Quick Answer

Start by treating pricing as a quote-to-booking control problem, not a fee-table exercise. On fx markup exchange rate spread platforms, the reliable comparison is corridor-level: capture quote ID, timestamp, expiry, executed rate, and net payout, then measure basis-point variance against one time-matched benchmark. Convert that variance into money at your monthly volume and include downstream deductions and return behavior. If those fields are missing, headline fees and mid-market claims are not decision-ready.

Why platform teams keep underestimating FX conversion cost#

Platform teams can underprice cross-border payouts because they start with visible transaction fees and transfer charges, while the rate-layer cost sits inside the conversion rate. Transfer fees are the easiest line item to spot, but exchange-rate margin can be charged separately and may not appear in that fee line at all.

For founders, that can show up as margin drift. For finance, corridor-level expected versus booked payout costs stop matching. For ops, it appears as re-quotes and unexplained shortfalls. For engineering, it becomes a data problem. Without quote ID, quote timestamp, expiry, currency pair, and executed rate, it is hard to reliably reconstruct what happened.

This article is practical: evaluate fx markup exchange rate spread platforms under production conditions, not pricing-page snapshots or demos. A low headline fee can still hide cost inside the applied conversion rate. Regulators and pricing methodology point to the same issue. Total cost is driven by multiple variables, and exchange-rate spread is not always quoted in the transfer-fee line.

What teams miss first#

The first mistake is treating a reference rate as enough. Comparing provider rates to a reference rate is useful, but incomplete. Reference rates are informational and do not necessarily match executable transaction rates. When a provider says it prices “near mid-market,” the real questions are: near it at what timestamp, for how long, and what happens if the quote expires?

Timing is often the gap. Some platforms offer 5 minute, 1 hour, or 24 hour quote windows. If your flow accepts one rate and books later, realized cost can move even when fees do not. Before launch, finance and engineering should align on one corridor test record that captures quote time, quote expiry, executed rate, and the reference-rate timestamp used for comparison. If timestamps are misaligned, the comparison is weak.

Why production payouts distort the neat pricing story#

This matters in payout flows where operational gates can shift execution timing. Approval and risk-review holds can delay fund availability, including holds of up to 72 hours in some provider flows. That does not always change the booked FX rate, but it can change when funds move and whether your original quote assumptions still match execution.

One failure mode is approving commercial terms from sample quotes, then discovering after launch that reconciliation data is too thin to prove rate outcomes. If you cannot export executed rate, rate timestamp, fee components, and payout status events together, you end up inferring leakage from net results.

Use this rule for the rest of the piece: if you cannot measure rate-layer cost separately from visible fees, your comparison is incomplete. The next sections show how to define markup versus spread, test corridor economics, and control quote timing, reconciliation, and policy delays so FX cost stays manageable.

At-a-glance comparison of FX pricing options#

The practical difference between a bank, a fintech payout provider, and a specialist FX platform is usually not the headline fee. It is whether you can separate transaction fee from FX margin, how durable the quote is, and whether post-trade exports let finance prove what actually happened.

How the main provider types differ#

| Provider type | Pricing method you will usually see | Distance from mid-market or interbank reference | Treatment of correspondent fees | Handling of stale quotes | Audit export depth |

|---|---|---|---|---|---|

| Banks | Commonly spread-based pricing, sometimes alongside explicit transfer fees | Harder to test if margin is not itemized; benchmark checks need timestamp alignment | For some cross-border currency flows, correspondent-bank processing can apply, so inclusion or exclusion must be explicit | Product-specific; expiry and reprice rules are not always clear in front-end quotes | Varies; confirm you can tie quote, conversion, fees, and payout events |

| Fintech or MTO-style providers | Often explicit fee plus rate, with possible embedded margin | Usually easier to compare in basis points if you capture quote time and execution time | May be passed through, absorbed, or partially disclosed by corridor or contract | Some providers offer guaranteed windows, with repricing after expiry | API and dashboard visibility varies; confirm export completeness |

| Specialist FX platform | Pricing can be negotiated around spread, size, and execution method | Benchmark only when booked-rate evidence is available | Must be defined in commercial terms, not assumed | Can be firm for defined windows when terms are explicit | Varies; confirm trade- and payout-level detail for your integration model |

Use this table to narrow options, not to prove economics. ECB reference rates are informational, published once per working day around 16:00 CET for 30 currencies, and should not be treated as executable outcomes. If a provider claims “near mid-market” or “interbank,” ask for the exact timestamp, corridor, and execution window used in that comparison.

What headline claims still leave unknown#

Public comparisons may not tell you the corridor mix, the volume-tier assumptions, or whether quoted economics include non-covered third-party fees at the receiving institution. World Bank remittance data is useful for provider-type comparisons, but taxonomy and corridor counts can differ by dataset vintage, so version labels matter.

