Quick Answer

Use a layered control model. The article’s core recommendation is to start with the strongest base your records can support (2-way against PO, or 3-way with dependable delivery evidence), then add contract price validation, duplicate checks, and an enforceable exception workflow before release. Payment should only move after one clear outcome is set: auto approved, queued for review, or blocked. This is how platform teams reduce overpayment paths that clean document matching alone does not close.

Why Invoice Matching Matters for Platform Teams#

Platform teams do not need another glossary entry on invoice matching. They need controls that stop real overpayment paths before money goes out the door. At its core, invoice matching compares an invoice with supporting records before payment. The practical question is what you add when a clean match still does not mean the invoice should be paid as submitted.

- Use the right base match

Start with the document pair you can actually verify. 2-way matching compares the invoice to the purchase order (PO) to confirm core details such as vendor, items, and agreed pricing. 3-way matching adds receipt evidence so quantity and condition can be checked against what was actually delivered. Its value depends on how dependable that receipt evidence is.

- Cover the gaps matching does not close on its own

A passed PO or receipt check is not the same thing as a commercially correct invoice. You may still need contract price validation where negotiated terms are not fully represented in the PO. You also need duplicate invoice detection, because duplicate submissions are a known error class. The real checkpoint is whether your approval logic checks only document consistency, or also checks what should be paid under the actual commercial terms.

- Make exceptions enforceable, not informal

Automation matters because it applies rules against the records that define what should be paid before approval. That lets standard invoices keep moving while true exceptions are routed for review. An exception workflow should assign ownership and escalation clearly: who reviews the mismatch, what evidence they need, and when payment is blocked rather than waved through. Without that routing, teams can drift into manual overrides, which can create audit gaps and overpayment risk.

This article focuses on that real-world middle ground. It compares concrete automation options, shows where each one breaks, and gives decision checkpoints Finance, Ops, and Engineering can put in place quickly. The thread is simple: pick the base match your evidence can support, then layer the controls that catch what matching misses, especially contract pricing, duplicate detection, and rule-based exception handling.

Related reading: Best Way for a German Agency to Pay a US-Based Freelancer.

How to choose the right matching model for your platform#

Choose the matching model your evidence can reliably support, not the one that sounds more advanced. In multi-entity accounts payable (AP), teams often label a process as 3-way matching even when PO or receipt records are not consistent enough to stand up in review.

- Use this section when legal-entity boundaries already affect payment operations

This guidance is most useful if AP runs across multiple legal entities and invoices intersect with product-led workflows. In Oracle matching, the PO available for matching must have the same legal entity as the invoice, so weak entity alignment directly weakens matching quality.

- Do not overbuild when document discipline is still weak

If you are a single-entity team with low invoice volume and inconsistent PO or delivery-note capture, a heavier model can add manual review without adding dependable control. That does not make 3-way wrong. It means the better first move is to improve document consistency.

- Set the model against four criteria before configuration

Decide up front based on overpayment risk, ability to verify receipt, tolerance for manual review, and need for an audit trail plus reconciliation pack. A practical check is whether you can consistently produce the invoice, PO, and receipt evidence, such as a product receipt or delivery note, where your process uses one. As transaction volume rises, receipt-invoice discrepancies tend to rise too, so stricter matching only helps if your exception workflow can absorb that load.

- If receipt evidence is unreliable, start with strict 2-way matching

2-way matching checks invoice lines against PO lines. 3-way matching adds product receipt lines. If you cannot reliably produce both PO and receipt evidence, use strict 2-way matching plus compensating controls, and document accepted discrepancies against tolerance. A passed match without review evidence is a label, not a control.

If you want a deeper dive, read 3-Way PO Matching for Marketplaces: How to Automate Invoice Verification at Scale.

Want a quick next step? Try the free invoice generator.

