3-Way Reconciliation Is an Operating Discipline, Not a Vocabulary Exercise#

For platform finance and payments ops teams, 3-way reconciliation is an operating discipline, not a vocabulary exercise. The job is to prove the same money movement across three records built for different purposes: the PSP ledger, your internal ledger, and the bank statement.

The operating model is simple: treat each record as required, but not sufficient on its own. The PSP ledger shows processor-reported balance movement on platform accounts. Your internal ledger is your system of record for balances, transactions, and money movement. The bank statement confirms whether cash actually landed or left.

All three can be correct and still disagree at a point in time. Providers may expose transaction activity in real time through API responses and webhooks, and Adyen explicitly recommends those event streams for real-time reconciliation. Bank confirmation can come at a different level of detail, such as payout batches matched to bank statement lines. Internal postings can also follow different processing timelines.

A practical early check is simple: can you trace one transaction or payout batch across all three records without changing identifiers? You should already know where the provider reference lives, where your internal transaction ID is stored, and how the bank line ties back to a payout batch or deposit. If that join depends on manual copy and paste, treat it as a control gap.

One risk is stopping after processor-to-bank matching. Stripe frames bank reconciliation as matching payouts to bank cash, which is useful but incomplete on its own. If you skip your internal ledger, you confirm money movement without proving your own posting logic and balances.

This guide is written for high-volume platform flows where settlement files, webhooks, payout batches, and exception handling are daily work. It does not assume every provider, country, or program offers the same data, timing, or features. Product behavior and compliance controls can vary by market, and AML/CFT approaches are risk-based rather than universal. Related reading: Best Merch Platforms for Creators Who Want Control and Compliance.

At a glance comparison of the three records#

Use each record to answer its own authority question, then use the other two to confirm timing and lineage. That habit makes three-way reconciliation more reliable.

| Comparison point | PSP ledger | Internal ledger | Bank statement |

|---|---|---|---|

| Owner | Payment service provider | Your platform | Your bank |

| Update timing | Via provider reporting artifacts, APIs, and webhooks; timing can vary | When your application posts events | On bank processing and statement cadence (EFT summaries at least monthly) |

| Source system | Processor-side balance transaction record of funds moving through the PSP account | Your system of record for balances, transactions, and money movement | Bank account record of cash activity |

| Common delays | Settlement timing, payout batching, asynchronous webhook arrival | Asynchronous event arrival, retries, duplicate processing risk, posting lag | Processing windows, pending items, holds, statement-cycle timing |

| Failure signatures | Missing payout-batch link, duplicate event impact, movement not aligned to internal posting | Balance change without traceable provider reference, duplicate journaling, stale status | Deposit/debit lands later than expected, payout grouped at different granularity, pending items not final |

| Hidden investigation cost when match keys are inconsistent | Provider reference exists but does not map cleanly to your transaction or payout batch | Internal transaction ID exists but is not stored with provider and bank-facing identifiers | Cash arrived but no preserved payout/deposit identifier to map back to a bank line |

A simple rule helps prevent false exceptions: the PSP ledger explains processor-reported movement, the internal ledger proves your posting logic, and the bank statement confirms cash movement.

The PSP ledger is authoritative for what the processor reports inside its account structure. It is not authoritative for whether your internal posting is correct, and it is not final proof that cash has landed in the bank.

Your internal ledger is authoritative for your platform’s balances, transaction state, and money-movement history. It is not authoritative for bank settlement timing.

The bank statement is authoritative for whether money hit or left the bank account. It does not usually show every underlying transaction inside a payout batch. Once that authority split is clear, the next question is which artifact gives you the best evidence at each step.

| Record | Settlement file | Webhook | API response | GL journal touchpoint |

|---|---|---|---|---|

| PSP ledger | Primary batch artifact for settled or paid-out activity; may include batch number, date, or unique identifier | State updates, but asynchronous and retry-driven | JSON responses provide point-in-time evidence | Supports mapping processor movement into accounting; not a replacement for event evidence |

| Internal ledger | Can ingest and normalize settlement data into internal postings | Can trigger status-driven posting updates | Can store provider payloads or normalized fields as evidence | Supports operational-to-accounting handoff and traceable journal creation |

| Bank statement | Confirms payout or deposit cash movement at statement-line level | Not applicable | May exist as an additional feed, but statement remains the formal cash record here | Cash confirmation input for cash and clearing entries |

Where teams force the wrong record to answer the wrong question#

Do not use bank lines to judge whether a PSP event is wrong. Bank data is often later and coarser, while payout reconciliation is based on matching each payout to its settled transaction batch and day-boundary report windows (12:00 am to 11:59 pm).

Do not treat webhook delivery as cash confirmation. Webhooks are asynchronous, retries can continue for up to 3 days, and handlers can be invoked multiple times for the same flow, so idempotent posting controls are mandatory.