For your deal, contract clarity matters more than marketing labels. If pricing is presented as “all in” but terms are silent on correspondent or downstream institution fees, you still carry reconciliation and cost-risk exposure. Require one evidence pack per priority corridor with quote ID, quoted rate, expiry, executed rate, visible fees, and any third-party deductions.

A common issue to test is stale-quote repricing. At least some providers document that a guaranteed rate is time-limited and reverts to a live rate after expiry. One documented example uses 2-48 hour lock windows, depending on currency, and can refresh after 30 minutes during setup. That is material if your flow includes approval, funding, or manual-review delays.

Matching the model to your payout pattern#

Start with payout shape, not provider category. The right model is the one that gives you acceptable economics and execution control under your actual operating pattern.

| Payout pattern | What to prioritize | Typical fit |

|---|---|---|

| Low-frequency, high-value payouts | Quote firmness, negotiated spread, explicit expiry and reprice terms, and conversion-level evidence | Bank or specialist channels may fit if reporting supports deal-level validation |

| High-frequency batch payouts | Deterministic quoting, API-level status events, and fast reconciliation across many conversions | Fintech or MTO-style rails may fit when data exports are complete |

Working rule: choose the model that gives you both acceptable economics and auditable execution control. If a proposal does not clearly state corridor mix, pricing-tier assumptions, quote-expiry behavior, and downstream fee treatment, the comparison is incomplete.

What markup and spread actually mean in contracts#

Contract labels alone do not tell you total cost. If a contract uses "spread" in one place and "fee" in another, do not assume the economics are different. Verify the booked rate, fee lines, and timing terms together.

Contract labels versus real cost#

| Contract language | What it can mean in practice | What to verify |

|---|---|---|

| FX markup | A provider-added margin over a base or reference rate, often embedded in the conversion rate | Which benchmark is used, the quoted rate, and whether markup is explicit or only implied in the rate |

| Exchange rate spread or bid/ask spread | The bid/ask gap, but in customer contracts it may also be used as shorthand for provider-retained margin | Whether you receive a clear customer rate and full all-in disclosure |

| Transaction fees or itemized fees | A visible fee charged outside the rate | Whether the rate is correspondingly closer to the reference, or both fee and margin are being charged |

| Mid-market + fee | A reference-style claim that still depends on quote timing and repricing terms | Quote expiry, re-quote logic, funding timing, and whether the final booked rate can move before receipt |

Rebundling can happen. At least one major platform states that the same conversion economics can be shown either through an adjusted rate or a separate conversion fee. Another states that its conversion rate includes a spread retained by the provider. Compare total outcome, not presentation style.

Where mid-market claims break#

"Mid-market + fee" is only reliable if the contract defines when the rate is fixed. A guaranteed rate is time-limited, live-rate flows can move between send time and provider receipt, and some card flows may apply a processing-time rate instead of an authorization-time rate.

Use a simple contract checkpoint: require timestamp, expiry, executed rate, and all additional fees in both transaction views and statement exports. Treat "mid-market" or "interbank" claims as incomplete when expiry, processing-time fallback, or markup language is vague. In EU-facing card conversion contexts, Regulation (EU) 2021/1230's percentage-markup-against-ECB format is a clearer comparison basis than generic "competitive spread" wording.

How to compute all-in FX cost before go-live#

Do not wait for live volume to find hidden FX cost. Use one repeatable sequence: capture the provider quote, capture one external reference at the same timestamp, convert the gap to basis points, then convert basis points to money by corridor and monthly volume.

Use one calculation path every time#

| Input | What to capture | Why it matters |

|---|---|---|

| Provider quote | Quote ID, currency pair, source amount, target amount, explicit fee, timestamp, expiry | Confirms the exact commercial offer |

| External reference | One source for that test round, such as a Reuters-linked benchmark, a mid-market reference, or Google Finance, with exact timestamp and pair orientation | Keeps the comparison consistent without assuming sources have identical methodology or latency |

| Output | Reference payout, actual net payout, shortfall, bps variance, money impact | Produces an auditable finance result |

A basis point is 0.01%. For pre-go-live testing, compare delivered net payout value, not contract wording, and use one variance formula every time in your test pack: bps variance = ((reference payout value - actual net payout value) / reference payout value) × 10,000. That makes embedded-rate pricing and itemized-fee pricing comparable.

If the provider quotes USD/EUR and your reference is EUR/USD, normalize the pair first. If there is a separate fee, convert it into payout currency or subtract it from delivered proceeds before calculating variance.

Turn basis points into money#

Basis points only matter when you turn them into money. In this illustrative example, USD 100,000 converts to a reference payout of EUR 92,000, but actual net payout is EUR 91,724; shortfall is EUR 276, or 30 bps. On 20 similar monthly payouts, that is EUR 5,520.