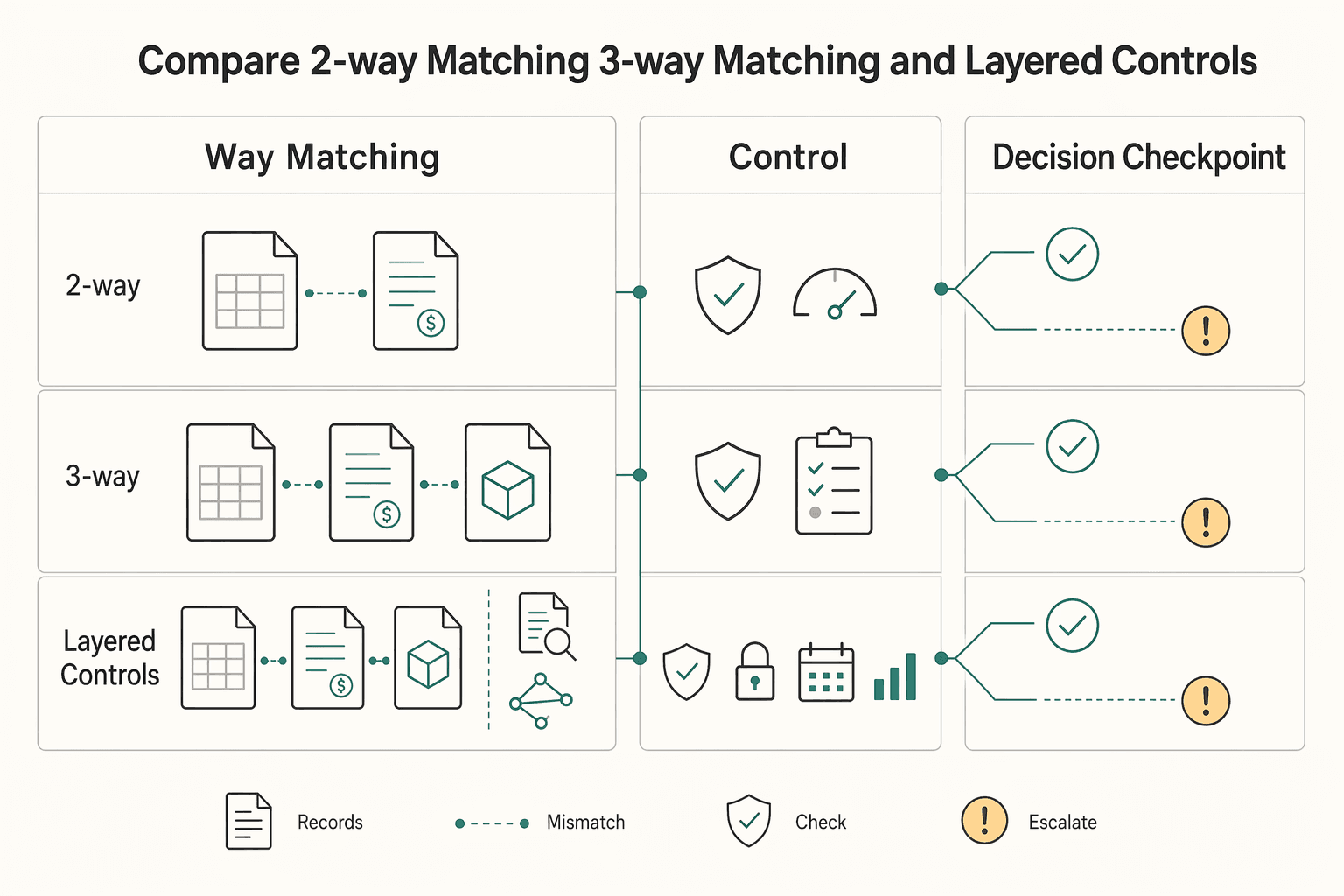

Compare 2-way matching 3-way matching and layered controls#

For scaling marketplaces, layered controls are usually the better endpoint than "3-way only" because different overpayment risks fail in different ways. Use 2-way or 3-way as your base, then add controls for duplicate risk and exception routing.

| Control type | Required documents | What it catches | What it misses | Implementation load | Ongoing ops burden |

|---|---|---|---|---|---|

| 2-way matching | PO and invoice | PO-versus-invoice differences within configured tolerances | No receipt proof; limited coverage for duplicate intake and non-document commercial issues | Lower | Lower to medium |

| 3-way matching | PO, invoice, and receipt evidence (for example, product receipt or delivery note where your process uses one) | 2-way checks plus billed-versus-received discrepancies | Duplicate-payment risk from parallel intake channels; issues that still align across PO, receipt, and invoice | Medium | Medium to high, especially as transaction volume grows and discrepancies increase |

| Layered controls | Base match documents plus pricing/contract reference, duplicate checks, and exception-routing data | Document mismatches, receipt gaps, duplicate risk, and policy/confidence failures routed to review | Weak source data, unclear ownership, or missing evidence | Medium to high | Higher setup effort, often lower reviewer noise when only failed cases are surfaced |

| Decision checkpoint | Same as chosen base model, plus payment-release status before Payouts | Clear split between straight-through approvals, review queue, and hard stop | Breaks when release logic is not tied to holds and exception outcomes | Medium | Medium |

- Use 2-way when PO discipline is strong but receipt capture is not.