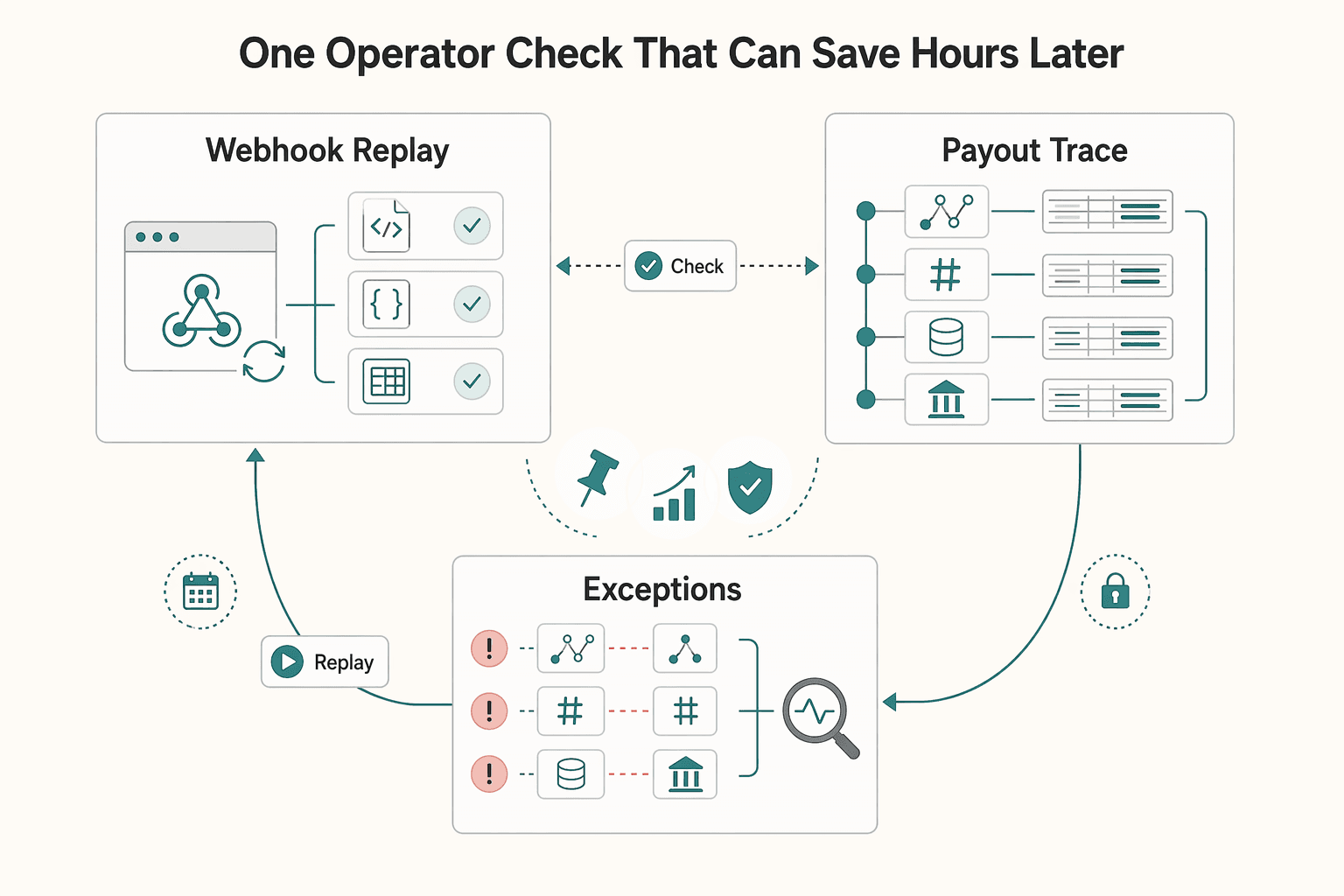

The one operator check that can save hours later#

Run four joins on one payout batch each day: provider reference, internal transaction ID, payout or deposit batch identifier, and bank statement line. If any key is missing, treat it as investigation risk, not a cosmetic data issue.

Preserved identifiers cut case time. Keep the webhook payload, API JSON response, settlement-file row, and internal or GL touchpoint linked so you can quickly tell whether the issue is timing, duplication, or a real reconciliation break.

For a step-by-step walkthrough, see Merchant of Record for Platforms and the Ownership Decisions That Matter.