For cross-border batch runs, test with real ticket sizes and real execution timing. A quote that looks fine once may not hold when quotes expire, refresh, or book later in the flow.

Test by corridor, not blended average#

Do not approve on one blended average across currencies. Test USD/EUR and your top payout corridors separately, then decide based on your real mix.

World Bank corridor surfaces are a useful reminder to version your benchmark inputs: one surface shows 367 corridors and another shows 365. Record which dataset surface or version you used in your test pack.

Make finance and engineering sign the same math#

Use one verification checkpoint. Finance and engineering should sign off on the same formula, timestamp source, and definition of “net payout.” If teams use different timestamps or different reference captures, they are not validating the same event.

If quote locks are available, record lock window and expiry behavior in evidence. For example, Stripe documents 5 minute, 1 hour, and 24 hour locks, and states a lock can expire if rate movement exceeds 3.5%. Approve go-live per corridor only when the formula, timestamp source, and monthly money impact reconcile across finance and engineering. Related: How Platforms Are Reshaping the Market of Foreign Exchange: A 2026 Deep Dive.

Hidden cost points that appear after pricing approval#

Signed pricing is not the same as realized payout cost. Once you move from approval to production, leakage can appear through third-party deductions, timing-driven repricing, delayed adjustments, and limited disclosure around foreign exchange costs.

Use one rule: approve only what you can trace from quote to final beneficiary amount. In cross-border payments, visible fees are only one layer. The World Bank methodology treats transaction fee, exchange rate, margin, and service speed as separate cost components, so headline comparisons can look cleaner than settlement reality.

| Leakage point | How it shows up after approval | What you should demand |

|---|---|---|

| Correspondent fees | The beneficiary receives less than the instructed amount because correspondent or beneficiary banks deduct charges | Corridor-level disclosure of who bears charges, whether payments are sent as SHA or another charge option, and reporting of instructed amount versus final credited amount |

| Asynchronous adjustments | Fees or deductions appear after the payment is processed, sometimes weeks or months later | Post-trade event feed and monthly adjustment reports tied to the original payment ID |

| Return handling | A failed or returned payout can create additional cost uncertainty when reprocessing terms are unclear | A documented return and re-conversion policy, including which rate is used and which fees survive the return |

| Settlement timing mismatch | Rate shown at quote or authorization differs from the rate used when conversion is actually processed | Quote ID, acceptance timestamp, booked rate timestamp, expiry logic, and stale-quote rejection behavior |

Correspondent fees are easy to underestimate because they often sit outside the headline price. Banks state that beneficiary banks may deduct fees and that the beneficiary may receive less than the original transfer amount. Under SHA charging, you pay your bank’s charges while other charges can fall to the beneficiary side. U.S. consumer guidance also notes these deductions are not always required to be stated as exact amounts up front. That means approved commercial terms may not equal full-principal delivery.

Timing mismatch is another common failure mode. One rate can be accepted and another applied later if quote and booking timestamps are not captured together. Card-network guidance shows this clearly: if an authorization-time rate is unavailable, conversion can use the processing-time rate, and displayed conversion amounts can be indicative only. The same risk can appear in payout flows when providers quote early but book later.

Set a stricter checkpoint than “rate accepted.” Require five fields on every conversion record: quote ID, quote timestamp, expiry time, final booked rate, and booked timestamp. If any are missing, finance cannot prove whether spread movement came from market change, provider logic, or operational delay.

Disclosure quality matters just as much as price. FCA guidance defines a reference rate as the benchmark used for pricing and calls out markup above that reference rate. So “zero-fee” FX should not be read as zero FX markup. Cost can be moved from an itemized fee into the rate layer, similar to providers that say their rate includes a currency conversion spread retained on a base exchange rate.

Two practical red flags are worth treating as blockers: no corridor-level breakdown of delivered amount, foreign exchange fees, and downstream deductions; and no clear policy for returns, rejections, or stale quotes. Notes from treasury teams that automate FX data into decision-making are a useful reminder that operational visibility matters. If you cannot get quote-to-book traceability plus beneficiary-side outcome reporting, pricing approval is incomplete, regardless of headline rate.

Picking the right model by payout pattern and corridor mix#

Pick the model by payout shape first, then validate corridor behavior under real execution timing. In practice, high-frequency low-ticket flows can reward tighter quote controls, while low-frequency high-value flows can reward stronger markup terms, as long as lock terms hold through funding.

| Payout pattern | Prioritize first | What to verify before go-live | Main risk if you skip this |

|---|---|---|---|

| High-frequency, low-ticket payouts | Deterministic quote handling and low exception overhead | Transfer-usable quote object, unique quote ID, lock window, and clear expiry behavior | Small repricing drift repeated at scale |

| Low-frequency, high-value payouts | Competitive FX markup at real ticket size and corridor mix | Lock duration, expiry terms, and whether quotes can be withdrawn | Approval-time economics differ from execution-time economics |

| Volatile corridors or timing-sensitive approvals | Explicit stale-quote rejection and refresh flow | Clear separation of indicative or reference pricing versus executable pricing | Team treats a reference rate as executable and absorbs slippage |

For high-volume payout operations, prioritize control and traceability before chasing a slightly better headline spread. FX costs are often a mix of explicit fees and exchange-rate margin, and comparison breaks down when only part of that stack is visible.