It is a PO-versus-invoice tolerance control, so it is fast to run and simple to defend. It does not prove receipt, and it does not by itself prevent duplicate scenarios from multi-channel intake.

- Use 3-way when receipt evidence is reliable enough to gate payment.

It adds receipt-to-invoice verification on top of PO matching. When tolerances fail, a matching hold is the right blocking point, since payment should not proceed until that hold is released.

- Add layered controls when failure modes are mixed.

Document matching catches one class of errors; duplicate control and exception workflow cover others. Keep escalation selective so only invoices failing matching, policy, or confidence checks go to manual review.

- Apply one release rule before Payouts: auto-approve, queue, or block.

Auto-approve when required artifacts are present, consistent, and unflagged. Queue when base matching passes but confidence is not clear; block when a matching hold or duplicate risk is unresolved.

Related: Invoice Matching: How Platforms Automate 2-Way and 3-Way Invoice Verification.

The five best automation setups and when each wins#

Pick the lightest setup that closes your main overpayment risk, then add controls only where the failure mode is still open. Most teams start with Setup 1 or 2, then move to 3 through 5 when price terms, multi-entity duplicates, or payout-release controls become the real gap.

| Setup | Best fit | Key win | Main risk | Must verify before auto-approve |

|---|---|---|---|---|

| Strict 2-way baseline | Services-heavy spend with weak receiving proof | Fast PO-versus-invoice control through an API | No receipt proof and weaker duplicate coverage | PO, invoice, and variance rationale are present |

| Classic 3-way enforcement | Goods or milestone delivery with dependable delivery note or GRN | Stronger gating because receipt evidence is required | Wrong commercial terms can still pass | PO, invoice, and receipt evidence agree |

| 3-way plus price-term guardrails | Recurring invoices tied to negotiated terms | Expected-amount variance checks catch overbilling a clean 3-way can miss | Stale contract/pricing data creates noise | Accepted variance is defined, and discrepancies require approval before posting |

| Multi-entity control stack | Multiple entities paying the same vendor network | Cross-entity duplicate checks catch repeats local queues miss | Vendor and invoice normalization is harder | Cross-entity duplicate result is clean before release |

| End-to-end platform-integrated controls | Marketplace flows where approval status drives Payouts | Retry safety, traceability, and policy-aware release | Deeper integration effort and event-design mistakes | Idempotent requests, event dedupe, and immutable audit trail are working |

- Strict 2-way baseline

Use this when you can reliably produce a PO and invoice but not dependable receiving proof. It compares invoice to PO and is a practical baseline for services without physical delivery. Keep the control honest by requiring the PO, invoice, and accepted-variance rationale for any pass.

- Classic 3-way enforcement

Use this when your AP process can consistently capture delivery notes or GRNs. It adds receipt confirmation to PO and invoice checks, so payment approval is tied to what was received, not just what was ordered. Keep the release rule simple: no usable receipt evidence, no release.

- 3-way plus price-term guardrails

Use this when 3-way passes but commercial overbilling still appears. Add expected-amount variance checks so invoice totals stay within accepted variance, and require approval before posting when discrepancies exist. This raises control quality, but only if contract and pricing reference data stays clean.

- Multi-entity control stack

Use this when the same supplier network invoices across entities. Multi-entity AP is a distinct capability area, and cross-entity duplicate checks catch repeats that can look valid in a single-entity queue. Standardize vendor and invoice fields first, or duplicate controls will miss obvious repeats.

- End-to-end platform-integrated controls

Use this when approval outcomes directly control whether Payouts happen. Matching is only part of the control; you also need idempotent request handling, webhook event dedupe, and an immutable audit trail of actions. Webhook endpoints can receive duplicate events, so payable-creating or payable-updating calls must be safe to retry; idempotency keys can be up to 255 characters and can be pruned once at least 24 hours old, so set retention to your retry pattern.