What each ledger is actually telling you#

Treat matching balances as a smoke test, not the approval test. A stronger approval test is lineage: the PSP ledger shows processor-reported funds movement, your internal ledger records what your platform posted, and the bank statement confirms cash movement in the account.

| Record | What it tells you | Best use | Weak if used alone |

|---|---|---|---|

| PSP ledger | Provider-reported movement into or out of the PSP account balance | Verify what the processor reports as moved | Does not prove your internal posting is correct or that cash reached the bank |

| Internal ledger | Your transaction system of record for balances, transactions, and money movement | Prove what your platform recorded and why | Can look internally consistent while missing a provider event or bank movement |

| Bank statement | External summary of account activity over a period | Confirm cash movement at bank-account level | May not include the transaction-level lineage needed to explain payout composition |

| General ledger | Accounting balances after subledger transactions are imported, accounted, and posted | Reporting and close | Not where payment events first appear |

The general ledger sits downstream from operational records, so close quality depends on traceable joins. A cash or clearing journal is most dependable when you can trace it back to the internal ledger entry, the provider reference, and the bank statement line.

Two flow designs can shift where events first appear. In Virtual Accounts setups, the first usable reference may be the virtual account identifier even though funds are held in the settlement account. In Merchant of Record (MoR) flows, the legally responsible payment entity may differ from the platform operator, which can change where the first authoritative merchant-side record appears.

Keep a chronological audit trail across records so you can reconstruct the sequence end to end. “Balances match” is weaker than “lineage matches,” because offsetting errors can hide behind a net-zero result.

Why records diverge on the same day without being wrong#

Start with timing, then test data integrity. In practice, the first question is usually "which record moved first?" not "which record is broken?"

| Divergence pattern | What you see first | Why it can be normal | Check before escalating |

|---|---|---|---|

| PSP ledger updates before cash reaches bank | Processor shows funds or payout movement, bank statement does not yet show it | Processor balances can show pending amounts before settlement, and settlement timing can depend on configured delay days | Compare provider event timestamp to bank posting or value date, and confirm the same provider reference or payout batch ID |

| Internal ledger posts after the PSP | Provider event exists, internal entry appears later | Posting may wait on a webhook, asynchronous processing, or a retry after a delivery failure | Check raw event receipt time, ingest log, and retry status before calling it a break |

| Events arrive out of order or get replayed | Status appears to move backward, or the same event seems to happen twice | Providers treat these flows as asynchronous, and failed deliveries can be resent | Sort by event timestamp, not arrival order, and verify whether the event was resent |

| Payout state stalls while transaction records look fine | Charge or transfer is recorded, payout remains pending or blocked | KYC, KYB, or other compliance checks can pause payout progression without invalidating earlier records | Review verification status, account requirements, and any compliance hold note tied to the account or payout |

Timing gaps are part of the design#

A processor can be accurate before your bank statement catches up. Funds can sit in a pending balance until settlement, and settlement timing can depend on configured settlement delay days rather than scheme transfer timing. In Adyen's payout quickstart example, the default sales-day payout delay is two business days, which can create a same-day mismatch between the PSP ledger and bank cash.

Your internal ledger can also be late without being wrong. If you post from provider events, a delayed webhook, temporary endpoint failure, or retry can shift your internal timestamp later than the processor timestamp. The check is straightforward: line up provider event time, ingest time, internal posting time, and bank posting date. If references still join cleanly, lag is often a reasonable first explanation, but not proof on its own.

Async delivery creates false alarms fast#

A webhook is an event-driven HTTP callback, and payment state changes are often asynchronous. Providers also position webhooks as an alternative to continuous API polling, so delivery timing is operational rather than immediate by default. Adyen advises processing in chronological order by timestamp, and Stripe notes webhook events help when a customer's bank confirms payment later.

Two common failure modes matter here. First, processing in arrival order instead of event-timestamp order can create apparent status reversals. Second, delivery failures can make one real event look duplicated because retries and replays happen. Stripe says undelivered events are automatically resent for up to three days, and Adyen says failed webhooks enter a retry queue. If an event looks missing, backfill from the provider's event-listing API instead of inferring from downstream balances.

Compliance pauses are not the same as reconciliation breaks#

Payout progression can pause when account verification is incomplete. Adyen states users must be verified before you can process payments or pay out funds, and Stripe states payouts are typically disabled if required information is not received by the current deadline. Adyen also notes payouts may be blocked for a compliance reason. These are operational holds, not automatic evidence of broken transaction or cash mapping.

Use a practical triage rule. If timestamps, amounts, currency, and references remain coherent across the PSP ledger, internal ledger, and bank statement, start with timing or compliance lag as a working hypothesis and monitor through the relevant provider window. If references break, such as a missing provider reference, an internal record that cannot tie to the original event, or a bank credit with no plausible payout batch, escalate it as a reconciliation break.

Build match keys before you automate matching#

Set your match keys first, then automate. Amount and date are not enough on their own. You need stable identifiers so ordinary timing lag does not turn into manual exception work.