For large, infrequent payouts, negotiate markup and lock terms together. Lock windows are time-bounded in market examples. One model uses 2-48 hours, while another offers 5 minutes, 1 hour, or 24 hours, with a 1-day cap. The commercial benefit depends on how your approval and funding timing actually works.

Treat quote labels carefully in volatile corridors. A guaranteed rate may be unavailable in volatile markets, expired locks can reprice at receipt time, and some time-bounded quotes are still not standing offers to transact FX and can be withdrawn.

Do not treat reference benchmarks as execution protection. ECB reference rates are informational, not intended for transaction use.

For route choice, compare direct-bank and aggregator or specialist paths on reliability, transparency, and exception-handling workload. Cross-border payments are structurally complex, correspondent banking is still prevalent, and intermediary hops can add fees and delays. Direct participation also typically requires direct connectivity and a central-bank settlement account.

Decision rule: for operationally noisy, high-frequency books, prefer the route with stronger quote integrity and exception visibility. For high-value books, prefer the route with stronger negotiated markup and clear lock-duration and expiry behavior. In volatile corridors, require stale-quote rejection instead of relying on indicative pricing.

Quote integrity controls product and engineering must implement#

If you do not control the quote lifecycle, production will quietly erase any pricing win. Implement quote lifecycle controls. Fail closed on expired quotes, and make retries idempotent end to end.

| Control area | Weak implementation | Strong implementation | What to verify before launch |

|---|---|---|---|

| Quote lifecycle | Treats every quote as usable until provider rejection | Separates indicative, locked, expired, and rejected states | Quote payload stores createdTime, an expiry field such as rateExpirationTime, and current quote state |

| Expired quote handling | Falls through to prevailing rate without policy check | Fails closed with a QUOTE_EXPIRED-style error and requires a fresh quote | Expiry test creates no conversion and no payout side effect |

| Retry safety | Retries POSTs and webhooks without idempotency or dedupe | Uses idempotency keys on writes and event-ID dedupe on callbacks | Timeout retry with the same key does not create duplicate provider actions or duplicate ledger postings |

| Audit trail | Logs only final settled amount | Logs provider reference, quote timestamp, rate source identifier, booked rate, and transaction linkage | Finance can trace one currency conversion from quote through payout |

Model the quote as a state machine#

Make the quote state explicit: indicative, locked, expired, converted, rejected. Airwallex documents indicative versus guaranteed behavior, and Wise exposes both createdTime and rateExpirationTime, so your platform has enough data to enforce state instead of inferring it.

Do not let expired quotes proceed into live conversion. Wise states that an expired quote is not usable to create a transfer if not used within 30 minutes of creation. PayPal instructs integrators to retrieve and lock a rate before processing. It also states that if a locked rate is no longer valid, processing can occur at the prevailing rate. If you accept that path without explicit policy, you have silent repricing.

Build retry protection for both APIs and webhooks#

Use provider idempotency controls and your own dedupe controls. On writes, send controls like PayPal-Request-Id or an Adyen idempotency key, and retry with the same key after timeout or no response. Adyen documents key validity for a minimum of 7 days.

Treat webhooks as at-least-once delivery. Stripe warns that duplicate events can occur, and Adyen documents three immediate retries followed by queued retries for up to 30 days. Ledger posting should key off internal conversion intent plus processed event IDs, not callback timing alone.

Log enough detail to explain the rate later#

For each currency conversion, record the provider reference, such as PayPal fx_id or an equivalent quote ID, along with the quote timestamp, expiry timestamp when present, final booked rate, and transaction linkage. Also record the rate source identifier and rate type.

That record helps you separate FX markup from spread movement or expired-lock fallout. Before launch, run one forced-expiry test plus timeout and duplicate-webhook simulation. Confirm the flow yields either one booked conversion or one clean rejection, with no duplicate ledger posting.