Where overpayments still happen after matching passes#

A passed match confirms document consistency, not payment safety. After matching is in place, overpayments usually come from four gaps: wrong terms, duplicate intake, replayed events, and manual bypasses.

| Gap | Why matching misses it | Control response |

|---|---|---|

| Passed match, wrong commercial terms | PO and receipt can both carry incorrect pricing or milestones | Show the approved amount or accepted variance before posting |

| Duplicate submissions across entities or intake channels | One-queue duplicate controls can miss repeats across teams or entities | Use cross-entity duplicate control and normalize vendor names, invoice numbers, dates, and amounts before comparison |

| Replay and timing failures in async payment flows | The same webhook event can arrive more than once | Use strict idempotency handling and confirm a resent event returns the prior result |

| Manual overrides that quietly break controls | Payment can be released without clear evidence | Record the reason, named approver, linked documents, and complete AP history |

- Passed match, wrong commercial terms

A clean 2-way or 3-way result can still approve the wrong amount when the PO and receipt both carry incorrect pricing or milestones. Invoice matching checks whether documents agree; it does not prove those numbers still match negotiated terms. Put a hard checkpoint before posting: the reviewer should see the approved amount or accepted variance. If that reference is stale or missing, teams tend to push invoices through despite exceptions.

- Duplicate submissions across entities or intake channels

Duplicate controls that work inside one queue often miss duplicates across teams or entities. Decentralized processing raises this risk, and duplicated or erroneous disbursements can still be material at scale (often cited at 1% to 2.5% annually). If shared suppliers bill multiple entities, use cross-entity duplicate control and normalize vendor names, invoice numbers, dates, and amounts before comparison.

- Replay and timing failures in async payment flows

Webhook-based flows are commonly delivered at least once, so the same event can arrive more than once. Without strict idempotency handling, retries can create duplicate payable actions, approval transitions, or release calls. Your control test is simple: resend the same event and confirm the system returns the prior result instead of creating a new object. This is also where replay-style retransmissions can produce unauthorized effects if handlers are weak.

- Manual overrides that quietly break controls

Temporary overrides can bypass policy gates and weaken otherwise solid controls. When people with authority can release payment without clear evidence, overpayment and fraud effects become easier to conceal. Treat overrides as fully auditable events: recorded reason, named approver, linked documents, and a complete AP history from intake through approval.

Decision rules for auto approve queue and hard block#

Use three states: auto-approve, queue for review, and hard block.

| State | Trigger | Requirement |

|---|---|---|

| Auto approve | Required artifacts are present and agree with each other | If receipt is required, include a delivery note or product receipt; in 2-way confirm invoice unit price matches PO unit price; in 3-way also confirm invoice quantity matches received quantity |

| Queue for review | Matching passes but price, rate, discount, or terms are still uncertain | Route to a named exception workflow owner and require approval before posting when variance exceeds tolerance |

| Hard block | Critical controls fail or compliance verification conditions are unresolved | Do not let payout release proceed while holds remain open; in one Stripe 1099-capability context, payouts are disabled if required information is not collected and verified by 600 USD in charges |

- Auto-approve only when evidence is complete and consistent

Auto-approve only when required artifacts are present in the record and agree with each other. If your process requires receipt before approval, include receipt proof (delivery note or product receipt) before release. In 2-way matching, confirm invoice unit price matches PO unit price. In 3-way matching, also confirm invoice quantity matches received quantity. If any required artifact is missing or a discrepancy is unresolved, do not auto-approve.

- Queue for review when matching passes but the commercial answer is unclear

Route to a named exception workflow owner in Finance Ops when documents match but price, rate, discount, or terms are still uncertain. This is where document-consistent but commercially questionable invoices belong. Keep discrepancy handling explicit: when variance exceeds tolerance, require approval before posting. For example, with a 5 percent net unit price tolerance, 1.05 can be acceptable while 1.10 is not.

- Hard block when funds should not move until conditions are cleared

Hard block payout release when critical controls fail, including unresolved compliance verification conditions. KYC is a clear case: connected accounts must satisfy required verification before they can accept payments and send payouts. In one Stripe 1099-capability context, payouts are disabled if required information is not collected and verified by 600 USD in charges. Hold discrepant invoices pending resolution; do not let payout release proceed while those holds remain open.

- Pick 2-way or 3-way based on receipt-proof reliability, then set block logic accordingly

If reliable receipt proof is not consistently available, run 2-way matching and use stricter blocking for unresolved discrepancies and compliance holds. If receipt proof is reliable, use 3-way matching, then keep contract and terms validation in the control path because receipt confirmation alone does not validate negotiated pricing. For the full breakdown, read PO Matching Exceptions for Platforms with Partial Receipts and Variances.