Start with a minimum join set#

Adyen explicitly uses Psp Reference and Merchant Reference to identify a transaction, and those identifiers are carried in APIs, webhooks, and reports. For payout-level reconciliation, Batch Number is the batch lookup field.

| Join target | Minimum keys | Must appear in | Why it matters | Hold if this is missing |

|---|---|---|---|---|

| PSP ledger to internal ledger (transaction level) | Psp Reference + Merchant Reference (or internal transaction ID) | API responses, webhooks, reports, internal posting record | Proves one processor event maps to one internal posting | Amount and currency exist, but no stable cross-reference |

| PSP payout or deposit activity to bank cash | Batch Number + internal payout or deposit record ID | Batch report, internal payout table, bank investigation record | Bridges processor settlement activity to booked cash movement | Batch exists in PSP data but was not stored internally |

| Bank statement ingestion | MsgId + account context from the file | Statement ingest log and imported bank rows | Prevents duplicate posting of the same statement file | Re-imported file or multi-account file treated as single-account |

Batch Number is a batch key, not a transaction key. Use it to tie payout or deposit groups to bank cash, not to resolve transaction-level breaks by itself.

Make retries harmless#

Idempotency should make retries non-destructive: the same operation key should resolve to the same accepted result, not create a second posting.

Adyen’s idempotency key supports safe retry after timeout or no response, has a 64-character maximum, and is valid for at least 7 days. Stripe supports idempotency keys up to 255 characters. Apply the same control to imports: one operation, one key, and duplicate attempts mapped back to the original result.

For bank files, dedupe before row-level processing. In camt.053, MsgId identifies the statement file, one file can include multiple accounts, and it contains booked entries only.

Normalize files before matching rules fire#

Normalize settlement and bank-statement feeds before matching. Use explicit, versioned mappings from external transaction codes into internal transaction types, then run join logic on normalized values. This helps reduce false breaks when feeds represent similar events differently or when new external codes appear.

Preserve enough evidence to replay every break#

For each unresolved break, keep raw evidence and transformed values together. That includes the original webhook or API payload, the original settlement row or bank statement line, parsed fields, normalized fields, and the parser or rule version used.

The checkpoint is replayability. You should be able to reconstruct what arrived, how it was transformed, and why matching failed. If that chain is incomplete, hold the item instead of auto-resolving it.

Decide what should auto-match and what should be held#

Default to conservative matching. Auto-match only when the candidate set gives one clear answer, and send ambiguity to the exception queue. That lowers the risk of quietly misclassifying records.

Rule order matters because auto-match rules are processed in sequence. Reference-led rules should run first, and weaker fallbacks should run later. Use explicit if X, do Y logic:

| Match class | Use when | Minimum condition to allow it | Main risk | Recommended action |

|---|---|---|---|---|

| Exact match | One candidate on each side has the same reference, amount, and currency | Reconciliation reference aligns, plus exact amount and currency | Low when the reference is stable and unique | Auto-match first |

| Time-window match | The same transaction is expected to post on different days across sources | Strong reference match plus an approved date tolerance window (for example, 0 to 1 days) | Wrong-row matching if references are weak | Run only after exact-match rules fail |

| Tolerance-based match | Small, known variance is allowed for a specific case | Strong reference match plus an approved tolerance limit | Real breaks can be hidden if used too broadly | Use narrowly and log rule changes in the audit trail |

| Manual hold | Multiple candidates qualify, or reference is missing or weak | Anything short of a unique, explainable candidate set | Silent misclassification | Send to exception queue |

- If amount + reference + currency align and only one candidate qualifies, auto-match.

- If reference is missing and the amount is common, hold for review.

- If a rule returns multiple qualifying candidates, hold instead of selecting a winner.

That tradeoff is the core control: more aggressive auto-matching can reduce manual queue volume, but it raises silent misclassification risk. Some engines can select a first or ordered candidate when duplicates qualify. Safer configurations keep ambiguous candidates unmatched.

Set approval before go-live: a preparer submits reconciliation changes, and responsibility passes to a reviewer. Log changes in the audit trail with old and new values, plus resulting status transitions, so each auto-match decision is explainable later.

Classify exceptions so teams can resolve faster#

Classify exceptions when they enter the exception queue so ownership, checks, and escalation are clear from the start. A small taxonomy can work better than a generic "unmatched" bucket because it turns triage into repeatable decisions. Use this as a practical operating model, not an industry standard taxonomy.

| Break type | What it usually means | Practical first owner | Handoff trigger from the exception queue |

|---|---|---|---|

| Missing event | Upstream event is expected but not present in your internal ledger or case record | Engineering | No raw webhook stored, no matching API payload, or retry/backfill evidence points to ingest failure rather than normal delay |

| Duplicate post | The same event appears to have been processed more than once | Engineering | Same provider reference or event appears twice in internal journal trace or downstream posting history |

| Timing lag | Records are coherent, but one source has not updated yet | Finance ops | Move to engineering only after provider retry window or expected posting window passes with no arrival |

| Reversal/chargeback | A payment has been disputed or reversed through the network process | Finance ops | Escalate to product if internal status model cannot represent the dispute state cleanly |

| Unmatched bank credit | Cash appears on the bank statement, but no linked PSP or internal transaction is ready yet | Finance ops | Escalate to engineering if import, statement parsing, or reference capture failed |

| Stale status | A transaction stops progressing even though evidence shows later activity elsewhere | Product | Escalate to engineering if the event never arrived or was processed out of order |