Reconciliation evidence finance teams should require#

Finance should require a transaction-level evidence pack that ties each payout to its quote, conversion outcome, fee breakdown, and final status. Without that, it is hard to explain FX variance or show whether a shortfall came from rate movement, fees, or route deductions.

| Evidence item | Why finance needs it | Practical source or field | Red flag if missing |

|---|---|---|---|

| Quote reference | Links the payout to the priced conversion | Wise quoteId required to create the transfer | You cannot reliably link the payout to the original priced conversion |

| Conversion outcome record | Shows what actually happened in conversion and payout flow | Provider transfer record plus ledger journal linkage | Only quote or indicative pricing is stored |

| Itemized fees | Separates transaction fees from rate-layer effects | Stripe balance transaction fee_details | Fees are netted into one total |

| Route deductions | Captures downstream intermediary or recipient-bank deductions | Bank tracking, returned wire detail, advised charges by currency | Payout shortfall is misclassified as FX |

| Status events | Confirms payout lifecycle outcome | Wise transfer state change webhook; Stripe payout.paid or payout.reconciliation_completed | Cash movement and payout status diverge |

What the minimum pack should contain#

At minimum, retain the provider quote ID, a conversion outcome record, itemized transaction fees, any visible intermediary or recipient-bank deductions, and payout status events. Wise is explicit that a quote is required for transfer creation and that transfer creation includes quoteId and recipientId, so quoteId should be preserved end to end.

For Stripe flows, use balance transactions as a core reconciliation object and keep fee_details with payout identifiers in the same reporting slice. That helps finance distinguish fee drag from exchange-rate movement.

Reconcile by corridor, not just blended totals#

Reconcile expected versus actual results by corridor and route, not only monthly blended totals. Aggregate performance can look acceptable while a specific corridor absorbs recurring intermediary deductions or other routing effects.

If a payout is short, do not attribute the full gap to FX until downstream deductions are ruled out. Recipient and intermediary bank deductions can occur during processing, and advised charges can be tracked by currency.

Make the ledger the source of truth#

The ledger should trace one request to one conversion to one payout outcome, with exception flags when that chain breaks. A practical checkpoint sequence is: payout request created, quote linked, funds converted, outgoing payment sent, then payout status confirmed.

Watch manual payout paths closely when you rely on transaction-level reconciliation. Stripe notes that transaction-level reporting is not supported for funds that comprise manual payouts. Stripe also notes fee-reporting lag of up to 96 hours and a 30-day event retrieval window, so retain raw webhook and event data rather than relying on UI history alone.

When you choose a provider, favor the option that gives finance auditable quote linkage, itemized fees, and payout-status evidence at corridor level.

Related reading: How to Negotiate a Higher Rate with a New Client.

Compliance and policy gates that change real FX outcomes#

Compliance gates can change realized FX outcomes even when reconciliation is clean. If KYC, KYB, AML, or sanctions checks delay or pause payouts in a corridor, treat that timing risk as part of FX cost, not as a separate ops problem.

Timing is the mechanism. Exchange rate mark-up is the difference between the interbank rate and the rate offered to the customer, and realized outcome depends on when conversion is allowed to execute. If a quote is valid for 5 minutes, 1 hour, or 24 hours, a hold beyond that window can push execution to a different rate or different quote handling, including fallback to mid-market processing when an extended quote becomes unusable.

| Gate or policy event | What it changes operationally | FX consequence to model | What you should verify |

|---|---|---|---|

| Verification tier escalation | Payouts can be temporarily disallowed until extra checks are completed | Quote can expire before execution | Country, legal entity, processed amount thresholds, and current tier |

| Platform payout pause | In-flight payouts can remain pending for up to 10 days | Execution timing drifts beyond quote assumptions | Whether pauses stop processing or only settlement status |

| Missing required verification data | Payouts can be disabled on deadline schedules such as 14 days after due date | Expected rate benefit may never be realized | Due dates, outstanding requirements, and remediation owner |

| Sanctions or OFAC screening | Transactions, including wire transfers and foreign exchange, can be blocked or rejected | No execution, or delayed reprocessing at a later rate | Reject-versus-block handling and retry policy |

Coverage is not uniform across markets or programs. FATF standards are implemented with local differences, and platform settlement options vary by country, so your model should not assume identical payout eligibility, processing timelines, or rate treatment across corridors.

Decision rule: if compliance holds occur in a corridor, model extra timing-related rate risk before accepting any “best rate” claim. Ask for executed-rate evidence on held payouts and timestamps for quote creation, quote expiry, hold start, hold release, and payout completion.

Procurement red flags in vendor pricing claims#

Procurement should reject FX proposals that market a mid-market rate but do not disclose all fees, quote timing, and fallback pricing behavior. If those terms are missing, you cannot validate all-in conversion cost.

What deserves an immediate red flag#

A common failure is presenting a reference screen as if it were an executable customer rate. Mid-market is a market midpoint, not a transactional rate, so “mid-market + fee” is incomplete unless the vendor shows booked-rate logic and execution terms.

| Proposal pattern | Why it is weak | What you should require |

|---|---|---|

| “Mid-market rate” headline only | Reference rate is not an execution promise | Booked-rate examples with quote timestamp, expiry, and executed rate |

| “No fee” or “zero fee” language | Cost can still sit in rate margin or other charges | Full fee schedule with transaction fees and currency conversion charges |

| Public “bank-beating” comparison table | Data may be marketing-led, stale, or not corridor- or amount-matched | Independent side-by-side checks at your corridor and payout amount |

| “Firm quote” without fallback terms | Quote may expire, be withdrawn, or convert later at a live rate | Contract terms for expiry, re-quote, withdrawal, and failure handling |

Quote-window mechanics are material. Some quotes are offered for 5 minute, 1 hour, or 24 hour windows. Some guaranteed-rate models run for 2-48 hours. Outside the lock window, conversion may happen at a live rate when funds are received and processed. If the model is unclear, your forecast is incomplete.

What to ask for at corridor level#

Do not accept blended averages. Ask for corridor-level examples on your real payout sizes, because total cost is a mix of rate, margin, fees, and timing.

For each corridor, require:

- Quoted rate and benchmark reference used for comparison.

- Transaction fees and currency conversion charges.

- When

wire transfercharges can apply and who pays intermediary deductions. - How failed, returned, or delayed payouts are handled, including repricing where applicable.

- If

swap feesare mentioned, the exact contract scenario where they apply.

A practical check is a side-by-side comparison against an independent benchmark reference (for example, Reuters), with timestamp and execution window shown together. Timestamp alignment matters when benchmark rates are published at fixed points.

How to treat public comparisons#

Treat vendor-owned comparison pages as directional, not procurement proof. Some pages explicitly state that data is not real-time and is provided for marketing use.

Use public tables to shortlist. Contract only after independent, corridor-matched verification and written fallback pricing terms. If a vendor will not provide that evidence, move on.

Decision checklist before selecting an FX provider#

Do not sign on headline rate alone. Select the provider that still gives you a reliable all-in price, predictable exception handling, and a defensible audit trail when real payouts start failing, returning, or arriving late.

| Check area | What you need confirmed | Red flag | Acceptance evidence |

|---|---|---|---|

| Commercial | Contract language defines FX markup, exchange rate spread or bid-ask spread, reference rate, and every non-rate fee | "Market rate" language without booked-rate logic or full fee schedule | Signed pricing schedule, corridor-level examples, statement sample showing FX rate plus additional fees |

| Technical | Quote expiry handling, stale-quote behavior, idempotent retries, webhook coverage, reconciliation fields | Indicative quote treated as locked, or no duplicate-prevention semantics | API docs, test evidence, sample events, retry test results, reconciliation field mapping |

| Operational | Returned payout states, payout failure reasons, unmatched deposit handling, reconciliation inputs | Manual exception handling with no structured reason codes or report path | Sample reports, payout state list, return timing examples, inbound deposit reporting |

| Governance | Named owners and measurable launch criteria across pricing, integration, and operations | Pricing approved before integration, reconciliation, and exception controls are proven | RACI or approval record, launch checklist, monitoring and termination plan |

Commercial terms that survive legal review#

Start with contract language, not sales language. Confirm whether pricing is a reference FX rate plus management fee, spread-table based, or an all-in price. If quotes are driven by user spread tables, treat spread configuration as a commercial term.

Also verify disclosure behavior end to end: FX rate and additional fees should be clearly shown at transaction time and on statements. If clause, fee schedule, and statement sample do not align, pricing is not yet procurement-ready.

Technical terms that prevent silent repricing#

Assume indicative quotes are not locked until conversion is booked. Your acceptance criteria should explicitly cover quote validity window, post-expiry behavior, and countdown handling before confirmation.

Require retry behavior to be both documented and tested. Idempotency should prevent duplicate effects on POST retries, including within documented key windows such as 24 hours. For webhooks, validate coverage and redelivery behavior instead of assuming exactly-once delivery. Retries, such as 5 more attempts after a failure, help, but reconciliation still needs to prove completeness.

Operational terms for real cross-border payments#

Before launch, walk three failure paths: returned payout, unmatched inbound deposit, and payout failure after conversion. Require structured states and reason codes, not support-only workflows.

Map provider timelines and states into your ledger and support processes. Examples include payout states such as processing, posted, failed, returned, and canceled, typical return timing of 2-3 business days, and auto-return windows for unclaimed items of 30 days. For reconciliation, confirm required report combinations and inbound wire or deposit coverage up front.

Governance terms before go-live#

Treat governance as lifecycle control, not a one-time pricing check. Define owners and gates for selection, contracting, launch, monitoring, and termination, with clear lines of responsibility.

Use a hard go-live rule. Named owners should sign off on corridor-matched realized cost logic, quote-expiry and idempotency behavior, and return-state handling plus report ingestion. If any gate is still unresolved, delay launch.

Before procurement sign-off, run your top corridors through a structured variance check with the Payment Fee Comparison.

Final takeaway for platform decision-makers#

Treat FX provider choice as an operating decision, not a headline-price decision. The practical winner is the provider whose FX margin, applied rate, and total fees stay measurable from quote through statement across your real corridors and exception volume.

| Decision lens | What it shows | What it misses | Approve only if |

|---|---|---|---|

| Headline fee or "zero-fee" claim | Visible transaction charge | Embedded rate margin and post-quote changes | You can also see applied exchange rate and total fees on booked transactions |

| Demo quote or benchmark snapshot | Point-in-time pricing | Expiry handling, withdrawals, and timing drift | Quote ID, timestamp, expiry, and final booked rate are all retained |

| Reconciled production outcomes | Realized all-in cost | Little, if the event trail is complete | Finance can match quote, execution, status changes, and statement references |

This standard matters because total cost is not one number. World Bank methodology separates transfer fee from foreign exchange margin and flags low transparency as a key driver of higher prices. If a vendor discussion stays at wire fee level or broad "mid-market" language without the booked rate, your conversion cost is still unclear.

Test the corridors that matter#

Do not approve on a blended average. World Bank RPW tracks country corridors, and as of its August 18, 2025 update it covered 367 corridors across 48 sending and 105 receiving countries. Follow that logic: test your highest-volume send and receive pairs separately, because results can vary by corridor.

Run a production-like pilot, not a sandbox screenshot. For each corridor, capture send amount, recipient amount in local currency, applied exchange rate, fixed and variable fees, quote timestamp, and booked timestamp. If those fields are missing in normal and exception cases, you are testing messaging, not price integrity.

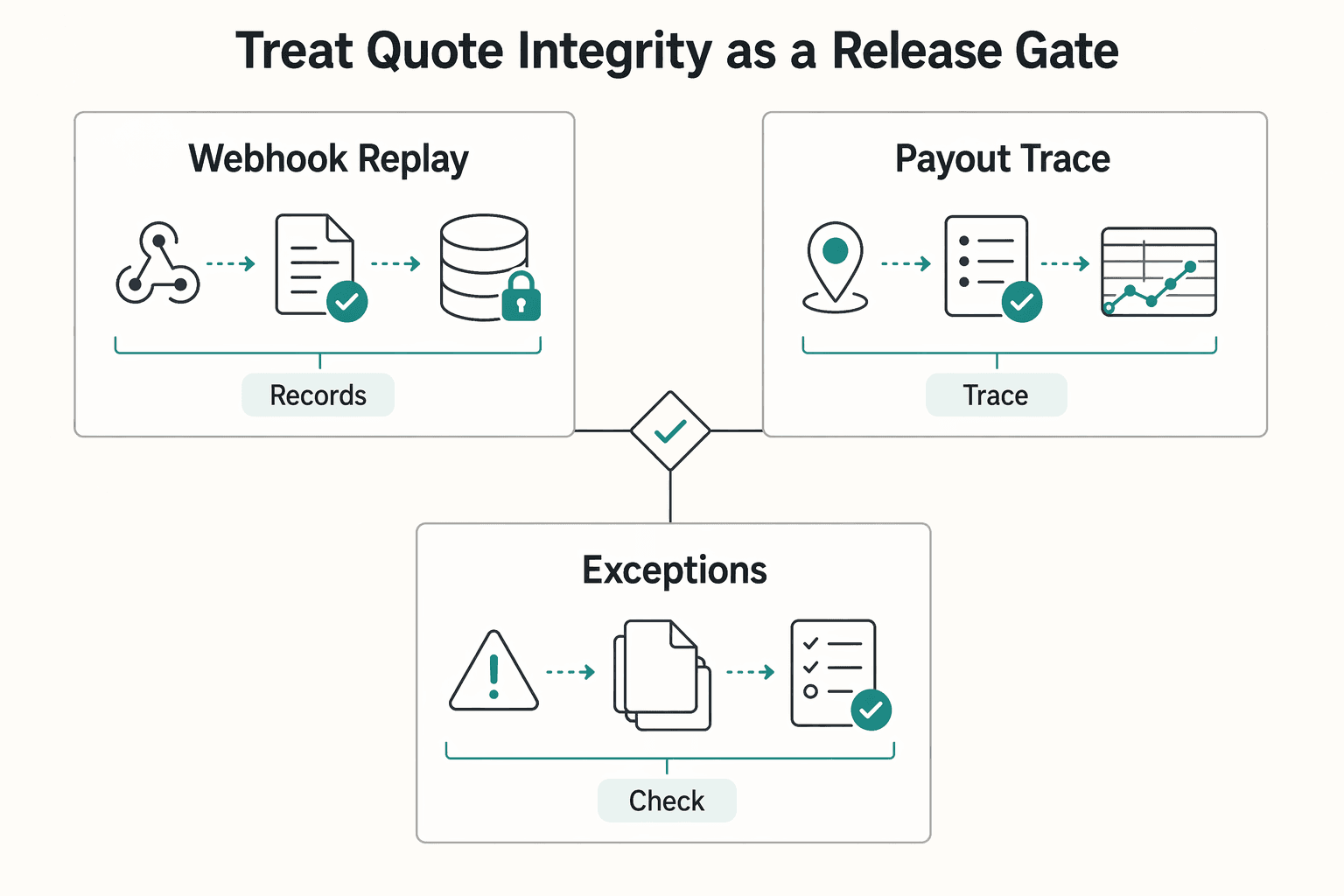

Treat quote integrity as a release gate#

Use quote controls as a hard go/no-go check. Extended quote windows, such as 5 minute, 1 hour, or 24 hour options, can reduce uncertainty, but a quote window is not the same as a guaranteed, irrevocable rate. Your system should fail closed on expiry or withdrawal, not silently reprice.

Require engineering to log quote ID, provider reference, timestamp, expiry, final booked rate, and status events for every payout. Keep transfer records current from webhook status updates, and enforce reconciliation that links notification IDs to statement reference fields. That traceability is what lets finance verify quoted versus realized economics.

Include delayed and held transactions in the pilot, not only happy-path payouts. Timing shifts from AML, compliance, or fraud checks can change realized outcomes even when the initial quote looked competitive.

Run a pilot on your highest-volume corridors with representative exceptions. Approve only when your review owners can confirm two outcomes: acceptable all-in realized cost and full traceability from quote to payout to statement. If either fails, the cheaper-looking option is not the cheaper operating choice.

For a step-by-step walkthrough, see How EOR Platforms Use FX Spreads to Make Money. If you need compliance-gated execution with status visibility and audit-ready payout records, review Gruv Payouts.

Frequently Asked Questions

What is the practical difference between FX markup and exchange rate spread on payment platforms?

In practice, they can describe a similar cost from different angles. The CFPB describes spread as the percentage gap between a retail rate and a wholesale benchmark, while the FCA describes markup as the amount charged above a provider reference rate. If a provider cannot show both the applied rate and the markup over its stated reference, transparency is limited.

Why can FX cost more than the visible wire or transaction fee?

Because part of the cost can sit inside the exchange rate, not only in the fee line. World Bank methodology treats total cost as transaction fee, exchange rate applied, and any margin charged, and that margin may not appear in the visible transfer-fee line. Recipient-side deductions can also reduce what is actually received, including recipient-bank fees and foreign taxes.

How do teams quickly calculate hidden FX cost on a single payout?

Use one transaction and pull four fields first: send amount, applied FX rate, recipient amount in local currency, and all fixed or variable fees. Compare the applied rate against your chosen reference at a matched timestamp, calculate the rate gap on the payout amount, then add visible fees for an estimated total cost. If you use ECB reference rates, treat them as informational benchmarks rather than transaction rates.

Which data points should we demand from providers before signing?

Ask for the applied exchange rate, recipient amount in local currency, markup above the reference rate, variable fees, fixed per-transaction fees, and total remittance fees. These are core disclosure fields in FCA transparency examples and a practical baseline for later reconciliation. If a provider cannot show those fields together in a sample quote, receipt, or statement, pricing evidence is still incomplete.

What is the biggest red flag in “mid-market” or “zero-fee” marketing?

The main red flag is a headline claim without the applied rate and full charges on the actual transaction. CFPB warns that it may be deceptive to market remittances as “no fee” or “free” when they are not in fact free. If “mid-market” appears in marketing but the applied rate, markup, and total fees are missing in the contract or sample output, treat price visibility as incomplete.

Why are public spread percentages hard to compare across vendors?

Because provider pricing is multi-variable, not a single number. World Bank notes that comparison is difficult for that reason, and public figures often mix different corridors, send amounts, fee treatment, and timing assumptions. Even where EU Regulation 2019/518 uses percentage markups over ECB reference rates to support comparability, that still does not make all public percentages directly comparable across vendors or programs.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/press/p250930.htmtrusted

- bis.org/publ/qtrpdf/r_qt1612c.pdftrusted

- bsaaml.ffiec.gov/manual/OfficeOfForeignAssetsControl/01_eptrusted

- consumerfinance.gov/compliance/circulars/consumer-financial-prot...trusted

- consumerfinance.gov/rules-policy/regulations/1005/interp-31trusted

- ecfr.gov/current/title-12/chapter-X/part-1005/subpart...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalregister.gov/documents/2024/04/17/2024-08007/consumer-fin...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: