need more time, IRS instructions state you can request an extension using Form 7004.

A short decision test:

- Stay on the Canadian path if clients can already pay you through your Canadian Stripe account and your main issue is USD settlement or payout configuration.

- Prepare, but do not switch yet if you see repeated payment friction and can document exactly what fails in your current setup.

- Use a U.S. LLC path only when you have a clear U.S.-specific requirement, can meet Stripe's country requirements, and are ready for ongoing tax and verification obligations.

Next steps, in order:

- Optimize your current setup first: verify USD settlement, add the matching payout bank account, and run one end-to-end payout test.

- Validate compliance obligations second: confirm filing and documentation requirements with a qualified cross-border professional.

- Escalate structure only if criteria are met: move to a U.S. entity or account only when the operational requirement and compliance readiness are both clear.

For a step-by-step walkthrough, see Opening a UAE Bank Account as a Non-Resident Freelancer.

If you want a simpler cross-border setup with invoicing, payout visibility, and compliance-aware operations in one place, review Gruv for freelancers.

Frequently Asked Questions

Do you need a U.S. LLC to accept USD from U.S. clients?

Not necessarily. Stripe states that accounts opened in Canada can use USD-denominated bank accounts, so a U.S. entity is not automatically required just to handle USD. Start by testing that Canadian USD path with your real business banking setup, and only consider a U.S. entity if you confirm a specific access issue your current setup cannot solve.

Can you open a U.S. Stripe account as a Canadian freelancer?

Yes, but only if you meet Stripe’s requirements for opening in another country. That means a legal entity in that country, a tax ID, a physical mailing address (not a P.O. box), phone number, government-issued ID, website, and a physical in-country bank account in a supported transfer currency. Before applying, check that your entity country, bank country, address, and tax ID all align.

Can you use a virtual U.S. bank account or just any USD account?

Not for the in-country bank requirement Stripe describes for another-country accounts. Stripe says that required bank account must be physical, not virtual, while Canada has a specific exception that allows Canadian Stripe accounts to use USD-denominated bank accounts. Choose your path first, either a Canadian account with USD handling or a U.S. account opening, then gather proof for that path.

What do ETBUS, beneficial owner, EIN, and personal versus business tax ID actually mean?

Treat these as compliance terms you need to verify for your exact facts, not terms to guess from a blog. This guide does not provide authoritative definitions for ETBUS, beneficial owner, EIN eligibility, or personal-versus-business tax ID rules across jurisdictions. Ask a qualified cross-border tax professional which definitions and IDs apply to your Stripe onboarding, banking forms, and tax filings, and keep that guidance in writing.

What compliance work should you expect, and should you use a bundled incorporation service or set up the LLC yourself?

Expect compliance and documentation work if you form a U.S. entity, but exact obligations depend on your facts and jurisdiction. The key operational step is to confirm your filing obligations with a qualified professional first, then maintain the documents and deadlines that apply to you. Choose your setup route based on how much direct control you want versus how much guided support you need. | Setup path | What it means for you | Watch for | |---|---|---| | Bundled incorporation service | More guided setup with less hands-on research | You still need to confirm requirements and ongoing filings | | Self-directed LLC setup | More control over each document and decision | More risk of mismatch across address, tax ID, bank, and Stripe country details | | Professional legal/tax help with either path | Extra support for complex facts | Clearer responsibility for definitions and filing requirements |

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- docs.stripe.com/currenciestrusted

- docs.stripe.com/payouts/multicurrency-settlementtrusted

- ecms.newportbeachca.gov/Web/0/edoc/1231212/1974-06-09%20-%20Orange%2...trusted

- federalreserve.gov/frrs/guidance/interagency-guidance-on-corres...trusted

- irs.gov/instructions/i5472trusted

- irs.gov/forms-pubs/about-form-5472trusted

- sba.gov/business-guide/launch-your-business/register...trusted

- stripe.com/resources/more/how-to-effectively-track-smal...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

Ho Chi Minh City Digital Nomad Guide for a 30-Day Move (2026)

Ho Chi Minh City is a strong base if your priority is keeping work momentum while relocating. You get density, plenty of places to work from, and a social scene that can help you settle quickly. It is a weaker fit if your best days depend on calm streets, easy walking, and long stretches of quiet. In practice, Saigon tends to reward people who want convenience and activity more than retreat pace.

How to Open a Stripe Account for a Non-US Business

**Treat your Stripe setup as a system for cashflow, not a quick signup, so your first payouts are more predictable.** If you run a small business, this is one of those setup decisions where "close enough" gets expensive later. If you are a nonresident operator, the pain usually shows up in a few places: payout delays, avoidable verification loops, and uncertainty about which path actually fits your business. If you guess early, you usually create rework later, especially when invoices are already waiting.