Check chronology before labeling anything as missing. Store webhook messages before downstream processing, and use timestamps to process in order. Also account for retry behavior. Stripe can resend undelivered events for up to three days, and Adyen retries three times immediately, then continues from a retry queue for up to 30 days. If references line up and you are still inside that window, classify it as timing lag.

Treat duplicate-post cases separately from finance review. If one provider event is processed multiple times, it is an idempotency and processing-control issue, so engineering should usually own root cause and remediation.

Route by cause, not by symptom#

Assign first ownership to the team that controls the likely fix. In this operating model, finance ops handles cash-facing exceptions, product handles lifecycle-state mismatches, and engineering handles ingest and processing defects.

Finance ops should usually take timing lag, unmatched bank credit, and reversal or chargeback on first pass. Chargebacks are cardholder disputes, and supervisory guidance tracks chargeback and unreconciled settlement trends as management-report signals, so these items should not be buried as low-priority noise.

Product should take stale-status breaks when the raw webhook or API payload shows a later state but internal status is stuck. Hand off to engineering when evidence shows missing capture, duplicate processing, or out-of-order application.

Age and impact should both matter#

Prioritize with aging buckets and impact tags together, not age alone. Aging buckets are defined time periods for reconciliation transactions, and even a broad bucket such as 1 to 30 days helps expose slow-moving exceptions.

Then layer impact tags tied to risk, such as cash movement, customer-visible dispute, close blocker, or repeated pattern. A newer unmatched bank credit can be higher priority than an older stale status because the bank statement reflects booked entries.

Make every ticket audit-replayable#

Require a minimum evidence pack on every exception ticket before resolution:

- raw

webhookwith headers and JSON body - original

APIpayload or failed request log - exact

bank statementline - internal journal trace tying the event to subledger and

general ledgeractivity

This keeps resolution replayable and prevents false closure on partial evidence. A statement line confirms booked cash, but not full lineage, so you still need raw event and journal trace to decide whether the break is timing, mapping, or a true reconciliation defect.

Close controls that make audits easier#

Close only when exceptions are controlled and explained, not when they feel "mostly understood." Close readiness comes down to three gates: open items are within your approved threshold, aged items are explicitly reviewed, and every remaining exception has a documented disposition. Use a clear period-end flow: match transactions during the period, then prepare and review the reconciliation at close. Because automated matching is rule-driven, your close file should show the rule set used, who reviewed the result, and how period-end balances tie to the general ledger.

Set gates that force a real close decision#

Define close gates before month-end so the decision is repeatable, not improvised:

- unresolved-break threshold for the period

- aging cutoff that forces explicit review of older exceptions

- required disposition for every open item (for example, timing difference, approved in-transit item, compliance hold, or defect pending remediation)

There is no universal regulator-set threshold or aging day count in the source material. What matters is verifiable close evidence: period-end counts, aging, owner, and disposition for each open item. If an open item has no owner, reason, or next action, treat that as a close-readiness failure.

Keep the evidence pack consistent#

Your reconciliation evidence should let another reviewer reproduce both the matching result and the approval decision.

| Close control element | What to retain | What it proves | Common failure mode |

|---|---|---|---|

| Open-exception gate | Period-end exception summary (for example, matched/unmatched counts and aging) | You closed with known exposure, not blind | Queue totals reported without aging or disposition |

| Rule governance | Rule set used in the period (for example, version IDs or a change log) | Auto-match results are reproducible | Rule logic changed mid-period and prior outcomes cannot be recreated |

| Reviewer accountability | Preparer/reviewer log with names and timestamps | A real preparer-reviewer split existed | Same person prepared and approved, or approvals exist only in chat or screenshots |

| Financial completeness | End-of-period subledger or internal ledger to general ledger tie-out | Operational records align to booked balances | Strong ops export but no trace to the GL balance used in close |

If your tool also breaks out unmatched, supported, or in-transit transactions, retain that view. It helps explain why items stayed open without treating all open items as equal risk.

Payout evidence is often incomplete for compliance and tax reasons#

For payout-heavy platforms, close gaps can happen at the edges of compliance and tax workflows. A payout can remain open because AML or beneficial ownership procedures are incomplete even when the payment record appears valid, and tax forms do not replace those AML/CDD obligations.