Implementation sequence across product finance and engineering#

Build this in order: define records first, then matching and retry safety, then payment gating, then operator controls. If you reverse that order, you create approval noise instead of overpayment control.

- Define canonical records first

Agree on one shared contract for invoice, purchase order (PO), and receipt or service evidence before you tune approvals. The practical check is whether one payable record can trace invoice lines to PO lines and, where your process supports it, receipt or service entry evidence. If receipt evidence cannot be linked reliably, you should treat the flow as 2-way in practice, not true 3-way matching.

- Implement deterministic matching and duplicate safety next

Make the first pass strict and explainable before adding exception logic. Oracle Payables begins PO matching as 2-way matching by default, which is a useful baseline for machine-checkable consistency. Protect create and approve actions with an idempotency key so retries do not execute the same operation twice, and treat every webhook as potentially duplicated by recording processed event IDs.

- Tie approval outcomes directly to payment release and the

ledger

A passed match should allow release, and a failed control should pause release automatically. Use one hold state across AP and payout paths so a failed tolerance or mismatch cannot be bypassed by system boundaries. Write each decision to the ledger with outcome, timestamp, and reason so Finance can reconstruct exactly why money moved or did not move.

- Expose operator states and escalation actions for Finance

Show clear states (auto approved, queued, blocked) with the exact reason and the next allowed action. Typical actions are attaching missing receipt evidence, resolving duplicate flags, or escalating pricing discrepancies. If Finance still needs Engineering to replay events or interpret match outcomes, the control logic may be correct, but operationally it is still too opaque.

Build the evidence pack your auditors and finance team will ask for#

The control is only real if you can export proof for each payment decision. If evidence is missing, treat the control as not implemented, regardless of UI status labels.

| Artifact | What to keep | Notes |

|---|---|---|

| Decision record | Match result, reviewer action, policy outcome, and an immutable audit trail | Capture event type, time, source, outcome, and identity |

| Reconciliation pack | Payable decision tied directly to ledger postings and exportable as a reconciliation pack | If the export stops at "invoice paid" and cannot show journal and subledger traceability, reconciliation is still partly manual |

| Cross-border tax and compliance artifacts | VAT validation results and tax-document state for W-9, W-8BEN, and Form 1099 readiness | Keep FBAR tracking context where relevant; Form 1099-NEC filing deadline reference is January 31 |

| Known limits and red flags | VIES validation helps verify EU VAT numbers | It does not by itself establish VAT-exemption treatment, and GB VAT number validation ceased as of 01/01/2021 |

- Decision record

Keep one record per payment decision with the match result, reviewer action, policy outcome, and an immutable audit trail. At minimum, capture event type, time, source, outcome, and identity, so Finance can answer who approved what, under which rule, and when.

- Reconciliation pack

Tie each payable decision directly to ledger postings and make it exportable as a reconciliation pack. If the export stops at "invoice paid" and cannot show journal and subledger traceability, reconciliation is still partly manual.

- Cross-border tax and compliance artifacts

Where enabled, include VAT validation results and tax-document state for W-9, W-8BEN, and Form 1099 readiness. Keep FBAR tracking context where relevant, clearly labeled as FinCEN Form 114 context. If you track Form 1099-NEC readiness, remember the filing deadline reference is January 31.

- Known limits and red flags

Treat checks as inputs, not standalone proof. VIES validation helps verify EU VAT numbers, but it does not by itself establish VAT-exemption treatment, and VIES notes that GB VAT number validation ceased as of 01/01/2021. A passed check with missing supporting evidence is still a control gap.

Conclusion#

The practical answer is not to treat 2-way matching or 3-way matching as if one switch solves overpayment risk. The better approach is to set the right base check for your evidence quality, then add the controls that catch what document matching misses.

- Pick the base model your evidence can actually support

If you can reliably prove receipt, use 3-way matching because it adds the receipt check to the invoice and PO comparison. If you cannot produce dependable receipt evidence, do not label the process as 3-way and hope for the best. Start with 2-way against the purchase order, then make out-of-tolerance results land on a matching hold and stay there until someone with authority releases them. A simple checkpoint helps here: before each payment batch, review open holds and confirm there is a named decision on every release.

- Add the controls that catch the common misses

A passed match does not, by itself, cover every payment-control risk. That is why many teams layer explicit hold-review and release rules on top of 2-way or 3-way matching, then tie payment progression to clear exception ownership. The red flag to avoid is a manual override that clears payment without a recorded release decision. If your team has repeated exceptions, fix release ownership and hold discipline before tightening tolerances alone.

- Tie approval to payout gating and transaction traceability

This is where many platform teams either gain control or create expensive cleanup work later. Your approval decision should directly control whether payouts can proceed, especially when verification requirements are still open. Stripe is clear that connected accounts must satisfy KYC requirements before they can accept payments and send payouts, and payouts can be paused when information is not provided or verified.

On the reconciliation side, keep the decision trace linked to the exact fund-movement record. Stripe balance transactions exist for every transaction that enters or leaves your account balance, which makes them a strong anchor for proving what actually moved.

If you want a concrete next step, map your current state against the setups from this article and choose the one that fits your data reality, not your target architecture. Then run a focused rollout with checkpoints for document availability and match logic, hold and exception release rules, and payout gating plus transaction traceability. If any payment decision cannot be traced back to its PO, invoice, receipt status where applicable, and final funds movement, treat that control as incomplete.

For a step-by-step walkthrough, see 3-Way Reconciliation Explained: PSP Ledger vs. Internal Ledger vs. Bank Statement.

Frequently Asked Questions

Does automated 3-way matching prevent all overpayments?

No. 3-way matching adds receipt validation to the PO and invoice check, so it adds an extra control beyond 2-way matching. It still does not prove your commercial terms are correct in every case, and a passed match does not eliminate duplicate-processing or manual-override risk.

When is 2-way matching enough for a platform team?

Use 2-way matching when you can reliably compare the purchase order and invoice, but you cannot produce trustworthy receipt evidence. Oracle’s definition is precise here: 2-way matching verifies PO and invoice information within your configured tolerances, and if the invoice is out of tolerance, it should go on matching hold and stay unpaid until the hold is released.

What controls should be added first beyond invoice matching?

Start with duplicate controls, contract price checks, and enforced exception routing. That combination can reduce common misses from document matching alone: the same invoice arriving twice, a matched document set with pricing that still needs review, and a reviewer bypassing policy without a clear audit trail.

What should happen when a match passes but the contract price is wrong?

Do not auto-pay it just because the match passed. In Dynamics 365, 2-way and 3-way matching always compare price information by unit price, so if your contract logic is more complex than unit price, route it to manual review and require the reviewer to attach the contract or approved pricing evidence before release.

Which exceptions should auto-block versus go to manual review?

Auto-block exceptions that make payment unsafe to release, such as out-of-tolerance matches and clear duplicate risk. Manual review is better for cases where the documents are present but the commercial interpretation is unclear, like a valid receipt paired with disputed pricing or terms. The red flag is any exception path that lets payment proceed without a named owner and recorded decision.

How do idempotency and webhook retries affect duplicate payment risk?

Retries are normal, so your payment creation path should be idempotent and your webhook consumer should deduplicate processed events. Stripe is explicit on both points: idempotency keys make retries safe, and webhook endpoints might receive the same event more than once, so log processed event IDs and reject repeats before they create a second payable action.

What proof should we keep for audits and reconciliations?

Keep the match result, reviewer action, policy outcome, and an audit trail for every payment decision. Your reconciliation pack should also tie that decision to ledger detail, because AP reconciliation depends on supporting detail agreeing back to the general ledger balance.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- csrc.nist.gov/glossary/term/replay_attacktrusted

- docs.stripe.com/api/idempotent_requeststrusted

- docs.stripe.com/webhookstrusted

- ec.europa.eu/taxation_customs/vies/index.htmltrusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- irs.gov/instructions/i1099mectrusted

- blackline.com/resources/glossaries/invoice-matchingexternal

- brex.com/spend-trends/accounting/prevent-duplicate-pa...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

3-Way PO Matching for Marketplaces and Automated Invoice Verification

**Start here: treat three-way PO matching for marketplaces as a control decision, not a software toggle.** If you are still checking invoices only against a purchase order, you can miss cases where the invoice looks right on paper. The delivered item or service may still not match what was ordered.

How Platforms Automate 2-Way and 3-Way Invoice Verification

The real question is not whether you know the textbook difference between 2-way and 3-way matching. It is whether your team can turn that difference into a real payment gate inside Accounts Payable. In an invoice verification platform, the distinction matters only when it changes what gets paid, what gets held, and what evidence must exist before settlement moves forward.

The Best Ways to Ask for a Deposit or Upfront Payment

You already know why you need to ask for a deposit. You feel it the moment you ship a draft, reserve time on your calendar, or turn down other work, then the client goes quiet on the **Deposit Invoice**.