Tax artifacts still matter for evidence completeness. A U.S. payee may provide Form W-9 for TIN-based information-return reporting, and a foreign beneficial owner may provide Form W-8 BEN. Reportable payments may involve Form 1099-NEC, while nonresident-alien reporting can follow a different path (for example, Form 1042-S). If your packet assumes every payee fits a single 1099 path, cross-border payout evidence can break.

Fit controls to your actual footprint#

Design close controls for your real market and program footprint, not a copied template. Control expectations should be risk-scaled by location, size, and service volume, and cross-country frameworks are not identical.

If your product supports only certain payout rails, or your reconciliation stack does not capture tax holds, reviewer actions, or compliance states, reflect that directly in the control design. Keep thresholds local, but keep one standard for readiness: fail close when you cannot reproduce the applied rule set, cannot show preparer/reviewer accountability, or cannot tie period-end operational balances to the general ledger.

Choose your operating model by transaction profile#

Choose the operating model that fits your transaction profile today, then automate the next bottleneck before volume exposes it. Low-volume bank-heavy activity can run with manual review, processor-led settlement batches often fit a hybrid model, and frequent multi-rail payouts often benefit from automation-first controls with strict exception governance.

| Operating model | Best fit | Automate first | Main risk if you stay too long |

|---|---|---|---|

| Low-volume manual review | Bank-heavy ACH or wire activity with scheduled windows and limited daily exceptions | Standardized exports, reviewer log, and one reproducible tie from bank statement to internal ledger | Keying errors, missed duplicates, and close evidence that depends on specific analysts |

| Mid-volume hybrid | Processor-heavy flows where settlement batch reconciliation reduces manual work but exceptions still need review | Settlement-file ingestion, matching rules, and queue-based exception handling | Partial automation can hide rule gaps, especially around timing differences and retries |

| High-volume automation-first | Frequent payout batches, multiple rails, or instant-payment expectations | Automated ingestion, retry-safe handling, and strict exception governance | Duplicate actions or misclassified breaks when ingestion and rule controls are weak |

For bank-heavy ACH and wire flows, scheduling discipline matters more than real-time handling. Same Day ACH runs on defined windows (for example, 10:30 a.m. ET, 2:45 p.m. ET, and 4:45 p.m. ET deadlines with later settlement points), so teams can work from scheduled pulls and explicit review cutoffs. If staff still manually pass details between an operator interface and the core banking system, that handoff can become an early scaling limit.

For processor-heavy flows, the core reconciliation step is tying processor funding data to bank deposits. Processor reporting supports that linkage, and payout tooling can differ between settlement-batch reconciliation and balance-style tracking. In this profile, hybrid usually works well: automate ingest and batch matching, then keep human review for contextual breaks.

If payout batches are frequent and multi-rail, prioritize automated ingestion plus strict idempotency key controls. Adyen supports keys up to 64 characters with a minimum 7-day validity window. PayPal warns that omitting its request ID can duplicate a request, with UUID guidance tied to a 38 single-byte character limit. Your control test is simple: on any replay or retry, prove the payment action posted once and duplicate attempts were routed to exceptions.

When faster rails are added, the operating constraints change again. Instant-payment models are built for 24x7x365 processing, and instant-payment guidance is explicit that batch-first processing is not practical when confirmation is expected within seconds. If your model still depends on end-of-day files, file-based or operator-feed handoffs can become a constraint and increase break aging.

Roll out in narrow phases so controls stabilize before scope expands. One workable approach is to expand rails and reconciliation scope incrementally, only after the break taxonomy is consistent enough that reviewers classify the same issue the same way. The validation check is traceability: you can follow a sample item from bank statement line or settlement file, through the internal ledger, to final disposition without changing categories week to week.

Compare tooling options without vendor hype#

Choose based on control and evidence, not brand. The safer option is usually the one that makes matching rules, exceptions, and exports easy to inspect.

| Option | Integration depth | Rule transparency | Exception UX | Evidence exports | Auditability |

|---|---|---|---|---|---|

| Build in-house | High potential if you ingest PSP ledger, settlement file, internal ledger, and bank statement directly, but each connector can become your maintenance burden | Full control if you also build rule versioning and approval history | Can fit analyst workflows exactly, but queues and aging controls can take longer to implement | You can export raw and transformed values if you design for it | Strong only if you preserve immutable history for rule changes, replays, and reviewer actions |

| Buy a broad reconciliation platform | Can be strong for finance and close data sources; verify support for your payment rails and bank feeds | Varies, so ask to see custom matching rules and rule history in-product | May provide reviewer queues and exception workflows; verify fit in-product | Should export matched, unmatched, and rule metadata cleanly | Often marketed with a full audit trail, but confirm the level of audit replay detail |

| Buy a context-specific tool | Better fit when built around PSP, payout, or regulatory workflows | Can be strong in-domain and weaker outside it | May be tailored to domain-specific exceptions | Verify exports preserve record references across systems | Can be strong when domain events are first-class; verify coverage when adjacent records must be bolted on |

Treat Trintech, SteelEye, HubiFi, and Reconwizz as positioning examples, not validated feature leaders. Trintech is positioned around transaction matching for month-end close. SteelEye frames three-way reconciliation in a MiFIR reporting context against ARM and NCA data. HubiFi emphasizes integration with existing systems and custom matching rules. Reconwizz targets PSP payouts, fees, and chargebacks.

Keep the known unknowns explicit. Sampled vendors route buyers to demo or quote flows rather than list pricing, so comparable public pricing is not readily available. Implementation timing is also unclear: a "within 48 hours" customized POC is not a production rollout timeline. Performance figures like "less than 20 seconds" and "99%+ reduction" are vendor-reported, not objective head-to-head evidence.

Run one practical proof before deciding: process a real sample from the bank statement and settlement file through the internal ledger, then export matched items, unmatched items, rule version, and reviewer history. If that end-to-end evidence path is weak, close will likely be painful. If your team cannot maintain matching logic and evidence controls in-house, prioritize tooling with strong rule governance and exportability.

Decision checklist before you scale volume#

Scale only when your joins, approvals, and evidence retrieval hold up under retries, delays, and exceptions. If you cannot replay data, explain rule changes, and retrieve proof quickly, higher volume will mostly hide more breaks.

Go or no-go by prerequisite#

| Prerequisite area | What “ready” looks like | What to verify before scale | Red flag that means fix first |

|---|---|---|---|

| Data integrity | Stable identifiers across PSP ledger, internal ledger, bank statement, and normalized settlement file mapping | Reprocess a known day twice and confirm the same records join the same way; test duplicate webhook receipts and replay handling | Keys change by rail or processor, or replay creates duplicate postings |

| Controls | Named approver ownership, rule change log, audit trail, and exception escalation path | Pull one exception and show raw evidence, transformed values, rule version, reviewer action, and approval history | Analysts can explain a match, but cannot prove who changed the rule or when |

| Measurement | Daily (or required-cadence) match rate, aged break counts, time-to-resolution, close-readiness pass or fail | Review recent cycles and confirm metrics are produced consistently, not hand-built when issues appear | You only detect problems at month-end |

| Compliance | Payout gating for KYC/CIP and AML where applicable, policy exceptions documented, approvals traceable | Pick a held payout and trace hold reason, approver, release decision, and supporting records | Compliance holds appear as unexplained recon breaks |

| Routing and funding dependencies | Gateway routing and payout-funding logic are reflected in reconciliation expectations | Check whether routing rules change references or settlement behavior, and whether reserves or minimum balances affect payouts | Cash shortfalls or processor switches create “mystery” mismatches |

Data first, because bad joins do not improve with automation#

Stable identifiers are the base control. If a rail provides a deterministic reference pattern, preserve it through ingest and normalization instead of replacing it with a weaker internal label. Where reconciliation depends on settlement files, treat mapping as a controlled transformation, not ad hoc cleanup; Nacha’s mapping guidance to ISO 20022 for return items is a useful model.

Replay testing should be tougher than the happy path. Webhook endpoints can receive duplicate events, and some providers resend undelivered events for up to three days. Before scaling, prove duplicate delivery does not create duplicate postings in your internal ledger, and that re-importing a settlement file does not change match outcomes unless a rule was intentionally changed.

Controls and evidence must survive scrutiny#

Manual review is manageable. Unowned change is not. Every production rule change should have clear approval, timing, and expected impact before go-live. In FCA CASS context, internal client money reconciliation is required each business day. Records must support an audit trail, retention is five years, and records should be retrievable within two business days in that context.

Keep jurisdiction scope explicit. AML and CIP obligations are program- and jurisdiction-specific, and FATF standards are implemented through local measures. Operationally, if payouts can be gated for KYC or AML reasons, those states should be visible in exception handling, with documented policy exceptions and traceable approvals. That way, compliance holds are not mixed with true data breaks.

Do not separate reconciliation from routing and liquidity#

Routing and liquidity decisions directly affect reconciliation outcomes. Routing rules can change processor references and settlement behavior, so routing changes should be treated as reconciliation changes. Funding policy matters too: paying out the full available balance or ignoring reserve logic can create insufficient-funds situations that block refunds, disputes, or payout obligations and then appear as unexplained breaks.

If those dependencies are still shifting, pause scale and settle them first, including your gateway routing strategy.

Scale when daily measurement is routine, exceptions have named owners, and you can reproduce a day’s outcomes with evidence. That is when reconciliation moves from fragile project work to a reliable operating control.

Related: Liquidity Management for Payment Platforms: How to Make sure You Always Have Funds Ready to Pay.

If you are turning this checklist into live workflows, use Gruv’s docs to align webhook handling, idempotent retries, and audit-traceable operations. Before expanding to more markets or payout programs, confirm coverage and control requirements through contact.

Conclusion#

Strong reconciliation works when match keys, rule governance, exception ownership, and evidence discipline operate together. When those controls are explicit, differences across PSP ledgers, internal ledgers, and bank statements become manageable operations work instead of period-end surprises.

Before adding more automation, lock in three working documents:

- A comparison table that defines what each record is authoritative for.

- An auto-match decision table that defines what can clear without review.

- An exception taxonomy that assigns ownership and handoff rules.

Treat same-day differences as a judgment call, not an automatic error. Payment operations can run continuously, and cycle boundaries may not match calendar days. FedNow runs 24x7x365 and uses a cycle day generally 7 p.m. to 7 p.m. ET the next day, so the real checkpoint is traceability: can you follow a coherent reference path and retain evidence plus matching outputs for replay?

Use evidence that holds up under audit, not just dashboard totals. Stripe’s Payout reconciliation report is designed to reconcile each payout with the transactions it settles, with drill-down to underlying transactions. Adyen’s Settlement details report supports transaction-level settlement reconciliation. Pair those with the bank statement line, internal journal trace, raw webhook or API payloads, rule version, and approver log where a break requires investigation.

Keep controls in documented policy, not tribal memory. Control activities should be implemented through policies and procedures, responsibilities should be documented by unit, and policies should be reviewed periodically. If a break type has no clear owner or required evidence, the process is not ready for more automation.

Finally, close control gaps before scaling automation: make ownership and resolution paths explicit, and enforce idempotency before adding ingest paths that can duplicate side effects. Adyen documents idempotency keys for safe retries, with keys valid for a minimum of 7 days after first submission.

Before rollout, validate control coverage and control requirements for the markets and programs you actually operate. Risk-based coverage should reflect differences across products, services, customers, and geographies rather than assuming one control design fits all.

Frequently Asked Questions

What is `3-way reconciliation` in a fintech platform context?

3-way reconciliation in this context means matching one payment movement across three records: the PSP settlement ledger, your internal ledger, and the bank statement. The goal is traceability, not just totals that look close. You should be able to follow the same payout or adjustment across all three records with supporting evidence.

What is the difference between a `PSP ledger`, an `internal ledger`, and a `bank statement`?

A PSP ledger reports what the processor says was settled and paid out, often at transaction level. Your internal ledger is your own books and records of transactions and asset dispositions. A bank statement is the cash-side record of booked entries, so it confirms bank-booked movement rather than every upstream processing state.

Why can all three records be accurate and still not match on the same day?

Timing differences are normal. Settlement can be batch-driven, payout frequency affects when movement appears, and webhook-driven updates are asynchronous. Treat these as timing mismatches first when references remain coherent, and escalate when references are missing, inconsistent, or duplicated.

Which break types should be auto-resolved and which should always go to an `exception queue`?

Auto-resolve deterministic cases, especially already-processed duplicate webhook events that can be safely ignored. Route ambiguous items to the exception queue, including missing references and payouts that do not reconcile to bank deposits. If auto-matching reduces queue volume but lowers classification confidence, tighten the rules.

What should a team automate first when transaction volume starts growing?

Automate ingest, deduplication, and evidence capture first. For request retries, use idempotency keys so repeat calls do not create duplicate side effects; Stripe supports keys up to 255 characters and notes keys may be pruned after at least 24 hours. For webhook retries, mark processed events, ignore repeats, and return success so they stop recurring as false breaks.

Which KPIs best indicate reconciliation health and close readiness?

Use payout-to-bank reconciliation status and checks that close data is complete enough to close books accurately. These show whether reconciliation is controlled day to day, not deferred to period-end cleanup. A close-readiness test is simple: can you reconcile payouts to bank deposits and produce the data needed to close books accurately?

What controls are required for an audit-ready reconciliation process at scale?

You need internal accounting controls designed to provide reasonable assurance, and books and records that accurately and fairly reflect transactions and asset dispositions. Your evidence should connect source records, transformed matching values, bank-booked entries, and final reconciliation status. Keep evidence relevant and reliable, not just voluminous.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bankcustomer.gov/help-topics/bank-accounts/statements-records...trusted

- bsaaml.ffiec.gov/manual/AssessingTheBSAAMLComplianceProgram/04trusted

- cisa.gov/sites/default/files/2024-10/ICT%20SCRM%20Tas...trusted

- csrc.nist.gov/glossary/term/audit_trailtrusted

- department.va.gov/financial-policy-documents/financial-documen...trusted

- ecfr.gov/current/title-17/chapter-I/part-38/subpart-K...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fdic.gov/risk-management-manual-examination-policies/...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: